5Y Capital's Xu Tian Jing: Why We're Bullish on Digital Pharmaceutical R&D | 5Y Talk

The ITBT track has a promising future ahead.

When we imagine the future, life sciences is a field that 5Y Capital has consistently believed in. Digital healthcare is undergoing unprecedented breakthroughs, and we have been continuously searching for and supporting entrepreneurs in this space.

As one of the earliest institutional investors to bet on the "ITBT" track, on April 18, 2021, 5Y Capital co-hosted the "Digital Pharmaceutical R&D (ITBT)" forum with VB Healthcare (IT = Information Technology, BT = Bio-technology). During the event, Jing Xutian, Managing Director at 5Y Capital, delivered a speech titled "5Y Capital's ITBT Investment Practice: Why We Are Firmly Bullish on Digital Pharmaceutical R&D."

Jing noted that an inverse Moore's Law has emerged in traditional drug discovery — the pharmaceutical industry is undergoing a transformation from "talent- and labor-intensive" to "technology-driven and automated." Information technologies such as bioinformatics, physics-based computing, artificial intelligence, and machine learning are not only rapidly changing how drug molecules are discovered, but also giving rise to entirely new therapeutic areas. Finally, benefiting from the IT revolution and China's healthcare system reform, the development, distribution, and medical service stages that follow drug discovery also present enormous opportunities for transformation in China.

Jing Xutian, Managing Director at 5Y Capital

Below is a transcript of Jing Xutian's speech:

Hello everyone, I'm Jing Xutian from 5Y Capital. The theme of this conference is "The Computation of Life," which fits very well with this ITBT sub-forum. We all know that life is essentially encoded by information — genes are information — so to decode life, we will certainly need computation. Today, I mainly want to share 5Y Capital's thinking and practical experience in the field of digital pharmaceutical R&D.

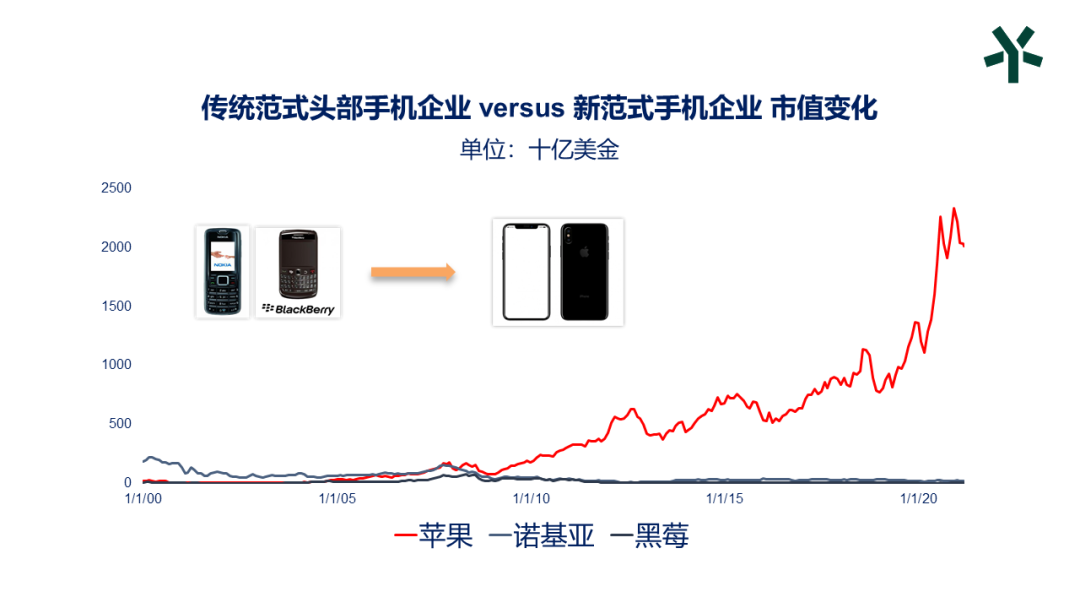

This chart shows the market cap changes of leading mobile phone companies in recent years. You can see that before Apple emerged, traditional mobile giants like Nokia and BlackBerry maintained relatively stable market caps. Apple also went through a long and difficult R&D phase, with its market cap hugging the floor for a while. But as its user base grew, Apple's market cap suddenly and dramatically surpassed the other two starting around 2009.

