When the Inventor of Unicorns Stops Believing in Unicorns

Using valuation as the benchmark for a unicorn's success is convenient, but far from perfect.

By Muxin Xu

In the fall of 2013, Aileen Lee was searching for a word.

A first-generation immigrant to America, this China-born investor had lived through days of running a restaurant to make ends meet, served as a partner at Kleiner Perkins, and was now founding her own seed-stage fund — Cowboy Ventures. She wanted a term for the kind of deal that every early-stage investor dreams of: a tech startup, less than ten years old, valued above $1 billion, and still private.

She landed on "unicorn." The word quickly swept through Silicon Valley and then the world, becoming the industry shorthand for breakthrough startup success. Yet while "unicorn" went global, Cowboy Ventures itself avoided using the term — until recently, when Aileen published a report on the fund's website titled Welcome Back to the Unicorn Club, 10 Years Later, tracking and analyzing the divergent fates of unicorns over the past decade.

Before that, though, the story of how the market itself changed.

In American venture capital, 2013 to 2021 was a golden age. Total VC assets under management more than tripled, growing by $580 billion. Over 1,000 new GPs were born, and fundraising records fell repeatedly. In 2021, peak easy money — low interest rates, a tech revolution, and sloppy due diligence driven by pandemic isolation — meant a new unicorn was crowned almost every single day.

Then 2022 arrived, and winter came without warning. As the Fed raised rates, the industry's Matthew Effect intensified: 64% of total VC capital raised that year flowed to funds managing over $1 billion. Most funds stopped writing checks; the following year, roughly 40% of VC firms ceased dealmaking altogether. Notably, Cowboy Ventures itself successfully raised $260 million in early 2023.

But the market remained cold. Highly anticipated unicorns collapsed: WeWork, the freight platform Convoy, EV companies Proterra and Embark, and biotech firms Nabriva and Goldfinch all delisted or filed for bankruptcy.

The fates of unicorns diverged widely. A decade ago, Cowboy Ventures studied thousands of VC-backed startups and found only 39 unicorns among them. Ten years later, tracking the same cohort, three had grown into super-unicorns worth hundreds of billions: ServiceNow, Uber, and Palo Alto Networks.

Back then, 60% of those 39 unicorns were consumer (B2C) companies, accounting for 80% of total valuation. By contrast, enterprise (B2B) companies were fewer in number but far more capital-efficient — 26x, or 2.4x that of consumer companies.

Ten years on, 62% of those original 39 unicorns had exited via IPO or acquisition, and 80% of the public companies had grown in market cap. Enterprise unicorns had largely survived, with average market caps six times their decade-ago levels. Meanwhile, 33% of consumer unicorns had seen their valuations shrink (such as Gilt and Lending Club), with layoffs and collapses aplenty — online retailer Zulily among them.

Here are Cowboy Ventures' six major findings, drawn from the fund's website.

Unicorn count has grown 14x, with B2B companies now at 78%

Over the past decade, the number of American unicorns has increased 14-fold, from 39 to 532, with total valuation rising from $260 billion to $1.5 trillion — yet they still represent less than 1% of VC-backed startups.

