When Professors Leave the Ivory Tower: Gold Mines, Chasms, and the Fame Game

Faced with a chasm, there will always be those who take the leap.

Produced by | 36Kr Venture Capital Research Institute

Written by | Yi Zhang

Edited by | Lili Yu, Zhuxi Huang

Hunting Professors

In September 2022, after just one week of engagement with a new energy startup, Hongshan issued a term sheet.

The company was Zhonghai Energy Storage, the first venture of Professor Quan Xu, then director of the Energy Storage Science and Engineering Department at China University of Petroleum. In the critical field of energy storage technology for large-scale new energy deployment, iron-chromium flow batteries represented one of the few commercially viable solutions — and Zhonghai Energy Storage stood as the leading company in this technical approach.

Moreover, Zhonghai boasted what most investors considered the perfect founding team: academician + CTO + CEO. Chief Scientist Chunming Xu, a member of the Chinese Academy of Engineering, lent his name to the operation. His protégé Quan Xu, who led energy storage research in the academician's group, served as CTO. And the CEO was Shan Wang, a seasoned executive with multiple successful startups under his belt. This configuration represented the powerful stacking of three essential entrepreneurial elements: resources, technology, and commercialization capability.

Within three months of Hongshan's investment, Source Code Capital, Matrix Partners China, and Qingliu Capital followed with a combined investment of several hundred million yuan.

By the first half of 2022, as early-stage deals in the primary market dwindled by the day, university professors like Quan Xu had become prime targets for investors. Across dual-carbon new energy, biomedicine, next-generation information technology, intelligent manufacturing, and other technology-intensive sectors, "finding projects at universities" had become the prevailing trend.

Investors' daily work was consumed by desk research — studying papers, checking publications — and the ability to read papers and discuss technical topics with professors had become a baseline competency. They scoured for leading researchers, mapped out professor networks at major universities, even pasted up photos to get a more intuitive feel for the community. Then came the emails, one after another.

A young investor at a top-tier fund, who had executed numerous such approaches and knew the game well, emphasized to us that the email "must mention the paper title and highlight it" — "that's how you boost your success rate." So a standard outreach email went something like: "Dear Professor, I learned a great deal from your paper [title]. I hope we could find time to chat."

Behind them, their institutions also began internal restructuring. Many shifted hiring from purely business backgrounds toward combined science and engineering profiles.

Meanwhile, young and mid-career associate professors mobilized too. Some teachers with industry-academia project experience even considered diving into entrepreneurship full-time. Like Quan Xu at China University of Petroleum — a 36-year-old PhD from the University of North Texas — who, beyond his teaching and research duties, poured all remaining energy into Zhonghai Energy Storage. The two-kilometer stretch between the university and the Shiji Technology Tower became his most frequently traveled route over the past year. And the energy storage program he represented, riding the sector's wave, had gained 20 additional doctoral training slots for urgently needed talent from the Ministry of Education that year.

Professors wielded enormous industry influence and extensive networks; with an academician at the helm, partnerships with industry ran more smoothly. For a moment, universities were seen as rich mines for quality startups.

A Gulf

But within six months, the enthusiasm for "finding entrepreneurs at universities" began to cool.

Investors realized the ROI on this "treasure hunt" was abysmally low: the vast majority of mapped professors were not viable candidates with clear entrepreneurial intent.

The young investor from the top-tier fund told Anyong Waves: "About 50% of professors are willing to talk after receiving the email, but those who actually start a company? Extremely few." The constraints were numerous — "I have a family to support," "the risk is too high," and other practical considerations. One investor sighed to Anyong Waves: "The scientific community's incomprehension of business is shocking."

For many scientists and professors, the sentiment was more mixed. On one side, a louder voice argued that "scientist entrepreneurship is essential for achieving national innovation-driven development." But others actively resisted the "scientist entrepreneur" label. One university professor who had supported students in incubating numerous startups believed that so-called technology transfer was a false proposition from the outset, detached from market considerations. And Yigong Shi, who had left Tsinghua University, noted in a speech that scientists going into business represented a misallocation of talent.

