Where Are the Bold State Investors?

Breaking Down the Most Active Local State-Owned Capital.

"Deconstructing the Most Active Local State Capital." By Guo Yunxiao, Huang Zhuxi, Xu Muxin, Shi Jiaxiang

Edited by Chen Zhiyan

The era of state capital in primary markets has arrived with great fanfare.

According to data from ChinaVenture Research Institute, over the five years from 2019 to 2023, one in every three companies received direct investment from state-owned institutions. Even in AI financing — long considered the "exclusive territory" of dollar funds — Beijing and Shanghai's AI industry funds have taken the lead.

One state capital insider told Anyong Waves with some exaggeration, "Behind every fund today, you'll find state capital."

Ji Xing, partner at Lighthouse Capital, told us that the new reality of China's primary market is this: government capital and state-owned assets have become the main contributors to RMB funds. "From 2014 to 2023, the proportion of government LP contributions to newly raised RMB funds grew from 20% to 41%."

As Xiao Bing, executive partner at Fortune Venture Capital, put it: "Individual destinies, investment institution destinies, and the destiny of the venture capital industry itself are now more closely tied to the nation's destiny than ever before."

Yet despite countless conversations about state capital, a common phenomenon persists: people hold only relatively vague impressions, unable to grasp the full picture.

Indeed, the landscape of state capital is intricate and complex. By type and tier, there are母基金 (fund-of-funds), guidance funds, and direct investment funds, operating at levels from national to provincial, municipal, and district/county. While GPs and entrepreneurs seeking state investment typically communicate most with investment attraction officers, tracing the capital behind these funds reveals funding "pockets" scattered across various levels of finance bureaus, SASACs, and development and reform commissions. Beyond government-affiliated capital, there is also a vast ecosystem of central and state-owned enterprises with more strategic, industry-oriented capital up and down the supply chain. Additionally, there are relatively mature institutions like Shenzhen Capital Group, Fortune Venture Capital, and Yuanhe Holdings that operate almost indistinguishably from market-oriented funds.

The ebbs and flows of state capital's equity investments have also remained relatively low-profile and opaque. Beyond cases like Hefei and NIO, most details and stories remain unknown. State capital commands the largest capital base of this era, yet sits quietly, implementing counter-cyclical adjustment.

To understand state capital, one must first understand its essence.

In Anyong Waves' interviews with multiple investors and financial advisors who have long collaborated with state capital, three points emerge as central to state capital behavior:

Policy orientation: serving the broad direction of national development and supporting key industries.

Investment attraction imperative: emphasizing impact on local GDP and contributing to local industrial upgrading and development.

Non-purely financial inclination: attention to compliance and risk.

Liang Sumin, partner at Winnovation Capital, told Anyong Waves that state capital investments often come with requirements for corporate commitment to local investment, with comprehensive calculations of tax revenue, employment, GDP, and fixed assets — even stricter accounting than market-oriented institutions. "Most investment processes include a session called the Party Secretary's office meeting, where they calculate the combined ledger of risk and output value."

In short, state capital must simultaneously balance investment returns, investment attraction, and risk.

If the past two decades of China's primary market, dominated by foreign capital, were about accelerating explosive growth — using capital injection to rapidly scale companies for offshore IPO harvests — then the key to sustainable development in this state capital-dominated era lies not in any so-called "state advance, private retreat," but in a three-wheel drive of government, industry, and capital.

However, state capital's inability to be "pure" has also triggered market criticism around phenomena like investment attraction involution and risk aversion. Over the past year, these issues have been receiving attention and resolution.

On April 30, 2024, the Political Bureau of the CPC Central Committee, while emphasizing "developing new quality productive forces according to local conditions," first proposed "patient capital."

On August 1, 2024, the Fair Competition Review Regulations took effect, prohibiting tax incentives, selective and differentiated fiscal rewards or subsidies for specific operators.

On January 7, 2025, the General Office of the State Council formally issued Guiding Opinions on Promoting High-Quality Development of Government Investment Funds, responding to problems with government guidance funds and pain points for local market-oriented investment institutions — from extending fund performance evaluation cycles, to not establishing government investment funds for investment attraction purposes, to diversifying exit channels and optimizing fault-tolerance mechanisms.

Shenzhen's Municipal Financial Office went further in its Shenzhen Action Plan for Promoting High-Quality Development of Venture Capital (2024–2026) (Public Draft for Comments), becoming the first in the country to propose developing "bold capital."

Across this series of government statements, one can see that state capital is clarifying its role in the overall equity investment capital pool: its core function is guidance, adjustment, and acceleration. State capital is not the protagonist standing at center stage of primary markets, but rather an important regulator and guidepost — directing capital and resources effectively toward economic structural transformation, new quality productive forces, and technological innovation.

Multiple primary market practitioners in frequent contact with state capital note that since the second half of last year, the professionalism of frontline state capital personnel has been improving. "Investment attraction officers used to only care about their own small patch of land; now they're also concerned with companies' commercial needs."

Liang Sumin has also observed that state capital direct investment is entering primary markets in large volumes. "Previously, capital flowed through fund-of-funds and guidance funds to GPs, with actual direct investment only accounting for 20–30%. GPs still had to satisfy other LPs' demands, and in the end might not even meet the regional industrial return requirements." She told Anyong Waves, "This is changing." Meanwhile, to diversify risk and enhance professionalism, Beijing's municipal direct investment fund has adopted a dual-GP model — opening a newer experiment for bold state capital.

Over the past six months, Anyong Waves has researched and mapped active local state capital entities across the country, interviewing multiple investors and financial advisors on the front lines who have collaborated and communicated with state capital, with data and information support from Winnovation Capital, Lighthouse Capital, Yibai Capital, Dust Consulting, Taihe Capital, Tianyancha, and Qichacha.

At this moment of renewal where state capital is reshaping itself and separating wheat from chaff, we hope to explore the "patient and bold state capital" worth recording over these years, in search of an answer to one question: What are the core factors that allow state capital to fully play its regulatory and guiding role?

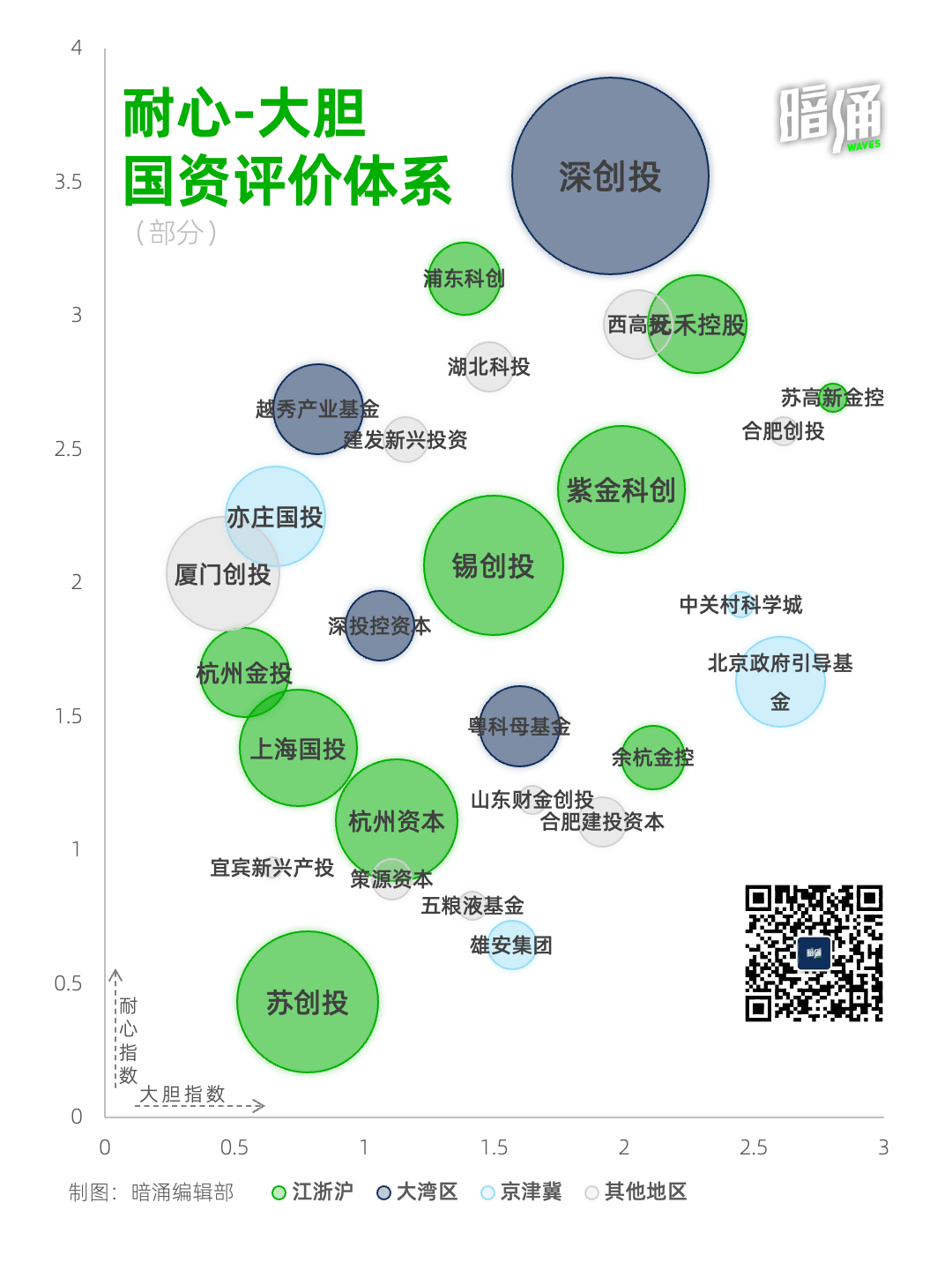

Based on multiple data sources and public information, Anyong Waves selected 30 local state capital entities and evaluated them across two dimensions — "Boldness Index" and "Patience Index" — producing this distribution map of local state capital entities in active cities nationwide.

