We Analyzed 1,000 LP Commitments and Found 30 Hidden Top Family Offices

They are also a microcosm of China's commercial evolution.

By Yunxiao Guo

Edited by Jing Liu

In March 2022, Waves published its inaugural article, The Hidden Gardens of China's Wealthy, turning its attention to a new trend in the investment world — the rise of family offices. Drawing on nearly 300,000 words of interview material, this lengthy piece sparked some genuinely valuable discussions within the family office industry. Through these conversations, we discovered even more of the industry's colorful complexity.

What kind of family offices are most sought after in China's primary market? We set out to analyze this question in a more quantitative way.

First, a clarification: in China's primary market, "family office" is an overly broad concept. It encompasses personal investments by entrepreneurs and their families, capital deployed through various investment vehicles under family control, and corporate investments by family businesses — distinctions that are difficult to draw clearly. Beyond this, a large number of multi-family offices exist; these represent a greater share by count, but fall outside the scope of this particular survey.

We define our survey targets as follows: all investment entities actually controlled by the principal operators of private enterprises and their families — that is, single-family offices in the broad sense. We focus on the domestic market, meaning the RMB fund fundraising landscape.

The survey comprises two main components: data analysis and questionnaire research.

We identified LPs at more than 20 top-tier domestic GPs, as well as major LPs in over ten star projects in the primary market in recent years. Drawing on publicly available information about listed companies and the entrepreneurs behind them, we compiled and screened the above categories of traceable investors, removing state-owned capital, insurance capital, marketized fund-of-funds, non-family-controlled industrial capital, and entities without clear industrial backing.

We also widely distributed questionnaires and conducted interviews with primary market participants about "family office investment," targeting fund leaders, fundraising partners, and frontline IR professionals to capture firsthand assessments from those actually operating in the market. Over 70% of respondents indicated they would consider family offices "on par with other types of LPs," while nearly 20% said they "prioritize family offices very highly."

Synthesizing this data and information, we compiled over a thousand investment records, analyzing total capital deployed over the past fifteen years and the past three years respectively, as well as average ticket size, investment frequency, number of GPs covered, and consecutive investment counts. We supplemented this with auxiliary indicators such as pro-rata share in single funds, reinvestment rates, and portfolio penetration to identify 30 "family offices most closely watched by China's primary market."

This is our inaugural special survey of "Family Offices on China's Primary Market Radar." We welcome feedback on any omissions.

The Family Office Map: Hidden Corners of the Business World

Hubei Century Elite Culture Development Co., founded in 2004, specializes in educational supplementary materials. Beyond the well-known Elite Tutorial series, their materials cover every subject from primary school through higher vocational education.

Yet this company, which seems to have little connection to the primary market, actually contributed RMB 29.7 million to Hongshan's RMB Fund II back in 2010 — a fund whose star projects included Botanee and ZTO Express. It also backed CDH Investments' RMB Fund VI in 2016, whose portfolio contained CanSino Biologics and iSoftStone, among others. Additionally, they have been long-term LPs in Daoyuan Capital and Noah Holdings' Gopher Asset Management.

Tibet Fumao Investment Management Co. has three shareholders — Zhang Zeqing, Zhang Jinyun, and Liu Yu — whose affiliated companies all point to Furong Garment in Danyang, Zhenjiang, Jiangsu province. About them, only a single 2020 article titled "Furong Garment: Transforming Through Adherence, Innovating Through Focus" can be found online. The article reveals that Furong Garment began building factories in Southeast Asia in 2012, and has since maintained a compound growth rate above 15%. This is a low-profile export garment factory.

