The Dawning New Cycle | 5Y Annual Share

Where our confidence lies.

Today we're sharing a speech delivered by Qin Liu, founding partner of 5Y Capital, at the firm's annual partner meeting in November 2022. The turn of the year is a natural moment for reflection and forward-looking — to review the path behind us and gather strength for the road ahead. We've compiled excerpts that we hope will offer some inspiration.

The speech was titled A New Cycle in the Making. The past year left many feeling uncertain and confused about the market; a cyclical perspective can help us see the present more clearly.

Technological innovation plays a critical role in driving cycle transitions. Looking at the four key elements of innovation — scientific knowledge, engineering, business models, and capital market validation — China's overall innovation ecosystem shows an unstoppable trajectory. The growth model of the last cycle is no longer sustainable, yet in the next cycle, innovative companies are springing up and growing at remarkable speed. China's dividend of tech talent and entrepreneurs is the foundation of our confidence.

Venture capital, from its very origins, has been a product of cycle transitions — investing in technological innovation, influencing and driving those transitions. We cannot be bystanders; we must be active drivers of industrial cycle change. This is 5Y Capital's mission, and it is a shared mission for all of us.

Qin Liu, Founding Partner, 5Y Capital

Many entrepreneurs and peers have come to me recently asking how to make sense of the present moment. I feel it's important to share our perspective at this juncture. Today's topic is A New Cycle in the Making — using a cyclical lens to understand present and future China seems particularly apt.

To explain this, I want to start with how we define innovation. There's no single answer, but successful technological innovation can be broken into stages — starting from scientific theory, moving into technology and engineering, then finding market demand and combining with business, and finally achieving market validation. These four links form the complete process of tech-industry innovation.

Scientific knowledge is shared human wealth — it cannot be blockaded

We can analyze where China stands at each stage.

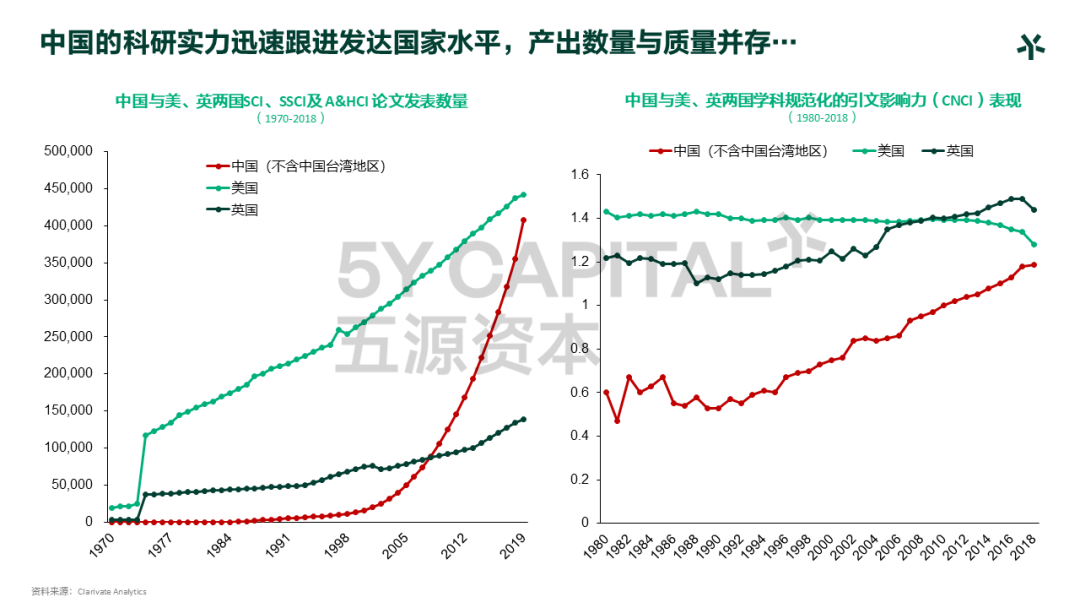

First, we can track the pulse of scientific theory through top global academic journals. We've reviewed China's performance against other developed nations in both publication volume and impact. Since roughly 2005–2006, China's research output has grown rapidly. Both in quantity and quality, China has undergone qualitative and quantitative transformation. And this isn't limited to a single field — across virtually all major scientific domains, China has achieved results that demand attention.