Of course, this gap stemmed from the vast chasm between research and commerce. And investors' search for scientist entrepreneurs was a process of constantly running into problems.

Some professors, for instance, would apply academic ranking logic to company valuation — "My student's company is thriving, how could I possibly fail?" or "My junior's company has such a high valuation, why is mine lower?"

Or after funding closed, only technical staff would be in place while other core members remained missing — "I just provide the technology; you investors figure out strategy and find talent." Or after finally reaching Series B, the technical founder would need to step away mid-stream because academic duties were too demanding...

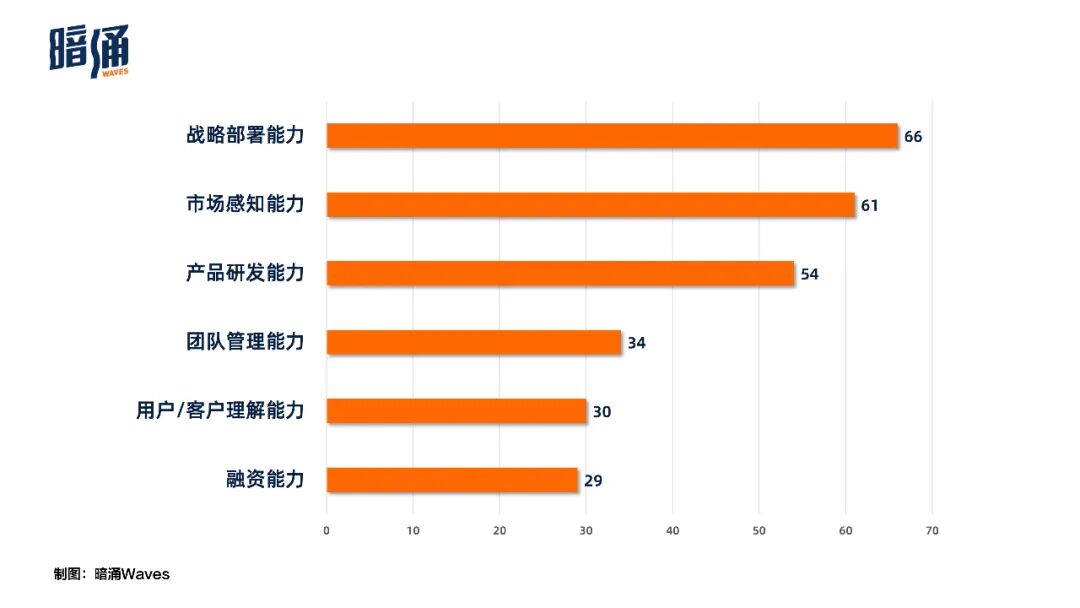

So what is the most critical entrepreneurial capability for professors and scientists?

To answer this, Anyong Waves launched a survey questionnaire to over a hundred companies. Responses clustered around six dimensions: strategic deployment, market sensing, product R&D, team management, user understanding, and financing. Strategic deployment, market sensing, and product R&D received the highest votes.

Key capabilities needed for scientist entrepreneurship

Strategic deployment, in particular, proved a brutal elimination round.

Yao Yao, founder of private rocket company Galactic Energy, told Anyong Waves that under this wave of technology innovation, manufacturing companies generally face successive hurdles: "Demo R&D is the first gate, product consistency the second. Then moving from small-batch production to semi-automated pipeline scale-up involves supply chain integration and cost control." Yao analyzed that in manufacturing, many moats aren't actually in technology. Technology might create a 12-month lead; engineering and production scale could open a 36-48 month gap. Those that ultimately break through win on production line maturity.

Team management was perhaps the most dramatic dimension.

The "academician + CTO + CEO" trio model, as in Zhonghai Energy Storage's case, didn't guarantee smooth operations. Because looming over all three was a fundamental question: who has final say, who makes the call? In a technology-dominated company, the technical lead's voice often unconsciously drowned out the nominal "commercial lead," creating situations where the "outsider" directed the "insider." The crux lay in the trust relationship between the technical lead/partner and the commercial lead — they should be equal partners, not superior and subordinate.

