Entrepreneurship Is the Most Hardcore Way for Young People to Change the World | Mono X Campus

Be a long-term partner to founders, not a short-term "referee."

The driving force of technological revolution has always come from the younger generation. This isn't just a romantic belief — it's a fact repeatedly proven by history.

Monolith seeks out and supports young people with ambitions to change the world, hoping to offer them genuine backing when they first set out to create something new. We also believe that a cohort of young people poised to reshape the future is right now gestating the next wave of transformation — in classrooms, labs, lecture halls, and dorm rooms.

Recently, Monolith founder Xi Cao and Iason Bance, an investor from European firm Sofina & Monolith, visited Tsinghua University and Peking University respectively to speak face-to-face with young people, sharing firsthand insights on entrepreneurship and venture capital.

This article is compiled from Iason Bance's talk. For young people eager to enter the VC industry or considering starting a company, it may offer some inspiration and food for thought.

Monolith will also be hosting MonoX, an event for founders, in the near future — bringing together the most transformative young people of this era for a relaxed, genuine, and open discussion. Scan the QR code below to join the conversation (whether to share or to listen).

Table of Contents:

-

The World of Investors

-

Key Factors for Success

-

The Core Logic of Venture Capital

-

Becoming a Top-Tier Investor

-

The Essence of Entrepreneurship and Investment

Breaking Stereotypes: The Real Worlds of Founders and Investors

Today, we want to share from two perspectives — both the investor's and the founder's. The reason for this dual lens is that society often harbors misconceptions about both groups.

People typically assume VC investors are arrogant know-it-alls, while founders are seen as product-obsessed or fundraising-obsessed storytellers. In reality, both views are overly simplistic. Only by truly understanding what each does and why they do it can we see the roles they play in this ecosystem.

1. The World of Investors

1.1 How Does a VC Fund Operate?

Let's start from the investor's perspective.

Suppose there's a $100 million venture capital fund. The team running it is called the GP (General Partner), and their primary task is to raise capital from LPs (Limited Partners).

LPs can be large institutional investors or family offices, among other types of capital providers. The GP then deploys this raised capital into promising emerging companies, providing them with resources and support. The ultimate goal: turn that $100 million into $300 million, $500 million, or even $1 billion.

Of course, this work isn't free. GPs charge LPs two types of fees: management fees and carried interest (Carry). Management fees typically run 2% of fund size, paid annually during the investment period. For a $100 million fund with a 5-year investment period, total management fees would amount to $10 million.

Carry is an incentive mechanism — the more the fund earns, the greater the GP's share of profits. If the fund ultimately generates $200 million in profit, the GP takes 20% as Carry, or $40 million. This gives GPs strong motivation to hunt for companies capable of delivering outsized returns.

In other words, a fund's operating costs (including management fees and Carry) might reach $50 million. For the investment team, this is both motivation and pressure.

We've calculated that if a fund's lifecycle is 12 years and it ultimately achieves 3x total returns, the net annualized return works out to roughly just 8%.

This raises the question: If the returns aren't particularly high, why don't LPs simply invest in index funds or other stable financial products?