This trend is also visible in the Nature Index 2022 Tables. Ranked by Share (where each article's Share value of 1 is divided equally among its authors — e.g., a paper with 10 co-authors gives each 0.1, and their affiliated institutions/countries each gain 0.1), the US remained first with a 2021 Share of 19,857.35, but its adjusted Share fell 6.2% from 2020. China ranked second with a Share of 16,753.86, up 14.4% from 2020 — the largest increase among the top 10 countries. We may need more time for this to fully settle, but the trend is already difficult to reverse.

Many worry that geopolitical tensions could obstruct technological innovation. But scientific knowledge is fundamentally shared human wealth. Any scientist seeking to validate their discovery as truly effective and authoritative must publish in the international academic community. In this sense, science is open — it cannot be closed off or blockaded.

Where lie our opportunities, and where our challenges

Scientific theory requires engineering innovation to realize it. If scientific knowledge is like tree roots, technology and engineering form the trunk of industrial innovation. Without the trunk, there are no products or engineering feats. Meanwhile, all high-tech companies strive to turn their science into proprietary know-how or intellectual property.

Tech-industry moats actually come in two forms. One is IP and process knowledge — somewhat closed by nature. The other is open-source ecosystems, where everything is opened to others. The deepest layer of scientific knowledge is inherently open-source, but at the industrialization stage, it splits into open and closed forms.

In information technology, much software grows on open-source ecosystems — including today's AI algorithms and foundational biological science. Some industries are closed-source, like semiconductors: globally, perhaps a handful of equipment makers dominate. Though scientific knowledge is open, materials, processes, and industry know-how form formidable moats for these companies.

For these closed-source industries where others have accumulated decades of experience, catching up quickly is genuinely difficult. Yet "chokepoint" pressures themselves create opportunities for Chinese innovators. In a fully open market, startups struggle to compete against decades of experience and mature products. But when massive demand exists and supply is disrupted, it forces innovative companies to find their application markets.

Beyond these industries, numerous emerging sectors have the world starting nearly from the same line — new energy, energy storage materials, batteries. Much of the process here is know-how, and China is running alongside or even overtaking others.

In open-source industries, the internet has already proven Chinese innovative capacity — we have distinctive payment platforms, social platforms, traffic ecosystems, and e-commerce. In emerging open-source sectors like cloud computing and AI, China is also among the global leaders. Take smart vehicles: built on battery/energy storage materials and autonomous-driving AI applications, the new energy vehicle industry currently sees China and the US running neck-and-neck, leading global development.

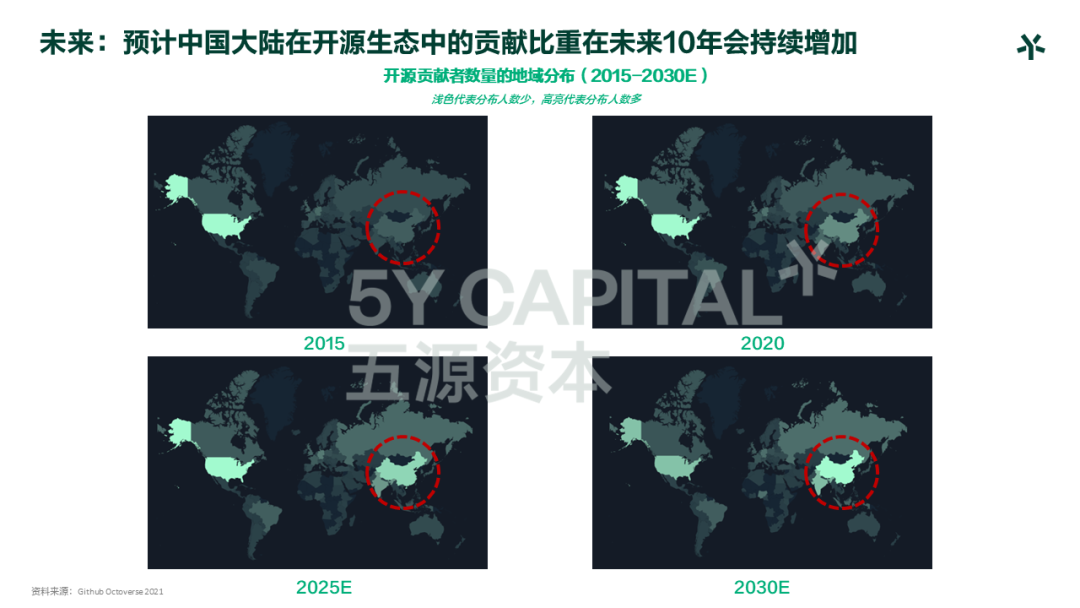

We can look at software to see how open-source ecosystems are evolving. On GitHub, a key developer community, the number of open-source projects created in 2022 grew year-over-year. Interestingly, while COVID-19 devastated many industries, it somewhat boosted open-source prosperity — creative programmers at home kept generating new open-source code. Open-source software as a whole is in rapid development.

