The Making of a Restructuring S Deal

New Alliance has partnered with SBCVC.

By Qian Ren

Edited by Jing Liu

Another S-Deal Crosses the Finish Line

An Yong Waves recently learned that SBCVC and NewLink Capital are nearing completion of a fund restructuring deal worth hundreds of millions of RMB.

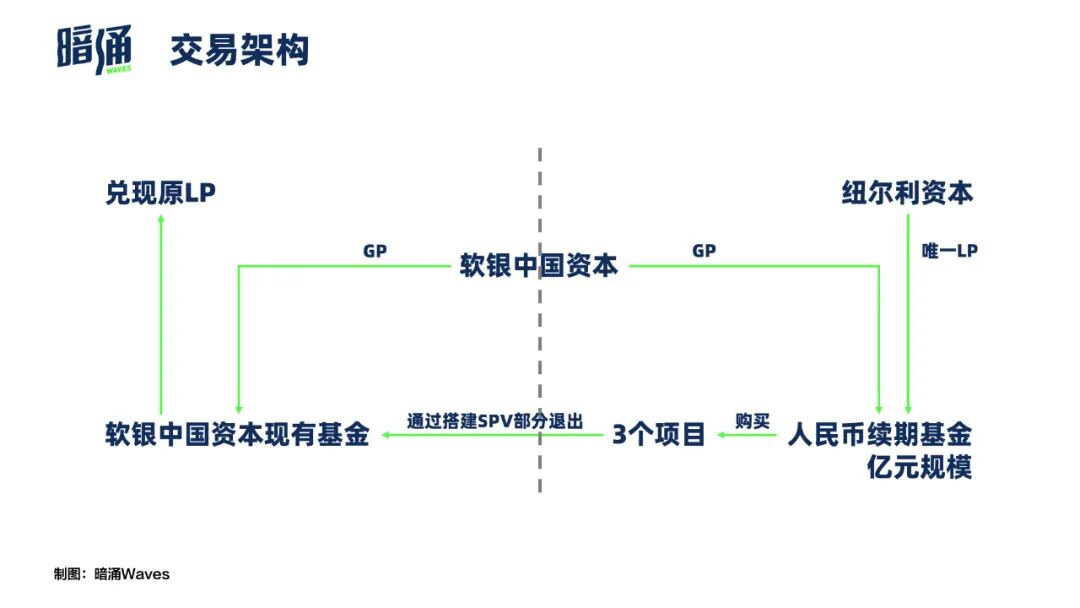

Under the specific structure, SBCVC will transfer three remaining portfolio companies from its existing fund into a new RMB continuation fund. NewLink Capital, as the buyer, will become the sole LP in the new fund, while SBCVC continues to serve as GP managing it.

Restructuring is undoubtedly the most complex type of secondary transaction. Unlike the more common LP stake transfers, the GP (general partner) typically initiates and leads continuation funds: the GP and an S-fund (buyer) jointly establish a new fund that acquires all or part of the underlying assets from the GP's existing fund. Original LPs can choose to exit through the transaction or roll their interests into the new continuation fund.

For an S-deal to actually close, it must create wins for multiple parties — cash distributions for existing LPs, DPI for the GP, and returns for new LPs.

The initial companies involved were Bluesail Technology, a polymer functional new materials company (invested in 2018), and Revopoint, a high-precision 3D camera hard tech firm (invested in 2016). A third company, a growth-stage semiconductor firm, was added later.

NewLink had already formed judgments about these portfolio companies and conducted due diligence. Upon engagement, it immediately modeled expected returns and proposed a packaged restructuring solution. Only after both sides reached consensus did they proceed to negotiate the finer details.

Unlike the motivations behind many S-transactions, SBCVC was not facing imminent fund expiration pressure at the time, nor was it rushing to offload underperforming assets. On the contrary, both projects had already generated multiple returns for their respective funds. Considering fund lifecycle and DPI, SBCVC communicated with existing LPs and decided on a partial exit. And as both companies continued to grow, there remained significant upside for the S-fund.

"Considering active portfolio management and overall fund performance, we chose to work exclusively with an LP we had a trust-based relationship with," SBCVC investor Bofeng Liu told An Yong Waves. "Both sides approached the process with maximum sincerity and an open mindset, doing everything possible to find common ground."

The choice of fund restructuring was designed to maximize LP value more quickly, fit within LP internal decision-making mechanisms, and serve as an exit pathway.

Notably, unlike many underwater stake transfers where founders remain unaware, NewLink Capital engaged in deep conversations with the founders during due diligence and was thoroughly familiar with LP exit motivations.

This relied in part on SBCVC's influence and trust on both sides — having been an early investor in Bluesail Technology and Revopoint, while also understanding original LP internal decision mechanisms, which allowed greater flexibility in project selection.

"Our cooperation with NewLink was a restructuring transaction, and it went very smoothly," SBCVC managing partner Ping Hua said publicly. "First, you need to communicate thoroughly with existing LPs, asking about exit preferences at appropriate financing milestones. Second, NewLink had sufficient trust in the SBCVC team. Third, the selected underlying assets were all star companies with prior round valuations as reference points, so everyone could easily reach consensus on market-based pricing. Execution was much faster than internally expected, without many obstacles."

