A Green Paper for VC Practitioners in an Era of Upheaval | 5Y View

Finding, discovering, and backing true innovators is what 5Y Capital has focused on for years, and it's also the standard we hold ourselves to as we continue to evolve.

Today we're sharing an original essay by Kai Liu, partner at 5Y Capital. He calls it a "green book," but it's really a letter to himself.

There's perhaps no better time than the present to look back at history, even though history offers no instruction manual. Predicting when crises will arrive and how long they'll last — using the present to forecast the future — is often no better than marking the boat to find a lost sword.

But reviewing history helps us understand cycles more clearly — the rotation of seasons, the eternal logic of nature. Lows always come, and they always pass. If cyclical change brings enormous uncertainty to the present, then the one certainty is that a new cycle will arrive, regardless of human will.

VC has been a product of cyclical change since its very inception — investing in technology and innovation, disrupting the status quo, and boosting productivity, thereby influencing and driving the transition between cycles. Markets have their highs and lows, moments of doubt and wavering. If investing in innovation is VC's mission, then actively evolving through each cycle transition must be its first law of survival — and only a fortunate few have the capacity to adapt to this difficult game.

Finding, discovering, and supporting true innovators — this is what 5Y has focused on for many years, and what we expect of ourselves as we continue to change and innovate.

A Green Book for VC Practitioners in an Age of Upheaval

Kai Liu

Partner, 5Y Capital

The name "green book" comes from a Texas Hold'em manual I've been reading lately, though this essay has nothing to do with poker. The meaning lies more in the self-reflection and utility that a green book implies — think back to the "little red books" from school, and you'll understand the warning function of a green book: it's always the first thing your eyes find on the shelf. Lessons and teachings in no-limit investing. These small tips may be especially important in the era we find ourselves in. Consider this a letter to myself.

Understanding Cycles Correctly, and Correctly Understanding Cycles

As we all know, cycles exist widely in nature — from the movement of celestial bodies to the alternation of agricultural seasons to the metabolism of cells. Cycles may be one of humanity's most profound understandings of the world's many irresistible forces since ancient times. Cycles are equally prevalent in human society, with economic cycles being among the most common phenomena.

It's worth noting that economic cycles are not a product of modern industrial civilization. Numerous economic historians have demonstrated that throughout the long feudal agricultural era, irresistible economic cycles also existed — except they were more influenced by climate change, religious belief, and dynastic succession. In China's unified empire, countless minor economic cycles occurred as well.

Similarly, in the half-century we have personally experienced, there have been five major economic recessions. Looking at the frequency, a crisis of ordinary magnitude occurs roughly every ten years.

- 1973–1974 oil crisis

- 1980–1982 international financial crisis

- 1990–1991 international economic crisis

- 2000–2002 dot-com bubble

- 2008–2009 subprime mortgage crisis

- 2020–2022 (and beyond) COVID-19 crisis

If we extend the timeline and look back at the last 100 years of global history, this pattern still holds. The world economy experiences a shock every ten years, but like a pendulum, over that decade-long cycle, the economy and technology rise to peaks and fall to troughs, then in the next cycle reach even higher peaks before returning to temporary lows. Of course this is a simple empirical summary — when the next crisis will come and how long it will last cannot be predicted by marking the boat. But there is an important psychological implication here: lows always come, and lows always pass. Everyone is sitting on the pendulum.

If we go further and categorize crises, we see even more interesting insights. The causes of crises are numerous, but we can roughly divide them into two types: systemic crises, or "gray rhinos"; and sudden crises, or "black swans." If we reclassify the last six crises, we get this table:

No mathematical analysis needed to reach a conclusion: most crises are systemic — things that were bound to happen. Very few crises fall into our blind spots. The implication here is: if systemic crises can always be resolved, then as accidental events, black swan crises are even less worth worrying about. The ecosystem of human society is very good at self-correction.

Returning to the venture capital industry itself, we too are experiencing a cycle: the tail end of one industry paradigm, the starting point of the next.

The Several Paradigm Shifts in VC Investing

For most VC practitioners, including myself, we have never fully experienced an investment cycle. I joined the industry during the mobile internet wave of 2014. If we use the Gartner Hype Cycle, our generation of GPs mostly entered during the Early Growth phase — we experienced the industry's expansion and its glorious peak. But our biggest problem is not knowing what happened in the previous cycle, what its peaks and troughs looked like.

