Decoding the Global Top 100 AI Apps Ranking: AI Video Heats Up, Vertical Apps Monetize | Yunqi Capital Tech π

DeepSeek made AI an overnight national conversation, but which AI applications have truly gained widespread adoption? And which products have already achieved the "double win" of traffic and revenue?

DeepSeek made AI an overnight mainstream phenomenon, but which AI applications are actually seeing widespread adoption? And which products have achieved the "double win" of traffic and revenue?

The latest "Top 100 Gen AI Consumer Apps" from renowned US venture firm a16z may offer some answers. In this edition of "Yunqi Tech π," we break down the industry trends behind the top 100 AI-native applications.

This article was compiled by the WeChat public account "FishAI"

Original title: "Dispatch | Top 100 AI Apps List ~ a16z"

a16z original article: https://a16z.com/100-gen-ai-apps-4/

In just six months, the consumer-facing generative AI market has transformed dramatically. Some products have risen rapidly, others have stalled, and unexpected dark horses have leaped to become industry leaders. DeepSeek, for instance, surged from obscurity to become a formidable rival to ChatGPT; AI video models evolved from experimental tools to viable short-film production options; and the rise of "vibecoding" redefined who can create AI content rather than merely consume it. Competition is intensifying, the market keeps expanding, and winners are no longer determined by simply "shipping a product" — they must earn users' long-term loyalty.

Through data analysis, we attempt to answer several key questions: Which AI apps are people actually using? Which products have not only attracted traffic but converted it into real revenue? Which tools are transitioning from curiosity-driven "try-outs" to daily essentials?

