5Y Capital's Kai Liu: The Evolution of Tech Supply Chain Investing | 5Y View

Three Ecosystems of Hard Tech Investment

During 5Y Capital's annual partner meeting this April, partner Kai Liu shared his reflections on hard tech investing. We've excerpted portions of his talk, hoping they might offer some useful perspective.

He discussed several ecosystems in hard tech investing, and how we should respond to change: "These changes may involve the evolution or stabilization of technology, innovation or continuity in business models, or even deeper shifts or constants in human nature. Change itself is not always positive, and constancy is not always negative. What matters is how we build and refine our own circle of competence."

Kai Liu, Partner at 5Y Capital

Three Ecosystems of Hard Tech Investing

We began thinking about hard tech investing back in the mobile internet era, introducing the concept of the technology supply chain. Looking back at nearly a decade of our hard tech investments, 5Y's methodology for technology supply chain investing has evolved through three stages: from bamboo forest ecosystem, to tropical rainforest ecosystem, to alpine grassland ecosystem.

The term "bamboo forest ecosystem" comes from our long history with Xiaomi, which was 5Y's first major bet after our founding and proved to be extraordinarily successful. At the time there was a book called Xiaomi Ecosystem: Notes from the Investment Battlefield, which contained a phrase that became widely quoted — that Xiaomi approached investing like planting bamboo. Bamboo grows in clusters; for long periods it appears completely still, but after a rain it shoots up rapidly. The roots of bamboo are interconnected underground, creating powerful ecological synergies.

Our early approach to technology supply chain investing was quite similar to Xiaomi's. In the early days of the mobile internet explosion, a billion people had yet to use a smartphone. The biggest opportunity then lay in driving penetration — how to rapidly put various smart hardware devices into users' hands. 5Y's hard tech investments began ten years ago, starting with Xiaomi. For the five years that followed, we stayed focused on this theme, and most of the companies we invested in during this period have since gone public or been acquired.

A particularly important aspect of early-stage investing is continuous evolution, especially in a market as dynamic as China's. As the market evolved, from roughly 2016 to the present, we entered a second phase (rainforest-style investing) with a much more mature playbook.

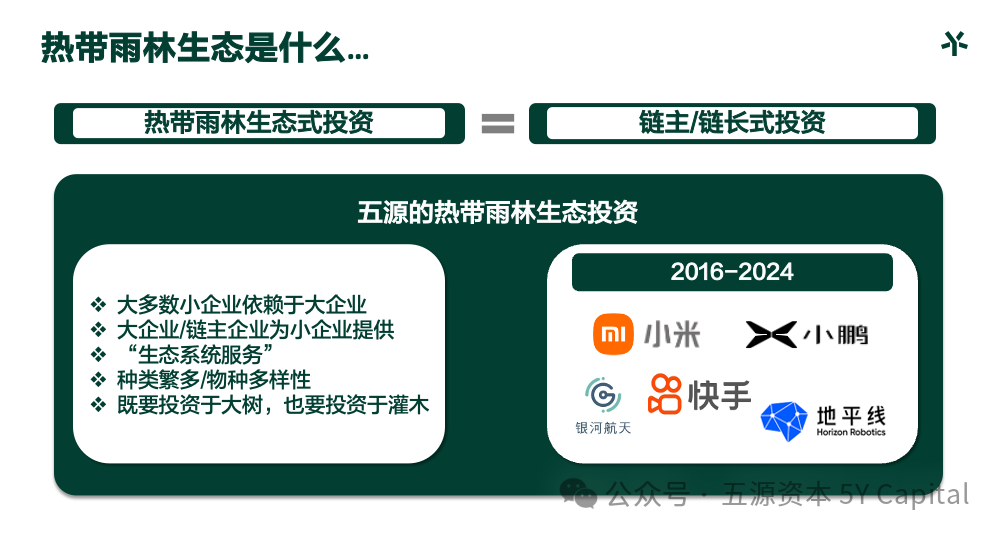

A tropical rainforest is a complex, rich biological network. The towering trees form the foundation of the ecosystem — these are the "chain masters." Beneath them thrive countless shrubs and small animals that depend on the great trees for nutrients and rainwater — these are the "chain leader ecosystem companies." This beautifully captures an investment philosophy: we must invest both in companies that can grow to become industry leaders — chain masters like Xiaomi, Kuaishou, Xpeng Motors, Horizon Robotics, and GalaxySpace — and in chain leader ecosystem companies. Only then does the entire ecosystem hold together. During this phase, 5Y invested in both category leaders and ecosystem companies.

