After Reading a 1,000-Page Prospectus, Here Are the Secrets Behind Mixue Bingcheng's Stock Price

Nobody gets a better Mixue ice cream or tea just because they're richer.

**

By Yiming Liu

Edited by Jing Liu

By now, you've probably heard more than enough about Mixue Ice Cream & Tea. At first glance, it's the legend of a small-town underdog conquering the world. The keywords are roughly: social mobility, supply chain miracle, extreme cost-performance, deep operational grind, and a 28-year marathon.

As of today — the day after Mixue's Hong Kong IPO — the company still commands a market cap of nearly HK$111 billion, breaking the curse of tea-stock debuts. By that measure, one Mixue equals four Guming Holdings, seven Chabaidao, or thirty-seven Nayuki Holdings.

Most people's first impression of Mixue is low prices. But low prices aren't a moat. Low prices achieved through low costs — that's the moat.

We've tried to unpack in more detail how this beverage empire was forged. Based on Mixue's two prospectuses totaling over 1,000 pages (2022 A-share filing, 2025 HKEX filing), you get this progression: at first glance it looks like a franchised fresh-brewed tea brand — then somewhat accidentally it expands into an IP company — and further out, a much larger picture of globalization and massive supply chain infrastructure.

At its core, Mixue's business model is about using modern industrial-system tactics to achieve extreme low cost, crushing the fragmented, guerrilla competition of fresh-brewed tea.

98% of Revenue Comes from Selling Raw Materials

Many people think Mixue is a consumer brand company. In reality, it's more of a supply chain company.

Around 2018-2019, China saw a wave of new tea brands emerge. They mainly sold brand premium. This coincided with the tail end of the mobile internet boom, and the rise of new consumer brands conveniently absorbed a large pool of investors with B2C experience. "Every consumer product deserves to be reinvented" was the prevailing thesis. These companies quickly became VC darlings — Hey Tea, Nayuki, and so on.

Another category of tea companies worked differently. Their true nature was hidden behind the "brand": build an efficient industrialized system, make money by selling creamer, jam, plastic cups, and straws to franchisees. The more vertically integrated the supply chain, the better. Rely on scale and advanced management to push costs to the extreme. The more franchisees, the more reliable the profit. If all else fails, spin up a side business and become an OEM factory for other brands. Mixue and Chabaidao belong to this camp.

As everyone knows, fresh-brewed beverages is a cutthroat arena. In tea alone there's Guming, Nayuki, Hey Tea, Chabaidao, Ba Wang Cha Ji; coffee has even more players, with Luckin in the same low-price tier, among countless others. Mixue's own prospectus shows China's beverage market has 26,000 pre-packaged drink companies and 660,000 fresh-brewed beverage shops.

In the tea industry, if we're talking about making money, those who sell the finished product have consistently lost to those who sell the ingredients. For example: Mixue sells cups at RMB 5-8, Nayuki at RMB 20-30. Yet Mixue has an 18.7% net profit margin, with RMB 3.5 billion in net profit for the first nine months of 2024. Nayuki? Negative 17% margin, losing RMB 470 million in the first half alone. Chabaidao, also in the "sell ingredients + franchise" camp, has seen growth momentum weaken, but still posted RMB 256 million in net profit with a 14.5% margin in its 2024 interim report.

