Coatue's 2023 in Detail: Half Sea Water, Half Flame

Could AI become the lifeline of the economy over the next decade?

By Qian Ren, Muxin Xu

Edited by Jing Liu

The era of easy money has paused, and the chill is global.

A "longest bull market" in US stocks that began in 2009 and stretched for 13 years came to an abrupt halt in 2022. The impact carried into 2023: according to the latest data from Crunchbase, American startups raised just $27.6 billion in Q2 of this year, compared to $45.2 billion in Q1 — a drop of roughly 40%. Year-over-year, the decline was a staggering 55%.

US hedge fund Coatue has long cultivated an image as a tech investor, and over the years its practical strategies for navigating different cycles and its grasp of macro trends have outpaced most peers. Particularly during the 2022 US inflation surge, when unprofitable tech stocks plummeted, Coatue planned its retreat early, slashing positions and freeing up nearly 80% in cash — a move widely praised in the industry. We've previously analyzed Coatue's investment strategy in China.

In recent years, Coatue has produced an annual Investor Deck almost every year. The key message in 2022: if a bear market is a line of dominoes, Coatue believed we hadn't finished watching them fall. The crash in unprofitable tech stocks was only step one (falling 73% from February 2021 to February 2022), and by Coatue's reasoning at the time, the market was far from bottoming out.

This year, Coatue goes further, pointing to the arrival of a recessionary era while also identifying the "breakthrough" moment for the next tech supercycle: AI could become the new lifeline for the economy.

In this year's 46-page deck, Coatue compiled extensive macroeconomic data to explain what this means for recession. They also offered some intriguing analysis on how mega-cap tech stocks have performed, and what founders can learn from it.

In June, at the East Meets West conference, Coatue presented this deck, noting that 59% of economist respondents believed the global economy would enter recession in the next 12 months. Here are the key takeaways from the presentation, as excerpted by Waves.

Tech Stock Boom: Dream or Reality?

Coatue begins by reviewing its 2022 Investor Deck. Its predictions about fundraising difficulties, cost-cutting, and efficiency proved accurate, but its macro forecasts were overly pessimistic: compared to its prediction of a hard landing in 2023, the economy instead appeared to bounce off the bottom, with the S&P 500 gaining 20%.

This rebound is broadly attributed to several factors:

-

Macro-level inflation has gradually retreated from its peak, falling from around 9% in mid-2022, with Coatue's charts projecting it will drop to 2021 levels for the remainder of 2023;

-

Despite massive layoffs at top Silicon Valley companies, overall US unemployment has hit historic lows over the past two years, at roughly 3.6%–3.7%;

-

Europe's energy crisis has eased, with natural gas prices returning to pre-Russia-Ukraine war levels;

-

China emerged from its COVID crisis, with economic vitality returning;

-

Silicon Valley giants have pivoted, returning to business fundamentals and focusing on profitability;

-

A brighter dawn has appeared in AI, where the frenzy around OpenAI and ChatGPT has people sensing that a new supercycle may be approaching.

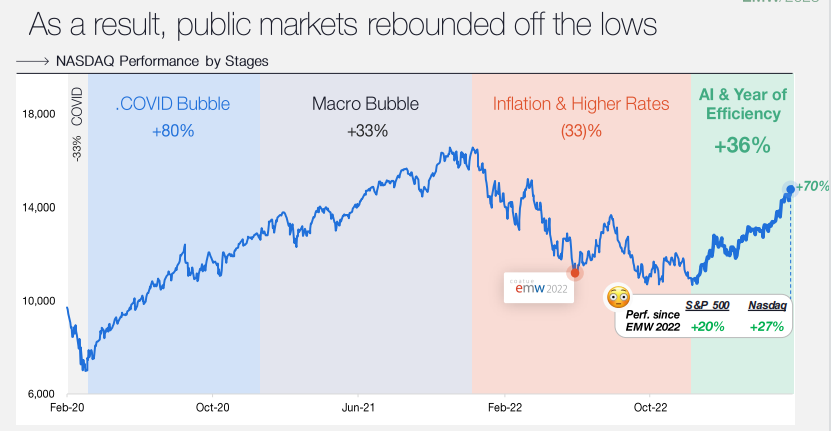

These factors have driven market recovery, with the S&P 500 up 20% and the Nasdaq up 27%.

(Nasdaq performance since February 2020, across five phases: COVID era, COVID bubble, macro bubble, inflation & high interest rates, and AI & efficiency year)

So do these data points signal that everything is looking up?