However, the survey found that truly complete "academician + CTO + CEO" configurations were rare. A more serious situation: many deep-tech companies failed to recognize the importance of establishing a commercial lead at all, which hampered subsequent growth for many Series A-stage startups.

The transition from school to company was itself a massive shift. "In research, the advisor chooses many topics, and masters and PhD students just follow — but company decisions require fully market-driven operations," said Professor Chao Zhong, founder and chief scientist of Baigen Biotech, in an interview with Anyong Waves.

Market sensing and user understanding were also common targets of criticism. Research and commerce sat on opposite ends of a seesaw: one side's ultimate purpose was conclusions and achievements, the other's was satisfying customers and markets as much as possible. Those who could simultaneously understand both mental models and balance them were exceedingly rare.

Limited time and energy prevented the seesaw from ever fully balancing. Guoqiang Chen, Tsinghua University School of Life Sciences professor who also serves as founder and scientific advisor of MicroConstruct Factory, told Anyong Waves: "The company handles small problems itself; only the truly intractable ones get escalated to me, which might become fundamental science questions. Normally I'm mainly organizing lab basic research at the school."

In our survey, the question "What do you see as the greatest commonality between research and entrepreneurship?" also raised the issue of time and energy investment — neither research nor entrepreneurship happens overnight. And for researchers entering entrepreneurship, they were stepping into an entirely new, time-consuming domain.

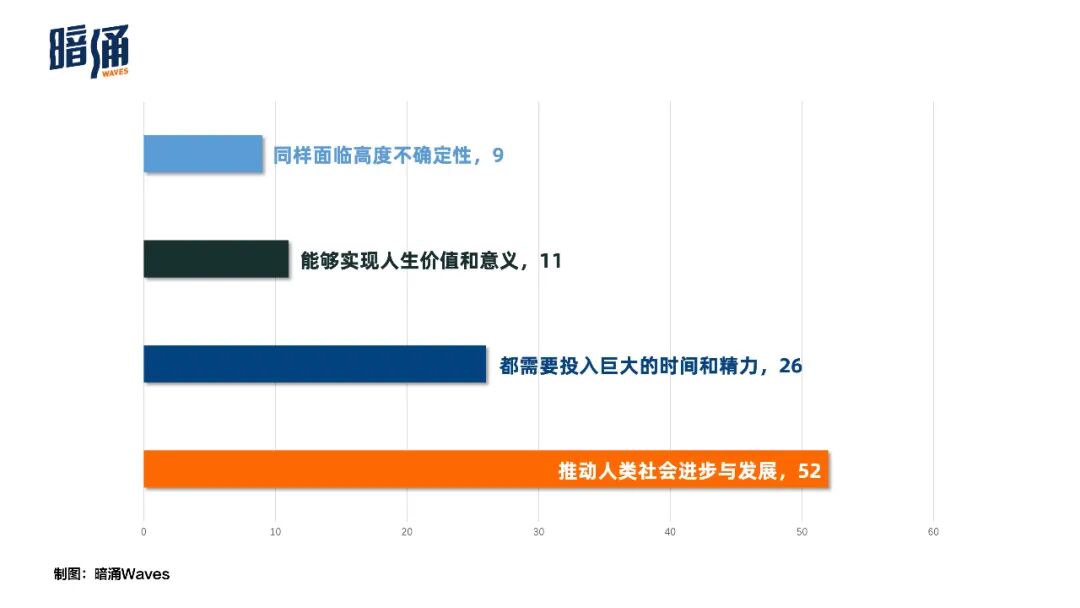

Yet interestingly, the top answer was grand in scope: "advancing human society's progress and development." Perhaps it is this level of alignment that leads many to take the leap despite the gulf.

