We Studied 1,000 Corporate Venture Capital Deals and Found That "Strategic Capital" Is a Myth

So what exactly is true industrial investment?

By Yunxiao Guo

Edited by Zhiyan Chen

The End of Expansion Logic

After prolonged wrangling among multiple parties in the energy sector, Snowway Mining has finally found its new owner — CATL. Despite being nicknamed the "Battery King," CATL still had to put up a "sky-high" price of 6.4 billion yuan to take control of this lithium mine at the center of the storm. Compared to the overall valuation of 3.68 billion yuan at the end of 2022, CATL's restructuring offer represented a 73.9% premium.

This deal was executed by CATL's strategic investment department, led by Qu Tao, who also serves as assistant to CATL chairman Robin Zeng. On the eve of securing Snowway Mining, CATL rolled out its "lithium ore rebate" program, kicking off the price war in power batteries.

For a lithium-ion battery R&D and manufacturing company, the strategic importance of controlling lithium ore sources goes without saying. From another angle, for Snowway Mining — which before 2022 was an overlooked, debt-ridden operation — and for the entire lithium mining industry, being 100% acquired by a downstream industry super-leader may well mark the beginning of their rebirth.

This most closely watched M&A case in the energy industry chain since 2022 is merely the most visible part of the sweeping wave of industrial investment currently underway in China.

According to Jingdata, from early 2022 to the present, 16,757 deals occurred in the domestic primary market, with roughly 70% concentrated in hard-tech sectors like new energy, new materials, semiconductors, robotics, commercial aerospace, and biomedicine. Of these, nearly half involved CVCs or direct government investment funds. In Xiaomi's most recent disclosure, equity investments accounted for nearly 20% of total assets — a remarkable phenomenon. CATL, charging ahead at full speed, saw its absolute equity investment value surge from 965 million yuan to 17.595 billion yuan over the past five years.

Industrial investment is rapidly emerging from scattered corners of the market, even showing signs of surpassing financial investment.

A former head of strategic investment at a listed company told Anyong Waves: "Industrial elements like raw materials, orders, technology, land, and policy are often mentioned in framework agreements outside the investment agreement, effectively becoming part of the transaction itself."

As the entire market's investment focus shifts toward hard tech, the importance of "money" in investment deals is declining. "Industrial investment," which places greater emphasis on the resource attributes of investors, is appearing with increasing frequency in today's investment discourse. If developing tech manufacturing is the most certain bet for the next decade, then industrial investment will clearly become the dominant form.

Industrial investment is hardly new in China. In fact, it started almost simultaneously with venture capital. For a long time, "expansion" was the most important keyword in industrial investment.

In 1998, IT manufacturer Start Group invested 12 million yuan in startup localization software company Mingtai Technology, widely considered China's first industrial investment of meaningful scale. The two parties announced they would collaborate on developing, marketing, and servicing Chinese localization and translation software — but this was far removed from Start Group's hardware core business. In subsequent years, Start Group made aggressive investments in the VCD industry, suffered consecutive losses, and hovered on the edge of delisting. Recall that in China's PC market before the millennium, they had been a presence rivaling Lenovo.

This was undoubtedly emblematic of most early industrial investments: launching into entirely new businesses with no exit returns in sight; more fatally, investors blindly expanded horizontally, and the strategic value they envisioned rarely materialized.

By the internet era of "everything can become an ecosystem," expansionary industrial investment transformed from "corporate poison" into the critical lever for tech giants to build their empires. Tencent's gaming, entertainment, and social empire; Alibaba's super e-commerce ecosystem; Meituan's local services map — all were built through investment. And their CVCs (corporate venture capital arms) shaped most people's basic impression of industrial capital: sweeping across territories, conquering markets.

Multiple investors have expressed the same view to Anyong Waves: for internet platform companies, "hardly any investment is not industrial investment."

This aggressive posture in industrial investment stems from the essential nature of internet business models as a "winner takes all" game. When core businesses approached their ceilings, cross-sector, cross-domain industrial investment became more of a tool to support valuations, stock prices, and employees' dreams.

Today, the face of industrial investment has changed.

