FreeS Fund Report 13: To Understand China's Consumption Upgrade, Look at Japan 40 Years Ago

Consumption upgrade versus consumption downgrade — which one holds more opportunity?

In this 13th edition of the FreeS Fund report, we're talking about the currently hot topic of consumption upgrading, and trying to find answers from history.

There's nothing new under the sun, and consumption upgrading is no new trend either.

The convenience stores now vying for prime street-corner real estate in China, the vibrant home goods sector, the coffee entrepreneurship that periodically makes waves, and the "flexible supply chain" that's becoming a buzzword — all of these happened in Japan during the 1970s and 1980s.

Accompanying waves of consumption upgrading is typically the rise of local consumer goods companies. In 1972, Japan's 100-yen shop chain Daiso was founded. That same year, Tokyo got its first FamilyMart convenience store. Two years later, Tokyo opened its first 7-Eleven. In 1980, the Japanese coffee chain Doutor opened in Tokyo; it has since grown into Japan's second-largest coffee chain after Starbucks. During the 1980s, IKEA swept through multiple countries, yet in Japan it lost to the local home goods brand Nitori. Meanwhile, the consumption-upgrading super-species Muji and Uniqlo were born in 1980 and 1984 respectively.

FreeS Fund remains bullish on investment opportunities in consumption upgrading. Our study of Japan's consumption trends from 40 years ago isn't about copying cat or following blindly — it's about abstracting the underlying logic: consumption upgrading doesn't mean expensive; the biggest opportunity in consumption upgrading is localization; "value for money" is a replicable model; good brands satisfy users' emotional needs... We hope this brings some insight.

We welcome your thoughts at the end of this article. The reader whose comment is most thoughtful and resonates most with the report's author will receive a brand-new copy of Downward Mobility Society — the only one FreeS Fund's mascot could find after scouring the entire internet. The book depicts Japanese society from the 1990s onward. One interesting phenomenon: after consumption upgrading, Japanese people didn't all buy expensive things. Society is stratified, and we've always found it difficult to capture a country's consumption trends with a single term, whether that's "consumption upgrading" or "consumption downgrading." This book may help us understand China's current consumption development trends.

Lessons from Japan's 1970s–1980s Consumption Upgrading for China Today

By Huang Hai (hai@freesvc.com)

01

Why Benchmark Against Japan?

Globally, internet entrepreneurship and investment are phenomena of roughly the last 20 years; consumption upgrading is far older. It has existed for 40 years or more.

The consumption upgrading that China is currently experiencing, treated as something novel, has already happened in countries like the US and Japan. Both Japan and the US were populous nations and manufacturing powerhouses before becoming consumption powerhouses. From a micro perspective, when economies develop to similar levels, similar companies emerge. This is the significance of studying how consumption upgrading unfolded in other countries.

In this report, we summarize and analyze Japan's consumption upgrading during the 1970s and 1980s, hoping to offer some insight for today's consumption upgrading.

Why choose Japan over the US?

Compared to the US, China shares more similarities with Japan in terms of the causes and development process of consumption upgrading.

The urban structures of China and Japan are alike: many cars, narrow roads, and dense concentrations of restaurants and commercial spaces, creating opportunities for consumption-related business models. The US is vast and sparsely populated; driving is convenient, and commercial density is insufficient.

Lifestyles and consumption habits between China and Japan also show similarities. Take FreeS Fund's portfolio company Guancha Tea, a matcha brand, as an example. Matcha originated in China, spread to Japan, and is now trending again in China.

Beyond cultural and geographic similarities, China and Japan also share similarities in economic development trends.