Greatest commonality between research and entrepreneurship

N Kinds of Attempts

Even facing this vast gulf, through two months of outreach we found a group willing to stay in the arena, attempting to bridge the divide. As representatives of technological innovation emerging from Chinese soil, their existence still suggests the many possibilities of the path from research to commerce.

The search for scientists' optimal position in entrepreneurship is itself a process of self-recognition and self-breakthrough.

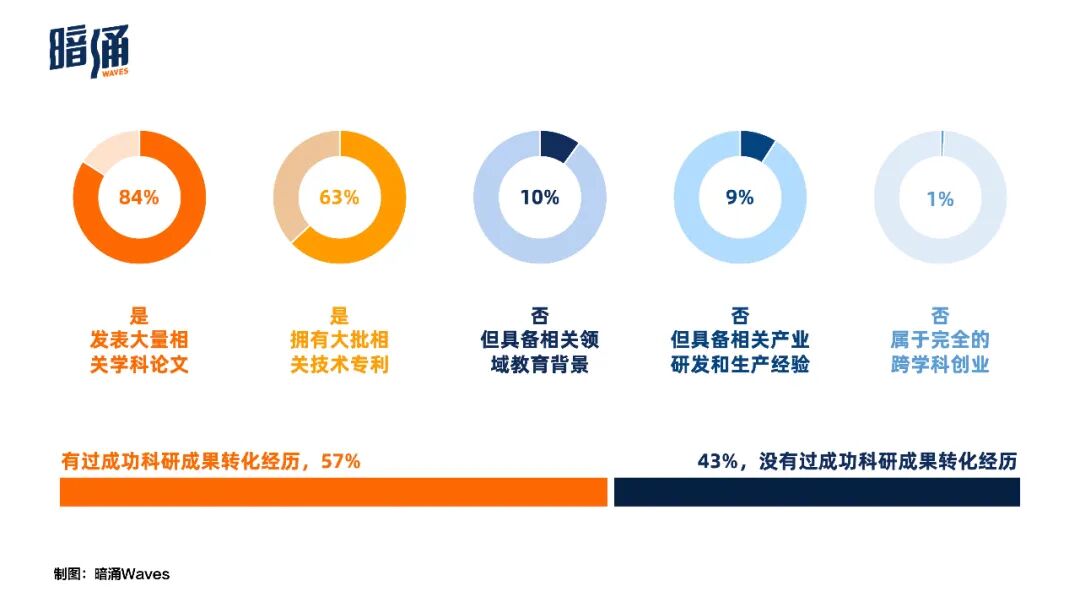

In the view of Mi Lei, founder of CAS Star, technology transfer doesn't simply mean encouraging scientists to start companies directly; many scientists are better suited as chief scientists or CTOs, with the transfer portion handled by a CEO or professional technology transfer department. Our survey results also showed that while 84% of science entrepreneurs had published academic papers before starting up, and 63% held relevant technical patents, fewer than 60% had actual successful technology transfer experience.

Whether science entrepreneurs held high-level technological achievements in their field before starting up

Notably, many companies face intellectual property conversion hurdles at their very first step. Some science entrepreneurs told us: "Universities and their affiliated foundations typically hold 5%-30% equity through IP stakes." But when companies reach Series B or C, the holding institution may suddenly demand exit for various reasons, consuming precious energy from companies still in early-stage operations. "The ideal arrangement is for the institution to package and transfer the IP outright to the commercial company at the outset."

In the survey, Galactic Energy founder Yao Yao also described his own completed self-breakthrough. In team management, for instance, with colleagues from different institutional research backgrounds and market-driven tech companies, he must do pre-communication with department heads on every decision to push everyone toward a common direction.

For investors, the crossing is equally underway.

In one tech founder's view, the cooling of the scientist entrepreneurship wave stems partly from much research still being in scientific validation stages. Projects at this stage, if financed through market mechanisms, combined with China's shorter capital market cycles compared to abroad, create excessively high commercial expectations. When expectations aren't met, market confidence plummets rapidly.

