A VC Lesson from Tian Xuan

Thirty years, a journey of departures and returns.

Last week, An Yong Waves published Wang Ran of E-Capital's "Reawakening China's Primary Market," which sparked widespread discussion. Fang Xinghai, Vice Chairman of the China Securities Regulatory Commission, stated at the 2024 Lujiazui Forum that PE/VC funds invested in 4,438 projects in Q1 2024, with total capital of 191.5 billion yuan — slower than before, but these are just Q1 numbers. If we look at the full year, investment volume will likely approach 800 billion to 1 trillion yuan. "At that scale, it's a bit of an exaggeration to say the primary market no longer exists." Either way, China's primary market is indeed in a period of rapid adjustment.

On the topic of Chinese venture capital, Tian Xuan is among the most qualified voices. As Dean of Tsinghua University's National Institute of Financial Research, Vice Dean of Tsinghua University's PBC School of Finance, and Chair Professor of Finance, Professor Tian offers a cooler-headed perspective on the VC industry than practitioners themselves. At WAVES 2024, he delivered a speech titled "The Past, Present, and Future of Chinese Venture Capital," reviewing thirty years of Chinese VC history and analyzing industry evolution and current challenges.

Full text of the speech below:

Good morning everyone! I'm delighted to be here. This seems to be a young people's event. Just now I was asked to give some advice to young people, and I was slightly taken aback. In universities, I give students plenty of advice — we're always indulging ourselves in that. But I rarely give advice to young people, because I've always seen myself as young. That changed when I saw my slides. My PPT used Tsinghua University's template — the first page shows the university's century-old auditorium with the great lawn in front, very serene. Then the 36Kr team said we needed to use their template. After applying it, I found the colors very vibrant — it refreshed my understanding of "young."

Today I'll discuss "The Past, Present, and Future of Chinese Venture Capital" in four parts. First, a brief review of Chinese VC history. Second, fundraising, investment, and exit trends. Third, alternative forms of venture capital. Fourth, challenges, opportunities, and outlook for the VC industry. I hope to present the whole picture and big picture using a large sample. Every investor has vivid cases and investment experiences, but many are relatively partial. What we scholars do is collect data, hoping for a bird's-eye, macro-level view of Chinese VC — where should it go next?