1.2 Power Law and Extreme Risk Structure

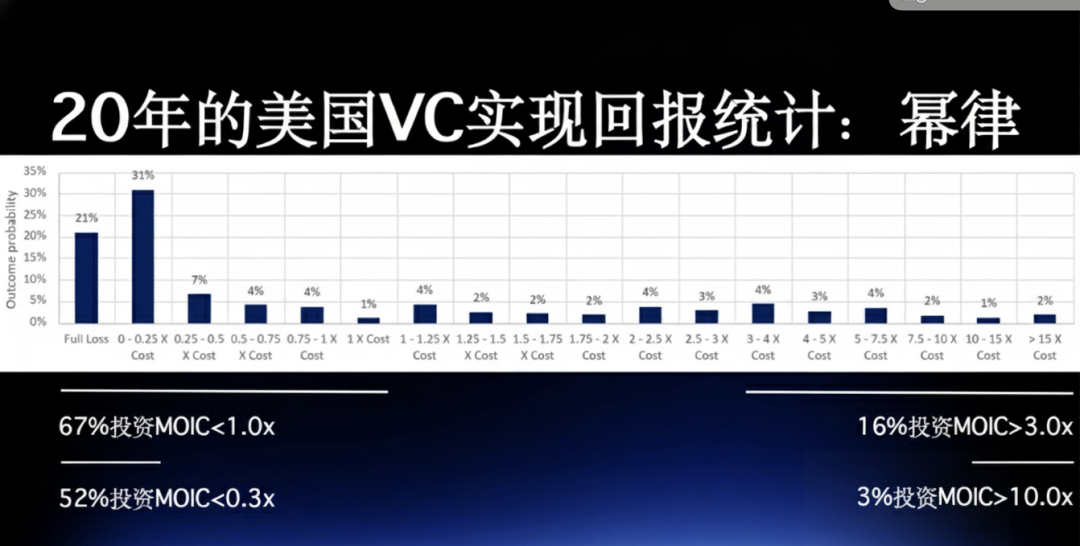

The answer lies in the power law distribution of venture capital returns. Simply put, VC returns are extremely uneven.

Suppose a $100 million fund invests in 10 startups. Reality often looks like this: one company delivers 20x or higher returns — say, $10 million invested becomes $200 million — while most of the rest generate meager returns or lose everything.

When all project returns are aggregated, the fund's total return might only reach about 3.2x — and that's gross return, before fees and taxes. If you miss that "super-unicorn," the fund's overall performance suffers dramatically.

Data shows that in a fund portfolio, measured by invested capital, the top 10% of companies typically contribute 60% to 70% of total returns. This is a pattern validated repeatedly within the industry.

From our experience across more than 50 years of fund investing, companies that ultimately deliver over 15x returns represent only 2% of all investments, while losing investments account for as much as 70%. This is the reality of venture capital.

1.3 The Social Value of VC

Given such high risk and such common failure, what then is the point of venture capital?

The answer: Without VC, many world-changing companies might never exist at all.

Think of these names: Xiaomi, Mindray, WuXi AppTec, CATL, Meituan, Li Auto... nearly all of these enterprises have venture capital in their DNA. VC was their earliest "believer," willing to bet on them before mainstream recognition.

Without venture capital backing, these "crazy" ideas might have died at the starting line. VC is a vital force driving innovation and industrial upgrading — it doesn't just create wealth for LPs, but injects new vitality into society.

1.4 Why Do the Best Funds Succeed?

While average returns across the VC industry aren't particularly high, the top funds still achieve outsized returns. The top 5% of funds often deliver annualized returns exceeding 20%, indicating that Alpha — returns above market average — does exist in this industry.

Elite funds share two common characteristics:

-

Fund size shouldn't be too large. The number of truly quality companies is limited; too much capital makes it difficult to concentrate bets on the best opportunities. The number of companies that can truly become "super-unicorns" each year may be just a handful.

-

Investors must possess the ability to "see, understand, get in, and get out." This is the core criterion for judging whether a GP is excellent.

Of course, VC isn't a perfect system. Capital can sometimes exert excessive pressure on founders, tempting them to deviate from long-term goals for short-term returns; in hot sectors, overheated competition can even lead to wasted capacity.

This reminds us that both investors and entrepreneurs must choose sectors capable of creating genuine differentiation and innovative value. Companies built on storytelling and pure cash-burning will eventually go to zero.