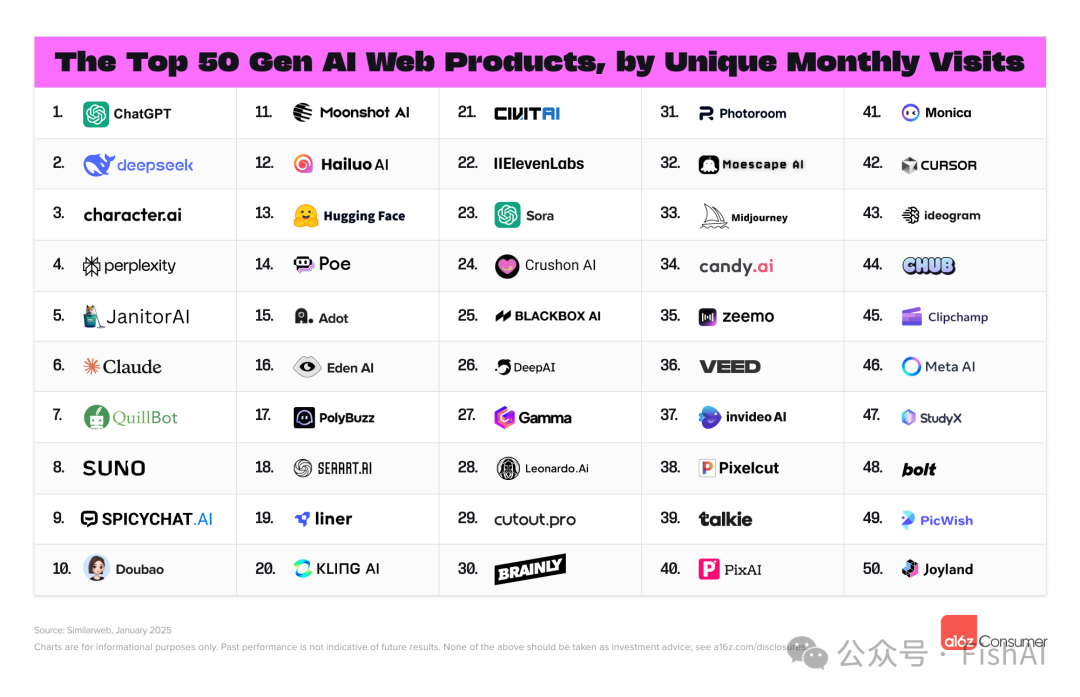

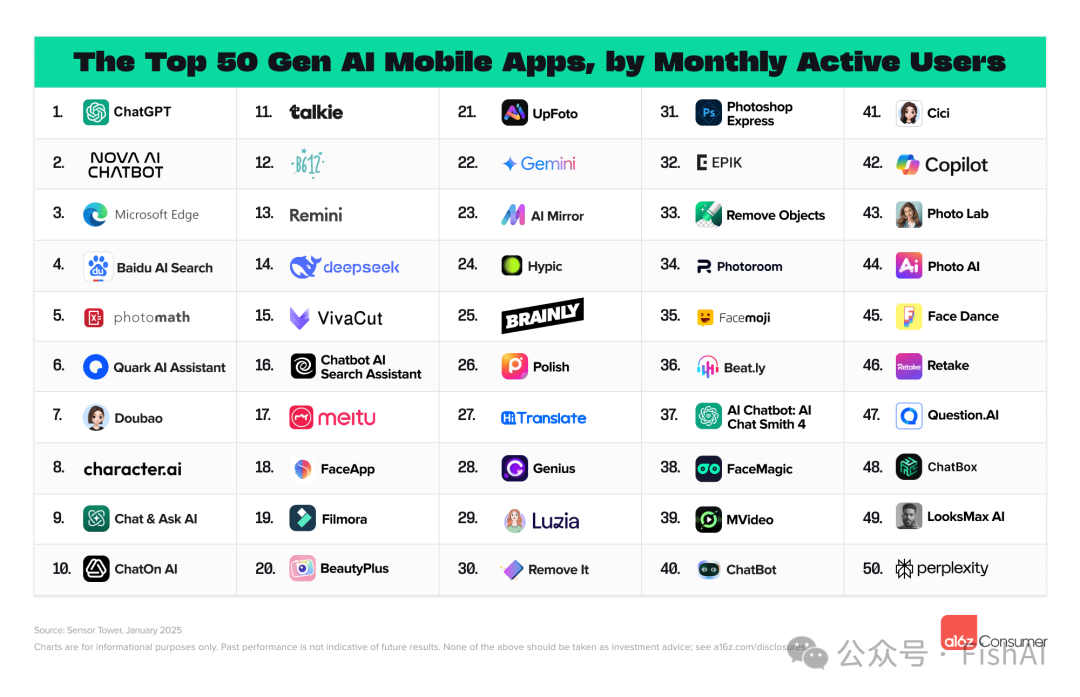

This is our fourth release of the "Top 100 Gen AI Consumer Apps" list (updated every six months), covering the top 50 AI-native web products (data source: Similarweb, ranked by monthly unique visitors) and top 50 AI-native mobile apps (data source: Sensor Tower, ranked by monthly active users). Since our August 2024 report, 17 new companies have entered the web product rankings for the first time.

Web Rankings

Mobile App Rankings

Methodology note: This list includes only AI-native products. Products like Canva and Notion, which have added significant AI features but are not AI-native, are excluded. Compared with previous lists, we have removed traditional photo editing tools such as Pixlr, Fotor, and PicsArt.

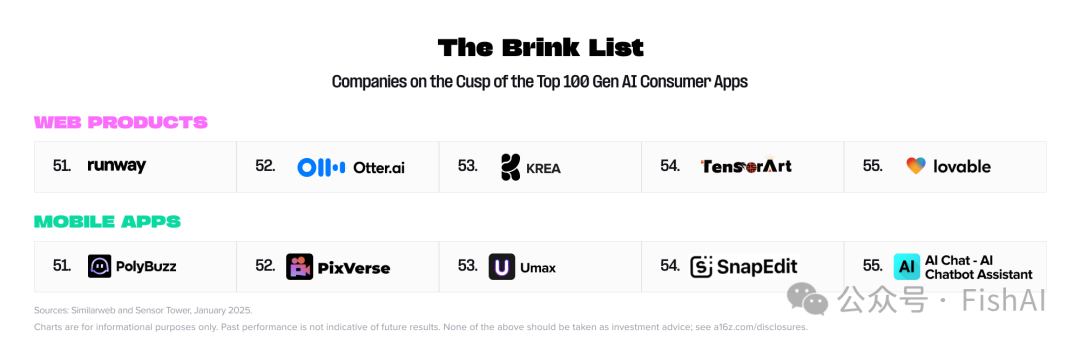

Additionally, we have introduced the "Brink List" this time, featuring 10 products most likely to break into the top 100 (5 web products, 5 mobile apps). Given the rapidly shifting AI landscape, we look forward to seeing whether these rising contenders can make the cut in our next list.

Brink ListBeyond ranking data, we also analyzed new developments in industry trends and consumer behavior, distilling several insights worth watching.

Brink ListBeyond ranking data, we also analyzed new developments in industry trends and consumer behavior, distilling several insights worth watching.

01

ChatGPT's Strong Recovery:

From Slowing Growth to New Highs

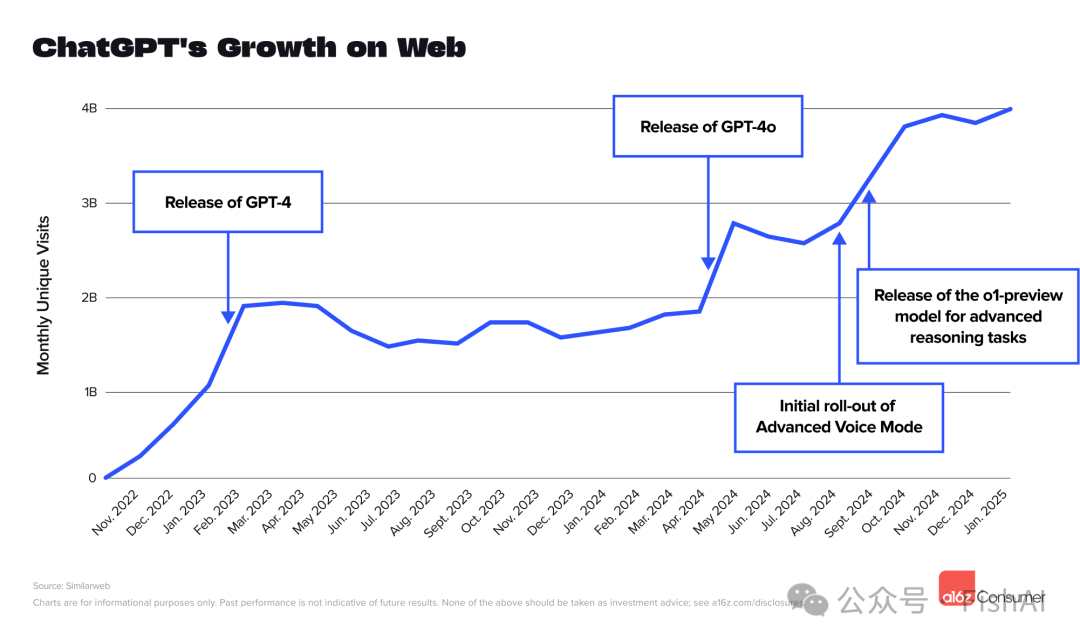

Since launching as a "research preview" in November 2022, ChatGPT reached 100 million users in just two months, becoming the fastest-growing consumer application. However, its traffic growth subsequently slowed, with global monthly visits remaining essentially flat from March 2023 to April 2024. Recently, ChatGPT's user growth has rebounded strongly. It took 9 months to grow from 100 million weekly active users in November 2023 to 200 million in August 2024; yet the jump from 200 million to 400 million by mid-February 2025 took less than 6 months — a remarkable acceleration.

ChatGPT Web GrowthThe early slowdown likely stemmed from novelty attracting massive user numbers without clear daily-use scenarios. As OpenAI continuously rolled out more powerful models and features, user engagement improved significantly — existing users returned more frequently, while new users kept joining. Specifically, each traffic surge coincided closely with product upgrades.

- April–May 2024: GPT-4o launched, bringing multimodal capabilities including real-time voice interaction and image recognition — snap a math problem for instant solutions, or brainstorm ideas with AI.

- July–August 2024: Advanced Voice Mode went live, substantially improving conversation fluidity.

- September–October 2024: The o1 series debuted, enhancing reasoning and problem-solving capabilities.

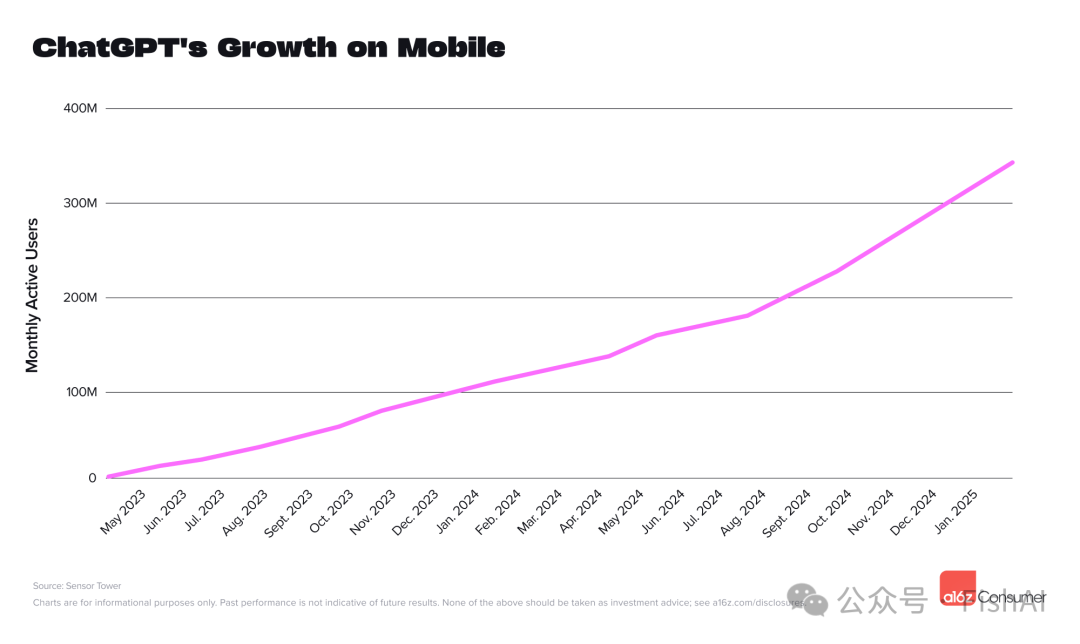

ChatGPT Mobile GrowthMobile performance has been more stable. Since launching its mobile version in May 2023, ChatGPT's user base has grown steadily at 5%–15% per month. Sensor Tower estimates that of its 400 million weekly active users, approximately 175 million come from mobile.