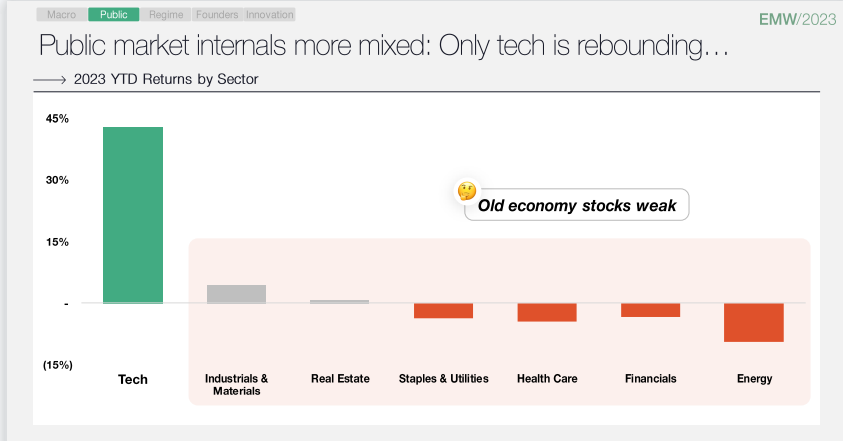

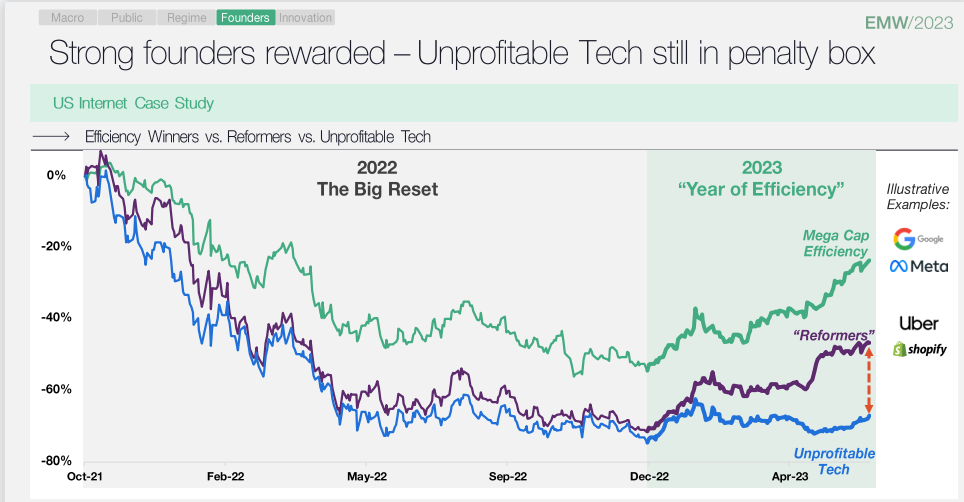

A closer look reveals that despite the S&P's climb, only the tech sector has rebounded meaningfully.

But tech stocks' eye-catching performance is partly a function of how low they fell in 2022. That year, multiple tech stocks dropped 90%, and the price-to-sales ratio of notable tech company Affirm even fell below 2 at one point — a year that thoroughly washed out and reset tech valuations.

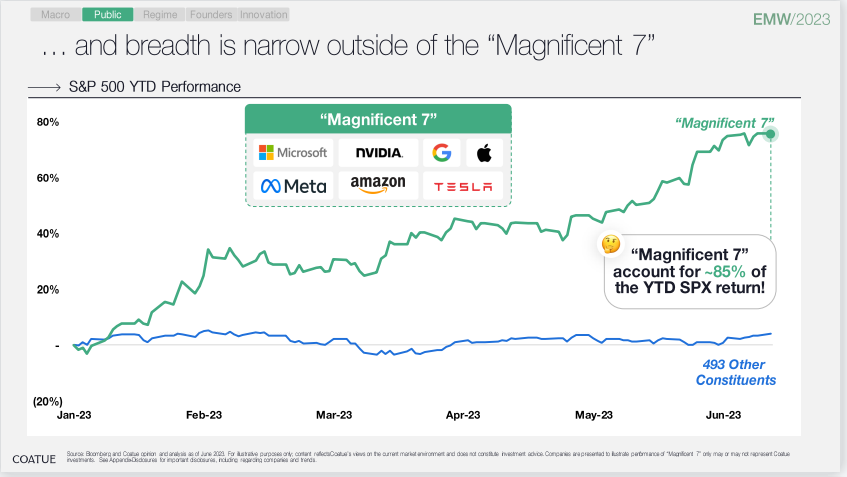

Another concern: of the 45% returns in tech stocks, the "Magnificent Seven" account for at least 85%. According to Bank of America data, the remaining 493 stocks in the benchmark contributed just 2.2 percentage points of the gain.

The "Magnificent Seven" — coined by Bank of America in its research reports — refers to Microsoft, NVIDIA, Google, Apple, Meta, Amazon, and Tesla. The naming may have been inspired by a film adaptation of Seven Samurai.