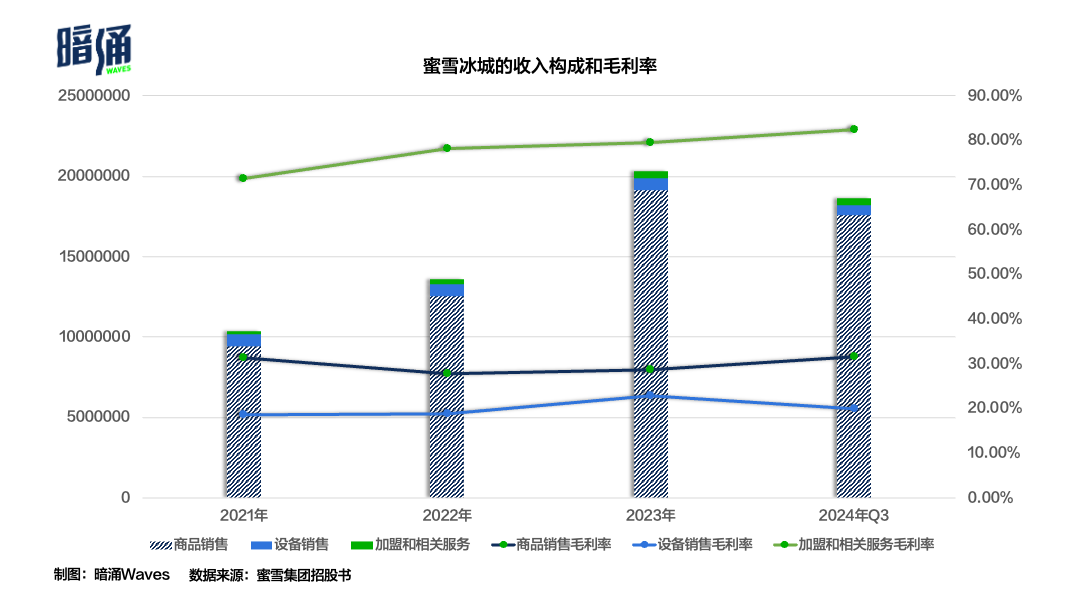

According to Mixue's prospectus, 97.6% of its revenue comes from selling food ingredients (sugar, milk, tea, coffee, fruit, grains, etc.), packaging materials (plastic cups, straws, etc.), and equipment (refrigerators, ice cream machines, ice makers, etc.) to its own franchisees.

Mixue also doesn't make money from franchise fees. It doesn't take a cut of franchisee profits, and its franchise fees aren't high — they account for just over 2% of total revenue.

This is very different from Western franchise chains like McDonald's or Starbucks. Some argue that taking a percentage of franchisee profits represents a deeper binding. (On store density: since Mixue doesn't share profits, it naturally wants as many stores as possible. But in prime locations, too many stores cannibalize each other, diluting per-store output. Mixue has anti-cannibalization rules, setting a protection radius of 200 meters in high-traffic areas — not especially generous.)

This also touches on another key question in tea: company-operated stores, or franchise?

The "company-operated camp" is represented by Hey Tea and SexyTea. The "franchise camp" is Mixue, Guming, Chabaidao, and Auntea Jenny.

So far, the franchise camp has won decisively. If the IPOs of Guming and Chabaidao weren't enough to prove franchise is the better model, Mixue's hundred-billion market cap pretty much settles the argument.

Since it's essentially a supply chain company, Mixue must maintain a delicate balance with its franchisees. They're a community of shared interests, but also locked in a zero-sum tension over profit distribution.

Mixue's franchise agreements typically run 3-4 years. Franchise fees usually range from RMB 7,000-11,000, with annual management fees of RMB 4,800 and training fees of RMB 2,000, plus a RMB 20,000 deposit. Overall, these costs are not substantial.

Historically, Mixue has occasionally sacrificed some profit to franchisees. In 2022, when COVID hammered many stores, Mixue cut prices on 69 core SKUs by an average of 15% in April — effectively thinning its own margins. Mixue essentially provides franchisees with the cheapest procurement channel possible, removing any incentive to secretly switch to other suppliers.

The franchise model has two critical design points: First, franchisees must actually make money. Only then will they sell more drinks, and buy more raw materials from Mixue, creating scale effects. Second, Mixue itself must invest in building an efficient supply chain — ideally handling everything from production to processing to delivery in-house, cutting out every middleman that takes a cut, to achieve extreme low cost.

While Chabaidao, Guming, and others follow the same business model, Mixue has clearly gone much deeper on supply chain intensity.

The main products Mixue sells are actually these powders, concentrates, and jams | Source: Mixue Group prospectus

Buying Nearly 1% of China's Edible Sugar in a Single Year

Building a stable, sustainable supply chain obviously doesn't happen overnight. To understand Mixue's supply chain Great Wall, let's start with its biggest hit product: fresh lemon water.

