A Conversation with Weijian Shan: Always Be Prepared

Even when cast into a barren wilderness of nothingness, a person can still make their own choices.

By Lili Yu

Edited by Jing Liu

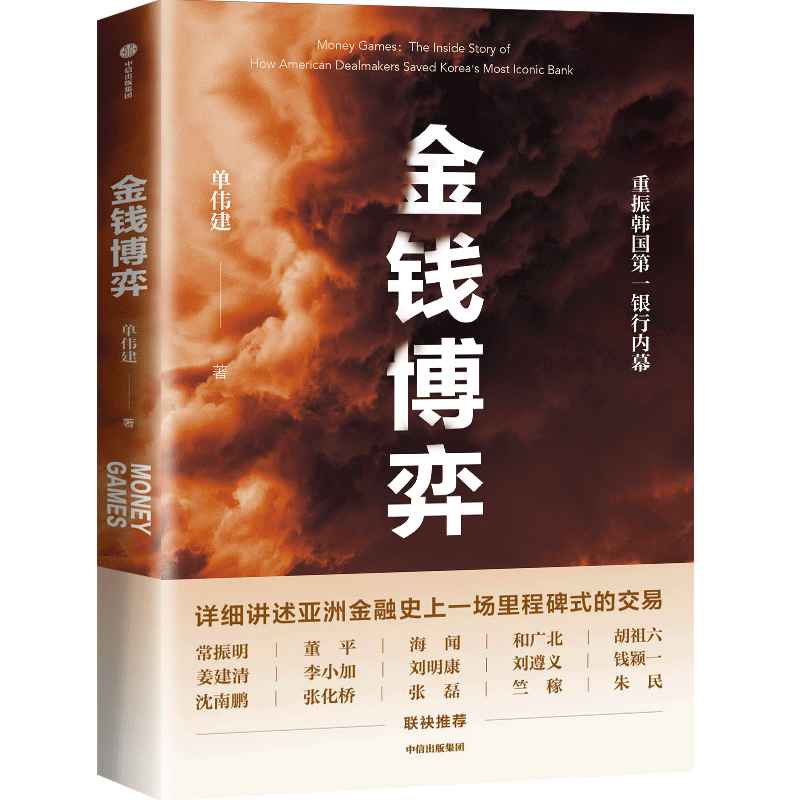

Barbarians at the Gate, the classic primer on investment and M&A, is widely known for its A-side: in 1988, KKR outbid three rivals to seize control of RJR Nabisco for $25 billion. But most people never learn the B-side — KKR exited 15 years later not having made a dime, but having lost $730 million.

Unlike typical financial investments, buyouts layer capital gains with operational value creation. Because they often involve massive sums, complex dealmaking, and control battles, buyouts have always carried a certain mystique of blood and thunder in the financial world.

This is precisely what makes Weijian Shan's newly published Money Games so rare: for the first time, an insider and participant records a major acquisition from entry to exit in full.

During the Asian financial crisis, amid Korea's tangled web of government-business relations, nationalist sentiment, and commercial competition, Shan — as lead negotiator for Newbridge Capital — wrested control of what was then Korea's largest commercial bank from the Korean government. Newbridge restructured and expanded it over several years, then exited perfectly. Shan became a legend overnight.

Shenzhen Development Bank was another crowning achievement. In 2004, with negotiations on the verge of collapse, Shan's team at Newbridge finally secured control — the first and only case of foreign acquisition of a Chinese national commercial bank. After a series of reforms and restructuring, the bank saw years of dramatic asset and profit growth, and Newbridge exited successfully.

Shan is a co-founder of PAG. His greatest contribution was establishing a fund focused primarily on buyouts, which has remained his consistent investment strategy. For many years, buyouts were not the mainstream; growth equity was far more common.

In Shan's view, growth equity features minority stakes, "growth above all else regardless of profitability," and "expansion at any cost — the kind of indiscriminate investing you see everywhere." Buyouts, belonging to the value-investing tradition represented by Warren Buffett, don't chase market fads. "They must be based on the target's profitability and potential for profit growth, creating value by acquiring control and improving operations."

For the past decade, growth equity was the market darling while value strategies lagged. But as central banks in developed economies pivot from quantitative easing to tightening, and the tide recedes, perhaps it's time to reconsider buyouts.