The "Boldness Index" measures: direct investment project activity, collaboration with market-oriented GPs, and early-stage investment enthusiasm. The "Patience Index" measures: years since establishment, organizational structure integration, consistency and stability of investment activity, and presence of incubation operations. Both indices also incorporate shared dimensions such as follow-on investments in the same projects and activity during market downturns, with different weightings.

In the chart, bubble size indicates publicly disclosed capital scale; bubble color indicates regional type; further right on the horizontal axis indicates bolder; higher on the vertical axis indicates more patient. The most representative local state capital entities in the chart and their distinctive characteristics and investment situations can be found in corresponding analyses in the main text.

Note: Due to the broad distribution, numerous entities, complex funding arrangements, and limited transparency of local state capital, it is extremely difficult to obtain the latest, comprehensive, and detailed information. The chart data may have lags and is for reference only.

Table of Contents

Part 01 Policy First

1.1 Beijing E-Town Capital: A Critical Link in Building Industrial Ecosystems

1.2 Xiong'an Group: The Pipeline for Industrial Import into a New District

Part 02 Technology at the Core

2.1 Zhongguancun Science City: A Regional Comprehensive Scientific Research Service Group

2.2 Shenzhen Angel Fund of Funds: A Typical Case of a Nurturing母基金

2.3 Shanghai Angel Investment Guidance Fund: A Bridge Between Industry and Innovation

2.4 Leaguer & Scino: Building an "Industry-University-Research" Network

Part 03 Industry as Foundation

3.1 Hefei Construction Investment: The "Chips, Displays, EVs, and AI" Hefei Model

3.2 Yibin Development Holding Group: Industrial Reinvention from Baijiu to Power Batteries

Part 04 Top-Level Coordination

4.1 Beijing State-Owned Assets Management: Industrial Segmentation

4.2 Shanghai State Investment: Integration and Optimization

4.3 Shenzhen Capital Group and Shenzhen Investment Holdings: A More Comprehensive Case

Part 05 Respecting the Market

5.1 Futian Guidance Fund: Patience and Delegation

5.2 Jiangsu High-Tech Investment Group: Yielding Profits and Exempting Liability

5.3 Xiamen C&D Emerging Investment: Standing with the Market and Industry

5.4 Suzhou Yuanhe Holdings: The Culmination of 20 Years of Market-Oriented Practice

Part 06 Courage Multiplier

Part 01 Policy First

Top-level policy support is the core guidance for local state capital's entry, development, and sustained equity investment.

The policy starting point for state-owned investment companies dates to 1988. As an important measure of that year's investment system reform, the State Council established six national specialized investment companies at the central level, while local governments across the country successively established a batch of local investment companies. The full flowering of local state-owned investment companies came after the establishment of SASAC in 2003.

At that time, gradually emerging from the impact of the Asian financial crisis and benefiting from a new round of global economic growth, China's economic development was accelerating and beginning to show signs of overheating. To prevent major economic fluctuations and maintain steady, rapid growth, central management froze land approvals in the second half of 2003 and launched comprehensive inspections and rectification of various investment projects. Against this backdrop, local governments began extensively using local state-owned investment companies for project investment as a way to drive local economic growth while circumventing central regulation. By 2008, as the financial crisis swept the globe, the "four trillion" stimulus triggered a new wave of investment frenzy among local governments. Previously economically backward regions also established local state-owned investment companies and built local financing platforms to access credit funds and drive local infrastructure construction. During this phase, numerous county-level cities established investment entities with the basic characteristics of investment companies, further expanding the ranks of state-owned investment companies.

Meanwhile, the policy foundations for government-guided industrial funds were being laid brick by brick. In his book Inside the Chinese State, Lan Xiaohuan notes that starting in 2005, the state introduced a series of policies and regulations — the Administrative Measures for Venture Capital Enterprises, the Partnership Enterprise Law, the Guidance on Standardized Establishment and Operation of Venture Capital Guiding Funds, and the Notice on Exempting State-Owned Venture Capital Institutions and Guiding Funds from Share Transfer Obligations, among others — that established the institutional groundwork for government-guided funds. Yet their explosive growth didn't occur until around 2014. The most direct "trigger" was a series of reforms centered on the new Budget Law.

After the reform, the State Council began strictly limiting local governments' direct subsidies to enterprises. As Lan Xiaohuan writes: "These fiscal funds originally used for subsidies and tax breaks had to find new vehicles and outlets — they couldn't just sit on the books. Because the new Budget Law stipulated that funds unspent for two consecutive years could be reclaimed by the same-level or higher-level government for reallocation." Thus, industrial guiding funds with local governments as their main protagonists finally embarked on their path to expansion.

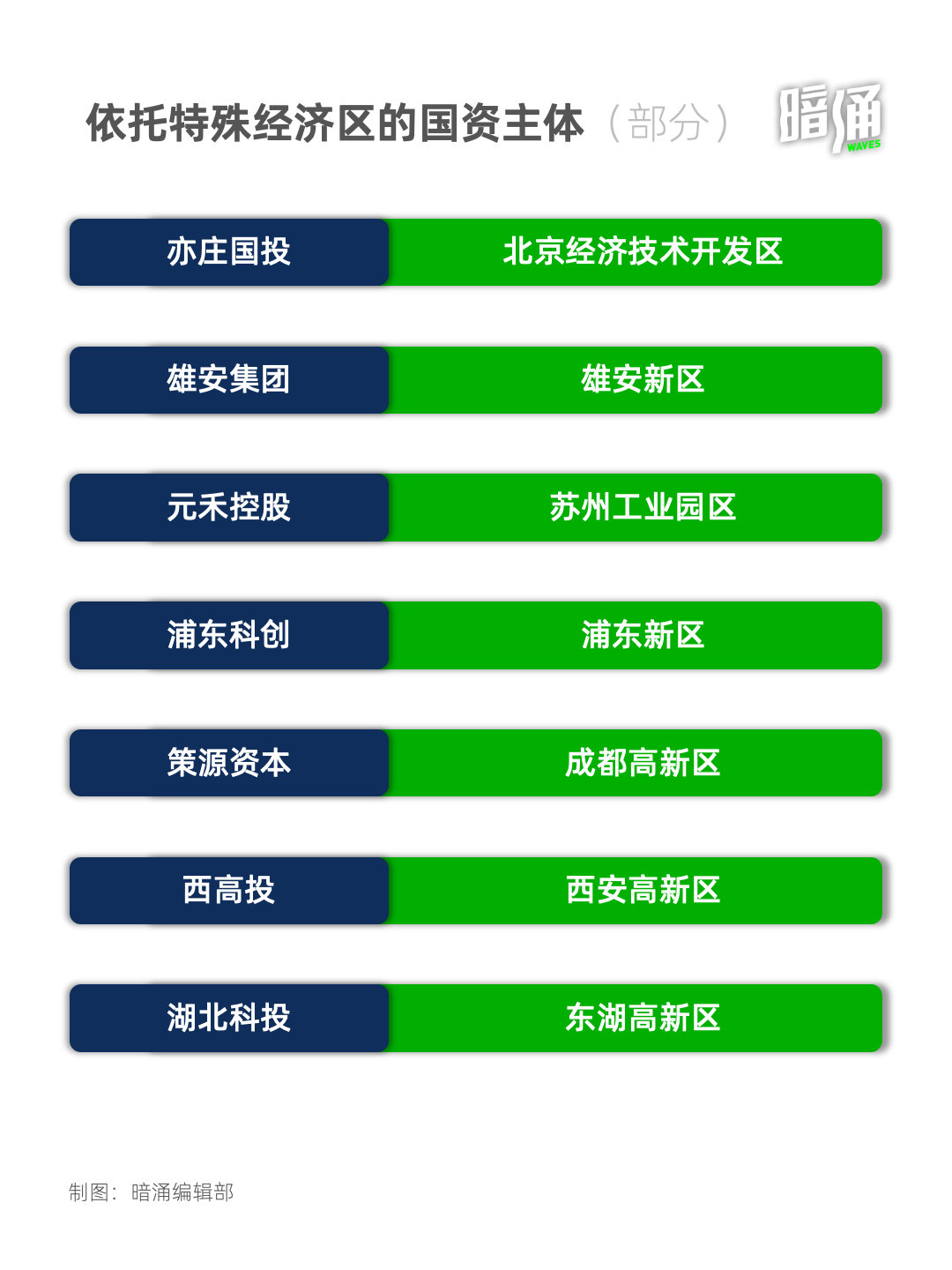

By this point, state-owned investment companies and government-guided funds — the two leading actors of state capital investment — had gained policy-level legitimacy. And those entities that were first to obtain and concentrate preferential policies enjoyed longer growth timelines and greater room for expansion compared to their peers. Through research into active domestic state capital investors, An Yong Waves found that a cohort of state-backed entities anchored to specific zones — national-level development zones (high-tech zones, economic-technical zones), national-level new areas, and the like — have delivered notably strong performance in investment practice.