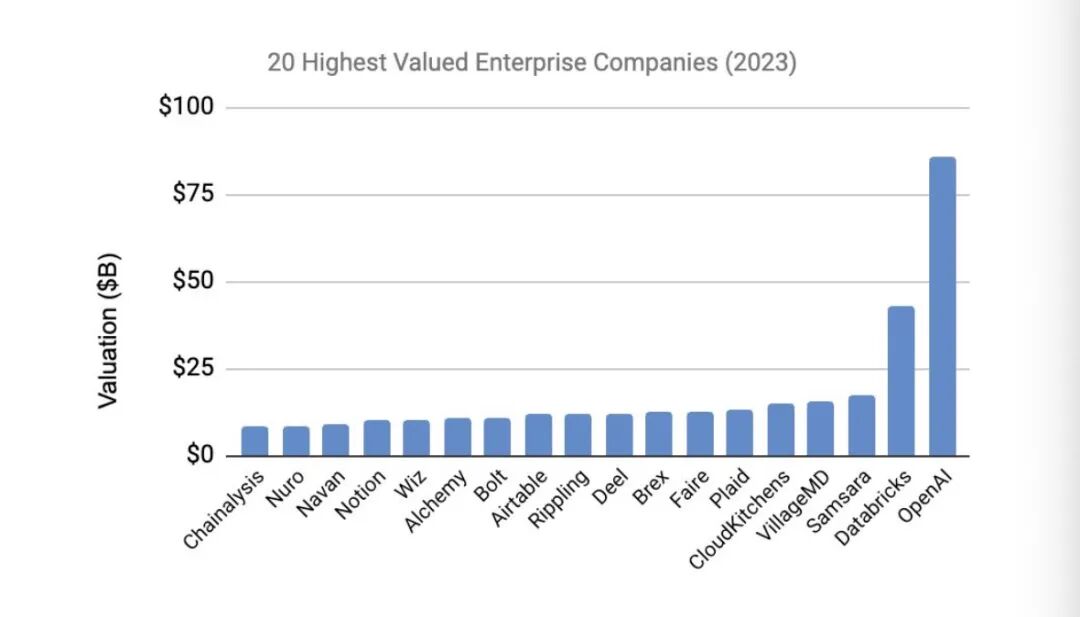

These unicorns span 19 sectors, led by fintech, SaaS, and healthcare. Enterprise unicorns number 416, making up 78% of the list and $1.2 trillion in total valuation, or 80% of the total. A decade ago, enterprise unicorns were 38% of the list with just 20% of total valuation.

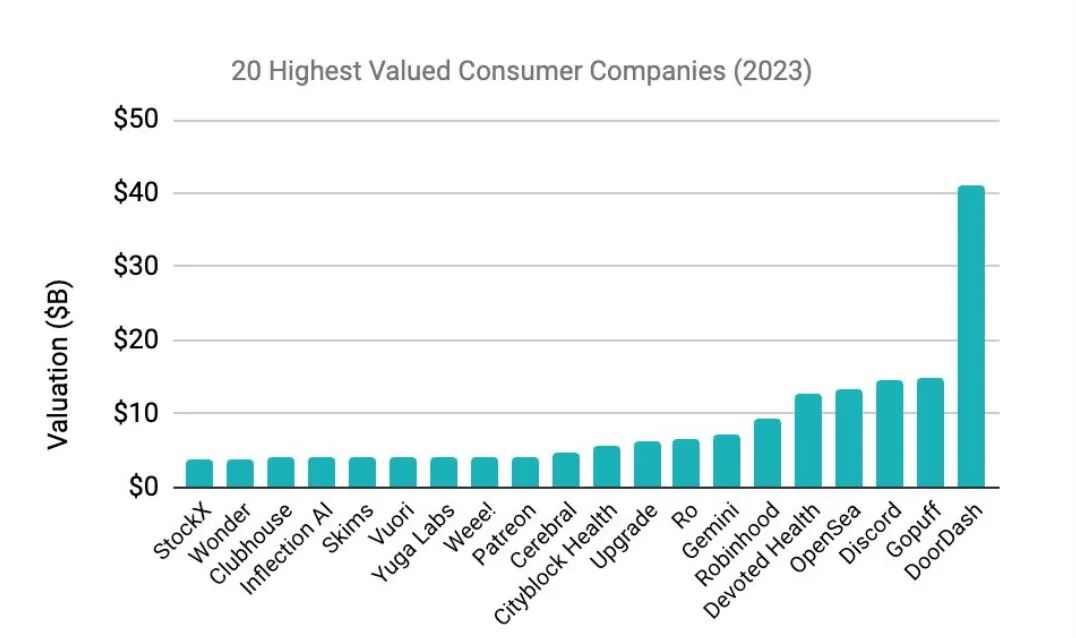

Consumer companies' share has dropped to roughly 20%. Compare the leaders in each camp and the gap is stark: in December 2023, Bloomberg reported OpenAI was raising a new round at a $100 billion valuation, while DoorDash sat at $42 billion.

