A History of Crypto's Rise and Fall: From Thin Air to $3 Trillion

Written as Bitcoin nears $90,000.

By JW

Edited by Jing Liu

The Web3 world parties every day. Late last night, people sighed over the slump of "Double 11" shopping festival while gasping at Bitcoin's surge. As of last night, Bitcoin broke through 89,000 USDT — a height never seen before in history.

This marks the seventh year of Web3's large-scale emergence in China.

People like to use "seven-year itch" to describe a turning point in a relationship. For the Web3 world, the past seven years have been its journey from niche to relatively mainstream in China, followed by widespread discussion and fierce debate.

Most people have gone from knowing nothing about Web3 to knowing a little, to even being immersed in it. Industry insiders have gradually moved from the margins toward the mainstream. This once-gray industry, like any other, has shown cyclical shifts beyond its initially captivating wealth effects, along with the intricate entanglements of human nature.

Today, there are over 500 million crypto users globally, and on-chain stablecoin assets have exceeded $173 billion. Yet many still don't understand what has happened, and what is happening, in the Web3 world.

Seven years ago, 24-year-old JW graduated from the Schwarzman Scholars program at Tsinghua University and, by a twist of fate, joined Web3. It was her first job. Most of her classmates had entered investment banking, consulting, government, or academia.

As she herself puts it, fate arranged for her to see a surreal world she never imagined: idealists obsessed with decentralization ideology, alongside scammers simply here to pan for gold; those who reaped outsized returns, and those who lost everything. And she herself went from someone who knew nothing about cryptocurrency to becoming a fund founder.

Where there are people, there is a Jianghu. Except in Web3, where money flows closer, the Jianghu is more brutal.

In this article, JW looks back on the past seven years of the crypto world in first person. "Reflecting on where we stand today, and why we continue marching in this space."

One Day in Crypto, One Year on Earth

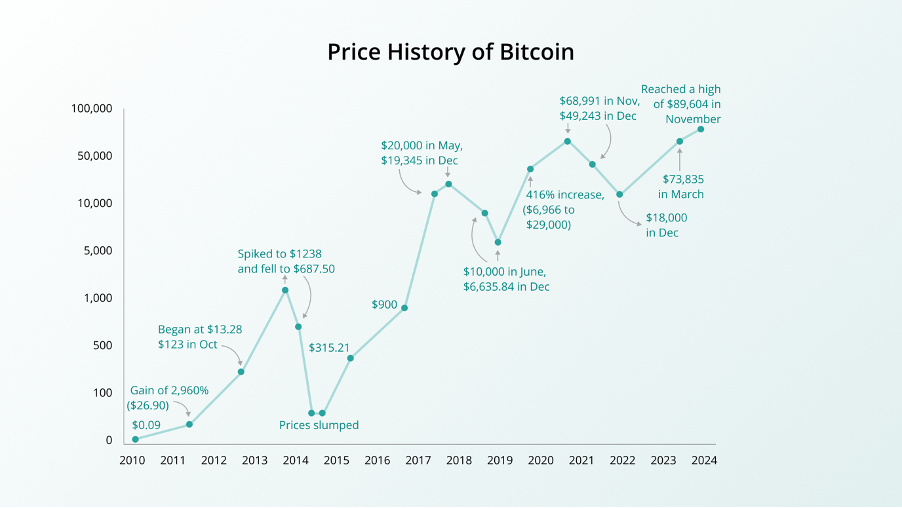

Price History of Bitcoin

Bitcoin's concept is generally considered to have been born on November 11, 2008, proposed by the now-missing Satoshi Nakamoto. In China, on June 9, 2011, Linke Yang and Xiaoyu Huang founded BTC China, the country's first Bitcoin exchange; OKCoin and Huobi were established successively in 2013.

But this was a game for the few — so few you could count them on two hands.

It wasn't until 2017 that Bitcoin became a "household name." That year, Bitcoin's price surged from under $1,000 at the start of the year to $19,000 by year-end. The 20x gain, along with the wealth-creation mythology of batch ICOs, instantly shook the entire internet and VC circles.

