A group of people everyone wants to know

They're scattered, hidden, yet everywhere all at once.

Produced by | 36Kr Venture Capital Research Institute

Research | Zhuxi Huang, Yunxiao Guo, Yi Zhang Edited by | Jing Liu

Industrial investment has stepped into the spotlight.

This is the reflection of China's industrial restructuring: even as the internet sector slows and international political and economic conditions grow more complex and severe, China continues to push forward with manufacturing upgrades, energy transition, and technological breakthroughs.

Compared with financial investment, industrial investment is far more intricate. Investors need deep understanding of specific industries to identify suitable opportunities along lengthy industrial chains. And because of how tightly interwoven each link of these chains is, post-investment synergy, empowerment, and collaboration carry weight equal to — or even greater than — capital itself.

Over the past year, Undercurrents has observed and discussed industrial investment extensively, arriving at some clear consensus: everyone in the primary market will inevitably have to push deeper into industry; industrial investment can be executed by any entity so long as resources are transferred and utilized efficiently; the shift of investment mainstream from pure financial purpose toward industrial purpose is a far more important development trajectory than changes in currency denomination; emerging enterprises attach themselves to "systems" built by chain leaders, coexisting and developing through continuous negotiation. We have tried to define more precisely what industrial investment actually is. What is clear is that the traditional cycle of fundraising, investing, managing, and exiting has undergone fundamental change: taking money with explicit non-financial objectives, investing into specific industrial segments, maneuvering various resources among multiple parties, and ultimately measuring returns through lenses that go far beyond "exit."

A month and a half ago, we compiled The Complete Map of Industrial Investment through desktop research, sketching the contours of the industrial investment landscape. Following that, we launched a nationwide "China Industrial Investment Fund" survey, widely soliciting participation from funds meeting our definition of "industrial investment" — that is, "industrial investors established with capital from national or local governments, enterprises, financial institutions (insurance, pension funds), family offices, and others, who focus long-term on one or several closely related specific industrial sectors, and who support and promote the development of particular industries through upstream and downstream investment布局 along industrial chains."

This survey of industrial investors has also confirmed something we observed: the boundary between financial investment and industrial investment is being broken from both directions.

Financial institutions continue to put down deeper roots in industry. Building on quality portfolio companies, they constantly extend and explore upstream and downstream along industrial chains, ultimately establishing their own "investment clusters" in specific domains — achieving the end goals of embedding themselves in industry, building moats, and empowering industrial development. Examples include: Challenger Venture in the consumer sector; Yuanhe Puhua and Fengyuan Capital in chips and semiconductors; Longpan Investment in healthcare; and Fenghe Capital in new energy.

Meanwhile, corporate venture capital (CVC) born from enterprises no longer limits itself to closed ecosystem strategic orientation, nor pursues financial returns completely detached from core business. What deserves attention is that some CVCs have identified their differentiated ecological niches within industry, moving toward an intermediate state where investment and industry mutually reinforce each other.

For example: Inovance Capital's portfolio spans major tracks including industrial software, energy, advanced manufacturing, materials, semiconductors, and automotive electronics. Of the more than 50 projects it has invested in to date, many have direct or indirect business connections with Inovance Technology. In fact, a substantial portion of these projects were "underwater companies" discovered through the parent company's business operations. In the process of supporting and empowering them, Inovance itself has gained returns far exceeding the financial dimension.

Industrial investors from different backgrounds are now leaning on their unique advantages in "industrial policy," "chain leader status," and "cognitive moats" — identifying and nurturing promising innovative enterprises within industry while promoting healthy industrial chain expansion. Ultimately, this strengthens their own and their LPs' industry position and voice.

Returning to first principles: How should we define a good industrial investment? And how should we evaluate an industrial investment fund's influence?

As industry observers repeatedly note, the most distinctive characteristic of industrial investment is the subordination of financial purpose. Past mainstream evaluation standards in the primary market have revolved almost entirely around financial returns. Differentiating from this, the central challenge in establishing an industrial investment evaluation system lies in finding a scientific mechanism to measure what kind of returns have actually been achieved — for investments of different scales, types, and objectives.

Therefore, building upon the quantification of typical financial data indicators — (1) assets under management; (2) investment reach (geographic and sectoral scope); (3) investment activity (number and amount of projects); (4) investment outcomes (number of star projects, number of IPOs) — we systematically examined industrial investment funds' management team and LP industrial backgrounds, investment strategy and portfolio concentration, and industrial empowerment systems and case studies.

We established "industrial returns" as a judgment criterion parallel to "financial returns," with independent and separate consideration for different types of institutions. For example: for local government guidance funds, local economic contribution (jobs created, GDP added, number of "chain-completing" projects, etc.); for large enterprise CVCs, parent company business relevance (number of projects integrated into parent company supply chain, parent company profit margin improvement, etc.).

