The "Pinduoduo" of M&A: A New Model of Entrepreneurship Built for Investors | Entering the Game

It was a hit in the US for three decades, but remains niche in China.

**

"Entering the Game" is a recurring column from Waves. It stems from our observation that once-reliable operating models are facing new challenges, and the industry rules long inherited from west to east have been disrupted. People are urgently seeking a new landscape and new order for innovation and capital. "Entering the game" is the most precious posture one can adopt."Entering the Game" was born amid transformation.**To summarize this column's subject in one sentence: we hope to identify new players and new strategies better suited to a changing environment. This is the eleventh article in the series.

By Muxin Xu

Edited by Zhiyan Chen

A new institutional form is emerging in China. It could make the recently much-discussed wave of M&A transactions no longer solely the domain of "big players" — listed companies, government-backed SOEs, or buyout funds — but instead a new survival opportunity for frontline investors. Its name: the search fund.

Searching for "Stable Returns"

To set up a search fund, simply complete the following steps:

Step one: raise several hundred thousand dollars from prospective LPs or friends and family, promising to find a "suitable company" within two years. This capital covers living expenses during the search period.

Step two: once a suitable company is found, raise additional capital from the market based on its valuation; acquire the company and become its controlling shareholder.

Step three: operate the business for five to seven years, increase its value, then sell the company and exit.

This closely resembles a traditional M&A transaction, but because search funds target much smaller companies, some jokingly call them "the Pinduoduo of the buyout world." In this process, the fund sponsor acts not merely as an investor, but as the operator and manager of a business.

For search fund entrepreneurs — known as searchers — this approach sits somewhere between starting from scratch and intrapreneurship. Compared to the former, it avoids the uncertainties of going from zero to one; compared to the latter, it maximally preserves entrepreneurial passion and autonomy.

This model of acquiring a mature company as a starting point for entrepreneurship originated in the United States. In 1984, Harvard Business School professor Irving Grousbeck first proposed the concept. As an innovation in financial modeling, he later guided his student Jim Southern to raise a search fund and complete the acquisition of Uniform Printing. Over ten years, Southern reformed the company, growing its business continuously. At exit, the investment's ROI was 24x.

Bringing the lens back to China's business context, search funds have begun to show faint signs of fertile ground.

The market currently contains no small number of family businesses in an awkward position. On one hand, they have stable operations but limited growth potential, making them unattractive for equity investment; their valuations are also relatively small, mostly under $50 million, disqualifying them from traditional M&A transactions. On the other hand, these companies are urgently seeking successor managers. Data shows that nearly 3 million family businesses in China are entering an intergenerational transition phase, yet among those in traditional manufacturing, only 10% of younger generations are willing to take over the family business.

Meanwhile, as the primary market has continued to reshuffle in recent years, some experienced investors find themselves in career turbulence. And the current fundraising environment, dominated by state capital, makes it difficult to launch new institutional brands. Against this backdrop, whether investors aspiring to become GPs or more market-oriented capital are seeking viable new opportunities in the primary market — supply and demand are nearing equilibrium.

