Coatue's Take on 2024: No AI Bubble, and US VC Exits Are Struggling Too

A tale of two extremes.

By Jiaxiang Shi

Edited by Jing Liu

Since entering China in 2014, the renowned hedge fund Coatue has hosted an annual closed-door event called East Meets West (hereafter "EMW"), bringing together business figures from China and the US. Each year, it publishes a public Investor Deck — this year's is the eighth edition.

In last year's 46-page presentation, Coatue continued its view from the previous year that the bear market hadn't fully run its course, pointing to the arrival of a recessionary era. It compiled extensive macroeconomic data and attempted to explain what this meant for economic decline. Coatue founder Philippe Laffont said, "Two years ago, I thought the world was ending, but I reserved the right to change my mind the following year, and then tell everyone once again that the world was ending."

But in this year's report, Coatue broke from form, arguing that macroeconomics may no longer be the biggest factor moving markets. "Despite macroeconomic uncertainty, markets appear somewhat desensitized to these factors and are showing resilience." As a result, Coatue believes the most likely path forward is a soft landing or continued growth.

Beyond macro, Coatue devoted massive space to AI and VC. Last year, Coatue noted that AI would become the new lifeline of the economy — and looking at this year, that prediction has come true: in the height of summer, the Nasdaq hit record highs, breaking 18,000. Philippe Laffont marveled that he never thought he'd see the day when a single company would be worth $3 trillion (NVIDIA), and that its one-day gain could equal the entire market cap of the 20th-largest company in the S&P 500.

Philippe Laffont also said that every year, Coatue tries to come up with something interesting. "Unfortunately, the only thing I can think about this year is whether AI will become more important than all of us combined."

Here are the key takeaways from the presentation, as excerpted by An Yong Waves (暗涌Waves):

AI Is Not a Valuation Bubble, But It's Mainly the Giants' Game

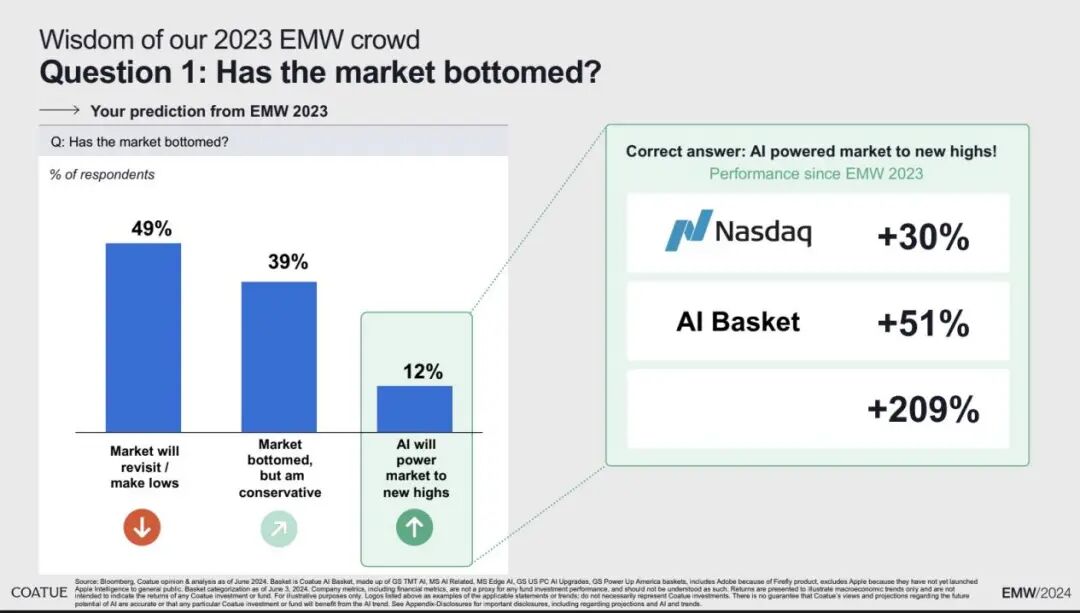

At the opening of the presentation, Coatue posed three questions. The first: Has the market bottomed? Nearly half of respondents believed the market would hit new lows, while the other half disagreed. Some 12% of respondents thought AI would drive the market to new highs, citing the 30% rise in the Nasdaq, the 51% gain in the AI basket, and NVIDIA's 209% surge since the 2023 EMW.