Whether you participated or not, everyone was talking about blockchain; the air was thick with whitepapers. Influencers like Xiaolai Li, Manzi Xue, and Weixing Chen vigorously preached decentralization ideology, hawking their invested projects to followers. In early January 2018, the WeChat screenshot from renowned investor Xiaoping Xu warning that "the blockchain revolution has arrived" remains memorable to this day.

At 3 a.m. on February 11, 2018, Hong Yu and a group of sleepless friends created a WeChat group called "3AM Blockchain." Within three days, the group "exploded"...

The combined net worth of this group's members probably exceeded a trillion RMB.

A popular saying in crypto circles went:

If you haven't heard of the 3AM Blockchain group, you're not yet in the chain circle;

If you haven't joined the 3AM Blockchain group, you're not yet a chain circle big shot;

If you haven't been flooded by 3AM Blockchain group posts, you haven't experienced what "one day in crypto, one year on earth" means.

But this was merely the prelude to the madness.

"This is the Godfather of Korean E-commerce"

In the summer of 2018, I traveled with my former boss (then one of the founders of Asia's most prominent fund) to Seoul for Korea Blockchain Week. Korea is one of the crypto industry's most important markets; the Korean won is the second-most traded fiat currency — second only to the US dollar. Crypto entrepreneurs and investors from around the world all wanted a piece of the action.

We were there to meet a company called Terra, a top-tier Korean project. The meeting was arranged at a Chinese restaurant in the Shilla Hotel, a traditional, almost conservative Korean hotel. As a government guesthouse, its lobby was packed with young people from around the world who were fanatical about crypto.

Terra was founded by two Koreans, Dan Shin and Do Kwon. Dan's company Tmon had been one of Korea's largest e-commerce platforms, with over $3.5 billion in annual GMV; Do was around my age and had tried several startups after graduating from Stanford.

"This is the godfather of Korean e-commerce," my boss told me on the way to lunch.

Similar to traditional investment thinking, betting on "the person" was also the golden rule of Web3 investing. Someone like Dan, who had succeeded in the Web2 world, instantly attracted co-investment from all top crypto exchanges and funds.

Later, we invested $2 million in Terra.

Perhaps because Do and I were peers, we stayed in touch. Do was much like my other classmates in computer science: standard American accent, wearing a t-shirt and shorts. Do told me they planned to make Terra's issued stablecoin a widely adopted digital currency, describing how they negotiated with Korea's largest convenience store chain, the Mongolian government, and Southeast Asian retail groups. They also developed a payment app called Chai. "It will become the Alipay of the world."

In an office that resembled a warehouse, as Do chatted with me over coffee about their grand plans, I felt somewhat dreamlike: at the time, I didn't actually understand how they would achieve these plans. I just felt it sounded so novel and ambitious.

Cryptocurrency was far from consensus then (and arguably still isn't today). Most of my classmates were either in investment banks, consulting firms, or big tech companies. They either knew nothing about cryptocurrency or were full of skepticism, while I was here chatting with someone planning to launch a "global payment network."

This was an era of chasing narratives, big funds, and professor coins.

"Help me track this link and tell me how much has been deposited; deadline is this week." My boss sent me a link to a Dutch auction project, a Layer 2 project running a public sale. In fact, we had never actually met this team. They had only provided a website and a whitepaper, yet raised over $26 million in 2018. Though that token has since dropped to zero.

People would rather trust a stranger on the internet, across continents, than someone in the same room.

I had just turned 24. Though I suspect most of the investment committee, much like me, often didn't really know what they were doing either. But they encouraged me to put another $500,000 into this project, "just think of it as making a friend."

They were trying to replicate the 2017 frenzy: with backing from famous funds, any ticker could pump 100x.

But the music stopped abruptly.

"When Will Bitcoin Get Back to $10,000?"

For a while, I thought this was the greatest job in the world: traveling the world at a young age; buying expensive business-class tickets and hotel stays; gliding through opulent conference halls; learning new things, making friends from all walks of life.

But the bear market came without warning.

