Deep Dive: The Latest ChatGPT and Claude User Reports — How AI's Top Players Are Diverging | Yunqi Capital Tech π

The Signal Behind the Numbers

Three years into the GenAI wave, the market's leading players have carved out distinctly different paths.

Recently, OpenAI and Anthropic released core user reports on ChatGPT and Claude, revealing significant divergence in market positioning, core application scenarios, and user interaction patterns. In this edition of "Yunqi Tech π," we analyze the industry signals behind these two reports.

This article is reprinted from "Silicon Rabbit" (excerpted)

Original title: ChatGPT and Claude Are No Longer Playing on the Same Field

01

The data from both reports clearly illustrates the different emphases of ChatGPT and Claude in user base and core functionality — the starting point for understanding their long-term strategic divergence.

ChatGPT:

Market Penetration in General-Purpose Applications

OpenAI's report confirms ChatGPT's status as a phenomenon-level application. As of July 2025, its weekly active users have exceeded 700 million. The user structure shows two key characteristics:

First, the user base has successfully expanded to a broader population. The early profile dominated by technical professionals has shifted to highly educated white-collar workers across diverse occupations.

Second, gender balance has been achieved, with female users rising to 52% of the total.

In terms of application scenarios, ChatGPT's core functions concentrate in three areas: practical guidance, information queries, and document writing — together accounting for nearly 80% of total conversations.

Users primarily employ it to assist with daily life and routine office tasks. Notably, the report explicitly states that programming and other specialized technical assistance has dropped significantly from 12% to 5%.

Taken together, ChatGPT's strategic path is to become a general-purpose AI assistant serving a broad user base. Its core moat lies in massive user scale and the resulting network effects, plus high penetration into users' daily information processing workflows.

Claude:

Focused on Enterprise and Professional Automation Scenarios

Anthropic's report paints a starkly different picture. Claude's user distribution shows strong positive correlation with regional economic development levels (per capita GDP), indicating that its primary users are knowledge workers and professionals in developed economies.

Its core application scenarios are highly concentrated. Report data shows that software engineering is the dominant application across nearly all regions, with related tasks consistently accounting for 36% to 40% — a sharp contrast to ChatGPT's trend in this domain.

The most striking data in the report concerns the share of "automation" tasks. Over the past eight months, "directive" automation tasks — where users issue instructions and AI independently completes most of the work — surged from 27% to 39%.

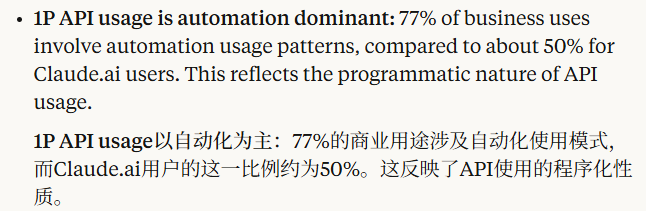

Among paid API enterprise users, this trend is even more pronounced: a remarkable 77% of conversational interactions exhibit automation patterns, with the vast majority being "directive" automation with minimal human intervention.

Thus, Claude's strategic positioning is crystal clear: to become a professional-grade productivity and automation tool deeply integrated into enterprise core workflows. Its competitive advantage lies in deep optimization for specific professional domains (especially software development) and relentless pursuit of task execution efficiency.

02

Based on the strategic divergence outlined above, cross-referencing data from both reports yields three forward-looking industry insights.

I: The "Programming Application" Divergence,

Foreshadowing the Rise of Specialized AI Tool Markets

The inverse trends of ChatGPT and Claude in programming applications do not reflect fluctuating market demand, but rather user demand upgrading toward "specialization" and "integration." General-purpose conversational interfaces can no longer satisfy professional developers' deep needs within complex workflows. What they require is AI functionality that seamlessly integrates with integrated development environments (IDEs), code version control systems, and project management software.

This trend signals an important market opportunity: "AI-native toolchains" purpose-built for specific industries (such as software development, financial analysis, legal services) and deeply bound to existing workflows. This demands that AI not only possess model capabilities, but also deep industry understanding. For relevant investment domains, evaluating whether a target can build this kind of "deep integration" will become a critical consideration.

II: "77% Automation Rate,"

Quantifying the Acceleration of Enterprise Task Automation

The "77% enterprise API automation rate" in Anthropic's report is an extremely strong signal, indicating that at the frontier of commercial applications, AI's role is rapidly shifting from "human assistance" to "task execution."