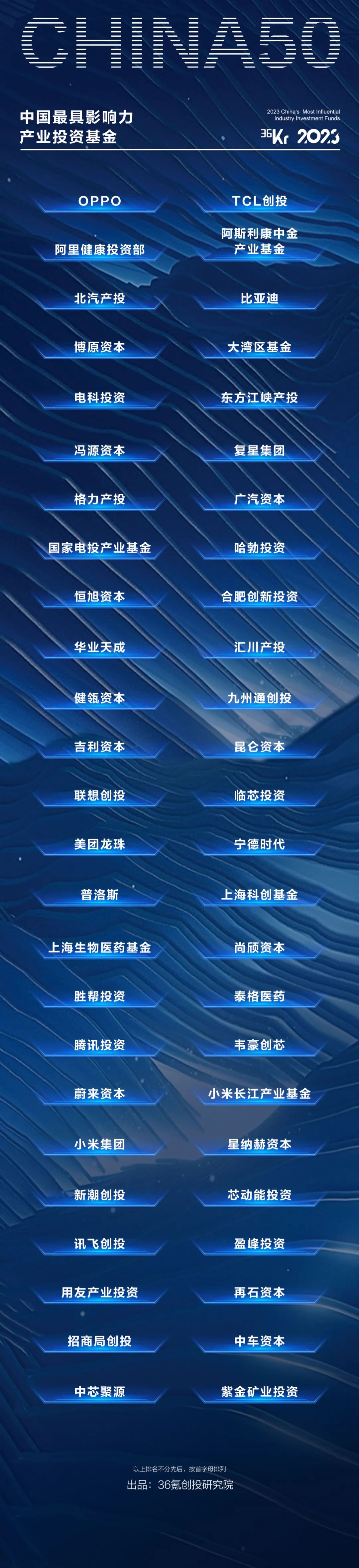

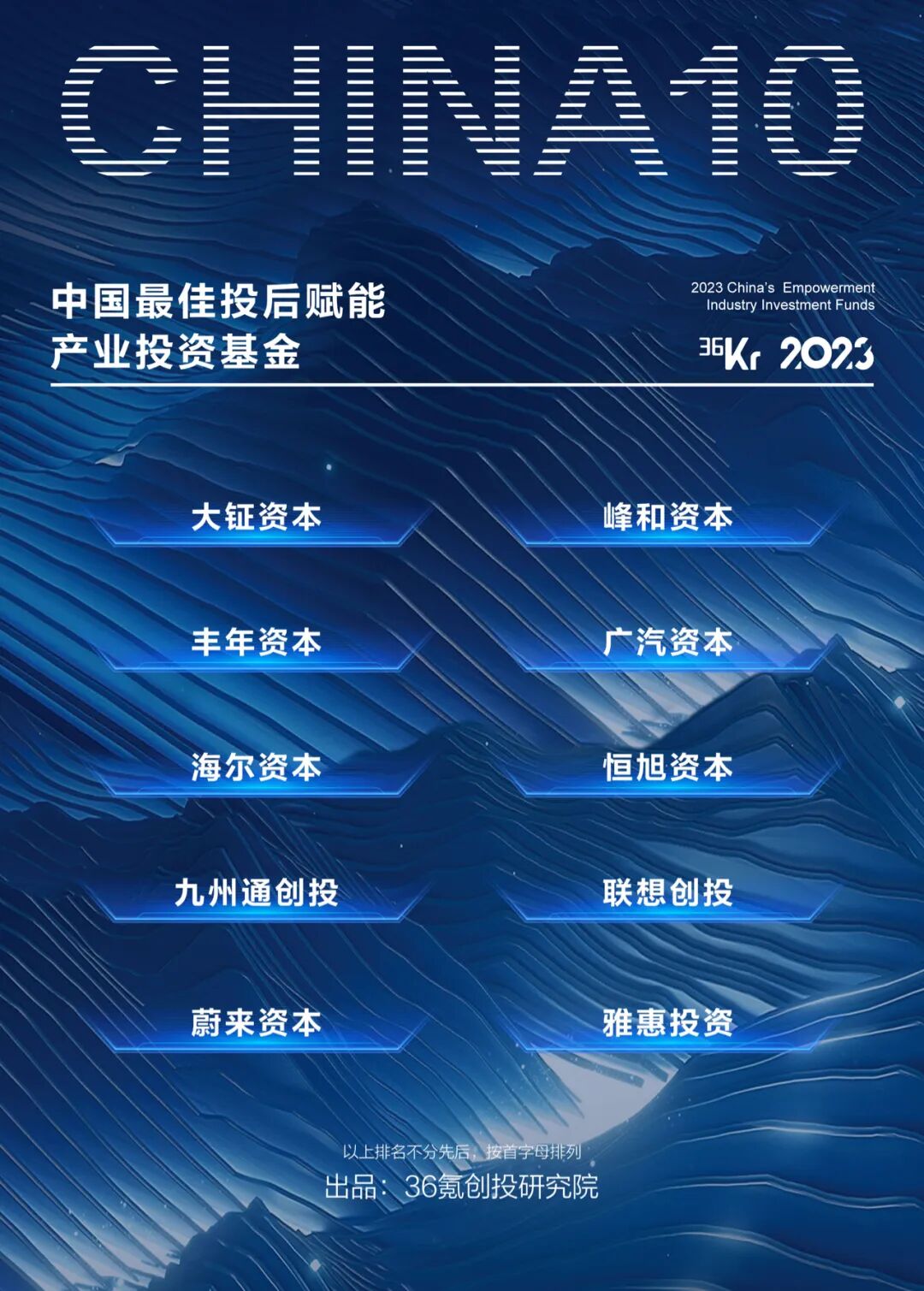

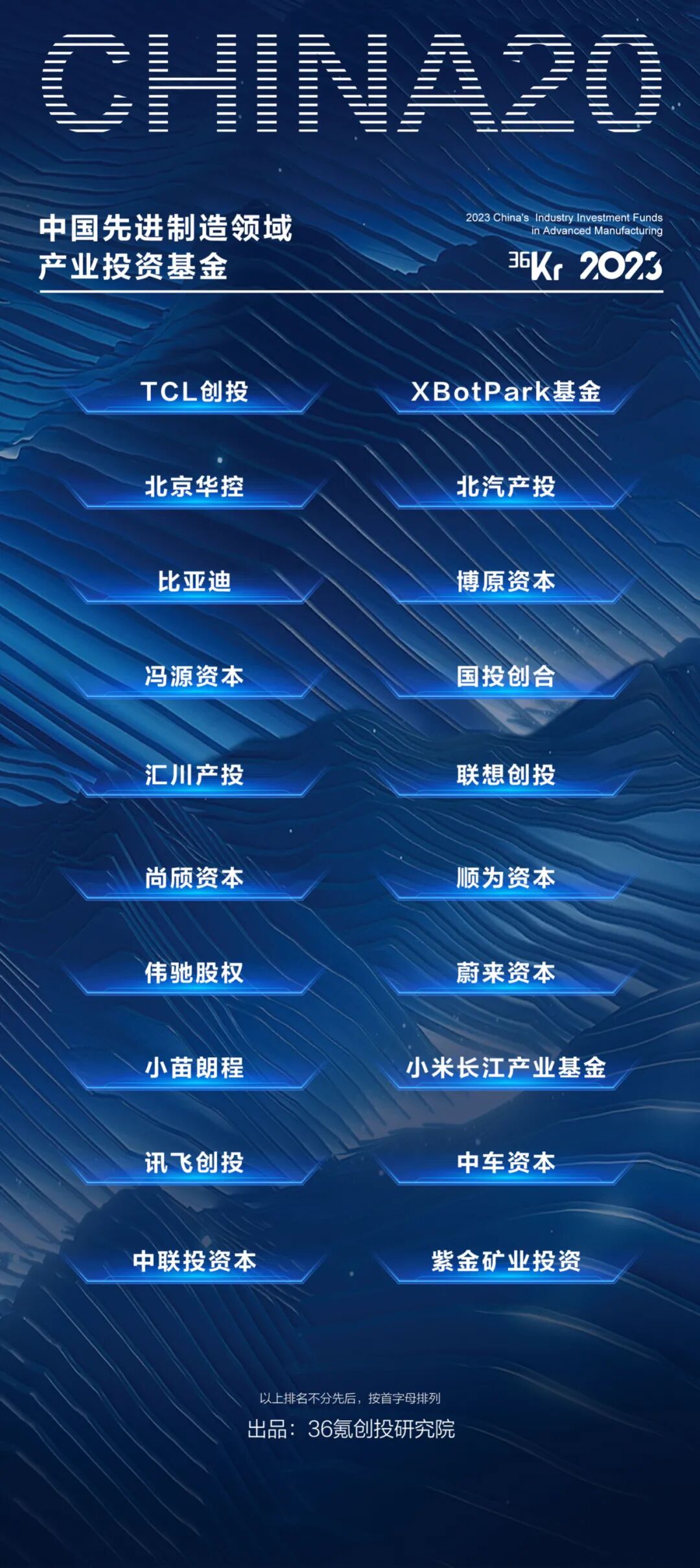