In December 2018, Bitcoin crashed from its peak of over $14,000 to $3,400. As a young professional just starting out, I didn't have much savings, but when I watched Ethereum fall from $800 to $400, then to $200, I decided to bet one month's salary.

In hindsight, it wasn't a wise decision. Less than a month after I bought in at $200, ETH dropped below $100.

"What a scam." It was the first time I thought that.

In the first half of 2020, the world was devastated by the pandemic, and the crypto industry took a heavy blow during the March 12 market crash. I was stranded in Singapore at the time. I still remember that afternoon — every time I refreshed the price tracker, Bitcoin had dropped another $1,000. A month earlier, it had been hovering around $10,000; within hours, it plummeted from $6,000 to $3,000 — far lower than when I had first entered the industry.

To me, it felt more like a farce. I watched how people reacted: some waited on the sidelines; some bought the dip; some got liquidated.

Even more experienced investors were pessimistic. "Bitcoin will never get back to $10,000," they said. There were even discussions about whether the crypto industry would survive at all — some thought it might just be a detour in tech history.

But some chose to stay. My firm wasn't making new investments then, but I was still looking at deals.

Soon, decentralized finance (DeFi) started becoming a topic of conversation. I wasn't a trader myself, but all my trader colleagues thought DeFi was a bad idea: everything was slow, order-book-based exchanges were impossible, there was no liquidity, and even fewer users.

What I didn't fully grasp at the time was that security and permissionlessness were DeFi's biggest selling points — but could permissionlessness really move people? After all, KYC on centralized exchanges wasn't that bad.

The DevCon IV and DevCon V I attended during the bear market were also eye-opening experiences.

Even though I had studied computer science in college and was no stranger to hackathons, I had never seen so many "eccentric" developers in one place anywhere else. Even with ETH down 90%, people were still passionately discussing decentralization, privacy, and on-chain governance on Ethereum. I had no faith in decentralization, no passion for anarchism — these ideas had only ever appeared in my classroom lectures.

But the developers seemed to genuinely embrace these philosophies. "You joined at a bad time," a colleague comforted me. The year before, at DevCon III in Cancún, our fund had made tens of millions of dollars simply by investing in projects showcased at the event.

During the bear market, we also missed the opportunity to invest in Solana when it was valued below $100 million (today its market cap exceeds $84 billion). Even though we had interviewed founder Anatoly and Multicoin's Kyle. Kyle was deeply convicted, believing it would become Ethereum's "killer."

Solana's TPS was 1,000 times higher than Ethereum's, thanks to a consensus mechanism called "Proof-of-History." But after a technical due diligence call with Anatoly, my colleague concluded, "Solana is too centralized. Centralized TPS is meaningless — why not just use AWS?" Clearly, my colleague wasn't a fan. "And the founder doesn't understand the value of a truly decentralized network like Ethereum, probably because he used to work at Qualcomm."

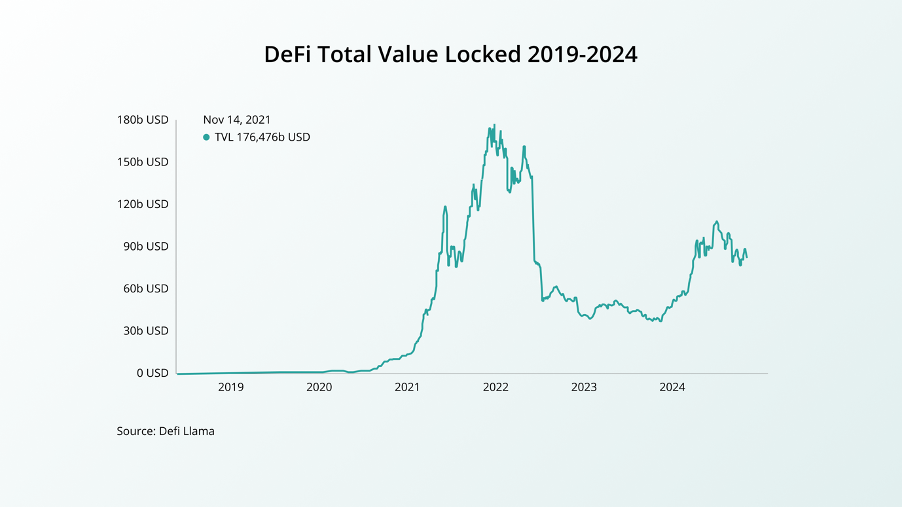

(DeFi TVL growth chart — the kind every VC goes crazy for) (Source: DeFi Llama)

