Why does KKR keep emphasizing "keep it simple"?

The truly valuable investment opportunities in the AI wave are the "non-tech" plays.

By | Muxin Xu

Keep It Simple, Tune Out the Noise

Quoting Steve Jobs's famous line — "Simplicity is the ultimate sophistication" — global private equity giant KKR made "keep it simple" the central theme of its 2023 mid-year report, maintaining the same keyword from its year-ahead outlook published in January.

At its Q1 earnings call, KKR co-CEO Scott Nuttall said: "There's a lot of noise out there, but we'll keep raising capital." The noise: geopolitics, war, the wave of bank failures led by SVB, and the surge of breakthrough technologies around AI. The distractions are alluring too — the S&P 500 is up roughly 14% year-to-date (while short interest on the index hovers near 30-year highs), and high-yield bonds have delivered total returns above 5%. Such chaos can cause traditional 60/40 investors to overlook some standout opportunities.

Faced with this cacophony, the storied PE house chose to "keep it simple." Simple doesn't mean easy — it means doing what best ensures survival through today's volatile cycle. Most notably: fundraising.

In the 2021 fundraising environment, KKR bucked the trend by announcing the close of its Asia IV fund at $15 billion, making it the largest PE fund in Asian history. This April, KKR announced the final close of European Fund VI at $8 billion. The firm's total assets under management now stand at $504 billion.

The question on everyone's mind: with such massive capital to deploy, how is KKR allocating in 2023?

In its 68-page report, KKR repeatedly emphasizes the importance of credit and collateral-based cash flows this year. Credit makes more sense than equities in most asset classes. KKR's forecast: 2023 EPS will decline 5% to $210, with 2024 growth slowing further to a tepid 8% rebound to $227. KKR continues to bet against the dollar, using real assets as a key hedge. Additionally, KKR believes 2023–2024 will be strong years for private equity, with sectoral and geographic advantages in private markets serving as important differentiators versus public markets.

We often favor complexity over simplicity to avoid paying a higher price, but such strategies ill suit the current cycle. How to keep it simple in today's asset allocation?

Take credit: KKR believes investors should buy liquid private credit, or well-structured mortgages with solid cash flows; on the fund side, convertible bonds merit greater allocation; in equities, small- and mid-caps look cheap by virtually every metric. By contrast, high-risk, high-reward plays — such as shorting unprofitable tech companies, or lending to "zombie companies" for 100–200 basis points of yield — are poorly suited to the present moment.

Looking back at KKR's annual keywords reveals its own journey through disorienting noise. Its themes for 2020 and 2021 were "Symphony" and "Another Voice"; by 2022's "Walk, Don't Run," the tone had grown simpler and more composed.

China Is Experiencing a Consumption-Driven Recovery

KKR's mid-year report analyzes economic trajectories across key global markets including the US, Europe, China, and Japan. Here we focus on China.

In fact, the S&P 500 bottomed as early as October 2022; we are now experiencing the fastest economic recovery since WWII. But globally speaking, this recovery is asynchronous.

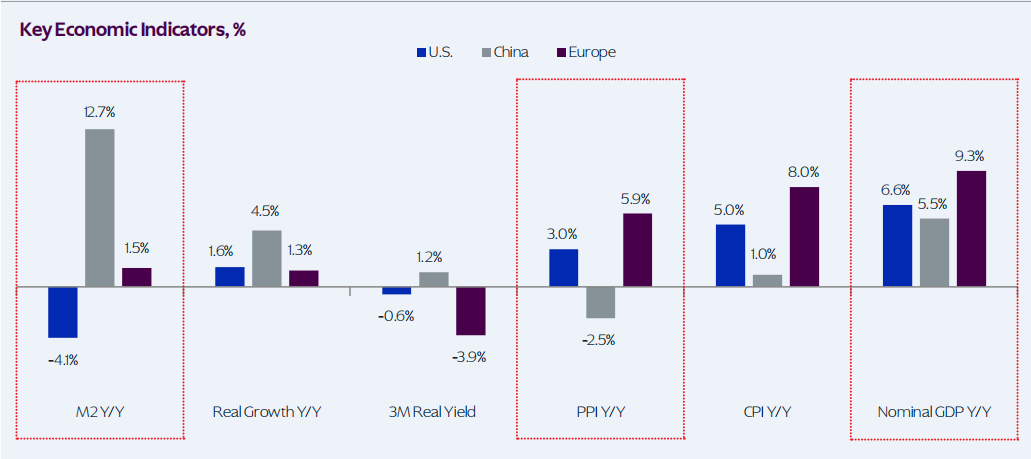

Compared to the US and European markets, China's M2 money supply, real growth index, and real interest rates all remain elevated, while PPI (Producer Price Index) and CPI (Consumer Price Index) recover slowly.

In KKR's view, China is experiencing a consumption-driven recovery — it's just still in early stages, which explains why this upturn feels less pronounced.