(Top 20 B2B service companies by valuation, via Cowboy Ventures)

(Top 20 B2C service companies by valuation, via Cowboy Ventures)

What explains this great migration from B2C to B2B? For the past two decades in tech, consumer companies generally grew faster and commanded higher valuations than enterprise plays. Among America's five tech giants — Apple, Microsoft, Google, Amazon, and Meta — only Microsoft was enterprise-focused. These behemoths built the Web 2.0 consumer internet era. But as mobile internet penetration peaked and consumer businesses hit their ceiling, nearly all internet giants moved into B2B — including China's Alibaba, Tencent, and ByteDance. Whether incumbents or a new generation of entrepreneurs and investors, the realization has spread that the high capital efficiency of B2B represents the next growth frontier.

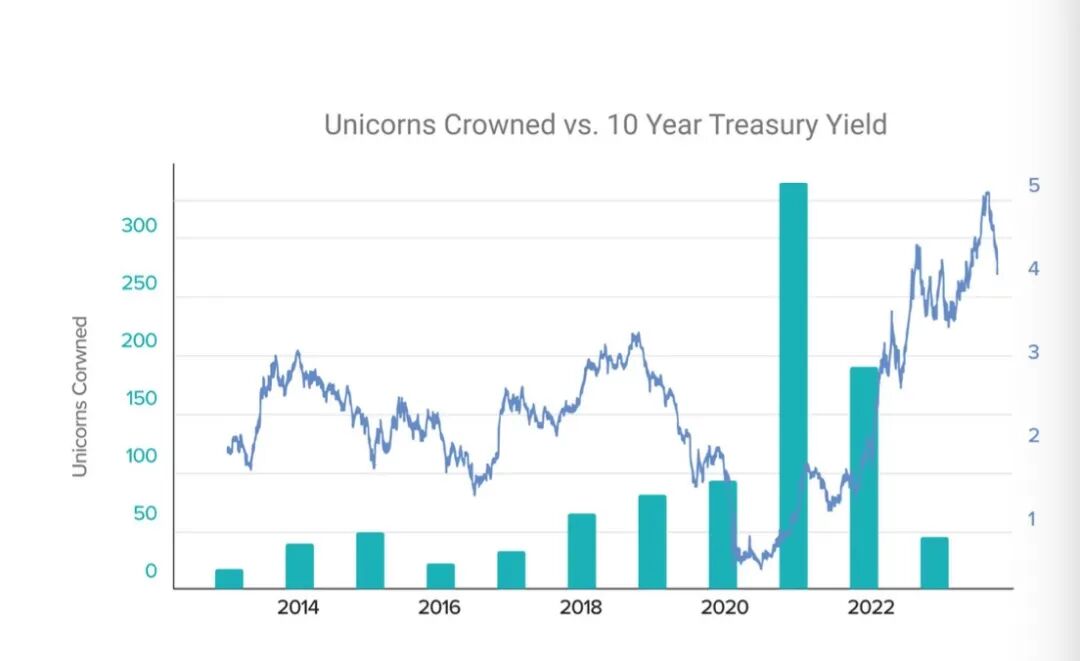

Unicorn count will briefly drop to ~350, but long-term exponential growth to 1,400 is expected

"ZIRPcorns" — unicorns spawned by zero interest rate policy (ZIRP). The chart below shows the inverse relationship between interest rates and unicorn numbers:

(via Cowboy Ventures)