These seven stocks contributed 8.8 percentage points of the S&P 500's roughly 10% gain this year, and represent 31% of assets in global wealth management divisions, up 44% since the start of the year. Take NVIDIA: since its stunning Q1 earnings report, its market cap has surged by roughly $185 billion, meaning this single stock contributed one-fifth of the S&P 500's gains this year despite comprising just 2.7% of the index's weight.

So what we're seeing may be merely the illusion of a "tech bull market." As Bank of America worries, when the weight of a market rally rests on the shoulders of a limited number of stocks, fragility emerges.

Beyond tech, pressure persists in economically sensitive sectors: crude oil, regional banks, transportation, and retail all show vertical downward trends.

Scarce Hot Money, Global Chill

While select tech stocks have soared, Coatue sees the predicament of a far greater number of tech companies. Coatue judges that if the past was an era of hot money flooding markets, now is the era of returning to common sense. The rules of the game have fundamentally changed:

-

If money used to be "free," now you must contend with a 5% risk-free rate;

-

The era of unchecked growth is over; now you face the possibility of slowing growth;

-

Valuations are returning from bubble territory to rational levels;

-

The driver has shifted from capital to innovation and management;

-

The focus has moved from expansion at any cost to profitability.

After surveying market conditions, Coatue found that based on last disclosed funding rounds, unicorns (companies valued above $1 billion) had a combined market value of roughly $5 trillion; today, that figure stands at just $2.5 trillion.

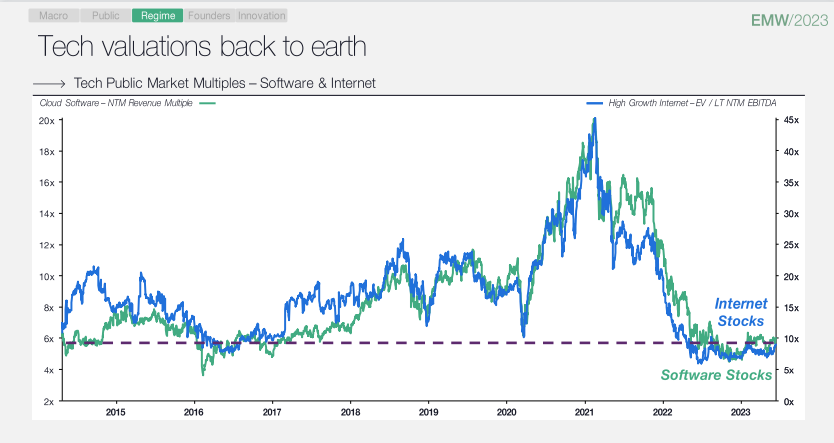

Tech stock valuations are falling from the sky back to earth.

Coatue's report shows that EV/NTM Revenue multiples for cloud software and internet companies have dropped from a 2021 peak of 20x to under 6x today, with valuation multiples falling from 45x to similar levels.

Behind this lies slowing revenue growth. According to Morgan Stanley's analysis of public enterprise software market caps, there's a very clear positive correlation between revenue growth rate and valuation.

Objectively, achieving revenue growth has become more difficult. In a survey of 68 cloud software companies, Coatue found their ARR (annual recurring revenue) growth was 20% between 2017–2020, reached 50% during the pandemic, but has dropped to -20% from 2022 to present.

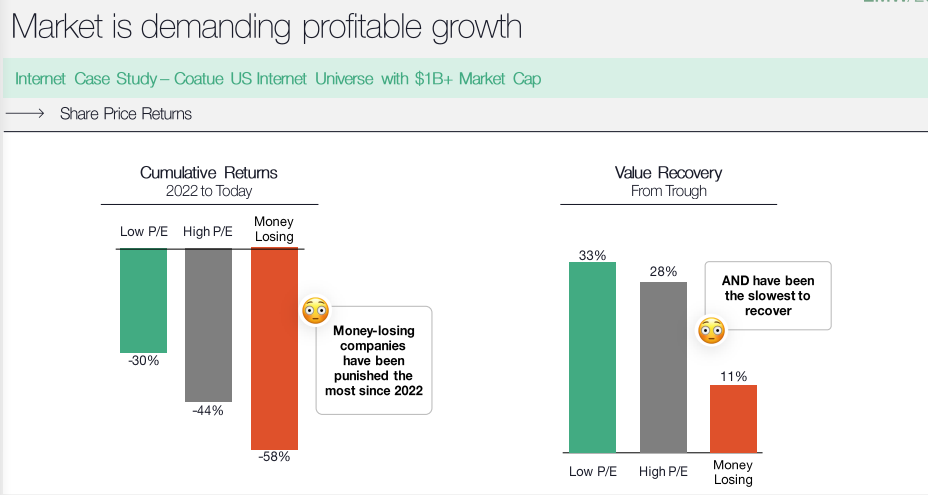

Nevertheless, the market is desperate to see profit growth, so unprofitable companies suffered the harshest punishment in 2022 and have rebounded slowest from their lows.