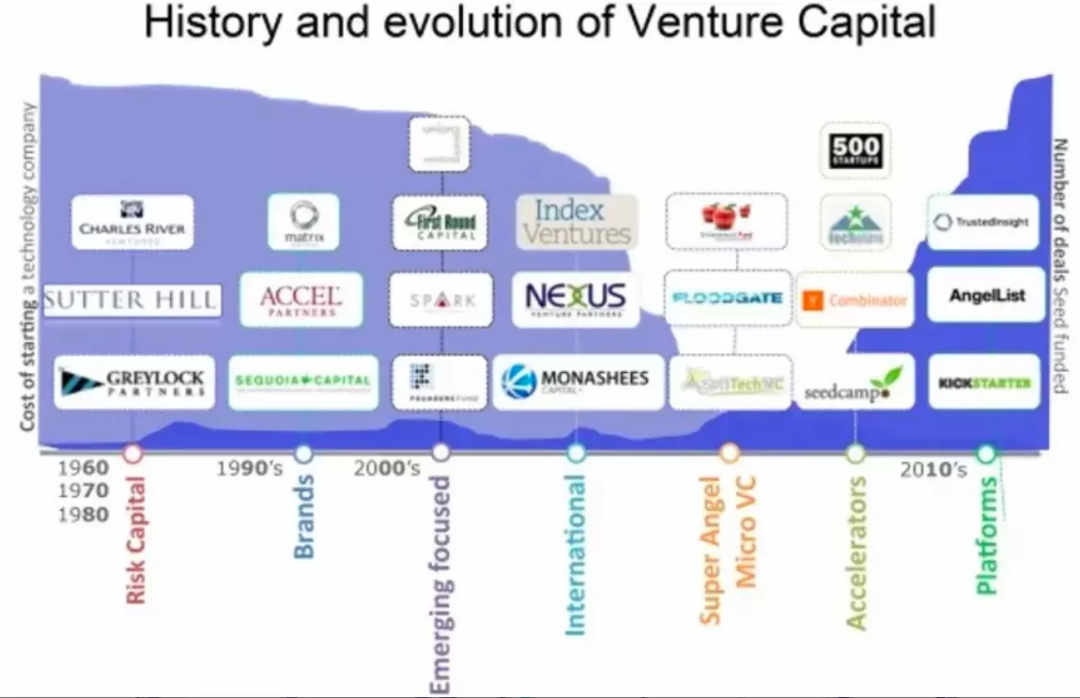

This inevitably leads us to study some history, starting from the origins of venture capital.

Venture capital originated in the United States. The first modern VC firm, ARD, was founded in 1946. At the time, regulations didn't support raising capital from institutional investors, nor could firms raise multiple funds with continuous existence. This forced ARD to go public, which severely limited its development.

But ARD itself became an incubator of industry talent. Elfers, who left ARD, founded the renowned Greylock Capital on the East Coast. Another group went west and successively founded KPCB, Sequoia Capital, Mayfield Fund, Sutter Hill Ventures, IVA, and other well-known firms.

Beyond this numerical proliferation, the VC industry has also experienced several major paradigm shifts. Initially, many of the West Coast titans who got into venture capital started from an understanding of how microprocessors could build and transform industries. Looking at Sequoia and KPCB's early successful cases, VC's core investment focus during this period was concentrated in hard tech (mainly semiconductors and biotechnology). Individual fund sizes were small, headcount at each firm was minimal — it was a master-apprentice workshop management stage.

As these firms accumulated more successful investments, the VC industry underwent dramatic changes in the early 2000s. Before the dot-com bubble burst in 2000, massive capital flooded into venture capital, enabling further institutionalization. Many firms expanded rapidly. With increased capital, internal structures changed — positions multiplied, and investment focus shifted more toward internet and business model sectors. After these large funds recovered from the internet bubble, many turned their attention back to hard sciences and began investing in two major technology trends of the time: nanotechnology and clean energy. The VC industry began its first return to domain roots.

It's worth noting that since most funds have roughly ten-year lifespans, the majority of funds established around the dot-com bubble performed worst during the subsequent decade (2001–2010). Comparing returns across asset classes during this period, venture capital was not only the riskiest asset class but also the worst-performing.

