Exclusive | Coatue Invested in Ba Wang Cha Ji — Can Dollar Funds Still Go Another 15 Years?

The Current Survival Reality of USD Funds.

By Qian Ren, Muxin Xu, and Yafei Yang

Edited by Jing Liu

Anyong Waves has learned that US hedge fund Coatue recently invested in Chinese tea chain Ba Wang Cha Ji at a post-money valuation of 3 billion RMB. No other new investors joined the round; existing shareholders include Congbi Qiushi and XVC. According to a recent Bloomberg report, Ba Wang Cha Ji is among six Chinese milk tea chains considering overseas IPOs.

Ba Wang Cha Ji has denied the funding news.

Like Chayan Yuese, Ba Wang Cha Ji is a tea brand with distinctive Chinese aesthetic sensibilities, though it was founded slightly later. Yet over the past two years, Ba Wang Cha Ji has grown rapidly: by end of 2022, its directly operated stores expanded from 425 to 1,100, a growth rate of 133.4%. Internationally, it has opened over 70 stores in Malaysia, Singapore, and Thailand, and has publicly stated plans to accelerate this expansion in 2023. Sources familiar with the matter told Anyong Waves that Ba Wang Cha Ji expects profits of 200–300 million RMB this year.

As one of its investors, Coatue has made numerous bets in new consumer brands, and in the new-style tea category alone has assembled a trio: HeyTea, Guming, and now Ba Wang Cha Ji. It is also among the investors in Manner Coffee.

For Coatue, this investment may carry a certain inevitability. But for a typical USD fund like Coatue, it is perhaps already something of an anomaly: over the past six months, most pure USD funds have nearly ground to a halt.

Consider Tiger Global — a fund from the same lineage that once believed it possessed "rainmaker" effects. Anyong Waves understands that before Tiger Global's widespread drawdowns last year, it had been preparing to open a new Shanghai office. Its China head, Pengfei Wang, had two headcount approvals, one of them designated for a hard tech investment lead. But hiring was ultimately suspended, and some members of the existing team departed. Meanwhile, Huanzhong Lei, who was based in the US and covered Chinese concept stocks (secondary market) at Tiger Global, also left last year.

In the view of someone close to Tiger Global, while the firm is not exiting China for now, these adjustments reflect a "strategic downsizing."

This single example offers a glimpse into the current reality of USD funds in China.

In summer 2022, Anyong Waves reported on personnel upheaval in the USD fund industry, then symbolized by layoff news from select top-tier firms. But in the past three months, the turmoil has spread across the entire industry's full chain.

The most recent development: "a USD fund claiming it will lay off all staff hired during the USD era." The logic, according to sources: "The firm is fully pivoting to hard tech, with compensation shifting to RMB fund standards." Anyong Waves reached out for confirmation; the response: "normal industry adjustments and turnover."

Another case involves a well-known fund from the VC 2.0 era. Rumors of its layoffs have circulated for months — first cutting some back-office staff, then restructuring the front-office team. In the past couple of years, this firm had been particularly successful at fundraising, leading to significant team expansion; the salaries it offered had become something of industry legend.

Beyond these two typical examples, few USD or dual-currency funds you could name have escaped this round of personnel adjustments. And the news always surfaces first on RedNote — now a new gathering place for investors who have switched careers — typically exposed via chat screenshots. From what we understand, aside from a few unsubstantiated rumors, most of this information is accurate.

Multiple headhunters told us that last year's VC optimizations focused on junior staff, but this year will reach VP and even MD (Managing Director) levels. At most firms, MDs are already core veterans, essentially the decision-makers for specific sectors.

Some firms have chosen to merge into others. On July 18, Ares, an American alternative investment manager translated as "God of War Management," announced its 100% acquisition of Crescent Point. Though not highly active, the Singapore-headquartered fund had made numerous investments in China, concentrated in consumer: Weimob, Huasheng Haoche, Qingke Apartments, Yunji, Yundian Technology, and others. But in fact, Crescent Point has not made a single China investment since 2021.

The above may represent only the micro-level picture. But S&P data shows that pure US private equity and venture capital invested $7.02 billion in China in 2022, a 76% plunge from $28.92 billion in 2021 — the lowest level in three years.

