Off the Beaten Path in Primary Markets: Beyond Equity Investments | Entering the Game

"Be like water: not racing to be first, but flowing on and on, unceasing."

Technological upheaval, capital reallocation, and the tangled roots of an era — together they compose the complexity of today's business world. Between innovation and capital, the operating models that once worked are now facing new challenges. The industry rules inherited from West to East have been scattered, and people are urgently seeking new maps and new orders.

"Entering the game" is perhaps the most accurate verb to describe the venture capital industry, Chinese society, and even the global landscape of the past five years. "Entering the Game" (Rùjú) will also be the name of a new column at Dark Tide Waves (Ànyǒng Waves).

"Entering the Game" is born amid transformation. To summarize in one sentence: we hope to find new players and new strategies better adapted to a changing environment — perhaps more industry-focused, more RMB-denominated, more technology-driven, more rule-savvy, more Chinese; or perhaps more wildly imaginative, more harmonious with the environment, more global; or possibly more limited, yet more distinctive.

Those willing to roll up their sleeves and enter the game always deserve attention and reward. We hope that the people, institutions, and choices recorded by "Entering the Game" will become the footnotes of this transformative era.

This is the second article in the column.

By Xu Muxin

Edited by Chen Zhiyan, Jing Liu

Has equity investment lost its magic? In the primary market, equity investment was once regarded as the industry's "holy grail" — at least in the internet era, equity was the best way to strike gold. But over the past three years, the "grail" has begun to "tarnish."

"Investors' money, most likely, won't come back." Ni Zewang, a well-known investor, once expressed this concern in a public speech. This was in 2018, when primary market investment cases exceeded 10,000, while IPOs numbered fewer than 200. In hindsight, this statement was not a conclusion but the preface to a prolonged exit dilemma.

The most typical example is the new consumer sector, which rose to prominence only to fall silent just as quickly. Its emergence benefited from the global "great monetary easing": investment institutions with nowhere left to deploy capital in the internet space simply replicated internet playbooks in the consumer sector. Yet new consumer brands failed to reproduce the investment myths of the internet era for these institutions. Countless star companies collapsed before reaching an IPO, and the wind died down abruptly.

In the relatively mature US market, exit channels include M&A, secondary transactions, and various other forms; IPO exits account for only about 5% (primarily among PE funds). China, by contrast, is a venture capital market highly dependent on a single IPO exit path — VC and growth funds rely on IPOs for 90% of their exits. With the A-share market's red and yellow lights, Hong Kong's liquidity crisis, US policy restrictions, and IPO markets elsewhere facing their own problems, the entire primary market has had to confront a stark reality: everyone is facing a market that has nearly frozen solid.

Where has the liquidity gone?

Liu Zizheng, CEO of Yongchuan Asset, told Dark Tide Waves, "The essence of the liquidity problem isn't scarcity of money — it's the end of an era of high leverage across the entire market."

In his view, without consensus-backed, high-growth assets, the market has developed fractures at several critical connection points, and the problem of equity monetization has erupted all at once. "If one person stops playing, the hot potato can skip them. When a whole group behind them stops playing, the game is over."

This is essentially a major problem hidden within the core of equity investment: there is no connection between capital and quality cash flow. Capital does not profit from quality cash flow; it profits from the接力 of excellent capital.

In the last era, internet companies had unlimited ceilings, and the investment institutions backing them could carry asset management scales ten times that of classic VC. But when the platform-type expansion driven by equity investment reached its end, this investment approach also hit a bottleneck.

Perhaps we can approach this problem from a different angle: Are there other, more liquid exit methods? Or, which industries with high-liquidity cash flows might be suited to venture models beyond equity?

Both Ends of the Pipe

Micro Connect, which just completed a $458 million Series C funding round, is attempting to answer this question.

