5Y Capital Investor Notes: Why Mingming Busy? The Truth Behind What's Misread as "Consumption Downgrade" | 5Y View

How does 5Y Capital identify "readaptation" signals in offline retail amid a challenging market environment?

On January 28, Mingming Busy (鸣鸣很忙) officially listed on the Hong Kong Stock Exchange (1768.HK).

From county-town street corners to the HKEX, 5Y Capital — as the lead investor in its A++ round — has been not just a backer, but a close observer over the years. At this milestone, Cui Zhiyuan, Executive Director at 5Y, shares his investment notes.

Looking back at that challenging inflection point in 2023, why did 5Y dare to pull the trigger? The answer wasn't simply "cheap." It was a deep experiment in Chinese retail efficiency.

To many, this looks like a product of "consumption downgrading." But those four words don't capture its vitality. This is actually a retail species unique to China. The core isn't simple low prices — it's a transformation of distribution efficiency.

Here are the key reflections from that time, shared with you.

Cui Zhiyuan, Executive Director, 5Y Capital

Investment Notes at a Glance

- Offline Retail's "Readaptation": E-commerce saturation doesn't mean offline death — it's the optimal window for new giants to emerge under "steady-state competition."

- Efficiency Upgrade, Not Consumption Downgrading: Low prices are the surface; the kernel is channel distribution efficiency gained from direct brand connections and cutting waste.

- $2$2*

- $2$2**$2**$2*

China's vast domestic market with genuine depth — innovations in consumer-facing products and services — has always been a core direction that 5Y continuously cultivates and prioritizes. From smartphones and short-video platforms to new energy vehicles and consumer-grade 3D printing, we're accustomed to finding structural opportunities amid the tides of the era, experiencing industry transformations alongside entrepreneurs.

Today, we want to talk through our thinking on offline retail over the past few years. Amid重重 challenges, several core hypotheses that 5Y's growth-stage team proposed are gradually being validated, while other reflections are becoming clearer as the market evolves.

Left to right: Yan Zhou, Founder, Chairman and CEO of Mingming Busy; Cui Zhiyuan, Executive Director at 5Y; Jin Jiangyun, Managing Director at 5Y

E-Commerce Penetration Nears Saturation

Offline Formats Enter a New "Readaptation" Cycle

Potentially Hiding High-Value New Opportunities

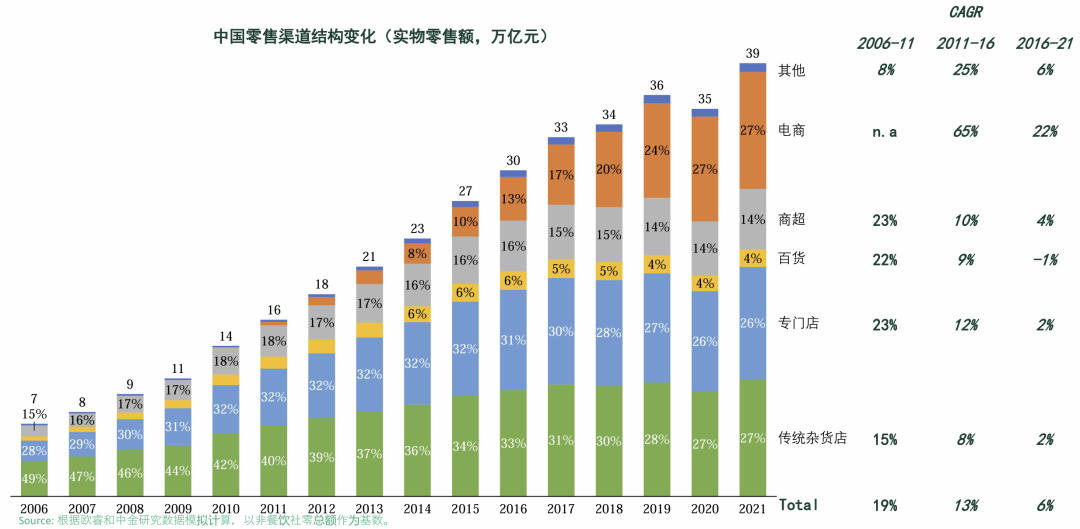

From 2015 to 2020, the explosive growth of e-commerce platforms reshaped the retail landscape. China's online retail sales climbed at a compound annual growth rate exceeding 20%, rising from 10% to over 25% of physical goods retail sales. Meanwhile, offline retail channels grew at a compound rate of merely around 2%.

E-commerce won consumers quickly through efficient internet tools, intelligent recommendation algorithms, plus full-category coverage, massive SKU counts, price advantages, and home delivery services — delivering intense competitive shocks to traditional offline formats.

Constrained by operational inertia and physical boundaries, offline channels struggled to respond rapidly. They needed longer cycles of internal and external management optimization, category restructuring, and pricing system reconstruction to complete adaptive iteration. During this process, the first wave of sharp-nosed entrepreneurs jumped in early, and continuous innovation and upgrading of old and new offline retail formats kept emerging.