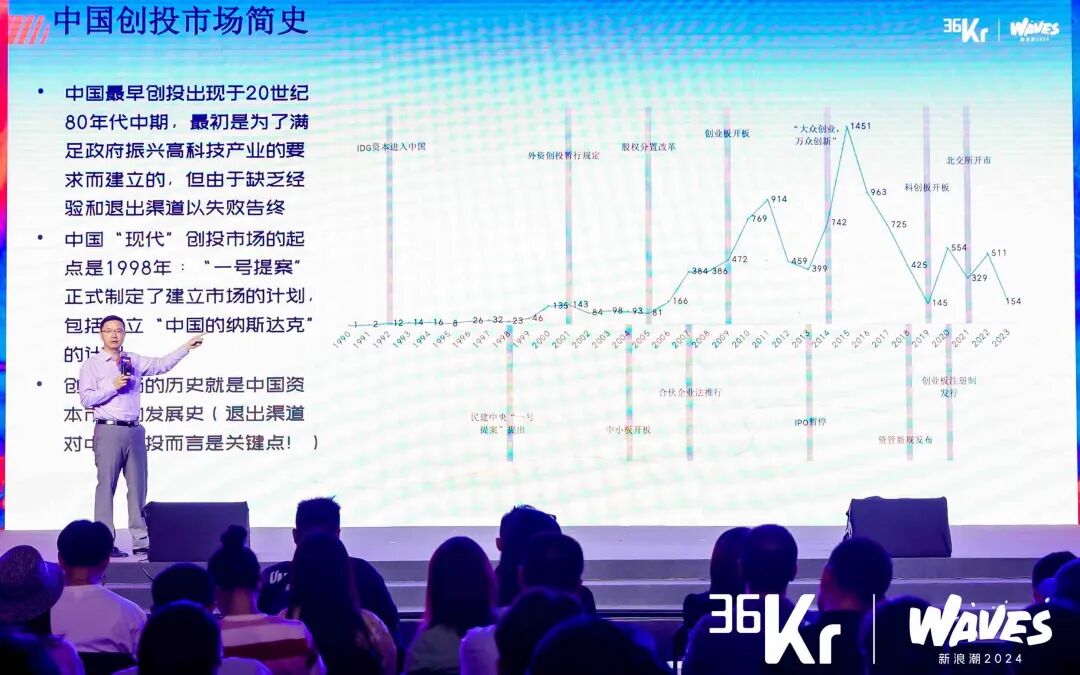

Chinese Venture Capital's Deep Ties to Macro Policy

To know where to go next, we must first understand Chinese VC's "past." I start from the 1990s — IDG entered China in 1993, thirty-one years ago. Looking further back, in the mid-1980s, it's hard to imagine: China's market economy system hadn't truly formed, reform and opening had only just begun. Yet there were already VC prototypes, called China Venture Capital. But it failed — because China had no capital market at the time. No one was willing to hold their arms raised forever like the Statue of Liberty with no exit possible. Without an exit market, China Venture Capital failed.

Looking at China's journey, this is our new venture capital deal count. We can see that every change in Chinese VC has been influenced by important macro policies. For example, in 1998, the China Democratic National Construction Association's Proposal No. 1 at the First Session of the Ninth CPPCC National Committee marked the true beginning of Chinese venture capital.

We later experienced the 2004 launch of the SME board, and the 2005 split-share structure reform, both critically important to China's secondary market. The 2009 launch of the ChiNext board truly brought spring to Chinese private equity. Our exit channels were finally opening, with the goal of creating China's Nasdaq.

Later came mass entrepreneurship and innovation, and we saw exponential growth in venture capital. Then the asset management新规 brought difficulties for Chinese VC, as much bank capital could no longer enter the venture capital industry. Recently we've seen a fairly obvious downward trend, despite the launch of the Beijing Stock Exchange and the pilot and full rollout of the registration-based IPO system. But looking at the overall venture capital wave, we're now in a downward phase — that's our brief history.

The Absolute Dominance of RMB Funds

To understand China, we must also understand the global context. Over the past eight years, global venture capital trends basically peaked locally in 2021. The background was the 2020 COVID-19 pandemic, when US capital markets suffered massive shock — the US stock market triggered circuit breakers four times in two weeks. Buffett said we were witnessing history, because he had only witnessed five market circuit breakers in US history, and we saw four in two weeks. The US began unlimited quantitative easing, printing money, and massive capital flooded into the primary market. We saw rapid growth in global venture capital markets in 2021. In 2022, the broader environment trended downward, and globally we can see China followed the same pattern — our 2021 Chinese venture capital had a small peak, though still operating in a relatively low range.

Last year's Chinese venture capital market situation, by investment amount: 8,322 new funds were established, down 4.7%. Overall, many investors I interact with are our students — Tsinghua PBC's MBA and EMBA students — and we communicate frequently. The general feeling is still not very optimistic; lack of fundraising progress has become a fairly common phenomenon.

In Q1 this year, new fund launches continued to decline — only about 1,390, down 38% quarter-over-quarter and 34% year-over-year. That's our current macro trend. From a fundraising perspective, blue represents RMB funds, red foreign-currency funds, through 2006. If we push back from 1998, we can roughly divide into two periods.

Before 2009, Chinese venture capital was dominated by USD funds. At that time, China didn't have clear exit mechanisms; domestic investment was "two ends abroad" — overseas fundraising in RMB fund form invested into domestic targets, then exited through overseas IPOs.

In 2009, with the establishment of ChiNext, China's domestic venture capital exit market opened significantly, so we saw RMB funds rise rapidly. RMB now has absolute dominance, coinciding with foreign capital retreating, and many USD funds facing US restrictions on investing in Chinese industries. Some industries truly can't receive investment, so we do see from a fundraising perspective that RMB funds have absolute dominance.