Fortunately, some funds discovered new territory: the rise of social networks (including e-commerce) and mobile internet — industries extremely well-suited to the VC investment model. Thus, from the late 1990s to early 2000s, the massive capital flowing into VC rapidly migrated toward social network (e-commerce) investments. Firms that didn't make this shift — approximately two-thirds of them — ultimately went bankrupt in what was the most difficult venture capital environment in history, during 2001–2010. Post-2011, the VC industry was fundamentally different from what came before.

The funds that survived post-2011 began making bold moves in internet and mobile internet, and because both sectors had strong network effects and scale advantages, the survivors began another round of consolidation and institutionalization. Fred Wilson of Union Square Ventures wrote as early as 2015 that the red-ocean competition in internet investing had made it nearly impossible for firms to make money on companies like Uber. The prescient began new explorations, and once again, a small number of funds with sharp instincts found two new blue oceans: SaaS investing and crypto investing, happily boarding a speedboat for a new decade. What happened in this later decade is well-known to most domestic peers, so I won't elaborate.

Reviewing this history, we can now summarize the patterns:

- The VC industry changes every five years, transforms every ten years — this is the pattern, and our own cycle.

- Funds that don't change proactively will certainly die; funds that do change proactively will probably still die.

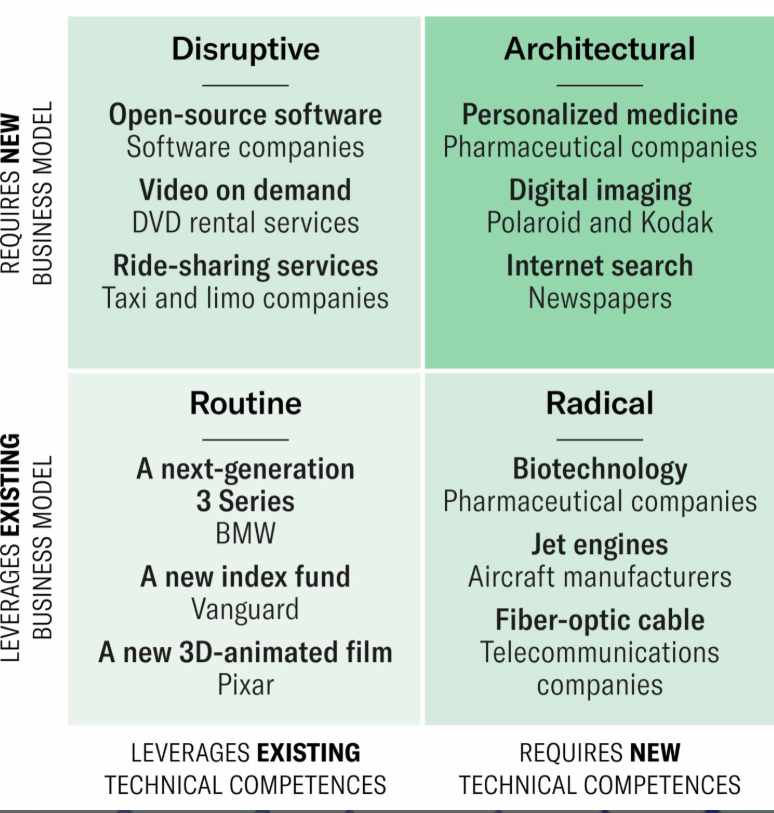

- The VC business model determines that we're better suited to investing in disruptive, structural-change startups — these are the areas where we're more likely to achieve outsized returns.

- Don't invest in incremental innovation in mature industries, and don't invest in companies where the market and industry don't yet exist.

Image source: Harvard Business Review

Building Simple Long-Term Faith: Technology Changes Productivity, Venture Capital Changes the Technology Industry

The foundation of the VC industry is investing in innovation. Innovation brings new tools; new tools boost productivity. But this also implies enormous risk. During every economic crisis and industry trough, skepticism toward innovation peaks, and faith in technology hits its lowest point.