Coatue raises further concerns.

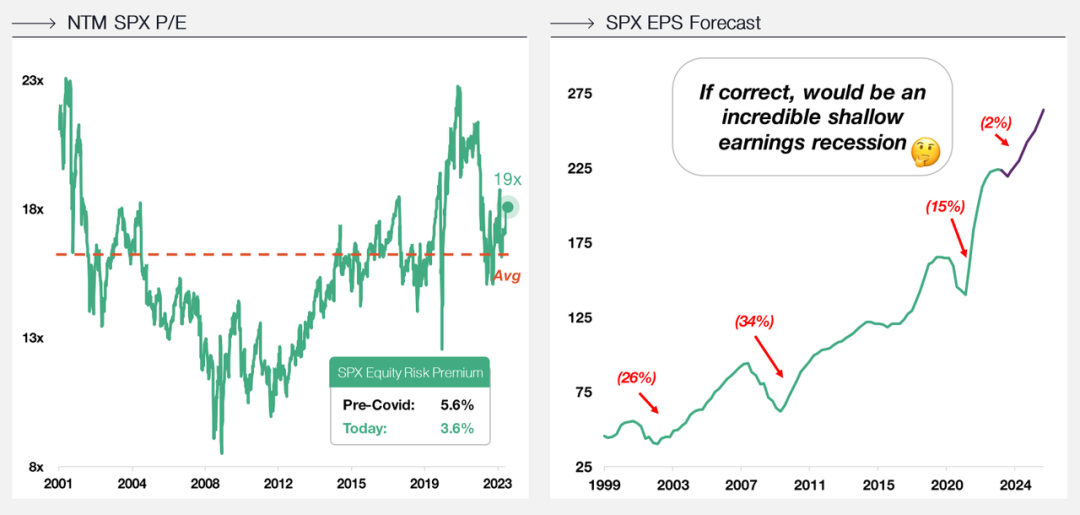

1. Stock valuations remain somewhat expensive

The equity risk premium has fallen from 5.6% before the pandemic to 3.6%, while EPS growth forecasts have plummeted from around 15% near 2020 to just 2% after 2024.

During the pandemic, the US adopted unlimited quantitative easing, massively oversupplying dollars and driving real interest rates to decade lows. This caused risk assets, particularly unprofitable tech stocks, to become frothy again. If this data holds, it would represent an incredible earnings recession.

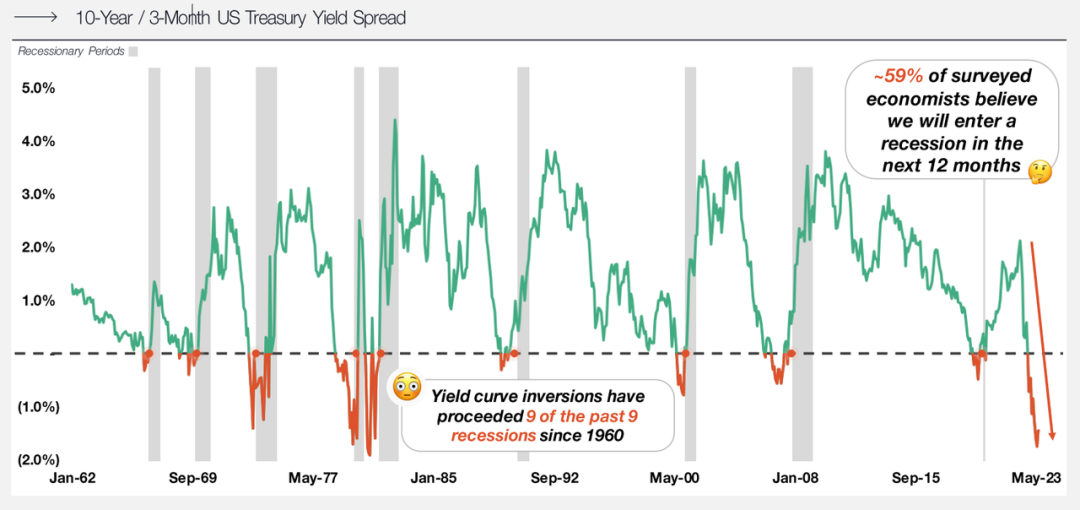

2. The economy hasn't escaped trouble

Looking at the 10-year/3-month US Treasury yield spread, Coatue notes that since 1960, yield curve inversions have preceded all 9 recessions. Now, 59% of economist respondents believe a recession will arrive in the next 12 months.