1.1 E-Town Capital

A Critical Link in Building Industrial Ecosystems

Beijing E-Town International Investment & Development Co., Ltd. ("E-Town Capital") was established in February 2009 as a state capital investment and operations company serving the industrial development and technological innovation of Beijing Economic-Technological Development Area. As of end-June 2024, its total assets stood at approximately RMB 123 billion.

Beijing Economic-Technological Development Area, abbreviated as "Beijing E-Town," is Beijing's only national-level economic-technical development zone. In the State Council's August 1994 approval for its establishment, the stated objective was to "fully leverage the capital's advantages, actively attract foreign investment, develop high-caliber industrial and technology projects, and promote technological transformation and industrial restructuring of Beijing's state-owned large and medium enterprises."

Precisely because it is backed by Beijing E-Town, E-Town Capital carries an exceptionally strong imprint of investment promotion and industrial cluster building. Most representative across its fifteen-year history are its successive investments in the digital television, integrated circuit, and automotive industries.

In August 2009, just six months after its founding, E-Town Capital contributed land-use rights for 370,000 square meters to participate in the construction of BOE's TFT-LCD Generation 8.5 production line. Following multiple subsequent investments, by early 2015 E-Town Capital had exited its BOE position, recovering approximately RMB 5 billion. Centered on BOE's Generation 8.5 line, the Beijing Digital Television Industrial Park attracted numerous name-brand enterprises including Corning, TPV, and Sumitomo, generating output value in the hundreds of billions and creating 20,000 jobs.

If E-Town Capital's initial investment strategy remained a relatively conventional investment promotion model, its concentrated investments in integrated circuits starting from 2012 constructed, to a significant degree, the entire northern ecosystem for that industry.

In 2012, E-Town Capital invested RMB 700 million through a combination of fund investments, entrusted loans, and equity investments to support the construction of SMIC's Phase II B2 large-scale wafer fab. In 2015–2016, E-Town Capital partnered with Hua Capital, SummitView Capital, and Chipone to successively acquire American CMOS image sensor chip company OmniVision, American IC design company ISSI, and American power management chip design company iML. In 2018, E-Town Capital joined with the National Integrated Circuit Industry Investment Fund and other institutions to invest RMB 4 billion in Yandong Microelectronics. In 2022, E-Town Capital contributed RMB 16.1 billion to jointly establish CXMT (Changxin Memory Technologies) with RuiLi Integration and the National IC Fund.

Through E-Town Capital, Beijing E-Town has assembled the strongest integrated circuit industry cluster in northern China. Beyond major players like SMIC, BOE, Yandong Micro, CXMT, and NAURA Technology Group, the three core subsystems for domestic lithography machines — light source (Keyi Hongyuan), objective lens (Guowang Optical), and wafer stage (Huazhuo Jingke) — have all established operations in the zone.

In the automotive sector, E-Town Capital demonstrated "big-ticket" assertiveness from the outset. In 2010, E-Town Capital partnered with AVIC Auto to successfully acquire century-old American company Nexteer for $480 million, subsequently driving its listing on the Hong Kong Stock Exchange — at the time, the largest overseas acquisition in China's auto parts industry. In 2013, E-Town Capital invested RMB 1 billion to support Beijing Benz factory construction, and the following year participated as a cornerstone investor with $100 million in BAIC Motor's IPO.

As China's new energy vehicles, intelligent connectivity, and autonomous driving sectors continued to develop, E-Town Capital also appeared in the growth trajectories of Huawei, Xiaomi, Jianzhi Robotics, and SemiDrive Technology. By 2023, Beijing E-Town's automotive industry achieved output value exceeding RMB 200 billion, accounting for approximately 60% of Beijing's total. Currently, Beijing E-Town has gathered over 120 intelligent connected vehicle enterprises and established three national-level R&D platforms.

As of end-June 2024, E-Town Capital has over 200 investments under management with total committed capital exceeding RMB 100 billion. As a state capital investment and operations company based in a development zone, E-Town Capital also demonstrates "chain master" characteristics in its investment and financing activities. For instance, it has undertaken capital contribution responsibilities for the National Integrated Circuit Industry Fund Phase I and Phase II, the National Manufacturing Transformation and Upgrading Fund, and others; partnered with StarNeto as cornerstone investors to jointly launch the Beijing Xinghua ZhiLian Investment Fund; and co-founded the E-Town Biomedical M&A Fund with SciGen Pharmaceutical and E-Town Biomedical Park.

1.2 China Xiong'an Group

The Pipeline for Industrial Import into a New Area

In April 2017, Xiong'an New Area in Hebei was established as a national-level new area — following the Shenzhen Special Economic Zone and Shanghai Pudong New Area as another zone of national significance, a "millennium plan, national priority." Three months later, China Xiong'an Group Co., Ltd. (originally "China Xiong'an Construction & Investment Group Co., Ltd.," abbreviated as "Xiong'an Group") was founded with registered capital of RMB 30 billion.

Among the eight registered funds totaling approximately RMB 15.7 billion under Xiong'an Group's management, one is a fund-of-funds: the "Xiong'an Industrial Guiding Fund." In 2024, Xiong'an New Area intensively launched four new funds with combined registered scale of RMB 2.6 billion, with the Xiong'an Industrial Guiding Fund as the primary contributor in each.

The fund-of-funds managed by Xiong'an Group was established the year after the new area's founding, with total scale of RMB 10 billion, comprising the RMB 9 billion Baiyangdian Environmental Protection Fund, the RMB 1 billion Central Enterprise Relocation Fund, and the Green Building Materials Fund and Infrastructure Fund with combined scale of approximately RMB 400 million.

In 2023, after five years of operation, Xiong'an state capital made a high-profile media appearance. Han Wei, Director of the Legal Compliance Department of China Xiong'an Group and Executive Director of Xiong'an Fund, explained to media that the Xiong'an fund-of-funds prioritizes "industrial import" in its investments, with five core industries identified: new materials, next-generation information technology, life sciences and technology, modern services, and modern ecological agriculture. To date, Xiong'an Fund Management Company, an investment subsidiary of Xiong'an Group, has ten associated funds under its name with combined registered scale of approximately RMB 22 billion.

Moreover, due to Xiong'an New Area's special historical mission, facilitating the relocation of central enterprise headquarters has become a regional priority. Throughout 2024, 40 second- and third-tier subsidiaries of central enterprises established operations in Xiong'an New Area. To date, central enterprises have established nearly 300 various institutions in the new area. Consequently, the RMB 1 billion Central Enterprise Relocation Fund carries distinctive policy characteristics of the region's state capital.

This fund focuses on supporting "equity diversification reform and mixed-ownership reform of central enterprises and their subsidiaries that align with Xiong'an New Area's industrial development positioning," serving central enterprise relocation and promoting orderly development of high-end, high-tech industries. According to Tianyancha information, its current external investments include China Satellite Network Digital Technology Co., Ltd. (with central enterprise "China Satellite Network" as majority shareholder at 65%) and Xinsheng Technology, a subsidiary of China Mobile.

Part 02

Technology at the Core

"Technological innovation" is the core driver of economic growth and industrial development, and the ultimate value proposition of venture capital firms.

In March 1985, the Central Committee of the Communist Party issued the Decision on Reform of the Science and Technology System, stating that for high-technology development companies characterized by rapid change and high risk, venture capital could be established to provide support. Six months later, the State Council formally approved the establishment of China New Technology Venture Investment Corporation — China's first high-technology venture investment company, with primary founding shareholders including the State Science and Technology Commission and the Ministry of Finance. And CTIC's foremost responsibility was to conduct venture investment in the national technology industry.

Shortly after CTIC's founding, this model was replicated on a broad scale nationwide, as local science and technology commissions and finance departments launched a wave of jointly establishing government-backed venture investment institutions.