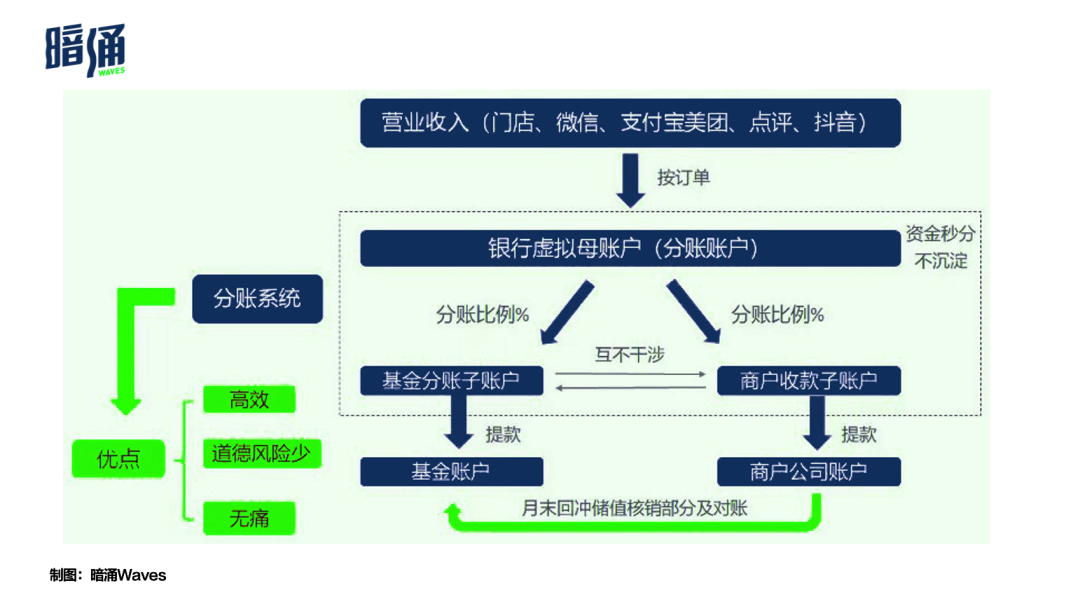

Founded in 2021 by former HKEX CEO Charles Li Xiaojia and Tung Shing Financial founder Zhang Gaobo, Micro Connect positions itself as an "innovative investment and fintech company." In its official description, the company's greatest "innovation" as an investment firm lies in its departure from the market-dominant "equity" financing path, instead adopting "Daily Revenue Obligations" (DROs) — an approach that specifies investment amount, joint operation period, and revenue-sharing ratio.

Several core elements enable this model: (1) targeting physical business owners in dining, retail, culture and entertainment with stable cash flow; (2) investing in individual stores rather than companies, with single-store investment not exceeding 40% of total store investment; (3) requiring both brand and store to have a certain foundation.

The key to successful equity investment is taking high-premium, multi-round bets on high-growth assets, then exiting immediately upon reaching scale. Micro Connect's model shifts from pursuing "equity appreciation" to pursuing "daily revenue."

This novel investment approach has already been explored in the US, where it's known as Revenue-Based Financing (RBF). Representative companies include Pipe, Velocity, and Clearco.

Among them, Pipe — which bills itself as the "Nasdaq for Revenue" — has been the hottest new financial company in the US in recent years. By providing financing to companies with recurring revenue and sharing in that revenue, Pipe became a unicorn in less than a year. Founded in 2019, the company's name means exactly what it suggests: a pipe — not unlike Micro Connect's own metaphor.

If the foundational logic of equity investment is "sharing the target entity's profits periodically and proportionally," then the RBF model introduces three key changes: first, instead of sharing profits, it shares revenue; second, instead of perpetual profit-sharing, it gets priority sharing with a defined exit; third, financing use is restricted to operating activities that generate cash flow.

(Comparison of equity investment and RBF differences)

RBF is an "equity-like investment" that sits between debt and equity — essentially a mezzanine product. It requires assets with three characteristics: (1) recurring revenue, meaning relatively stable cash flow; (2) high certainty, with predictable future cash flow; (3) clear, verifiable revenue.

These requirements make physical stores (Micro Connect's primary investment targets) particularly suitable for RBF investment. Under RBF logic, a financial product called RSO — Revenue Sharing Obligation, or revenue-sharing right — has also emerged.

What is RSO?

The essence of RSO is connecting capital with operating cash flow. Through investment, it helps build or enhance the target entity's ability to generate cash flow, then obtains the right to share in that incremental cash flow. For example, investing in a restaurant store and sharing a portion of that store's revenue over a certain period. Unlike traditional equity investment in a parent company, which takes the full profit and loss of all chain stores, RSO invests only in a single store and relates only to that store's cash flow.

RSO has two phases. Briefly, RSO-1 is the capital recovery phase; RSO-2 is the return phase. From a fund's perspective, the most important metrics are IRR and DPI, so recovering the principal is the highest priority.

The entire logic is derived through reverse calculation: guaranteeing LPs DPI = 1 within 12 months, so the investment amount in a store is placed on the right side of the equation. Based on due diligence of the store's average monthly revenue in year one, a conservative revenue estimate × phase-one deduction rate × 12 months ultimately equals the investment amount for that store.

(RSO-1 phase deduction rate calculation logic: most conservative revenue figure × deduction rate × 12 months = final investment amount)

Take Yongchuan's investment in a store of Dashu Restaurant, a modern Cantonese cuisine brand, as an example. With estimated monthly sales of 2 million RMB and a mutually agreed 17% deduction rate, 340,000 RMB can be recovered monthly from the start of operations, reaching the 3.88 million RMB investment amount in 11.4 months.

In the restaurant industry, premium assets that recover capital in 12 months represent roughly the top 10% — hardly a miracle. But translate this into LP-facing language: DPI > 1 in 12 months, and it takes on greater significance for the investment industry.