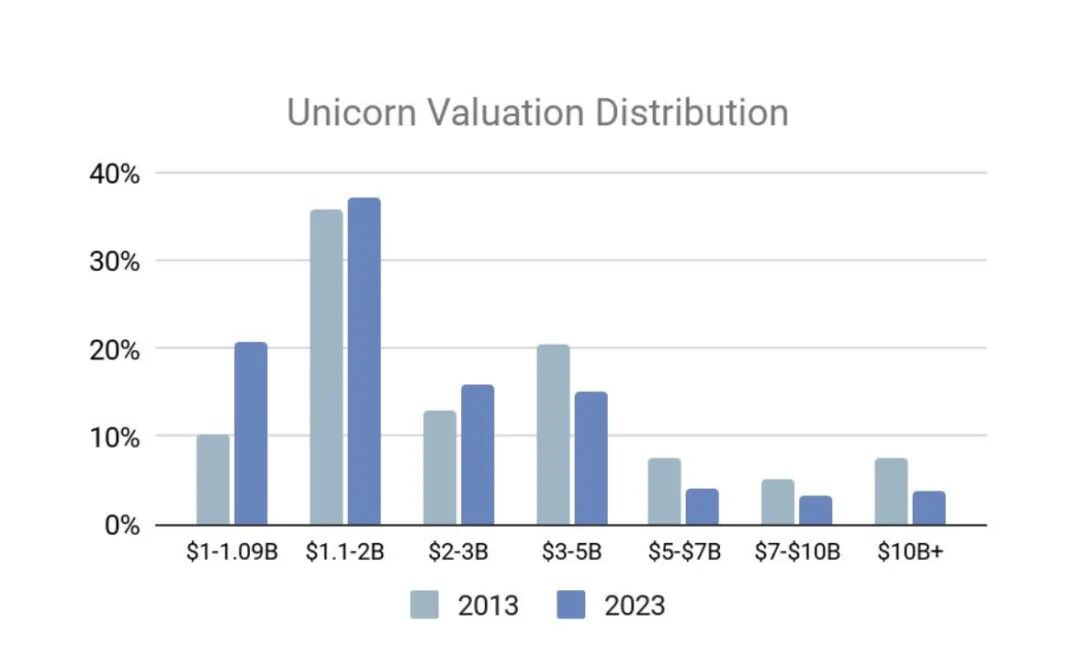

Of today's 532 unicorns, 60% are these hot-money-ripened "ZIRPcorns." As valuation bubbles deflate, these "ZIRPcorns" will come back down to earth. The data shows significant valuation compression over the decade:

(via Cowboy Ventures)

Being crowned a unicorn too quickly can be a curse. Hopin and Bird hit $1 billion in just one year; car rental company Fair took two; Convoy and Knotel took three. All have since collapsed. The average age of current unicorns is seven years — unchanged over the decade.

With investors more cautious, a hostile M&A environment, and founders resisting restructuring, 2024 is expected to bring more shutdowns. Cowboy Ventures predicts: after a wave of closures, the number of American unicorns will gradually stabilize around 350.