02

DeepSeek's Sudden Rise:

China Market Explodes, Global Influence Emerges

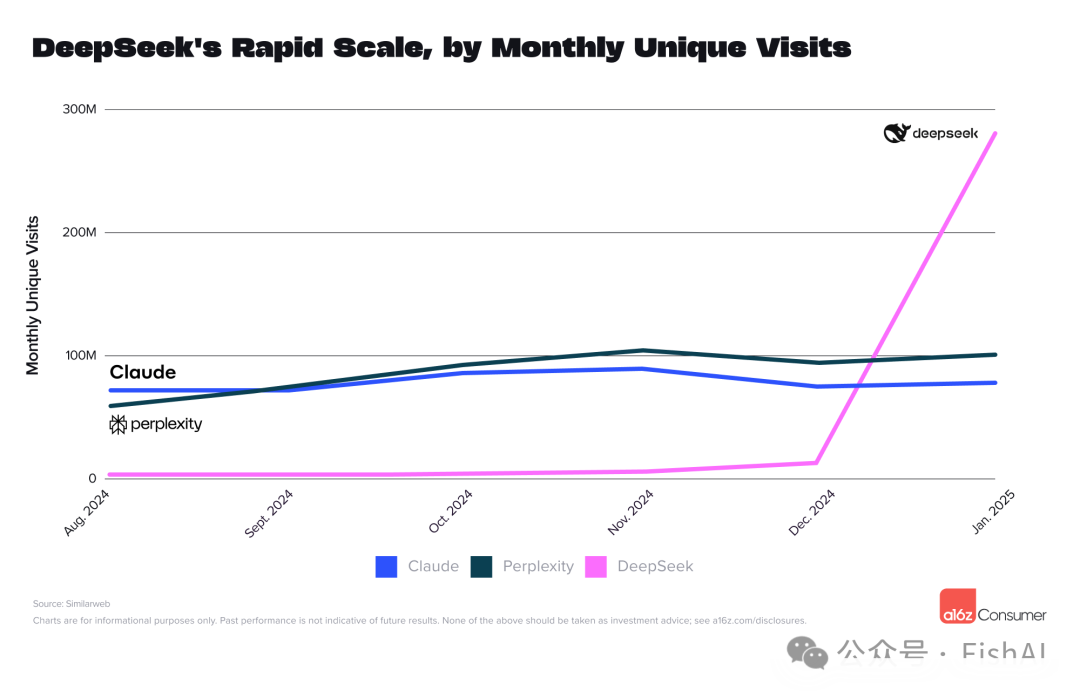

DeepSeek has been making headlines lately. Its chatbot launched on January 20, 2025, and within just 10 days it jumped to second place globally among AI products by monthly visits.

Developed by Chinese quantitative hedge fund High-Flyer, 21% of DeepSeek's January 2025 traffic came from China (where ChatGPT is blocked), with the US and India accounting for 9% and 8% respectively. However, restrictions or bans have been imposed in South Korea, Australia, Taiwan, and on some US state government devices.

Compared to other general-purpose large language models, DeepSeek's growth has been explosive. Official data shows it reached 1 million users in 14 days — not matching ChatGPT's 5-day record, but then surpassing ChatGPT's 40-day milestone by hitting 10 million users in just 20 days.