For example, in 1992 the Shanghai municipal government established Shanghai Technology Investment Co. (among the first batch of local venture capital companies nationwide) to address the "pain of industrializing high-tech achievements" since reform and opening up. The following year, to attract more social capital into investments for industrializing scientific achievements, Shanghai Tech Investment partnered with several state-owned banks and enterprises to establish Shanghai Technology Investment Co., Ltd.; and in the same year cooperated with IDG to establish Shanghai Pacific Technology Venture Investment Co., Ltd. — China's first Sino-foreign joint venture venture capital firm. This was the predecessor of what would become IDG Capital, known as the "elder statesman" of Chinese VC.

Thereafter, China's venture capital development entered two decades of rapid advancement. This was an emulation that spread from central to local state capital, then to broader society, with the ultimate goal of effectively deploying capital and resources into strategic emerging industries, completing the transformation of scientific research achievements and local industrial development, and achieving economic growth.

Statistics on funds registered with the Asset Management Association of China whose names contain the keywords "achievement" or "transformation" show that achievement-transformation-related fund registrations have risen year by year. As of 2024, the number of such funds has reached a historical high.

An Yong Waves has roughly tallied and categorized state capital institutions specifically focused on "technological innovation" and "scientific achievement transformation," investing in seed- and angel-stage technology enterprises. They can be broadly divided into four categories:

2.1 Zhongguancun Science City

A Regional Comprehensive Scientific Research Services Group

In Haidian District, dozens of technology startups are born every day on average. Zhongguancun Science City, located in the northwest of Beijing, is the core zone of Beijing International Science and Technology Innovation Center — its main area encompasses Zhongguancun Haidian Park, extending to the entirety of Haidian District and parts of Changping District.

This area has assembled a massive concentration of high-tech enterprises and innovation resources, including: prestigious universities and research institutes such as Peking University, Tsinghua University, and the Chinese Academy of Sciences; the most dynamically innovative talent among scientists and entrepreneurs; innovation platforms like overseas returnee startup parks, university science parks, and new-type incubators; and innovation service providers including investment institutions, IP service firms, and talent agencies. At the same time, it has attracted emerging internet companies such as ByteDance, Didi, and Megvii, along with established tech enterprises like Xiaomi, Baidu, Lenovo, and Tsinghua Unigroup; international companies including Microsoft, IBM, and SAP have also set up R&D centers here.

This may represent the most complete innovation and entrepreneurship ecosystem in all of China, with an IP-intensive industrial base, carrying the critical mission in Beijing's "Three Science Cities and One Zone" initiative as the launchpad for technological innovation, the source of original innovation, and the main battleground for indigenous innovation. According to public data, by 2019, high-tech enterprises in Zhongguancun Science City had achieved total revenue exceeding 2.6 trillion yuan, with annual growth above 10%. The science city hosts 10,448 national-level high-tech enterprises, roughly 40% of Beijing's total; and 40 "unicorn" companies, approximately one-fifth of the national total.

In May 2019, accompanying Zhongguancun Science City's entry into a new development phase, the Haidian District Committee and District Government established a new market-oriented operations platform — Beijing Zhongguancun Science City Innovation Development Co., Ltd. — wholly owned by the Haidian State-owned Assets Supervision and Administration Commission (SASAC). With registered capital of 6 billion yuan, the company encompasses three fund systems: the "Sci-Tech Innovation Fund Series," the "Sci-Tech Growth Fund Series," and the "Haidian Government Guidance Fund Series." Among these, most of the "Haidian Government Guidance Fund Series" predated the science city company's establishment, with the earliest dating back to 2009.

As of 2025, according to the Zhongguancun Science City company website, the "Haidian Government Guidance Fund Series" has directly invested in 106 early-stage technology enterprises and established 47 sub-funds; it has nurtured well-known companies including TINAVI, Cambricon, Loongson Technology, and凌云光 (Lingyun Guang).

The "Sci-Tech Growth Fund Series," since its establishment in 2019, has deployed two funds totaling 10 billion yuan to support scientist funds such as the Zhongguancun Zhiyou Scientist Fund, the Sinovation Ventures Scientist Fund, and the CAS Star Hard Tech Phase II Fund, as well as industry sub-sector funds including Gaorong Capital, Glory Ventures, the Innovation Dark Horse Fund, Jiangmen Ventures, and Yahui Investment Fund, building a network for early-stage hard tech investment. Its more than 50 direct project investments evolved from Phase I's focus on medical health and integrated circuits/chips to Phase II's gradual expansion into artificial intelligence, big data, next-generation information technology, and intelligent manufacturing. Notable portfolio companies include Zhipu AI, DP Technology, ModelBest, Shengshu Technology, Fourth Paradigm, Unitree Technology, and GalaxyBot in AI and robotics, and Moore Threads and Kunlunxin in the chip sector.

In February 2025, following closely on Phase II, the Zhongguancun Science City Sci-Tech Growth Phase III Fund was announced with a total scale of 10 billion yuan — funded by the Haidian District Government increasing its investment in Haidian State-owned Investment Group, which serves as the sole LP committing 9.9 billion yuan to the fund.

2.2 Shenzhen Angel Fund of Funds

A Paradigmatic Case of a Nurturing Fund of Funds

The Shenzhen Angel Fund of Funds was established in 2018, capitalized by the Shenzhen Government Guidance Fund, with a current total scale of 10 billion yuan. Its investment mandate covers strategic emerging industries, future industries, and other priority industries that Shenzhen supports and encourages. To date, the fund has invested in over 80 angel sub-funds, with effective committed capital exceeding 20 billion yuan, covering nearly a thousand portfolio companies, including 161 with valuations exceeding $100 million and 6 with valuations exceeding $1 billion.

The Shenzhen Angel Investment Guidance Fund Co., Ltd. (Shenzhen Angel Fund of Funds) was established as a strategic, policy-oriented fund initiated by the Shenzhen Municipal People's Government. Its policy orientation is manifested in its non-profit purpose — if the fund is profitable, it shares gains with partners; its strategic nature means investment is not for short-term returns but for optimizing the growth environment for Shenzhen startups and supporting the development of more enterprises like Tencent and Huawei.

The Shenzhen Angel Fund of Funds is entrusted to the Shenzhen Angel Investment Guidance Fund Management Co., Ltd. (Shenzhen Angel Fund of Funds Management Company), jointly established by Shenzhen Investment Holdings and Shenzhen Capital Group, for market-oriented operation and management. It aims to lead the angel investment industry, cultivate outstanding startups, and perfect the full-process innovation ecosystem chain of "basic research + technological breakthroughs + industrialization of results + sci-tech finance + talent support."

In April 2024, according to Yao Xiaoxiong, Chairman of the Shenzhen Angel Investment Guidance Fund Management Co., Ltd.: since its establishment in 2018, the fund has invested in sub-funds including Songhe Capital, Lihe Sci-Tech Innovation, ZhenFund, InnoAngel, HighLight Capital, and CDH Investments, covering TMT, medical health, and artificial intelligence. Direct investments in startups include: Moffett AI, Saiqiao Biotech, and other mid-early stage enterprises.

Additionally, in recent years, another seed fund managed by the Shenzhen Angel Fund of Funds deserves attention — the Shenzhen Sci-Tech Innovation Seed Fund (hereinafter referred to as the "Seed Fund"), established in November 2023 with 2 billion yuan from the Shenzhen Municipal Government, dedicated to promoting technological innovation and commercialization of scientific achievements. It is the nation's first policy-oriented fund of funds with a science and technology administrative department serving as the industrial supervisory department, and is currently in its investment period.

2.3 Shanghai Angel Investment Guidance Fund

A Bridge Between Industry and Innovation

Established in 2014 under the guidance of Shanghai Municipal Development and Reform Commission, the Shanghai Angel Guidance Fund operates with the purpose of "government leading social capital to share innovation risks and rewards," leveraging the multiplier effect and guiding role of government capital to mobilize more social capital to "invest early, invest small, invest in technology."

The Shanghai Angel Guidance Fund exists as a bridge between industry and innovative enterprises. According to Dong Ruoyu, the fund's operations lead, in an annual report: as of October 2024, the Shanghai Angel Investment Guidance Fund has total assets under management of 3.5 billion yuan, with over 140 approved funds (including nearly 20 early-stage investment institutions such as Kai Feng Ventures, Frees Fund, Shicui Capital, and Plug and Play China), and 27 exited funds. It covers over 1,400 enterprises, with startups accounting for over 70%.

Since its establishment, the fund has guided industrial capital toward earlier stages, partnering with corporate capital and vertical industry investors. A high proportion of its partner funds have listed company industrial backgrounds, covering companies such as Fudan Microelectronics, Titan Scientific, Yonyou Software, Weimob, Wangsu Technology, Jinzheng Computer, Aerospace Science and Industry, Jingrui Electronic Materials, Raytron Technology, Junshi Biosciences, and Shanghai Pharmaceuticals. Among these, the Titan Heyuan Fund, partnered with Titan Scientific, has deployed a series of early-stage projects around the scientific services industry chain; the Shanghai Biomedical Translation Fund, partnered with Shanghai Pharmaceuticals, has invested in a series of university professor projects including Baiquan Biotech, a Fudan University technology transfer project.

