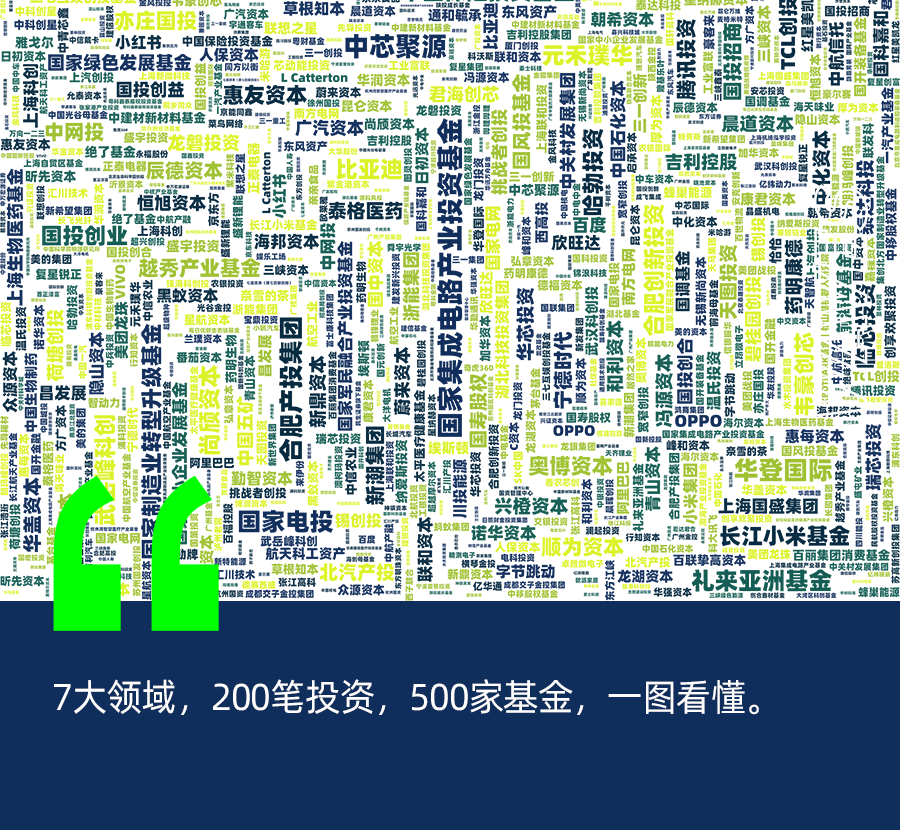

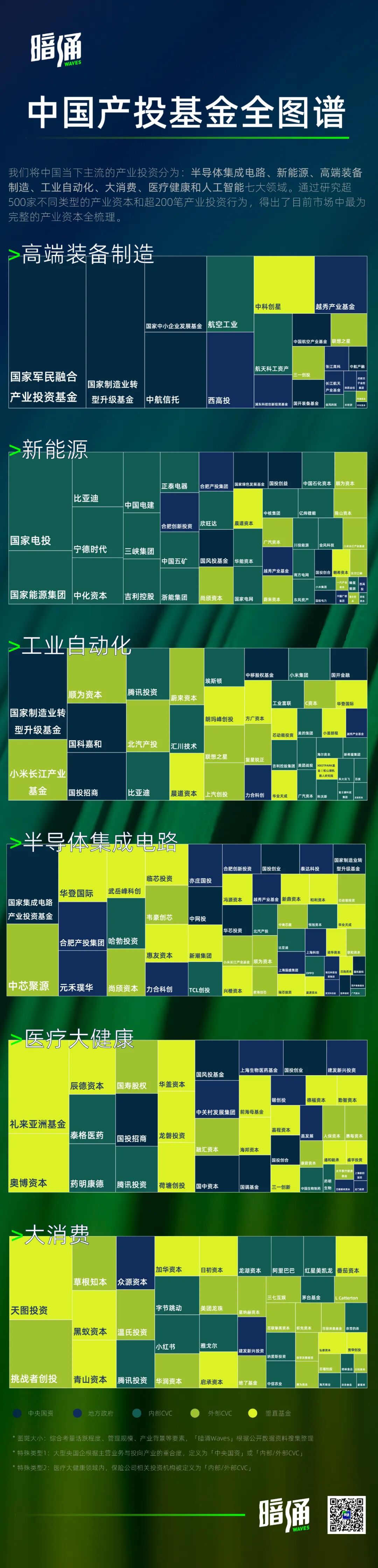

A Complete Map of China's Industrial Investment: When the Gears of Fate Begin to Turn

Seven sectors, 200 investments, 500 funds — all in nine charts.

Produced by | Dark Tide Editorial Department

If an investor time-traveled from ten years ago to today, they'd likely be stunned by this entirely different venture capital world —

The internet is no longer the investment theme of the day. Instead, peers are discussing energy, materials, and artificial intelligence. Investors with finance backgrounds are mired in anxiety, while PhDs in science and engineering are courted by the entire industry. In super deals, even the most prestigious VCs and PEs have to line up behind state-backed funds and major corporations, and dollar funds are no longer the golden ticket. The words entrepreneurs mention most: technology, orders, and empowerment.

Although industrial investment had sporadically entered the conversation since 2019, it was repeatedly interrupted by periodic bouts of euphoria. It wasn't until 2022 that large numbers of practitioners were forced to confront something: the era of industrial investment had truly arrived.

Compared to financial investment, industrial investment is more complex and intricate. Investors need deep understanding of specific industries' development to discover suitable investment opportunities along the industry's lengthy value chain. And because of the interweaving of every industrial link, post-investment coordination, empowerment, and cooperation carry equal or even greater importance than capital itself.

