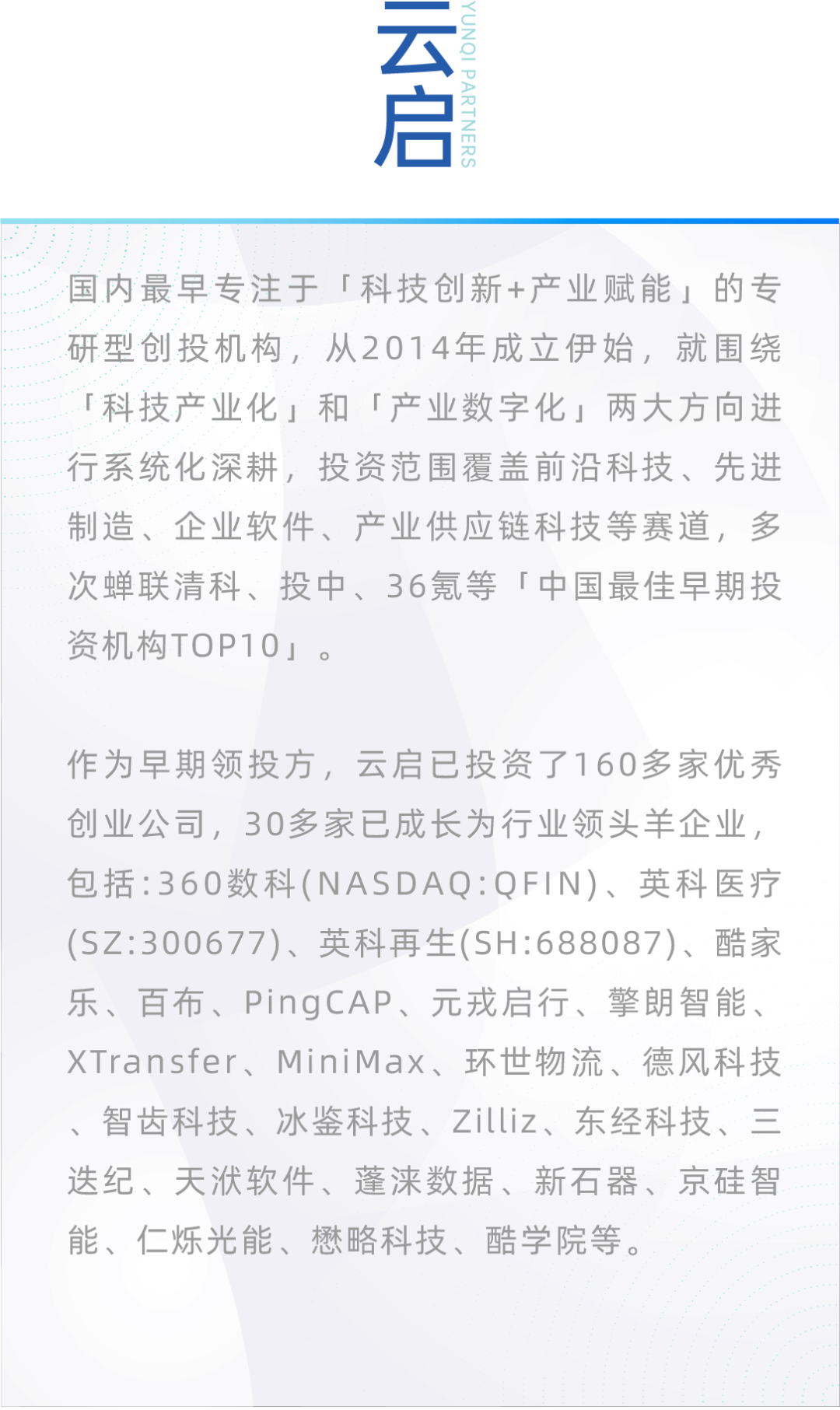

Think of Yourself as a Large Model: Quantity First, Then Emergence | ASK VC x Yunqi YoUNg Talent

Actively explore, accumulate over the long term, embrace complexity.