Many say investors earn what they deserve. Shan is a devoted practitioner of this truth. In his 12 years at PAG's helm, apart from a handful of financial investments like Nayuki, nearly all of PAG's deals have been buyouts: Yingde Gases, Zhenai.com, Universal Studios Japan (USJ), and others. By end-2021, of the $70 billion PAG had invested, $40 billion had already been realized. At end-March this year, PAG filed for a Hong Kong Stock Exchange listing, potentially becoming the city's largest IPO of 2022.

The publication of Money Games was the immediate reason for An Yong Waves's recent interview with Shan. But more interesting is the relevance of his experience to the present moment.

In 1969, having just finished elementary school, Shan was sent down to the countryside as part of the Down to the Countryside Movement, assigned to reclaim wasteland in Inner Mongolia's Gobi Desert. For six long years, through bitter cold, he worked alongside wheat and corn. Many descended into despair, frittering away their time. Shan's choice: cupping a kerosene lamp (hiding it from others), reading everything he could get his hands on — even pesticide manuals.

It wasn't until 1979 that Shan, now a "worker-peasant-soldier student," graduated from the University of International Business and Economics and stayed on as faculty. He later went abroad for graduate studies at UC Berkeley, where his advisor was Janet Yellen — later Federal Reserve Chair and now U.S. Treasury Secretary.

His early years left instinctive marks: he still can't stand the smell of kerosene, dares not waste time, and lives perpetually in tomorrow, always on the move.

This even showed in our interview. A sudden 15-minute gap before our conversation made him "uneasy" — so he quickly disposed of it by reading through a magazine.

"If I never get opportunities in this life, there's nothing to regret. But if I wasn't prepared, I can only blame myself." Shan repeated an exceptionally plain sentence many times during our conversation: "So, always be prepared."

Shan's story demonstrates: even when cast into the void of the wilderness, a person can still make their own choices.

The Most Important Thing in Investing

"An Yong": I heard the simplified Chinese title went through several changes before landing on "博弈" (games/contest). Is M&A dealmaking essentially a game?

Shan: A title needs to pique reader interest. To negotiate any acquisition well, you must know yourself and know your enemy. Knowing yourself is relatively easy; knowing your enemy is hard. "Games" captures the mutual calculation between both sides, the process of reaching consensus.

"An Yong": Why is "knowing your enemy" always difficult?

Shan: Because you don't understand the other side's predicament from day one. You gradually come to realize it. When talks get stuck, you feel frustrated — you don't understand why they suddenly back out of what was agreed. But once you understand their predicament, problems become easier to solve. That's my experience.

"An Yong": So the key is building empathy.

Shan: To succeed in a negotiation, you must put yourself in the other side's shoes, consider their interests, build trust. This takes enormous time to read their psychology and understand their thinking. If we could empathize more during negotiations, they probably wouldn't be so fraught.

"An Yong": Can you give an example?

Shan: Yingde was a Hong Kong-listed company that we took private. Initially, the majority shareholder promised to sell us their stake, but it was a conditional promise: if someone bid higher, the promise would automatically cancel. Such a reversible promise was essentially meaningless to us. But we considered their predicament — of course they wanted the highest price. So we reached this arrangement: if a third party bid more than 5% above us, they could exit the promise; but if we matched that 5% increase, we'd have right of first refusal. This way, they were reassured, and so were we. Because of our priority right, many would consider the cost and not even compete. The core of this process is: you must think for the other side.

"An Yong": In your long investing career, what was your most expensive tuition payment?

Shan: $40 million, total loss. It was searing.

"An Yong": Why did it fail?

Shan: It was a network integration company. Its main business was taking imported routers and other equipment, adding its own software, and integrating them into mobile phone networks. At the time, the American supplier's products were in severe shortage. So you had to maintain good relations with their China team to get any equipment.

After we took over, we discovered the American supplier's China team was demanding kickbacks from customers. I reported this to my then-boss at TPG, David Bonderman. Together we called the supplier's CEO and told him — effectively reporting his China team. They were fired and replaced. But we could never get their equipment again. And this wasn't the only American company in the industry taking kickbacks. Our investment collapsed. Total loss.

"An Yong": What if you had looked the other way? Some believe there's room for certain gray areas in the market.

Shan: For us, any illegal, unethical, or non-compliant behavior is intolerable. We manage other people's money. We must be spotless, zero-tolerance, not a single misstep.

"An Yong": Indeed, reputation matters enormously.