2. Key Factors for Success

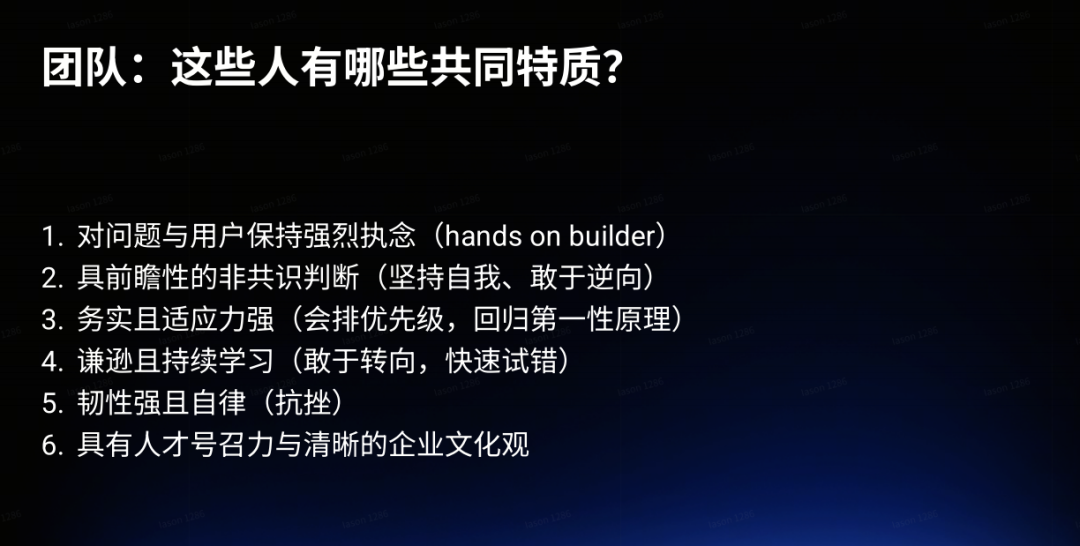

2.1 Team: Founders Determine a Company's Ceiling

Behind every successful company, the founding team is often the most critical determinant. An exceptional founder can almost single-handedly change a company's destiny.

Based on long-term exchanges and observations with top VCs and companies at home and abroad, we've identified six traits commonly found in outstanding entrepreneurs:

1. Intense obsession with problems and users.

2. Forward-looking, non-consensus judgment.

Successful people often dare to bet on directions most others dismiss. Take Li Auto as an example: in its early days, it chose the extended-range electric vehicle (EREV) technology path. Many in the industry considered this a wrong turn, but the Li Auto team saw an opportunity with relatively sparse competition and clear user pain points. Time has proven their judgment correct — Li Auto's profit margins today speak for themselves.

3. Pragmatism, rationality, and first-principles thinking.

This means breaking problems down to their most essential level, then prioritizing and adjusting direction accordingly. A classic example is Pony Ma. In 2011, when QQ was already a national-level product, he still decided to have his team go all-in on WeChat. Even though WeChat might compete with QQ, he insisted: "Whichever product is better and more representative of the future, that's the one we support." This way of thinking is based on first principles — focusing on what's truly beneficial for the company in the long run, not immediate interests.

4. Humility, continuous learning, and rapid experimentation.

After three years in the gaming business, Yiming Zhang realized it was dragging down ByteDance's overall profit margins, so he decisively spun it off and walked away — even though it meant "cutting off something he loved." If even such a large company can correct course from mistakes, how much more so for early-stage entrepreneurs?

5. Resilience and self-discipline.

6. Ability to attract talent and shape culture.

2.2 Sector: Choosing the Right Direction Matters More Than Hard Work

Beyond team, sector selection is another key factor determining whether a startup succeeds.

An exceptional founder who chooses the wrong sector may still fail. For VCs, this is even more true — pick the wrong industry, and even the most precise bets may yield nothing.

So what makes a "good sector"? We've identified some patterns.

1. Sustained growth with deepening moats

First, it must be a market in sustained growth. More importantly, this market must enable ever-strengthening moats. The deeper the moat, the more defensible a company's competitive position.

The essence of moats is often network effects: more users means greater product value, which means higher switching costs. WeChat is the most typical example — as user numbers grow, social networks become denser, making any new platform difficult to dislodge.