On the other hand, it guides the industrialization of source innovation. The Shanghai Angel Investment Guidance Fund's custodian institution, Angel Plus Fund, has partnered with a series of early-stage institutions focused on technology transfer project investment, such as the Xiaomiao Langcheng Fund (which invested in Linding Optics, a Shanghai Jiao Tong University technology transfer project), the Plug and Play China Fund (which invested in Qionche Intelligence, a Shanghai Jiao Tong University technology transfer project), and Changlei Capital (which invested in Tanxu Technology, a Fudan University technology transfer project).

2.4 Lihe Sci-Tech Innovation

Building an "Industry-University-Research" Network

The history of Lihe Sci-Tech Innovation (Shenzhen Lihe Sci-Tech Innovation Co., Ltd.) can be traced back to 1996, when the Shenzhen Municipal Government and Tsinghua University established the Shenzhen Tsinghua University Research Institute. In 1999, the Research Institute initiated the establishment of "Shenzhen Tsinghua Technology Development Co., Ltd." (the predecessor of Lihe Sci-Tech Innovation). In 2015, the Shenzhen Tsinghua University Research Institute and Lihe Sci-Tech Innovation jointly built an industry-university-research integrated sci-tech innovation incubation system, forming the Lihe Sci-Tech Innovation Group.

Lihe Sci-Tech Innovation is controlled by the Shenzhen Municipal SASAC. Leveraging Tsinghua University's research resources, it has built an extensive industry-university-research cooperation network. With a dual-wheel-driven business model of "sci-tech innovation services + strategic emerging industries" at its core, it has created a full-chain sci-tech innovation service system from technology R&D, achievement transformation to industrial landing.

Through direct investment and sub-fund partnerships, Lihe Sci-Tech Innovation has supported the growth of numerous technology enterprises, collaborating with investment institutions such as Shenzhen Capital Group, Songhe Capital, and Cowin Capital to jointly invest in early-stage technology projects. It has also established national-level incubators, maker spaces, and other physical innovation platforms across the country, providing startups with office space, capital support, technology matching, and market promotion services, helping growth-stage enterprises rapidly scale and achieve industrialization.

Part 03

The Foundation of Industry

"The primary goal of state capital is not profit, but strengthening or filling gaps in industrial chains." Compared with relatively nimble market-oriented institutions, state capital institutions, driven by strategic needs to stimulate local economic development, must pay greater attention to and leverage their regional industrial foundations.

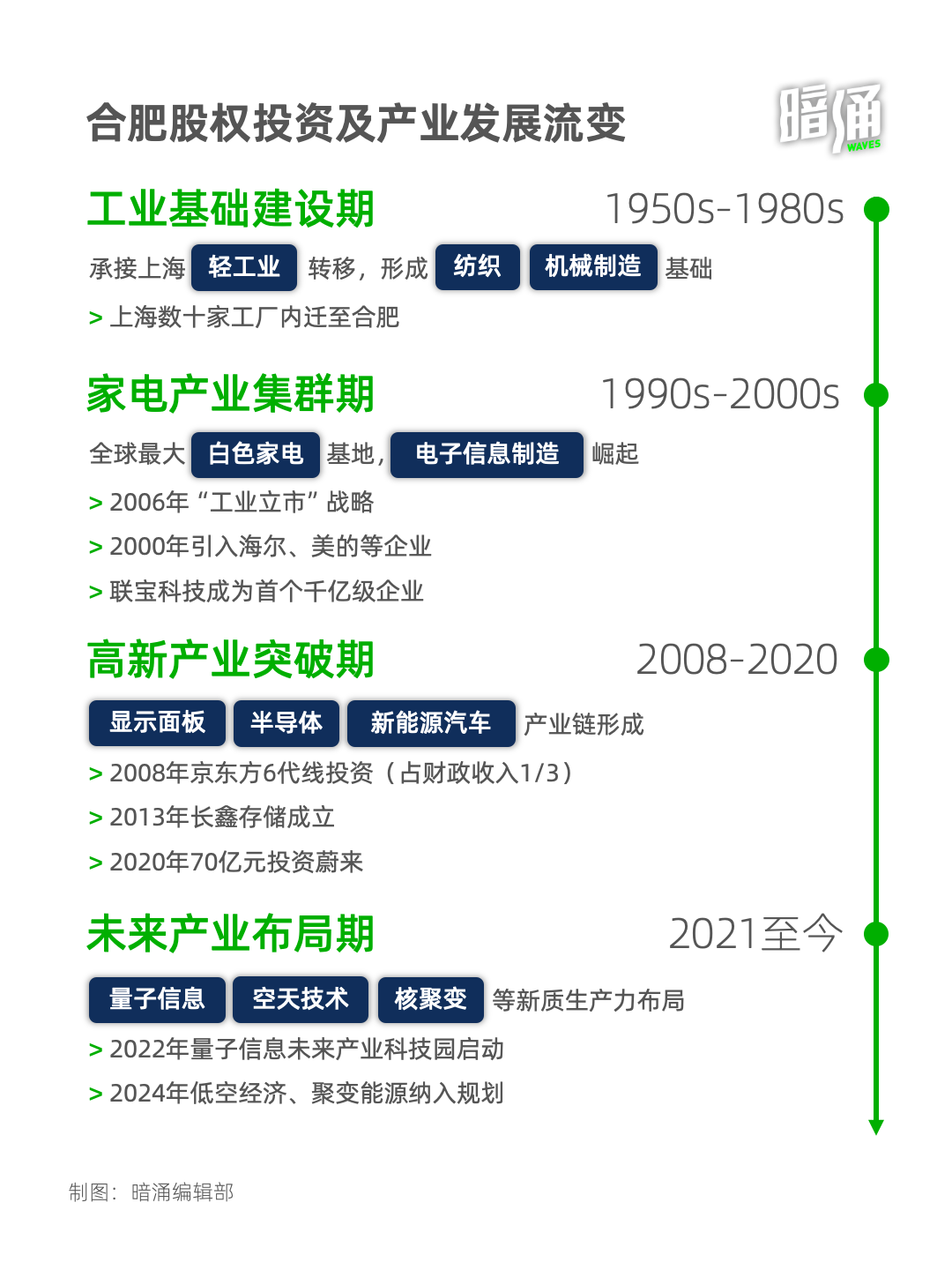

3.1 Hefei Construction Investment

The Hefei Model of "Chips, Displays, Vehicles, and Integration"

Hefei, with its historically weak industrial base, has used an "investment-led attraction" model to focus on strategic emerging industries, leveraging state capital to catalyze industrial chain upgrades.

In 2008, with municipal fiscal revenue of only 30 billion yuan, the Hefei Construction Investment Group nonetheless made a "bet-the-house" move to invest 17.5 billion yuan to attract BOE's 6th-generation LCD panel production line. The context for this decision: at the time, domestic display panels were entirely import-dependent; BOE was technologically leading but had posted consecutive years of losses, while multinational corporations attempted to strangle its development through below-cost dumping. Hefei Construction Investment designed an innovative "capital injection + agreed exit" structure, requiring BOE to bring in strategic investors to buy back partial equity, while committing to localizing supporting industry chains.

This decision directly rewrote Hefei's industrial DNA: after BOE's Gen 6 line began production, domestic panel prices dropped 30%, breaking the Japan-Korea monopoly; it attracted over 300 upstream and downstream enterprises including Sumitomo Chemical (glass substrates) and Corning (liquid crystal materials) to establish operations, forming a complete industrial cluster "from sand to finished product." By 2023, Hefei's new display industry output exceeded 200 billion yuan, with 10% of global display panels produced in Hefei, making it the world's largest display industry base.

In 2020, Hefei Construction Investment struck again, injecting 7 billion yuan into NIO, then on the verge of delisting, with put option terms (requiring annual sales of 500,000 vehicles by 2024). This investment not only saved the company but also triggered explosive growth in Hefei's new energy vehicle industrial chain: NIO China headquarters relocated to Hefei, building a smart factory with annual capacity of 1 million vehicles; 120 enterprises including Gotion High-tech (power batteries) and Huating Power (BMS systems) clustered there, forming a complete ecosystem covering complete vehicles and the "three electric" systems.

On CCTV's Dialogue, Li Hongzhuo, Chairman of Hefei Construction Investment, revealed Hefei's state capital investment decision-making process: "At that time, Hefei was operating on four parallel fronts. First, we organized professional teams and commissioned some top domestic experts for evaluation, conducting comprehensive analysis of NIO's technology, supply chain, and market; second, we paid close attention to national policy orientation, regarding support for the development of intelligent electric vehicles, including their battery swap model, to provide support for decision-making; third, we commissioned professional institutions to conduct comprehensive legal and financial due diligence on the enterprise; the fourth front was our detailed, thorough, and rigorous business negotiations with them."

By 2023, Hefei's new energy vehicle output exceeded 300 billion yuan, accounting for over 10% of the national total. Additionally, in 2021, Hefei Construction Investment invested 2.2 billion yuan in OFILM, then in distress, to help it build an optoelectronics industry base, filling the gap in onboard camera lenses for the new energy vehicle industrial chain.