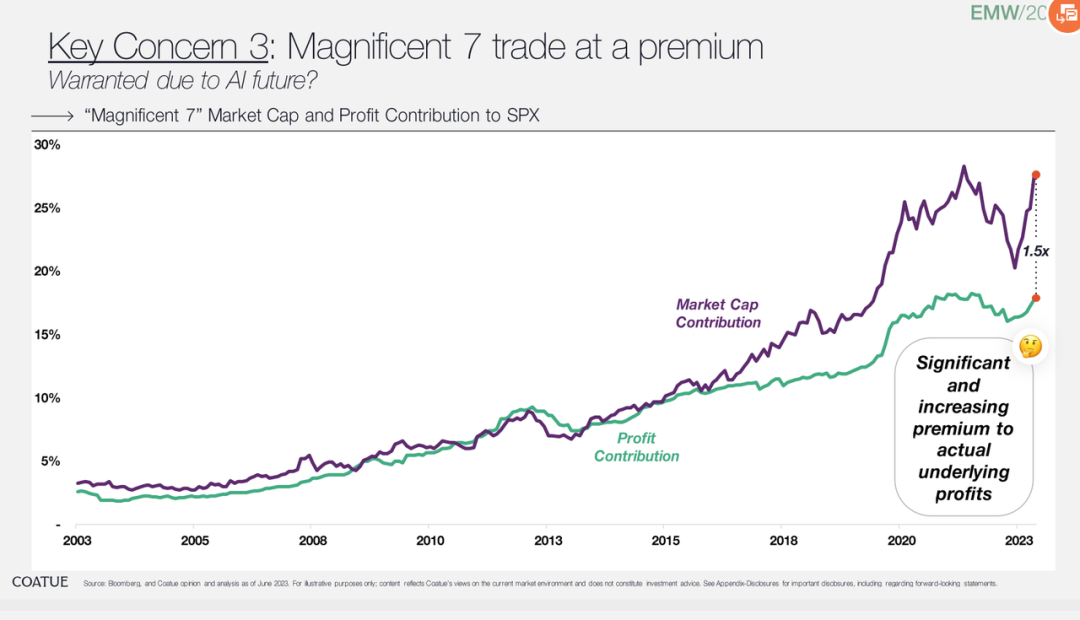

3. The Magnificent Seven's market cap and profit contribution

Before roughly 2016, market cap and profits tracked closely together, but in recent years, the premium on actual underlying profits has grown markedly and persistently.

Unicorns Will Be Repriced

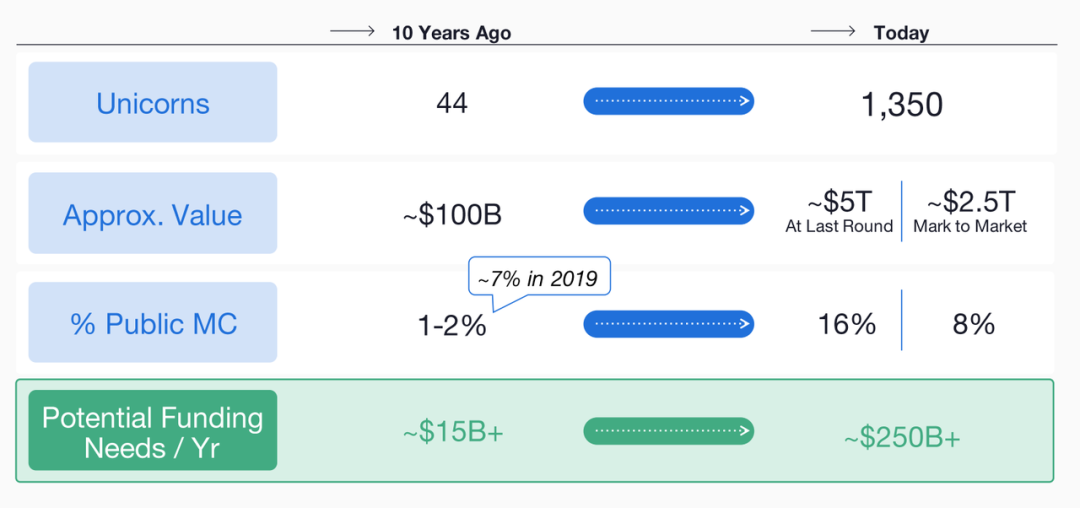

Coatue points out that the global unicorn count has reached 1,350, a 30x increase from 44 a decade ago; total valuation has grown from $100 billion to $5 trillion. Alongside this, these unicorns' annual potential funding needs have surged from $15 billion to $250 billion.

But here's the practical question: can these unicorns actually raise that much money? The answer is no. Because investors now have more attractive alternatives: they can buy Meta or Google at 20x P/E, or NVIDIA at 50x P/E. And there's another factor — in the past money was "free," but now you must accept a 5% risk-free rate.