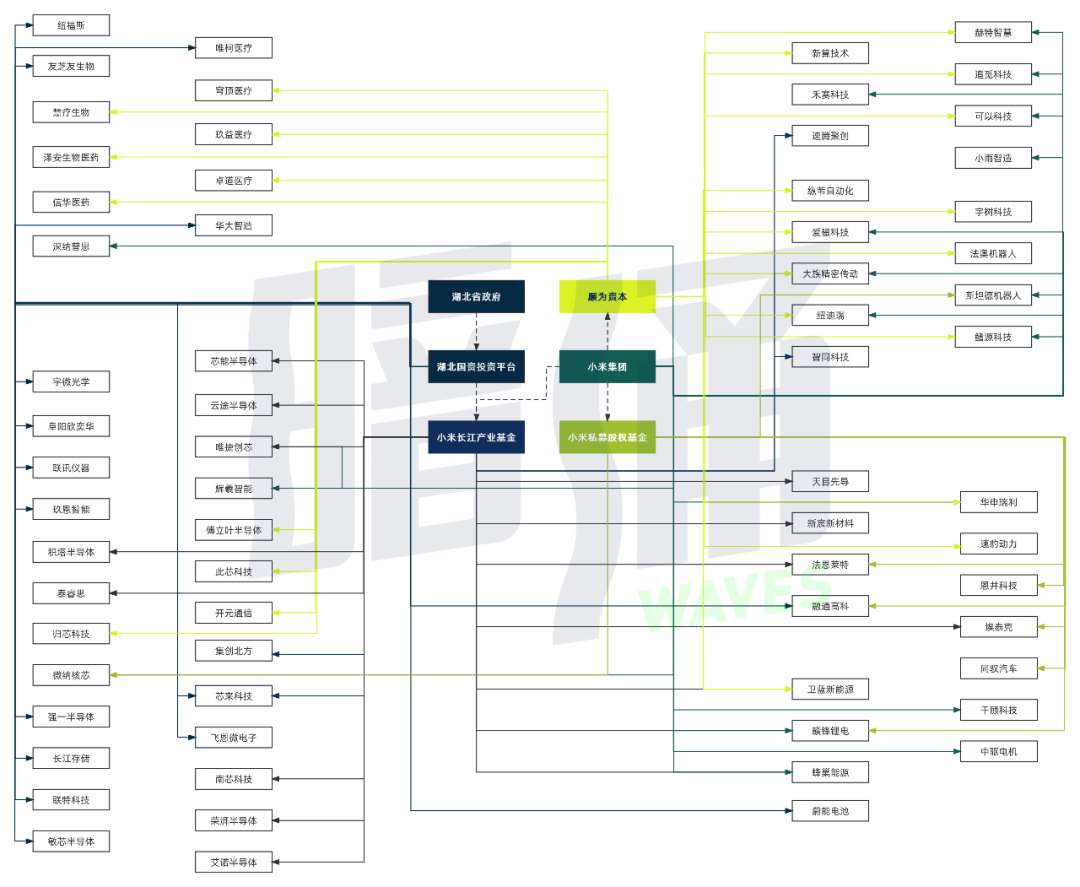

Using Xiaomi as a focal point, its ecosystem layout amply demonstrates the intricacy of industrial investment ecosystems. One can observe that the Xiaomi Changjiang Industrial Fund focuses more on technology manufacturing such as semiconductors and new energy; Xiaomi Private Equity Fund pays more attention to new energy vehicle industry layout (Xiaomi had previously announced its car-making plans); and as a fully independently fundraised firm, Shunwei Capital also dabbles in industrial and household robots that Xiaomi cares deeply about, but by comparison, Shunwei also invests in healthcare, consumer, and internet sectors, with broader coverage. Meanwhile, Xiaomi-affiliated funds also collaborate considerably with relevant government bodies in Lei Jun's home province of Hubei — the Xiaomi Changjiang Industrial Fund is regarded as a model of cooperation between leading enterprises and local governments.

Hubei Province and Xiaomi ecosystem investment landscape, Dark Tide illustration

Just recently, China National Integrated Circuit Industry Investment Fund Co., Ltd. (Huada Semiconductor) underwent industrial and commercial changes: the company's registered capital increased from approximately 10.035 billion yuan to approximately 17.282 billion yuan. The list of new shareholders covers nearly 30 institutions, with capital from state-owned assets, military, local governments, automotive leading enterprises, banks, and other backgrounds interwoven together. This seemingly extreme case is merely the most typical investment in the semiconductor integrated circuit industry.

The world of industrial capital is completely different from purely market-driven funds. They are diverse: they can be independent investment platforms or companies, or they may simply be small departments within large enterprises. They are complex: behind them can lie state will, local governments, corporations, families, or individuals who emerged from industry. Most are also difficult to detect: quietly cultivating specific industries for years, yet rarely appearing before the public eye.

This is also a major motivation for Dark Tide Waves to map industrial capital at this moment. We hope to present, at the threshold of a new era, an investment continent that has actually been slowly forming but long ignored by people. For China's primary market going forward, the mainstream shift from purely financial objectives toward industrial investment emphasizing industrial understanding, building industrial chains, and empowering industrial upgrading is a far more important development thread than the currency shift from dollar to RMB.

We have divided China's current mainstream industrial investment into seven sectors: semiconductor integrated circuits, new energy, high-end equipment manufacturing, industrial automation, consumer, healthcare, and artificial intelligence. On one hand, by collecting active industrial investment institutions and their investment behaviors in each sector from public information; on the other hand, by tracing the industrial capital behind important financing cases in these industries over the past two years, we have produced the most complete industrial capital mapping currently available in the market.

For this industrial capital research, Dark Tide Waves also received assistance from multiple primary market investment banks: Gaohu Capital, Lighthouse Capital, K&C Capital, Mumian Capital, Potential Capital, Taihe Capital, Yibai Capital, and Yunxiu Capital (in no particular order, sorted alphabetically by institution name). Our sincere thanks.

Semiconductor Integrated Circuits

Growing Investment Participants Under Policy Support

Semiconductor integrated circuits to modern industry are like cells to organisms. Differentiated designs for different functions ultimately become the nerves, heart, or brain of machinery. From infrastructure construction on the eve of the internet, to the era dividend of consumer electronics, to today's wave of automotive intelligence and AI emergence, the semiconductor integrated circuit industry connects to virtually every sector. Data shows that in 2023, China's semiconductor industry market size will exceed 1.5 trillion yuan.

Since 2000, the semiconductor integrated circuit industry has established its strategic industry position under continuously strengthening policies. With the 2014 release of the National Integrated Circuit Industry Development Guidelines and the establishment of the National Integrated Circuit Industry Investment Fund (Big Fund) Phase I, industrial investment in this field further entered a state-led era, with domestic semiconductors beginning their push toward mid-to-high-end substitution.