Through interviews with various industrial investors and founders of portfolio companies, Anyong Waves found that based on three dimensions — "investor," "investee," and "transaction characteristics" — one can broadly define industrial investment as practitioners in today's primary market see it: participation by corporate investment arms, government industrial funds, sector-specific vertical funds, and similar institutions, investing in equity of companies within tech and manufacturing-related industrial chains, with transactions typically accompanied by transfers of industrial resources beyond capital.

In the internet era, industrial investment was primarily made by major tech CVCs, emphasizing "business synergy" between investee and investor, with the investing enterprise as the core. Today, the importance of investees is rising, and the influx of different types of industrial capital is making more people recognize the value of investment transactions for entire industrial chains.

Making Investment Belong to Industry

Despite Huaye Tiancheng, founded by Sun Yelin in 2015, being thoroughly a market-oriented fund with generating returns for LPs as its primary goal, this doesn't prevent him from being called an "industrial investor" by all manner of people every day.

Several factors support this label: Sun's 18 years of experience at leading tech enterprises, Huaye Tiancheng's vertical focus on information technology, and its keen sense of investment value points in industrial chains through a four-layer track rotation of semiconductors, intelligent computing infrastructure, smart terminals, and intelligent applications. One example: in 2021, when the market still couldn't determine whether the 4D millimeter-wave radar track would prove viable, Huaye made an early bet on incubating company Muyewe. After Tesla formally equipped the Model S/X with its new Autopilot hardware HW4.0 and 4D millimeter-wave radar, the sector began accelerating.

In February this year, battery binder developer Haodian Technology announced a Series A of over 150 million yuan, led by Fengyun Capital (which evolved from SVOLT's strategic investment department), with nine institutions including Oriental Fortune Capital, Zhejiang Energy Group, and Amperex Technology Limited participating — while the angel round investor a year prior was EVE Energy. Haodian Technology targets the market gap for domestic high-end binders. Even though this auxiliary material with extremely low usage accounts for only about 2% of lithium battery cost structure, it has attracted numerous industrial capital players.

Manufacturing a single chip involves roughly a hundred sub-sectors, integrating tens of billions of transistors and other electronic components through 2,000–5,000 process steps, with precision controlled to one ten-thousandth of a human hair.

Compared to the internet industry, the vast majority of tech and manufacturing-related industrial chains are orders of magnitude more complex. The result: while internet products pursue traffic economies and rapid iteration, tech manufacturing sees one move affect the whole system.

"Long and precise" is the natural attribute of industrial chains. From semiconductors to consumer electronics, from power batteries to new energy vehicles, from reducers to robotics — without exception. This practically concentrates all of human wisdom: at the most upstream, raw materials unevenly distributed in nature, or artificial materials with extreme performance; midstream, thousands of extraordinarily precise processes and production lines relying on economies of scale to drive down costs; after multiple transfers, end products reach consumers' daily lives.

These characteristics of industrial chains also shape the form of industrial investment.