The success of the Hefei Model relies on the operations of the core state capital platform Hefei Construction Investment Holding Group (Hefei Construction Investment), which was actually transformed from a traditional urban development investment platform. Its fame was cemented by the BOE deal: when it exited the BOE Gen 6 and Gen 8.5 line investments, it gained approximately 20 billion yuan in returns, which were subsequently reinvested into new domains such as semiconductors and artificial intelligence.

3.2 Yibin Development Holding Group

From Baijiu to Power Batteries: An Industrial Reshaping

The story of how Yibin's state capital brought in CATL is a classic case study of an inland city upgrading its industry through strategic capital operations. The transformation was driven by urgent needs for urban renewal, enabled by precise state-led positioning and resource integration — ultimately turning Yibin from the "Capital of Liquor" into the "Global Capital of Power Batteries."

Around 2016, Yibin faced a dual crisis of stagnant traditional industries and population outflow. Coal and baijiu — the "one black, one white" industries — accounted for over 60% of the local economy. But coal was shrinking dramatically under environmental policies, and baijiu alone couldn't sustain growth. By 2018, baijiu still contributed 55% of the city's industrial profits, while emerging industries were virtually nonexistent.

Meanwhile, China's new energy vehicle industry was exploding. Power batteries, the "heart of NEVs," became fiercely contested strategic territory. The Yibin municipal government seized this opportunity, positioning power batteries as its breakthrough direction. The problem: the city had zero relevant enterprises. Yibin's answer was simple — find the chain master.

CATL was undeniably the best choice, but Yibin was not yet CATL's best choice. So Yibin did three things. First, it leveraged its regional advantages: Sichuan holds 57% of China's lithium reserves, the Yangtze River offers waterborne freight costs 40% lower than land transport, and the Xiangjiaba hydropower station provides cheap green electricity at rates 30% below eastern China — forming a "lithium-energy-logistics" hard-power triangle.

Yibin Development Holding Group (Yibin Development) served as the core operator, establishing a 30 billion yuan industrial fund matrix in partnership with top institutions like IDG Capital and CICC Capital, creating a capital leverage model of "government-guided funds + market-based fundraising." Its subsidiary, Yibin Emerging Industry Investment, directly participated in CATL project equity investments while completing preparatory work including thousand-mu land leveling and factory construction.

During CATL's site selection phase, Yibin formed a "chain master" task force led by the Party secretary, promising "delivery of thousand-mu land in 81 days," and coordinated Wuliangye Group to participate through a 13.6 billion yuan industrial fund for supply chain investment — creating a "dragon head + chain master" synergy effect.

Once the chain master landed, the next step was building a power battery enterprise cluster. Yibin Development led the construction of a "1+6" industrial spatial layout, with Sanjiang New Area as the core. It placed diaphragm production in Changjiang Industrial Park, copper foil in Luolong Industrial Park, and anode materials in Gongxian — forming a 3,500-mu power battery industrial park that attracted over 120 upstream and downstream enterprises including KDL and Dynanonic. Wuliangye Group broke through its traditional boundaries, investing through its Pushe Industry Development Fund in supporting projects like Tianyi Lithium Industry (lithium salt production) and Heguang Tongcheng (photovoltaic components) — transforming "baijiu capital" into "new energy capital."

This strategic investment completely reshaped Yibin's economic landscape. Power battery output went from nearly zero in 2019 to surpassing 101.3 billion yuan by 2023, accounting for 15% of national capacity — meaning one in every seven power batteries worldwide is produced in Yibin. The city's emerging industry employment surged, achieving population inflow reversal.

Part 04

Top-Level Coordination

In recent years, cities across China have been systematically studying the advanced state capital experiences of Hefei, Suzhou, and others. Nearly every first- and second-tier city has announced industrial fund clusters ranging from billions to hundreds of billions, even trillions of yuan. According to Zero2IPO Research, by 2024, the cumulative target scale of China's industrial investment and venture capital guidance funds exceeded 10 trillion yuan. At the time, press releases were filled with phrases like "full industry chain coverage," "cultivating innovation ecosystems," and "trillion-yuan fund matrices."

However, fund scale "satellite launches" don't automatically convert into local industrial development. In the rapid expansion of state capital fund clusters, multiple GPs seeking fundraising and entrepreneurs seeking financing told Yong Waves that they often returned empty-handed from these "key industry-supporting" local governments, with enormous time consumed in searching and waiting. "Which places actually have money?" became a frequently discussed question.

From the local government perspective, the picture looked different: investment performance lacked market-based incentive alignment, investment entities were numerous but unprofessional, and investment attraction objectives intensified blind competition on valuation and supporting conditions — ultimately causing massive government funds to spin idly within multi-layered structures.

Market-based GPs face market discipline; those unable to find distinctive advantages gradually disappear. State institutions must rely more on top-level coordination, constructing meaning for different entities through resource allocation and scheduling.

In the State Council Office's "Document No. 1" at the beginning of the year, the first detailed rule was "clarify fund positioning," with subsequent articles mentioning "grading," "differentiation," and "consolidation and optimization" — directly targeting the chronic ailment of "overlapping positioning, duplicated functions, and scattered resources" in local government funds. The document constructed a full-cycle coordination framework covering "establishment-operation-exit" through institutionalized graded management, cross-regional collaboration, and dynamic adjustment mechanisms, aiming to transform government investment funds from dispersed and粗放 to intensive and efficient.

The underlying systemic goal for state capital emerges clearly: every state institution must possess uniqueness, finding differentiated positioning in stage, region, and industry, while functionally overlapping institutions face "consolidation and optimization."

Based on our observations, certain local governments improved overall efficiency earlier through top-level coordination, achieving better results in cultivating innovation ecosystems.

4.1 Beijing State-Owned Assets Management

Industrial Segmentation

Beijing State-Owned Assets Management's Beijing Municipal Government Investment Guidance Fund Management Co. oversees the city's "Eight Major Industry Guidance Funds." This is an extreme case of using industrial categories to create differentiation in a state investment system.

The so-called "Eight Major Industry Guidance Funds" are eight sector-specific funds covering information technology, robotics, and other industries, with total initial scale of 100 billion yuan. After establishment, the Beijing Municipal Government Investment Guidance Fund led the deployment of these eight funds to various districts and counties, respectively entrusting management to Shouchang Holdings (robotics), Legend Capital (information technology), Qiming Venture Partners (AI), C-Bridge Capital (healthcare), Cornerstone Capital (advanced manufacturing and intelligent equipment), ZGC Capital (new materials), Fortune Venture Capital (commercial aerospace and low-altitude economy), and BAIC Capital (green energy and low-carbon).

The eight guidance funds minimized sector overlap, with market-based GPs selected according to their respective strengths, ultimately managed by eight different institutions. This top-level industrial differentiation has yielded solid results.

At year-end 2024, Guo Chuan, Deputy Party Secretary, Director, and General Manager of Beijing State-Owned Assets Management, revealed in a speech that the eight funds had completed investment decisions on 167 projects, with total approved investment of approximately 17 billion yuan (120% of the annual investment plan), and had actually contributed approximately 12.733 billion yuan to 135 qualified projects. Among funded projects, 18 were investment attraction projects, accounting for nearly 20%.