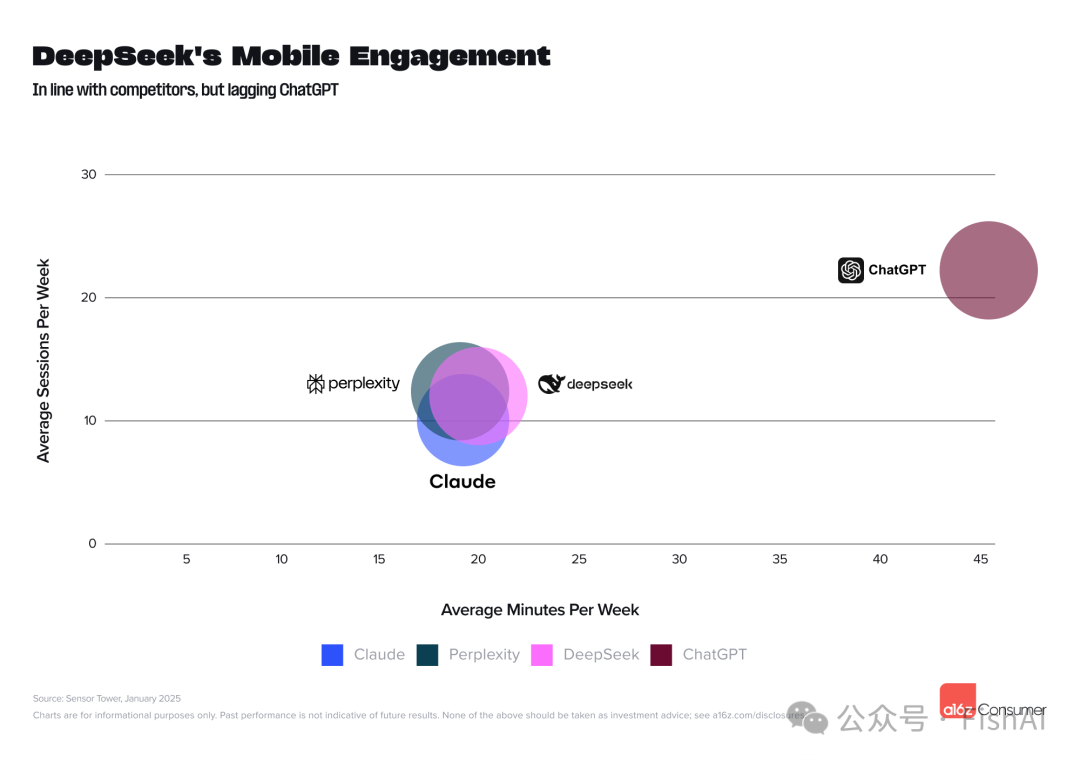

DeepSeek Monthly Visit GrowthOn mobile, DeepSeek launched on January 25, 2025, ranked 14th in monthly active users within 5 days, and jumped to second place by February — reaching 15% of ChatGPT's mobile user base. Sensor Tower data shows its weekly user session duration and frequency slightly exceed Perplexity and Claude's, though still trailing ChatGPT.

DeepSeek Monthly Visit GrowthOn mobile, DeepSeek launched on January 25, 2025, ranked 14th in monthly active users within 5 days, and jumped to second place by February — reaching 15% of ChatGPT's mobile user base. Sensor Tower data shows its weekly user session duration and frequency slightly exceed Perplexity and Claude's, though still trailing ChatGPT.

DeepSeek Mobile EngagementDeepSeek's rapid rise in tech circles owes much to its strong performance on reasoning benchmarks and its widely publicized training cost of just $5.6 million — far below competitors. This low-cost training was seen as a "Sputnik moment," sparking widespread discussion. On January 27, 2025, Google Trends showed its global search interest matching ChatGPT's, briefly surpassing it in the US.

DeepSeek Mobile EngagementDeepSeek's rapid rise in tech circles owes much to its strong performance on reasoning benchmarks and its widely publicized training cost of just $5.6 million — far below competitors. This low-cost training was seen as a "Sputnik moment," sparking widespread discussion. On January 27, 2025, Google Trends showed its global search interest matching ChatGPT's, briefly surpassing it in the US.

03

AI Video Heats Up: From Experiment to Practical Tool,

Especially Active in Short-Form Video

Over the past 18 months, AI video technology has oscillated between "nearly practical" and "still unreliable." But in the last six months, quality and controllability have improved markedly. Three new companies entered the web top 50 in this list:

- Hailuo (12th)

- Kling AI (17th)

- Sora (23rd)

Additionally, established product InVideo ranks 37th, while Runway and Krea (which aggregates multiple video generation models) made the Brink List.

Both Hailuo (based on MiniMax's model) and Kling AI are from China, launching in September and June 2024 respectively, and by January 2025 their visits exceeded Sora's. Sora began limited preview in February 2024 but didn't officially launch until December. Service providers are gradually differentiating in features and style:

- Sora: Relatively generic output style.

- Hailuo: More precise understanding and execution of prompts.

- Kling AI: Offers features like camera movement control and lip-sync alignment.

AI Video Related LinksAI video editing remains a core consumer use case, enabling one-click smart editing, auto-captioning, and other tedious tasks. For example, Veed (36th) and Clipchamp (45th) made the web list. On mobile, apps blending photo and video processing stood out, such as B612 (12th), VivaCut (15th), and Filmora (19th). For revenue, Splice, Captions, and Videoleap performed particularly well on mobile.

Going forward, new models like Google's Veo 2 may bring further innovation. But at $0.50 per second, its pricing skews toward commercial use and may struggle to meet large-scale consumer demand.

04

"Vibecoding" Takes Off:

Empowering Developers and Everyday Users Alike,

AI Reshapes Who Creates Products

Currently, two sub-sectors are booming, targeting different audiences:

1. Agentic IDE: Intelligent integrated development environments for developers, such as Cursor, supporting bug detection, code completion, and generation — essentially an "AI assistant for developers." 2. Text-to-Web App platforms: Generate websites or apps through text prompts, suited for non-technical users — what Andrej Karpathy dubbed the epitome of "vibecoding." In this list, Cursor entered the web rankings for the first time (41st), with the company claiming hundreds of thousands of developer users. Text-to-Web App lets ordinary people generate websites or apps through text prompts alone, no coding required — like magic. This product category has recently exploded, enabled by large models' ability to generate executable code, mature web frameworks, and easy integration with ecosystem components like Resend, Clerk, and Supabase.