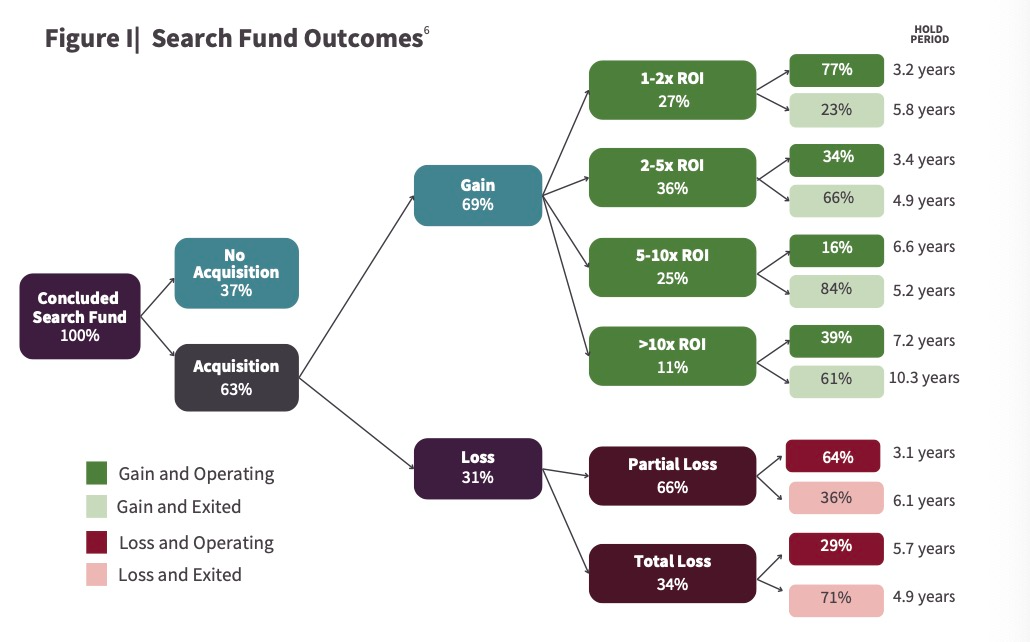

In 2021, after leaving a private investment firm, Yiqiao Wang chose to continue his studies and encountered the search fund model at Yale School of Management. He discovered that after three to four decades of development, search funds in the U.S. had reached maturity. Stanford Graduate School of Business's 2024 Search Fund Study showed that 94 new search funds were launched in the U.S. in 2023, a record high. Stanford GSB attributed this to "the stable returns and success rates that search funds have historically delivered."

Historical returns of search funds. Source: 2024 Search Fund Study

Stable returns stem from two sources. The upside of a search fund is capped only by the entrepreneur's personal capabilities, while the downside risk can be controlled through precise financial analysis and upfront due diligence on the target company. From this, it's also clear that for search funds, the search phase — the process of identifying the right target — may be the most critical.

Yet among so many new searchers, Chinese remain rare. Wang explains: "Search fund acquisitions often carry a sense of succession, so trust and emotional connection between buyer and seller are extremely important. Based on experience, locals in any country find it easier to raise capital and search successfully, and in the U.S., whites still comprise over half."

Precisely for this reason, Wang returned to China in 2023 and founded the Search Panda™ community, aiming to aggregate entrepreneurs and investors interested in launching search funds in China, along with industry veterans, academic mentors, and service providers. Currently, the ecosystem community has roughly 20–30 members explicitly committed to founding search funds.

Wang told Waves: more and more prospective search entrepreneurs are joining, with topics of universal interest including M&A and value creation for SMEs, and each person is attempting derivative models of search funds from different starting points — self-funded searches, serial acquisitions, holding companies, SPACs, accelerators, and more.

Although search funds remain in a very early stage in China, as we discussed in "Countless Lies and One Truth About M&A in China", China's objective environment has already produced numerous factors supporting the arrival of an M&A wave, and search funds, as a lower-threshold form of mini-M&A, allow more people to enter the game.

A Crack, An Opportunity

Compared to generalist blind-pool funds, where the core competencies evaluated are portfolio construction and asset management, operating a search fund requires search and operational skills. The process of searching for and acquiring a company generally takes 1–2 years. The searcher begins sourcing targets, conducting evaluations, sending letters of intent and performing due diligence, optimizing strategy throughout, maintaining multiple potential deals simultaneously to avoid a single failure derailing the entire process. Additionally, they must prepare to demonstrate the project's attractiveness to investors and creditors, and negotiate protective provisions with sellers. Beyond certain strategic considerations, or in relatively specialized fields like innovative pharmaceuticals, the core metric for most M&A targets is cash flow — naturally no exception for search funds. Search target cash flows can be divided into five tiers: Tier one is contractually bound recurring revenue, such as when perhaps 80% of a company's customers have signed three-year contracts. Tier two is subscription customers, whose churn rates tend to be lower — a characteristic more commonly seen in SaaS. Tiers three through five are "ordinary recurring revenue," "non-recurring revenue," and "one-time revenue."

Taking the preferences of Qianjing Search Capital, "China's first search fund," as an example, founder Xue Lin established several core screening criteria: contractual recurring revenue >70%, asset-light operations, annual EBIT > RMB 7 million, EBITDA >15%, positive cash flow for 3 years, controlling shareholder stake >70%, among others.

In the U.S., search funds favor SaaS, while some investors suggest the China market should focus more on asset-light leaders in smart manufacturing sub-sectors; other investors prefer to search within sectors they have long specialized in.

After identifying a target, the search fund formally raises capital for the acquisition. Purchase prices generally run around $15 million, and a successful acquisition-based entrepreneurship can deliver $6–7 million in returns to investors. Beyond the carried interest from investment returns, the searcher serving as CEO can also earn an annual salary between $200,000 and $300,000.

Wang told Waves that the two-year search period is the most grueling. It may require contacting 100 potential targets per month, attending numerous high-quality, high-intensity meetings, while simultaneously conducting due diligence on these prospects.

Moreover, the search period carries significant uncertainty — one-third of searchers fail to acquire a company during this phase and must abandon the effort, terminating the fund.

And the most universal pain point for China GPs — fundraising — is relatively easier for search funds. Search fund fundraising occurs in two rounds. The first round primarily raises "search capital"; because capital needs are modest, this is generally handled through friends and family. In the second round, the searcher must present 10–16 investable targets for investors to "claim," with participants receiving pro-rata priority investment rights in the acquisition round. Generally, investors at this stage have clearly defined financial investment objectives.