Yet since contributing RMB 50 million to CDH Investments in 2008, their cumulative primary market investments have approached RMB 1 billion. Beyond CDH, they have backed Hongshan, Hillhouse Capital, CPE, and other blue-chip GPs, as well as niche healthcare funds like Hengrui Capital and Qingsong Capital. Interestingly, among search results for Zhang Jinyun, there appears a May 2022 major asset restructuring report for Hualian Supermarket. This was actually the backdoor listing of Innovation Metal — a core aluminum supplier to Apple valued at RMB 11.5 billion — in which CPE, Shangqi Capital, Yunhui Capital, and CDH Investments all participated. Tibet Fumao also hides within the 47-page list of穿透出资人.

Among vast commercial empires, Century Elite and Furong Garment hardly rank as top-tier investors, but they both illustrate a point: entrepreneurs who consistently engage with the domestic primary market can emerge from any corner we might overlook. This was the most illuminating finding of our survey.

Here are some other unexpectedly familiar names:

China Dongxiang, holder of the Kappa brand — founder Chen Yihong and his wife, actress Miao Pu, have cumulatively deployed over RMB 2 billion across a stellar GP portfolio including Hongshan, Boyu Capital, Yunfeng Capital, and CPE;

Spider King Group, a leather goods company born in Wenzhou, Zhejiang, invests only in blue-chip funds and is now an LP in Hongshan, Hillhouse Capital, Source Code Capital, Matrix Partners China, and Meituan Longzhu;

Supor Group has dominated China's cookware industry for years — founder Su Xianze has backed Hillhouse Capital, Loyal Valley Capital, and Decheng Capital, while Yuanqiao Asset, founded more recently, participated in CardiMED's Series D;

Houcaller Group began localizing Western steakhouse dining in 1993. Beyond being a long-term LP in Loyal Valley Capital and Fukun Venture Capital, they have made direct investments in offline restaurant chains Bamian and Chenxianggui.

At that time, China's economic development had another major thread: real estate.

Beyond large property conglomerates, regional real estate enterprises emerged across the country, along with an even greater number of real estate ancillary businesses. In this survey, we included four private real estate companies — Qingdao Century Sunshine, Wuhan Nanguo Real Estate, Xu Hang's Pirui Group (his second venture after Mindray Medical), and Yinshengtai Capital, which has now fully transitioned to investment — as well as adjacent-sector companies like home furnishing leader Sofia Group and lighting leader Opple Lighting, all active in the domestic primary market LP layer. Notably, Wu Yajun's dollar-denominated family office Twin Lakes Capital, founded after Longfor Properties, has long been regarded as a pioneer in professionalizing China's family office industry.

Yinshengtai Capital may help us better understand real estate entrepreneurs' transition. In 2017, CIFI Holdings formed a strategic partnership with Yinshengtai, after which the latter's founder established Yinshengtai Capital and embarked on his family office investment journey. After investing in Hongshan, Hillhouse Capital, and Northern Light Venture Capital, Yinshengtai Capital also began making direct investments and acquiring secondary shares in star projects. Open its website and the homepage displays IPO celebration announcements for CALB, Heartcare Medical, Giant Biogene, and Full Truck Alliance — presenting itself very much as a direct investment institution.

These family enterprises active in the domestic primary market, while not necessarily top representatives of every industrial category, span traditional consumer goods like footwear, apparel, textiles, and food & beverage; traditional energy and manufacturing; healthcare; logistics and transportation; and real estate and adjacent industries — indeed encompassing most of the narrative of China's economic development over the past three decades (especially 1990–2010).

Top-Tier Family Offices Become Major LPs for Select Funds

Capital deployment capacity has always been the first lens through which outsiders observe family offices.

This is the most practical way to understand them. In our survey questionnaire, 82.3% of responses identified "capital deployment capacity" as the "primary consideration when fundraising from family offices." The prevailing impression is that "family offices don't write large checks, and considering their other demands, fundraising from them has low ROI" — a sentiment that repeatedly surfaced in our interviews.

Data indicates this is changing.