Some context is needed: US VC investment activity overall fell sharply in 2022. PitchBook reports total venture deal value at $238.3 billion for the year, down 30% from $344.7 billion the prior year.

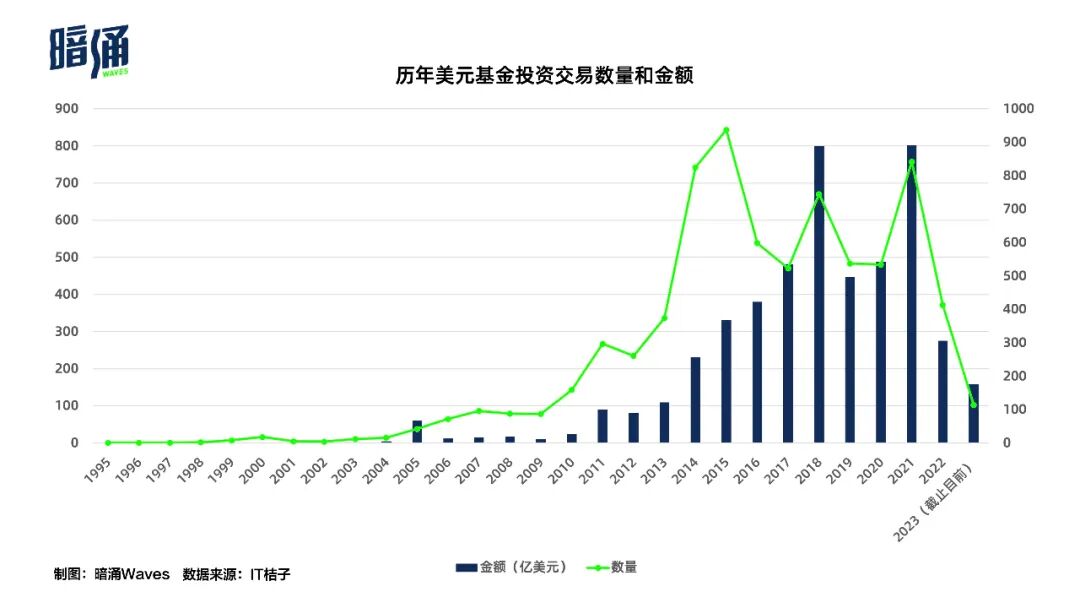

Another data set is even more stark. According to IT Juzi's real-time statistics, USD funds' investment transaction value in the domestic market was just $6 billion in 2005, peaked at nearly $80 billion in both 2018 and 2021, then fell off a cliff: just $15.7 billion from 2023 to present.

Historical USD fund investment transaction count and value

Recently, beneath an article titled "How USD Investors Successfully Pivot to Hard Tech," the top comment read: "For a USD VC, take an investor making 100K/month — swap in an RMB investor at 60K/month who's spent 5–6 years in semiconductors/new materials. Double their salary, and it's still 30% cheaper than the 100K, plus they're more loyal, harder-working, and bring top-tier industry knowledge and deal flow. If you're the boss, who do you choose? Others just haven't made the cuts yet."

Over the past year, USD investors have been leaving one after another: some becoming content creators, some returning to family businesses, some moving to CFO roles, others to state-owned platforms, and so on. But they face a common awkwardness — their former high salaries (for instance, the rumored VP at a foreign PE firm in Guomao earning over $800K annually) are burdens that most industrial or state-owned platforms can scarcely bear.

Of course, given the lagging nature of the investment industry, whether fund retreats or talent outflows, most shifts do not happen instantaneously.

Early this year, amid the GPT explosion, long-depressed USD funds were briefly electrified — some even declared they could "work another 15 years." But as domestic AI entered a temporary slump, this "paradigm revolution" in investors' words quickly dulled.

Many years ago, there was a widely celebrated feature on Fortune Venture Capital titled Learning from Sequoia's Example. But this past May, after closing its first 8 billion RMB fund, Xiao Bing told media: "The pendulum of the era has finally swung to the RMB GP side."

Image source: IC Photo; Farewell My Concubine still

Layout: Meng Du