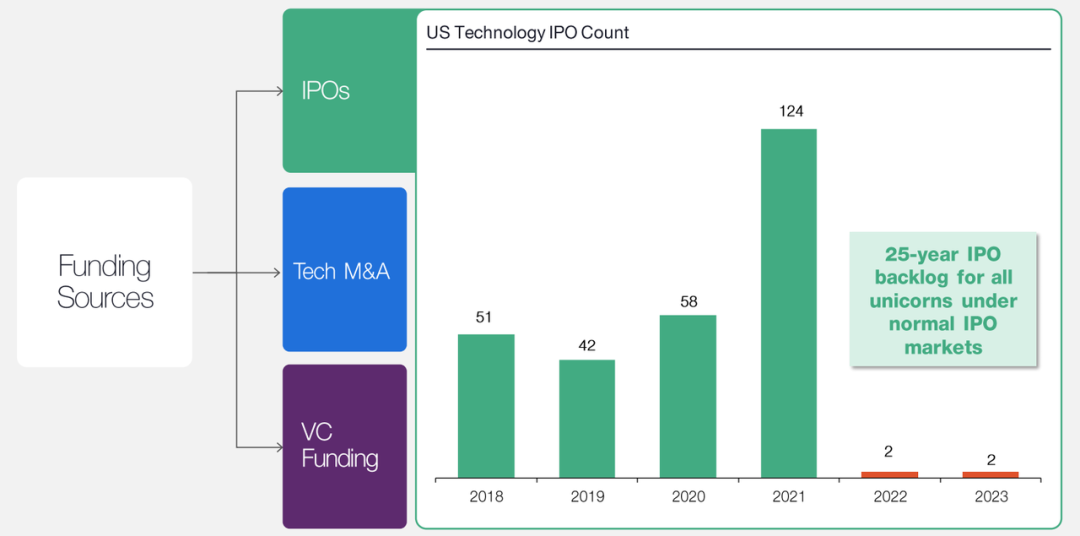

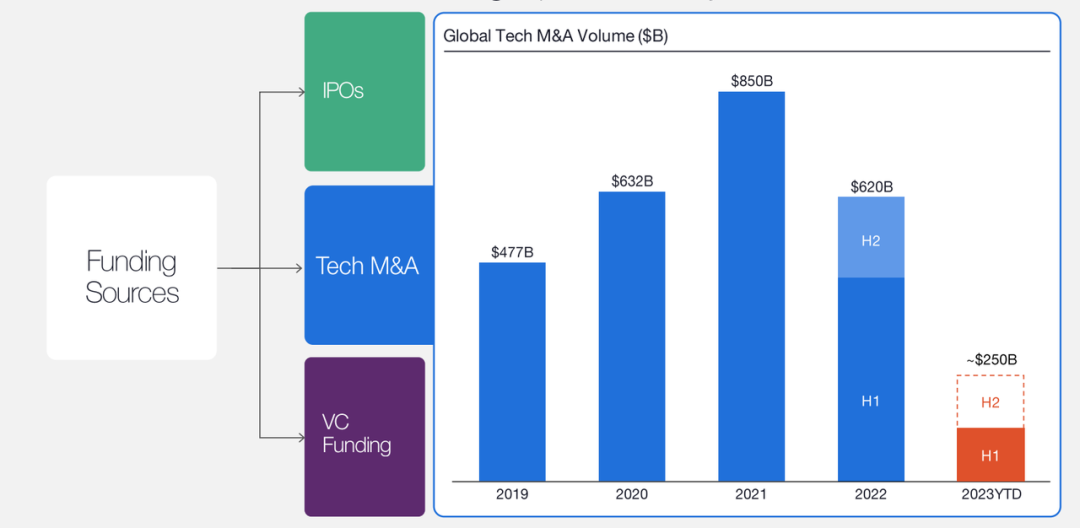

Another unavoidable trend: exit channels and follow-on financing options are narrowing. US tech IPOs peaked at 124 in 2021, but dropped to just 2 each in 2022 and 2023, freezing over.

Global tech M&A transaction volume was $620 billion in 2022, but Coatue projects just $250 billion for 2023.