Growth figures are striking: Bolt (48th) reached $20 million annualized revenue and 2 million registered users within two months of launch; Lovable hit $17 million annualized revenue in three months and made the Brink List.

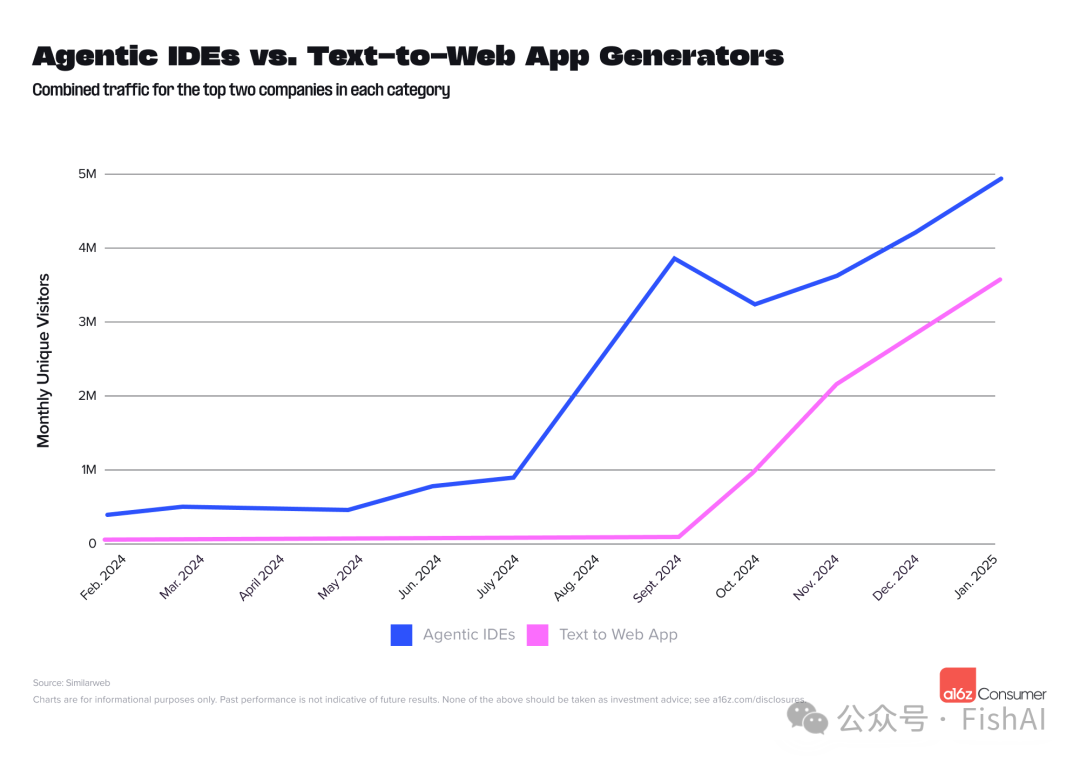

Agentic IDE vs. Text-to-Web AppBy monthly unique visitors, the top two Agentic IDEs have slightly larger user bases than Text-to-Web App platforms, but growth rates are comparable. Agentic IDEs target developers — a smaller group but with high usage frequency; Text-to-Web App has broader applicability but requires users to have specific needs driving adoption.