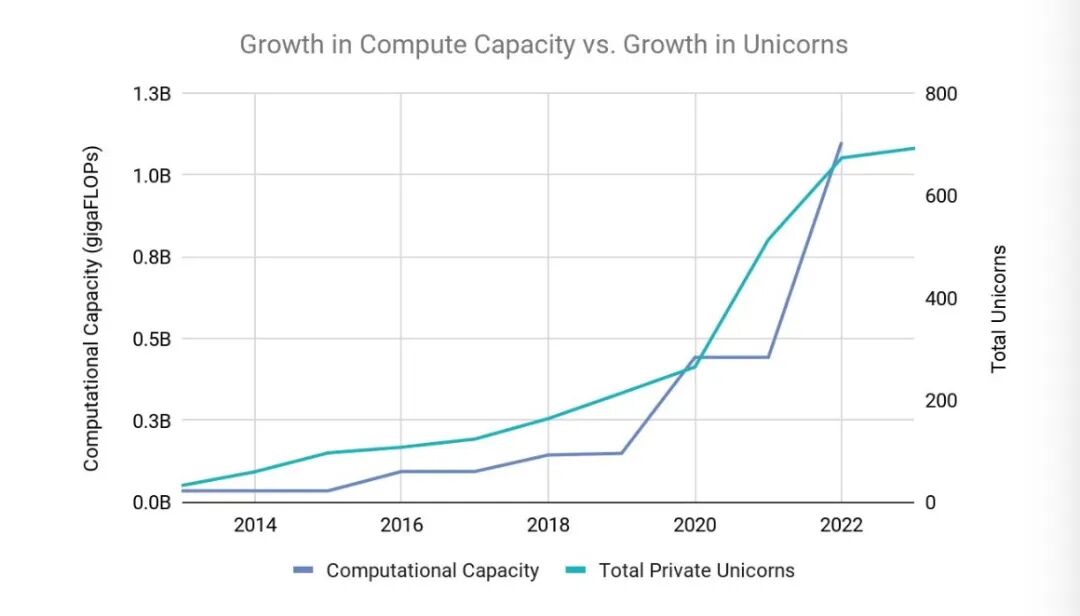

But there's good news for the long view. Looking a decade ahead, unicorn counts should see exponential growth. Here's why: despite the bubbles noted above, 350 is still 10x the number from ten years ago, representing roughly 30% compound annual growth. The power law that governs venture capital is equally at work in unicorn formation. And with breakthroughs in computing power and AI development, even if the annual growth rate drops to 15% over the next decade, a modest improvement in capital efficiency would mean North America could have 4x as many unicorns by 2033 — approximately 1,400.

(Computing power development vs. unicorn count, via Cowboy Ventures)

93% of unicorns are paper wealth only

In 2013, 41% of unicorns successfully went public. Ten years later, that figure has fallen to 3% — just 14 companies. Thus, as many as 93% of today's unicorns are merely paper wealth. Even the successful public debuts haven't been smooth sailing; over the decade, at least 20 unicorns saw their market caps fall below $1 billion post-IPO.

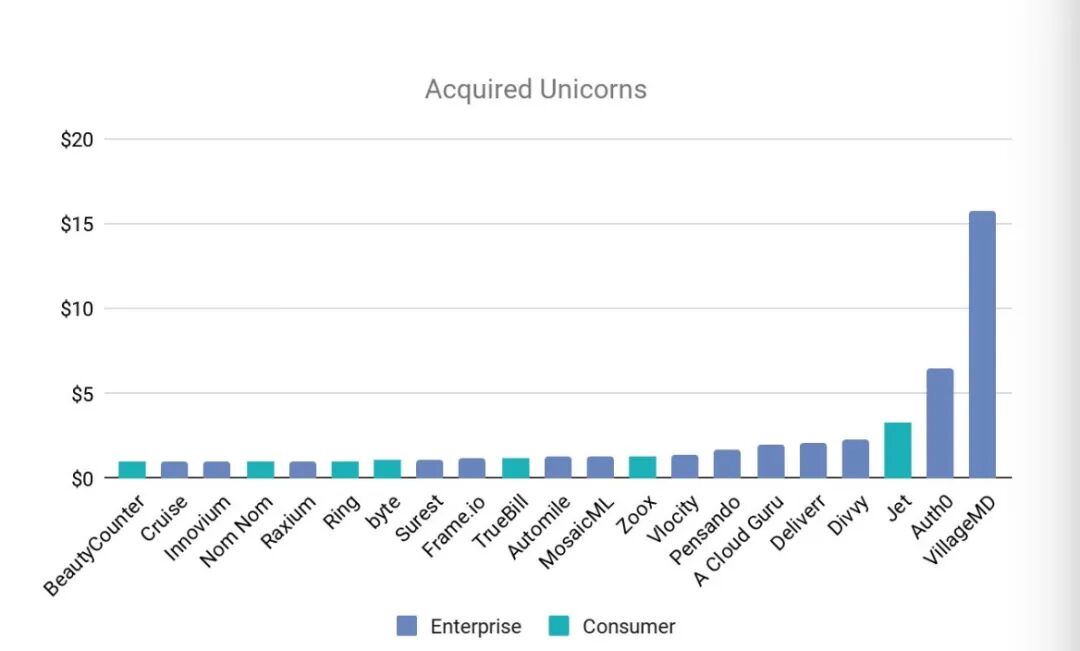

M&A represents another exit path, but success rates there have declined too. Twenty-one unicorns were acquired, or 4% — down from 23% a decade ago. Two-thirds of these were B2B companies, with an average acquisition price of $2.4 billion, roughly double the decade-ago figure.