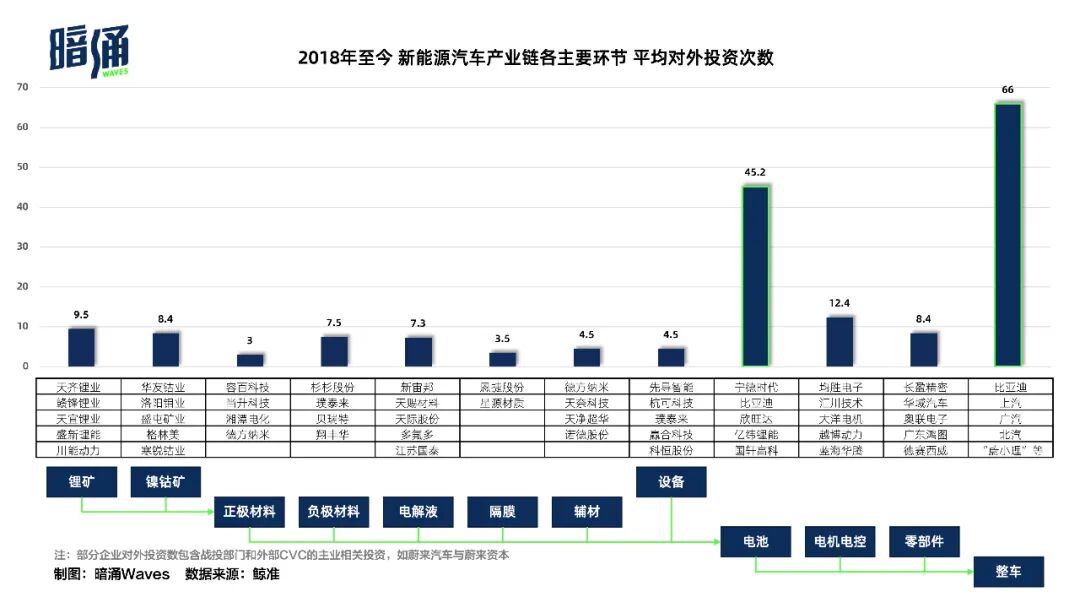

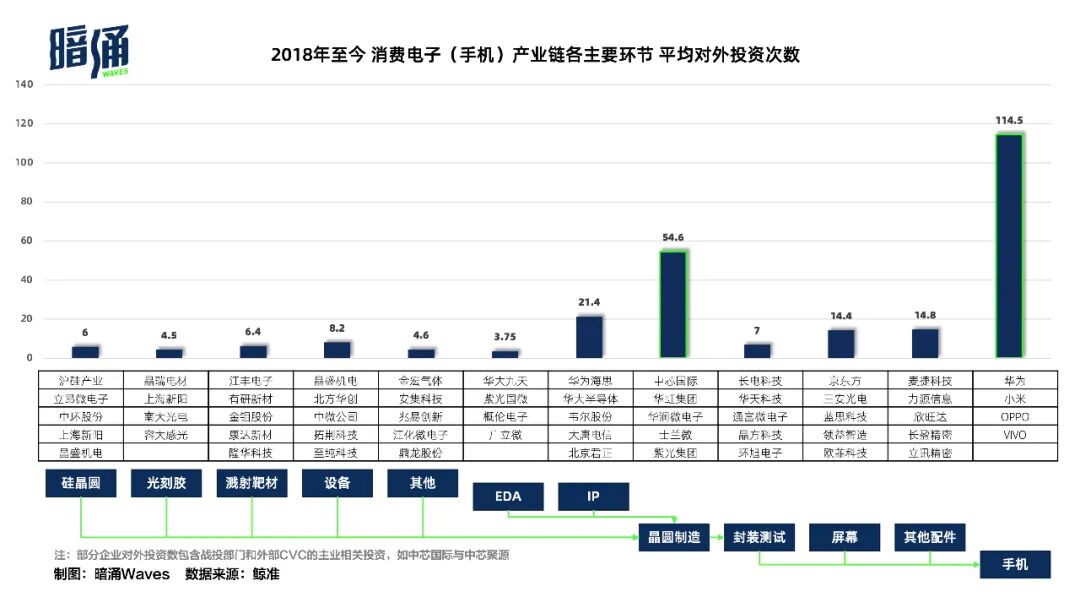

Using lithium batteries and chip semiconductors as midstream cores, we respectively tallied the outward investment activities of leading enterprises in the most representative new energy vehicle industrial chain and mobile consumer electronics industrial chain. This can to some degree sketch the basic appearance of industrial investment.

Outward investment by major segments in industrial chains (1)

Outward investment by major segments in industrial chains (2)

Looking across various segments in the industrial chain, midstream critical nodes and downstream terminal manufacturers possess capital scale, voice, strategic imperatives, and other factors, making them the true protagonists of industrial investment.

From the data, outward investment by segments in the new energy vehicle and consumer electronics (mobile phone) industrial chains shows remarkable consistency. Upstream enterprises belong to various niche sectors, difficult to scale, lacking both capability and motivation to expand further downstream. Over five years, their equity investments have mostly been horizontal M&A consolidation, with limited participation in globally notable large transactions (for instance, Ganfeng Lithium participated in GAC Aion's 18.294 billion yuan Series A).

Midstream reaches power battery manufacturers and chip semiconductor fabs (foundries), the crucial integration link connecting upstream and downstream, whose stage products also occupy substantial portions of terminal product cost structures. Their outward investment appears considerably more active — since 2018, leading enterprises have on average made outward investments of roughly 50 deals in various forms. Downstream, where products face consumers directly, the massive investment scale of automakers and phone makers has long been no secret. This broadly characterizes the investment landscape of tech manufacturing giants.