In 2006, Mixue's RMB 1 ice cream cone went viral, kicking off rapid store expansion. But by 2013, Mixue realized it needed a summer drink. Founder Hongchao Zhang turned his attention to lemon water.

To sell fresh lemon water at RMB 5 — most people thought this was nearly impossible. After all, bottled lemon iced tea at the supermarket costs RMB 3.50. And in the first nine months of 2024, Mixue sold 1.1 billion cups in China alone — about 4.07 million cups per day. How to source lemons from growing regions, how to flash-freeze them, how to cold-chain deliver to every store, how to process them in-store with standardized operations (without food safety incidents), how to match production to sales... And most importantly, at a price of just RMB 5.

Here's how Mixue pulled it off.

First, upstream lemon selection: after tasting lemon varieties worldwide, Mixue's team settled on the Eureka lemon — a variety grown in Anyue, Sichuan — for its suitable sugar content, acidity, juice yield, and weight. Mixue established a local subsidiary, Snow King Lemon (now Snow King Agriculture), to work directly with local farmers, eliminating middleman markups.

In Tongnan District, Chongqing — bordering Anyue — Mixue built a factory locally, ensuring lemons go from harvest to factory in under 48 hours. Once inside, they're washed, sanitized, and sorted. Grade A fruit is packed and cold-chain delivered to Mixue stores globally for fresh lemon water. Grade B/C fruit is juiced on the spot, then made into concentrate or lemon slices for beverage blending. The peel, pulp, and seeds all find uses — what they call "one fruit, six separations," achieving 100% resource utilization and avoiding waste.

In upstream procurement, Mixue has essentially turned itself into a large-scale agricultural deep-processing enterprise. Another example: its factory in Ding'an, Hainan leverages local coconut and coffee resources. A project in Chongzuo, Guangxi mainly produces fruit products, since the area abounds in fruit, taro, and sugarcane — raw materials for taro balls and syrup needed in milk tea.

Another example: non-dairy creamer (a food additive) commonly used in milk tea. Previously Mixue relied mainly on supplier procurement, but creamer production isn't technically difficult, so Mixue also shifted to large-scale self-production. This inevitably brings to mind another "cost killer," BYD — both rely on deep vertical integration across their industrial chains. Once a product has profit margin, they'll start making it themselves, enabling extreme low prices at the consumer end.

Mixue established its first central factory as early as 2012 — among the earliest in China's fresh-brewed beverage industry to build its own. From another angle, the reason Mixue can push drink prices so low while still letting franchisees make money is that it must employ industrialized methods to mass-produce cheap, operationally convenient semi-finished ingredients for stores — various powders, syrups, jams.