If a business lacks such accumulation mechanisms, it easily falls into low-margin, low-profit predicaments.

2. No middlemen

Ideally, a company should be able to reach end customers directly. If it must rely on distributors or intermediary channels, that means market control rests with others. For B2C businesses, serving users directly not only improves efficiency but also yields more authentic feedback.

3. Dispersed suppliers and customers

Supply chain structure matters too. If upstream suppliers or downstream customers are overly concentrated, a company's bargaining power is squeezed. Conversely, when supplier and customer bases are sufficiently dispersed, the company's negotiating position in the chain strengthens.

4. Short customer value realization cycle

This means customers can perceive value relatively quickly after purchasing a product or service. If customers need six months or even a year to see results, sales and marketing become difficult. The ideal model lets customers be "wowed" in the shortest possible time, willing to repurchase or continue paying.

5. High margins and differentiation

Gross margin is a direct reflection of product differentiation. High margins typically mean customers see your product as unique and irreplaceable, willing to pay a premium. Conversely, if products are heavily homogenized, you're left fighting price wars.

6. Extensibility

Finally, a good sector should offer room for extension. In other words, when the core business matures, are there natural directions for expansion? Whether moving up or downstream from the core product, or deriving new service models — this determines a company's future growth potential.

2.3 Avoiding "Trap Sectors"

If there are good sectors, there are naturally bad ones. We consider the following common "difficult sectors":

Low-frequency consumption: Too few usage scenarios, low repurchase rates, difficulty achieving scale effects.

High customization: If products or services must be tailor-made for each customer, standardization and scaling become nearly impossible.

High customer churn: Especially when the customer base consists of small and medium enterprises, low survival rates mean extremely unstable revenue.

Dependence on specific channels or regulatory environments: For example, the "double reduction" policy in education forced countless companies to pivot overnight. Founders must assess policy risk.

Long payment cycles: If primary customers are large enterprises, slow capital recovery severely impacts cash flow.

Before starting a company, founders must repeatedly ask themselves:

"What is my moat? Does it deepen as I scale? Is the sector I'm in truly the right one?"

These questions often determine a company's fate.

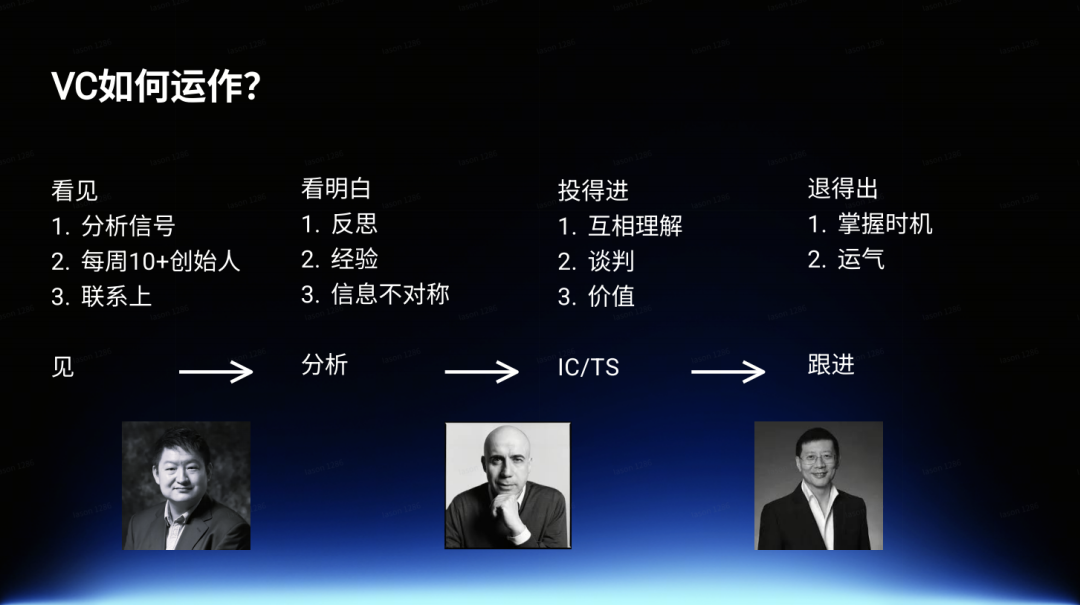

3. The Core Logic of Venture Capital: See, Understand, Get In, Get Out

Now let's discuss how VC operates. In eight words: see, understand, get in, get out.