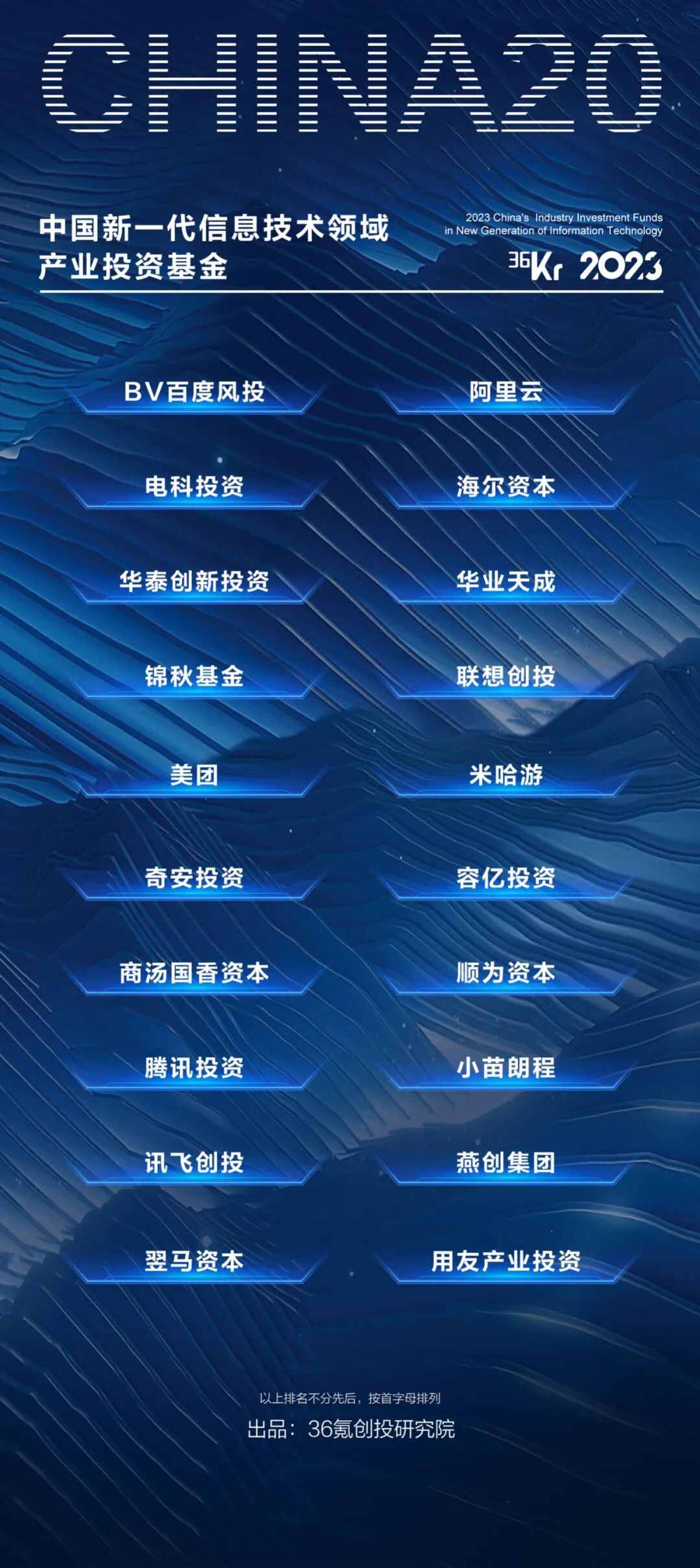

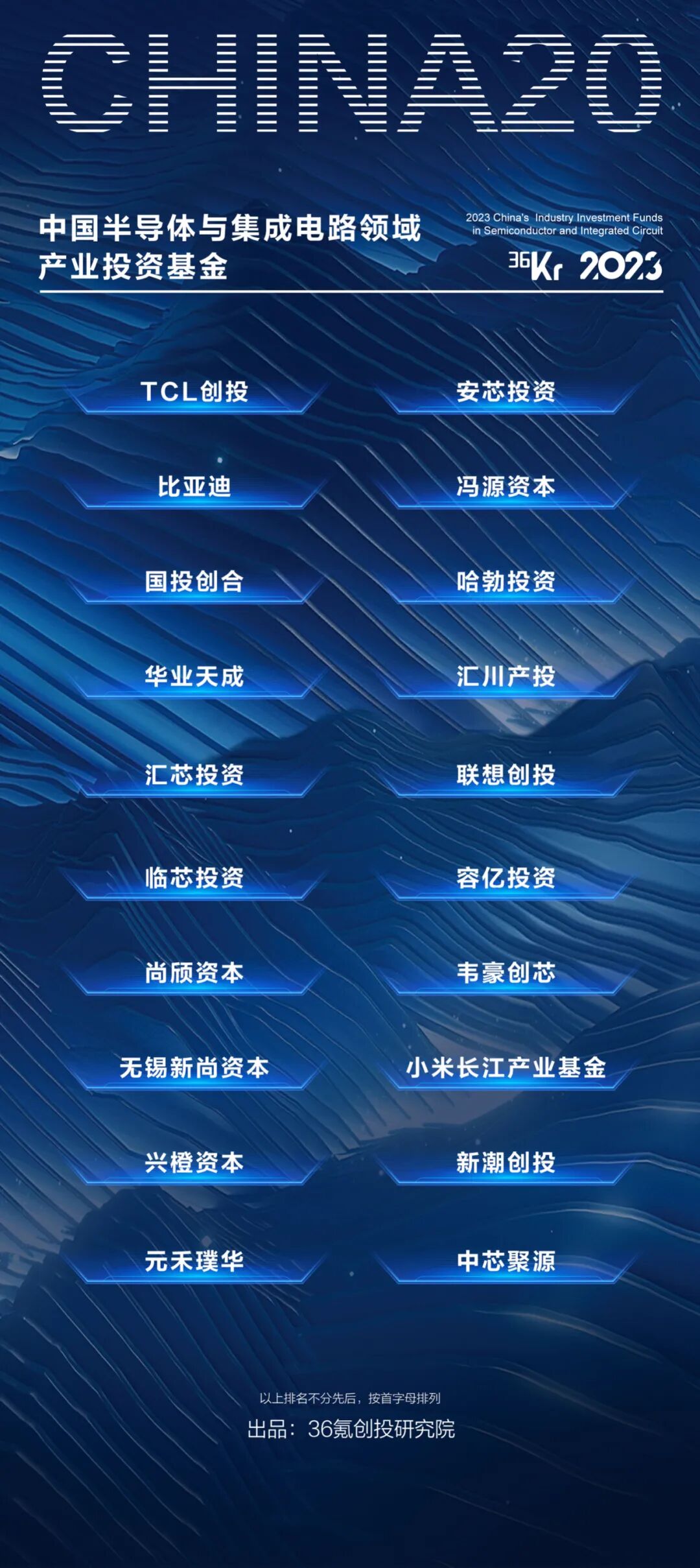

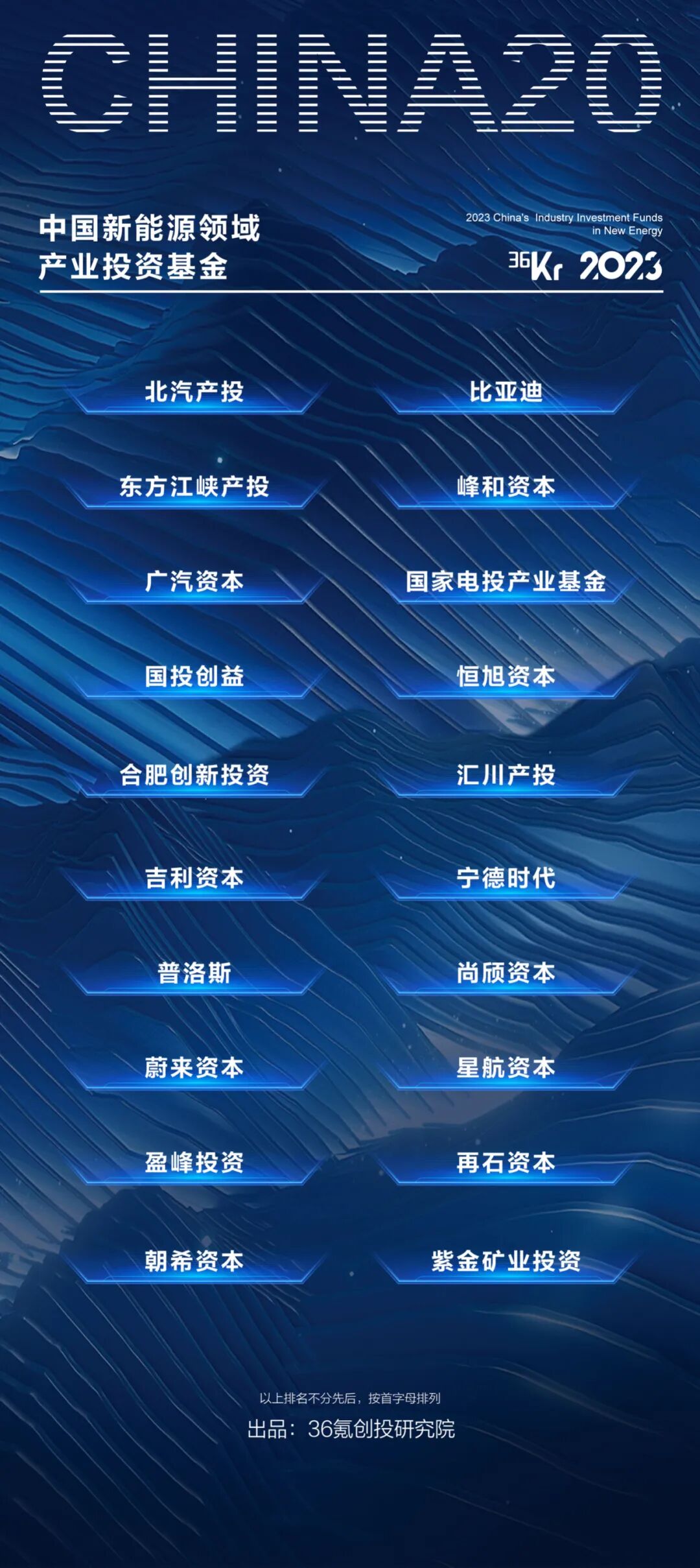