Patient Capital Is Rare; Exits "Much Ado About Nothing"

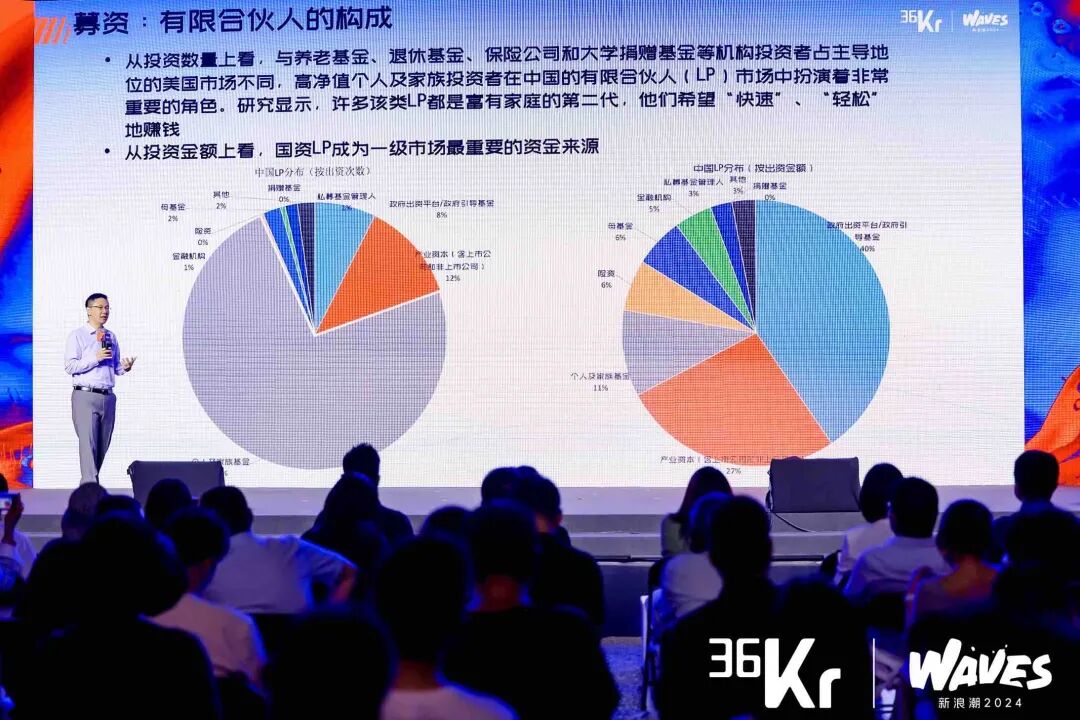

Venture capital funding sources are limited partners or LPs. Looking at domestic LP composition, we find it differs from the US. By number of investments, we can see that about 75% are wealthy families and individuals.

The biggest problem with wealthy families and individuals is shorter investment horizons. Unlike US LPs where 98% are institutional investors and only 2% are individual investors, in China by investment count, most are individual investors. For a family to invest a "small target" [100 million yuan] into a fund locked for 10-12 years — that's immense pressure. Domestically, people prefer quick money, easy and fast returns. Investing for 10-12 years is too much pressure. China's market changes very rapidly; in ten to twelve years, things change beyond recognition.

By investment amount, government guidance funds, local investment platforms, and various central and state-owned enterprises now dominate. Essentially, state money should be the most patient capital. But because domestic investment focuses more on investment attraction, local employment and tax revenue, and economic GDP.

These government officials mainly consider their own performance records, then possible promotion — their time horizon is three to five years. It's very difficult to achieve patient capital, very difficult to truly invest early, invest small, invest in hard technology — this is the difference between Chinese and US venture capital. Our fund style is 5+2, 3+2, but the US is 10+2. They can invest earlier, smaller, truly accompany companies as they slowly grow, allowing them to continuously explore and trial-and-error — that's true patient capital. That's the China-US difference.

I used four countries/regions: the US, China, Israel, and Europe. Red represents China — the typical holding period before portfolio company IPO is 3-4 years, investing in relatively early-stage projects. The US is seven to eight years, because these are 10+2 duration institutions.

From an investment stage perspective, domestically we indeed invest more in mid-to-late-stage projects. There used to be the Pre-IPO model — the "final kick" investing in very mature companies with stable cash flow and clear business models, then earning the primary-secondary market spread. Buying at net asset value, packaging for IPO, selling at 30x PE. We now invest slightly earlier, but observed data shows projects are still basically mid-to-late stage.

US investment over this decade has been relatively stable: IT, healthcare, pharmaceuticals, and biotech projects. China chases trends faster — IT has always led, with e-commerce and mobile internet heavily invested in 2014-2019. Data, medicine, automobiles, and other hard tech industries have become current hotspots.