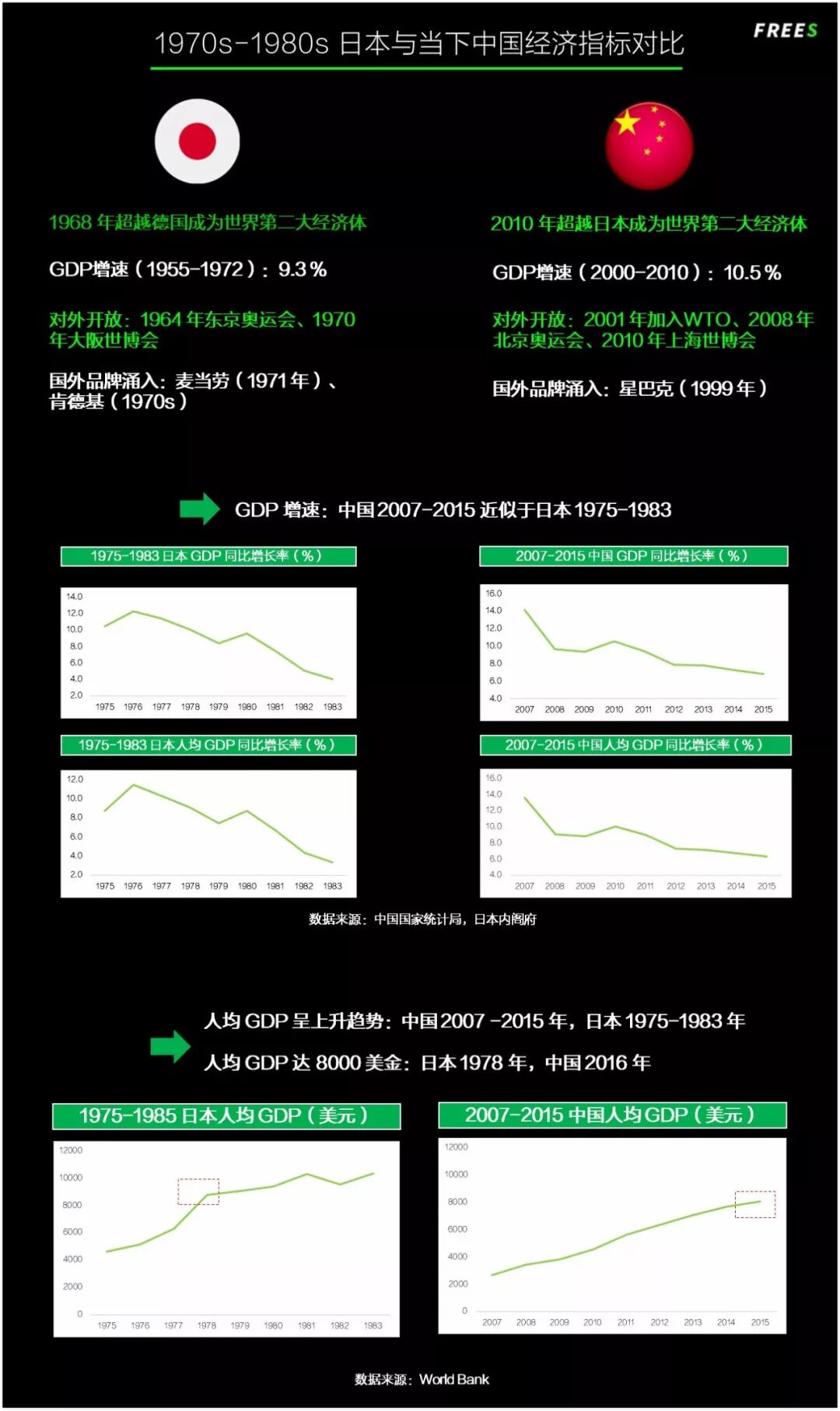

Both countries experienced sustained high-speed economic growth for over a decade, with GDP compound growth rates around 10%. Japan entered its high-growth period in the 1950s, and after surpassing Germany in 1968, it held steady as the world's second-largest GDP until 2010, when China overtook Japan.

As GDP grew, Japan and China successively hosted the Tokyo Olympics, Osaka Expo, Beijing Olympics, and Shanghai Expo, actively integrating into the global system. Opening up also meant that many foreign brands rapidly flooded into Japan and China; domestic consumer brands in both countries faced global competition, and consumers bid farewell to eras of material scarcity. By contrast, the US experienced virtually no "invasion" of foreign brands during its consumption upgrading.

After more than a decade of economic development, both countries transitioned from high-speed to medium-speed growth.

Japan's turning point from high-speed to medium-speed growth came in 1975. The 1974 oil crisis caused Japan's economy to contract that year. From 1974 to 1990, Japan's annualized growth rate fell from around 10% to roughly 5%. China, after 2012, entered the "new normal," with GDP growth rates around 6–7%. China's current growth rate resembles Japan's between 1975 and 1985.

It is when the economy enters a medium-speed phase that consumption upgrading truly begins. Moving from scarcity to possession isn't consumption upgrading — it's just "I've finally eaten my fill," "I've finally used something good." After material abundance, consumers go from being dazzled to becoming "unfazed by change," losing their freshness for many things. Consumption aesthetics need upgrading, and spending structures need optimization.

Most Japanese consumer goods companies we know today were founded between 1970 and 1980. In 1972, FamilyMart, Daiso, and Nitori were established. In 1974, Tokyo opened its first 7-Eleven. Muji was founded in 1980. Uniqlo was founded in 1984.

Per-capita GDP is an economic indicator we often discuss in the context of consumption upgrading. Once per-capita GDP reaches $8,000, many remarkable changes occur in the business landscape.

Japan reached roughly $8,000 per-capita GDP around 1978; China did so in 2016. In the late 1970s, consumption accounted for roughly 55–60% of Japan's GDP; in China today, it's around 35–40%, indicating that our consumption demand has not yet been fully unleashed.

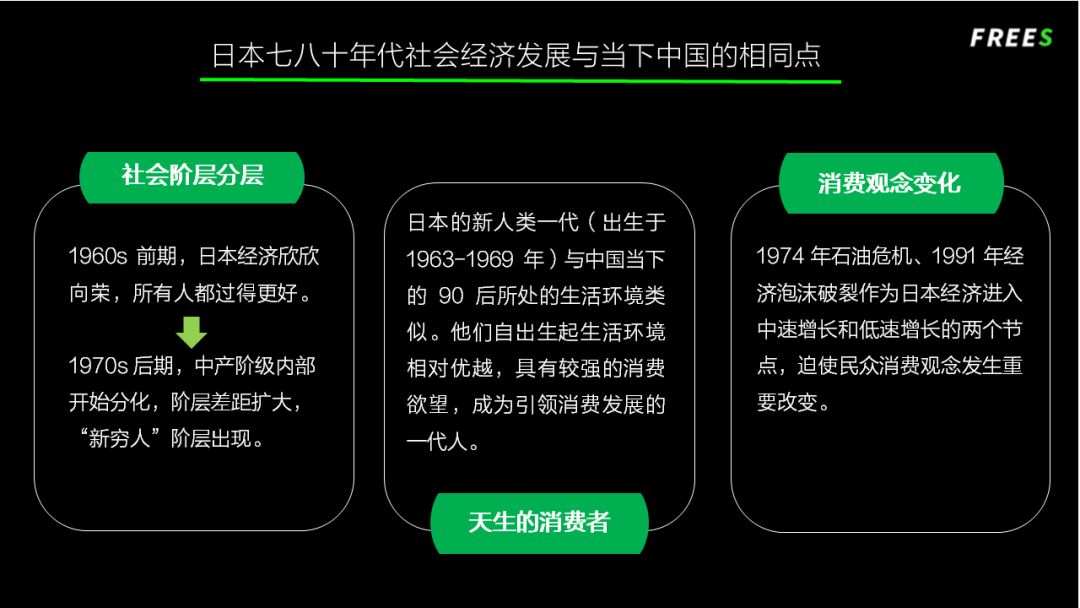

In a high-speed, thriving society, public consumption preferences are relatively uniform. After economic growth slows, class gaps widen and demands begin to diverge. Some people consume low-priced products; others buy luxury goods. Consumers' geographic distribution and needs become increasingly diverse.

For example, Japan's best-selling instant noodles fell into two categories: the first was premium noodles priced above 700 yen (about 42 RMB), sold to health-conscious users. The other was noodles priced below 300 yen (about 18 RMB), sold to those below the middle class. These two product types target different needs and different demographics, and both can make money.

It's hard to sum up Japanese consumers of that era or Chinese consumers today in a few words, but what's interesting is that Japanese youth of the 1970s–1980s closely resemble China's post-90s generation. They were born during the middle period of their country's high-speed economic growth, and their living environments were relatively comfortable from birth. Consequently, they have stronger consumption desires, are bolder in spending, and pursue personalization more intensely.

A question to consider: In the process of social stratification, which has more potential to scale — companies pursuing the affordable-luxury route, or those focused on being cheap?

FreeS Fund Perspective (freesvc)

Based on observations of Japan's consumer goods industry and Japanese society, we have summarized four patterns regarding Japan's consumption upgrading:

- First, localization. Japanese society was deeply influenced by the West, yet from the 1970s onward, a large number of local brands emerged, defeating international giants in competition and becoming household names.