3.1 See: Discovering Opportunities

First, you must be able to "see." If you can't even access deals, there's nothing to discuss.

Investors are constantly capturing information: browsing industry news, WeChat articles, data reports, discovering potential deals through various channels. For early-stage investing, the volume of deals is enormous — investors typically meet with more than ten new companies weekly.

I personally meet with about 10 new startups each week, and many of them don't actually reply to emails or agree to meetings. For entrepreneurs, I have one simple but important piece of advice —

Leave an entry point on your company website where investors can reach you directly.

Whether an email address or a form, it could become your first step toward connecting with capital.

3.2 Understand: Judging Value

After meeting with entrepreneurs and engaging in deep conversation comes the step of "understanding."

This step appears simple but is actually the hardest. It requires investors to discern in complex markets: is this sector worth betting on? And if so, could this company be the one that wins in this sector?

True masters often possess an "information asymmetry" advantage — knowing what others don't. This insight typically comes from accumulated experience, industry understanding, and cross-domain comparison.

3.3 Get In: Winning the Opportunity

After understanding, you still need to "get in."

This isn't just about judgment ability, but the art of negotiation and strategy. Globally renowned investor Yuri Milner is a classic example. In 2008, he invested $200 million in Facebook for 2% of the company — today that stake is worth over $30 billion.

He succeeded in getting a seat at the table because he himself came from an entrepreneurial background and deeply understood internet product logic. When he saw Facebook's data, he immediately recognized this as the super-platform of the future. So in negotiations, he told Zuckerberg: "I don't care about board seats or veto rights, I just want to invest — even if it means buying secondary shares."

His confidence came from insight into the product and founder, and from tremendous execution capability. Because he knew — "I absolutely must get in." This is the combination of "understand" and "get in."

3.4 Get Out: Exiting Successfully

Finally, "get out." To realize returns on investment, you must be able to exit at the right time.

Take a well-known domestic fund's investment in DJI as an example — when they realized changing US regulatory conditions might make exit difficult, they decisively chose to exit early, locking in gains. The ability to coolly make such decisions amid complex situations is a capability top-tier investors must possess.

4. Becoming a Top-Tier Investor

To become a truly top-tier investor, the required traits are strikingly similar to those of excellent founders: both must think in first principles, both need continuous learning ability, tremendous resilience, and an almost obsessive passion for their goals.

Among the top investors I know, their minds are occupied by almost nothing else — finding and investing in great companies.

Their passion for investing borders on obsession; some might even say they have no other interests. It is precisely this focus and dedication that allows them to constantly discover overlooked opportunities.

4.1 Non-Consensus Conviction

Additionally, excellent investors often share one common trait — they possess contrarian conviction.

In other words, they dare to act decisively based on independent judgment when most others are bearish. The core of VC isn't "following trends," but whether you can see through the chaos to the future.

If a view is already accepted by the masses, it often means the investment opportunity has already been priced in. Conversely, those opportunities ignored by the mainstream are where outsized returns might be born.

But this doesn't mean blindly taking contrarian positions. True "non-consensus" isn't stubbornness, but deep understanding of facts and forward-looking insight into trends.

4.2 Maintaining an Open Mind

At the same time, top-tier investors understand the importance of staying open.

In the world of investing, there are no absolutely correct judgments. You may be skeptical of a particular sector, but reality often proves that the strongest founders can make work modes you originally thought "wouldn't work."