So I've listed some of the laws of innovation here — their development proceeds regardless of human will:

- Moore's Law: The number of transistors or components that can be accommodated on an integrated circuit doubles every 18 months

- Carlson's Curve: The performance doubling and price decline of DNA sequencing technology keeps pace with or exceeds Moore's Law

- Rose's Law: The growth rate of qubits in quantum computers approaches or has already surpassed Moore's Law, roughly doubling annually; Neven's Law asserts this growth rate is double-exponential

- Battery performance doubles every 9–14 months

- Cooper's Law: The wireless communications capacity in a given area doubles every 30 months

- IoT connected devices grow at 15%–20% annually

- Gilder's Law: Total bandwidth of internet services triples every 12 months

- Global OLED screen area grows roughly 30% annually

- Haitz's Law: Every year, LED lumen output increases 20-fold while cost per lumen drops to 1/10 of the initial price

- In industrial production, for every doubling of market scale, productivity improves by an average of 5%–10%

- Koomey's Law: The energy consumed to process a given amount of data drops 50% every 18 months

- Kryder's Law: Hard disk drive storage recording density improves 1000-fold every ten and a half years

- Moore's Law Marginal Corollary: The price of digital products with equivalent performance drops 30%–40% annually

- The world's total data volume doubles every two years

- Nielsen's Law: High-end individual user internet speed improves 50% annually

- Computer storage prices drop 20%–30% annually

- Since the 1960s, the triple product (density, reaction temperature, and confinement time) in nuclear fusion experiments has doubled every 1.8 years

- Ziman's Law: Global scientific activity doubles every 15 years — meaning it grows 100-fold every century

All of this is exhilarating, especially since this list keeps growing. Behind every law is the result of technology continuously boosting productivity. Innovation is accelerating, and VC has played enormous value in this process.

Power Laws of Venture Investing

Peter Thiel once said: The greatest secret in venture capital is that the best investment in a successful fund equals or exceeds the total returns of all other portfolio investments combined.

This is the so-called power law of the VC industry, fundamentally determined by fund size and lifespan. For a standard ten-year venture fund, the correct way to allocate capital is to ensure every single investment has the potential to return the entire fund. Take a $200 million single fund: if it plans to invest in 20 companies over its lifespan, that's roughly $10 million per ticket, which in turn requires each investment to have the potential for a $200 million return — equivalent to 20x per investment. At an average market entry valuation of $50 million, the company must reach unicorn scale to achieve this return. And this doesn't account for dilution in subsequent rounds; factoring in average dilution, a company needs to reach at least $2–3 billion in valuation for early investors to hit a home run.

The VC industry's game of pursuing home-run investment returns is unlikely to change in the near term, because this is the nature of VC investing. Of course, in this process, some firms like to swing at every pitch, while others prefer to wait patiently for the right pitch — different preferences and habits both have successful cases. But one thing is crucial: you must hit home runs, and then wait for the next home run.

What Texas Hold'em Teaches About VC Investing

In Texas Hold'em, the most important decision happens pre-flop: Should I play these two cards?

Play aggressive poker: Before considering checking or folding, first consider betting or raising. Apply pressure to opponents. Aggressive poker is correct poker.

Bayesian thinking: Use new information to refine your hypothesis as you go. Poker is fundamentally about accepting uncertainty in the game through probabilistic thinking.

Texas Hold'em, like venture capital, is a practical application of Bayesian statistics — gathering information through chips is faster than any other method.

Use questions to get answers, thereby predicting futures that are more likely to occur.

Have patience. Wait for favorable situations before entering the pot.

Have courage. You don't need the nuts to bet, call, or raise.

Continuously refine your skills to become a better player. Discuss hands with others, practice, read poker tutorials, analyze your own play to find weaknesses and improve them.

Returning to the Challenges and Opportunities of New-Era Hard Tech Investing

Timeframe Mismatch: Find Industries That Have Taken a Time Machine

Due to open-source software and cloud computing, the initial startup costs for internet model entrepreneurs have dropped dramatically. Ten years ago, starting capital was in the millions of dollars; now you just need a laptop. Open-source and cloud computing have reduced both early R&D costs and subsequent operating expenses by over 90%. Meanwhile, because internet products more easily find product-market fit, trial-and-error and iteration cycles typically take just months. This rapid feedback, small-investment model is extremely well-suited to early-stage VC. And once early positive feedback is achieved, subsequent user growth can become exponential, making new funding easier to secure.

By contrast, look at several major hard tech investment sectors: semiconductors, energy materials, biotech and medical. Early technology R&D typically takes 3–5 years, market adoption another 3 years, and engineering scale-up yet another 3–5 years. The highest cost barrier is semiconductors — between EDA software and IP licensing, $5 million disappears quickly. The longest timeline is biotech and medical: without ten years, it's hard to reach clinical and validation stages.