- Second, individualization. Japan's unit of consumption shifted from the household to the individual; consumption style shifted from pursuing conformity to expressing the self; convenience stores rose.

- Third, "better and cheaper." Consumers' judgment of product value and price strengthened; supply chain efficiency gains shortened retail channels; consumer goods delivered higher value for money.

- Fourth, consumers' psychological and emotional needs gradually became the dominant force in social consumption. This manifested in consumers pursuing "small but certain happiness": by the early 1970s, large-ticket items like home appliances had largely become widespread, and products gradually trended toward miniaturization; consumers craved instant gratification at small prices. Additionally, products' spiritual attributes strengthened: consumers began valuing the spiritual satisfaction brought by products' added value.

02

The Biggest Opportunity in Consumption Upgrading Is Localization

Accompanying waves of consumption upgrading is typically the rise of local consumer goods companies.

Both China and Japan have experienced phases where foreign brands flooded their domestic markets. Over the past decade, brands like Pizza Hut, KFC, McDonald's, and Unilever enjoyed rapid growth in China. In recent years, the growth of foreign brands has slowed while local consumer goods companies have begun to stand out. It's a zero-sum shift.

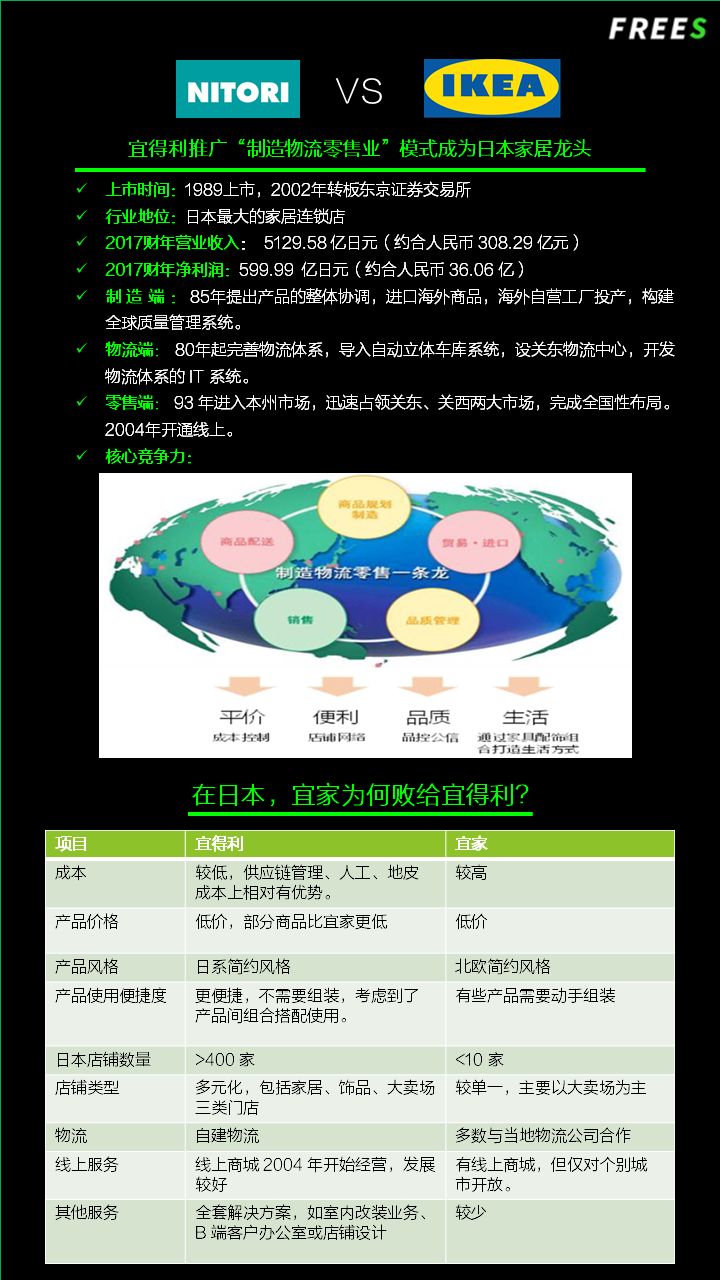

Japan offers a classic case of a local company defeating an international giant. IKEA entered Japan in 1974 but gradually lost ground to the domestic brand NITORI because its products didn't fit Japanese market needs. In 1986, IKEA withdrew from Japan and didn't return until 2006.

The core reason for IKEA's failure in Japan was the strong local characteristics of Japan's home furnishings industry.

From a sales channel perspective, most Japanese furniture stores are small-format because of the compact urban layout and limited land resources. NITORI's Shanghai locations, for instance, sit in inconspicuous corners of shopping malls — about four or five stories, 500–1,000 square meters. In Europe and America, IKEA operates megastores of tens of thousands of square meters; the large format extends customers' shopping time, with food service alone accounting for roughly 10% of IKEA's sales.

IKEA's big-box retail model has deep historical roots, making it unlikely to fundamentally transform this format for any single overseas market — leaving an opening for competitors.

Moreover, from supply chain management and production efficiency perspectives, Japanese furniture companies' production costs were far lower than overseas competitors. Once, Japan's traditional handmade production model lagged behind IKEA in supply chain management, but Japanese furniture companies adopted IKEA's supply chain methods, reduced costs, and gained price advantages.

From a product style perspective, while both IKEA and NITORI belong to the minimalist category, Nordic minimalism tends toward deep blues and grays, whereas Japanese style centers on wood tones.

Based on how NITORI defeated IKEA, local companies can find opportunities in sales channels, supply chain management, and product style.

Will IKEA face the same fate in China?

Twenty years ago, when IKEA entered China, the country's local production capacity, entrepreneurial teams, and capital landscape weren't sufficient to build a company capable of challenging IKEA. Now that IKEA has been rooted in China for 20 years, the likelihood of being defeated is even smaller.

However, China's furniture market has volume of at least one trillion RMB. IKEA's 2017 China sales were 13.2 billion RMB, only about 1% of the furniture market. So local companies still have large remaining market segments to capture.

Beyond furniture, China has highly localized categories like dumplings, roujiamo (meat sandwiches), rice wine, and tea — especially tea. Based on China's cultural and resource advantages, influential local tea brands may emerge.

Strong consumer brands enjoy longer windows of opportunity than internet trends — which typically last just 3 to 6 months. Investing in livestreaming products or ride-hailing apps now is largely too late; the battle is over. But in consumer goods, there may still be a 5–10 year window.