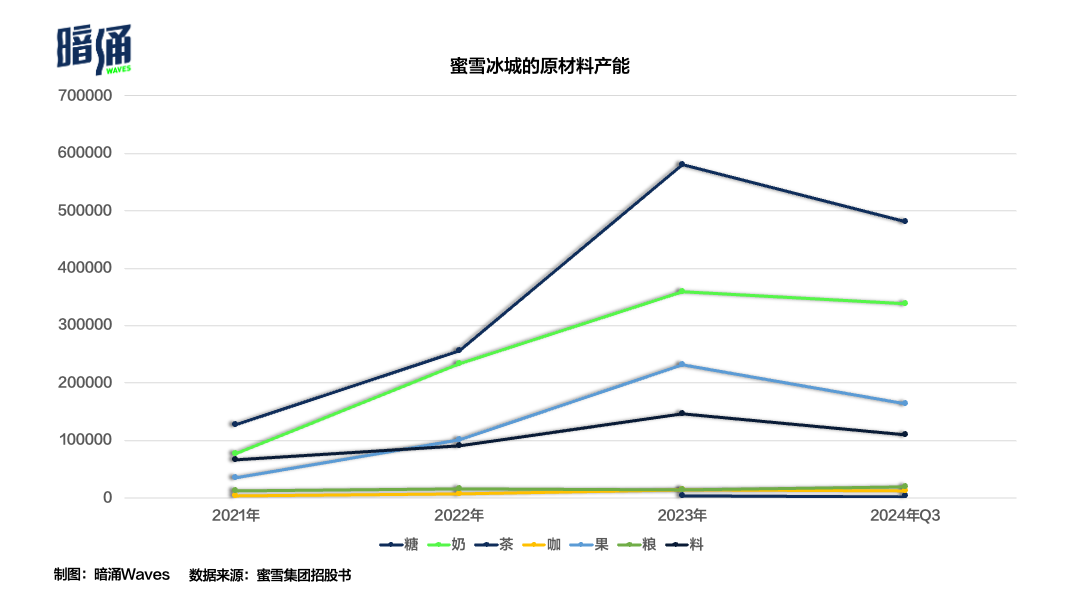

This also means Mixue's products are very high in sugar. In 2021, it bought roughly 1% of all edible sugar consumed in China.

Today, Mixue is the company with the most comprehensive product range and largest production scale in China's fresh-brewed beverage supply chain. Over more than a decade, it has built five production bases in Henan, Hainan, Guangxi, Chongqing, and Anhui, with combined annual capacity of 1.65 million tons.

Beyond food ingredients, Mixue also produces core packaging materials and equipment. Packaging means straws, cups, etc. — for example, reducing packaging bottle costs for honey and fruit nectar by 50%. Equipment includes refrigerators, ice cream machines, ice makers, and coffee machines. The prospectus notes that over 60% of beverage ingredients Mixue provides to franchisees are self-produced, the highest in China's fresh-brewed beverage industry, with 100% self-production for core beverage ingredients.

Finally, another critical link is logistics. Mixue was also the first in the fresh-brewed beverage industry to build its own logistics network (starting 2014). Today it operates the industry's largest warehousing system, comprising 27 warehouses totaling approximately 350,000 square meters. Additionally, to support overseas business, Mixue has established localized warehousing in four Southeast Asian countries — seven warehouses covering about 69,000 square meters.

On delivery, Mixue covers 90% of county-level administrative divisions in mainland China, with 12-hour delivery. Most importantly, franchisees have always used Mixue's logistics for free — also the first in the industry to do so.

By now, you should understand why investors are flocking to Mixue. Over the past two to three decades, many chain restaurant companies have collapsed, and behind them all were supply chain problems.

Haidilao became a dining king because of its powerful supply chain construction — not merely a hot pot restaurant brand, but a platform-level company backed by a professional industrialized system that could sell various products to the entire industry.

Mixue is the same. It recognized the importance of supply chain early on, and step by step built an end-to-end supply chain system.

The "Snow King" IP: Beyond the Playbook

Mixue has consistently emphasized the concept of "fully self-built." Combined with the above, this isn't hard to understand. But surprisingly, on the brand side, Mixue can also self-build. This is rare among consumer companies. Most brands either tie themselves to traffic stars or build the founder's personal IP. Mixue pursues a pure self-built IP strategy.

Starting in 2018, Mixue launched the "Snow King" IP — a chubby, endearing cartoon figure holding an ice cream scepter — paired with an advertising jingle adapted from the tune of Oh! Susanna. The song has accumulated 9.7 billion plays across major social platforms.

It's a commercial product, yet the catchy lyrics and melody never mention business. Instead, it's a childishly naive "you love me, I love you" — absurdly catchy and brainwashing. Played across tens of thousands of stores, it instantly spread through streets and alleys, then gained further life through online remixes and memes.

In August 2023, Mixue struck while the iron was hot, launching a 12-episode animated series The Snow King Arrives, streaming free across platforms with over 200 million views, scoring 9.9 on Bilibili. The plot was classic — love and courage, friendship and adventure — never mentioning milk tea once, just a pure cartoon. It has now surpassed 220 million plays.

By December 2024, Mixue released a second season, The Snow King: Fantasy Desert, unexpectedly a Dunhuang aesthetic Western, still without a single mention of milk tea.

Both are finely produced animation products, costing roughly over RMB 100,000 per minute, with production expenses exceeding RMB 10 million per season. For this, Mixue even established a company called "Snow King Loves Animation," with business scope not in advertising but in entertainment services, performances, film production — cultural dissemination-related businesses. The "Snow King" IP originated from beverages, but Mixue clearly hopes it can transcend beverages to become a cultural symbol.