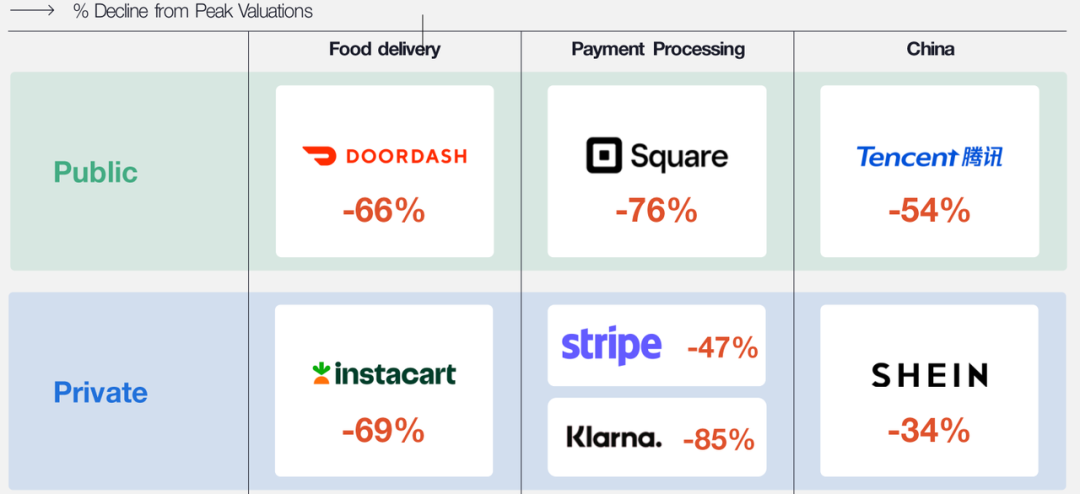

Most unicorn valuations are currently unjustified, and many large companies face repricing. Those that have raised new money have seen dramatic valuation cuts — Klarna -85%, Stripe -47%, SHEIN -34%.

Coatue believes that if many unicorns aren't repriced, they may never secure new funding.

For founders, the environment now looks like this: from focusing solely on growth, to focusing on efficiency, to now having to focus on both efficiency and scalable growth.

The economy is more resilient, but we haven't escaped trouble. For founders, this means the free money era is over, a new market regime is being established, and companies need to adapt to the "new normal."

The statements from Silicon Valley's star CEOs this year are telling —

Mark Zuckerberg, after layoffs, said "leaner is better," and in Meta's "Year of Efficiency," he recognized the importance of cutting costs and boosting efficiency.

Shopify CEO Tobi Lütke said "keep the main thing the main thing," realizing that companies must find the true pillars they rely on to survive, rather than expanding boundaries aimlessly.

And Coatue's pick for "Elon Musk quote of the year": "We're going to fire 80% of Twitter's employees." The Silicon Valley Iron Man, who acquired Twitter with such bold strokes, perhaps realized this year that "Twitter can run itself without anyone"?

AI Brings a New Supercycle

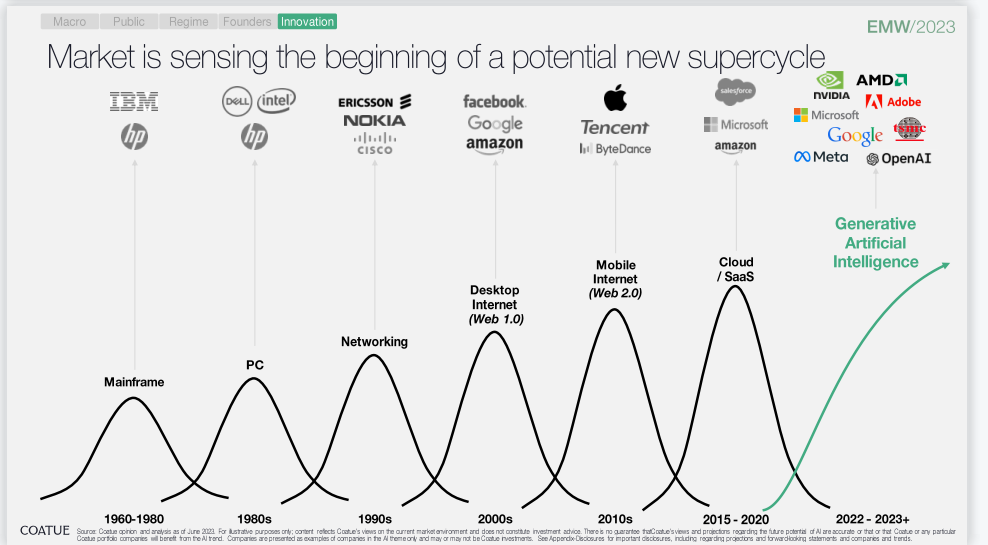

Coatue believes NVIDIA's blowout Q2 report represents the "breakthrough" moment for the next tech supercycle, and AI could become the lifeline for the economy over the next decade.

Every major supercycle in global business typically originates from underlying technological innovation. And 2023's biggest variable has been the emergence of generative AI.

Coatue analyzed the great companies born from supercycles since the 1960s. The CPU era had IBM; the PC era had HP and Intel; the networking era had Nokia and Cisco; Web 1.0 belonged to Facebook, Google, and Amazon; Web 2.0 to Apple, Tencent, and ByteDance; the cloud era to Salesforce and Microsoft; and today's hottest "Magnificent Seven" may be signaling that the "singularity moment" of the AI supercycle is approaching.

Every major cycle has had a breakthrough moment. Coatue uses mobile internet and cloud computing as examples.