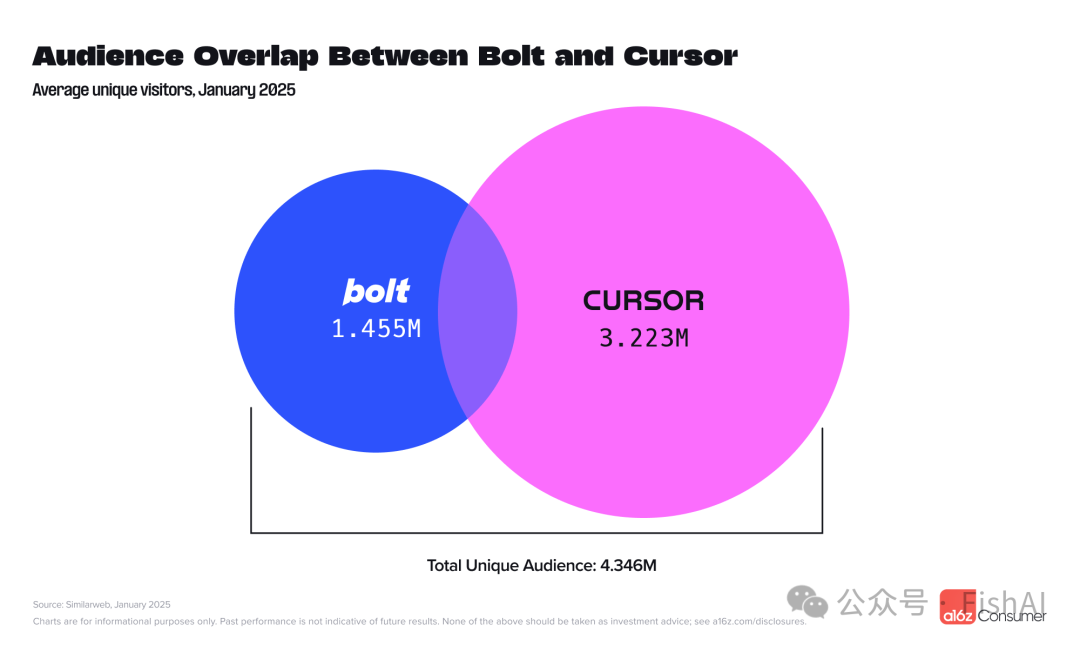

The two user groups overlap somewhat. Technical users might start with Text-to-Web App for rapid prototyping, then refine with an IDE. Similarweb data shows that in January 2025, 23% of Bolt users also visited Cursor.

Bolt and Cursor User Overlap

05

Specialized Apps Monetize Deeply:

Scale Doesn't Equal Revenue

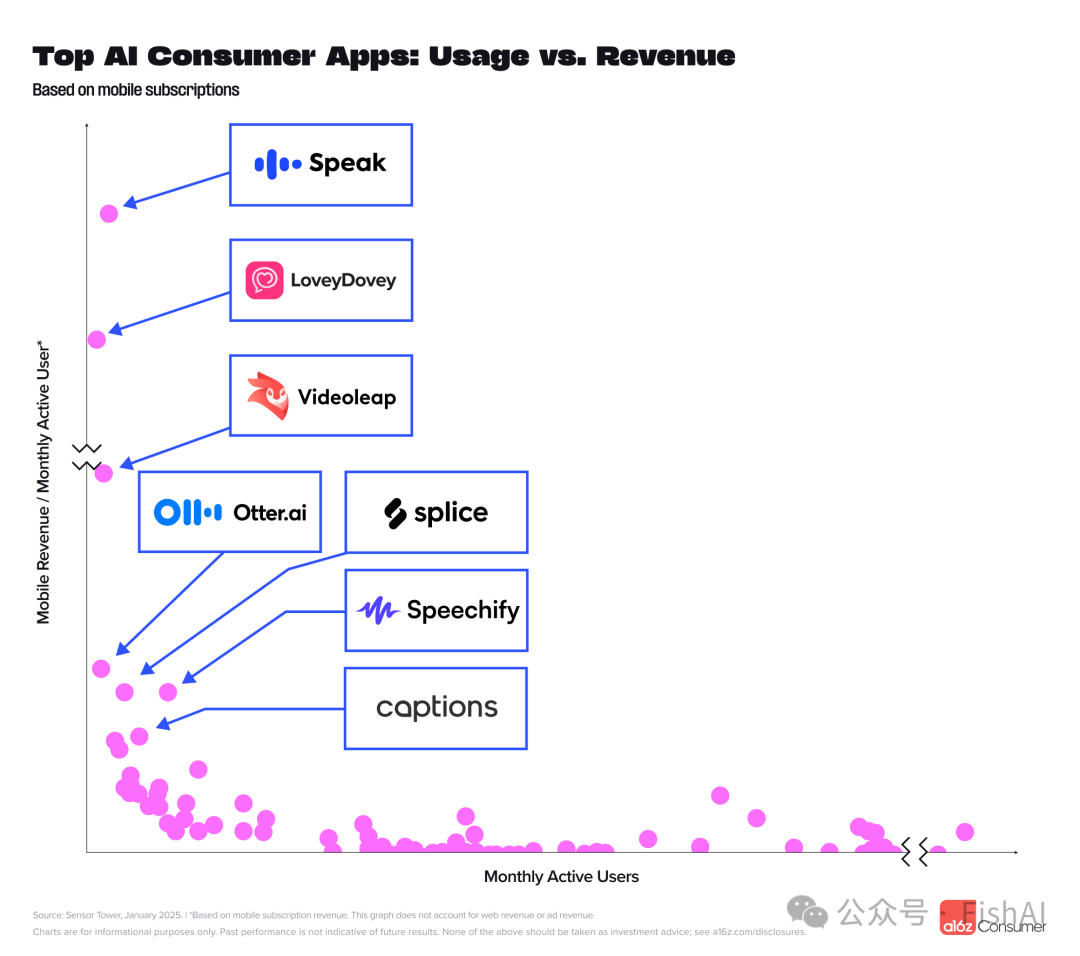

The mobile rankings are based on Sensor Tower's monthly active user (MAU) figures, with an entry threshold of 8 million MAU. But high MAU doesn't mean strong revenue. Some apps with lower MAU outperform many "traffic giants" in revenue thanks to high paid conversion rates and revenue per user. ChatGPT leads in both MAU and revenue, yet the overlap between the top 50 apps by activity and top 50 by revenue is only 40%.