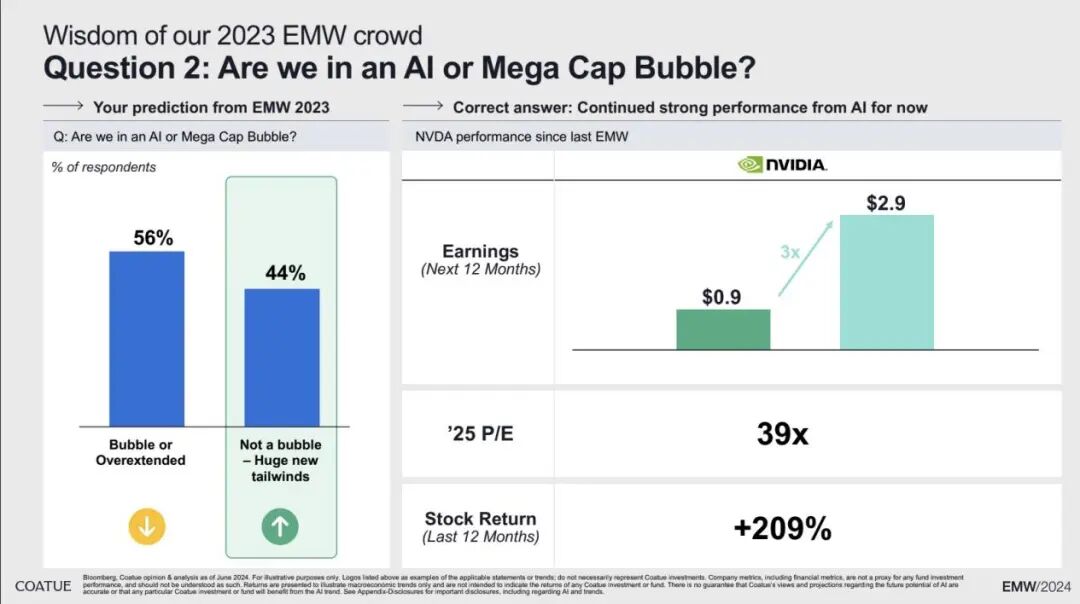

So Coatue followed up: Are we in a massive AI capital bubble? Fifty-six percent thought AI had already overheated, while the rest believed we were at the dawn of a new era. The latter view was again supported by NVIDIA's strong performance. Philippe Laffont, with a quarter-century of investing experience, noted that despite NVIDIA's revenue tripling, its P/E ratio hadn't changed. He'd only seen this twice before: once with Google's 2004 IPO, and again with Apple's 2009 iPhone launch. A Coatue partner had also once cited Google's 2004 IPO at $85, which quickly rose to $109 — at the time, everyone thought 40x P/E was too expensive, yet years later Google stock surged 1,200%.

The next question: Which AI company will be most valuable in five years? The most votes went to Microsoft, followed by NVIDIA, Apple, and Google — suggesting most believe the giants will maintain their dominance. In fifth place was the current hot name, OpenAI — the only company valued below $2 trillion — with Meta and Amazon trailing. However, Coatue also noted that the "Magnificent Seven" (Microsoft, NVIDIA, Google, Apple, Meta, Amazon, Tesla) may reshuffle, and a new "AI4" could emerge. In the past, riding with the market-moving "Magnificent Seven" was always the safest bet when entering the market, but that changed in 2024. Coatue listed the year-to-date performance of the "Magnificent Seven": NVIDIA absolutely led the other six, while Tesla clearly fell behind as the only one with negative returns. Philippe Laffont added that just a week before the conference, Apple was still in the red.