A similar pattern can be seen in the automotive industry. Previously, the two largest traditional automakers, Toyota and Volkswagen, also maintained stable market caps. But after Tesla's initial R&D phase, its stock price exploded in recent years, surpassing all traditional carmakers.

Why does this trend keep appearing across industries? An important reason is that when a new technology emerges, it can change the business logic of an entire sector. Technology may develop linearly, but the application of new technologies creates unequal supply capabilities, which in turn produces nonlinear commercial growth in business outcomes — bringing disruptive paradigm shifts to industries.

These changes tend to make the head effect of new-generation tech companies more pronounced. It's not just the mobile phone and automotive industries — whether B2B or B2C, leading companies across sectors including Microsoft, Amazon, Facebook, and Tencent have all seen their stock prices keep rising.

However, one phenomenon stands out: the stock prices of leading pharmaceutical companies have remained stable. If you factor in inflation over the past two decades, buying these stocks would actually underperform the broader market.

Why have leading companies in other industries established such strong head effects, continuously capturing market share, while current leaders in pharma haven't demonstrated this effect?

I've been thinking about why. Let me share our hypothesis.

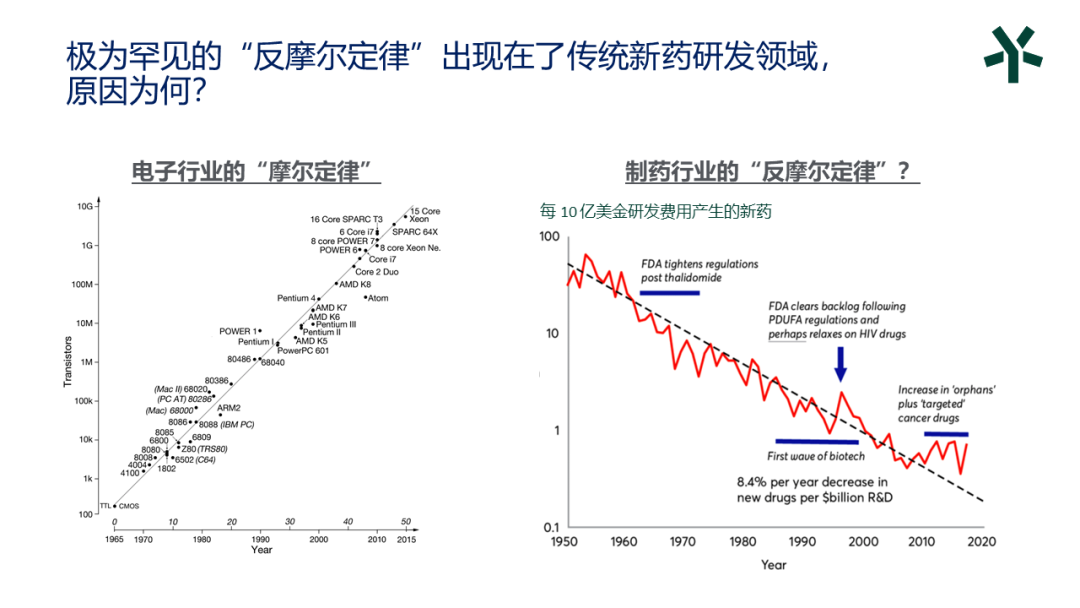

In the chart below, on the left is the familiar Moore's Law from the electronics industry — the number of transistors on a chip roughly doubles every 18 months, driving ever-faster technological development in electronics. In the pharmaceutical industry, we see an inverse Moore's Law emerging — the resources required to develop each new drug keep increasing, while the market sales of each drug are decreasing.

This is a strange phenomenon. Imagine this scenario: you have a fairly fixed business model, but as you produce more products, costs don't decrease — they increase. What other industry behaves this way? Currently, aside from very traditional extractive industries like mining and oil, I can hardly think of any. Because mineral resources are finite, discovering new deposits requires progressively higher investment.

Returning to the fundamental question: why does this phenomenon exist in pharma too?

All enterprises exist to solve problems. If we categorize all problems in the world, they basically fall into two types: human-defined problems and nature-defined problems.

What are human-defined problems? For example, a social app founder might dream from day one of building a platform with 1 billion daily active users — that's a human-defined problem, and there are various ways to reach that goal.