This data demands that we reevaluate the speed of AI's impact on enterprise productivity, organizational structure, and cost models. The market has broadly focused on AI's "efficiency enhancement" value, but now must incorporate "replacement" value into its core analytical framework.

Investment logic needs to expand from evaluating "how AI assists human employees" to "in which knowledge work domains can AI independently complete standardized tasks with higher efficiency and lower cost." Areas such as financial report generation, contract preliminary review, and market data analysis — process-oriented, high labor-cost domains — will be where AI automation technology first generates significant economic returns.

III: The "Collaboration vs. Automation" Mode Difference,

Revealing the Evolution of AI Business Models

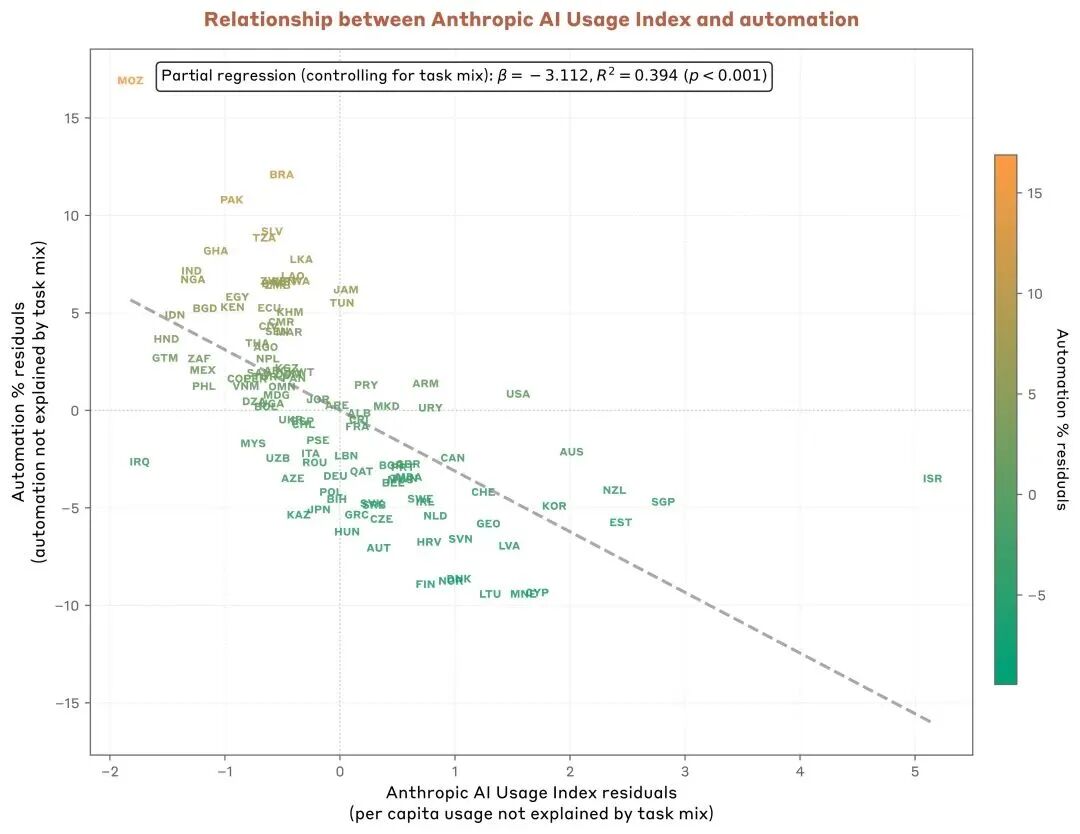

A counterintuitive data point from the reports: in regions with higher per-capita Claude usage, users tend toward "collaboration" mode; conversely, regions with lower usage tend toward "automation" mode.

This may reveal an evolutionary relationship between AI business models and user maturity. In early market penetration stages, users tend to treat AI as a simple efficiency tool for replacement completion of independent tasks (automation).

But when users — especially professional users — develop deeper understanding of AI's capability boundaries and interaction patterns, they begin exploring complex collaborative work with AI to accomplish more creative tasks that were previously unachievable (collaboration). This poses new questions for AI's long-term business models.

Beyond cost reduction through automation replacement (SaaS model), creating entirely new value and improving decision quality through human-AI collaboration may catalyze more advanced business models, such as outcome-based pricing or decision support subscriptions. When evaluating AI projects, investors should simultaneously assess their development potential along both "automation" and "collaborative creation" paths.