Where does China stand in this ecosystem? In the figure below, color brightness indicates contribution level to open-source software. The US leads by a wide margin, but from 2015 to 2020, China's color has grown increasingly bright. Projections suggest that by 2030, China's open-source contributions may surpass other countries.

5Y Capital has also invested in several open-source ecosystem companies, such as PingCap and Zilliz, which have achieved significant global success. Currently, open-source projects led by Chinese developers account for 12.5% of the global total, but generate only 1% of cash flow — in our view, these represent opportunities.

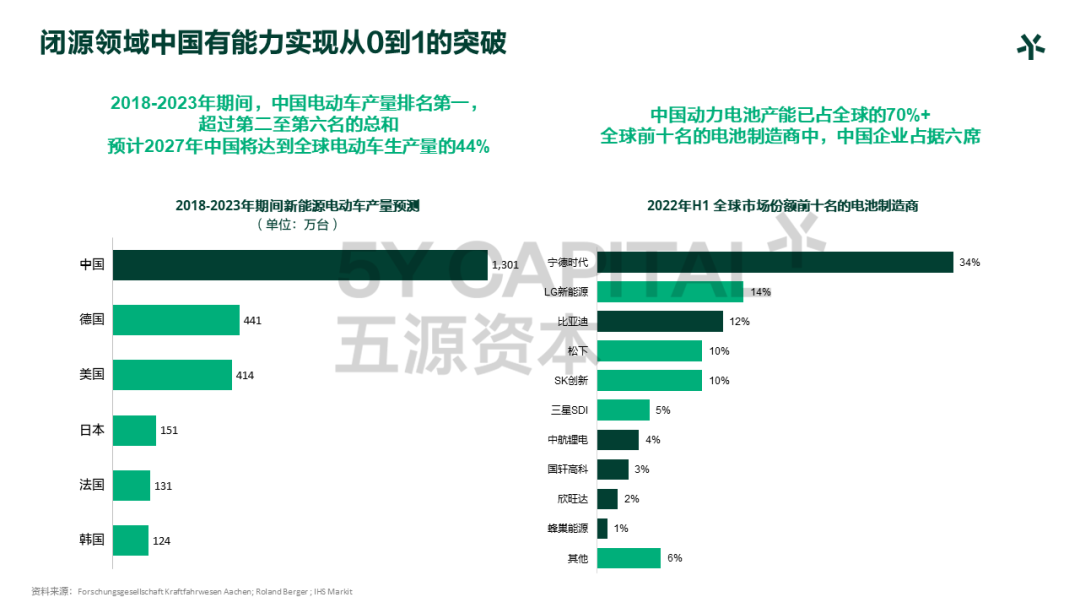

We can also look at closed-source technology breakthroughs using energy storage batteries as an example. Batteries underpin new energy vehicles — among the world's top 10 battery manufacturers by market share, Chinese companies occupy six seats. In fact, across many high-tech industries, China is producing world-class pillar companies.

Overall, technological innovation is one large open-source ecosystem. Our challenge is converting this shared human wealth into genuine industrial advantage. For the present, we have no reason for pessimism — rather, we should clearly see where our opportunities lie and where our challenges stand.

Our comparative advantages

So what are China's true comparative advantages in technological innovation?

First, we have an enormous market. Many underestimate this — there are dozens of developed economies worldwide, but only China and the US are large enough to sustain the venture capital industry and truly sustain profitable technological innovation long-term. Why? Because innovation is extraordinarily expensive. Innovation demands massive trial-and-error costs; essentially, innovation is a game of scale economies. If your economic scale is hundreds or thousands of times larger, you have entirely different comparative advantages.

Second is the breadth and depth of China's commercial application scenarios — this means fertile soil for innovation. The internet's development proved this: never underestimate the innovative soil created by population scale and demand diversity.