With the introduction of yield farming, my skepticism about DeFi was quickly shattered. By depositing tokens into DeFi smart contracts, users could become liquidity providers for platforms and receive rewards in protocol fees and governance tokens. Whether you call it a growth flywheel or a death spiral, DeFi protocols achieved massive growth in user numbers and total value locked (TVL).

Specifically, DeFi protocol TVL soared from under $100 million at the start of 2020 to over $100 billion by mid-2021. Thanks to open-source technology, copying or modifying a DeFi protocol took just a few hours. Because the process of providing liquidity was called "yield farming," DeFi protocols were often named after food.

For a while, new "food coins" were born almost daily — from Sushi to Yam. Crypto people loved this wordplay; even a protocol handling millions in transactions could be named after food and use an emoji as its logo.

But the hacks and exploits in DeFi projects made me nervous. I'm not a risk-taker. My friends, however, were farming like crazy: they'd set alarms for 3 a.m. just to be among the first into new liquidity pools.

In the summer of 2020, annual percentage yield (APY) was the hottest topic — everyone was chasing pools with the highest APY. Noticing market demand for deploying capital to yield farms, industry veteran Andre Cronje launched a yield aggregator product: Yearn. It made a huge splash.

As more money flooded into DeFi, we also witnessed the rise of some "gods" on Twitter: SBF from FTX, Do Kwon from Terra, and Su and Kyle from 3AC.

Terra launched multiple DeFi products, including Alice, a payments app targeting the US market, and Anchor, a lending protocol. Anchor was probably designed for on-chain novices like me — just deposit your stablecoins into the contract and earn close to 20% APY, practically brainless.

At its peak, Anchor's TVL exceeded $17 billion. "Congrats on Anchor, it's a great product, I've put some money in too," I messaged Do on WeChat, unsure if he'd reply.

But I knew by then he was no longer the young person I had known — he had a million Twitter followers and had announced plans to buy $10 billion worth of Bitcoin.

"Thanks — you've done well on your portfolio too," he actually replied. He was referring to some gaming projects I had invested in earlier. DeFi had also transformed gaming in crypto — now everything was about "earn."

As the mania continued, I also invested in a lending project from Three Arrows Capital.

A few months later, questions about Anchor's profitability began emerging. It turned out that Terra's lending products weren't generating enough yield to cover the interest paid to liquidity providers like me; the current payouts were largely being subsidized by the Terra Foundation. Seeing this, I immediately pulled my money out; around the same time, I also redeemed my investment from Three Arrows Capital.

The vibe on crypto Twitter was getting weird. Especially when Do tweeted "Enjoy being poor" and Su was shopping at luxury malls in Singapore — it felt like a top signal. I was lucky to have dodged the Terra and Three Arrows Capital collapses; months after the crashes, I learned that the payments app wasn't actually processing payments on-chain, and the borrowed funds were being used to lever up so high that they could never be repaid once market direction changed.

But when FTX collapsed, I wasn't so lucky.

For weeks, there had been rumors that FTX had suffered massive losses from the Three Arrows Capital and Terra collapses and might already be insolvent. Billions were being withdrawn from the exchange daily. Out of caution, my company had withdrawn some — but not all — of our assets from FTX.

It was a turbulent period. Almost every day brought panic rumors about stablecoins USDT and USDC depegging, and Binance potentially going bankrupt. But we hadn't lost hope. I trusted SBF — what could a billionaire who believed in effective altruism and slept on the trading floor do that was bad?

Then one day, on my way to the gym, my partner called: FTX had filed for bankruptcy, $8 billion was missing. Because they had misused customer assets, we might not get our money back.

