A Conversation with Qin Liu: An Investor Needs the Coolest Head and the Wildest Heart | 5Y Talk

Entrepreneurs of this era are a band of mad explorers.

There are people who are simply born to build.

They're like mad explorers, blazing trails on slopes where no path exists. They may not be understood in their time — and it's precisely this lack of understanding that pushes the boundaries of what's possible, breaking through existing paradigms and the limits of human imagination.

They are rare and precious. What 5Y Capital does is identify them, believe in their madness and imagination, and support them in turning vision into reality. The you that others see as crazy — we start by believing in you.

The following is an interview with Qin Liu, founding partner of 5Y Capital, conducted by Run Liu, founder of Runmi Consulting. We hope you find it illuminating :)

Author / Run Liu

Editor / Jiao Pi

I'm a business consultant. When do companies come to me? When they're sick — sometimes dying.

So most of the companies I encounter are deep in crisis.

Seeing so many life-or-death situations, constantly going in and out of the ICU — emotionally, it can make you rather pessimistic.

That's why I need to meet with investors regularly.

When do companies seek out investors? At birth, or while they're growing.

So the companies investors see are like newborns delivered from the maternity ward — mostly vibrant, full of life, infinitely promising.

And the new lives that catch an investor's eye are more likely to break through the soil, sprout, bloom, and bear fruit. Investors use their deep thinking and real money to validate their judgment and vision.

A few days ago, I went to 5Y Capital (formerly Morningside Capital) and spoke with founding partner Qin Liu.

5Y Capital has invested in companies like Trip.com Group, JOYY, Xiaomi, Kingsoft Office, Agora, Xpeng Motors, Kuaishou, WeDoctor, SenseTime, Horizon Robotics, and Pony.ai.

Qin Liu has not only his own distinctive thinking, but also a rare quality — a fervent sense of hope.

Below, I'd like to share some of Liu's most valuable perspectives with you. You'll see the investor's coolest head and most fearless heart.

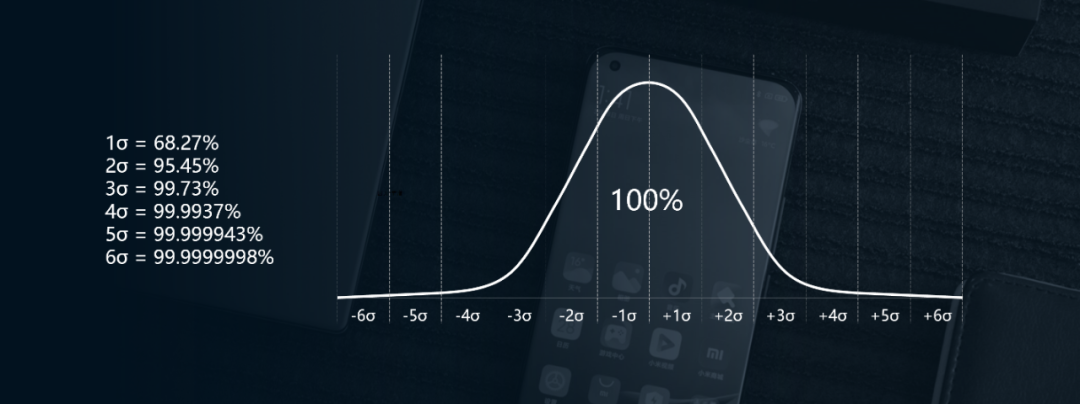

1. "We don't invest in people within 3-sigma."

Business is a game that's both serious and playful.

The players in this game are all kinds of people. Entrepreneurs are all kinds of people.

We believe the most important thing in investing is: back the founder, back the founder, back the founder.

And for early-stage investors like us, it's even more about backing the founder.

But before knowing who to back, it's more important to first know who we definitely won't back.

Liu says: We don't invest in people within 3-sigma.

What does that mean?

Sigma is a statistical concept, called "standard deviation" in Chinese, used to measure how much a set of data deviates from the "standard." We typically measure this standard deviation using "defects per million opportunities."

That's too abstract. Let me give an example. At 1-sigma, you have 690,000 defects per million samples — equivalent to 170 typos per page of a book.

At 3-sigma, you have 67,000 defects per million samples — equivalent to 1.5 typos per page.

People in this world generally follow a bell curve, a normal distribution. Most people fall within 3-sigma.

That means 99.73% of people probably won't get our investment — they don't offer anything new. 99.73% also means that out of 1,000 people, we might only consider 2 or 3.

So you can probably see that what investors look for isn't "normal" people, but people who are different.

Only such people have a chance to become outstanding entrepreneurs.