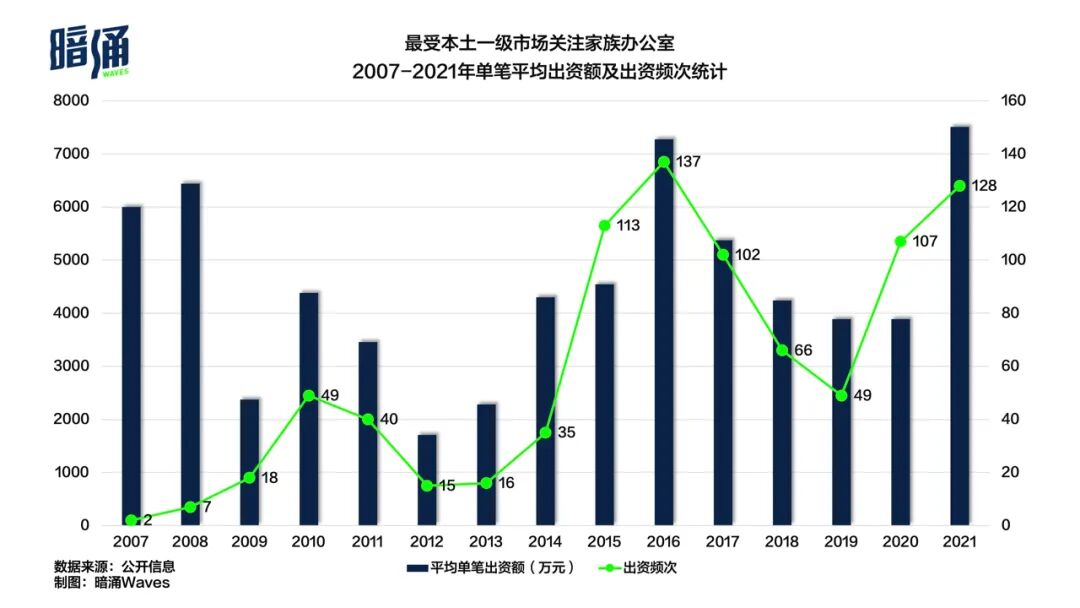

According to Tianyancha corporate registration data, excluding 2007 and 2008 when sample sizes were too small and data skewed significantly, the average ticket size and investment frequency of top domestic family offices over the past fifteen years show a markedly consistent trend, reaching successive peaks in 2010, 2016, and 2021.

We explored the evolution of RMB funds in Twenty Years of RMB Funds: Between Life and Death: share structure reform, the launch of the ChiNext board, NEEQ expansion, and the STAR Market opening all drove market expansion and contraction. Clearly, market sentiment and expected returns have continuously influenced family offices' willingness to invest.

Yet positive signals can also be read from this. For instance, the volatility itself demonstrates the high degree of marketization among family offices — something precious among RMB LPs. Equally important, overall deployment scale and frequency have steadily grown: the 30 family offices in our survey currently average roughly RMB 50 million per ticket and approximately 90 total investments annually (with conservative estimates placing blind pool commitments at over half).

This means these top-tier family offices each year become major marketized LPs for two RMB funds.

An exemplary case is Septwolves Group's family office, a name with exceptional industry reputation. According to incomplete statistics from corporate registration data, over more than a decade, various Septwolves entities have invested 70-plus times across 36 GPs, with total deployment of approximately RMB 3 billion. Among its deepest relationships is Loyal Valley Capital: the Septwolves family office made several investments beginning in 2015, with single tickets reaching RMB 150 million. This amount would represent under 5% of a large RMB PE fund's main vehicle, but could very likely make it the largest shareholder in a sub-fund.