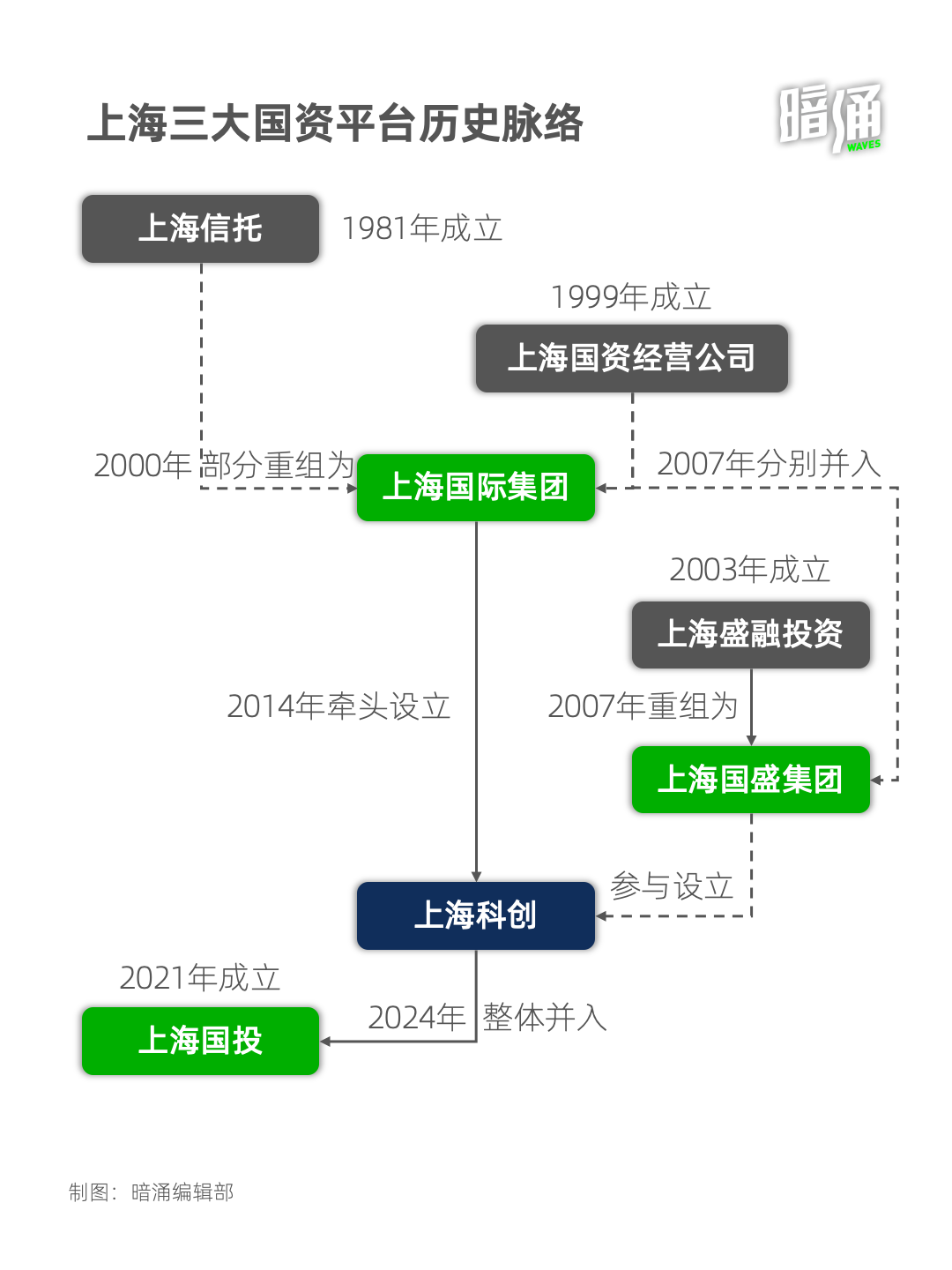

4.2 Shanghai State Investment

Consolidation and Optimization

In early 2024, Shanghai's local government equity investment system was brewing multiple major adjustments. At the time, He Qing, Party Secretary and Director of the Shanghai Municipal State-owned Assets Supervision and Administration Commission, elaborated on relevant thinking in an interview with Jiefang Daily, stating the need to "coordinate state-owned asset fund management and clarify functional positioning of private equity funds by category." The most eye-catching among these adjustments was the merger and reorganization of Shanghai State Investment and Shanghai Science and Technology Innovation Group.

On April 16 of the same year, the Shanghai Municipal SASAC officially announced this merger, which soon received approval. Before the reorganization, while the two enterprises had different emphases, they had functional overlaps in fund deployment and industrial investment, leading to scattered resources. The problem of numerous but poorly coordinated funds within Shanghai's state asset system urgently needed consolidation to concentrate forces in serving national strategy.

Post-reorganization, Shanghai State Investment manages over 140 billion yuan in assets and 170 billion yuan in fund scale — reaching top-tier levels among national local state capital platforms. In terms of division: Shanghai State Investment focuses on strategic shareholding and capital operations, coordinating母funds and industrial investment; Shanghai Science and Technology Innovation Group, as a second-tier subsidiary, continues deep cultivation of early-stage venture capital and strategic emerging industry incubation.

In retrospect, this merger may have been an advance pilot of Article 11 of the State Council Office's "Document No. 1" on "promoting fund consolidation and optimization," accumulating valuable experience for top-level coordination in more local state asset systems.

4.3 Shenzhen Capital Group and Shenzhen Investment Holdings

A More Comprehensive Case

The Shenzhen state asset system is a more complex case of top-level coordination. Across its decades of development, we can summarize how this system responded to environmental changes and evolved into its current form.

Shenzhen claims four major state capital platforms, among which Shenzhen Capital Group and Shenzhen Investment Holdings are relatively closely connected to equity investment in the narrow sense. Overall, the two respectively emphasize early-stage startups and mature industries, though there is also functional overlap between them.

Shenzhen Capital Group was founded in 1999; its subsequent story is largely well-known, so we'll focus on just two key junctures.

In 2004, the Shenzhen Municipal SASAC transferred Jin Haitao, former deputy general manager of SEG Group and general manager of SEG Co., to serve as chairman, switching Shenzhen Capital Group from a president responsibility system to a chairman responsibility system. The group's first two chairmen, Wang Suiming and Li Heihu, had both been principal leaders of Shenzhen Investment Management Company. Meanwhile, after studying the Temasek model, the Shenzhen Municipal SASAC merged and reorganized its three asset management companies — Shenzhen Investment Management Company, Commerce Holdings Company, and Construction Holdings Company — into Shenzhen Investment Holdings. The loosening of personnel and organizational ties marked the beginning of Shenzhen Capital Group and Shenzhen Investment Holdings pursuing their respective missions from 2004: Shenzhen Capital Group continued deep cultivation of early-stage sci-tech innovation, while Shenzhen Investment Holdings focused more on mature-stage industrial integration and strategic investment.

In 2018, the Shenzhen Angel Fund of Funds was inaugurated, with Shenzhen municipal leaders announcing joint management by Shenzhen Capital Group and Shenzhen Investment Holdings. In fact, prior to this, Shenzhen Investment Holdings already had multiple equity investment entities including Shenzhen HTI, Shenzhen Investment Holdings Capital, and Toukong Donghai; this co-management of "Shenzhen Angel" marked that the two no longer had clearly demarcated divisions in equity investment or even venture capital, but shifted toward more comprehensive ecosystem collaboration.

The value of this experience lies in demonstrating how the Shenzhen Municipal SASAC, managing trillions of yuan in non-innovative assets, can respond to markets and innovation with maximum agility.

Part 05

Respecting the Market

The state asset system's requirements for security have always been in tension with the "risk" in venture capital. But innovation is born with risk; therefore, if state capital wants to drive social capital toward independent innovation and industrial upgrading through equity investment, respecting market principles and delegating authority within certain boundaries is a required course for growing into "bold capital."

5.1 Futian Guidance Fund

Patience and Delegation

Across the country, Shenzhen's state institutions stand out as exemplars of market-based approaches. After all, Shenzhen is the home base of RMB funds and the birthplace of Chinese venture capital. For instance, Shenzhen enacted China's first local venture capital regulation in 2003. Another landmark: the now 25-year-old Shenzhen Capital Group chose Kan Zhidong — one of the "Three Godfathers of China's Securities Industry" — as its leader on day one specifically for his "more market-based experience."

Li Fan, CEO of Fujian Capital, once said: "The defining feature of Shenzhen's funds is that the government only exercises veto power over projects on compliance grounds."

Futian District is Shenzhen's financial hub, and its guidance fund may well be the city's standard-bearer as an LP — one that also shoulders heavy responsibilities. According to Hurun's 2024 Global Unicorn Index, the Futian Guidance Fund and its sub-fund cluster have invested in 122 global unicorns.

But more important than results is the establishment of systemic frameworks. On December 10, 2024, the Futian Guidance Fund announced that, in response to the policy call for "patient capital," it would extend the lifespan of all its managed sub-funds by two years — making it the first fund in China to officially announce such an extension.

As of end-November 2024, the Futian Guidance Fund had cumulatively participated in 51 sub-funds with combined scale of approximately RMB 160.447 billion. Its GP selection logic has evolved through four phases: first, local top-tier venture institutions such as Shenzhen Capital Group, Fortune Venture, and Songhe Capital; then financial institutions with strong market returns; then CVCs backed by listed companies with real-economy backgrounds, valued for their "advantages in investment attraction and M&A exits"; and finally, investments in national and provincial mega-funds, with the requirement that they establish operations in Futian to create amplification effects.

In interviews, the Futian Guidance Fund has summarized how it built a sound, market-oriented sub-fund selection system. The key lies in "selecting GPs." Thus, in its agreements with sub-funds, it primarily specifies industrial direction and a mandatory 1.5x reinvestment ratio, with explicit stipulations that: LPs only review project compliance and do not evaluate or interfere with the projects themselves.

5.2 Jiangsu High Investment Group

Profit-Sharing and Liability Exemption

Beyond exercising flexible, market-oriented management of sub-funds and GPs, state capital has recently been restructuring its own organizations — with something of an attitude of "keeping the talented in the halls of power rather than sending them into the rivers and lakes." Xu Jinrong, previously Chairman and Party Secretary of Jiangsu High Investment Group, once told media: "Managers like us in the market earn RMB 5–10 million annually, but we can only take RMB 300,000–400,000. The gap is too wide."

Jiangsu High Investment's response: mixed-ownership reform and employee stock ownership.