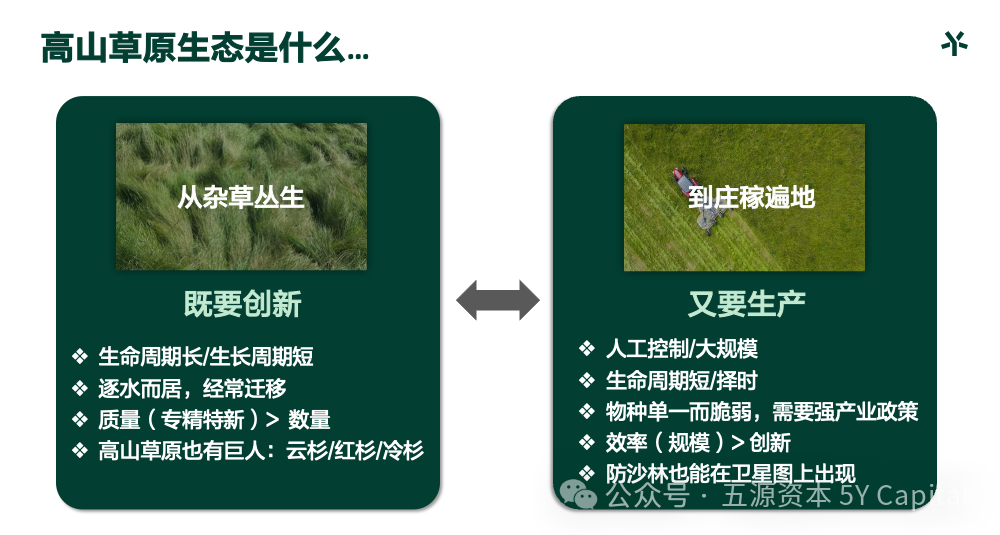

What is the alpine grassland ecosystem? It's a distinctive ecological environment. In China, vast alpine grasslands stretch across Xinjiang, Inner Mongolia, and other regions. The herbaceous plants grow densely but not tall — mostly tangled weeds. These areas are also used for agriculture; people plant alfalfa and other annual crops along the edges of the grasslands. This corresponds to a form of investing that combines both innovation and production.

The scene of weeds growing wild symbolizes an ecosystem brimming with innovative potential. Humans can barely control innovation — this is one of our deepest realizations as investors. Weeds have long growth cycles; they surge quickly when rain comes, wither during drought, and this cycle of flourishing and decay may repeat for decades. Yet weed life is remarkably tenacious. Though grazed by all manner of animals, with the first rains of a new year they spring up again.

On the other hand, can the alpine grassland ecosystem generate outsized returns? In fact, great innovation can emerge even from tangled weeds. Consider the firs — the spruce, the sequoia, the fir — these are among the rare trees that can exceed 100 meters in height, and they all grow in high-altitude, cold regions. Today, we too are searching for globally leading innovation, not only in technological leadership but also in production scale and efficiency.

Innovative Opportunities

Facing the opportunities of the present and the coming decade, what are we looking for?

Economics often discusses beta as the rising tide, alpha as individual effort. In short, we should focus primarily on innovative opportunities driven by mega-scale beta variables. Specifically, there are three layers: First, we are tracking the major wave of battery technology and green foundational energy in China and globally. Second, the improvement of labor productivity. And finally, I'll briefly discuss our understanding of the new globalization.