For exits, US M&A plays a very important role. While IPO is also an important successful exit channel, M&A became decisive after the 2001 Sarbanes-Oxley Act. Domestically, IPO has become by far the most important primary market exit channel, so we're relatively heavily affected by IPO policy. Starting last summer, the IPO path faced significant obstacles.

S-funds can provide more exit channels for VC funds. We've seen booming domestic S-fund development in recent years. Early this year, multiple S-funds were announced in Shanghai, Anhui, and Fujian. On the surface it appears very lively and prosperous, but actual trading activity hasn't matched the surface prosperity — there's a certain gap, mainly due to asset pricing disagreements. S-funds are relatively hot, but I summarize them as "much ado about nothing." Our funds still find it very difficult to exit through S-funds.

CVC: More Patient Capital Supporting Enterprise Innovation

What I just described is traditional venture capital — independent investment institutions raising capital from LPs into funds, managed by GPs, then invested project by project. I want to introduce a new venture capital organizational form: CVC.

CVC is also fundamentally a fund. On the asset side, it's the same as traditional methods — equity investment in projects one by one. But funding sources don't require raising from LPs. Funding comes from the parent company. The CVC I refer to is venture capital funds established by non-financial enterprises. Through this affiliated institution, they directly conduct early-stage venture investment — the name doesn't matter; some companies call it venture investment department, some strategic investment department, some industrial investment department. What they do is help invest in early-stage projects and help the parent company with layout.

In the US, Intel and Google are the two best CVCs, along with GE, Microsoft, Dell, Oracle all doing CVC. Domestically, BAT, Xiaomi, Huawei, and Lenovo also do CVC.

These days we no longer talk about "anti-capital无序扩张" [disorderly expansion of capital]. If you followed Chinese VC and entrepreneurship in previous years, there was a saying: if you were doing tech or internet entrepreneurship, when you reached a certain stage you had to "choose sides" — would you take Alibaba's investment or Tencent's? Looking back, Alibaba and Tencent were making these early strategic investments.

The difference between strategic investment and venture investment: what's the sole purpose of traditional venture capital? Some students are embarrassed to say it. Some say investment is to help entrepreneurs realize their dreams, or to improve social welfare, or poverty alleviation. I directly tell students: don't be embarrassed, don't be shy, say it out loud. The sole purpose of traditional venture capital is to make money — maximize financial returns, make money for LPs. Nothing to be embarrassed about.

But for corporate venture capital (CVC), the most important purpose is strategic layout for the parent company — that's strategic consideration. Financial return isn't the primary goal; it's more about upstream-downstream industrial chain layout, or entering new industries. CVC basically uses its own capital, has no exit pressure, very long duration — even longer than US funds — representing higher tolerance for failure. It's patient capital, so it supports portfolio company innovation.

Tencent and Alibaba are completely comparable to very strong traditional IVCs. They've invested in many unicorn companies, and compared to IVCs, Chinese CVCs invest more in earlier-stage projects. It's more strategic consideration, not just financial returns. No need to raise externally; they can get resources from the parent company. With Alibaba, Tencent, Xiaomi — seeing a project, they can provide continuous funding support, accompany its growth, let it continuously explore and trial-and-error. So they have high tolerance for failure — that's CVC's characteristic.

What they most like to invest in now: intelligent manufacturing, healthcare, and enterprise services. Leading cities: Guangdong, Shanghai, Jiangsu, Zhejiang, Beijing — that's the first tier. Top 5 domestic CVCs: Tencent, Alibaba, Ant, Xiaomi, Baidu.

CVC Is the Form That Can Truly Support Technology Innovation

Why do companies engage in CVC? It's more strategic consideration, less economic or financial return. They want to understand latest industry trends, get first-hand technology. Most importantly, they outsource their R&D to startups, because as we know, disruptive innovation, 0-to-1 innovation, is done by small companies, not large ones.

Because small company culture, flat architecture, sensitive information transmission, and innovative culture support 0-to-1 innovation. But as companies grow larger, they need vertical management, internal information transmission lags and distorts, and they no longer have innovative culture.

We see large companies doing CVC investment, even mixing these portfolio companies with their own R&D centers in combined teams, working together in R&D labs. This can serve as a "catfish effect" [stimulating competition]. Large company R&D staff are used to 9-to-5; the company next door is not just 996 but even 007. This catfish effect can effectively stimulate their own innovation, create synergies, and provide opportunities to acquire quality employees.