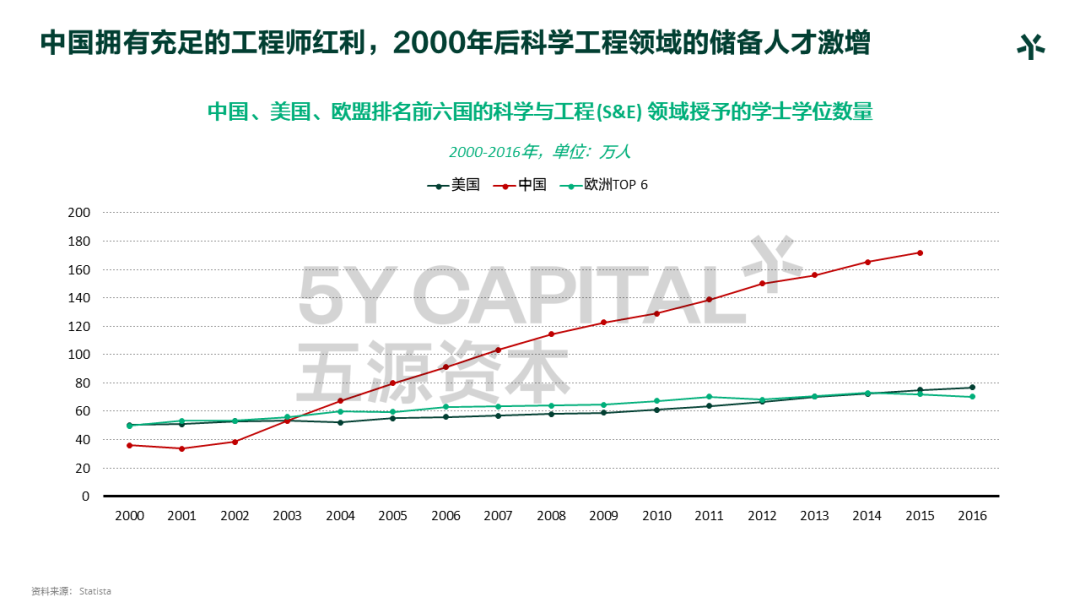

Third is the engineer and entrepreneur dividend. Many today say China's demographic dividend has disappeared, but another dividend is rising. If the past 30 years of manufacturing relied on China's labor dividend, present and future innovation relies on the rise of China's quality human capital dividend.

For now, the US remains the world's largest innovation economy, but China has joined the top two global economies and possesses one of the only two home markets with sufficient scale to amortize innovation's trial-and-error costs.

Regarding innovative application scenarios in hard tech: our portfolio company Agora has become infrastructure for the entire real-time interaction field, using pure software algorithms to provide real-time audio/video infrastructure — building a cross-border, integrated internet-scale telecom network globally, with various emerging companies using their APIs.

PingCap is a database company that open-sourced its code on GitHub. People used to ask whether only top database vendors like Oracle could become infrastructure. But open-source software's nature gives smaller companies opportunities — they can showcase products and code directly, and clients can trial them. When enterprise clients adopt for production use, they also consider paid services. PingCap has already developed global customers.

While many remain fixated on last cycle's industries and capital market prices, the companies truly at the core of the new cycle are springing up and growing at remarkable speed. Chinese companies' innovative capacity isn't merely conceptual — it's being market-validated across domains.

Biotech is another example. Chinese innovators are using AI tools to create disruptive drug R&D infrastructure serving global pharmaceutical companies. Our portfolio company XtalPi uses intelligence- and automation-driven drug discovery to improve new drug success rates, empowering top global drug developers. Another portfolio company, Helixon, was founded only in June 2021 but has already made major breakthroughs. In July 2022, they developed OmegaFold, an algorithm predicting 3D protein structure from single sequences alone — a milestone in computational biology history.

Across technological innovation's various domains, Chinese companies have achieved numerous breakthroughs. An important factor behind this is that China's government is a genuinely industrially proactive government. The government provides macro-level industrial guidance and promotion — in new energy vehicles, for example, Xpeng Motors benefited in its early development from China's efficient NEV subsidies, which helped address early industry challenges of insufficient range and lacking infrastructure. These policies also guided the entire industry's trajectory.

So due to market scale, the breadth, depth, and richness of commercial application scenarios, and proactive government guidance among other factors, China's technological innovation industry possesses very powerful momentum. But these are necessary conditions; the crucial sufficient condition remains China's entrepreneurs. Technological innovation ultimately depends on talent innovation, and China's innovation talent foundation lies in the far greater number of STEM graduates China trains annually compared to Western countries — this is China's quality human capital dividend, a structural high-tech human capital dividend.

China has already produced world-class entrepreneurs, and we believe a major wave more is on the way. Our quality human capital dividend and entrepreneurs are the source of our confidence.