Shan: Building a company's reputation takes years, but it can be destroyed in an instant. When I was an independent director at Bank of China (Hong Kong), the CEO was arrested. Another independent director — a former Citibank executive — resigned over this. He feared his lifelong clean reputation would be tarnished. I didn't agree with but understood his choice. It was precisely when independent directors were needed to help the company. Caring about reputation isn't about building some image — it's about protecting what you have from being damaged.

Why Transforming Companies Matters So Much

"An Yong": PAG has done many buyouts, but for the past decade or two, conventional wisdom held that China lacked a fully developed buyout environment.

Shan: In global capital allocation to Asia, the vast majority flows to venture capital and growth equity; the proportion going to buyout funds is relatively small. But this doesn't mean China lacks buyout opportunities. In fact, among Asian markets, China offers more acquisition opportunities than any other.

For example, AirPower Technology — which we fully control — was formed from our wholly acquired Yingde Gases and our 65%-acquired Baosteel Gases. When we acquired Yingde, we had some competitors, but few. When we acquired Baosteel Gases, our competitors were two strategic investors; no other financial investors participated because they didn't understand the industry well.

"An Yong": What informed your judgment on Yingde Gases?

Shan: Investment opportunities are often serendipitous, but encountering one doesn't mean everyone can recognize it as a good opportunity — it depends on your understanding of the entire field. We happened to know industrial gases extremely well. I had exposure to the industry over 20 years ago and knew that customer-supplier relationships are governed by long-term contracts. These companies produce gases — oxygen, nitrogen, rare gases, etc. The production equipment is built on the customer's site; they're my only customer, I'm their only supplier. Both sides are contractually bound to buy and sell, so cash flow is extremely stable.

When we learned of shareholder disputes at Yingde Gases, we immediately moved to seize the opportunity. Actually, I happened to run into a major shareholder's financial advisor at a hotel. When he mentioned Yingde, I immediately expressed acquisition interest. Coincidentally, our Shanghai team was already in discussions with other shareholders to acquire their stakes.

"An Yong": How did you handle Yingde's internal shareholder disputes?

Shan: We bought 100% of the equity.

"An Yong": The conflicts suddenly became unimportant.

Shan: Not just unimportant — they ceased to exist. All previous shareholders were out. We replaced management.

"An Yong": Is replacing management the most critical step in a buyout?

Shan: There's no fixed rule; it depends on the company's actual needs. But the single most critical person is the CEO. If it's already a troubled company, there's more work to do. Our restructuring of Shenzhen Development Bank was more extensive than the Korean bank in Money Games. If the company is relatively stable, we have less to do. But our operating team functions more like management consultants — we don't step in to manage directly, we help the company's management team.

"An Yong": What are the other steps after buying out a company?

Shan: We have two teams: an investment team and an operating team responsible for post-investment management. When making investment decisions, it's not just the investment team giving opinions — the operating team also participates, doing analysis, developing plans, figuring out how to restructure or expand the target's business. We often have a "100-day plan" before we even invest.

Henry Kravis, co-founder of KKR, once said: "Any fool can buy a company." Meaning, if you pay enough, you can acquire it. But what really matters is what happens after you buy it — whether you create value. Improving operations to create value: that's our main work.

"An Yong": Some believe buyouts struggle to take root domestically due to certain Eastern cultural factors: many entrepreneurs want their companies transformed, yet don't truly want to relinquish control.

Shan: This problem is actually quite solvable. Say we have a partner who won't give us majority control — as long as our interests are aligned and management achieves agreed targets, shareholders can coexist peacefully. We agree upfront: if targets aren't met in one or two years, we must change people. The entire point of having control is the ability to replace management.

"An Yong": But many precedents prove how hard that person is to choose. And a chronic China problem is the general shortage of professional managers.

Shan: The first choice often isn't the best fit. We had the same experience with Shenzhen Development Bank. Once we realize someone isn't optimal, we replace them. You need that flexibility.

"An Yong": Why not step in and run it yourselves?

Shan: Because you must choose the best talent in that industry. We can invest in banks, industrial companies, retail — our team has diverse experience, but we can't know everything, so we can't replace them or overstep. Managing it ourselves would definitely not be optimal.

"An Yong": Some buyout funds rely on spread arbitrage to make money.

Shan: If you acquire a company and leave it completely unchanged, how do you create value? Just from the buy-sell spread? There's no such free lunch in the market. In private equity, creating value means improving the company, improving operations, increasing value. Looking at PAG's completed projects, we calculated that 71% of value created in our buyouts came from restructuring or improving company operations. About 20%-plus came from control premiums, because companies with control can sell at slightly higher multiples — cash flow or earnings multiples.