In the primary market, the Big Fund tends to participate in projects at Series A and B rounds and beyond. One exception was its 2021 angel round investment in Ningbo Nanda Optoelectronics, a photoresist developer — the strategic considerations need no elaboration. Meanwhile, the Big Fund also participated in several massive private placements of listed companies in the secondary market. For example, the over 2.6 billion yuan directed issuance of Tongfu Microelectronics in 2022. Listed company private placements are a relatively common financing form in the semiconductor integrated circuit industry; affected by technology cycles, funding demands are large at time points such as new product development and production line upgrades, and the Big Fund provides support for this.

Under the strong guidance of national strategy, participants in semiconductor integrated circuit industry investment have grown increasingly diverse.

First, Various Local Government Investment Platforms

When the Big Fund Phase II was established in 2019, its LPs included not only central cornerstones such as the Ministry of Finance, China Development Bank Capital, and China National Tobacco Corporation, but also over ten provincial and municipal local government-backed investors from Shanghai, Chengdu, Chongqing, Zhejiang, Anhui, and others — and these provincial and municipal local government investment platforms also broadly participated in direct investment projects across every link of the semiconductor industry.

From the perspective of investment purpose, local government investment platforms can be roughly divided into three categories: (1) Asset management type (e.g., Shanghai Guosheng Group, etc.), whose main responsibility is preserving and increasing the value of state-owned assets, with investment being one means among others, large capital scale, and compared to direct investment more inclined to contribute as LPs; (2) Regional development type (e.g., Yuexiu Industrial Fund, etc.), where supporting local enterprises and boosting regional economy through investment is an important mission, and in terms of targets often covers multiple regional pillar industries, with most of their capital coming from the first type of contributing platform — by number, this type of institution constitutes the main portion of local state capital; (3) Industry cultivation type (e.g., Beijing Integrated Circuit Manufacturing and Equipment Fund, etc.), which compared to the former focuses more on the development of a specific industry, "strengthening, supplementing, and extending chains" based on the local current industrial chain.

Local government contributions also relate to several semiconductor industry clusters. The Yangtze River Delta region developed semiconductors earlier with relatively better industrial foundation; the Pearl River Delta region has gathered downstream manufacturers and has gradually attracted and undertaken industrial transfer in recent years; the middle Yangtze River urban agglomeration has developed characteristic sub-sectors such as Wuhan Optics Valley optoelectronics.

Second, Leading Enterprise CVCs

From the parent company business perspective, these can be further subdivided into semiconductor enterprises and downstream application enterprises. Typical semiconductor CVCs include: TCL Venture Capital (TCL Group), ZTE Venture Capital (ZTE Corporation), Inovance Industrial Investment (Inovance Technology), etc. — these leading enterprises sit at different links of the semiconductor industry chain, invest according to their own characteristics, and have gradually moved toward raising external capital. The more widely discussed CVC is Hubble Investment under Huawei, which was entrusted with a critical mission when Huawei faced US blockades, with capital mainly flowing to "chokepoint" links in semiconductors.

Compared to internal corporate CVCs, in the semiconductor integrated circuit industry, the approach where industry players serve as main sponsors, joining with fund managers possessing financial investment experience to jointly establish industry funds, is more common. Representative institutions of this "external CVC" type include SMIC Capital (SMIC), Xindongneng Investment (BOE), Wehao Chuangxin (Will Semiconductor), Junhai Chuangxin (SK China), Xiaomi Changjiang Industrial Fund (Xiaomi Group), Xinwei Capital (Xinwei Technology), etc. Their core characteristic is the ability to accept broader and more flexible investment directions, not completely pursuing business synergy, possessing dual characteristics of both industrial and financial investment.

Industry leaders connected to the semiconductor integrated circuit industry also make industrial investments in this field. For example, various investment platforms under large automotive groups such as SAIC Motor and GAC Group, as well as new energy vehicle-related leading enterprises such as CATL and BYD, have all participated in investments in silicon carbide materials, power chips, power management chips, and other areas.

Additionally, there exist financial investors with various kinds of "industrial backgrounds" — founding partners with years of frontline industry experience, having raised key industry player or government funding, early portfolios growing into industry leaders, or even unverifiable personal connections all become associations with industry. Representative institutions include: Walden International, WY Capital, Huaye Tiancheng Capital, Xinchao Group, Xingcheng Capital, Xinding Capital, Linxi Investment, Heli Capital, Fengyuan Capital, etc.

It is necessary to specially note here that although new materials are often regarded as a unique and independent track, because the characteristics and applications of different materials vary enormously, there are relatively few investment institutions specializing in new materials.

State-backed investment vehicles include CNBM New Materials Fund, Sinopec Capital, etc., while market-driven institutions are represented by Chuanliu Investment. New materials funding mainly flows to three areas: silicon carbide and other third-generation semiconductor materials in the semiconductor field, as well as domestic photoresist and other consumables; perovskite, cathode/anode materials, thin films, coatings, etc. in the new energy field; and high-performance general-purpose materials such as graphene and superconducting materials.

New materials are tightly bound to downstream applications, but most markets are relatively niche with limited imagination space, leading to strong interest from internal CVCs in semiconductors and new energy for corresponding projects, while other institutions participate relatively less. On the new energy side, industrial investors such as CATL, BYD, Shangqi Capital, NIO Capital, and Svolt Energy respectively participated in important battery material projects such as Hefei先导薄膜 and Zhongcai Lithium Membrane; on the semiconductor side, Hubble Investment and BOE also participated in projects such as Fuyang Xinyihua and Tianyu Semiconductor. This article will not separately analyze and count industrial capital in the new materials field.

New Energy

Government-backed Funds > Industry-backed Funds > Financial Funds

Typically, government-backed funds enter at earlier stages, followed by funds with industry backgrounds that can bring industrial resources, and finally purely financial funds.

Energy transition is an effective path to promoting sustainable economic development, and transforming energy utilization methods and developing new energy is the consensus of countries worldwide. In 2010, the State Council executive meeting reviewed and approved in principle the State Council Decision on Accelerating the Cultivation and Development of Strategic Emerging Industries, establishing new energy as one of seven strategic emerging industries.

In September 2020, China formally announced its "dual carbon" goals: peaking carbon emissions before 2030 and achieving carbon neutrality before 2060. Following the introduction of these "30·60" targets, China's energy transition accelerated, renewable energy development intensified, and new energy investment surged. Some estimates project the total scale of the new energy industry could reach 10 trillion yuan.