"Snow King" IP | Source: Mixue Group prospectus

"Snow King" IP | Source: Mixue Group prospectus

Financially, the result has been massive marketing cost savings. In the first nine months of 2024, Mixue's brand promotion expenses accounted for just 0.9% of revenue.

And this purely white, chubby figure knows no national boundaries — people worldwide might like it. In Mixue's Indonesia expansion, the topic "Mixue Ice Cream & Tea Indonesia" has accumulated 2.6 billion exposures on TikTok. Netizens often say "the Snow King never collapses."

Mixue's Snow King strategy closely resembles Hasbro's launch of the Transformers IP. In the early 1980s, the toy market was white-hot, with every company straining to release novel products to capture consumer attention. At that time, Japanese toy company Takara designed toys with unique mechanical structures that could transform between vehicles, animals, and robot forms. Hasbro敏锐ly recognized the enormous potential in these transforming toys, immediately reached a cooperation agreement with Takara, introduced them to the American market, and gave them a resounding name — "Transformers."

Hasbro's most important move was producing a同名 cartoon TV series, telling the thrilling battles between the Autobot and Decepticon Transformer factions. This animated series quickly swept the globe, with children instantly captivated by the Transformers' heroic combat, cool transformation scenes, and the gripping drama of good versus evil. As the cartoon exploded in popularity, Transformers toys became supply-constrained.

In the 21st century, Hasbro moved the Transformers IP to the big screen. In 2007, the first live-action Transformers film debuted. With spectacular visual effects, thrilling action sequences, and clever adaptation of the original story, it achieved massive global success. Subsequently, a series of Transformers films followed. These films not only elevated Transformers' global recognition to new heights but also brought Hasbro substantial returns.

Mixue's two animated series haven't pursued short-term monetization. Instead, they aim for longer-term vitality. And the registered animation company's business scope — film performances, cultural dissemination — suggests they intend to do something in this space.

10%, Already Southeast Asia's Top Brand

Mixue's next growth engine is undoubtedly overseas.

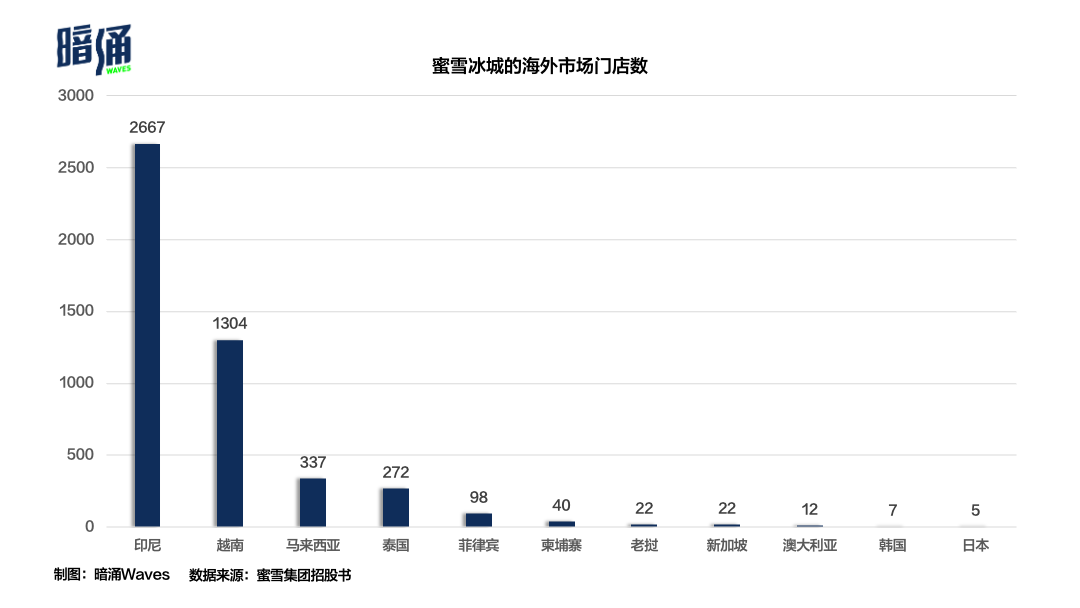

Currently, 90% of Mixue's stores are domestic, with another 10% (4,792) overseas. Indonesia (2,667) and Vietnam (1,304) have the most. But that 10% has already made Mixue the largest fresh-brewed tea brand in Southeast Asia.