Japan has already passed its consumption upgrading window, yet companies born during that period remain enormously influential and continue growing rapidly — their upside remains very high.

FreeS Fund Perspective (freesvc)

- The biggest opportunity in consumption upgrading is localization. Japan experienced the rise of local brands in the 1970s–80s, and we believe China will see the same — and that time window is now.

03

Targeting the Single Person's Wallet

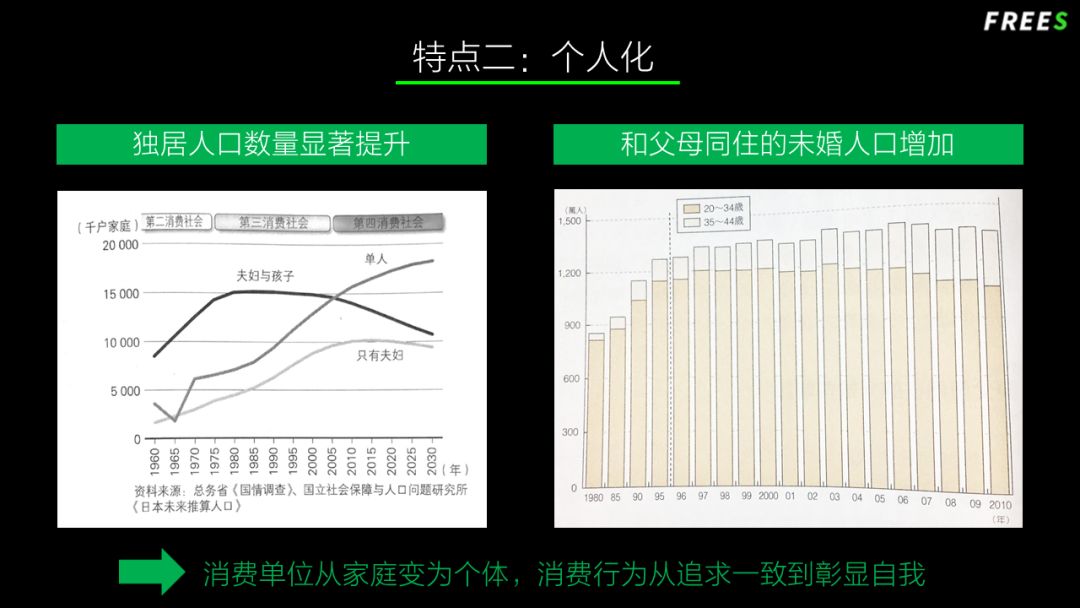

The second lesson from Japan's consumption upgrading is individualization.

From the 1970s onward, Japan's societal trend toward individualization grew increasingly pronounced. Of Japan's 100 million people, nearly 20 million live alone. The accelerating pace of social life has spawned small-quantity, high-frequency individualized consumption behaviors.

This individualization trend has driven the birth and growth of many new consumer companies. The first manifestation is the rise of convenience stores.

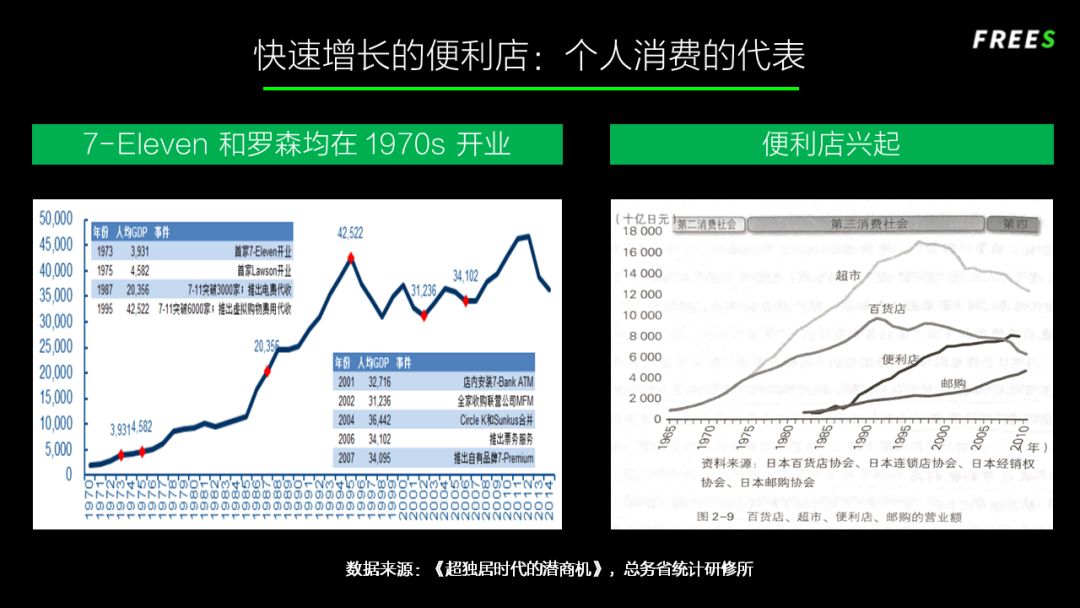

In the early 1970s, Japan imported the convenience store model from the US, and the format rapidly took off, led by the local brand FamilyMart (1972) and the American brand 7-Eleven (1974).

In Japan, convenience stores went from emerging in the 1970s to becoming a core retail format in just over 20 years. Today, convenience store retail sales account for roughly 10% of Japan's retail market — close to the proportion that e-commerce represents of total retail in China.

A key reason convenience stores have achieved such status in Japan is that, compared to supermarkets which primarily sell to families, convenience stores serve individuals. People are accustomed to buying small amounts, multiple times.

Beyond the individualization angle, data shows that Japan's convenience store boom from 1973 to 1995 tracked closely with per capita GDP growth. In 1973, the first 7-Eleven opened. In 1987, when Japan's per capita GDP was around $20,000, 7-Eleven surpassed 3,000 stores. In 1995, when Japan's per capita GDP peaked at around $40,000, 7-Eleven broke through 6,000 stores.

The second manifestation of individualization is the massive popularity of vending machines. Vending machines in Japan's 1970s consumption upgrade played a role equivalent to food delivery in China today — both satisfy consumers' need for quick meals.