Technology waves keep repeating, so looking back matters. Coatue summarized seven tech waves since the 1950s: Mainframe, PC, Networking, Web 1.0, Web 2.0, Cloud and SaaS — roughly one every decade, with GenAI being the most recent. Their expectations for AI far exceed market consensus. Philippe Laffont's explanation: we are transitioning from CPU-based computing to GPU-based computing. He referenced The Matrix, where the protagonist wakes from his cocoon — "there are millions of cocoons — that's my explanation for GPU infrastructure."

Over the past 70 years, people spent trillions of dollars building CPU-based architecture. Going forward, they will spend $10 trillion or $20 trillion rebuilding everything around GPUs. Coatue noted AI will go through four phases: core infrastructure (GPUs, cloud), edge AI, AI applications, and embodied intelligence. We are currently in the edge AI phase. In Philippe Laffont's view, infrastructure is like the left brain, solving the most complex problems, while edge AI is like the right brain, relying on intuition for rapid problem-solving — though not always accurately. AI has become the absolute force driving growth, contributing two-thirds of the S&P 500's returns — with one-third coming from NVIDIA alone. Looking at median returns, AI-enabled stocks have outperformed others by tenfold. In just a year and a half, the market cap of AI infrastructure has grown by $6 trillion. "For founders, you have to think about telling a good story when going public, because the market is really voting," Philippe Laffont cautioned.

Coatue then posed two questions: Are we in a massive AI bubble? And is software dead?

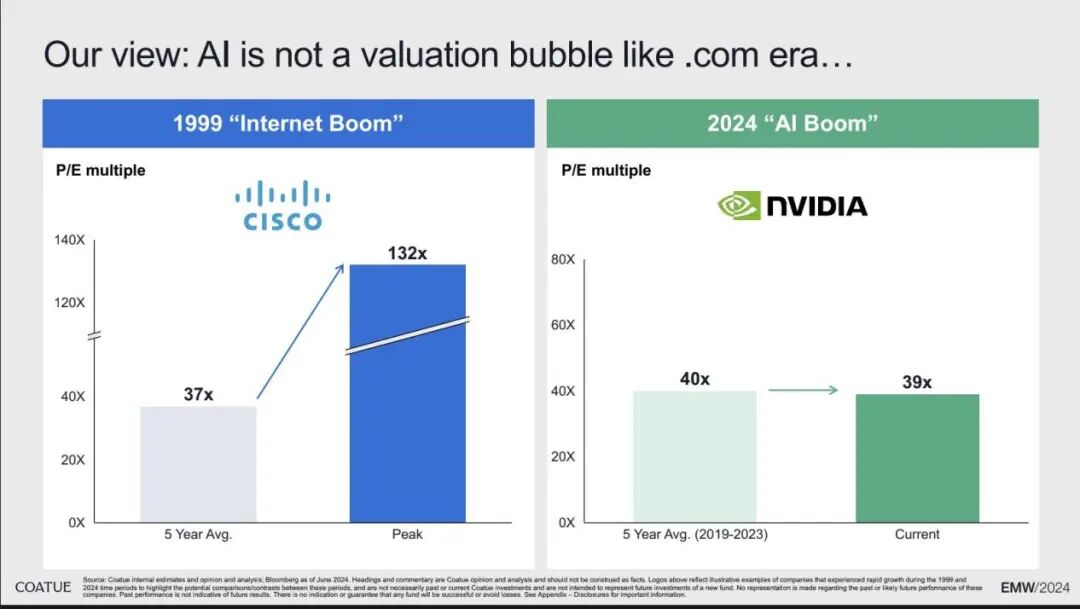

Coatue believes AI differs from the dot-com bubble of 2000. The report uses Cisco as an example: its average P/E over a certain five-year period was 37x, but at its peak reached 132x. Applying the same calculation to NVIDIA, its five-year average P/E is 40x, while today it stands at just 39x. "So if there's a bubble, it's not a valuation bubble — it's a bubble where profits have been pulled forward," Philippe Laffont explained.

So is software headed to the grave? Software was long considered an attractive model — stable revenue without heavy capital investment. But today, software growth has fallen from peak levels above 20% to around 10%, with P/E multiples down to just 5.5x.

Still, Coatue believes future software interaction will primarily use natural language, where users simply input commands like "show my emails," and the model processes the request and interfaces with the software. "Software will come back — it's just been naturally delayed," Philippe Laffont said.