Another reality: tech investment in China remains in early development. In the above founder's view, most Chinese investment institutions transitioned from internet investing, not industry backgrounds, meaning much investment logic requires an adaptation period. In Yao Yao's view, the cognitive gap between those who've done industry and those who haven't is enormous. In lidar, for instance, building a demo and model is easy; achieving reliability, stability, and consistency across hundreds of units is extremely difficult.

Investing in tech companies differs from internet investing in another crucial way: tech investment success rates average only 5%, and if the technical path is wrong, returns may go to zero — whereas internet companies of any size may yield returns.

Beyond this, bridging the gulf requires a larger system. Between scientific research, product landing, and commercial monetization, a recent successful path transformation example is OpenAI.

In 2015, Elon Musk and Sam Altman donated $1 billion to launch OpenAI — initially purely a nonprofit AI research lab with some 60 top engineers and scientists. While making continuous contributions to AI research, they chose to publish patents and research findings without reservation, engaging freely with other organizations and researchers.

Then in 2019, to aggregate greater capital and resources and incentivize researchers, OpenAI shifted its status from "nonprofit" to "capped-profit" — with a 100x profit cap on all investments. Once it fulfilled obligations to investors and employees, it would revert to nonprofit status.

This unique and innovative organizational structure secured $1 billion in support from Microsoft and established deep collaboration with its Azure cloud platform. OpenAI ultimately broke through with GPT-3.5, GPT-4, and the application-layer ChatGPT.

This is indeed an extreme example, but it may offer Chinese startups many lessons on the path from research to commerce.

Internally, it suggests key elements of an innovative organization. Beyond wildly ambitious visions, "collaboration among top talent" and "flexible, innovative organizational structures" are important foundations and catalysts for success.

Externally, OpenAI also signals innovation's hunger for long-term, patient capital. This is indeed a key predicament for many frontier tech companies today. As China's primary market risk appetite contracts and market expectations lower, with local governments and industrial capital each having their own agendas in startup investment, capital flowing into frontier technology has become scarce.

One tech founder told us: "In the US, 30 years after industrial investment rose, some wealthy families and individual investors began providing capital to tech startups. In China, because older-generation entrepreneurs themselves lack sufficient security, plus their own indifference to technology, the notion of deploying capital to benefit technological development isn't widespread."

Among the hundred-plus science entrepreneurs we surveyed, many founding teams self-funded in early company development. One industrial SaaS company's founders sold several apartments to support R&D; one synthetic biology company's core team personally contributed millions during last year's market downturn.

Some Findings

In this observation of scientist entrepreneurship, we combined basic information collection, questionnaire surveys, and field interviews. We had many interesting findings about these science entrepreneurs.