2. "What's your non-consensus view?"

But how do you judge whether someone is "different"?

Hmm. Good question.

We often ask entrepreneurs: What's your non-consensus view?

What do you believe that people find a bit strange? Even bold, crazy, absurd.

Because only behind madness can there be massive innovation.

If your idea is consensus, someone has definitely already done it. What you can think of, others have already thought of — probably better than you.

But non-consensus, fringe ideas — these are what can challenge the existing order.

5Y Capital's meeting rooms in Beijing are all named after explorers.

Because they weren't understood. And it's precisely this lack of understanding that expanded the boundaries of humanity, pushing past the limits of human imagination.

We hope the entrepreneurs of this era are a group of mad explorers.

This madness is essentially a non-consensus view. And only non-consensus brings asymmetric returns.

We have a saying: The you that others see as crazy — we start by believing in you.

You have a non-consensus view; we're willing to identify it and invest in it.

The you that others see as crazy, we start by believing in you. Beautifully put. This madness is what Liu means by people beyond 3-sigma.

But for these people beyond 3-sigma, to the left are frauds and delusional patients; to the right are the real entrepreneurs and explorers.

How do investors tell them apart?

3. "Logic and human nature."

Back to first principles.

In investing, there are two foundational things: logic and human nature.

Does your startup make basic business sense? Does your idea insightfully address human needs?

For early-stage investing like ours, due to massive information asymmetry, we can't rely entirely on quantitative analysis. We rely more on qualitative analysis to make investment decisions.

So many people are curious about us, and perhaps misunderstand us:

Some think investment decisions are pure mysticism and art. Others think there's a formula — plug in the variables and out comes a decision.

Neither is true.

We don't read the stars at night, snap our fingers, and know whether the entrepreneur sitting across from us is good. Nor do we have a mature SOP where doing X guarantees Y.

5Y Capital's investment approach is somewhat similar to an entrepreneur's decision-making process.

Outstanding entrepreneurs and business leaders are necessarily visionaries — prophets.

Their strategic vision, their sensitivity to industry trends — these are the foundations for building a vision. This thinking requires logic.

Then, you need deep understanding of human nature, judgment of people.

Remember? Business is a game that's both serious and playful. The players are all people. Without thinking about people, it's hard to succeed in entrepreneurship.

4. "Why did we invest in Kuaishou?"

Logic and human nature. Can you be more specific?

Well... let me give an example.

Why did we invest in Kuaishou?

In 2011, after we invested in Xiaomi, we internally asked ourselves: What is a phone, really?

We came to this conclusion: A phone is a PC, but a PC is not a phone.

What does that mean?

A phone has a CPU, memory, all kinds of computing environments — so it has PC characteristics.

But a phone also has three very important things that PCs don't have.

- Phones have location parameters. Because you carry your phone with you everywhere; it goes where you go.

- Phones have address books. What's an address book? Social relationships.

- Phones have cameras, have speakers. So a phone is also a natural multimedia generator.

Put these three together — what do you see?

Non-consensus.

At that time, around 2011, our investing still followed Americans. Whatever America invested in, China invested in.

But we saw and proposed a non-consensus view: that the next opportunity would be mobile. The mobile internet was coming.

So we invested in a series of companies. Including Kuaishou.

That's the logical foundation.

What about human nature?

5. "How did Kuaishou address human nature?"

Human nature doesn't change.

Human nature is always love and hate, passion and conflict.

But the way human nature is addressed — that changes. It always changes.

Before, people would go to cinemas, sit quietly for two hours, watch a story, experience the complexity of human nature.

But in the mobile internet era, people became less patient; time was sliced into smaller fragments.

Two hours became a luxury.

So what to do?

Watch one-minute short videos.

Those loves and hates, that complexity and brilliance — all condensed into one minute. Human emotions still repeat, only the form has changed.

Beyond this, Kuaishou addressed another aspect of human nature, perhaps an even more important one.

Kuaishou returned the power of content creation and the desire for personal expression to ordinary people.

Previously, people thought content was high-end — celebrities, expensive equipment, polished cinematography, PGC (Professional Generated Content).

This process developed its own closed loop, formed its own industry, leading us to believe this was what content should be.

But because of Kuaishou, because of short video, more ordinary people had the chance to open up and express themselves.

The right to create content was no longer held by institutions; it could belong to individuals.

UGC (User Generated Content) became mainstream.

Technology and entrepreneurs made this happen.

Making content production simple, making content distribution simple.

This is human nature — and it's more fundamental, more expansive human nature.

6. "Find your asymmetric advantage."

Got it.