What is the YoUNg Program? — It's a tech ToB young investor training program initiated by Yunqi Capital. Nearly 100 young people who are passionate about tech ToB, self-driven, and goal-oriented come together here to learn and grow rapidly. We respect diversity and encourage new experiments. You'll not only receive 1-on-1 mentorship from professional advisors, but also expand your thinking and explore independently on the front lines of the tech industry.

The new cohort of the YoUNg Program is now recruiting on a rolling basis. Click here for detailed job information.

Recently, YoUNg Talent partnered with ASK VC to host a dialogue event. Yao Feng, Managing Director at Yunqi Capital, engaged in a three-hour intensive Q&A session with a group of passionate, thoughtful young people. They discussed topics including industrial digitalization, AI's empowerment of industrial upgrading and intelligent industrial scenarios, and the differences between software and hardware investment. Below is a transcript of the dialogue. Enjoy~

Yao Feng, T-LAB Mentor

Managing Director, Yunqi Capital

Graduated from Peking University with a degree in finance. Focus areas include industrial digitalization, enterprise services, and healthcare.

Led and participated in investments in Baibu, JD Industrial, Dongjing E-commerce, Xiaoyang Education, Penglai Data, Bailing Intelligence, Lingmao SCM, and other projects.

Named to Forbes China's "30 Under 30" list, recognized by Sci-Tech Innovation Daily as "Pioneering Investment Force," and was the youngest finalist in PEDaily's 2020 "F40 Outstanding Young Chinese Investors."

Q&A Highlights

New Technologies, New Industries — How Can Young People Seize Opportunities?

Q: Industrial digitalization is a massive track. How do you break it down and analyze it? How do you choose which industry to research first? How do you screen targets? And how does AI empower industrial upgrading and intelligent industrial scenarios?

A: First, I believe that for any industry we're not familiar with, whether top-down or bottom-up, the principle of quantity leading to quality never lies. For example, a friend of mine, when looking at an industry, put in the hard work of first examining all overseas related products, testing them one by one, and following up on their progress every quarter. He even reached out through Facebook to the teams behind these products to maintain continuous tracking and mapping. But it was precisely because of this accumulation that he was able to invest in similar successful products domestically.

From my own perspective, I'd like to share three points:

- We ourselves are also an AI model. The people and things you encounter daily are your input, and you need to adjust your algorithm through this input to ultimately produce an output. We need sufficient quantity to build our own model. Otherwise, it's hard to say whether the project you're seeing now ranks in the top 10, top 50, or beyond 100. At the same time, you need to constantly review past projects to see if your previous assessments were correct, and then adjust your model based on this feedback.

To be specific, in the earliest stage I mapped out roughly 40 to 50 industries. Vertically, I broadly divided industries into raw materials (such as steel, yarn, coal), industrial semi-finished products (such as textile fabrics, industrial auto parts, components), and consumer goods (such as FMCG, alcohol, 3C, apparel). Each segment contains more than a dozen industries, and each sub-industry can be further subdivided. For example, in textiles, from upstream to downstream, you have cotton, chemical fiber, yarn mills, weaving mills, dyeing and finishing mills, fabric distribution markets, garment factories, wholesale clothing markets, Taobao e-commerce or foreign trade, and retail stores. So this absolutely requires putting in the hard work to study.

-

When choosing specific industries, I tend to prefer industries with longer and more complex supply chains. Because the more complex they are, the more opportunities there may be for transformation. So at that time, we deliberately picked the toughest, most difficult-to-understand industries to research.

-

When you don't know much about an industry early on, I more recommend starting from the top down. Once you figure out an industry, especially its first principles, 50% of your model can be reused for other industries, and 50% can be customized for the specific industry. Subsequent bottom-up work can then expand on this foundation.

Q: You previously invested in Penglai Data, and last November Yunqi Capital continued to increase its stake. For enterprise service software, is AI capability a necessity? Or do you think there are still enterprise software companies that won't be displaced by AI?

A: This is a highly topical and worthwhile question.