Domestically, new energy supply chain investment primarily covers: upstream "basic resources" including lithium, cobalt, nickel, tin, and potash mines; "basic materials" such as separators, electrolytes, cathodes and anodes, auxiliary materials, alloy materials, and energy storage materials; midstream "components, integrated modules, and power batteries" including battery cells, generators, photovoltaic modules, silicon wafers, power batteries, motors, electronic controls, PACK, and BMS; and downstream new energy vehicles, power station operations, and service companies.

Currently, among investment opportunities in the new energy sector, funding for the power battery track has cooled. What investors still favor are "fuel cells, sodium-ion batteries, and energy storage." Over the past year, as wind and solar power's share of the grid has increased, demand for peak shaving and frequency regulation across the new energy supply chain has grown, triggering an explosion of investment opportunities in energy storage. According to joint statistics from KPMG and the China Electricity Council, 38,000 new energy storage-related companies were established domestically in 2022 — 5.8 times the 2021 figure.

The most active investor groups in new energy fall into two categories: financial funds that have been deploying since the early days of new energy vehicles, and large funds established by state-backed investors — either proactively or as LPs — following the introduction of national policies. Examples include SDIC Venture Capital, SDIC Innovation Investment, SDIC Chuangyi, CNNC Capital, and Three Gorges Energy.

Overall, active investors in new energy can be divided into three types: (1) State-owned investors, represented by SDIC Venture Capital, SDIC Innovation Investment, SDIC Chuangyi, China Life Equity, Guoce Investment, China Structural Reform Fund, National Social Security Fund, Hefei Industry Investment, and Xigao Investment; (2) Corporate investors, represented by State Grid, China Southern Power Grid, Three Gorges Green Energy, Sinopec, Kunlun Capital (CNPC), Xiaomi Changjiang Industrial Fund, SAIC-affiliated entities, CATL, and BYD; (3) Financial investors with resource endowments, represented by China Merchants Capital, Yuexiu Industrial Fund, CICC Capital, Goldstone Investment, and Yingke Capital.

Among these, SAIC is widely recognized in industry circles as a well-capitalized investment fund. SAIC's active investment entities include SAIC Investment (69 deals), SAIC Group (77 deals), Shangqi Capital (170 deals), and Hengxu Capital (102 deals), totaling 418 investments. SAIC has made broad-based investments across the new energy supply chain: upstream in basic materials and resources, backing companies like ESWIN Materials, Rongtong Gaoke, QingTao Energy, Hunan Yuneng, Tangfeng Energy, and Changyuan Lico; midstream in components, integrated modules, and power batteries, investing in CATL, Sunwoda Electric Vehicle Battery, Jinli Permanent Magnet, Zhilv Technology, and Jiejing Technology; and downstream in new energy vehicles and power stations, where SAIC Group owns IM Motors, Rising Auto, and new energy mobility company Xiangdao Technology.

NIO Capital is another representative emerging active investor in new energy, with 98 total investments. Founded in 2016 and relatively independent from NIO the automaker, NIO Capital focuses on upstream and downstream investments across the new energy vehicle supply chain, including power batteries, autonomous driving, new energy vehicle manufacturing, and power station operations — key segments of the NEV industry chain.

It's worth noting that due to the manufacturing nature of new energy projects, the entry sequence of their backing investors follows certain patterns. Generally, government-backed funds, industrial funds, and large financial funds form the standard investor mix. In terms of priority, government-backed funds typically enter earliest, followed by industry-backed funds that can bring industrial resources, and finally purely financial funds.

Meanwhile, some emerging specialized investors with vertical industry resources are playing an increasingly important role in new energy, with representative examples including Chaoxi Capital, Jinyu Maowu, Yunhao Capital, and Chendao Capital.

Take Chaoxi Capital as an example. Founded in 2015, this investment firm focuses on new energy and semiconductors. Managing Partner Hui Hengyu, who leads its new energy practice, has spent his entire career in investment banking and consulting focused on the photovoltaic industry, building deep industry connections. Vietnam Solar is among his representative projects. Thanks to years of industry accumulation, Chaoxi Capital's portfolio focuses mainly on midstream supply chain companies, including Hithium, FOX麦田能源, Jingkong Energy, Jinyuan Sheng, Chint New Energy, and斯威克新材料 — all "component and integrated module" companies. Chint New Energy, a photovoltaic cell and module company under the Chint Group, is particularly notable: Chaoxi Capital played a leading role in its spin-off and financing. This exemplifies the typical development path for investment firms with deep industrial resources and understanding.

Recently, the most noticeable change among new energy investors has been the increasing participation of local government funds, with notably larger capital commitments than before (Hefei Industry Investment being one example). Because new energy companies need to establish factories and industrial parks, this leads to various forms of binding arrangements between local governments and project companies.

Furthermore, the investor base behind new energy companies has become more diverse: beyond industry leaders making strategic investments through their corporate venture arms, cross-industry CVCs have also emerged. Examples include Midea Group, Wuliangye Company, Nanfang Black Sesame, miHoYo, Bilibili (which invested in Zeekr), OPPO (which invested in Sunwoda Electric Vehicle Battery), and Meituan Longzhu (which invested in Deli Technology, an ultra-high-purity fluorinated gas manufacturer).

High-End Equipment Manufacturing

Aviation and Satellite Equipment: Strongholds for Corporate Investment

High-end equipment manufacturing represents the premium segment of the manufacturing value chain, characterized by technology and knowledge intensity, high added value, strong growth potential, and significant linkage and spillover effects. It serves as an important indicator of a country's core competitiveness. Specifically, it encompasses six sub-sectors: aerospace equipment manufacturing, nuclear power equipment manufacturing, satellite equipment manufacturing, IoT-related equipment, marine engineering equipment, and rail transit equipment.

On October 10, 2010, the State Council issued the Decision on Accelerating the Cultivation and Development of Strategic Emerging Industries, incorporating high-end equipment manufacturing into the strategic emerging industries category. This was followed by successive policy documents including the Industrial Transformation and Upgrading Plan (2011-2015), Made in China 2025, the High-End Intelligent Remanufacturing Action Plan (2018-2020), and the 13th Five-Year National Strategic Emerging Industries Development Plan. With national policy support and domestic and international market demand, the high-end equipment industry's total scale has continuously expanded, reaching 21.33 trillion yuan in output value in 2022. It is projected to approach 40 trillion yuan by 2024, representing a massive market scale.