Logic and human nature are the foundation of investment judgment. But beyond these two points? Why do some people who satisfy both logic and human nature still fail?

Because you also need to look at the specific team, at your core competitiveness.

What exactly is this core competitiveness?

It's your "asymmetric advantage." What is it that only you can do?

Why did we invest in Xpeng Motors in the new energy vehicle race? Because they had their asymmetric advantage.

This category, more specifically, should be "intelligent electric vehicles."

So here's the question: In intelligent electric vehicles, do you value "intelligent," "electric," or "vehicle" more?

Clearly, probably not "vehicle." Otherwise you should invest in BBA (Mercedes-Benz, BMW, Audi).

Is it "electric" then? Also no. If it were "electric," you should invest in battery companies, energy companies.

In our view, the core should be "intelligent."

The hard part of intelligent electric vehicles is the "intelligent" part. This isn't just an auto industry; it's a technology industry.

So when I decided to invest in Xpeng Motors in 2017, I knew this was actually an autonomous driving track, an AI track.

Therefore, in this race, understanding cars isn't enough, understanding batteries isn't enough — most importantly, you need to understand intelligence.

And He Xiaopeng is an engineer-turned-product manager.

He understands technology, and he can build products.

Xpeng's first prototype, though rough, already had the G3's ability to avoid obstacles ahead and stop automatically — it already had autonomous driving features.

That was their asymmetric advantage.

7. "You can fail three times."

Great. Business needs logic and human nature; teams need asymmetric advantages.

But you'll still fail. What then when you fail?

Failure is completely normal.

We're not Midas — we don't touch a project and make it succeed. On the contrary, we fail often.

Investing is looking from the macro to improve the probability of micro success.

But entrepreneurship is quantum, random, uncertain. Failure is inevitable.

What matters is how you view failure.

The entrepreneurial process is essentially trial and error.

We have high immunity to founders making mistakes, even failing. We'll even patiently wait for founders to experience errors and failures.

Because we firmly believe that mistakes are wealth, and a powerful force for rapid growth.

As long as a founder has reflective ability, strong learning ability, and wants to be great rather than just good — that's enough.

We're willing to accompany founders through failure and growth. Try again.

But how many "try again" chances does a founder get?

Three.

Think about it — three times is about right. One entrepreneurial cycle, if it fails, is roughly three years. Three times, ten years pass. A person's prime entrepreneurial window is probably only about ten years.

So you can lose.

But you can probably only lose three times.

8. "What is the real value of VC?"

So as investors, our value is accompanying founders in growth, helping founders grow.

Today, the wealth from entrepreneurial success is unprecedentedly high. But the probability of entrepreneurial success is also unprecedentedly low.

We hope to help founders control risk, using every tool at our disposal to extend founders' trial-and-error time and space.

Liu told me: You do strategic consulting. I think we do strategic consulting too.

We give advice, and we give money — betting our money on our decisions and vision.

This might help founders escape some of the fear and anxiety of immediate survival, using capital to push visionary people toward realizing massive dreams.

VCs — entrepreneurs behind entrepreneurs, gamblers behind gamblers.

Final Thoughts

Walking out of 5Y Capital, I remembered something Liu told me during a 2014 conversation — the story of his 2010 decision to invest in Xiaomi.

One night, Lei Jun called Liu to explain Xiaomi's business model. The call stretched from evening into the next day — a full night, over ten hours, burning through three batteries.

After that conversation, Liu decided to invest in Lei Jun.

But even now, was that investment decision necessarily correct?

Xiaomi's internet hardware, priced at cost — on this basis, the business model was something almost no one understood. But we invested in three consecutive rounds.

Especially that $1 billion round — the company wasn't even profitable yet. Do you invest? Do you dare?

We decided to lead.

Was that moment more rational or more emotional?

Like bungee jumping — you can think all you want, prepare all you want, carefully check the ropes strapped to your body. But when it's actually time to jump, you still need tremendous courage. Eyes closed — jump.

Madness.

Hearing this, a sentence suddenly appeared in my mind:

Investors are the coolest heads and the most fearless hearts.

It's these cool yet fearless investors who accompany equally cool and fearless founders in their growth.

And it's because of this that China's business environment has more vibrant lives that can break through soil, sprout, bloom, and bear fruit.

What do you see?

I see a vigorous vitality, and an upward fervor and hope.

Thank you, 5Y Capital. Thank you, Qin Liu.

5Y Capital (formerly Morningside Capital) currently manages approximately $5 billion across USD and RMB dual-currency funds. We believe that if the you that others see as crazy starts to be believed, the world becomes a better place.

BEIJING · SHANGHAI · SHENZHEN · HONG KONG