"An Yong": Looking back at buyout projects you've executed, what do they have in common?

Shan: The logic is connected. Like warfare — every campaign, whether Liaoshen, Pingjin, or Huaihai, the greatest commonality is what Mao Zedong said: "Better to break one finger than hurt ten; better to annihilate one division than rout ten." Every investment differs, but the analytical approach is consistent — that's how you ensure high investment quality.

"An Yong": What "value" did PAG add to Yingde Gases?

Shan: Cash flow grew 2.5x in four years. Previously the company focused mainly on direct supply; retail was neglected. The massive cash flow growth came from heavy investment in retail. Also, when we acquired it, Yingde had virtually no clean energy business; now it accounts for 25%.

Most Investment Opportunities Are Serendipitous

"An Yong": How do you evaluate PAG's gains and losses in Asian markets over the past decade?

Shan: By the numbers, we manage over $50 billion in capital across three businesses: real estate, private credit, and private equity. Over the past decade, all three have delivered returns above 20%.

"An Yong": Those are astonishing returns. What did you do right?

Shan: Over the past decade, we've looked at no fewer than 5,000 projects. About 150 entered due diligence. We seriously studied only several dozen — so about a 1% rate. Extremely selective. Many projects fell through on valuation. We're very cautious.

"An Yong": Because of your prudence, your risk aversion.

Shan: I'd say we never gamble. The first priority of investing is ensuring you don't lose money; how much you can make is another matter.

Our typical judgment is: over three to five years, how much value can this project create for our investors? If the math doesn't work, we simply can't accept it. If it does, we can even bid above what others expect.

Venture capital invests in 10 projects at $1 million or $10 million each; nine can fail as long as one hits big. We do acquisitions — minimum several hundred million dollars per project — so we can't afford a single loss.

"An Yong": You also invested in Nayuki.

Shan: First, such growth investments represent a very small portion of what we do, including our controlled %Arabica. For any project, our first judgment is whether it has uniqueness. What's unique about these two companies is their brand and product characteristics. %Arabica's products are far more refined than Starbucks — including details like when coffee beans are roasted, and how long after roasting they can no longer be used. Much higher standards for taste and quality.

"An Yong": Most late-stage funds tend to invest in clear category champions, yet neither Nayuki nor %Arabica obviously are.

Shan: Often, investment opportunities are serendipitous. China's coffee market is enormous and highly competitive. Every company will have its own network; it may not be as large as the leader, but the market can accommodate companies with brands and distinctive products.

"An Yong": What about Tencent Music?

Shan: When we first invested, it was called Ocean Music. Ocean Music's main asset was music copyrights; combined, its copyrights accounted for over half the Chinese market.

Before we invested, music copyright protection in China was inadequate. We invested because the state was beginning to emphasize copyright protection. We owned roughly 50% of Ocean Music. After acquisition, the first thing we did was merge the Kuwo and Kugou music platforms with Ocean Music, making it China's largest music platform company. Later it merged with QQ Music and was renamed Tencent Music, at which point we became minority shareholders. We exited near the market peak.

"An Yong": How do you view the relative merits of growth versus buyout investing?

Shan: For the past decade in the West, especially the U.S., there's been constant debate over growth versus value investing. Value investing represented by Buffett seemed to be at a disadvantage, making many question so-called value investing. But recently, many hedge funds have plunged, and investor sentiment has shifted back toward Buffett.

"An Yong": Is this also because markets have entered a downturn?

Shan: Investing depends heavily on macro environment, partly on your own judgment and selection ability — actually, luck is also a key factor in investment success. Why was growth investing so hot for the past decade? One very simple reason: the Fed was printing money.

So-called quantitative easing was flooding the market with money like a deluge. Where did all that money go? That's why growth investing became so popular.

"An Yong": But the flood has stopped.

Shan: The market environment has changed dramatically. U.S. inflation has hit 8.6%, the highest in 40 years. So whether the Fed or other Western central banks, they need to raise rates and tighten money supply. Liquidity has shrunk. Companies or businesses without visible cash flows in the near term will take heavy hits. This explains why many growth funds have suddenly fallen to earth.

Always Be Prepared

"An Yong": At PAG, what team culture do you cultivate to ensure your valued principles are passed on?