Among the sub-sectors of high-end equipment manufacturing, nuclear power equipment, IoT-related equipment, marine engineering equipment, and rail transit equipment have relatively lower degrees of privatization in their supply chains. Meanwhile, innovation in these areas has progressed relatively slowly in recent years, essentially remaining at the stage of new technological breakthroughs, with limited room for explosive growth by startups (private enterprises). Therefore, before emerging technological breakthroughs and supply chain restructuring occur, market-oriented investment institutions and industrial capital will remain in a wait-and-see posture toward these fields. Where corporate investment can participate is mainly in aviation equipment manufacturing and satellite equipment manufacturing.

Aviation equipment refers to manned or unmanned flight vehicle operations within Earth's atmosphere, encompassing aircraft, aero-engines, aviation equipment and systems, and aviation components. Since China's leading aviation equipment enterprises are essentially state-owned with clear advantages, possessing strong capital and technical capabilities and mature organizational coordination, they hold natural advantages and irreplaceable roles in core supply chain segments. The aviation equipment industry features high capital thresholds and high technical barriers, with core technologies remaining in the hands of leading enterprises represented by the Aviation Industry Corporation of China.

As China's participation in international aviation equipment division of labor deepens, private aviation technology enterprises have made rapid progress in aviation R&D and manufacturing, with small and medium enterprises emerging in mid-upstream non-core manufacturing segments such as materials and components, where strategic industrial investment is led by major enterprises. For example, the aviation industry has invested in testing equipment supplier Taihang Testing, landing gear producer AVIC Aircraft Landing Gear, die casting supplier Huafeng Casting, and instrument manufacturer Nanhang Electronics — these SMEs often had only one single customer, the leading enterprise, in their early stages. Other aviation equipment leading enterprises' corporate investors include AVIC Group and China Aerospace Science and Industry Corporation, among others.

The satellite and applications industry includes satellite equipment manufacturing, satellite application technology equipment manufacturing, satellite application services, and other spacecraft and launch vehicle manufacturing. The satellite application supply chain structure is relatively complex, but where private enterprises have emerged in greater numbers alongside corporate investment is mainly in rocket launch and development — primarily because there are comparable foreign companies (SpaceX), and successful testing reveals considerable market potential.

Rockets are the propulsion devices for spacecraft, the transport vehicles that deliver satellites into space. Although China's private aerospace enterprises remain in early development stages with incomplete supply chain formation, numerous corporate investors have already entered the field. According to analysis, beyond leading aerospace enterprises, many related funding sources have made industrial layout moves in commercial rockets. For example, small launch vehicle manufacturer LandSpace has received investment from leading enterprise AVIC Trust, as well as related state-owned platforms (National SME Development Fund, Xigao Investment, CMB International), manufacturing-related industrial capital (China Development Bank Equipment Fund), and real estate industrial capital (Sunac Investment).

Additionally, some corporate investors with broader sector scope and focus on frontier technology have made investments in rocket launch and R&D. For example, aerospace technology developer Orienspace has corporate investors including Legend Star, Sany Venture Capital, miHoYo, and Turing Venture Capital.

Industrial Automation

The Manufacturing Domain Most Accessible to Financial Investors

Industrial automation refers to the widespread adoption of automatic control and adjustment devices in industrial production to replace manual operation of machines and machine systems for processing and manufacturing. Since the 20th century, industrial automation has been one of the most important core technologies and industries in modern manufacturing, encompassing power, electronics, computers, artificial intelligence, communications, and electromechanical systems, requiring advanced technologies such as control theory, instrumentation, and computer information technology. It is a comprehensive interdisciplinary industry with notable characteristics of technology intensity, high investment, and high returns — a typical high value-added industry.

Data shows that China's entire industrial automation market will reach 311.5 billion yuan in 2023. In January 2023, the Ministry of Industry and Information Technology and 16 other departments jointly issued the "Robot+" Application Action Implementation Plan, requiring that by 2025, manufacturing robot density double compared to 2020 levels, with service robots and special robots seeing significantly deeper and broader industry applications.

Industrial automation and robotics already have relatively complete domestic supply chains, including: upstream (reducers, servo systems, controllers, machine vision, chips, sensors) — midstream (robot body suppliers) — downstream (robot system integration developers). Although the three most important core components of robots are "servo motors, reducers, and controllers," with investment events occurring across various supply chain segments, different industrial investors have different purposes.

Established domestic leading enterprises focus primarily on strategic investment and M&A. Listed companies in China's industrial robot industry mainly include Estun, SIASUN, Inovance Technology, and STEP. As established domestic industrial robot manufacturers, these leading enterprises' core purpose as industrial capital is still business expansion and extension.

Take Estun Automation, founded in Nanjing in 1993 with industrial robots and CNC machine tools as its main business. Since its 2015 IPO, Estun has accelerated its vertical integration upstream through strategic acquisitions of domestic and foreign companies, deepening its presence in core industrial robot components and establishing a full-industry-chain model of "core component production + robot body production + system integration," gaining strong competitive advantages across the entire value chain.

For example, in 2017 Estun acquired a 30% stake in Barrett Technology for $9 million, gaining mastery of integrated micro servo system key technologies and laying groundwork for entry into high-end servo applications including core components for service robots. To date, Estun has achieved important breakthroughs in servo systems, controllers, and other areas. By product category, Estun's portfolio mainly comprises automation core components and motion control systems, and industrial robots and intelligent manufacturing systems — with the latter being the company's primary revenue source, accounting for over 66% of revenue.

Compared with established players making strategic acquisitions later in their development, the upstream and downstream of industrial automation are filled with "financial investment institutions with industrial backgrounds," focusing primarily on strategic and early-stage investments.

In other upstream core component areas, industrial investors with state capital platforms, new energy vehicles, intelligent hardware, and internet backgrounds are active. Their investment domains mostly center on: key technology nodes in the industry, upstream/downstream partner enterprises, or frontier technology layout. For instance, harmonic reducer manufacturers Laifoo Harmonic Drive and Leader Harmonious Drive received investments from the National Manufacturing Transformation and Upgrading Fund, and from SDIC Venture Capital and F&G Capital respectively (key technologies). There are also corresponding domestic substitution opportunities in sensors and other fields — LiDAR developer Hesai Technology received investments from Baidu, Xiaomi, and Meituan (frontier layout); RoboSense in the same space received investments from Fosun, BAIC Capital, Cainiao Network, BYD, Xiaomi Changjiang Industrial Fund, Geely Holdings, GAC Capital, Yuexiu Industrial Fund, China Mobile Equity Fund, and other industrial players (business cooperation).