Why IPOs Are Under Pressure

On private equity, Coatue first noted that fundraising is gradually normalizing. The 2021 peak of over $700 billion is no more; Coatue expects just $265 billion this year — back to 2017 levels.

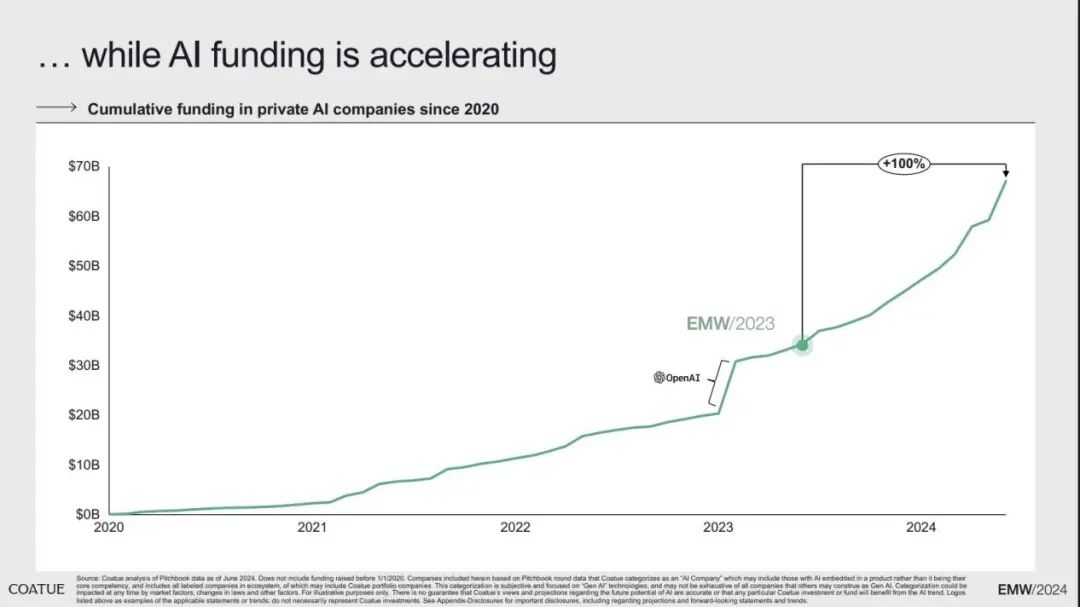

Yet AI company fundraising is accelerating — so fast that from mid-2023 to now, it has doubled to nearly $70 billion. Coatue cited data showing that in 2024 to date, pure AI deals account for only 3% of total deal count but 15% of total investment value, with average valuations of $1 billion (5x that of non-AI companies) and average round sizes of $120 million (6x that of non-AI companies). This even surprised Coatue, long a booster of tech stocks: "Is it getting a bit too hot?"

Of this, 62% of capital flows to model-layer companies, 20% to applications, and less than 1% to AI semiconductors. Coatue co-founder Thomas Laffont offered reassurance: models will consume tens of billions of dollars, but many people don't need to build models — the AI trend will benefit everyone.