Notably, 33% of these companies had hardware in their core business.

(Acquired unicorns and their transaction values, via Cowboy Ventures)

Another point worth noting: founders are extracting more money from their companies than before — WeWork's founders took $700 million, Hopin's $200 million — potentially creating misalignment with investors and employees.

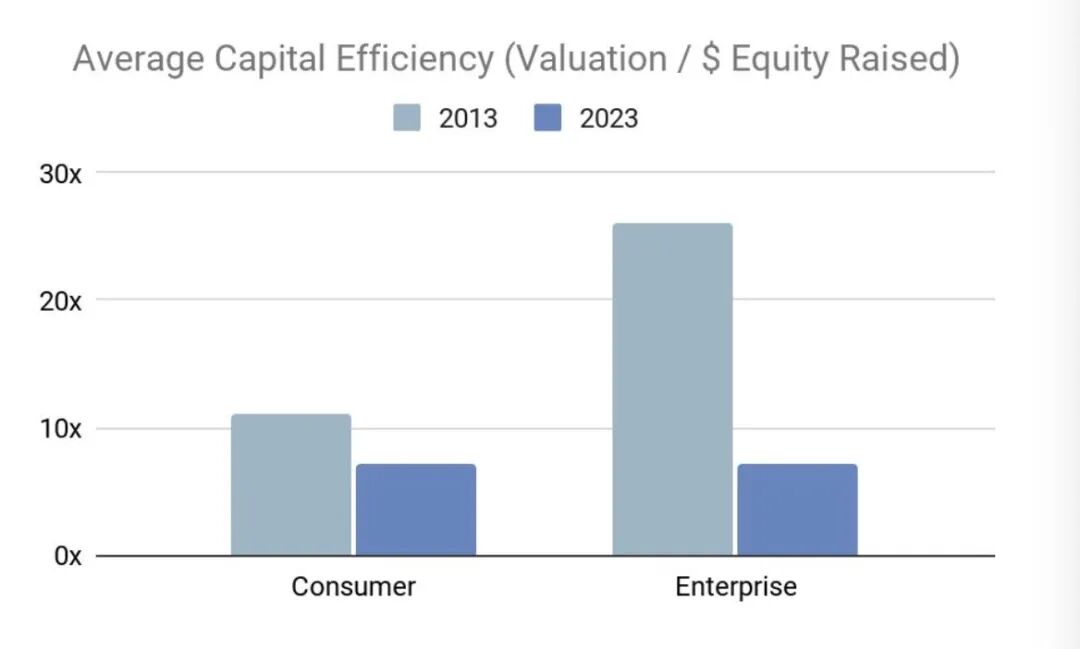

Capital efficiency has declined, especially for B2B — returns now lag buying big tech stocks

Over the past decade, tech has lost its capital efficiency edge. As shown, average capital efficiency (valuation divided by capital raised) has dropped significantly, with B2B companies falling from 26x to 7x, and consumer companies from 11x to 7x. Given the inflated valuations of many unicorns, this is arguably an optimistic estimate.