Over the past 10 to 15 years, Chinese VCs have invested heavily in green energy — from early wind power to solar PV, batteries, new energy vehicles, and energy storage, with wave after wave of technological revolution. From a technology transformation perspective, a critical inflection point arrived in 2023 and 2024: the cost of green energy, especially solar PV, has approached or fallen below that of traditional coal-fired power.

This marks a crucial tipping point for technological explosion. Everyone knows infrastructure requires massive upfront investment, primarily to recover costs in the future. So many people have been waiting for this turning point. I believe by 2023, people could see the sustainability of green energy, because its costs could now compete with coal power. The challenge ahead is how to enable more people to use electricity at lower cost — the reduction in production costs is only the first step, while transmission and storage costs remain relatively high. This may become an important trend in global green energy investment. Over the next 50 years, we will likely enter an era of virtually unlimited, near-zero-cost energy. How to use this almost infinite energy to boost productivity and improve quality of life for everyone is an extraordinarily important question.

Against this grand backdrop, the green energy sector will not only give rise to a cohort of large enterprises but will also nurture a generation of outstanding entrepreneurs. Just as 19th and 20th century America produced railroad magnate Vanderbilt and electricity titan Edison, we are confident that China too will produce similar extraordinary entrepreneurs.

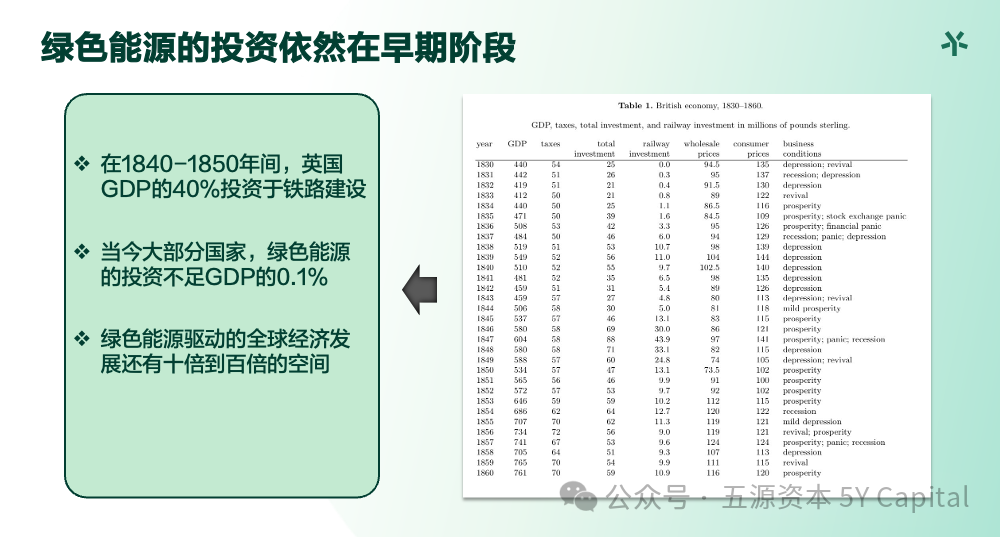

On the other hand, our investment in green energy is still in its early days. Looking back at history, railroads were humanity's first mega-scale infrastructure. Between 1830 and 1860, Britain invested roughly 40% to 60% of its GDP in railroad construction. Today in most countries, green energy investment still amounts to less than 0.1% of GDP. The potential ceiling for green energy is extraordinarily high, and the cycle extraordinarily long — green energy may still be in rapid development when everyone in this room has ended their career.

I recently came across two data points in the news. In the first half of April this year, China's new energy vehicle penetration rate exceeded 50% for the first time, up from just 33% in 2023 — a remarkably fast breakthrough. This means that for every 100 cars sold, 50 are new energy vehicles, whether pure electric, extended-range, or hybrid — all green energy vehicles in some sense.

What does this 50% threshold signify? Smartphone penetration reached 50% in 2014. Something very interesting happened around that time: after this point, software began making real money. This was also roughly when Warren Buffett started looking at Apple and building his position. Globally, 50% penetration signals a major shift in commercial dynamics. Once this level is reached, the probability of software profitability increases dramatically. This is also why people closely watch Tesla's penetration in the US, and whether FSD can become a major revenue driver for Tesla once it hits 50%.