Hard Tech Investing Can Still Deliver High Returns — You Just Have to Wait Longer

Many investors coming from the internet investment paradigm have a misconception that hard tech and manufacturing investments, because they take too long and require too much capital, may have limited return multiples. This is not the case. I can cite a few anonymized examples:

- Company C in new energy: Series A and B investors achieved over 100x returns on a single project

- Company B in new energy vehicles: Series A investor achieved over 1000x returns on a single project

- Company H in smart security: Series A investor achieved over 1000x returns on a single project

Blinds Are Too High: Find Industrial Leverage

Take several highly successful hard tech investment cases from recent years. Flagship Ventures' first investment in Moderna Therapeutics was $600 million. ARCH's investment in Juno Therapeutics raised $300 million across two rounds within a year. This massive increase in initial investment amounts can, on one hand, help hard tech companies raise enough capital to survive R&D challenges. On the other hand, it poses greater challenges for investors: for a $400 million early-stage fund, daring to invest over 20% in a single project requires absolute confidence in the investment's success rate. Otherwise, the fund faces catastrophic destruction.

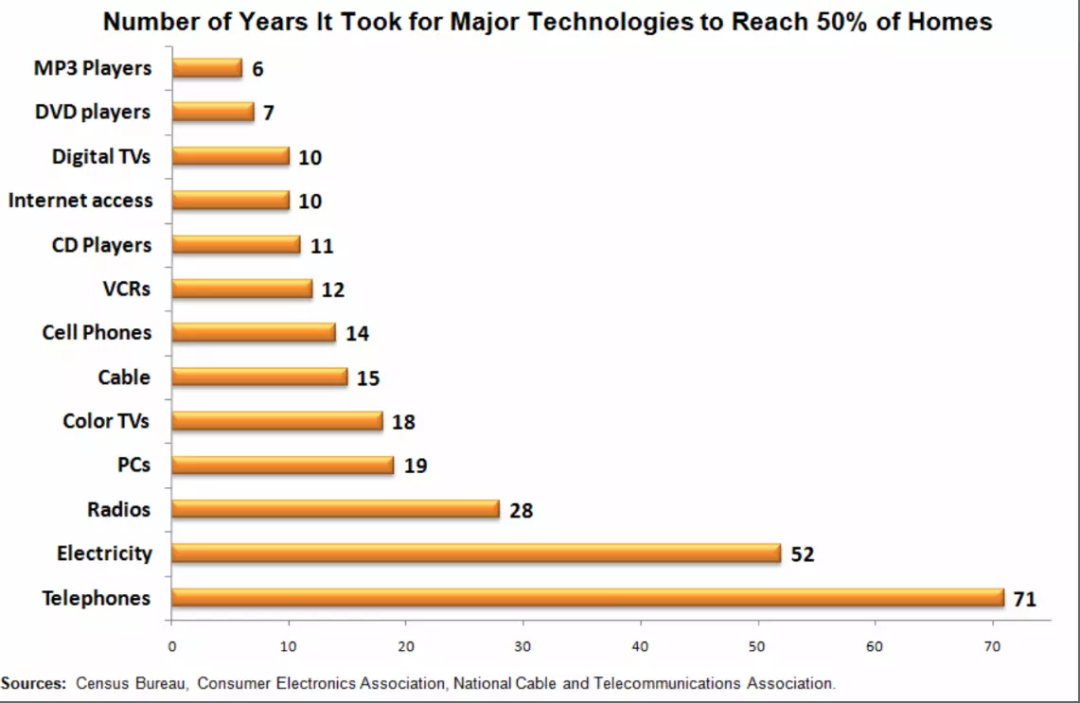

New Technology Diffusion Takes Time: Getting Timing Right Is Extremely Important

Finally, take another look at this old chart — hard tech inflection points do indeed take time.

Comment to Win

We welcome you to share your thoughts, perspectives, and views in the comments. We'll select two featured comments to receive a 5Y Capital commemorative hoodie + mystery book box. (Comments accepted until November 20. Please reply with shipping information within 24 hours of receiving our message.)

5Y seeks out, supports, and inspires lone entrepreneurs, providing support from the spiritual to all operational aspects. We believe that if the you whom others see as crazy begins to be believed in, the world will become a different place.

BEIJING · SHANGHAI · SHENZHEN · HONG KONG