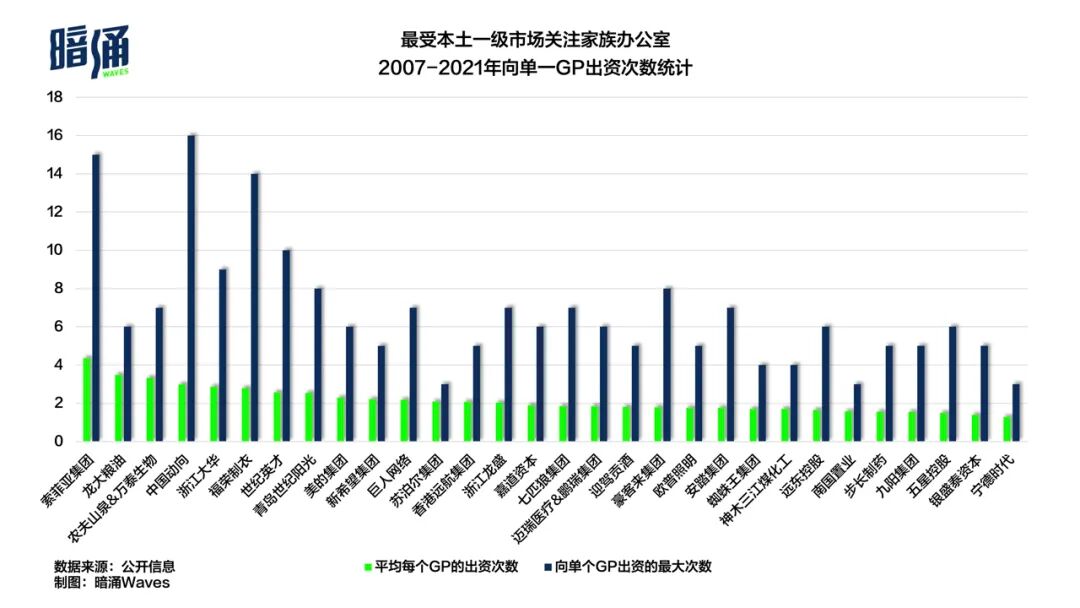

Beyond ticket size, we can also observe investment continuity — a dimension often overlooked when describing deployment capacity.

During 2007–2021, the 30 selected family offices averaged approximately 2.16 investments per GP, with maximum consecutive investments averaging about 6.67. This essentially means that for their best-relationship institutions, they participate in every new fund raise to varying degrees. This aligns with information from our interviews: "family offices have very high reinvestment rates among legacy LPs." This confirms that in the world of family offices, trust matters most.

Every family office has tightly partnered GPs — Hongshan for Buchang Pharmaceutical, Sharing Capital for Mindray Medical, F&G Capital for Zhejiang Dahua, Eagle Capital for Qingdao Century Sunshine, and countless others. The capital deployment capacity of top domestic family offices deserves serious attention from all GPs.

Investment Strategies Are Complex, But the Ultimate Goal Is Singular

If one mark of "smart money" is sophistication, then investment strategy should be the clearest indicator.

Yet domestic family office investment has consistently carried a "relationship-driven" impression.

Entrepreneurs like to "huddle." This huddling occurs among non-blood-related executives within groups, as well as among regional or industry peers.

As mentioned, Septwolves Group's origins trace to Jinjiang, Fujian, where enduring Min commercial culture forged a tight-knit community across a generation of Jinjiang merchants. This no-longer-mysterious group includes this survey's Anta Group and Houcaller Group, as well as paper giant Hengan Group, snack empire Dali Group, zipper leader SBS Group, and countless footwear, apparel, and textile brands. Data shows they are also active participants in the domestic primary market.

Their stories circulate everywhere in the market.

One vertical-sector fund fundraiser told Waves, "One (Jinjiang family office) we contacted didn't look at our direction, and referred us to another family office"; an even more intriguing version holds that "among Jinjiang family offices, Septwolves carries relatively more sway."

We attempted to find data corroboration: Septwolves Group's family office and Anta Group's family office have co-invested in Huakong Fund, Meituan Longzhu, and Cornerstone Capital — in each case, Anta and other Jinjiang family offices invested in the GP's next fund 2–3 years after Septwolves' initial commitment.