Among numerous strategic imperatives, supply chain security is the core of cores.

Compared to Apple's three-decade self-developed chip journey, Huawei's HiSilicon — "spare tire转正" (promoted from backup to primary) four years ago — has only just begun, facing circumstances a hundredfold more difficult.

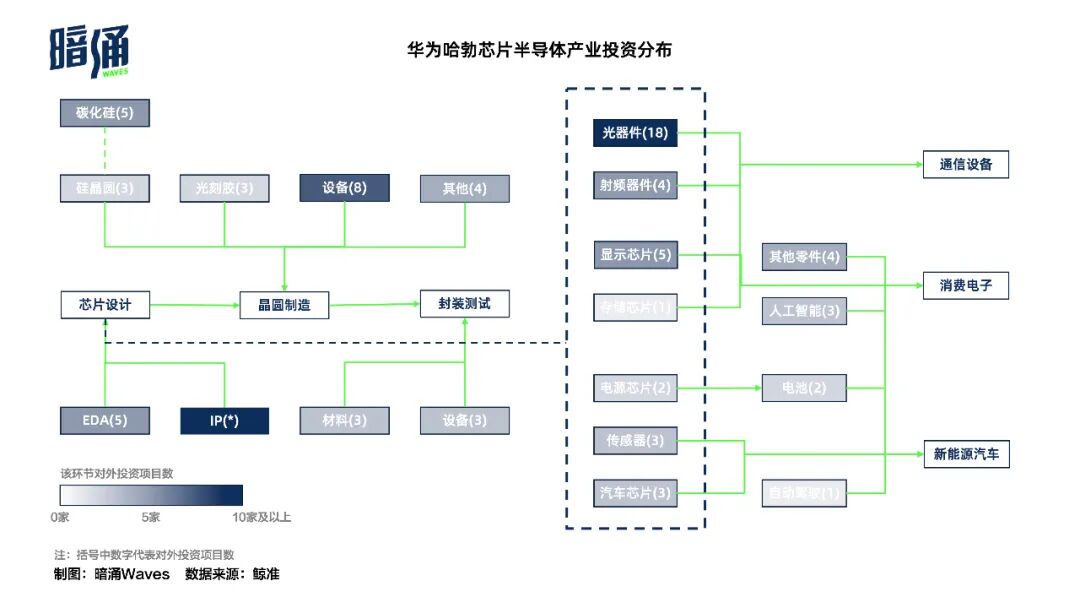

According to public information, in April 2019, Hubble Investment, wholly owned by Huawei, was established under Bai Yi, then president of Huawei's Global Financial Risk Control Center, with executives also including HiSilicon Semiconductor chairman Zhou Yongjie and former Huawei wireless network R&D president Ying Weimin. In Huawei's recently disclosed 2022 annual report, "interests in joint ventures and associates" reached 7.1 billion yuan, while Hubble Investment's AUM is reportedly 7.5 billion yuan and growing.

To date, this industrial capital appointed in crisis has invested in nearly 100 enterprises. Apart from a small number of enterprise service investments, all others concentrate in chip semiconductors and terminal product supporting industries, covering virtually every segment of the industrial chain.

Hubble Investment's chip semiconductor industrial investment distribution

Across all segments, Hubble has invested in numerous chip semiconductor R&D manufacturers, with optical devices and RF devices directly related to Huawei's communications business as key focus areas. Subsequently, Hubble successively invested in EDA software vendors including NineCube, Feipu Electronics, and Arcas Microelectronics; upstream semiconductor equipment vendors including Keyi Hongyuan and Jingtuo Semiconductor; and photoresist manufacturers including Fuyang Xin Yihua and Bokang Information — all considered "chokepoint" segments.

The "chokepoint" issue that began emerging in 2018 was the starting point of the industrial investment boom. Today, domestic substitution across industries has even developed into a distinct subcategory of industrial investment. For industrial investors, investing in domestic substitution is hardly difficult; it essentially competes on project sourcing capability — as long as it exists, it can be found with help from business units or financial advisors.