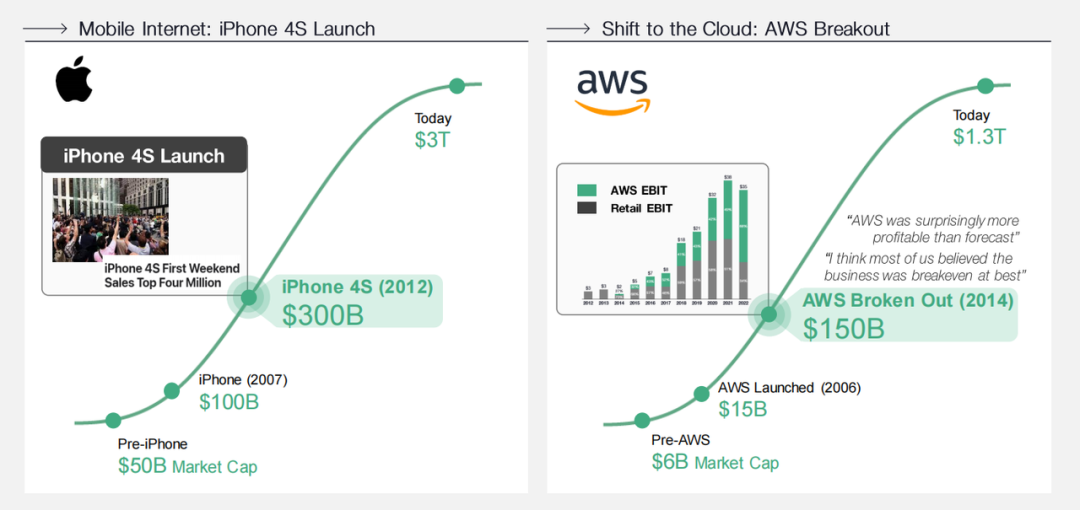

First, the launch of the iPhone 4S (the fifth-generation iPhone).

If the smartphone market was worth $50 billion in the pre-iPhone era, the 2007 iPhone launch lifted it to $100 billion, while the 2012 iPhone 4S increased that magnitude threefold — to $300 billion.

The iPhone 4 was the most successful iPhone in Apple's history, and a monumentally significant product in phone history. If the first three iPhone generations represented Apple's success as a participant, the fourth iPhone's role was that of an industry disruptor.

Second, the cloud computing cycle arrived because of AWS's breakthrough.

Most people thought AWS would at best break even; instead its profitability stunningly exceeded expectations. Amazon's cloud business surpassed $80 billion in revenue in 2022, contributing 40.5% of business growth.

When Amazon released its 2014 annual report, the company — not known for prioritizing profit — shocked the outside world again: cloud computing revenue approached 50%, reaching $1.56 billion. That day, Amazon's stock jumped 14.1%, with a P/E ratio nearing 1,000x. AWS was Amazon's explosive inflection point. As a standalone category, AWS's growth rate and profitability far exceeded the company overall.

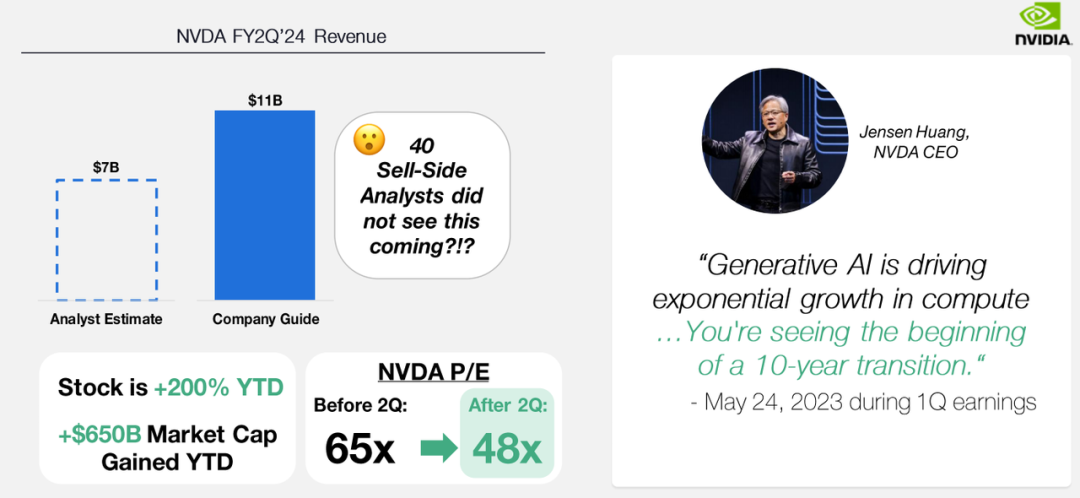

So, looking at NVIDIA's Q2 revenue (NVIDIA stock has risen 200% year-to-date, adding $650 billion in market cap), does this also mean we've reached the breakthrough moment of the AI era?

NVIDIA CEO Jensen Huang said, "Generative AI is driving exponential growth in computing. We are at the beginning of a decade-long transformation."

Image source | Visual China

Layout | Meng Du