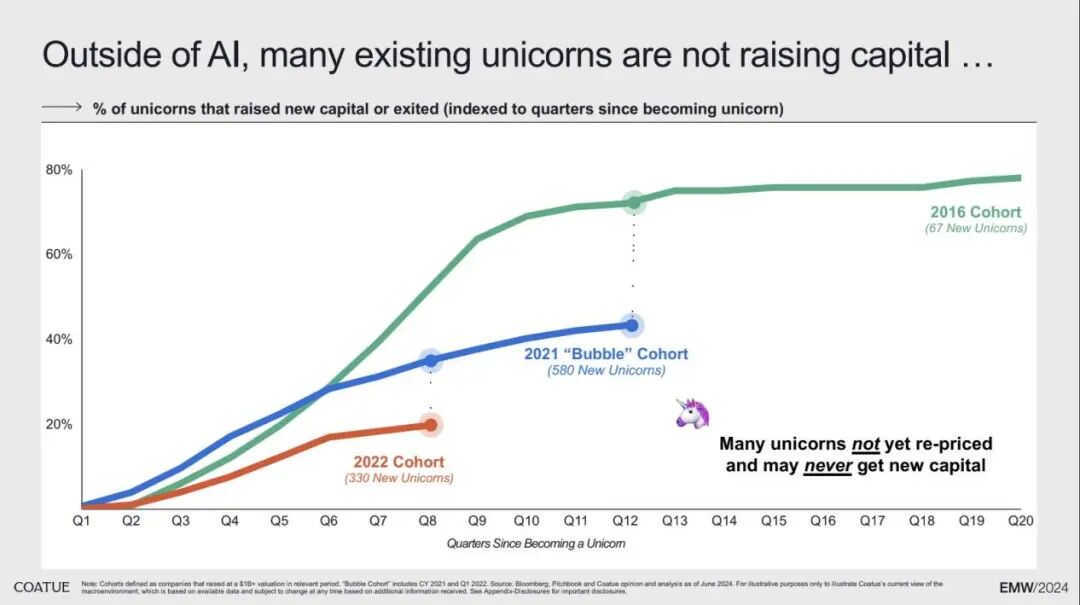

Fire and ice: most of the excitement belongs to AI alone, while unicorns tread on thin ice. The number of private unicorns has skyrocketed from 44 in 2013 to 1,420 today — surpassing the number of listed unicorns. Coatue put it bluntly: many unicorns have yet to be repriced, "and may never see new capital injections." Thomas Laffont recalled entering the market during the 2008 financial crisis, squeezed into a tiny office watching the Nasdaq drop 7% or 8% daily. "Even that year, there were more tech IPOs than recently."

It seems the world truly shares the same chill — so why are IPOs so hard to achieve on the other side?

Coatue identifies three main problems:

First, the rise of passive index funds and ETFs. They favor scale, so the IPO threshold for unicorns has risen from $10 billion to $100 billion.

Thomas Laffont recalled that when he started out, there were many small-cap funds whose sole job was to meet young people and shepherd them to going public — but the market environment has completely changed. "Competing against machines and ETFs is harder than competing against Sequoia and Benchmark," he said.

The second problem: private company valuations may exceed public valuations after listing — the primary-secondary inversion. Coatue noted that top 1% company valuations have returned to pre-pandemic levels, but overall market valuations remain halved. It reminded participants to consider market realities when evaluating assets and to recognize the importance of liquidity.

In an aside, Thomas Laffont mentioned one asset that has returned to peak form: Bitcoin. In his view, Bitcoin has three advantages: dominant market position, strong liquidity, and broad investor appeal through ETFs. "Bitcoin proves that compelling ideas always have a place in public markets." From this angle, it's not hard to understand why Web3 has recently returned to private equity funds' (especially secondary funds') field of vision.

The third problem: public market investors have many alternatives, so they demand growth, profitability, and reasonable valuations.