Smartphone普及其实也经历了一个漫长的渗透过程,电动汽车的渗透速度对比智能手机其实丝毫不低,这也为我们看未来的发展趋势提供了宝贵的启示。目前中国是唯一一个在基础设施和应用层面都已经开始形成商业闭环的国家,不管是在基础建设投资,还是商业模式的变化,中国都在驱动整个电动汽车行业发展。

Smartphone普及其实也经历了一个漫长的渗透过程,电动汽车的渗透速度对比智能手机其实丝毫不低,这也为我们看未来的发展趋势提供了宝贵的启示。目前中国是唯一一个在基础设施和应用层面都已经开始形成商业闭环的国家,不管是在基础建设投资,还是商业模式的变化,中国都在驱动整个电动汽车行业发展。

The普及 of smartphones also went through a lengthy penetration process. The penetration speed of electric vehicles is no slower than that of smartphones, which offers valuable insights for understanding future trends. Currently, China is the only country where commercial closed loops have begun forming at both the infrastructure and application levels. Whether in infrastructure investment or business model evolution, China is driving the entire electric vehicle industry's development.

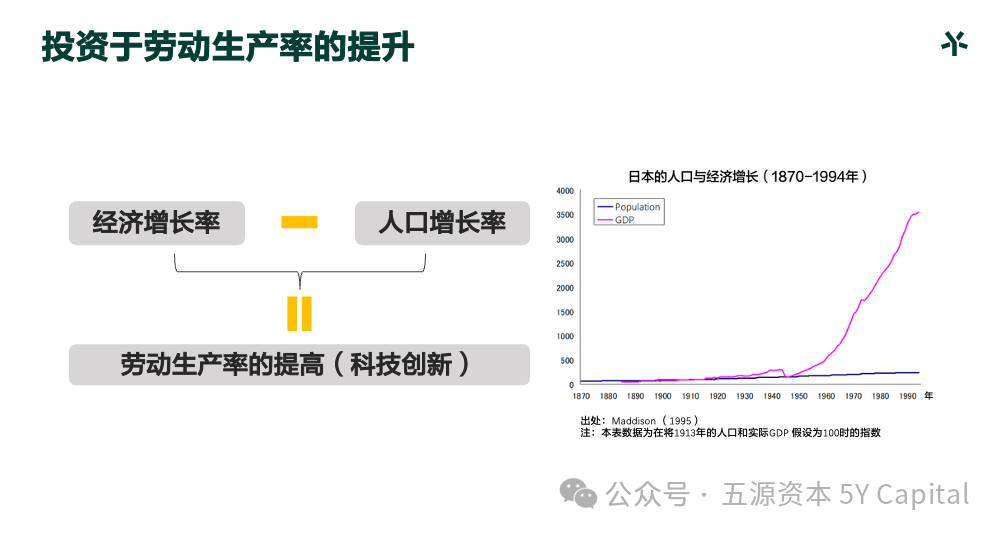

I'd also like to discuss labor productivity. There's a fundamental formula in economics, first mentioned by Schumpeter when discussing the Industrial Revolution's impact on humanity: improvement in labor productivity can be calculated as the economic growth rate minus the population growth rate. Raising labor productivity depends mainly on technological innovation — not on existing stock, but on new increments.

Many people worry that population decline will affect China's economic development. However, if we look at Japan in the 1960s and 1970s, despite experiencing similar population decline, Japan's GDP began growing rapidly. How was this achieved? Because Japan embarked on its first industrial revolution, underwent digital transformation, and developed its semiconductor and automotive industries.

This is why we invest in technology — because technology can significantly improve our productive efficiency. AI, for example, is a fundamental and crucial theme for the next era. Although some believe that after 60 years of development, Moore's Law appears to be weakening, we have actually entered the era of "Huang's Law," which in scale has even surpassed Moore's Law, heralding faster growth.