If your vision and focus are on the next cycle, you'll be full of confidence

With scientific knowledge, engineering capability, and business model integration, we finally need market validation.

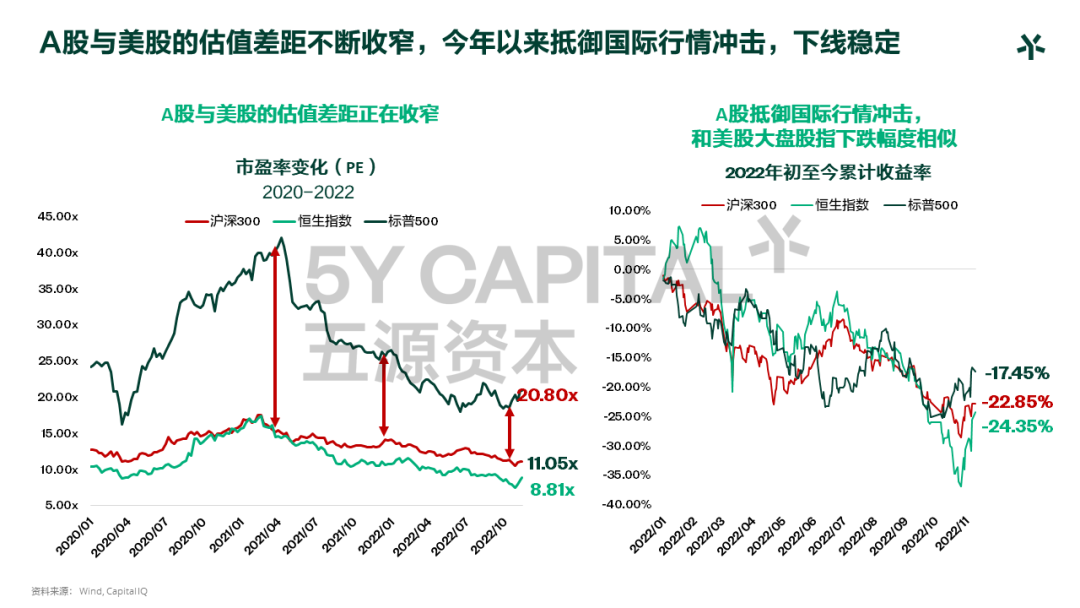

The figure below shows that due to global capital market linkage, both Chinese and US valuations were impacted this past year, but overall, A-share valuations have increasingly converged with US markets. This somewhat demonstrates A-shares' resilience against international market shocks. Also by trading volume, China's markets are more active.

We've also tallied IPO counts across A-shares, Hong Kong, and US markets over the past three years. Due to pandemic effects, 2021 saw some gap between China and the US, but in 2022 with US Fed rate hikes, China surpassed the US by IPO count. And among the world's top ten IPOs by fundraising scale, A-shares had four and the Hong Kong Stock Exchange had two.

As for the tech sector, with the STAR Market's launch, emerging tech industries' capital market performance has actually grown against the trend. We can see A-shares' industry structure gradually shifting toward "hard tech" — in 2022, 70% of IPOs concentrated on the STAR Market and ChiNext, with 80% of these companies commanding P/E ratios above 30x. Compared to US markets, A-shares also grant higher valuations to these emerging tech industries. From 2020 to 2022, A-shares' industrial, materials, energy, and utilities sectors saw notable market cap share increases, corresponding to declines in financials, real estate, and consumer sectors' shares.

From a cyclical perspective, we must look beyond surface appearances to deeper structural changes. Capital market cycles reflect industrial economic development — so-called cycle transition means the growth logic of last cycle's core industries and companies has become unsustainable, while many emerging industries of the next cycle are growing rapidly. If your vision and focus remain on the last cycle, you'll be pessimistic; when you stand in the next cycle, you'll be full of confidence. Don't let surface emotions interfere with long-term judgment.