(via Cowboy Ventures)

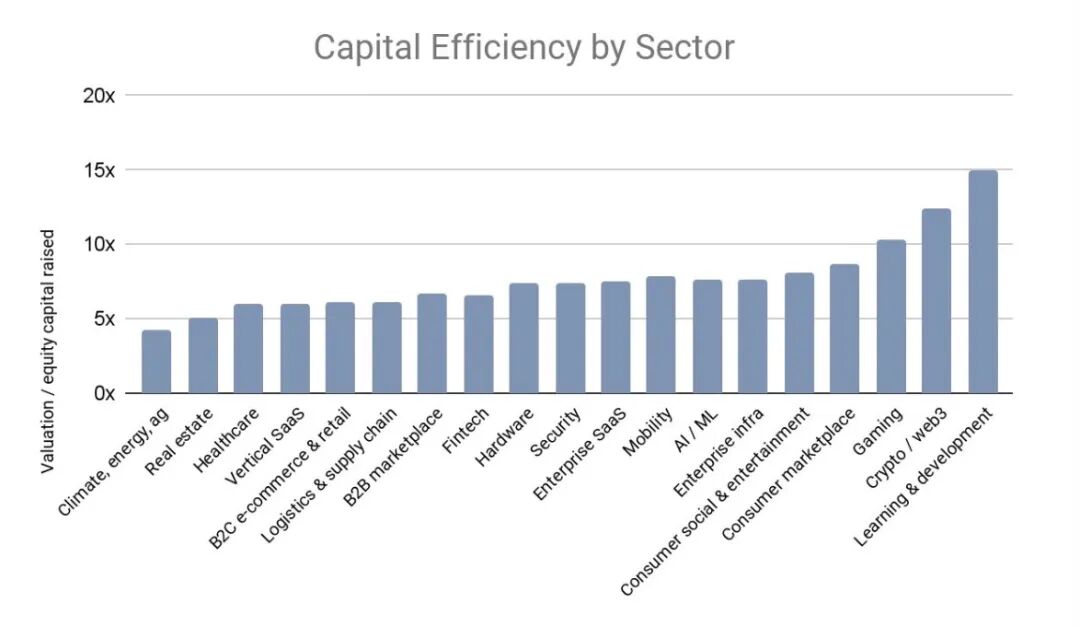

**Roughly 20% of companies on the unicorn list have capital efficiency below 4x or worse. The categories with the lowest average capital efficiency include climate/energy, healthcare, and fintech. This means that even for investors who backed numerous unicorns, actual returns may have trailed simply buying shares of Salesforce, Amazon, or Microsoft — which grew 8x, 9x, and 9x respectively over the past decade.

(Capital efficiency gaps across sectors, via Cowboy Ventures)

**There are of course home-run investments. A decade ago, Workday and ServiceNow delivered 60x returns, and their market caps have since expanded 5x and 18x respectively.

The Bay Area is no longer the sole center of gravity

**The era of unicorns clustering in the Bay Area has passed. Over the decade, Bay Area-based unicorns fell from 70% to 50% of the total. But it still hosts the four highest-valued unicorns: OpenAI, Databricks, DoorDash, and Samsara.

**Other regions are accelerating, most notably New York, rising from 11% to 19% and now home to 100 unicorns. Forty percent of these are in Web3 or fintech.

**Some unicorns, of course, choose neither. According to FlexIndex data, at least 22 unicorns have no physical headquarters at all.