I believe that enterprise service companies that don't embrace AI will definitely face significant challenges. The reality now is that most companies are thinking about how to layer on AI capabilities. Here, I need to first explain some differences between the Chinese and American software ecosystems:

First, I personally believe that China doesn't really have purely productized companies. What we have more of is productization plus project-based work, productization plus customization, productization plus supply chain, productization plus services, or deep vertical industry integration. The reason behind this is that different industries have very strong demand differences, awareness gaps, and data barriers, so it's unlikely that there will be a complete set of best practices that can be productized and applied across different industries, as you see in the US.

Second, the payment environments in China and the US are also very different. More capital in China flows to large and medium-sized enterprises, while in the US, significant funds do flow to SMBs (small and medium businesses). This makes it more viable in the US to support a PLG (product-led growth) company.

My view is that the more PLG and the more generalized a product is, the greater the disruptive potential of AI — or the likelihood of it being displaced. However, for pure AI-native companies in vertical industries, displacing an established software company that has already secured its position in the industry is extremely difficult. Companies that can survive long-term and do well in China, especially at the application layer, often have very strong ecosystem positioning. For example, if a large model company wants to enter a specific industry, you'll first face the question of whether the client is willing to give you their data. Second, does the client trust you? Third, do you have sufficient business development capability to win these orders? Only after that comes whether you have enough delivery, operations, and service capabilities to solve the specific problems of that industry.

So the impact of AI now is that it has improved efficiency, while also dramatically changing cost structures and core competitiveness, lowering the technology barrier. This has brought more people into this track, making competition at the application layer more intense. But looking back, while technology barriers have been lowered, data barriers, industry knowledge barriers, and business development capabilities remain — and these are often even more important in China than in the US. So without these capabilities, it's still very difficult to sustainably hold a strong position in China.

Q: Many of the companies we invested in before probably already existed abroad, whether in internet, industrial internet, or SaaS. But AIGC is just getting started both domestically and internationally. We don't have benchmarking objects. Business models haven't been proven out anywhere. Many models are open source. In this situation, how should investors make investment decisions?

A: First, looking back, even during the mobile internet era, aside from underlying technology, application-layer innovation in China far surpassed that in the US. Many excellent companies visible in the market today are innovations based on China's ecosystem. My own feeling is that we do look at how US companies have grown, but what can actually be borrowed probably doesn't exceed 20%. More importantly, we need to look at what China's soil is like, what product forms should look like in China, what China's ecosystem structure is like, and what different points exist based on China's environment. So simply copying is very difficult to succeed.

Second, I believe that in the current immature state of AIGC, we need to follow changes more closely. Now, whether entrepreneurs or investors, everyone is groping in the dark. So mentally, you need to embrace change. When evaluating CEOs, we pay more attention to whether they are open-minded enough, capable enough, and forward-looking enough. AI's transformation of various industries is basically inevitable. But taking a longer view, this transformation will certainly go through stages from peak to trough to maturity.

Third, there is indeed a large gap between China and the US at the underlying technology and foundational model level. This is also the biggest challenge and uncertainty for future development on the application side.

Treating Yourself as a Large Model — How to Train?

Q: I come from a business background, but now many VCs prefer science and engineering backgrounds. How should I compensate for this?

A: First, looking at the conclusion: whether within Yunqi or across the entire VC industry, whether at the director level or up to managing partners, people's professional backgrounds are very diverse. So we need to return to two essential points:

-

VC itself is a highly non-standardized profession. Therefore, whether you have a science or engineering background doesn't directly determine long-term career success. Funds don't have rigid criteria when looking for team members.

-

The current preference for science and engineering backgrounds is a strategic supplement for institutions. For example, if an institution lacks talent in new energy, they'll want to find professionals in that field. But from a market perspective, looking back at the development of VC over the past 20 years, people from different backgrounds have had opportunities to succeed.

So what I want to tell everyone is that while institutions may hope you have a science or engineering background, what they care more about is whether you have sufficient perception of and interest in new technologies or products. For example, people in our firm with purely liberal arts or business backgrounds also read AI papers or learn some basic coding. More specifically, you could organize the core technical highlights of papers you've recently read, or put together a mapping of domestic and international AIGC companies, or perhaps you're an active participant in certain open-source communities, or maybe you've initiated some interesting technology-focused activities. These would all be major pluses on your resume. So if you're genuinely interested and willing to actively explore, your background doesn't matter. The further you go, five or ten years into your career, what you studied as an undergraduate gets leveled out.