Investors in mid- and downstream robot body suppliers and integrated development manufacturers are mainly intelligent hardware and internet-backed corporate investors. For example, commercial autonomous cleaning robot developer Gaussian Robotics counts Meituan, Tencent, and Meituan Longzhu among its investors. Humanoid robot developer UBTECH's investors include iFlytek, Tencent, and others. Taking Xiaomi Group as an example, in consumer robots it has Ninebot, Viomi, Roborock, and Dreame; in industrial robots it has Standard Robots, Zhitong Technology, and Xiaoyu Intelligent Manufacturing.

Consumer

Internet Giants and New/Old Consumer Leaders Take Center Stage

China's consumer market has undergone continuous expansion and now ranks first globally. In 2016 and 2019, China's total retail sales of consumer goods successively surpassed 30 trillion yuan and 40 trillion yuan. In the first half of 2023, national retail sales of consumer goods exceeded 22 trillion yuan, with full-year market size expected to surpass 45 trillion yuan.

On July 31, the General Office of the State Council forwarded the National Development and Reform Commission's Measures on Restoring and Expanding Consumption, which called for leveraging market resource allocation, building a unified national market, achieving a virtuous cycle of consumption recovery; improving the quality of consumption supply and demand to achieve high-quality development; and improving mass-market, inclusive consumption.

From an industry perspective, the consumer sector encompasses core segments including beauty and personal care, apparel, home living, consumer electronics, pets, and sports and fitness. Among these, the tea drinks, dining, and snack tracks that have surged in popularity since 2020 can, based on differing business models, be divided into "food and beverage" dominated by online channels, and "offline dining" dominated by offline chains, tracing upstream to encompass the supply chain of the "food" domain.

With the rise of the "new consumption" concept, the entire consumer investment market peaked in 2020-2021. However, as valuations soared and supply-demand imbalances emerged, some capital chose to wait and see. After 2022, consumer company valuations and financing generally suffered setbacks, and financial funds withdrew in large numbers.

Due to the inherently B2C nature of consumption and offline consumption's dependence on commercial real estate, the mainstream forces of industrial investment in this field mainly include:

First, internet giants whose primary audience is B2C consumers, such as Alibaba, Tencent, and Meituan Longzhu. Taking Meituan Longzhu as an example — formerly the Meituan Industrial Fund focused on consumer sectors, it has become a "viral brand harvester" in new consumption, investing in Mixue Ice Cream & Tea, Hey Tea, Manner, and Momo Dim Sum, among others. But the most distinctive feature of these internet giant CVC investment strategies is their alignment with parent company strategy. In recent years, as Meituan's overall investment logic has shifted toward hard tech, Meituan Longzhu's investment direction has changed accordingly.

Second, leading enterprises from traditional and new consumer sectors. Traditional consumer leaders include Moutai Jianxin Fund, a joint venture between Kweichow Moutai Group and CCB Trust, mainly investing in food supply chains and packaging materials; L'Oréal Group, which established the BOLD fund for direct investment and subsequently set up its China market investment company Meicifang, co-investing with Cathay Capital in fragrance brand Documents. New Hope Group has established Grassroots Zhiben, Shengwang Fund, and incubation platform Xiaocao Infinite — the synergy among these three lies in enterprises being sensitive to industrial capital taking too large an equity stake, so Shengwang can enter first with small equity investments, then Grassroots Zhiben takes over. In new consumption, tea drink representatives directly invest in Hey Tea, Chayan Yuese, Nayuki, among others; there is also Challenger Ventures founded by Yuanqi Forest's Tang Binsen, which remains active in consumer sectors. On July 30, Bestore's wholly-owned subsidiary invested 100 million yuan to participate in establishing a food and consumer goods fund, with investment directions including brands, retail, supply chains, and consumer technology.

Third, real estate-backed CVCs sitting on commercial properties across regions. Country Garden Venture Capital invested in Wenheyou, co-invested with Wens Capital in tea brand Chali, and co-invested with Qinqin Foods in Hankou No. 2 Factory. Longfor Capital, backed by Longfor Properties, has invested in Perfect Diary, Yuanqi Forest, Dingdong Maicai, Hefu Noodles, Shuhai Supply Chain, Haimati, Gaussian Robotics, and a series of other projects.

More enterprises choose to enter investment by establishing external CVCs. Mengniu established Mengniu Venture Capital, mainly looking at biotechnology to support its food business, and green low-carbon technology to support Mengniu's massive animal husbandry industry chain. In 2022, Yili established Shenzhen Jianling Innovative Seed Private Equity Investment Fund Partnership, mainly around healthy food, health-related, and other investment-worthy areas. Other representative enterprises include Shanghai Chuangweilai Investment Co., Ltd. established by Qiaqia Food's investment, and Shanghai Laiyifen Private Equity Investment Fund Partnership established by Laiyifen with registered capital of 100 million yuan.

Beyond direct investment, consumer sector leaders also enter the primary market as LPs. For instance, in 2018, Juewei Food's Wangju Capital deployed capital to Tomato Capital, which focuses on early-stage dining investments. Another example is Jinding Capital, which partners with multiple consumer listed companies. This is an investment institution specifically undertaking listed company CVCs, having assisted more than twenty enterprises with CVC investments including Care Pet Food, Marubi, and Laiyifen — all in the form of jointly establishing 100-million-yuan-level funds.

From the target perspective, the most obvious aspect of consumer sector industrial investment is investment in brands, with the core appeal being to find a second growth curve for brand development. Through investment layout, leading new consumer brands hope to explore new business models and complete industrial chain layout to cope with future commercial competition. From this starting point, Hey Tea took a stake in coffee brand Seesaw; Mixue Ice Cream & Tea's "Snow King Investment" invested in Hui Cha; Pop Mart's strategic investments are mostly concentrated in core business IP-related companies.