But the unicorn founder profile hasn't changed much

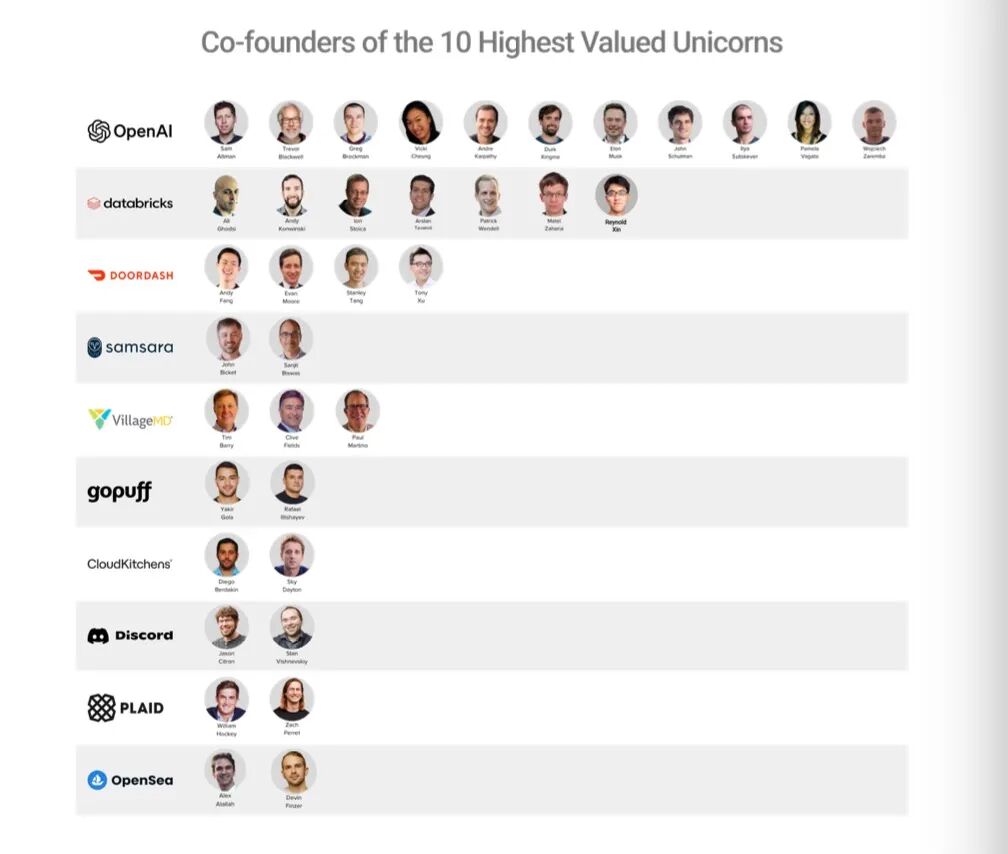

**Unicorn counts grew 14x over the decade, and founder team sizes grew roughly 14x as well. Eighty-three percent of unicorns have co-founders, down 7 percentage points; the average is three co-founders, unchanged.

(Top 10 unicorns by valuation and their founding teams, via Cowboy Ventures)

**Founders' average age at company founding is 35, up just one year — little change. Twenty-year-old college dropouts remain exceedingly rare.

**Seventy percent of founders previously worked in tech. Sixty-five percent of founding teams were classmates or colleagues, down 25 percentage points.

**Twenty percent of founders graduated from top-10 universities, down 42% — a dramatic shift. Stanford still produces the most founders, but at just 5%, down 26%.

**Ten years ago, 90% of founders had engineering backgrounds; now that's 60%, with 25% from business and 15% from the humanities.

**Six percent of founding teams have worked at Google.

**Over the decade, female CEOs rose from 0% to 5%, and female co-founders from 5% to 14%. A fun fact: there are more CEOs named Michael, David, or Andrew than there are female CEOs altogether.

Implications for venture capital amid the change

In 2013, there were 850 active venture funds; today there are 2,500. If unicorns do rapidly disappear as predicted, venture capital itself will transform: some funds will die, others will shrink.

For VCs, several lessons are worth absorbing:

**Among today's Fortune 500, fewer than 10% are considered tech companies. That share is expected to rise in coming decades, including many firms that became unicorns in 2023.

**This cycle is not over. More layoffs, down rounds, and shutdowns are coming in the years ahead.

**No one in the industry — whether by headcount or AUM — wants VC to shrink back to 2013 levels. But founders, investors, and LPs alike should learn from a decade of too much money, too early, too fast.

**Funds above $1 billion must keep playing the greater-fool game. But founders too should understand: the $1 billion "unicorn" threshold is a convenient yet imperfect measure of success. Becoming a unicorn too early can be a curse, and chasing valuation blindly leads to unexpected ruin.

References:

[1] Aileen Lee & Allegra Simon: Welcome Back to the Unicorn Club, 10 Years Later

Image source | Photo by Annie Spratt on Unsplash

Layout | Muxin Xu