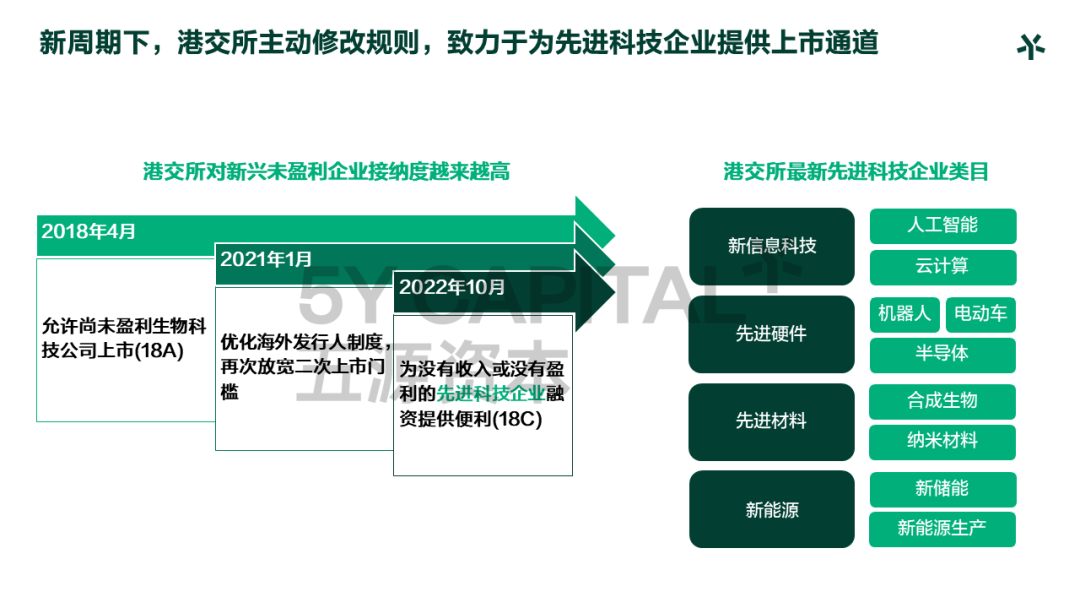

We can also look at Hong Kong — "the spring river's warmth the duck knows first," capital market players have already begun positioning with next-cycle perspectives. Hong Kong has made very positive changes these two years: 2018's Chapter 18A specifically for life sciences, and October 2022's added 18C, which essentially facilitates listings for information technology, advanced manufacturing, and materials/energy sectors — no profitability required. Hong Kong is also extending greater support to emerging tech sectors.

As the four key elements of technological innovation — from scientific knowledge to engineering, business models, and capital market recognition — our path today is widening. China's overall innovation ecosystem has an unstoppable, irreversible development trajectory.

The macro challenges we face are essentially China's need to achieve genuine industrial structural adjustment. Looking at America's historical path, they too actively restructured industry every 10–20 years, with each adjustment led by technological innovation creating entirely new industries. China rode the fast lane with the internet wave, and today in AI, life sciences, carbon neutrality and other emerging fields, China and the US are running neck-and-neck, actively leading the next industrial structural adjustment.

Investing in "people"

At its core, investing comes down to two things: investing in "trends" and investing in "people."

Entrepreneurs share certain characteristics — vision and insight about the future, very strong execution capability, and innovative capacity. But hard-tech innovators must simultaneously possess global vision and resource integration capability, because this is inherently global competition. They need not just business acumen but also technical taste and technical judgment — this "dual-core" capability to gather global tech talent.

In fact, the hard-tech entrepreneurs we invest in show clear global and cross-boundary characteristics. Because today's technological innovation isn't vertical-domain innovation but cross-domain integrative innovation. As companies evolve, 5Y Capital is also actively evolving.

We cannot simply repeat past track records — we must iterate and evolve upon them. Our core judgment of people hasn't changed, but we must add different elements, combining rationality and sensibility, technology and business. Our cognition must penetrate into highly specialized knowledge structures. If we're to think in first principles, we need systematic connections with global institutional labs and scientists, because innovation cannot be done well behind closed doors.

Many today express pessimism, opening with macro questions, but macro questions are fundamentally about industrial structural adjustment. Truly solving macro problems requires starting from the micro level. If we can actively iterate away from last cycle's unsustainable industries, find the core industries supporting the next cycle, and cultivate them, we can enter the new cycle.

Venture capital, from its very birth, has been a product of cycle transitions — investing in innovation, thereby promoting industrial structural adjustment. We cannot be bystanders; we must actively be drivers of industrial cycle transition. This is 5Y Capital's mission, and a mission we all share.

Giveaway

We welcome your thoughts and perspectives in the comments. We'll select two commenters to receive a "5Y Capital New Year Book Blind Box."

Note: Giveaway closes at 18:00 on January 19, 2023. Please reply with shipping information within 24 hours of notification.

5Y Capital seeks out, supports, and inspires lonely entrepreneurs, providing support from the spiritual to all operational aspects. We believe that if the "crazy you" in others' eyes begins to be believed in, the world will become a different place.

BEIJING · SHANGHAI · SHENZHEN · HONG KONG