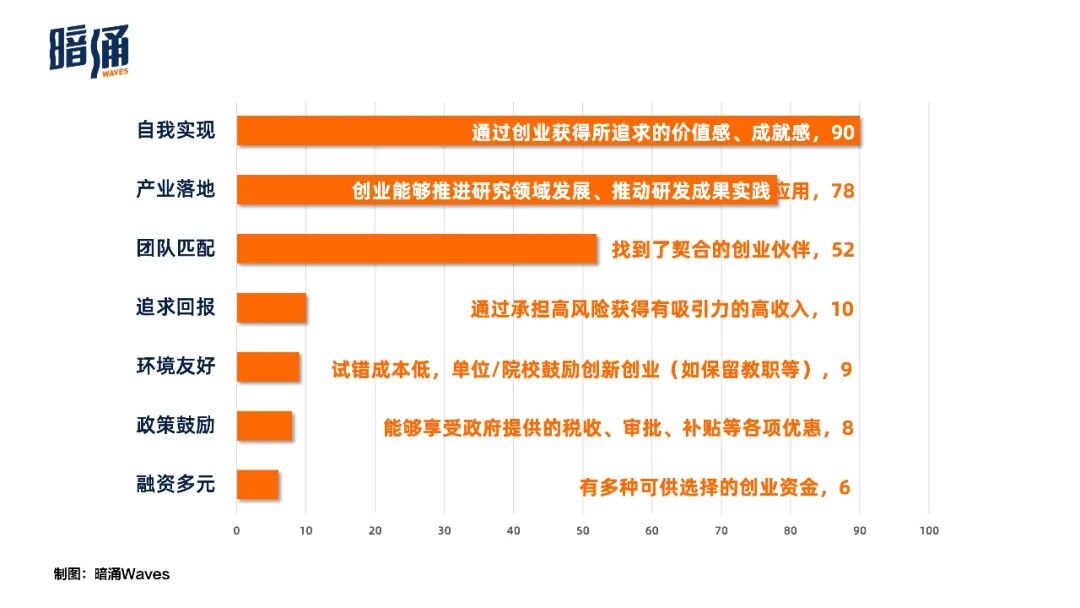

For instance, in our questionnaire survey, we found: At the outset, the overwhelming majority of scientists' motivations for entrepreneurship were "self-actualization," "industrial application," and "team match." Most hoped to unite compatible entrepreneurial partners, push research outcomes into practical application through entrepreneurship, and thereby gain a sense of value and achievement.

Key factors triggering scientist entrepreneurship

But returning to reality, when this group of science entrepreneurs self-assessed their companies: they confidently scored 8.81 and 8.82 (out of 10) on R&D level and market competitiveness, yet on revenue (6.69), profit (6.63), and orders (6.66), they indicated merely meeting expectations.

Still, traits like "courage to explore," "persistent focus," and "optimism" were universally displayed. When facing difficulties, they responded: "Enjoying it, solving problems feels emotionally exciting," and "Do my best, believe there's always a way."

In the evaluation process, we established a dual-weighted assessment system for both research and entrepreneurship —

For the research component, beyond basic innovation direction, academic rank, and alma mater, we emphasized quantitative evaluation of candidates' papers (quantity, journal tier, citations), patents (quantity and tier), and incorporated reference opinions from each candidate's recommenders.

For the entrepreneurship component, we conducted quantitative evaluation across business model, employee metrics (total headcount and R&D ratio), financials (profitability, revenue level), and funding metrics (investor type, funding stage, amount raised, and valuation), ultimately identifying these notable science entrepreneurs.