Japan's vending machine explosion began with the 1970 Osaka Expo. That year, expo attendance hit 64.22 million, breaking the all-time record. The vending machines throughout the venue were instrumental in meeting the food needs of this enormous crowd. At the time, all of Japan had only 1 million vending machines. By 1975, this number reached 3 million. Growth continued until 1990, when the count hit 5 million and the growth rate flattened. With roughly 100 million people in Japan, that's about one vending machine per 20 people.

Which raises the question: If one vending machine per 20 people is a reasonable density, then with China's 1.3 billion people, shouldn't there be over 50 million vending machines? Japan's convenience stores started in 1973; China's current economic development has certain similarities with Japan's 1970s–80s. How high is the ceiling for convenience stores in China?

FreeS Fund Perspective (freesvc)

- Convenience stores, as a retail format serving the small-quantity, high-frequency consumption pattern of individuals, definitely have room in China. But China's convenience stores and vending machines will most likely not become as high-density a format as in Japan.

- One reason is that China's internet influence on commerce is too strong. If you open a 5,000-square-meter O2O fresh grocery store guaranteeing 30-minute delivery within 3 kilometers, it can basically substitute for convenience stores and vending machines.

- Additionally, the trend toward individualized consumption will profoundly affect the restaurant industry.

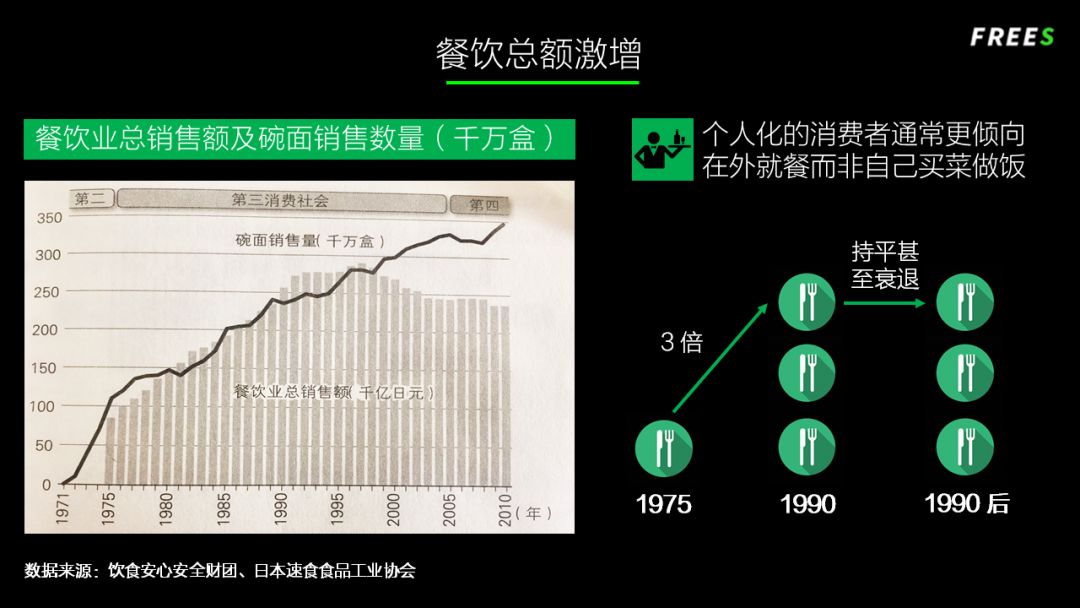

Today, Japan's largest restaurant company is 7-Eleven, which buys countless bento boxes in Japan — doing food service alongside convenience retail. In 1975, Japan's restaurant industry market cap was less than 10 trillion yen; by around 1990 it neared 30 trillion yen, a threefold increase. After Japan's economic bubble burst, the restaurant industry entered a plateau period.

In 2017, Japan's restaurant industry market size was around 25 trillion yen, close to 1.5 trillion RMB. China's population is 13 to 15 times Japan's, yet its restaurant industry market size is roughly 3 trillion RMB — only twice Japan's.

FreeS Fund Perspective (freesvc)

- From a macro perspective, China is very likely to produce excellent restaurant companies in the next 10 to 15 years.

- However, macro optimism coexists with micro difficulties; restaurant entrepreneurship requires tremendous patience. It is fundamentally a service industry, and the journey from zero to $10 billion is extraordinarily difficult.

04

Better and Cheaper: How Is That Possible?

The third major trend in Japan's consumption upgrading is "better and cheaper." Consumers developed stronger judgment about product value and price, supply chain efficiency improvements shortened retail chains, and cost-performance ratios increased.

The essence of consumption upgrading is selling better things more cheaply, not more expensively. "Cheaper" means lower than — or at least within — our expected price range. For example, consumers might have originally spent 20% of their budget on food, but now spend only 15% while enjoying better quality.

There are already quite a few "better and cheaper" products in China. MINISO has a hit product — a coin purse priced at 9.9 yuan. "90 Points" uses materials of the same quality as the American brand Samsonite, but at a much lower price. HEYTEA offers drinks made with fresh fruit and brewed tea, priced lower than beverages sold by foreign coffee chains.

During Japan's consumption upgrade, low-price, high-quality brands represented by Daiso and Muji began emerging in the 1980s, and continued to rise against the tide after the economic bubble burst in the 1990s.

Another typical brand that fits the "better and more affordable" mold is Uniqlo.

The key to Uniqlo's control over quality and price lies in its use of the SPA (Specialty Retailer of Private Label Apparel) model, which vertically integrates product planning, manufacturing, and retail to maximize offline retail efficiency. In the SPA model, the brand controls the entire production process from end to end — from upstream raw material sourcing and quality control to downstream sales, inventory management, e-commerce, and customer service.

The SPA model is efficient, but complex to build. Brands like Uniqlo, IKEA, ZARA, NetEase Yanxuan, and Xiaomi all operate under this model. Let's analyze its characteristics:

First, in the SPA model, the supply chain extends all the way to material manufacturers. Uniqlo's classic Heattech line, which keeps wearers warm, represents the kind of raw material innovation that only an end-to-end company can achieve. Xiaomi also controls product components to support the development of its entire product ecosystem.

Second, SPA brands rarely advertise. For end-to-end retailers like IKEA, ZARA, and Uniqlo, their stores themselves are advertisements. With low marketing costs, brands can return more profits to consumers, creating a positive cycle.

Third, data flows through the entire chain in the SPA model. Sales data from a ZARA store might reach headquarters in Spain the very next day. When a retail brand can connect the entire production and information chain, inventory management — one of retail's core challenges — becomes readily solvable.