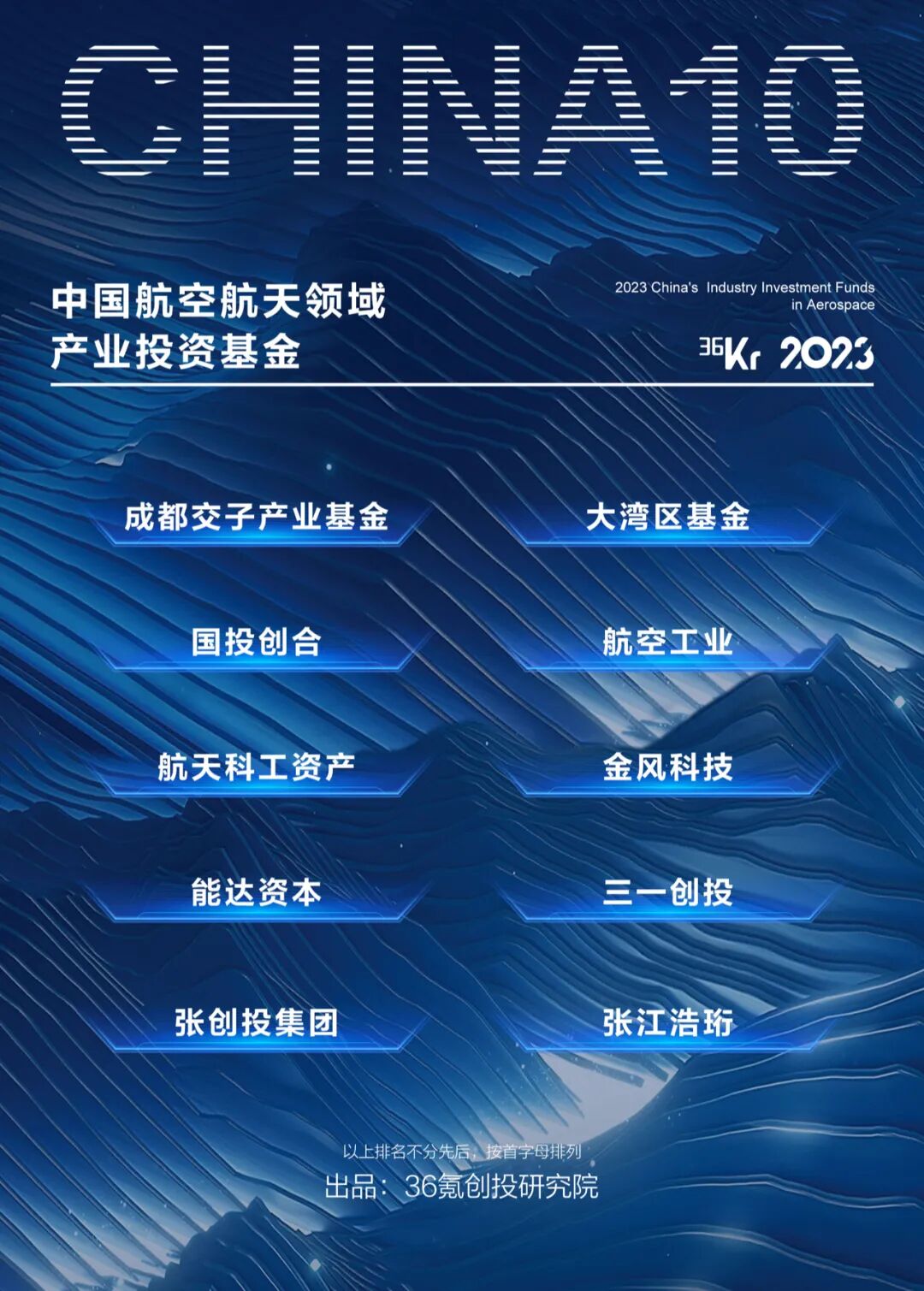

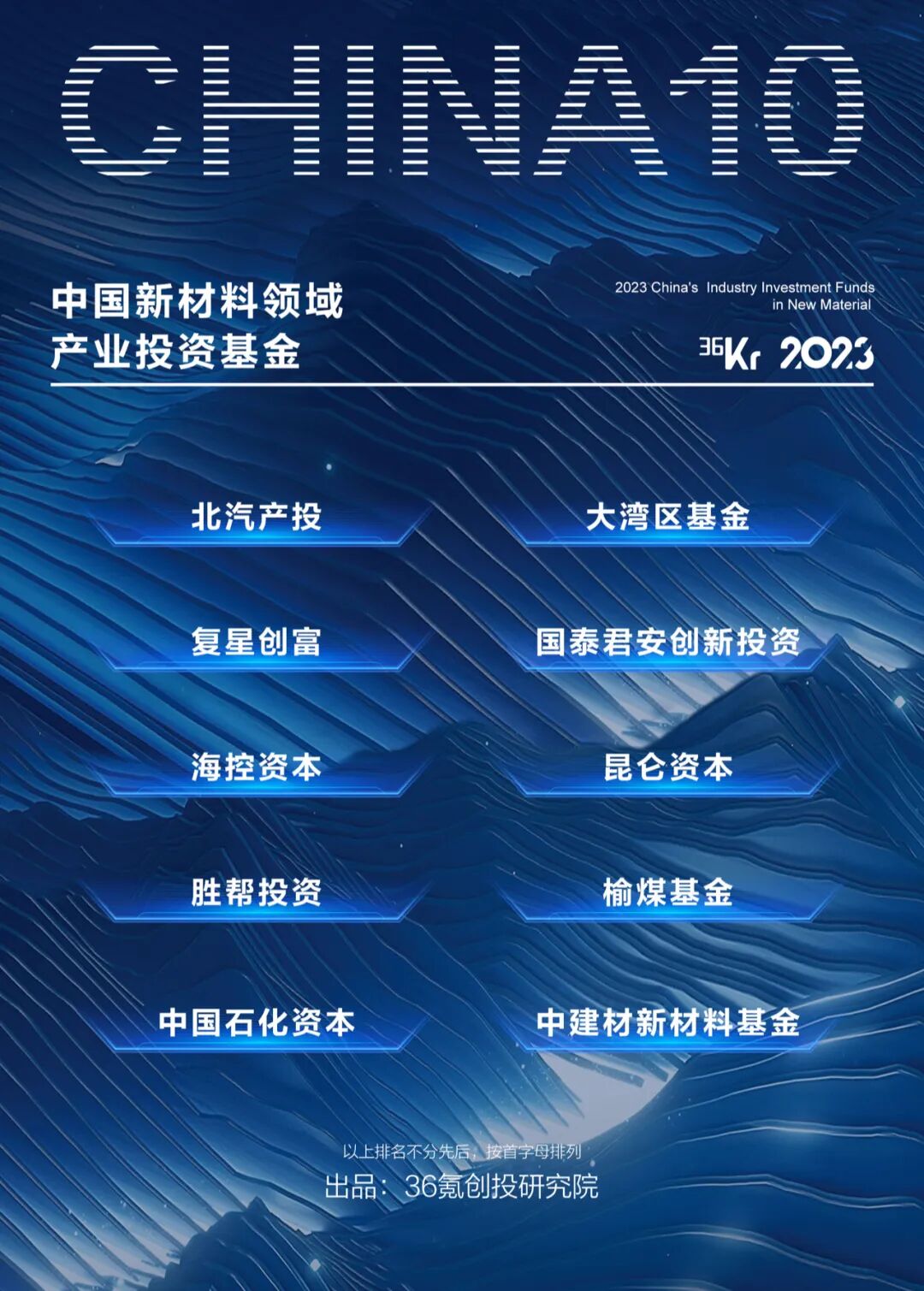

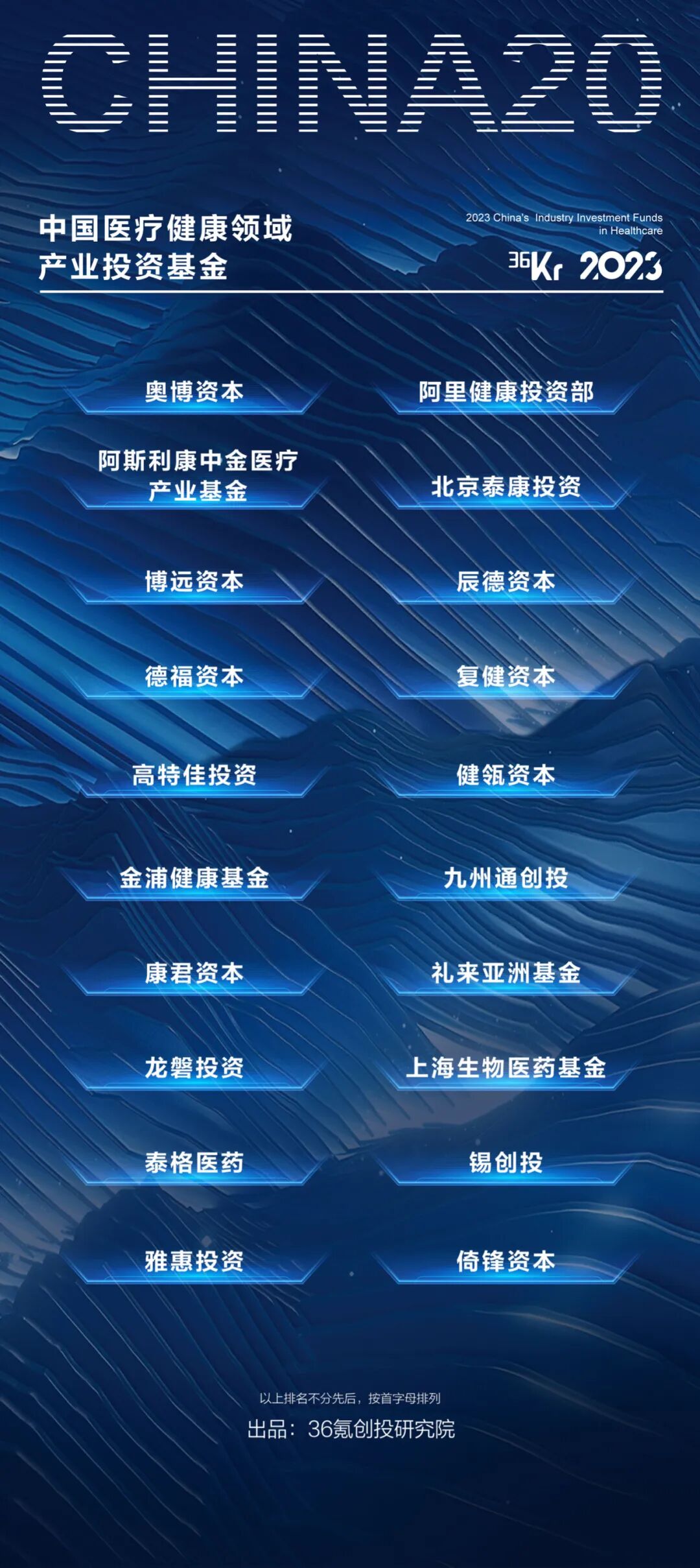