Moreover, investing in supply chains is also one of the core contents of industrial investment in consumer sectors. Consumer brands may experience life and death, but the supply chains behind them remain standing. In the past three years, more than 15 supply chain companies have successfully listed or are in the process of listing, especially concentrated in new tea drinks and coffee. Looking through their financing history, downstream corporate CVCs usually appear. Haidilao's supply chain arm Shuhai Supply Chain completed a new funding round of 800 million yuan last September, with China Resources Group, Yonghui Cloud Innovation, Super Species, and Longfor Capital participating. Guoquan Shihui received billions of yuan from Sanquan Food, Wumart United Capital, Moutai Fund, and other investors.

Healthcare > Centered on Innovative Drugs

The healthcare industry is an important component of the national economy and receives attention from multiple stakeholders. Its main components include healthcare, medical services, and medical information technology. Fu Qiang, Secretary of the Party Committee and Director of the National Health Commission's Health Development Research Center, stated at an event that in 2020, the total scale of national health services was approximately 8.1 trillion yuan, "and it is expected that by 2025, the total scale of China's health services will reach 12.4 trillion yuan."

Before 2014, industrial investment in healthcare was sparse, until a turning point in 2015. In August 2015, the State Council issued Opinions on Reforming the Review and Approval System for Drugs and Medical Devices, launching a magnificent reform. Superimposed on the "mass entrepreneurship and innovation" wave, structural adjustment driven by policy, product iteration driven by technology, and industrial transformation driven by talent began to occur. In 2018, HKEX launched the Chapter 18A policy (allowing unprofitable biopharma companies to IPO), bringing healthcare investment to a climax.

During this period, besides biopharma specialized funds rooted in the industry and diversified investment institutions active across technology, consumer, and healthcare sectors, CVCs — especially internal CVC investments by healthcare enterprises — participated at high levels.

And among all healthcare sub-sectors, innovative drugs represent the largest financing volume, highest attention, and greatest potential for legendary stories, as well as a sector that numerous healthcare CVCs cannot avoid, followed by medical devices.

Our research found that in this R&D-intensive field, large pharmaceutical industry groups and their CVC investment institutions play important roles. Pharmaceutical groups established for 5-10+ years with certain achievements in their respective segments all possess their own CVCs to some degree, with four specific stages: (1) The parent company's industry is undergoing transformation, needing new products or services to build new moats, generally through M&A; (2) The parent company's core business model is mature with stable revenue capacity; (3) Innovation is active at the industry tail, becoming an important force for achieving industrial chain completeness; (4) Industry competition is relatively concentrated, and the parent company's industrial chain strength is sufficient to incubate and accelerate startup development, gaining greater financial returns through investment.

But relatively well-known and more active are paradoxically the "pick-and-shovel" CXO companies. They extended into the pharmaceutical industry earlier, investing in early- and mid-stage companies through internal CVCs, external fund partnerships, and even as LPs — such as the trio of WuXi AppTec, Tigermed, and Pharmaron.

WuXi AppTec's investment history roughly began in 2012; to date, its corporate venture capital fund has invested in over 60 companies, with the most at Series A and B stages. It mainly conducts controlling and minority equity investments through establishing investment management companies (such as Shanghai WuXi AppTec Investment Management Co., Ltd.) and participating in equity investment funds (such as Mint Ventures and 6 Dimensions Capital funds). Though Tigermed has not established a specialized asset management subsidiary, it has made minority equity investments in innovative biopharmaceutical and medical device startups through initiating and participating in equity investment funds, such as participating in multiple funds from Yingke Capital, Beike Venture, Oriental Ares, and Mint Ventures. Pharmaron's jointly established Kangjun Capital with Legend Capital is also quite active, for instance recently participating in investments in allergy immunotherapy innovative drug developer Biomunova and innovative drug company Trinomab.

What makes healthcare CVCs special is that as resource providers in the CVC relationship chain, beyond capital and brand credibility, parent companies more importantly output industrial chain support elements, even helping invested companies complete the difficult growth process from 0 to 1. For CXO companies, innovative drug enterprises are both their customers and their investees, enabling tighter binding of commercial relationships.

In the past year, state capital and local government platforms have shown up more frequently behind healthcare companies.

Two striking examples: Yanming Biotech, which just completed a 700 million RMB Series A round, saw new investors that were entirely state-owned or insurance-backed: SDIC Venture Capital, China Reform Fund, Taiping Healthcare Fund, China Life Sci-Tech Fund, and Lotus Venture Capital. Around the same time, Sinotau Pharmaceutical announced a new funding round exceeding 1.1 billion RMB, with investors including SDIC Venture Capital, Goldstone Investment, China Reform Fund, Genertec Venture Capital, CITIC Securities Investment, and Xihong Investment, while existing shareholders China Life Equity and Lotus Venture Capital followed on.

Beyond these players, healthcare has also attracted funds with distinctive capabilities and resource coverage. Take Lilly Asia Ventures, which spun out from Eli Lilly's corporate venture unit and became an independent investment management firm in 2011. It was among the earliest biopharma-specialized funds to dig deep into China's innovation market, and remains one of the industry's leading life sciences and healthcare CVCs — as well as a critical source of intelligence and product pipeline for Eli Lilly's own innovation capacity.

In addition to the above, in recent years diversified participants have entered healthcare — insurance companies, real estate developers, and cross-sector companies looking to pivot. Insurers have moved into medical services through investment, acquisition, and greenfield development, accumulating experience for exploring managed care models. Representatives include Taikang, Sunshine Insurance, and Ping An. Real estate developers such as Wanda, Evergrande, Sino-Ocean, and Yihua have years of senior housing operation experience and later expanded into general hospitals and specialty hospitals. China Life Equity has been particularly active in healthcare investing. Established in June 2016 as China Life's specialized private equity investment platform, the China Life Healthcare Fund was also the first insurance-funded private equity fund approved after the former CIRC issued relevant policies, and has since made dozens of investments in the space.

Optimistic about healthcare's growth trajectory, numerous companies whose core business lay elsewhere began making "crossover" moves — Leo Group, Gree Electric, Changbao Co., Jinzuo Ham, Guangzheng Group, among others. Changbao Co., which primarily researches, develops, and manufactures specialized steel pipes for natural gas, boilers, and machinery — a quintessential industrial manufacturer — made a nearly 1 billion RMB investment in 2017 to acquire three hospitals in one go.

Artificial Intelligence > The Tech Outpost for Internet and AI Giants

As an emerging industry, China's AI sector has maintained strong momentum with continuously expanding market scale in recent years. According to LeadLeo's 2023 China Artificial Intelligence Industry Overview, China's overall AI industry reached 375.1 billion RMB in 2022.