The SPA model provides consumers with quality products at controllable prices, generating high consumer surplus (also called net consumer benefit, defined as willingness to pay minus actual payment).

The SPA model produces remarkable results in home goods and apparel, but success is difficult. Once achieved, it might even make you the richest person in your country. Uniqlo founder Tadashi Yanai has topped Japan's rich list multiple times, and for a long time Europe's richest person was ZARA's founder.

SPA brands have remarkable staying power. People joke about "million-yan salary, still wearing Uniqlo" — even as consumers' incomes rise, they continue choosing the brand.

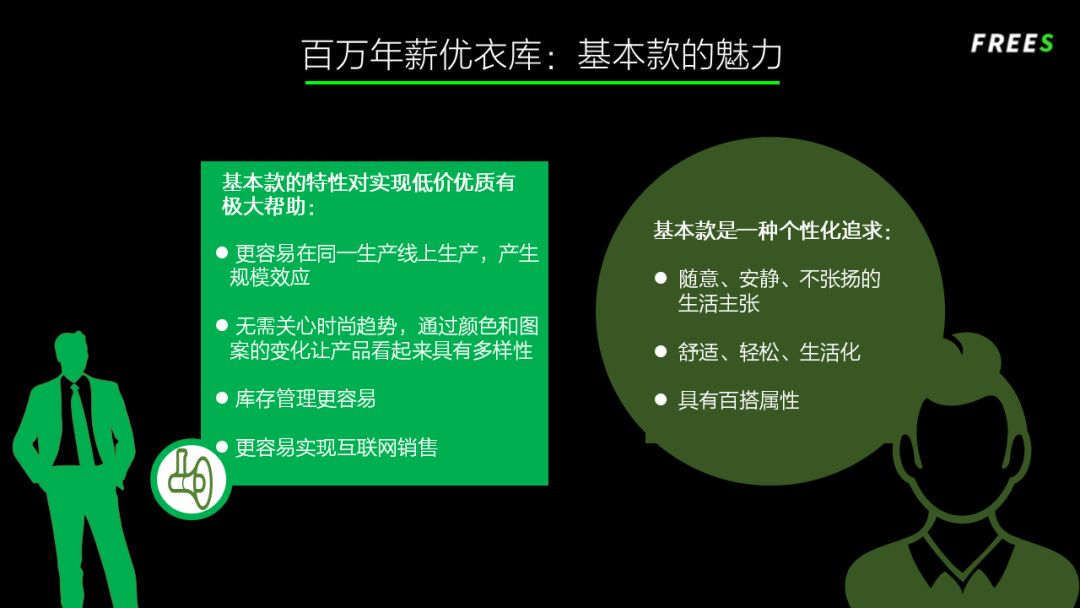

Beyond the SPA model, the basic-goods positioning also helped Uniqlo achieve "better and cheaper" while improving commercial efficiency.

Basic styles allow a single SKU to achieve higher sales volume, making economies of scale easier to attain. This gives brands greater bargaining power with suppliers and simplifies inventory management. Additionally, basic styles lend themselves to online purchases because they are universally fitting, consistently quality, minimally tied to fashion trends, versatile, and don't require trying on. This partly explains why Uniqlo's sales on Tmall far exceed ZARA's.

In China, very few companies can execute the SPA model. Many Chinese consumer brands are "dealer brands" — they collect money from dealers rather than directly from consumers, meaning their real customers are the dealers. With poor information feedback, brands cannot quickly respond to consumer demand when managing SKUs. In the SPA model, there is no dealer role.

Another model is the "Red Star Macalline model." As a retail terminal, it collects rent from brands for floor space but does not directly control products. Simply put, products pass through multiple intermediaries from production to consumer — spending tens of thousands of yuan on a bed is common. Red Star Macalline is profitable and viable as a business model, but it does not maximize efficiency.

FreeS Fund Perspective (freesvc)

- Founded in the early 1980s, Uniqlo is the archetype of quality at low prices. At its founding, Japan's per capita GDP was roughly $20,000 — about double China's current level. But China's consumption upgrade is accelerated by mobile internet, so the rise of Chinese consumer goods companies will come faster than Japan's.

05

"Value for money" is a replicable model

Good brands satisfy users' emotional needs

Japan's fourth important trend in consumption upgrading is the emphasis on satisfying consumers' psychological and emotional needs. This is easy to understand. As many people recognize, brand value is essentially emotional added value.

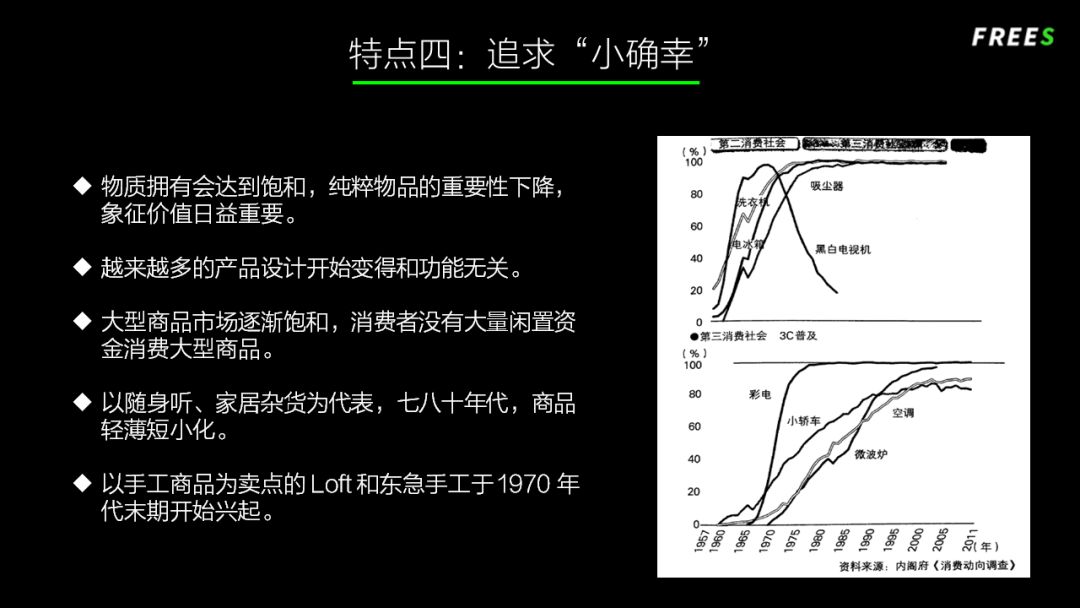

By the early 1970s, large appliances like televisions, washing machines, refrigerators, and air conditioners had already become widespread in Japan. When material abundance becomes excessive, the importance of purely functional products declines, and consumers gravitate toward smaller products or those with stronger spiritual attributes. China is currently at this stage.