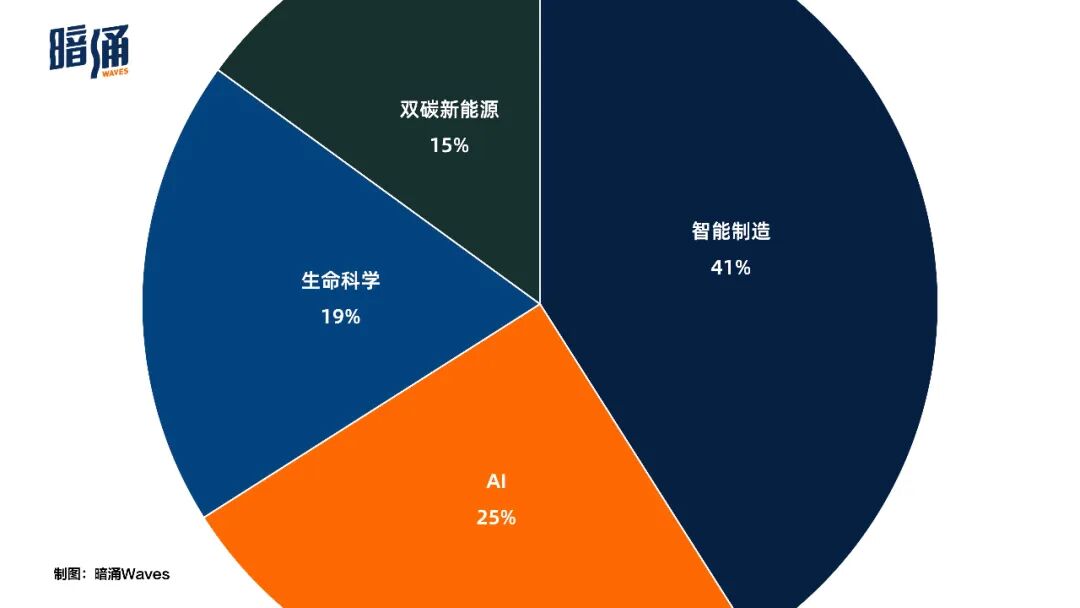

The general profile of this group: average age 40.96, with 70.12% concentrated in the 30-45 range — the most creative, mentally active years. Their companies were 41% Chinese intelligent manufacturing enterprises tackling manufacturing technology challenges, followed by AI companies at 25%.

2023 Science Entrepreneurs by Sector

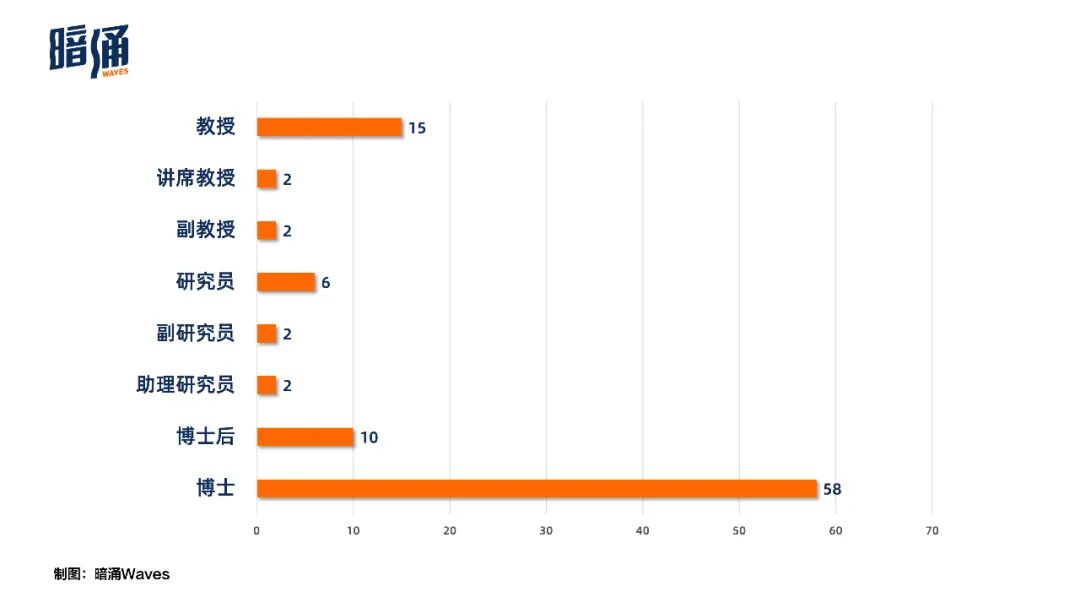

Academically, all held doctoral degrees (or equivalent research experience) or higher in their fields, with PhDs and postdocs comprising nearly 70%. They averaged 41.33 papers and 39.64 patents. 58% had studied at global top-20 institutions including Harvard, Oxford, Cambridge, Stanford, MIT, Tsinghua, and others.

From the entrepreneurship perspective, 40% of their founded companies were over five years old, with R&D staff exceeding 62%. 47 were at Series B or beyond; 64 held valuations above 1 billion yuan. Early-stage companies before Series B had all addressed chokepoint technologies to varying degrees.

2023 Science Entrepreneurs by Highest Degree

To emphasize: "2023 Science Entrepreneurs" is our first survey focused on science entrepreneurs, and our observation of scientist entrepreneurship will continue. This year's "2023 Science Entrepreneurs" awards ceremony will be held at our inaugural "Waves Conference," recently organized at Bibo Island, Jinhai Lake, Beijing. For event details, click Read More at the end of this article.

Below is the full "2023 Science Entrepreneurs" list:

About WAVES:

Image Source | IC Photo

Layout | Yunxiao Guo