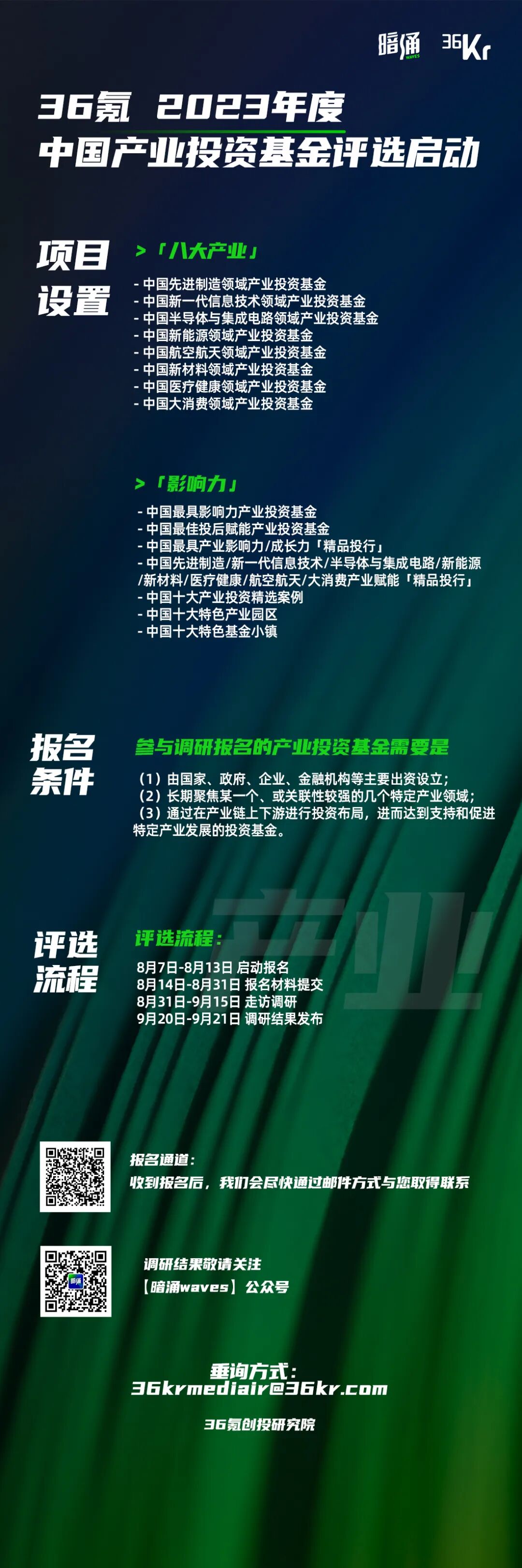

Which Corporate Venture Capital Fund Deserves the Spotlight Most | List Nomination

Welcome to the brave new world.

Produced by | 36Kr

We are standing at a new starting point for the venture capital cycle: structural transformation has already taken place on both the asset and capital sides.

The balance of dealmaking on the VC stage has visibly shifted from a TMT-centric distribution toward manufacturing across multiple sectors. From early 2022 to the present, nearly 70% of the 16,800 transactions in China's primary market have occurred in areas such as new energy, new materials, semiconductors, industrial robotics, and biomedicine. An even more pronounced trend is the exceptional activity of industrial capital on the venture stage — corporate investors have become the dominant source of funding directing market winds. CATL, one of the leading companies in the new energy sector, saw its absolute equity investment value surge from 965 million yuan to 17.595 billion yuan over the past five years, an 18-fold expansion — and this doesn't even include the numerous CATL-affiliated industrial investment funds that have spun off from it.

Behind this dramatic adjustment in the venture market lies the urgent need for China's industrial upgrading, driven by international competition. The reshaping of every link in the industrial chain will carry with it structural investment opportunities across the value chain.

Unlike the internet era, when investors needed sharp judgment about the rapid iteration capabilities of business-model innovators, the "industrial" mega-theme will demand far more diverse capabilities from investors. They must identify fields with global horizontal competitiveness based on technological content, supply chain complexity, and standardization; then, combining vertical growth velocity and cyclical characteristics at different development stages, filter for industrial chain investment opportunities with greater long-term value. Without question, only by embedding oneself more deeply within industry can one track the market more closely and judge it more accurately.

As massive waves of industrial transformation crash in, we see numerous participants rushing in: state-level industrial funds with substantial financial resources and policy foresight serve as the most critical force directing capital into core industries; local governments, as key coordinating units for implementing industrial upgrading, use equity investment to address a series of regional economic development goals including tax revenue, employment, and GDP growth; market-oriented funds with strong industrial attributes have also developed flexible maneuvering capabilities amid the changing landscape, uncovering latent industrial opportunities and contributing value; and CVC divisions at industry-leading companies have been more explicitly positioned as "watchtowers" to help their firms keep pace with industrial evolution...