Consumers crave products that bring joy at small prices, pursuing "small but certain happiness" (shōkichi), valuing the spiritual satisfaction that comes from a product's added value.

If we analyze basic styles through the lens of psychological and emotional needs, the reason they possess such vitality during consumption upgrading is that basic styles represent a life philosophy — expressing universal attitudes or values: casual, understated, quiet, not self-important. This resonates easily with white-collar workers and the moderately highly educated.

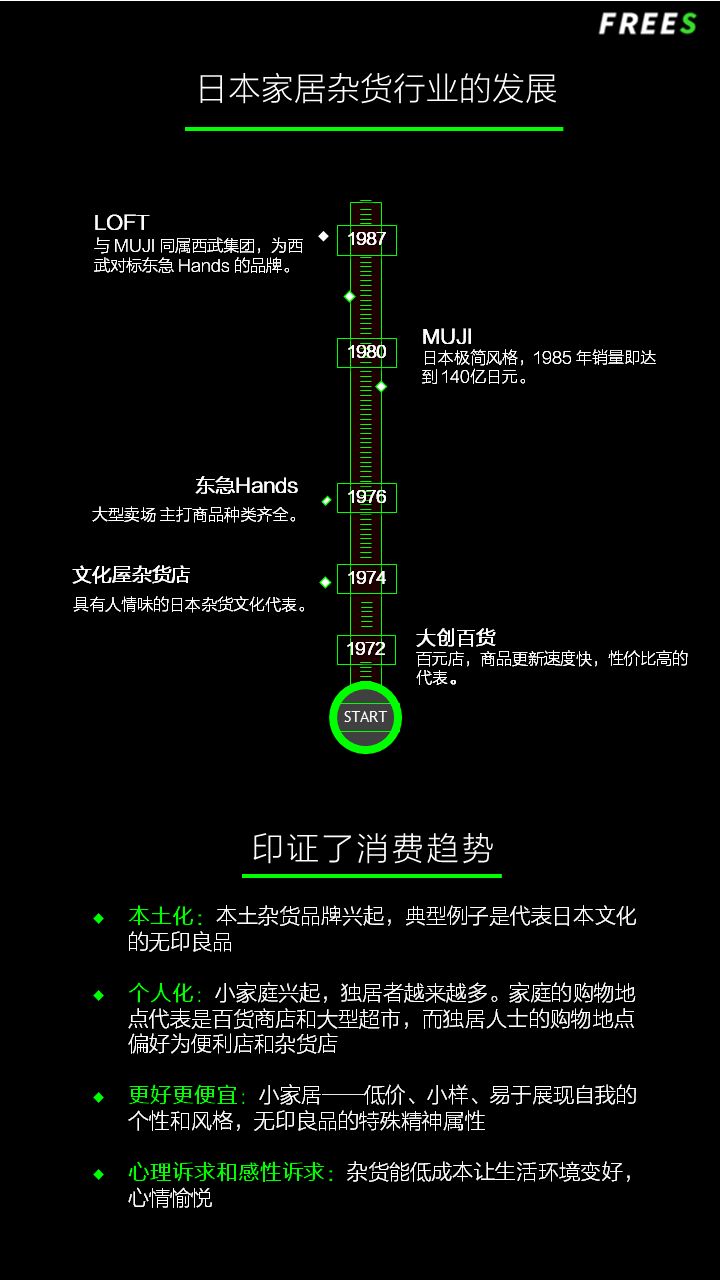

The fastest-growing category in Japan's consumer sector during the 1970s and 1980s was home goods and general merchandise, which grew roughly tenfold over a decade. Muji, Daiso, and Tokyu Hands all belong to this category. Home goods are low-priced, don't take up space, and deliver the kind of "small but certain happiness" that satisfies consumers psychologically. A small picture frame, a bouquet of flowers — these make a home warm and tasteful.

Beyond "small but certain happiness," consumers have other psychological needs. A product's brand positioning is closely tied to consumer psychology. For example, Three Squirrels' category positioning is nuts, with an emotional positioning of cute and adorable. Jiang Xiaobai's category positioning is baijiu, with an emotional positioning of "life is simple."

Endless personalization and self-expression represent one emotional positioning. For instance, everyone wears Nike, but I wear PARTICLE FEVER to show my individuality and style. But what is my individuality? What products can express the self? These are fundamentally sociological or philosophical questions — not necessarily answerable through consumer purchases — yet many people attempt to find answers through consumption.

Second, consumers pursue timeless brands. Many luxury brands have histories spanning centuries, creating a sense of eternal nobility. Consumers are drawn to the timelessness of premium brands, which explains the frequent "retro" and "nostalgia" trends.

Additionally, consumers feel anxiety and have a psychological need for self-improvement. Purchasing fitness courses and using knowledge-payment platforms are two typical consumption behaviors aimed at alleviating this anxiety.

Consumers have many psychological needs. A product doesn't need to satisfy all of them, but it must hit at least one to develop sustainably.

It's worth noting that "value for money" is not a psychological need but a model — one that any brand can replicate. However, if a consumer brand suddenly shifts from "value for money" to satisfying a specific psychological need, it may alienate consumers who don't share that need. Still, no positioning choice can influence everyone.

So as a brand's user base grows, it may actually find itself in a weaker position regarding branding, hesitant to define its emotional calling or specify which psychological needs it aims to satisfy. But new brands like "Nagu" can boldly choose to serve loyal users, maximizing word-of-mouth spread.