Q: When you specifically look at a project, what factors and dimensions do you value more? How do you judge whether it's worth investing in? What do you do when you and your team disagree?

A: For this question, the broad framework is basically consistent for everyone — things like the founder's learning ability and leadership, the market size of the industry, product and commercialization capabilities, and team iteration ability. But what constitutes "good" differs for each person, so you still need to accumulate sufficient volume to develop good taste. The companies each person invests in will to some extent reflect their individual personality and experiences.

For disagreements, we first need to accept them, because companies that ultimately grow into super deals or unicorns often appear to have huge disagreements and non-consensus in their early stages. Projects without much early disagreement aren't necessarily bad — it's just that they might only become billion-dollar companies rather than ten-billion-dollar or greater companies. Then you need to continuously expand your sample size, so you can have the confidence to stick to your taste and capabilities, and build reputation and trust.

Q: For newcomers, should we cast a wide net or deeply understand one direction? How can we get more out of many quick research projects?

A: First, we need to concretize the definition of "direction." For example, new energy — under new energy you have lithium batteries and photovoltaics. Lithium batteries have upstream, midstream, and downstream, materials, technology, and equipment. So are you focused on lithium battery equipment, lithium batteries, or new energy? So if broadly you're looking at both new energy and enterprise services, that would be somewhat scattered. I personally don't recommend this. If it's a specific dimension within a broad direction, then that's how this industry works. It's hard to say you've focused on an extremely specific niche — you need to pull up one level, because even if you do focus, there will still be many scattered things and small directions, and they're constantly changing.

Second, I still more recommend going deep into one direction to see more sample projects. With insufficient sample size, what you fear most is jumping to conclusions. Sample size is a T-shaped model — while you're going deep vertically in a single track, you also have the horizontal breadth. Investment is like this: you're always balancing and trading off between breadth and depth.

Third, to gain more from your efforts, I suggest obtaining more feedback paths across time and space dimensions. On one hand, actively communicate with your mentor and ask for their views on your project assessments, or collect others' opinions and ask your mentor what they think. On the other hand, you can review CEOs — for example, you can meet a CEO this year and chat with them again next year to see how they've changed.

Q: For someone who wants to establish themselves in the investment industry long-term, develop deep insights, and ultimately become an excellent investor, when we've just graduated, should we first go into industry to experience and learn, or directly start from a more general investment perspective?

A: If I have to stand at this point in time, I'd more recommend going into industry first. There are mainly two reasons:

-

The feedback cycle in investing is longer. Sometimes it even gives wrong feedback in the short term, which is very unfriendly to young people.

-

The investment industry itself is highly competitive. If you haven't made good representative investments in three to five years, it becomes harder to continue down this path. So there's a certain risk component here. And this risk isn't 100% tied to your ability — there's also luck, industry cycles, your institution's deal frequency, and many, many other factors beyond your control. So from this perspective, going into industry first to accumulate more resources may be the better choice at this point in time.

Message Board

I'm very glad to have had this opportunity to participate in the ASK VC event. As a newcomer to the industry who hasn't experienced market cycles, listening more to seniors' experiences, lessons, and advice is a very necessary step in shaping correct investment perspectives. It can also help clarify directions for development and avoid blindly following trends. Looking forward to the next event!

— Ruisi Li

Thank you very much to Teacher Yao Feng for sharing and to the ASK VC team for organizing. As a newcomer to venture capital, I learned a lot of valuable experience and insights that seniors have accumulated over many years in the investment business. What I found most rare was that Teacher Yao Feng, when facing every question from students present, could as much as possible stand in our shoes to understand what guidance we were really trying to get through these questions, and the fundamental confusion hidden behind our questions. While working hard to empathize with the stage we're at and the current venture capital environment, she expanded on as many angles and areas of knowledge as possible to inspire us to think more deeply around a question.

— Jin'ou Wang