"The real test lies in judgment of trends, timing, and people," Sun Yelin told Anyong Waves. Industrial investment often attempts to answer which of old and new technologies will win when — conclusions difficult to reach through customer base, financial data, or other metrics. "The worst thing is investing $1 billion when Nokia is at its peak, only for Apple to emerge the next year."

Currently, the power battery field alone contains lithium-ion, sodium-ion, solid-state, and hydrogen fuel cells, and even finer divisions like ternary, lithium iron phosphate, lithium manganese iron phosphate cathode materials, with energy storage, photovoltaics, and other fields each having their own technology route competitions. Yet dramatically, if controlled nuclear fusion achieves commercialization someday, all the aforementioned "new energy" empires will collapse.

"Technology" determines the unique advantages of new technologies; "manufacturing" determines cost reduction after mass production. It is before these two intersect that industrial capital should optimally enter.

Who Is the Better Industrial Capital?

The closer to industry, the more accurate the judgment of future technology directions likely is. For this reason, nearly all interviewees mentioned to us that corporate CVCs possess powerful "technology validation" capabilities — "the R&D department knows very well who's good and who's bad." Does this mean CVCs can make better investments for industrial chain prospects? The answer isn't so easily reached.

One unavoidable reality is that CVCs must account for current mainstream technology development for their parent companies, often simultaneously betting on multiple technology routes in a single track. In new energy vehicles, for instance, CATL is advancing both charging and battery swap routes in parallel. Beyond its core business, CATL is also laying out its battery swap business, having invested in Gecko Technology, a developer of skateboard chassis. This technology envisions integrating the frame, battery, motor, and other key components on a sliding chassis, greatly enhancing the convenience of battery swapping.

On the other hand, for startups, securing investment from industry heavyweights means orders and entry into supplier systems. This is the core reason industrial capital is especially favored by tech entrepreneurs in today's era of surging hard-tech investment.

But this was never so straightforward. After actually engaging with several CVCs, an automotive entrepreneur told Anyong Waves that obtaining orders through being invested in is not as easy as imagined — "it only improves my success rate for getting some business."

The reasons still relate to the characteristics of tech and manufacturing industrial chains. For these long and precise chains, any error in any segment can cause unimaginable damage to a batch of products or even an entire brand, then transmit downstream with almost no possibility of rapid correction. So for startups with financial institutions, risk exists almost only at the monetary level. But if brought into the supply chain through CVC investment, it means product-level instability with no corresponding high returns. This is unacceptable for large enterprises.

Conversely, behind every industrial investment made by a CVC lies a precise calculation synthesizing parent company financial returns, business strategy, technology scouting, and other factors.

In CATL's just-released 2022 financial report, long-term equity investments totaled 17.595 billion yuan, with investment income contributing 2.515 billion yuan in profit, accounting for 6.86% of current profit. This conclusion clearly omits more important parts.

A veteran logistics practitioner calculated for us: for the Snowway Mining acquisition mentioned at the beginning, "the price difference between international ocean shipping and domestic short-haul road transport roughly exceeds 500 yuan per ton. After Snowway Mining reaches production, annual lithium ore raw material transport costs alone will save CATL nearly 100 million yuan" — and this doesn't account for the value of the lithium ore itself, or the immeasurably valuable supply chain stability.

CVC investments must calculate cost reduction and efficiency gains across raw materials, transport, key technologies, production processes, and more. State-owned industrial capital has similar comprehensive considerations. Local government investments must consider tax revenue, employment, GDP growth, and other regional economic issues, while national-level industrial funds need to build competitiveness for entire industrial chains.

These matters not so directly related to startups themselves are precisely crucial to understanding much industrial investment behavior: as components, industrial investments must create wealth and value for far larger machines.