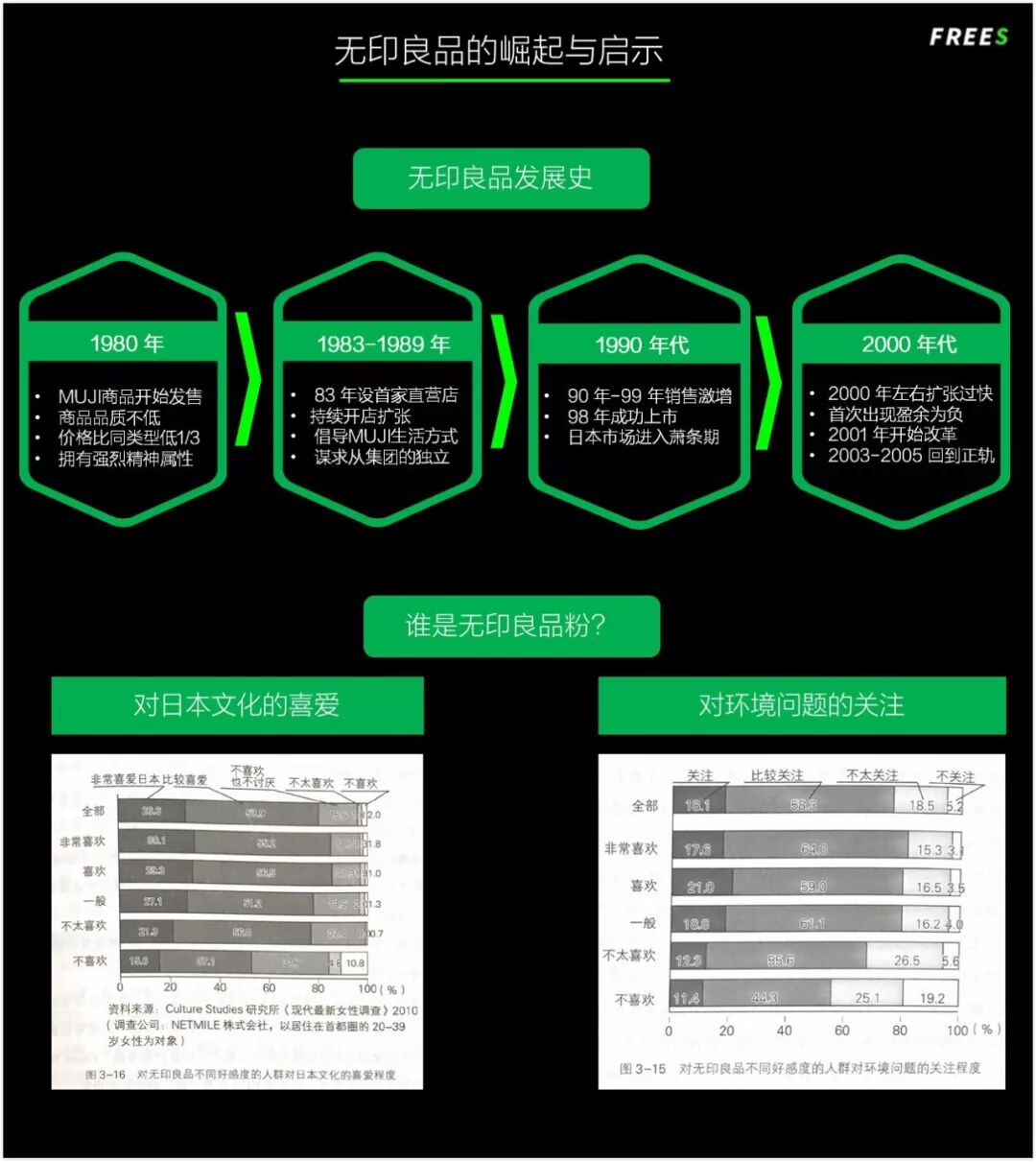

Muji is an excellent brand at satisfying consumers' psychological and emotional needs. What is its emotional calling?

First, environmental consciousness. Consumers who love Muji appreciate the beauty of returning to simplicity and dislike overly industrialized products.

Second, extraction and identification with Japanese culture. Muji successfully distilled core concepts of Japanese Zen culture — such as "nothingness is form," "empty space," and so on — into its brand DNA. It resonates with Japanese consumers' desire for本土化, something difficult for other countries to replicate.

FreeS Fund Perspective (freesvc)

-

Muji's early slogan was "better quality, lower prices," with products priced one-third below comparable alternatives. But in China, it costs more than in Japan because it targets the mid-to-high-end market there — a different positioning from its home market. We need to distinguish between a product's domestic positioning and its overseas positioning.

-

Value for money and emotional resonance together built Muji; neither alone would suffice. Currently, Muji has emotional appeal in China but lacks the value proposition. Domestic brands can find their opening there.

06 Conclusion

Finally, we'll use Japan's home goods and lifestyle retail sector to summarize how its development illustrates the consumption upgrade trend, and what lessons we can draw from it.

In Japan, the home sector posted extremely high compound growth in the 1980s, second only to insurance across all industries. Home goods and lifestyle products grew out of native Japanese culture. They're small, affordable, meet the consumption needs of people living alone, and add flavor to daily life while expressing individuality.

When we analyze historical consumption trends, we're not copying formulas or following blindly. We look back to abstract the underlying logic. Any industry that can grow rapidly for more than a decade during a consumption upgrade must, in some dimension, resonate with a broader societal trend — that's what allows it to develop in sync with society. We hope Japan's consumption upgrade journey can offer us useful reference points.

Bonus for This Issue

We welcome your comments at the end of this article. Share your perspectives and views. The reader whose comment is most thoughtful and resonates most with the report's author will receive Downward Society — the only brand-new copy Feng Xiaorui could find anywhere online. The book depicts Japanese society from the 1990s onward. One interesting phenomenon: after the consumption upgrade, not all Japanese consumers bought expensive things. Society is stratified. It's always difficult to capture an entire country's consumption trend with a single term, whether "consumption upgrade" or "consumption downgrade." This book may help us understand China's current consumption trajectory.

(Feel free to share to your Moments. For republication on other official accounts, websites, or mobile apps, please reply "reprint" to learn our republication rules and contact FreeS Fund for authorization. All rights reserved by FreeS Fund.)

▲ FreeS Report 10: The Secret Shared by Snack Hits That Survived Economic Cycles

▲ FreeS Report 9: How Can Sportswear Brands Achieve Brand Upgrade?

FreeS Report 8: Will the Matcha Industry Produce the Next Starbucks?

FreeS Report 7: Four Major Directions for Health Data Entrepreneurship in China

FreeS Research 6: Keep Has Raised Four Rounds — What's Left in the Abs and Gym Business?

FreeS Report 5: We've Collected So Much Health Data — How Far From Living Our Best Lives?

FreeS Report 4: The SaaS Boom — Opportunities, Logic, and Challenges

FreeS Report 3: Is an Online IKEA Possible? — Home E-Commerce Investment Analysis

FreeS Report 2: China-U.S. Healthcare Investment Outlook

FreeS Research 1: Opportunities and Future of Export Cross-Border E-Commerce