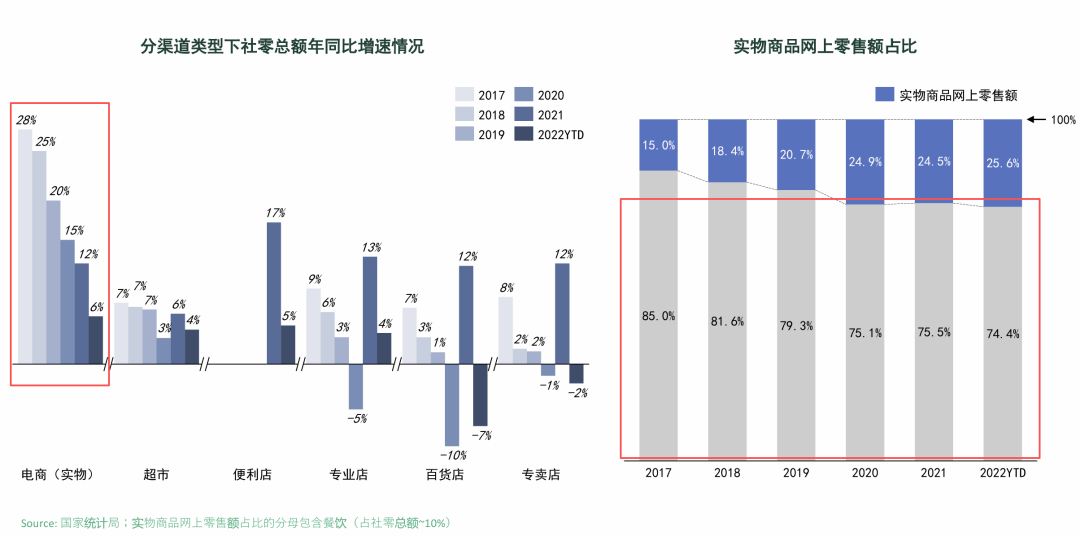

From 2020 to 2025, we observed China's e-commerce penetration gradually entering a stage of approaching saturation. Although interest-based e-commerce and content e-commerce maintained high growth, their essence had shifted to structural changes within online retail channels. Overall physical goods online retail entered single-digit growth territory. Based on this, we attempted to form two rough judgments:

First, when e-commerce platforms were advancing triumphantly, innovation signals from offline formats tended to mix in "empty heat."

As e-commerce penetrated further into population segments and expanded categories, some positive signals could feed back incorrectly. Enterprises that moved into standardized replication too early wouldn't necessarily capture first-mover advantages. For growth-stage investment teams, when online-offline competition entered relative steady-state, it反而 became more favorable for a new generation of offline retail formats to achieve scaled breakthroughs from 10 to 100 to 1,000.

Second, improving channel distribution efficiency and upgrading consumer shopping experience are eternal through-lines in global retail evolution. Pushing either to the extreme can build great companies.

On the experience dimension, online and offline each have strengths: online wins on massive selection and convenient delivery; offline excels at immersive experience, face-to-face service, and what-you-see-is-what-you-get. On the distribution efficiency side — precisely the core bottleneck of traditional offline formats, and also the key breakthrough for competitiveness — if offline formats can precisely find scenario entry points for coexistence or complementarity with e-commerce platforms, their value could achieve exponential amplification.

Based on China's Distinctive National Conditions

A Globally Unique Offline Retail New Format May Emerge

Take discount retail, frequently in headlines in recent years, as an example. Discount retail isn't new, and discount operating philosophies abound: Everyday Low Price, abundant without duplication, B-street A-point locations, highly standardized SOPs, and so on. Globally, numerous market-tested leaders have emerged — Germany's ALDI, Turkey's BIM, Japan's DONKI, America's COSTCO/TJMAXX/DOLLAR GENERAL, among others.

Though these enterprises vary in format, their kernels are highly consistent: pursuing extremes in the balance between distribution efficiency and shopping experience.

"Copy to China" is a reasonable and easily understood investment approach, but when落地 to the retail sector, we have some fresh concerns.

China is a sufficiently distinctive country. We have densely clustered population distribution, diversified taste demands under abundant supply, province-level dietary culture differences, and more critically, a断层式 lead in e-commerce penetration and fulfillment infrastructure. These unique national conditions pose higher requirements for constructing new-generation offline retail business models. Beyond benchmarking mature enterprises, unprecedented innovative formats may also emerge.

In the current market, Hema NB and ALDI, regarded as "China's ALDI," as well as BIGOFFS and HotMaxx, benchmarked against TJMAXX and Don Quijote, have all achieved notable success.

Meanwhile, we also see Mingming Busy as a typical representative of this China-characteristic format: its product overlap with ALDI-style hard discount supermarkets is less than 10%; geographically, it achieves vertical depth from tier-one cities to rural markets, while also realizing nationwide provincial coverage and extending to neighboring countries. The market broadly defines it as "discount snack shops under consumption downgrading." 5Y has its own understanding:

First, it's more than a "snack shop." We're inclined to see it as an innovative packaged food retail solution.