Lin told Waves that professors in North American business schools who teach related courses are generally search fund investors themselves, whether directly investing in their students' funds or serving as LPs in funds of search funds. "Another common search fund investor type is family offices."

Taking Ambit Partners, an investor in Qianjing's search fund, as an example — this is a private equity fund specializing in investments in emerging-market search funds. In their view, search funds' track record over the past three years has been 2x that of traditional PE/VC, and globally search funds have averaged 32% IRR. From a financial returns perspective, this is a safer returns model.

Both China and Mexico are favored targets, because they have faster GDP growth comparatively, more small and medium-sized family businesses in their economic models, and in Mexico's case possibly lower private equity penetration, fewer competitors for large transactions, and lower valuation expectations — in highly fragmented industries, rapid acquisitions can expand product range for higher returns.

Sanyi Capital is one of the few domestic PE institutions to have invested in search funds. Investment partner Kun Wang told Waves: for search funds to localize in China, industry identification and selection is one of the key factors to consider. For example, SaaS/software is a sector overseas search funds greatly favor, but it may not suit domestic market conditions. Including the complexity of China's market environment, and whether a local entrepreneur can nimbly handle complex issues involving government, clients, and other aspects — these are also the most challenging parts of localization.

After completing the acquisition and entering the operational phase, the value creation period lasts 4–7 years. The searcher becomes the controlling shareholder, establishes a new board, and invites investors to join. Because the acquired business is relatively stable, the operator won't make major changes initially; once comfortable, they can pursue business expansion, efficiency improvements, innovation, leverage adjustments, M&A integration, and other reforms.

For instance, two MIT graduates, after a year of searching, decided to acquire a Heineken ice factory in Mexico, naming it Aguafría and separating from Heineken within 10 weeks. As CEO, they decisively launched crushed ice and bagged ice for retail consumption scenarios, such as ice specifically for cocktails, priced 40% higher than standard block ice.

Thereafter, operators continuously seek exit timing, considering shareholder preferences, and monetizing at the appropriate moment. Exit methods include: sale to mid-to-large PE funds, strategic investors, IPO, or buyback. Returns distribution follows private equity's "waterfall" structure, with the searcher receiving carried interest last — the residual after all other stakeholders have been allocated — typically harvesting 17% to 30% of equity proceeds. For shareholders not seeking immediate exit, continuous dividends or evergreen funding models allow long-term holding of private shares.

According to Stanford's report, in North America, searchers' professional backgrounds are mostly finance-related, with private equity at 22%, ranking first, followed by investment banking, finance, and management consulting.

In the China market, those currently interested in search funds broadly fit two profiles: one, entrepreneurs who have undergone systematic study, began fundraising while at business schools like Harvard or Stanford, and have support from internationally renowned search fund investors. The second is senior professionals with complete M&A experience in China, deep post-investment management and exit experience, or industry and corporate governance experience.

Lin belongs to the former. She is from Wenzhou, from a Zhejiang merchant family, and was immersed in a family business with exit needs. She later enrolled in Yale's MBA dual-degree program MAM, encountered search funds, and developed entrepreneurial aspirations. She told Waves: a search fund combines two career paths. The left hand is finance — one could call it a "mini-PE." The right hand is entrepreneurship.

The latter investor type may be more numerous. Victor, formerly at a PE firm, is one example. Previously, a portfolio company of that PE firm was in need of a CEO, and Victor stepped into the role. After nearly four years of operation and management, Victor successfully sold the company to a well-known buyout fund and exited. Currently, Victor is raising a $448,000 search fund, with plans to launch in 2025. One of his search targets is "consumer supply chain enterprises in the Shanghai and surrounding areas undergoing generational transition."

In Wang's view, because China's search funds remain early-stage, it's difficult to objectively evaluate the merits of these two searcher types. But according to U.S. search fund investor experience, younger searchers have performed quite well historically. And in recent years, some U.S. funds have specifically invested in searchers with mature industry experience; while there isn't yet sufficient full-cycle data to fully validate this, the future looks promising.

China's financial markets have evolved to this point, and the primary market has seen many new strategies emerge — Case Funds, RBF (revenue-based financing), and so on. No matter how the macro environment changes, there are always those who can find investment opportunities in the cracks. Search funds in China remain in a nascent stage, and the problems implicit in the model are still numerous. For example: whether the motivation to become a searcher genuinely exists, the fundamental question of value creation in M&A targets themselves, and whether diversified exits can be achieved.

But one thing is clear: search funds are attempting to capture market-oriented capital that has long since lost interest in the primary market, through a flexible structure combining characteristics of M&A, SPVs, SPACs, and other product types. From this perspective, though search funds' future remains uncertain, they are still worth continued attention.

Image source: IC Photo