But there are other problems in the world that humans don't get to define. For instance, what drug molecule can best bind to a particular target — that's a nature-defined problem. According to Schrödinger's equation, there theoretically exists a perfect molecule that binds to a protein in the optimal way, releasing the most energy and achieving the most stable state.

When facing problems that nature has already fully defined, what we do is solve them. There are different methods of solving, and theoretically there must exist an optimal approach that lets us solve most efficiently — rather than getting fixated on one particular path.

In the past, humans made a somewhat "foolish" decision by creating disciplinary silos. Biology students spent their days doing experiments; computer science students focused on software development. People doing computation never imagined they could work on drugs; people in biology naturally assumed the burden of drug discovery fell solely on them. But as I mentioned earlier, this is a nature-defined problem — our starting point is here, our goal is there, and theoretically there's a most direct path between them. This path must harness the combined power of all human disciplines, using the most efficient methods to get from here to there.

Yet historically, human drug discovery took a purely biological approach, constantly running experiments to find results. This produced the inverse Moore's Law phenomenon, becoming a form of "mining" like resource extraction.

So why do we believe drug discovery is well-suited to computation? First, the human brain excels at complex logical synthesis and感性分析 — for example, deciding what UI an internet product should use, how to arrange different tabs, whether to show "read" receipts when messaging someone. These are decisions suited for humans.

What do computers excel at? Simple logic, structured problems, and massive rapid calculation. So consider: whether it's the stick-and-ball structures of chemical molecules, or the linear ATCG sequences of genes, these are precisely the types of information computers handle best. ATCG is very similar to binary computer language; stick-and-ball structures are also easily structured. These problems should be handed to computers. Therefore, today's interdisciplinary convergence brings enormous variables to this industry, and we are indeed seeing that never before in human history have biologists and information scientists worked so closely together.

So we boldly predict that, like other industries, the pharmaceutical industry will also undergo this transformation, shifting from a relatively labor-intensive industry to a technology-driven one. In fact, agriculture and manufacturing have already gone through this transition.

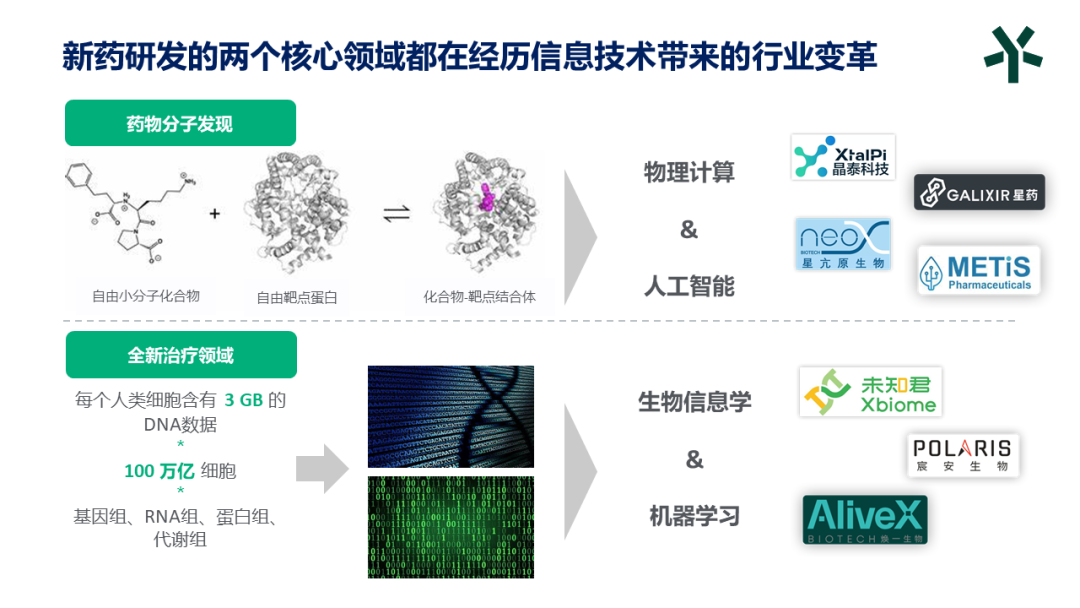

Where exactly will these transformations occur? We divide them into two parts: drug molecule discovery and entirely new therapeutic areas.