Usage vs. RevenueCertain categories appear on both lists but with notably different rankings. AI video/photo editing accounts for over 20% of both lists — the user ranking top three are VivaCut, Filmora, and Beat.ly, while the revenue top three are Splice, Captions, and Videoleap. Mass-market apps attract more users; specialized apps more easily drive payment willingness.

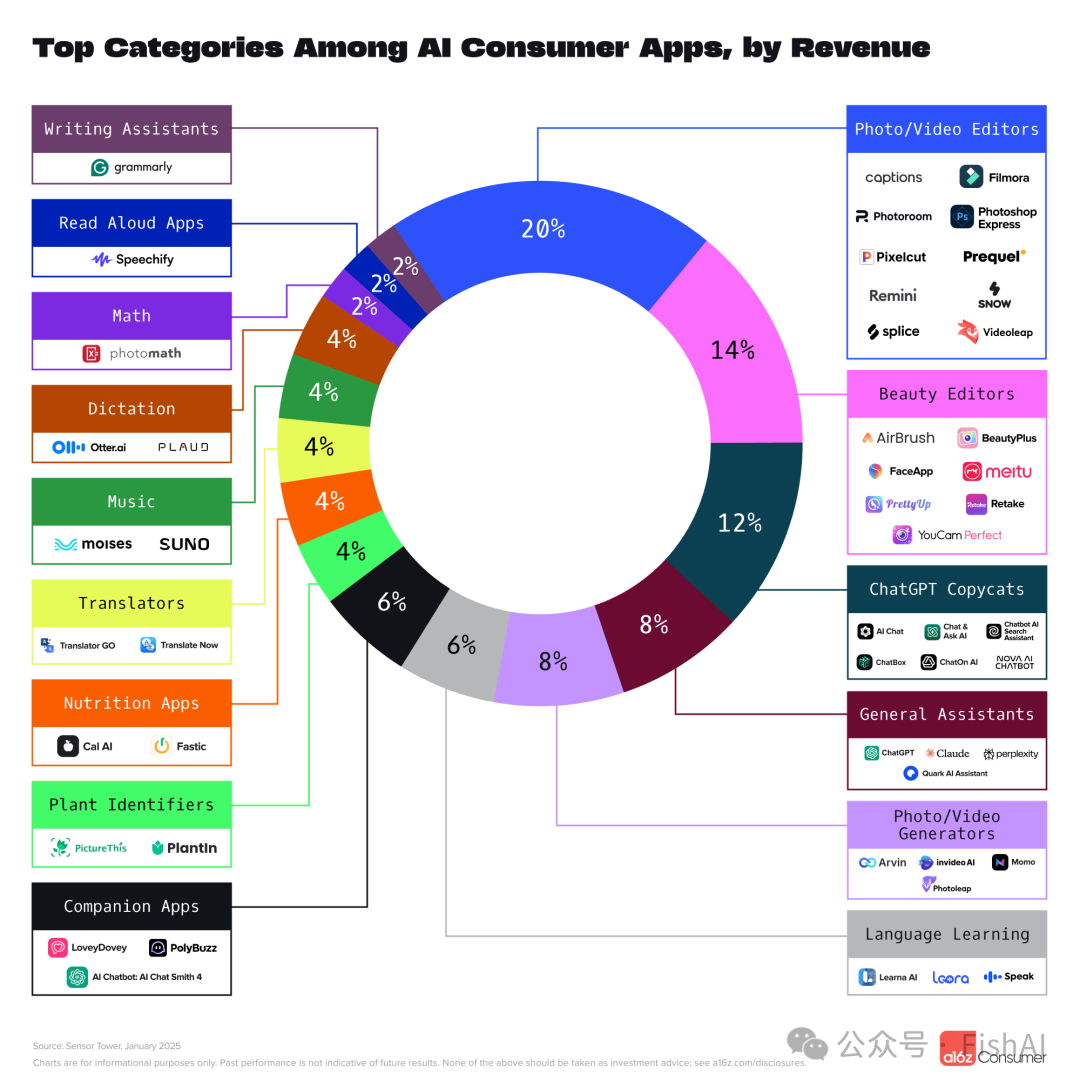

Some categories appear only on the revenue list:

- Plant identification: e.g., PictureThis, PlantID

- Nutrition/diet: e.g., Cal AI, Fastic

- Language learning: e.g., Speak, Learna, Loora

- Music: e.g., Moises, Suno

- Voice transcription: e.g., Otter, PLAUD

These niche scenarios have clear demand and strong user payment willingness, with standout subscription revenue.

Revenue List Main CategoriesNotably, ChatGPT "clone" apps account for 12% of both lists, attracting users through mimicked names and icons, low prices, and constantly adjusted app store information to evade copyright issues, maintaining steady downloads.

Conclusion

AI-native products are growing at unprecedented speed, with user stickiness continually strengthening. But this field still holds massive untapped potential. In coming years, AI will spawn a cohort of industry-defining leaders. Right now, competition has entered white-hot territory — technological breakthroughs emerge constantly, user acceptance keeps rising, and the willingness to pay is becoming increasingly evident.