In this new-generation format, snacks are indeed the core category establishing consumer mindshare, but dairy products, baked goods, instant foods, frozen foods, packaged beverages, and others also contribute significantly to revenue. This is what distinguishes it from traditional snack shops and breaks through market capacity ceilings — theoretically cutting into every household's consumption spending wallet.

The snack category itself possesses characteristics complementary to e-commerce,核心源于 "browse-and-buy" and "bulk/scoop" traits. E-commerce's hit-product logic and last-mile fulfillment constraints better suit large-package stockpiling scenarios; snack shops can satisfy personalized, diversified purchasing needs down to single-SKU quantities, with per-item pricing as low as 1-3 RMB. At prices matching e-commerce, they offer significantly richer selection than general supermarkets. Our field visits found that after new-generation formats entered communities, they not only drove up nearby consumers' total snack spending and created incremental demand, but also shifted consumers' snack spending share from e-commerce platforms and supermarkets/convenience stores.

Notably, while a single snack category is often classified as "optional consumption," the aggregation of thousands of snack SKUs with other packaged food categories transforms "optional" into "mandatory consumption," laying the category foundation for becoming a community's core commercial配套.

Additionally, this isn't a simple mapping of "consumption downgrading," but a natural product of channel evolution.

Taking Mingming Busy as an example, its first batch of stores opened in 2017-2018. By 2023 when 5Y entered, the vast majority of stores had been stably operating for nearly five years; now that cycle has extended to seven years, having successively weathered both consumption upgrading and downgrading cycles, demonstrating robust format vitality. This advantage stems from its broad customer age coverage, low consumption barriers, and high, stable repurchase frequency. In merchandise management, standardized display, store decoration, and other aspects, the new format provides an upgraded experience; in some county towns and townships, it even functions as a "mini shopping center."

"Affordable and good value" is consumers' core perception of this format. On the surface, this is achieved through direct brand-to-store connections, compressing intermediate link waste and markup rates to pass savings to consumers. But the kernel is the inevitable law of continuous distribution efficiency improvement in retail. Just as e-commerce was early labeled with "low-price, counterfeit" tags, as the industry gradually matures, genuine value creation continuously earns consumers' authentic choices. What survives cycles is never single operating tricks, but a "consumer-centric" business philosophy — precisely meeting consumers' real needs under commercially sustainable conditions.

Business Models with Efficiency as Their Underlying Color

Competition Likely Converges on Chain Brands

Breaking Through the "Big Market, Small Company" Bottleneck

Barrier height, homogenization degree, and demand sustainability are the soul-three-questions of numerous offline formats, and also the core reason why most细分领域的头部集中度 has historically been low. But we see positive signals emerging in the new era: in new-generation freshly-made tea, freshly-made coffee, Western fast food, and other sectors,头部集中度 is rising significantly, confirming leading brands' competitive resilience and consumer trust in complex environments, breaking the固有认知 that "low barriers must mean homogenization."

Synchronously, retail shows similar trends. New-generation retail leaders like Sam's Club, Hema, and Mingming Busy, even when reaching tens of billions in annual sales, maintain growth above 40%, with industry concentration continuously rising. They not only surpass上一代 retail leaders' peak sales, but also dramatically shorten the cycle to achieve scale.

Limited by single-community consumption carrying capacity, there's a ceiling on store counts for same-price-band, same-type formats (like McDonald's and KFC's regional balanced layout for similar fast-food brands). In efficiency-driven business model competition, scale effects become core advantages — both the foundation for enterprises to weather price wars and抢占优质商品 resources, and the key to attracting external partners. Single-store profitability, competitive resource reserves, and platform security/stability are all equally important, and all deeply bound to scale advantages.

Merchandise is the core载体 and language medium through which brands communicate with consumers. Product development capability is another core competitiveness, directly reflecting a brand's precision in interpreting consumer needs and speed in sensing changes, inseparable from完善的数字化 systems and strong-control, strong-execution organizational capabilities. Merchandise management runs through retail enterprises' entire lifecycle; more precise, more massive data accumulation continuously improves enterprises' operational容错率 and decision quality.

Notably, new-generation retail innovative formats haven't neglected providing positive emotional value to consumers. Pang Donglai integrates sincere care into every detail of the consumption流程, letting trust take root naturally; Mingming Busy, around its mission of "creating happy lives, becoming the people's snack brand," extends into食玩, designer toys, toys, and other categories; Hema provides烟火气的 on-site service and ultra-timely after-sales response, and so on. Beyond efficiency, bringing consumers the warmth and experiential value unique to offline formats.

5Y seeks, supports, and inspires lonely entrepreneurs, providing support from spirit to all operational matters. We believe: if the you whom others see as crazy begins to be believed, the world will become refreshingly different.

BEIJING·SHANGHAI·SHENZHEN·HONGKONG