Shan: An owner mentality. Everyone should have the mindset of being a boss. If you were investing your own money, you'd be extremely careful. When investing others' money, risk aversion might be relatively weaker. So in every PAG investment, our employees have skin in the game — we're not just managing others' money, we're participating ourselves. Whether in participation or decision-making, our people have an ownership mindset.

"An Yong": How do you measure owner mentality?

Shan: We do annual reviews, 360-degree performance evaluations: colleagues above, below, and beside you score you. Whether you have an owner mentality — those around you know perfectly well. The masses have sharp eyes.

"An Yong": Who has influenced your understanding of investing and dealmaking most?

Shan: Without question, TPG founder David Bonderman. He's brilliantly intelligent, decisive, and resourceful.

There was one project we'd negotiated for a long time with extremely complex deal structure. Even colleagues who participated in the negotiations needed considerable time to understand the thinking and care behind it. But when I explained this structure to Bonderman by phone, he simply said: "That works." That call probably totaled under three minutes. A deal worth over $2 billion was finalized in three minutes.

"An Yong": Many believe TPG's distinction lies in its unique team culture and distinctive investment culture. What makes it unique?

Shan: TPG's most unique feature was having Bonderman. Bonderman is extremely humorous — only someone whose mind works incredibly fast can be that humorous.

In 2009, I became a senior partner at TPG. Months later, I told him I'd promoted myself: no title on my business card now. Because I thought printing a title was somewhat pretentious. He replied, "I'm still one up on you — I don't use business cards at all."

"An Yong": Then why did you decide to leave TPG and found PAG?

Shan: After Newbridge merged into TPG, I didn't adapt well to its internal decision-making mechanisms, so I left.

"An Yong": What's your secret for moving freely between different cultures and being fully accepted?

Shan: Understand others' cultures. When I first went to Korea, I knew neither the language nor the culture, so I read extensively. Once you understand the history, communicating with locals becomes much easier.

"An Yong": What principles do you apply when facing disagreements?

Shan: All cultures have commonalities. If you understand others, you can naturally control such disagreements. Without putting yourself in others' shoes, without reading their psychology, conflict comes easily. I'm not saying I do this very well — the book describes how initially, I and the Korean side lacked mutual understanding and trust, but later we built a trust mechanism.

"An Yong": By worldly standards, you'd be considered successful. What opportunities do you feel you've missed?

Shan: Everyone's standards differ. I don't feel successful; sometimes I feel quite the failure.

"An Yong": Where have you failed?

Shan: Some think earning however much money equals success. But I believe true success lies in contribution to society. By that measure, my contribution is utterly negligible, not even worth mentioning.

"An Yong": Besides Money Games, you previously published Out of the Gobi. Why did you want to write that book?

Shan: One important reason is that experience wasn't personal — it was generational. I came out of the Gobi, then went abroad, experienced reform and opening. Without reform and opening, I wouldn't have had the chance to go abroad, nor would China have had its later great development.

"An Yong": What's been the Gobi Desert's greatest influence on your later life?

Shan: My best friends are all from the Gobi. We shared everything, depended on each other for survival — friendships forged in such circumstances last a lifetime. In Out of the Gobi I wrote about a friend named Rongtian Li — "rong" as in honor, "tian" as in field. Something he said affected me my whole life: "Wasting time is a crime against yourself."

"An Yong": Is this constant tension an imprint of your era? During your Gobi years, while others played cards and relaxed, you were buried in books.

Shan: For your generation, many opportunities are probably obtainable. For ours, they were unobtainable — you could only wait. Persisting in reading in the Gobi was actually quite bitter. Working over ten hours daily, utterly exhausted afterward. In the depths of winter, in a toolshed, holding a small oil lamp, secretly reading — that took some willpower. But books let you see different worlds; that was the joy.

"An Yong": Did you ever prepare for the worst possibility — that you might never get a chance?

Shan: My thinking then was: if I never got any opportunity in this life, if I rooted myself in the frontier, there was nothing to regret — many people throughout history were born at the wrong time. But if an opportunity came and I wasn't prepared, I could only blame myself. So you need to always be prepared.

Image source: Visual China

Layout: Yunxiao Guo

Book Giveaway

Money Games

By Weijian Shan

Citic Press Corporation, May 2022. Price: 98 RMB

We welcome enthusiastic comments from readers. We will give one copy of Mr. Shan's new book Money Games to each of the three commenters with the most likes. Deadline: 20:00, June 25, 2022.