But I was strangely calm about it. Maybe that's just our industry: magic Internet money. All assets ultimately are just strings of characters and numbers on a screen.

Money is a test of character, and crypto just accelerates everything. Even fast-forwarding to today, I still don't doubt that Do and SBF started with good intentions. Perhaps they got drunk on the inflation brought by unrealistic growth; or they thought they could "fake it till they make it."

DeFi is like Prometheus's fire for the crypto industry: it brought hope, but at a devastating cost.

The Misunderstood Crypto World

As the old Chinese saying goes: "Sickness comes like an avalanche, but leaves like silk unwinding." It took the crypto industry years to recover from the crash.

From the outside, this looked like just another Ponzi scheme. People associated crypto founders with flashy designer clothes, an obsession with internet memes, parties thrown around the globe, and an anything-goes approach to getting rich quick. At an alumni gathering, I was catching up with old classmates. When I mentioned I'd invested in crypto, they joked, "So you're a crypto bro now." I wasn't offended, but it was a strange framing — as if crypto were somehow separate from tech and VC. Traditional internet and tech investing was seen as the respectable path, while a young person with decent credentials joining the crypto industry had, to some degree, gone astray.

For a long time, "Web3" and "Web2" were frequently used in oppositional contexts. But you don't see this kind of split in other industries. No one deliberately tries to distinguish AI founders from founders in SaaS or other sectors.

What exactly makes Web3 unique in a venture capital context?

My personal view is that crypto fundamentally changed how venture capital and early-stage investing work, which means the requirements for crypto startup success differ slightly from equity-based startups. Briefly put, token economics in crypto created unparalleled opportunities for startups and VCs. At the end of the day, it all comes down to product-market fit (PMF), user growth, and value creation — no different in essence from the Web2 world.

And as the crypto industry matures, the convergence between Web2 and Web3 companies is growing.

It's time to re-examine this industry.

In crypto's early days (and we're still early), what people wanted might have been a grand vision (like a digital currency independent of central banks), a new computing paradigm (general-purpose smart contract platforms), a story they hoped would come true (decentralized storage networks to replace AWS), or even a Ponzi scheme everyone wanted to get ahead of. Today, crypto users have a clearer sense of what they want, and they support these demands by paying for them or moving capital toward them.

For outsiders, it may be hard to intuitively grasp that "magic internet money" can actually generate revenue; some crypto assets even offer more attractive P/E ratios than stocks. Let me illustrate with data:

- $2.216 billion — Ethereum's protocol revenue over the past year

- $1.3 billion, $97.5 billion — stablecoin issuer Tether's Q2 2024 net operating profit, and total US Treasury holdings

- $78.99 million — meme launch platform Pump's revenue from March 2024 to August 1

Even within the crypto industry, opinions on memes are deeply divided: some see them as a new cultural trend and tradable consensus — Elon Musk wants to use Dogecoin in his Martian colony; others see them as a cancer on the industry, since memes themselves have no product and deliver no user value.

But I believe that purely in terms of participation numbers and capital scale, memes are already an unignorable social experiment — tens of millions of users worldwide and hundreds of billions of dollars in real money. Perhaps there's no tangible, graspable meaning. But by the same logic, what is postmodern art?

Many people's first impression of crypto markets may still be: storytelling, hype, and trading. This was partly true during the 2017 ICO bull run, but after several cycles, the industry's playbook has changed significantly.

Five years on, DeFi protocols' revenue-generating ability has proven PMF. From trading comparables, these projects' valuations increasingly resemble those in traditional stock markets.

Beyond differences in asset liquidity, connection to the real world is generally seen as the main divide between Web2 and Web3. After all, compared to AI, social, SaaS, and other internet products, Web3 products still seem somewhat distant from reality. But in some countries, like Southeast Asia, the largest super-app Grab (ride-hailing, food delivery, financial services) already supports crypto payments; in Indonesia, the world's fourth most populous country, users trading crypto assets outnumber those trading stocks; in Argentina and Turkey, where local currencies have severely depreciated, crypto has become a new choice for storing wealth — Argentina's crypto trading volume exceeded $85.4 billion in 2023 alone.