If this is not coincidence, then the "pathfinder" role may explain Septwolves family office's broad coverage of dozens of GPs.

A domestic family office rivaling Septwolves in renown is that of Buchang Pharmaceutical's Zhao Tao. A key reason for both names' primary market fame is their vast coverage — rumor holds that the Buchang family office "has practically DD'd every GP in the market." Incomplete statistics show the Buchang family office has invested in at least 50 GPs in RMB, with 2015–2016 post-"Mass Entrepreneurship and Innovation" marking its peak, when it backed 26 GPs — averaging more than one per month.

In a sense, this reflects a mindset of being prepared to "pay tuition": evolving into a more professional institution in pursuit of higher returns.

Which GPs count as Buchang's investment preferences?

In 2017, then-Buchang family office CIO Situ You told 36Kr that he personally favored GPs "with foresight about the future, capable of creating trends."

Documented Buchang GP investments include: CDH Investments RMB Fund I in 2008, Hongshan RMB Fund II and Tiantu Capital's founding in 2010, Source Code Capital and Ming Shi Capital in 2015, and Chuxin Capital and Feidian Capital in 2016. Across these waves, new RMB GPs with dollar-fund backgrounds and approaches seemed to receive particular favor from Buchang.

If high-risk-high-reward represents a more mature strategy, then case funds and secondary transactions edge closer to certainty.

Consider Sofia Group's two entrepreneurs and their collaboration with IDG Capital. For early projects like HeyTea Series A, Blue Bear Fresh Milk Series A, and WonderLab Series A+, both invested personally in IDG's single-project funds.

A more typical case is Narwal's Series C. Announced in June 2020 with Hongshan as lead investor, Hongshan's commitment was partially executed through "Sequoia Nuochen (Xiamen) Equity Investment Partnership (Limited Partnership)" — an entity with no other portfolio companies, making it a case fund. Drilling down through its LPs reveals participation by Xu Hang of Mindray Medical, Zhao Tao of Buchang Pharmaceutical, and Xu Chengjian of Spider King Group.

Similar to case funds, when LPs seek shares in star companies, they may do so through secondary transactions. We discussed in The Underwater Mysteries of the Primary Market how GPs package portfolio company equity for sale, using this as "bait" to secure commitments for new funds.

One respondent told us: "Some family offices took the materials, went back to study intensively, and never mentioned investment again." But the more frequently repeated story in our survey was: access to star project shares is a precondition for blind pool fund commitments — an open secret between GPs and LPs.

In fact, family offices and GPs are constantly engaged in such games. What they truly seek from case funds, secondary transactions, and even blind pool funds is often more certain opportunities, less eroded returns, and that most elusive of "investment strategies" — direct investment.

On the strength of Nongfu Spring and Wantai Biological's massive wealth, Zhong Shanshan has long held China's top fortune. Compared to other billionaires' enthusiasm for investing, Zhong has shown virtually zero interest in the primary market — though this has shifted somewhat in the past three years.

In 2020, Zhong personally committed RMB 500 million to Lingcheng Venture Capital, becoming the cornerstone LP for a new fund of this small healthcare fund founded in 2019. Lingcheng's fund followed on with over RMB 300 million in Joyever Pharma's Series B; months later, Zhong injected nearly RMB 3 billion through multiple entities into Guanzi Venture Capital, his direct investment family office, to lead the company's Series B+.

Similarly, numerous family offices have established their own direct investment brands. Jiadao Capital founded by Hikvision major shareholder Gong Hongjia, Qicheng Capital founded by Septwolves scion Zhou Shiyuan with friends, Huayan Capital established by Zhejiang Dahua executives, and Heling Capital under Far East Holding Group's Jiang Xipei all carry strong family hues.

Using GPs as "outposts" for direct investment may be the most efficient tool for deal sourcing.

The roster follows:

We welcome your feedback via email (36krmediair@36kr.com) or WeChat comments.

Image sources | Visual China

Layout | Yunxiao Guo