RSO-2 is the return phase. Based on the lifecycle of stores in different industries, it typically collects returns over 24-36 months at 4%-6% of monthly revenue, then exits upon maturity or when a return multiple ceiling is reached. It holds no equity in the company and provides no operational input. Tying returns solely to "revenue" avoids the complexity of other parts of the income statement, and this simplification is a prerequisite for scalability.

Additionally, the RSO-2 formula incorporates a betting mechanism — a wager with the owner on whether RSO-1 can be completed within 12 months — using a tiered return structure. This addresses the problem of actual revenue diverging from projection models.

The specific deduction method involves revenue-sharing from the moment the customer pays:

(The introduction of a digital revenue-sharing system allows RSO products to be built on a technical system from day one, providing another guarantee of scalability)

Compared to conventional loans, a notable distinction of RSO is that the transaction involves no collateral. Investments not tied to individual owners assume some risk, and require industry understanding to establish sound investment principles and risk control logic for quality store screening. This partly answers that crucial question: "Why would the best stores let you invest?"

Of course, this design makes risk control particularly important. Similar to Micro Connect's certain scale requirements for physical stores, Yongchuan has its own risk control model. For example, it uses "three no-gos" to control brand risk: no new brands, no sub-brands of major brands, and no deals where the founder hasn't invested their own capital.

More soft downside protection tools are also being introduced, one being the setting of "store closure trigger conditions." For Dashu Restaurant, the contract stipulates that "six consecutive months of losses, with revenue below a certain number, can trigger closure" — providing some buffer for both parties. However, another name for "downside protection" is investment failure. Compared to VC, the RSO model has lower tolerance for "downside protection."

Liu Zizheng told Dark Tide Waves that Micro Connect's Macau exchange will become a type of equity trading platform in the future, while Yongchuan hopes to provide underlying assets for upper-layer trading platforms.

At the end of March 2023, Micro Connect (Macau) Financial Assets Exchange (MCEX) launched. Sources say that after a trial operation period, MCEX is about to officially open, becoming the world's first licensed DRO product exchange. If Micro Connect shifts its focus to the trading platform in the future, the underlying assets will open more space for new entrants to fill — such as restaurant chains and other targets that Micro Connect avoids for various reasons.

Crossing the Drake Passage

Though RBF currently appears best suited for physical stores, in the US it has already been applied across industries. Whether offline or online, physical or virtual, wherever there is revenue, there is potential for revenue sharing. Applications include copyrights and technology. A relatively well-known success story is Royalty Pharma's RBF investments in the biotechnology field.

Royalty Pharma was founded in 1996. While typical VCs invest in biotech startups one by one, Royalty Pharma chose to make RBF investments in promising drugs. The company does not seek equity in the institutions that own these drugs; instead, it invests in exchange for a share of future sales revenue from these drugs. Since the inventors of these drugs often come from universities and other research institutions, they typically license drug patents to commercial companies for development, earning royalties in return.

In June 2020, Royalty Pharma listed on Nasdaq, raising $2.2 billion — one of the largest IPOs of the pandemic year.

Liu Zizheng believes that while RBF was previously considered merely an "equity-like investment," it is actually becoming a more fundamental "settlement method" — a new settlement method parallel to equity.

"In the past, we rarely challenged the world beyond profit settlement, just as we didn't know what lies beyond the Drake Passage. But in the future, we have two choices: equity, or RBF?" Liu Zizheng told Dark Tide Waves. "This isn't just an opportunity for offline retail — it's an opportunity for the entire investment industry."

Hou Wang and Duan Xinbin of Tsinglaw Law Firm studied eight RBF investment institutions including Lighter Capital, Wayflyer, Uncapped, Arc, Pipe, Viceversa, Liberis, and Outfund. They found these institutions share common characteristics: established around the past five years, they raised substantial capital in short order; their founders typically have financial industry backgrounds, and their co-founders often have experience at internet companies, familiar with e-commerce and SaaS operations. The study concludes that internet platform companies, large industrial companies, private equity investment institutions, financial institution asset management businesses, and commercial banks are all domestic entities with potential to engage in RBF.

However, RBF has only just emerged. As a new "operating system," it will face many market challenges. For investment institutions, beyond lacking collateral and holding only equity-like rights, RBF also has a clearly visible return ceiling. Tsinglaw's research also notes that RBF has not yet taken off domestically, and regulators have not yet turned their attention to it.

Compared to the sweeping "internet + equity investment" era, the growing recognition of RBF — from Royalty Pharma and Pipe to Micro Connect and Yongchuan — carries a certain inevitability. In the equity investment era, what captivated people most were legendary stories like Kathy Xu and Richard Liu, or Richard Liu Qin and Lei Jun: meeting when unknown, mutual admiration between heroes, accompanying each other to success. But when the external environment changes dramatically and people's tolerance for risk and uncertainty grows ever lower, accelerated capital recovery and defined exits may not be a bad new way to survive.

Staying alive — stay in the game — is also a form of long-termism.

Disclaimer: The information and views provided in this article are for reference only and do not constitute any investment advice.

Image source: Visual China

Layout: Du Meng