Though we haven't fully achieved an "ownership internet," we've already seen crypto bring vibrant innovation to the current internet.

For example, stablecoins represented by Tether (USDT) and Circle (USDC) are quietly reshaping global payment networks. According to a Coinbase research report, stablecoins have become the fastest-growing payment method. Stripe recently completed its acquisition of stablecoin infrastructure project Bridge for $1.1 billion — the largest acquisition in crypto history.

Blackbird, founded by a Resy co-founder, focuses on transforming the dining experience by letting customers pay for meals with crypto, particularly its own token $FLY. The platform aims to connect restaurants and consumers through a crypto-powered app, while also serving as a loyalty program.

Worldcoin, co-founded by Sam Altman, is an avant-garde movement pushing for universal basic income, relying on zero-knowledge proof technology. Users scan their irises through a device called the Orb, which generates a unique identifier called an "IrisHash" to ensure each participant is a distinct human, combating fake identities and bot accounts in digital spaces. Worldcoin already has over 10 million participants globally.

If we could go back to that summer of 2017, none of us would have imagined what the next seven years would mean for crypto — that so many applications would grow on blockchains, or that hundreds of billions in assets would be stored in smart contracts.

How AI Can Use Crypto as a Mirror

Now I'd like to discuss the similarities and differences between crypto and AI. After all, too many people draw analogies between the two.

Comparing crypto and AI may be like comparing apples and oranges. But viewing today's AI investment through a crypto investor's lens may reveal some parallels: both are full-stack technologies, each with its own infrastructure and application layers. But the confusion is similar too: it's still unclear which layer will accumulate the most value — infrastructure or application?

"If Toutiao does what you're doing" — this may be every entrepreneur's nightmare. The history of the internet has proven this fear well-founded, from Facebook cutting ties with Zynga to build its own mobile games, to Twitter Live and Meerkat, where big tech's resource advantages made it hard for startups to compete.

In crypto, because the economic models of the protocol and application layers differ, each project's focus isn't on building every layer of the ecosystem itself. Take public chains (ETH, Sol, etc.) — their economic model means the more people use the network, the higher the gas revenue and token value. So top crypto projects spend most of their energy on ecosystem building and attracting developers. Only breakout applications can increase underlying chain usage, thereby boosting project market cap. Early infrastructure projects even directly gave grants ranging from tens of thousands to millions of dollars to qualifying application developers.

Our observation: value capture between infrastructure and application layers is hard to call, but for capital, infrastructure and application layers alternate in popularity — yet both are winner-take-all. For example, massive capital flooded into public chains, top chain projects improved performance, enabling new application models and eliminating mid- and lower-tier chains; capital flooded into new business models, user scale grew, top applications captured capital and users, creating higher demands for underlying infrastructure and forcing infrastructure upgrades.

So what does this mean for investing? The simple truth is that investing in neither infrastructure nor application layers is wrong — the core is still finding that top player.

Let's rewind to 2024 and look at which public chains ultimately survived. Here are three rough conclusions:

Disruptive technology accounts for a smaller share of project success than you'd think. The "Ethereum killer" projects previously hyped by US and Chinese VCs, built on professor and academic concepts (Thunder Core, Oasis Labs, Algorand, etc.) — ultimately only Avalanche made it, and that was after the professors left and it became fully EVM-compatible. Conversely, Polygon, which investors dismissed back then for lacking technical novelty (just a fork of ETH), has leaped into the top 5 ecosystems by on-chain assets and users.

More regrettable is Near Protocol, which championed sharding technology with TPS that crushed Ethereum's, whose founder was a co-author of the original Transformer model paper, which raised nearly $400 million — and now has only ~$60 million in on-chain assets. Of course, numbers fluctuate daily with market conditions, but the trend is unmistakable.

Developer and user stickiness comes from the ecosystem. For public chains, users include not just end users but developers (miners excluded here — a completely different model). For end users, whichever ecosystem has richer applications and more trading opportunities creates more stickiness. For developers, whichever ecosystem has more users and better infrastructure — wallets, block explorers, decentralized exchanges — gets prioritized for development. This creates a flywheel where developers and users drive each other.