As the Chinese market matures, Southeast Asia has become the world's fastest-growing region for fresh-brewed tea. The global compound annual growth rate from 2023 to 2028 is roughly 7%, while Southeast Asia's is 20% — triple the global rate. In 2023, Southeast Asian per capita annual consumption of fresh-brewed beverages was 16 cups, lagging other markets (US: 323 cups, EU and UK: 306, Japan: 172, China's tier-1 cities: 70, but tier-3 and below: 13, averaging 22).

Before opening its first Vietnam store in 2018, Mixue had secretly prepared its overseas project for over a year, mainly through its Chengdu Southwest branch office. It identified key operators, built overseas trainer teams, and intensively studied machine maintenance, recipe formulation, and flavor adjustment.

In 2018, Mixue entered Vietnam first, opening its debut store in Hanoi. Because Vietnam is a long, narrow country, Mixue started from the north, penetrating the single market of Hanoi first, then gradually spreading to surrounding cities. In 2019, Mixue came to Indonesia through Oppo and Vivo — at the time, these were China's most successful brands going overseas, with very rich offline phone distribution channels, and these people were natural franchisee candidates. Mixue piloted in Indonesia's peripheral cities, like Semarang in Central Java and Bandung in West Java. The test results showed West Java had many university students — it exploded immediately, opening over 100 stores, then extending toward the capital Jakarta.

At this point, Indonesia's tea market resembled China 10 years ago, with standardized brands just emerging. Indonesia is a tropical country with hot weather, giving ice cream natural hit product potential — even becoming a promotional tool. And Mixue's ice cream was a flagship product, once accounting for 40-50% of single-store output.

In the push into Jakarta, it happened to coincide with the 2020-21 Indonesia pandemic, when large numbers of street shops emptied out and went unwanted at cheap prices. Mixue franchisees took the opportunity to bottom-fish a batch of storefronts. Mixue's average prices in Indonesia remained very cheap: 8,000-15,000 rupiah (RMB 3.5-6.6), highly competitive, while also being an international brand image. Mixue also completed halal certification in Indonesia — all products are Halal, so Muslims can drink with confidence.

In 2020-2021, large numbers of Mixue stores achieved "payback in six months," driving franchisees to frantically open stores and race for territory. This also created considerable supply chain challenges at the time — "Mixue's problem is always out of stock." But supply chain issues will soon be resolved. Mixue's Hainan production base is scheduled for completion in 2025, and it plans to build a multi-functional supply chain center in Southeast Asia, enabling local processing of tropical fruits.

From its first overseas foray in 2018, Mixue extended its domestic franchise model, backed by Chinese supply chain, and quickly surpassed Southeast Asian local brands. Its store count exceeded KFC, making it Southeast Asia's largest fresh-brewed tea company. In 2023, Southeast Asia's fresh-brewed tea shop chain rate was about 25%, significantly below China's 56% — leading brands still have vast room to grow.