In drug molecule discovery, physics-based computing and AI can greatly help us parse drug structures. The four companies mentioned here — XtalPi, Galaxy Therapeutics (星药科技), Neox Biotech, and METiS — are all 5Y portfolio companies in this space.

Another category of companies focuses on entirely new therapeutic areas, which is also fascinating. I've listed some numbers: human cells contain 3GB of DNA data; each person has an average of 100 trillion cells; beyond genomics, our data dimensions include transcriptomics, proteomics, metabolomics, even the microbiome. Building multi-omics data analysis capabilities together, empowered by bioinformatics, can generate entirely new application categories — things that would be fundamentally impossible without IT and computation. Unknown (未知君), Mission Bio (宸安生物), and Huanyi Biotech (焕一生物) are all important players in this space.

We believe computation and experimentation will bring a new pharmaceutical paradigm. What exactly will this paradigm look like? How large will future pharma companies grow? These remain unknown, but we have some clues.

Currently, leading pharma companies like Novartis and Pfizer have market caps around $200 billion. A key reason they've been able to grow so large is the strong scale effects in the pharmaceutical industry. For example, on the clinical research side, there are many critical stakeholders — clinical research organizations, major hospital PIs, regulators. Large pharma companies can build their drug development ecosystems through strong CRO relationships and academic partnerships. Meanwhile, market access and drug sales also exhibit strong scale effects, including pharmacy distribution channels, negotiation leverage with payers, and sales promotion to physicians. Because large pharma companies have strong clinical research and market access capabilities, they dare to acquire early-stage molecules, allowing them to grow relatively large.

However, on the drug discovery side, large pharma still lacks scale effects. Under traditional experimental screening methods, discovered drugs largely don't originate from large pharma companies themselves, but rather emerge somewhat randomly from various sources — perhaps small biotechs or university labs. So large pharma often builds pipelines through acquisitions and partnership R&D; pipelines don't synergize or reinforce each other on the R&D side.

But looking ten to twenty years out, future pharma companies may develop stronger scale effects not just in clinical research, market access, and drug sales, but also in drug discovery. On one hand, IT-plus-biotech R&D platforms can continuously generate new pipelines. At the same time, future pharma companies can use IT to build self-iterating systems, establishing stronger scale effects on the discovery side. When enough data accumulates, every drug developed — whether successful or not — will help make the next drug faster and more accurate.

So we boldly predict that looking twenty years ahead, with the empowerment of information technology, future pharma companies will undergo tremendous transformation, with market caps potentially far exceeding $200 billion.

Finally, let me share some of our other investments and thinking in digital healthcare beyond drug discovery. Most of my earlier examples stopped at drug discovery, but from drug discovery to ultimately benefiting patients, there are several core stages: clinical trials, drug sales, and healthcare service delivery. In each of these stages, the US has very mature companies with market caps ranging from tens of billions to hundreds of billions of dollars.

We haven't yet seen companies of this scale emerge in China, though there are many reasons for this. For example, in drug development and clinical trials, IQVIA is a technology-enabled CRO, while in China the CRO industry remains very fragmented and traditional — though it will shift in the US direction. We've invested in companies like Taimei in this space.

In drug sales, we've also invested in companies that can better help with pharmaceutical marketing and patient access, including Nuoxin and Yunhu. Finally, we believe healthcare service delivery presents enormous opportunities, because China's commercial insurance market will certainly grow. There will be companies like SIPA that can provide cost management and PBM services, and within the social insurance system there are also opportunities for informatization and operations companies — for example, WeDoctor has made very good progress recently. Meanwhile, regardless of who ultimately delivers healthcare services, on the new application supply side we've also invested in excellent companies like Shukun and Shenzhi, which are creating a new generation of healthcare service supply through novel technologies.

We believe that against the backdrop of the IT revolution and China's healthcare system reform, digital healthcare in China presents enormous opportunities for transformation. 5Y Capital will continue searching for exceptional entrepreneurs in this field. If you have entrepreneurial ideas in this area, please reach out to us.

5Y Capital (formerly Morningside Venture Capital), currently manages approximately $5 billion across USD and RMB dual-currency funds. We believe that if the "crazy" you in others' eyes begins to be believed, the world becomes a better place.

BEIJING · SHANGHAI · SHENZHEN · HONG KONG