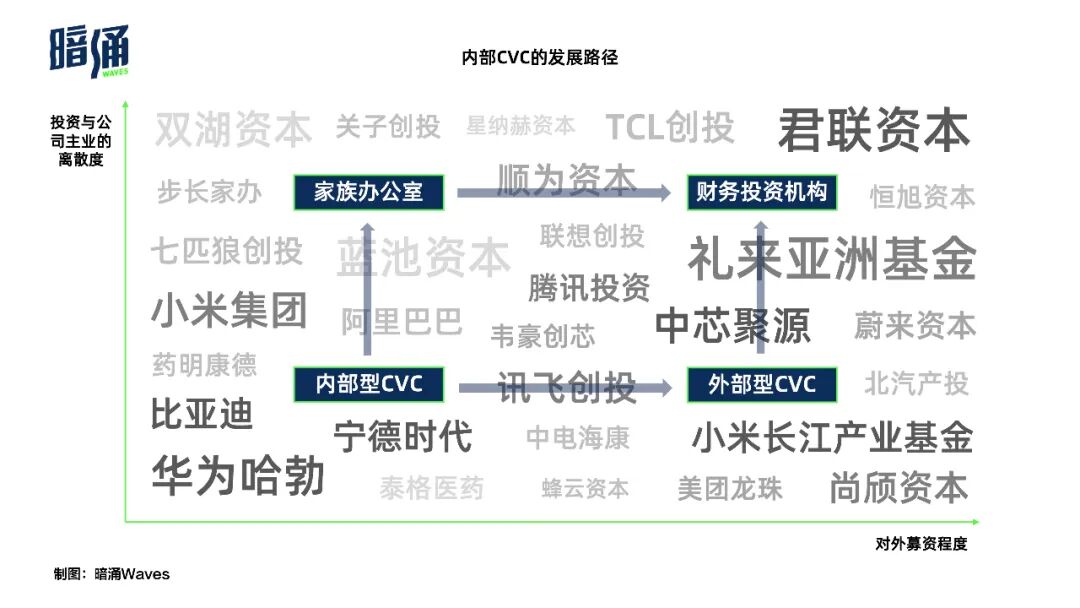

Of course, some large companies have recognized that internal CVCs, as vehicles of corporate will, often cannot maximize investment value while imposing numerous restrictions on investees. Thus, beyond CVCs with intense business synergy emphasis, multiple paths have emerged for investing in industrial companies: establishing family office direct investment departments, co-investing in industrial funds with state capital as LPs, or even establishing pure financial investment institutions. Today, all these are considered forms of industrial capital.

Take Xiaomi: within the group exist both industrial investment and strategic investment departments; the Hubei Province co-founded Changjiang Xiaomi Industrial Fund, whose external LPs include CITIC Bank Investment, BAIC Group, GF Qianhe, Gree Financial Investment, and others, has become a considerable force in China's semiconductor sector; and Shunwei Capital, bearing Lei Jun's strong personal imprint, after 12 years of institutional development, has long ranked among China's top-tier funds.

Internal CVC development paths

Beyond this, between comprehensive financial investment institutions and more restrictive CVCs and state-owned industrial funds, market-oriented funds with strong industrial attributes are increasingly emerging and being discovered by the market. The aforementioned Huaye Tiancheng is representative among these.

Xia Zuoquan is one of BYD's three co-founders, and his Zhengxuan Investment, also a market-oriented institution, concentrates most of its portfolio in the new energy vehicle industrial chain, with internal investors mostly having BYD backgrounds.

In 2021, they led the Series A in domestic CAD software supplier Xindi Digital. Half a year later, BYD's strategic investment arm quickly followed with a strategic round. In the subsequent Series B, BYD veteran Yang Longzhong's Huiyou Investment also participated in this 700 million yuan club deal, alongside other participants including SDIC Venture Capital, Bohai Industrial Investment Fund, Shenzhen High-Tech Investment, and other government-background funds, plus more financial investment institutions.

What BYD likely considered was more about CAD software assurance in vehicle design; other participants' expectations were enterprise growth returns, local economic stimulus, and filling a niche gap in domestic software ecosystems.

As industry is elevated to current strategic heights, the protagonists of industrial investment are gradually shifting from large corporate CVCs toward more diversified investment institution types. Strategic value, financial returns, regional economy — these varied demands converge, but in China's current context, their ultimate underlying color should be only one: overall industrial chain advancement. This goal means industrial investment is no longer merely a tool for large enterprises to reinforce themselves; capital, orders, technology, land, and other resources should be efficiently transferred and utilized by investees capable of evolving the industry. These should become the most dynamic components in the ecosystem.

As long as this can be achieved, industrial investment can in fact be completed by any institution.

(Anyong Waves intern Yitao Yang also contributed to this article.)

Image source | Visual China

Layout | Yunxiao Guo