Previously, TSMC's CEO published an article in IEEE Fellow magazine pointing out that within the next decade, the number of transistors integrated into GPUs could potentially reach 1 trillion. Two major drivers underpin this breakthrough: connectivity technology and advanced packaging technology. From Moore's Law to Huang's Law, the model of technological progress is shifting — from simple two-dimensional stacking to 3D processing techniques, and then to GPU innovation — with the momentum of technological development growing ever stronger. Some worry that as chip sizes increase, so will power consumption, potentially making them unsuitable for phones, and wonder whether this might lead to a stagnation in consumer-level innovation. But this is not the case. As chip parameters increase, their power efficiency and utilization rates actually improve. Both underlying technologies — technical principles and manufacturing processes — are providing powerful momentum for AI's development.

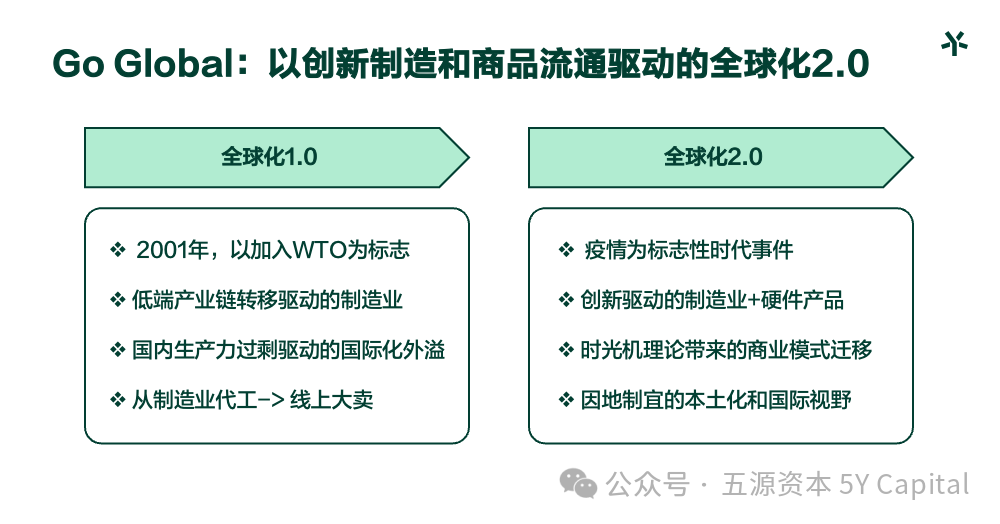

Next, I'd like to share how we view globalization. The hallmark of the previous globalization era was China's accession to the WTO, more than 20 years ago. This era of globalization was characterized by low-end manufacturing and large-scale production, giving rise to certain manufacturing giants.

For Chinese companies, globalization has gone through a very distinct 2.0 phase, with the pandemic as a landmark event. Many of the overseas companies we invested in saw explosive growth after 2020. They no longer limit themselves to traditional low-end manufacturing but have shifted toward innovation-driven high-end manufacturing, including certain hardware products. At the same time, we also see that a large number of Chinese companies succeeding abroad are essentially taking a theory from China to overseas markets — the "time machine theory." Because China has already experienced 20 to 30 years of rapid development, this theory can be very easily migrated to other, less developed countries.

Finally, I'd like to discuss how we understand change and constancy. For VCs, both change and constancy have their advantages and disadvantages. The changes here may involve the evolution or stabilization of technology, innovation or continuity in business models, or even deeper shifts or constants in human nature. Change itself is not always positive, and constancy is not always negative. What matters is how we build and refine our own circle of competence.

Comment to Win

What thoughts and perspectives do you have after reading this article? Feel free to share them in the comments. We will select two standout comments to receive a gift prepared by 5Y Capital :)

5Y Capital seeks out, supports, and inspires lone entrepreneurs, providing them with support ranging from the spiritual to all aspects of business operations. We believe that if the you whom others see as crazy begins to be believed in, the world will become a different place.

BEIJING · SHANGHAI · SHENZHEN · HONG KONG