Centered on intelligent computing, the entire industry encompasses a complete system of infrastructure (data center construction), hardware infrastructure, and software infrastructure. Specifically, the industrial chain breaks down as follows: upstream suppliers of IT and civil engineering infrastructure; midstream intelligent computing service providers, cloud service providers, and internet data center operators; and downstream industry users in internet, finance, telecommunications, and transportation whose AI application demands drive related industries including autonomous driving, robotics, the metaverse, smart healthcare, entertainment content creation, and intelligent scientific research.

Industrial capital stationed in AI has historically concentrated among internet giants perpetually exploring frontier technologies, AI companies themselves, and application-oriented firms in gaming, robotics, and automotive whose future business could synergize with AI. Investment directions showed a clear divergence before and after ChatGPT ignited a new round of AI industry competition. The previous AI wave, enabled by deep learning breakthroughs, primarily deployed in computer vision, speech, and surveillance/security applications. Active corporate investors mostly clustered around these directions, entering along single or niche-scenario investment logics dictated by commercial ecosystem-building needs.

At that time, representative AI CVCs included Baidu Ventures and SenseTime's Guoxiang Capital (AI industry fund). Among the BAT trio, Baidu made the most conspicuous AI moves. In 2016, Baidu Ventures was established as an independently operated fund without Baidu strategic KPIs. Overall, it had limited connection to Baidu's core business — an independent venture capital institution with relatively flexible decision-making mechanisms, but one that could help the parent company explore new business models, build commercial ecosystems, and consolidate market position.

Under the influence of internet giants like Alibaba and Tencent whose CVCs were aggressively expanding in prior years, many smaller giants and even unicorn-stage companies began investing in other startups in their domain. SenseTime, one of the "Four AI Dragons," exemplified this trend. In May 2020, SenseTime led the 30 million RMB Series A round for Honghong Robotics, an AI educational robotics company.

SenseTime later established Guoxiang Capital, an industry fund focused on AI investments.

In 2021, Guoxiang Capital led the 138 million RMB Series A round for Mantis Vision, funding 3D technology R&D, 3D studio deployment, and metaverse content production. In 2022, Guoxiang Capital not only led the nearly 100 million RMB angel round for domestic 3D graphics engine provider Xuan Guang Technology, but also co-led the nearly 100 million RMB B1 round for intelligent driving high-performance computing software platform InChorus, among other deals.

A particularly notable sub-sector within AI is autonomous driving. The computing power, massive data processing capability, algorithmic decision-making, and sensor data collection required for an autonomous vehicle represent a remarkably high bar within AI. Moreover, achieving road-ready autonomous driving demands extreme sensitivity and precision in automotive electronics' perception, decision-making, and feedback loops. Autonomous driving can be considered AI's ultimate landing scenario.

Representative companies that have emerged in this space include Pony.ai, Momenta, and MINIEYE. The investor bases behind scaled autonomous driving companies consistently feature industry leaders, with notably active participants including: OEMs (Toyota, SAIC Motor, Dongfeng Motor, GAC Group, Yutong Group), components giant Bosch Group, and map provider NavInfo. Additionally, ecosystem-linked giants like Tencent, logistics company GLP, JD Group, and SF Holding have also made investments.

It's worth noting that autonomous driving companies typically require substantial R&D funding, so their investor rosters usually include major financial funds. However, TrunkTech is an exception — its backers are overwhelmingly industrial capital or institutions with strong industry backgrounds. These include: iFlytek and iFlytek Venture Capital at the angel round; NIO Capital and GLP at Series A; Hidden Hill Capital and Bosch Ventures at A+; Yuexiu Industrial Fund and Bohai Industrial Investment Fund; and BAIC Capital and SDIC Assets at Series B.

ChatGPT's emergence brought new platform opportunities and a fresh battle for traffic entry points. This led many institutions to initially pour into general-purpose large model investments. But the heavy resource requirements and intense capital needs of general large models — destined to be "a game for the few" — quickly gave pause, prompting migration toward vertical large models in healthcare, law, and education, as well as middle-layer and application-layer opportunities.

To date, notably active CVCs in this space include miHoYo, Meituan Strategic Investment, and Tencent Investment.

Given AIGC's clearly foreseeable cost-reduction and efficiency gains for game production, plus its potential for pushing other boundaries, the gaming industry has been among the most enthusiastic embracers of this new AI wave.

miHoYo, for instance, participated across multiple rounds in Minimax, currently the highest-valued startup in China's large model entrepreneurship wave. Minimax's core team members hail primarily from AI teams at SenseTime, the Chinese Academy of Sciences, and Uber.

Meituan Strategic Investment has also been especially active in this AI wave. Not long ago, due to health issues, Wang Huiwen's Lightyear Beyond was rapidly acquired by Meituan for $285 million — making it the largest M&A transaction in China's large model space to date. Meituan also made a sole investment in another highly-valued star company in the current large model wave, Zhipu AI. Following its B-2 round, Zhipu was valued at over $500 million.

Of course, because AIGC applications are heavily dependent on underlying large model capabilities and difficult to truly differentiate, much related investment has yet to form industry consensus, largely remaining under the radar or in wait-and-see mode.

However, one common collaboration emerging now involves model customization and resource exchange: companies with relatively mature large model development but insufficient familiarity with landing scenarios, partnering with application-layer companies that control downstream vertical and niche scenarios but lack the compute or capabilities to support model development and fine-tuning.

Meanwhile, because AI's industrial chain — unlike new energy or semiconductors — is not a lengthy modern manufacturing chain, it shows no strong geographic preference. Talent density is likely the most critical factor. Thus Beijing, Shanghai, Shenzhen, and the Yangtze River Delta, where relevant talent clusters most densely, are where AI-oriented industrial capital is more active. Compared to some financial funds in this domain, industrial capital with greater funding, resources, ecosystem, and scenario advantages clearly holds the upper hand.

Because AI has consistently occupied a relatively frontier exploratory zone, for most companies it often has limited connection to current strategy and core business, playing more of an "outpost" and "experimental field" role. Many companies use external AI investments to explore and supplement cutting-edge technologies and business models, using innovative forces to push parent company development or build more commercially competitive ecosystems.

Image source | Chart by Waves Editorial Team

Layout | Guo Yunxiao