A Product of Its Time

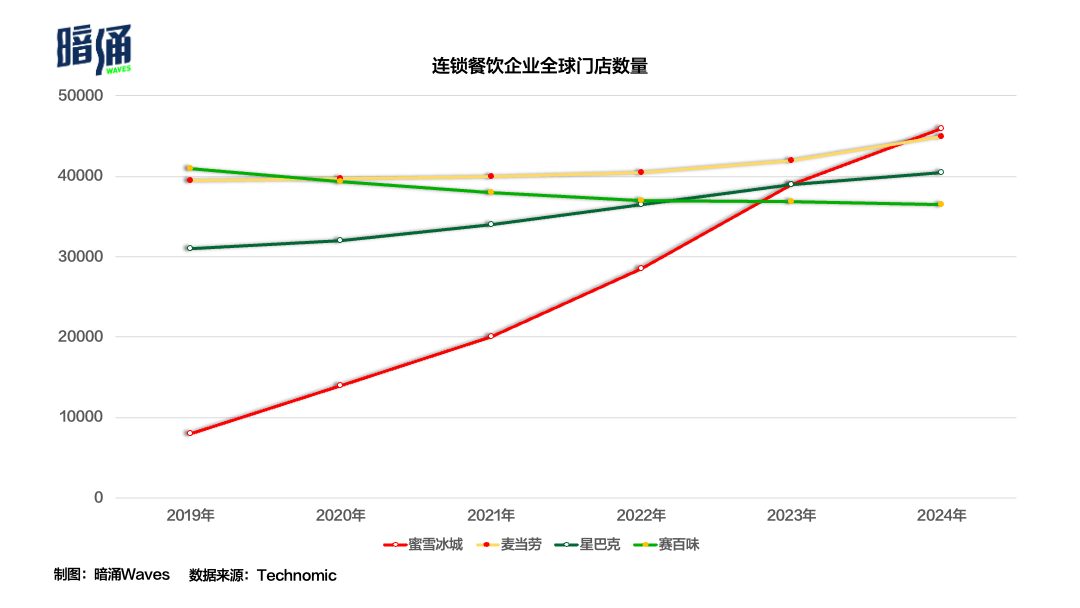

Today Mixue's store count exceeds 46,000, surpassing McDonald's and Starbucks. But by global revenue, there's still a long road ahead. Of course, Mixue's valuation isn't outrageous either — its 23x PE is similar to Luckin, and below Starbucks and McDonald's.

If we're talking risk, Mixue's biggest risk is that someday, if front-end stores become too crowded and franchisee profitability weakens, the heavily invested supply chain could instead become a burdensome weight. In the prospectus, we can see Mixue's capacity utilization is somewhat underutilized — sugar and grains, for instance, are below 50%.

Store payback periods are also lengthening. According to industry chain research, some franchisees say that in 2016-17, investing in a new Mixue store might take 12 months to pay back. During the 2020-21 boom, this shortened to 6 months. But now, as competition intensifies, from second-half 2023 to present, payback periods have stretched to around 18 months, and closure rates are gradually rising.

In the franchise industry, there's an old saying: "Quantity before quality" — grow fast first, then solve problems in the process of growing. This is a typical growth methodology. "But when density gets too high, these store operators stop benefiting," says a Mixue franchisee in Indonesia.

Through this IPO, Mixue has also laid out an ambitious expansion plan. 66% of raised funds will go to supply chain and overseas expansion, enhancing the breadth and depth of end-to-end supply chain, including replicating China's mature supply chain system overseas and further raising raw material self-sufficiency rates. 12% will go to brand and IP building and promotion — Snow King IP animation, films, and co-branded merchandise. Another 12% will strengthen digitalization and intelligent capabilities across business segments, improving franchisee inventory turnover. The remaining 10% will go to working capital and other uses.

The Mixue story remains a fairly legendary Chinese business tale. It demonstrates a small-town underdog life path: how a "Cold Wave Shaved Ice" shop in Zhengzhou, Henan became a massive efficiency machine, growing into a beverage giant with 45,000 global stores, attracting HK$1.84 trillion in subscription amounts and 5,324x oversubscription, becoming a capital market darling.

Of course, behind the massive subscription amounts, there's also the presence of brokers offering high leverage, and the Hong Kong Stock Exchange's FINI system reducing retail investor new-issue costs. But high leverage has always existed — it still depends on whether investors have the confidence to use it.

Mixue's secret weapon — hardly even a secret — is extreme low price. Behind this simple move lies decades of deep accumulation. To some extent, Mixue doesn't even resemble a food and beverage brand. It's more of a "production geek," obsessed with capacity expansion, determined to reverse-engineer a drink that requires fresh preparation into individual industrial processes, and becoming the largest manufacturer of every single link.

What it ultimately brings is product democracy. Just as no one drinks better Coca-Cola because they're richer or more powerful. In today's economic climate, this may be the best product of the era.

Image source | IC Photo