Therefore, excellent investors don't prematurely dismiss any direction, but continuously observe, listen, learn, and leave room for reality to teach them.

4.3 Patience and Goodwill

Finally, and what I most want to emphasize: truly excellent investors understand patience and goodwill.

The essence of venture capital is "high risk" — it's right there in the industry's name. Since this is the case, investors shouldn't expect to see results within a year or two. Pressuring founders to deliver returns in the short term not only violates the nature of the business, but may also disrupt founders' rhythm and original intentions.

The meaning of capital isn't just money, but understanding and support. A good investor should be a founder's long-term partner, not a short-term "referee."

5. The Essence of Entrepreneurship and Investment

5.1 Classic Questions from Top Investment Institutions

To make this more concrete, let's look at what the world's most renowned early-stage institutions typically ask when evaluating entrepreneurs.

Y Combinator (YC) keeps its questions simple:

- What problem are you solving?

- Why does this problem matter?

- How do you verify this demand actually exists?

- Why is now the right time to do this?

These questions seem basic, yet they encompass the entire logic of entrepreneurship. Any team unable to clearly answer them hasn't truly understood their own business.

Founders Fund (founded by Peter Thiel) prefers philosophical questions:

- "What important truth do very few people agree with you on?"

Benchmark asks:

- "Where does your Secret Insight come from?"

Accel emphasizes customer understanding:

- Who are your target customers? Who are your non-target customers?

They want founders to be crystal clear about: what they won't do, and who they refuse to serve.

Greylock focuses more on expansion logic:**

- "What is your path to scale? From step one to step two to step three, how does the business naturally grow?"

5.2 Co-Founders: Vision and Mechanisms

Many top investors also ask another question:

- "How do you and your co-founders handle disagreements? What mechanisms help you stay aligned?"

This is because VCs have seen too many companies die from "internal dysfunction."

If the founding team lacks shared vision, or if incentive mechanisms aren't aligned, even the best product and largest market may crumble due to internal conflict.

So in the early stages of a startup, the team must confirm whether they truly want to do the same thing, whether incentives are fair, whether long-term goals align. This is often more fatal than the business model itself.

5.3 The True Meaning Behind Investors' Questions

These questions aren't meant to trip up entrepreneurs, but to help them discover blind spots.

An entrepreneur who can answer these questions with composure has typically already thought deeply about their business.

In other words, before fundraising, try asking yourself these questions from an investor's perspective.

If you can answer yourself with logical consistency and data support, then no matter which investor you face, you'll handle it with ease.

Conclusion

Finally, I want to close today's talk with three points.

One, investing is a high-risk game of probabilities.

Building something from 0 to 1 is fundamentally a high-risk exploration. It requires a bit of madness, and the courage to fail.

The probability of success is low — this is true for both entrepreneurs and investors.

The venture capital industry is equally brutal — if an investor hasn't backed a standout project in ten years, they may be forced out of the industry. For young people, the timeline is even shorter, perhaps just two or three years.

But precisely because of this, once you succeed, the rewards are sufficiently massive.

It is this high-risk, high-reward uncertainty that attracts a group of people willing to take risks and passionate about creation.

Two, don't tie your self-worth to your company.

A company may fail, but that is merely an event, not a personal failure.

Entrepreneurship is a journey, not an exam. True growth comes from experience and learning, not from outcomes themselves.

Statistically, the most successful entrepreneurs are often serial entrepreneurs — don't easily dismiss someone because of previous failures.

Three, success requires luck.

Whether founder or investor, we've seen people with tremendous ability and execution who still didn't succeed. We've also seen seemingly ordinary people who, at a particular moment and in a particular sector, seized an opportunity and leaped to become industry legends.

The role of luck is often underestimated. But truly mature people respect luck while also knowing how to create conditions for good fortune.

As the old saying goes: "Luck is what happens when preparation meets opportunity."

You can't control the wind, but you can adjust your sails — and so it is with life.