During its recent China research trip, KKR found shopping malls packed with people and tourism in full swing. Sales of jewelry, automobiles, apparel, dining, sports, and entertainment grew roughly 25–45% year-over-year. In March, China's overall retail sales grew 10.6%, nearly double the pace of the first two months of the quarter, with more spending likely still in the pipeline.

Yet Chinese consumers still hold over RMB 6 trillion in "excess savings," equivalent to 15% of annual retail sales.

And unlike past cycles, real estate may not serve as a pillar of future economic growth. Though home sales volumes rose 8.8% year-over-year, new housing starts fell more than 20% due to inventory overhang, while households continue prepaying mortgages. Meanwhile, falling energy prices and overcapacity in certain sectors will compress industrial profit margins concentrated in upstream and midstream industries.

Beneath the AI Hype, "Non-Tech" Investment Opportunities Deserve Attention

Following the first close of its $8 billion fundraise, KKR European Private Equity co-head Philipp Freise noted with no small pride: "When the macro environment is down, private equity has always been the strongest. PE consistently produces its best years during volatile times." Yet he cautioned: "In the second half of 2023, the private equity world will see undercurrents."

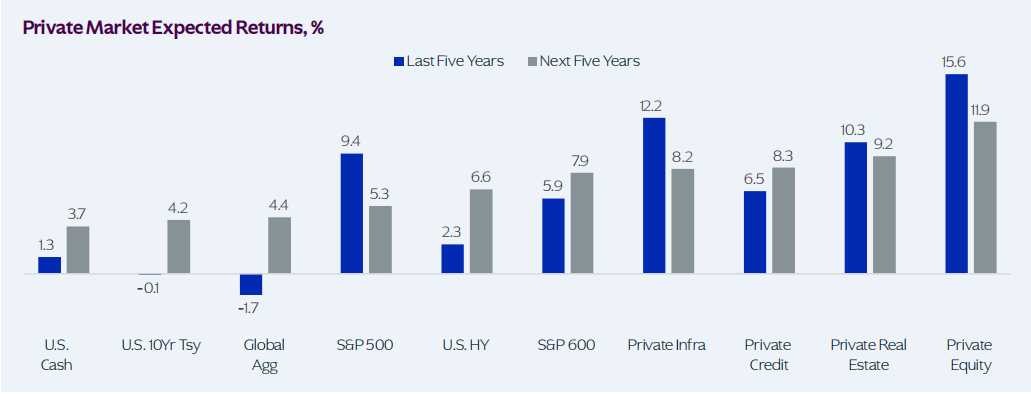

As things stand, 2023/2024 may represent "the best year in the next five" for private equity markets. KKR's expected return framework suggests lower total returns from private markets over the next five years, requiring investors to think differently about asset allocation.

In the chart, nearly every category projected to underperform its historical returns over the next five years falls under private assets (private credit, private infrastructure, private real estate, and private equity). By contrast, cash and bonds see their forward returns surge.

Yet historically, including private equity in a portfolio has typically helped deliver better performance in diversified allocations.

For primary market investors, the core strategy for this year and next remains "keep it simple" — focus on securing stable returns rather than blindly taking risk. Because "a B-grade investment today could become an A in tomorrow's market, but if an investor pushes for risk expansion, a C could become an F."

Days earlier, Coatue's mid-year report treated AI as the lifeline of the next decade's economy. KKR also devoted substantial space in its key investment themes to analyzing the emergence of generative AI, with other themes tangentially connected to artificial intelligence as well.

In sum, "non-tech" investment opportunities beneath the AI wave may represent the truly submerged, valuable part of the picture. A recent IBM study found that roughly 40% of companies are currently exploring AI use in their businesses, which will produce significant impact. In services, for instance, thoughtful AI integration into business models can drive revenue growth and cost efficiencies, restructuring the P&L.

Regrettably, the market's recent obsessive focus on a handful of tech stocks (such as NVIDIA) may signal that most investors are missing the genuine value creation in this new mega-theme.

Consider new energy: AI brings both pressure and opportunity from another angle — research shows AI servers consume 10–30 times more energy than traditional cloud storage. Energy thus becomes critical for companies in related businesses. Data indicates that by 2030, data centers alone will consume 8% of global energy, with half going to cooling — and the emergence of AI only amplifies the upside risk.

Additionally, persistent labor shortages coupled with breakthroughs in AI technology will accelerate automation and digitization in traditional industries.

Beyond artificial intelligence, the backdrop of benign globalization giving way to great-power competition warrants attention. This shift means nations, corporations, and even individuals must accept and adapt to transformations across energy, data, food, pharmaceuticals, technology, water, and transportation.

Finally, the post-pandemic consumption recovery, though still in early stages, also merits watching.

KKR's picks and pans in secondary markets may offer additional guidance: beyond its long-standing bullishness on Japan and collateral-based cash flows, KKR has added to cash, liquid credit, convertible bonds, more uncorrelated assets, and greater tilt toward middle-income consumers.

Image source | KKR

Layout | Yunxiao Guo