The Art of Mutual Benefit

China's S-market began rapid development in 2020, with transaction volumes rising in a spiral pattern and reaching a peak in 2022: ZERONE data shows 405 cumulative transactions that year with total deal value of 102.145 billion RMB, the latter up 52.90% year-over-year.

Following 2022's intensity, many institutions did enter 2023 with greater enthusiasm for S-deals, but multiple practitioners told An Yong Waves, "Transaction volumes are declining, likely below last year's level." Several notable shifts emerged this year: beyond "convergence" in investment themes and capital sources, deal motivations and tactics have become more "deepened."

This means S-transactions have evolved from a relatively passive investment approach, such as stake purchases, to a model requiring more proactive capabilities.

We discussed in our article "The Hidden Secrets of the Primary Market" that S-transactions have long faced an irreconcilable tension: sellers want to bundle in and dispose of poor-quality assets, while buyers only want to cherry-pick the best.

This directly caused many deals to collapse during early negotiations. Breaking up packages for different buyers to purchase different assets inherently increases transaction complexity and post-deal management difficulty.

The NewLink-SBCVC transaction, to some degree, offers a model for balancing stakeholder interests and actively managing exits: the seller became willing to proactively release purely high-quality assets (rather than mixed-quality bundle logic), and the buyer was willing to provide a mutually beneficial overall solution (including asset pricing, incentive mechanisms, etc.). This may push the S-market forward significantly.

Yet even with the deal ultimately closed, Bofeng Liu recalls the process was extremely meticulous. "Getting the term sheet out was the most critical step, involving project selection, allocation adjustments," he said. "From August through October last year, we basically had meetings every day, going through projects one by one."

For SBCVC, this was its first restructuring-style S-transaction. NewLink wanted to see clear exit expectations, and its restructuring strategy can be summarized as: a portfolio combining late-stage projects (safety cushion) with growth-stage projects (potential upside). From SBCVC's perspective, the quality of the two projects was strong enough to consider other transaction forms such as direct secondary sales or case funds.

"The greater advantage of restructuring transactions lies in achieving enhanced returns through project selection and term structuring — better multiples than pure stake transfers,"

Boyang Deng, NewLink Capital director and transaction lead, told An Yong Waves.

Indeed, after closing, Bluesail Technology raised nearly 200 million RMB in its Series D in February 2023, then secured a 100-million-plus RMB Series E from CICC Capital six months later. Revopoint also completed a new funding round in May 2023. This meant the new fund had paper gains shortly after the assets were transferred in.

"Doing" Is Easy, "Doing Well" Is Hard

Returning to the transaction itself, the question we most want to examine — and perhaps the most valuable one — is: can this deal be replicated at scale?

In the highly non-standardized S-market, uncertainty is often the only certainty. Restructuring deals are especially so: from assets to new and old LPs and the GP, every element affects all others, requiring deeper stakeholder involvement than LP stake transfers.

"S-deals are indeed not easily replicable; they demand comprehensive team capabilities," Boyang Deng emphasized. "First, on the GP side, we have a multi-billion RMB fund-of-funds platform covering a comprehensive GP network, with clear understanding of fund track records — this forms the basis of trust between partners. Second, on the asset side, our direct investment team assists, giving us capability to judge quality assets across sectors and quickly provide fair pricing benchmarks. Finally, our P+S+D multi-business-line coordination also facilitates further cooperation with GPs."

Before joining NewLink in 2021, Boyang Deng worked at TR Capital. In 2020, Kunwu Capital and TR Capital led China's first RMB-to-USD fund restructuring transaction, in which Deng participated.

What lessons does this deal offer the industry? Boyang Deng summarized three: a GP with high credibility, incentive mechanism design, and the S-fund's own active management.

"In S-transactions, people tend to focus more on assets, but we are GP-centric. The new fund is still managed by the GP, so GP quality is what we value most in this type of deal," Deng explained. SBCVC and NewLink had long intersected on multiple projects, and this trust foundation was a necessary precondition for the S-transaction.

Additionally, all restructuring transactions face one problem: how to motivate the original GP to continue managing the new fund well?

"How much to invest in each project, at what valuation, how much carry to give the GP — these are all customized," Deng said, thinking more at the fund level. "First understand each asset's true situation, model returns, then discuss transaction valuation, allocation, incentive structure, etc."

Moreover, for continuation funds, original LP support and transparent communication are critical, which depends more on the GP's drive and attention to detail.

Bofeng Liu told us that GPs need to communicate carefully to secure LPAC support, including forming working groups, assigning dedicated contacts, fully disclosing necessary information, and cooperating with buyers on project work. LPs from different backgrounds have distinct characteristics: USD LPs are primarily financial investors focused on returns; RMB LPs balance investment risk and payback periods alongside financial returns. But both USD and RMB LPs emphasize transaction compliance and approval processes.

From the underlying asset perspective, since both GP and buyer conduct relatively deep due diligence on portfolio companies, the challenge is ensuring strict confidentiality to prevent information leaks while not negatively impacting ongoing or future fundraising for the companies — this requires advance communication.

Additionally, within the GP team, how to properly arrange interest transfers for the continuation fund so that its incentive mechanism doesn't conflict with the original fund's exit incentives is also crucial.

Indeed, S-transactions are becoming increasingly important in today's market environment, but this isn't an ending — it's just the beginning of multi-party cooperation.

Image source | Visual China

Layout | Xuemei Guo