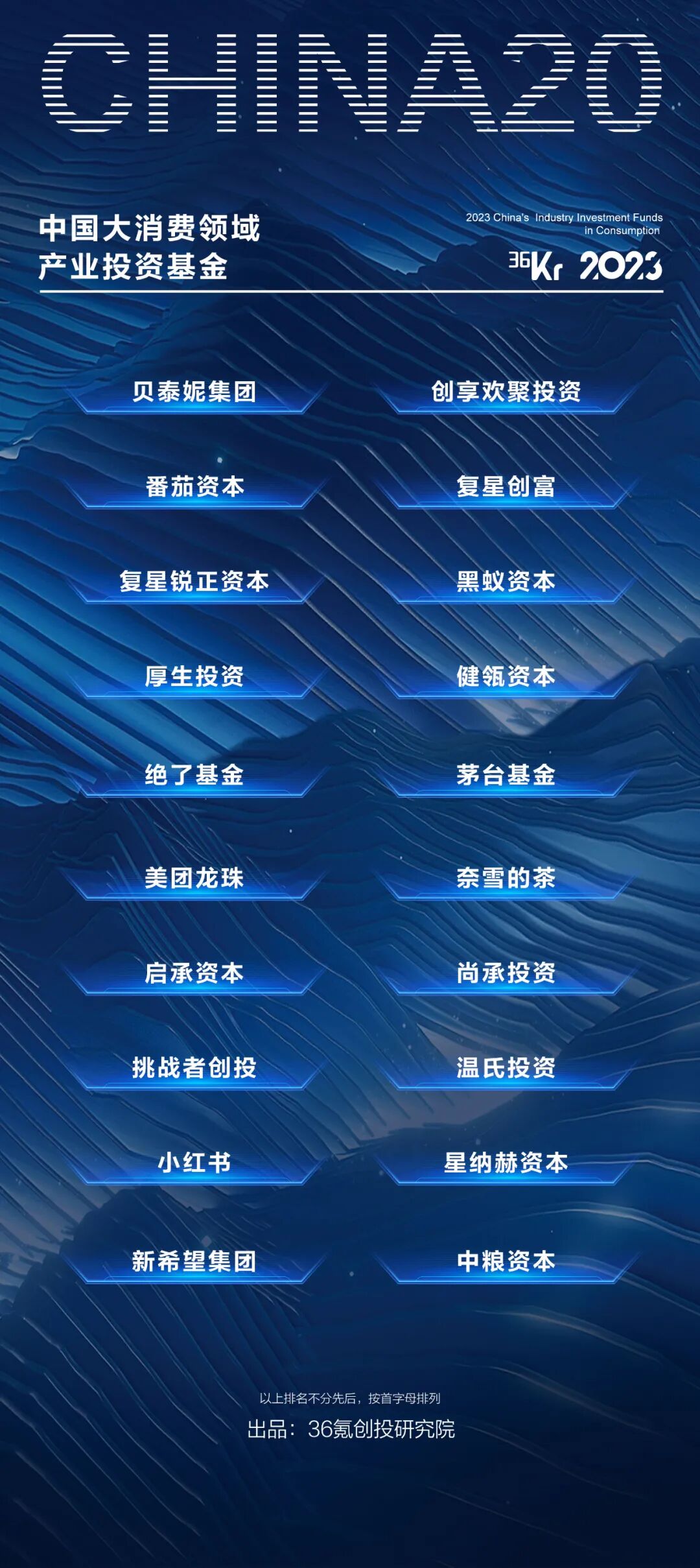

Ultimately, we identified 50 influential industrial investment funds in the market, 10 industrial empowerment funds, and quality industrial investors across eight sectors: advanced manufacturing, next-generation information technology, semiconductors and integrated circuits, new energy, aerospace, new materials, healthcare, and consumer.

The full list:

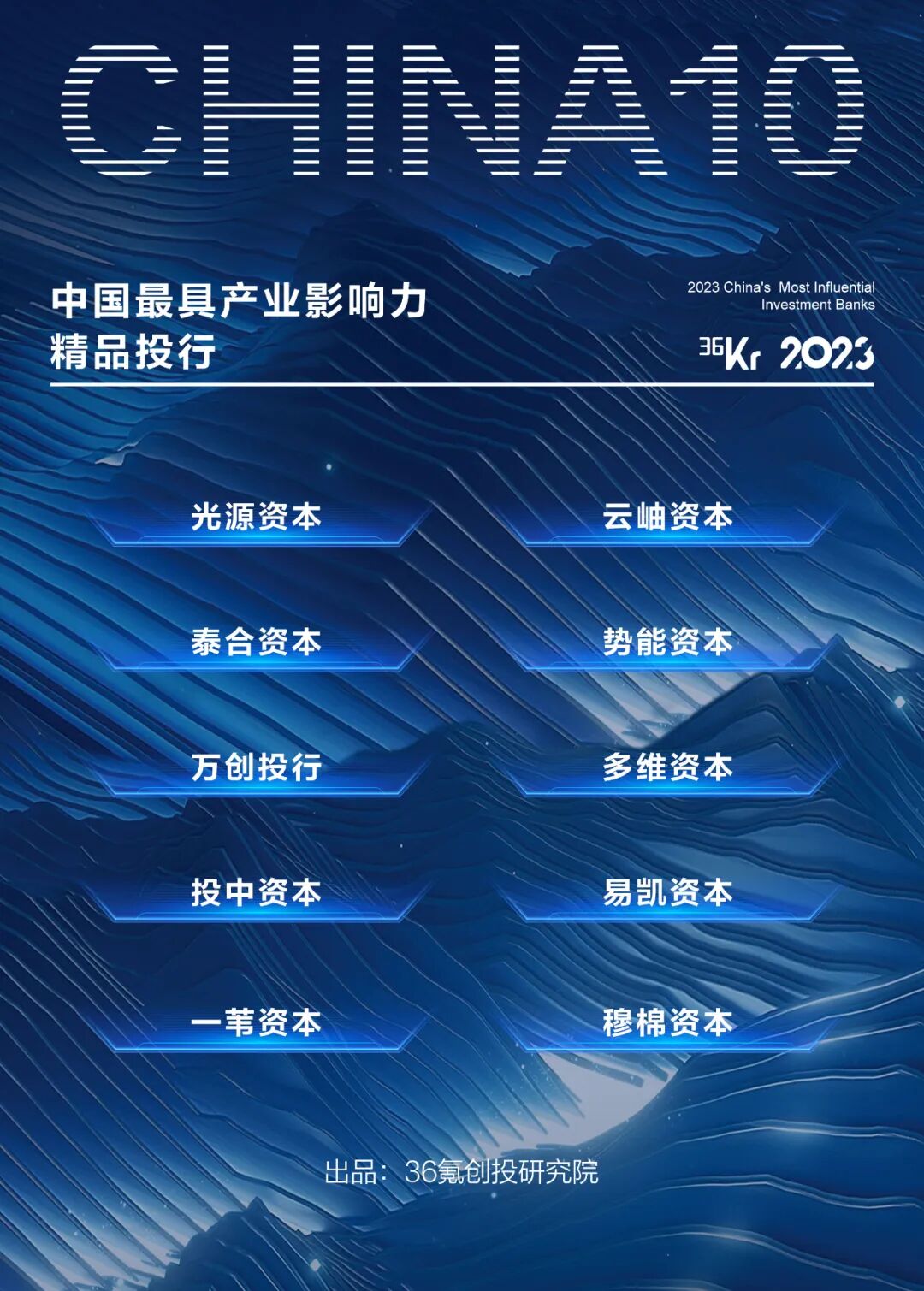

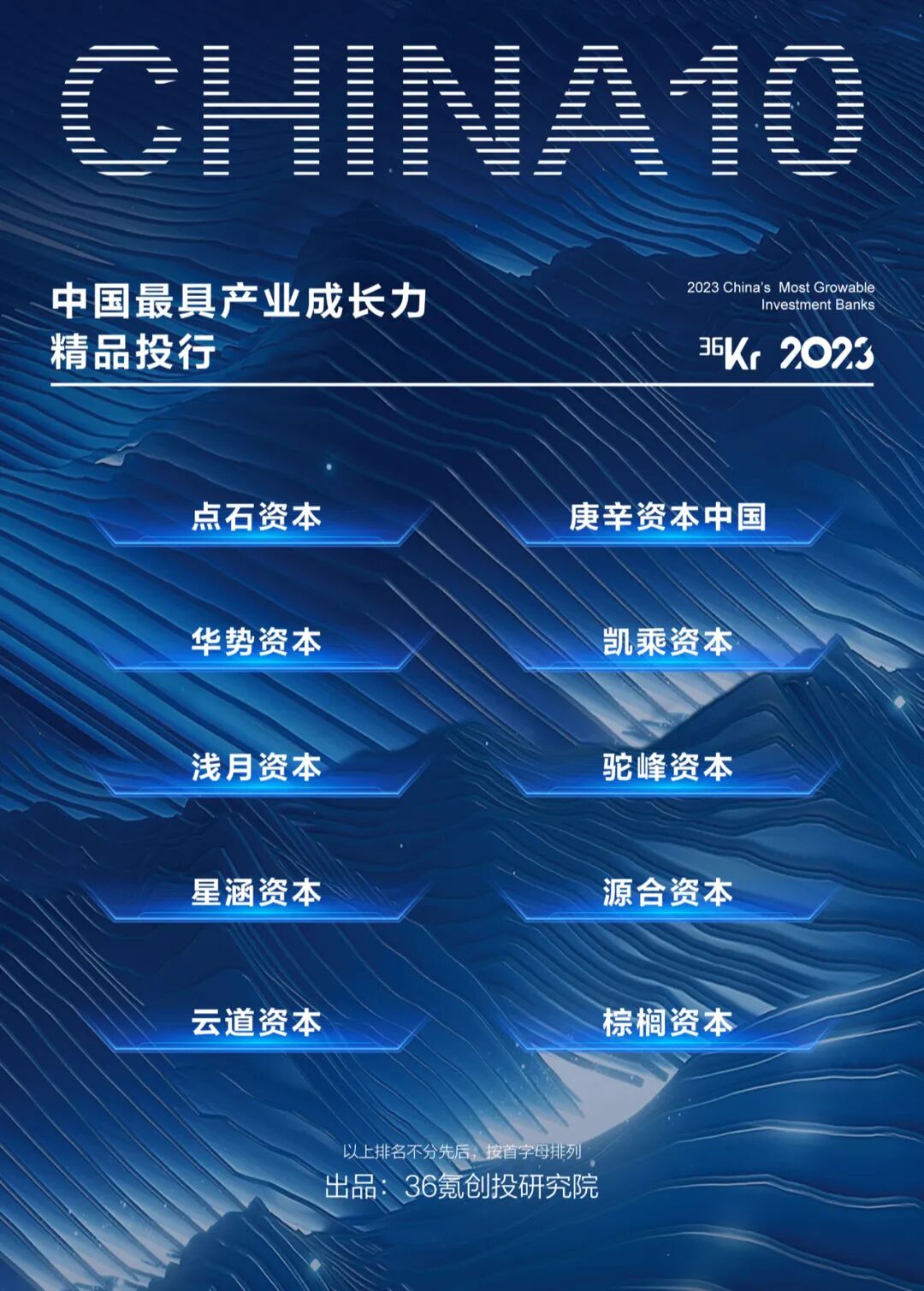

At the same time, we also identified boutique investment banks working across various industrial domains, constantly pushing deeper to the foundational layers of industry.

The full list:

Image source | Visual China

Layout | Meng Du