With "industry" elevated to its current strategic height, we urgently seek to identify the real forces making an impact across various sectors. Standing at this new starting point of the venture capital cycle, we are launching the "China Industrial Investment Funds" research initiative, broadly soliciting funds that meet the definition of "industrial investment" — that is, funds established with capital from the state, local governments, enterprises, financial institutions (insurance, pension funds), family offices, and other sources, which maintain a long-term focus on one or several closely related specific industrial sectors, and achieve the goal of supporting and promoting the development of particular industries through investment and strategic positioning across upstream and downstream segments of the industrial chain.

Unlike "financial investment funds," our evaluation of "industrial investment funds" will extend beyond standard financial metrics, such as (1) assets under management; (2) investment reach (geographic and sectoral scope); (3) investment activity (number and value of deals); (4) investment performance (number of star projects, IPO count).

Beyond this, we will further investigate through site visits and due diligence how industrial investors perform on dimensions including (1) management team's industrial background; (2) the industrial group's capital contribution ratio to the fund; (3) industrial investment strategy; (4) policy alignment (consistency with national and local policy guidance); (5) industrial fit (whether investments effectively center on the industrial group's core business or focus on specific industries); (6) degree of industrial empowerment (whether they assist portfolio companies in business cooperation with the industrial group, providing integrated services in management, technological innovation, market expansion, and more).

> Below are the guidelines for the "China Industrial Investment Funds" selection:

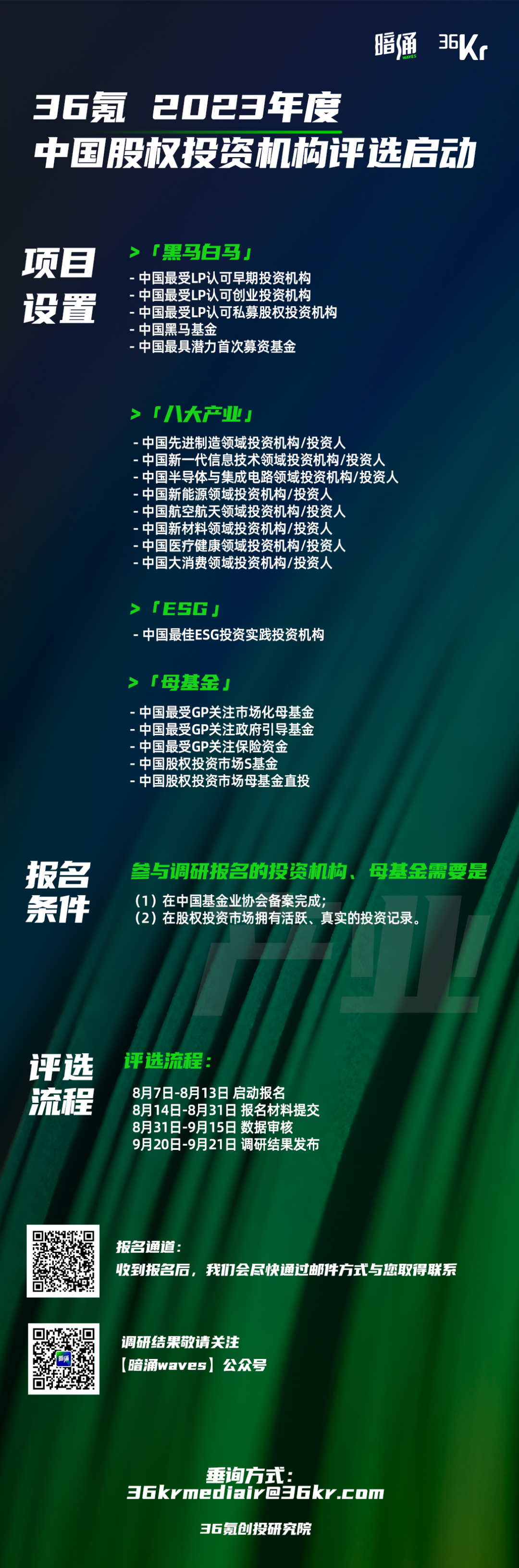

At the same time, we are also launching the 2023 White Horse / Dark Horse Institutions, Eight Major Industries, ESG, and Limited Partner research initiatives, continuing to track those investment institutions that adapt flexibly and maintain their edge in this new venture capital cycle.

> Below are the guidelines for the "China Equity Investment Institutions" selection:

Image source | Visual China

Layout | Meng Du