18 Charts That Explain the Shifting Global Supply Chain | FreeS Research Institute

Under US-China competition, the global supply chain is being reshaped.

As the vast network connecting supply and demand across the globe, the shifting dynamics of global supply chains have long been a focal point of attention. They shape the rise and fall of different economies and deeply influence the strategic positioning and growth prospects of companies going global. For a considerable time, China has held a commanding lead in global manufacturing. Yet the interplay of US-China competition, regional conflicts, and other factors has introduced significant volatility into supply chain stability. We wanted to understand: What changes are underway in global supply chains? How will these changes affect China? And for companies "born in China, facing the world," where do opportunities lie, and what challenges must they confront?

To explore these questions, we reviewed data and reports on global supply chains, hoping to map out the broad contours. Our key findings:

- Global supply chains are being restructured — not fully decoupled, but growing more complex and diversified, requiring coordination across more countries.

- The underlying logic of this reshaping is driven less by economics than by great-power competition in the context of US-China rivalry.

- Supply chain diversification is shifting from the former "All-in China" model to "China plus N."

- "Nearshoring" and "friendshoring" are fueling trade growth in countries and regions like Eastern Europe and Mexico. In the Asia-Pacific, foreign direct investment is diversifying, with new hotspots continually emerging.

- Even as direct supply chain links between China and the US diminish, China's supply chain connections with America's major trading partners are increasing. China is, in effect, trading more with the US through third countries.

- Supply chain restructuring is raising the costs of global trade — costs that may translate into consumer inflation or corporate losses.

- For companies going global, embracing internationalization does not mean abandoning the Chinese market.

If you're interested in or building a business around going global, feel free to reach out to Ying Shen, Vice President at FreeS Fund, at shenying@freesvc.com.

The main arguments here also echo discussions from our podcast High Energy. You can find it on Xiaoyuzhou, Apple Podcasts, or Ximalaya — search and subscribe to "高能量."

Giveaway

What do you think about the changes in global supply chains? Leave a comment below. We'll randomly select 5 readers to receive a copy of Marc Levinson's The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger.

/ 01 / What Does the Global Manufacturing Competitive Landscape Look Like?

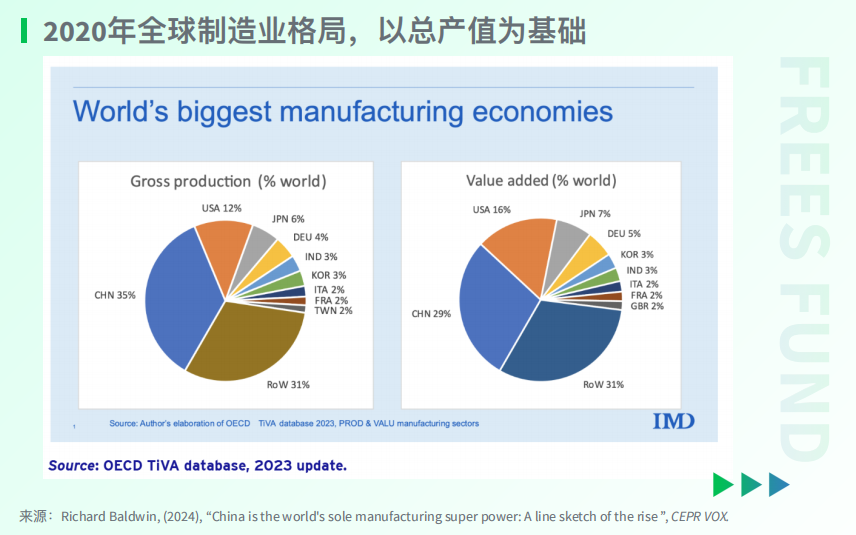

Research by economist Richard Baldwin shows that China holds absolute dominance in global manufacturing output at 35% — roughly triple America's share, six times Japan's, and nine times Germany's. Among the six countries accounting for over 3% of global output, three are legacy industrial powers — the US, Japan, and Germany — while the other three, China, India, and South Korea, are newly industrialized nations.

Meanwhile, in global manufacturing value-added rankings, China claims 29% of the total, about 1.5 times the US, four times Japan, and six times Germany. Whether measured by absolute output or value-added, China's manufacturing lead remains substantial.

/ 02 / The Changing of the "Global Manufacturing King"