Comparing CVC-invested companies versus IVC-invested companies: horizontal axis is time, vertical axis is patents measuring portfolio company innovation level. Before receiving first-round CVC or IVC investment, portfolio companies' innovation levels are similar — one or two, two or three patents per year. But after receiving first-round CVC or IVC investment, in the following 1-5 years, both types show significant innovation improvement. Because they have money, because they received IVC or CVC investment, they can do R&D, so innovation improves significantly.

"Have money" is too vulgar — not language a scholar can use in top international journals. The academic term is: after receiving first-round investment, both types of companies' financial constraints are relaxed — basically, they have money. After financial constraints are relaxed, their innovation levels improve significantly. And the blue line, CVC-invested companies, is above the red, with steeper slope, faster growth rate. The logic behind this is that CVC investment doesn't aim solely at financial returns, but has more strategic considerations. This is true patient capital adapted to innovation's long cycles, uncertainty, and high failure rates. So CVC is truly a form that can support technology innovation.

Government guidance funds, also in the last three to four years since the pandemic, have rapidly risen to play very important roles. Their investments consider more things like investment attraction, local fiscal revenue, local taxes, employment, GDP logic. We now see the new national system, with the third phase of the Big Fund also established. We hope they can truly invest early, invest small, invest in hard technology, invest in industries meeting major national strategic needs, and support our technology innovation. The results remain to be seen.

Unicorn Numbers and Patient Capital

To summarize current challenges: fundraising faces relatively big challenges, affected by local government economics and fiscal conditions. State money indeed needs to play a very important role. Our investments, under industrial policy influence, often pile into the same sectors — when everyone favors a certain industry, they all invest, creating excessive competition and high overlap. For exits, domestic M&A exits are not the main channel; IPO is the dominant exit channel, so we're affected by secondary market issuance pace.

Although we've implemented the registration-based system, we hope issuance pace can be marketized, not subject to administrative interference. But objectively, we see marketization reform of the secondary market still has a long way to go. These are all challenges.

Objectively speaking, China's government plays a very important role in economic life. The macro policy environment has recently been actively improving, and at an accelerating pace — increasingly密集 policy positives.

Last June 16, the Private Investment Regulations specifically proposed encouraging the private equity fund industry to serve the real economy and promote technology innovation. A full chapter was dedicated to venture investment funds.

At year-end, the Central Economic Work Conference communiqué, for the first time, proposed encouraging development of venture capital and equity investment — this hadn't appeared in previous Central Economic Work Conference communiqués. During this year's Two Sessions, encouraging venture investment and equity investment again appeared in the Government Work Report. March 5, April 13, the new State Council Nine Articles were promulgated. The CSRC said 1+N, where 1 is the new State Council Nine Articles and N is a series of supporting measures. April 19, 16 measures were introduced encouraging venture funds to invest early, invest small, invest long-term, invest in technology.

April 30, the Politburo meeting — a very high-level meeting where every word must be carefully read — mentioned actively developing venture capital, strengthening patient capital. Patient capital appeared for the first time in a Politburo meeting document, and central documents mentioned actively developing venture capital.

May 10 evening, the Shenzhen Stock Exchange restarted listings, resuming IPO review. The first case May 16. We see IPO restart pace approaching.

May 23, the General Secretary held a symposium in Jinan with ten experts and entrepreneurs, including a Shenzhen Capital Group leader, specifically proposing developing venture capital, and raising what I call the General Secretary's question: Why is the growth rate of unicorn companies in our country declining? This represents the highest decision-making level's attention to venture capital, to venture investment, to patient capital.

The last thing I saw was May 27, the 14th Politburo collective study session discussing employment, which for the first time proposed encouraging entrepreneurship, encouraging youth to engage in key areas, key industries, urban and rural grassroots, and small and medium enterprises for employment and entrepreneurship. The center is密集 mentioning entrepreneurship,密集 mentioning venture capital and venture investment. I think in the important meeting to be held in July, some重磅 policies and重磅 reforms are very much anticipated.

I've reviewed Chinese investment's past and present. We must always maintain optimism about the future. Thank you all.

Image source | WAVES2024 live event

Layout | Yao Nan