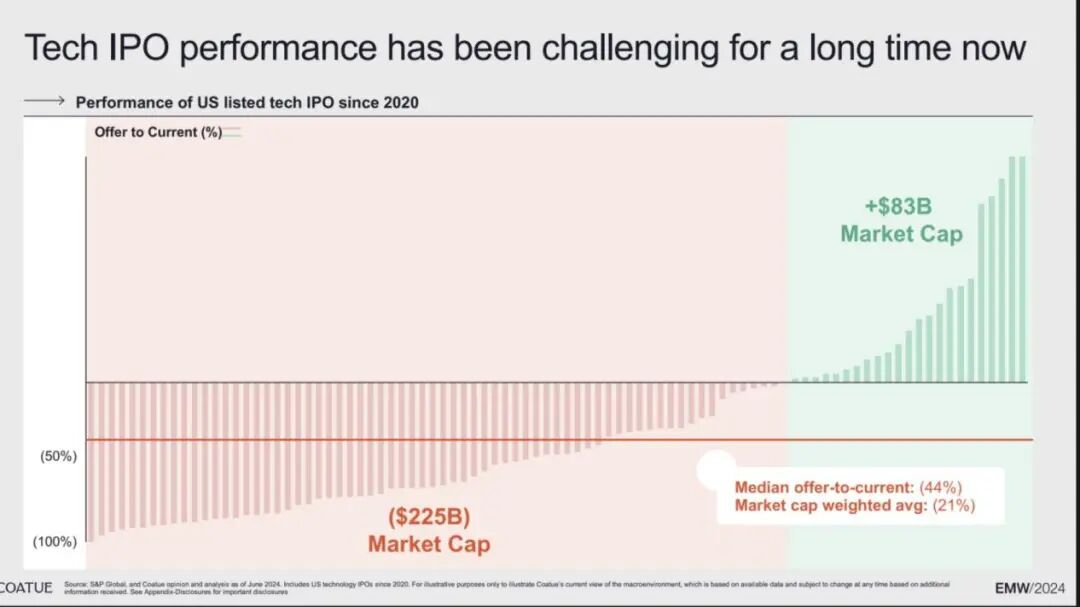

And an IPO isn't the finish line. Over the long term, tech companies still face challenges post-IPO. "Recent IPOs have actually played the role of value destroyers," Thomas Laffont said. Since 2020, tech IPOs have seen a market-cap-weighted average decline of 21%, with a median decline of 44%.

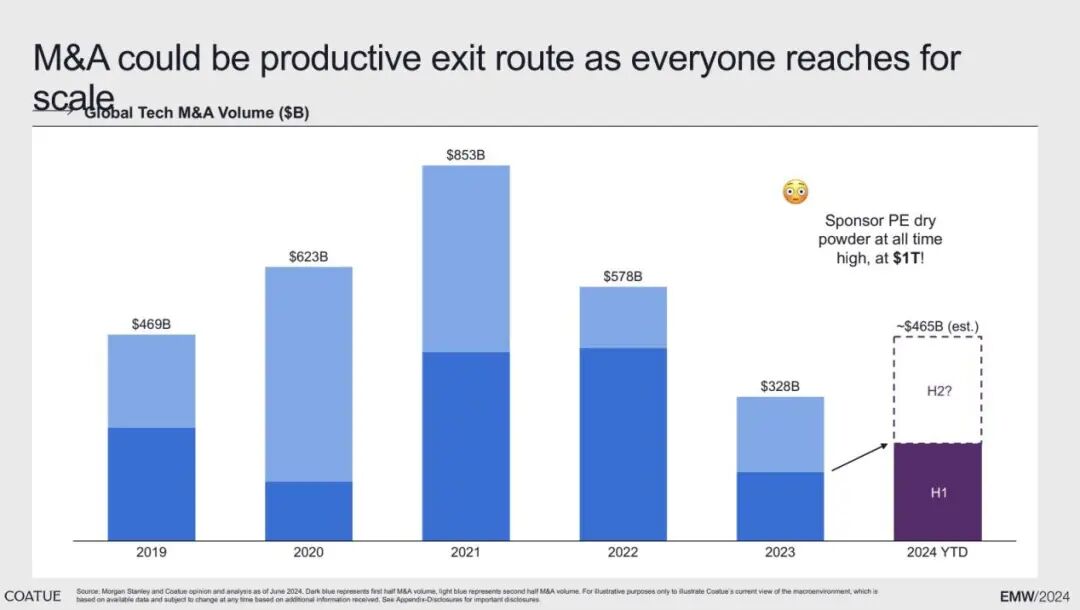

But going public isn't the only answer. Coatue believes M&A may be another productive exit path. Though tech M&A value has declined since 2021, Coatue predicts it will rise to $465 billion this year.

A representative case is Metropolis, which acquired publicly traded SP+ for $1.5 billion. Metropolis is an AI technology startup providing digital payment systems and infrastructure for parking lots, aiming to let drivers enter and exit without swiping cards or using cash. SP+ is a US parking facility management services provider, overseeing over 2 million parking spaces. Through the acquisition, Metropolis hopes to push its AI system into the parking industry. "Even a parking company can apply AI leverage," Coatue remarked.

Image source: IC Photo

Layout: Nan Yao