The head effect is larger than imagined. Ethereum's user count and on-chain application capital exceed all "Ethereum killers" combined. Everyone (especially outsiders) thinks of Ethereum first when they think of smart contract chains — just as people think of OpenAI when they think of AGI today — it has become the de facto industry standard for blockchain application development.

Moreover, existing top public chains already hold massive cash reserves, able to offer developers investments or grants that new startups can't match. Finally, because most blockchain projects are open-source, mature top ecosystems allow for more composability building blocks for decentralized applications.

So what are the key differences between public chain and large model development?

Requirements for infrastructure. According to a16z statistics, most AI startups spend 80-90% of early-round funding on cloud services. AI application companies on average spend 20-40% of revenue on per-customer fine-tuning costs.

Put simply, the money is going to NVIDIA and AWS/Azure/Google Cloud. Although public chains have mining rewards, hardware and cloud costs are borne by decentralized miners, and the scale of data processed by blockchains is still trivial compared to the billions of data labels AI requires. So infrastructure costs for public chains are far lower than for large models.

Liquidity, liquidity, liquidity. A public chain without a mainnet can still issue tokens, but an AI large model company without users or revenue will struggle to go public. So while various "professor chains" may ultimately underperform expectations (after all, Ethereum is still the undisputed No. 1), from an investor's perspective, you're unlikely to lose money, and even less likely to get wiped out. Large model companies are different — miss the next funding round, find no buyer, and you're dead. From this angle, venture capital should be more cautious.

Actual productivity gains. Through ChatGPT, LLMs found their product-market fit and began being adopted at scale by both B2B and B2C users, boosting productivity. Public chains have been through two bull-bear cycles but still lack a killer app; use cases remain exploratory.

End-user perception. Public chains have strong ties to end users — to use certain decentralized applications, you have to know which chain they're on, then painstakingly move your assets there, creating some stickiness. AI is more invisible, like cloud services or the processor in your computer — no one cares whether their ride-hailing app runs on AWS or Alibaba Cloud. Because ChatGPT's memory is so fleeting, no one cares whether you're chatting with it on ChatGPT's homepage or through an aggregator. So retaining C-end users is harder.

As for crypto's applications in AI, many teams have offered their own perspectives. The consensus is that decentralized financial networks will become the default transaction layer for AI agents. I think the image below captures the current stage quite accurately.

Finding Needles in a Haystack, More Agilely

When I joined the crypto industry, I had almost no faith in decentralization. I suspect most early participants felt the same. People entered for all kinds of reasons — money, technology, curiosity, or pure chance.

But if you ask me today whether I'm confident in crypto, I'd say yes. You can't dismiss the entire industry because of scams, just as you couldn't dismiss all of finance because of Madoff.

A recent example from my own circle: my friend R (pseudonym). He successfully turned an idea into a company with 200 employees, positive cash flow, and a valuation over $200 million.

R built his startup around his understanding of decentralized value. "My girlfriend is a small influencer on TikTok, but influencers only get a tiny fraction of viewer tips," he once told me. The world's largest creator network isn't fair. "I want to build a decentralized version." I thought he was joking at the time, but about three years later, he actually launched it. The platform now has hundreds of thousands of users.

For someone who joined this industry at 24 right after graduation, the past seven years have shown me enough slices of the world: idealists and gold-rushing scammers; those who earned outsized returns and those who lost everything.

Remember the former boss I mentioned at the start of this article — an OG who made a lot of money in crypto once said: "You still have to work hard, or you'll just become a rich ordinary person."

I recall a respected investor who described VCs' work as "finding needles in a haystack." For me, crypto VC investing is the same process.

Perhaps the only difference is that crypto's haystack moves faster. So we must stay agile at all times.

This article was written by JW (@bestmosquito), founder of Impa Ventures. Impa Ventures is an early-stage fund focused on the Web3 industry.

Shiran, James, and Yongxiao Guo, analyst at Anyong, also contributed to this article.

Image source: IC Photo