As of 2023, Jiangsu High Investment's total fund assets under management exceeded RMB 120 billion, covering government guidance funds, market-oriented funds, and specialized industry funds — making it one of China's largest provincial-level venture platforms. Better known, however, is its market-oriented investment platform Yida Capital, established in 2014. Through mixed-ownership reform, Yida Capital's equity structure gives Jiangsu High Investment a 35% stake, while certain Jiangsu High Investment managers hold up to 65% — allowing the management team to earn not just management fees and carry, but also excess returns through co-investment.

Beyond "profit-sharing," there is also "liability exemption."

Suzhou High-Tech Venture Capital has stated in interviews that Suzhou New District applies "due diligence exemption" to state-owned equity investments — if project risks force investment managers or administrators to bear losses, it could make state capital hesitant about early-stage projects.

Additionally, there are new-model state institutions like Shenzhen Investment Holdings Donghai, formed through a partnership between Shenzhen Capital Group, Cowin Capital, and Haier — an attempt to bring together government guidance funds, market-oriented managers, and industry players for investment.

5.3 Xiamen C&D Emerging Investment

Standing with the Market and Industry

C&D Emerging Investment is an independent platform under Xiamen C&D Inc. specializing in minority equity investments. C&D Group itself boasts impressive investment track records — for instance, its participation in Xiamen Airlines' capital increase and expansion in 2002, which, riding economic development and aviation industry dividends, generated returns of at least several dozen-fold.

To date, C&D Emerging Investment has committed to over 70 funds, covering more than 800 enterprises, with frequent GP collaborations including Legend Capital, China Renaissance, and Qiming Venture Partners. It has achieved 37 IPOs, including Bloomage Biotechnology, MicroPort CardioFlow, and Titan Scientific. Healthcare leads its investment focus — because Xiamen is neither a financial center nor a traditional manufacturing powerhouse, so it concentrates on lighter sectors like healthcare, TMT, and consumer, such as Mango TV and Bajiuming.

C&D leverages strengths and avoids weaknesses, focusing on healthcare, advanced manufacturing, and TMT/consumer new economy sectors. C&D Emerging Investment positions itself as an LP with industrial background and direct investment capabilities.

Investment cases include CATL, Mango TV, Pharmaron, MicroPort Scientific, and Bajiuming. Cai Xiaofan, General Manager of C&D Emerging Investment, noted at a forum that in most sectors, "you can achieve good market returns while also nurturing relevant industries."

Another expression of market respect: trusting market-oriented GPs. Over its more than ten years, C&D has invested in Legend Capital, Qiming Venture Partners, Mango Cultural and Creative Fund, Black Ant Capital, Cathay Capital, Centurium Capital, Gaorong Capital, and Source Code Capital — all star GPs. As of end-2023, it has supported over 60 GPs cumulatively, with 20 partnerships exceeding five years.

"Venture capital investment was quite different from our investments back then. Much of our early investing was industrial investment. This technology and innovation-oriented investing — we're not particularly skilled at it. What to do? Naturally, we invest in GPs and become GPs' LP. This lets us quickly understand these industries and how GPs do venture investing," explained Wang Wenhuai, Chairman of C&D Emerging Investment. The Mango Cultural and Creative Fund, for example, serves as their most important collaboration platform in cultural media within C&D's portfolio. Meanwhile, C&D Emerging imposes no restrictions on GPs regarding registration location or reinvestment ratios, making no additional demands — virtually a "perfect LP" in GPs' eyes.

"Market-oriented fund-of-funds and LPs with Chinese characteristics and professional investment management capabilities are a crucial link in the venture capital industry chain," Wang said.

5.4 Suzhou Oriza Holdings

The Culmination of 20 Years of Market-Oriented Practice

If the "Hefei Model" represents the ultimate expression of top-down will combined with bold decision-making rewarded, then the "Suzhou Model" emphasizes collaboration.

The "Suzhou Model" is an equity participation model: local government investment funds partner with institutions to establish sub-funds, bringing venture capital institutions to Suzhou, which then invest in local enterprises to drive regional industrial development.

Suzhou's most representative institution is Oriza Holdings. Controlled by Suzhou Industrial Park Administrative Committee with Jiangsu Guoxin Group as a participating shareholder, Oriza Holdings manages multiple funds: Oriza Green Willow (Southeast Asia-focused), Oriza Genesis (early-stage), Oriza Huawang (growth-stage), Oriza Puhua (integrated circuit industry), and Oriza Chenkun — China's first market-oriented professional fund-of-funds team, jointly launched by Oriza Holdings and China Development Bank in 2006.

Where does "market-oriented" show? Oriza Chenkun, it is understood, has never had reinvestment requirements and does not interfere with investment destinations, requiring only that registration be in Suzhou.

Oriza Chenkun is often mistakenly considered not a government guidance fund because, although its primary goal is also boosting regional economic development, its operations are highly market-oriented — inseparable from its connection to Suzhou Industrial Park.

When Oriza Chenkun was founded in 2006, it was a critical moment for Suzhou Industrial Park's transformation. At that time, as the park's sole state-owned investment platform, Oriza Holdings had already recognized that directly investing in local enterprises could only leverage limited resources. It should bring more VC institutions to the park to invest in local enterprises, using market-oriented methods to achieve investment attraction — and this task naturally fell to Oriza Chenkun. From then on, Oriza Chenkun began inviting investment institutions to establish in Suzhou, organizing multiple events annually to bring investors to see projects. No reinvestment requirements were needed; as long as the investment environment and projects were good enough, the market would vote with its feet.

In recent years, as introduced investment institutions have reached scale, an East Shahu Fund Town was established in eastern Suzhou Industrial Park, officially passing Jiangsu Provincial Development and Reform Commission inspection in January 2023. With fund industry as its focus, the town has cumulatively hosted 267 equity investment management teams, established 563 funds, and aggregated capital exceeding RMB 289.6 billion — far surpassing the scale of some government guidance funds claiming hundreds of billions.

Part 06

The Courage Multiplier

In fact, state capital has no shortage of marvelous stories of courage and boldness.

One day in 1999, the chairman of Hunan TV & Broadcast Intermediary told an assistant: "I'll give you RMB 100 million. Go to Shenzhen and start a venture capital company." TV & Broadcast Intermediary had recently gone public and already tasted capital's sweetness. And the chairman's "boldness" was also a response to market rumors that "the Growth Enterprise Market is about to launch."

This assistant was Liu Zhou. The institution was Dachen, which would later carve out a unique position in the RMB market. Recently transferred to TV & Broadcast Intermediary, he plunged into Shenzhen with venture capital seeds in hand. Then, from the GEM's suspension in 2001, TV & Broadcast Intermediary treated Dachen's losses with patience and tolerance — but Dachen's pattern of "only spending money, not booking revenue" still somewhat shook the parent company. In 2005, the board once passed a resolution to shut down Dachen entirely, leaving just one or two people to wind things down.

Dachen Chairman Liu Zhou, then in Beijing's Fragrant Hills, spent two days upon receiving the news writing a "ten-thousand-character letter" to shareholders — "Preserve the business, keep the flame alive." Ultimately, TV & Broadcast's management decided: "Give it one more year." Fortunately, 2006 arrived as promised, and Dachen welcomed its first successful exit — Tongzhou Electronics, achieving 40x returns.

And Hefei's rescue of NIO from the ICU with RMB 7 billion — its perilousness remains unsurpassed to this day. This move also cemented Hefei's reputation as the venture capital city.

Before Hefei's capital injection, Li Bin had been rejected by 18 cities from north to south. State capital was his last chance. Recalling this experience, he said: "Only government sees very far ahead. No investment institution would save us."

Founded in 2006, Hefei Construction Investment initially was merely a traditional urban investment company. The turning point came in 2008, when BOE — primarily engaged in new display panels — encountered difficulties. With recognition and support from Hefei Municipal Party Committee and government, it chose to invest through equity participation. According to China Economic Weekly, Hefei Construction Investment invested RMB 47.8 billion in the BOE project cumulatively, has fully exited RMB 24.4 billion of that, with profits of RMB 23.1 billion on the exited portion.

"Back then, few local state-owned assets dared to use equity investment methods. Most would lend you money, but that's debt — a heavier burden for enterprises. We went in with equity, sharing their fortunes and setbacks," Li Hongzhuo later recalled.

This set Hefei Construction Investment on a path different from most urban investment companies — daring to make heavy bets on major projects, which also laid groundwork for the NIO story 12 years later. More critically, bold Hefei seized two major industrial clusters: display and new energy. Currently, six complete vehicle manufacturers have established operations in Hefei — JAC, BYD, NIO, Volkswagen, Changan, and Ankai.

The "boldness" of the above state capital is merely a public-facing image; the deeper foundation is local governments' willingness to bear risk and responsibility for technological innovation and industrial upgrading. A journalist visiting Hefei once wrote with feeling: "Only with great responsibility can great undertakings be accomplished; only with full commitment can great achievements be made." This statement will have even more profound influence and significance for every local government and official now standing under the banners of technology, industry, innovation, and development.

Image source | Unsplash / AnYong editorial department

Recommended Reading

Where money flows, people rise and fall