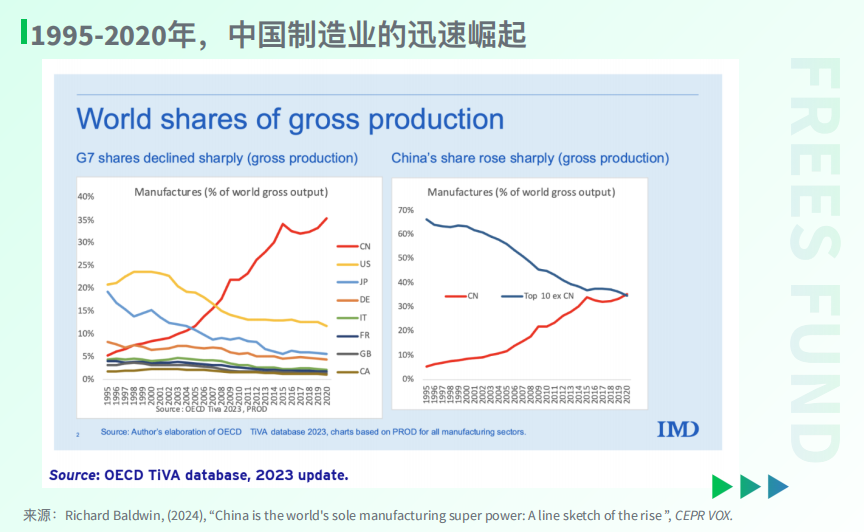

Professor Richard Baldwin's research traces back to 1995. At that time, China's manufacturing strength was comparable to Canada, the UK, France, and Italy. China surpassed Germany in 1998, Japan in 2005, and the US in 2008. Since then, China's share of global manufacturing has increased by more than 10 percentage points, while America's has fallen by roughly 3%.

The last time the "world's top manufacturing nation" changed hands was on the eve of World War I. It took the US nearly a century to displace Britain. China's surpassing of America, by contrast, took just 15–20 years.

/ 03 / China's Manufacturing Growth Slows as the US Pushes for Decoupling

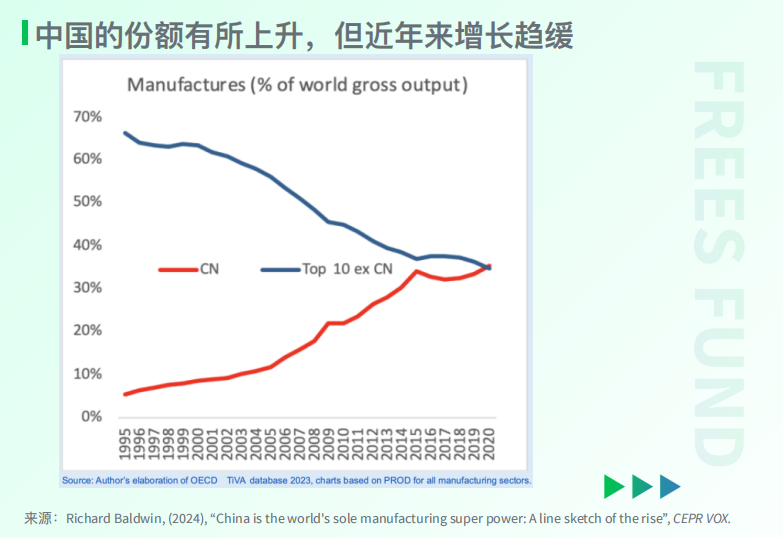

In 2020, China's manufacturing share exceeded the combined total of all other top-ten manufacturing nations. However, China's manufacturing growth has since decelerated, with its global share now fluctuating around one-third. Notably, since the escalation of US-China trade friction in 2018, the US has pushed for supply chain decoupling from China, ushering in an era of global supply chain reshaping.

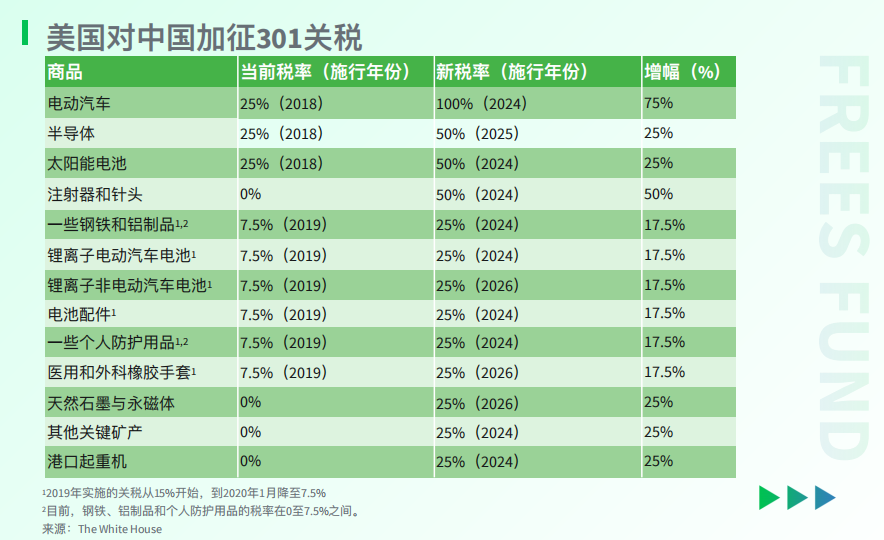

/ 04 / Escalating Tariffs

To strengthen domestic industry protection and reduce dependence on Chinese manufacturing, the US has adopted multiple measures, foremost among them imposing steep tariffs on Chinese goods. Rates range from 7.5% to 25% for products including electric vehicles, semiconductors, electronics, and machinery.

The latest development: On September 27, 2024, the US government announced it would implement punitive tariffs on certain Chinese exports, including a 100% tariff on electric vehicles (a 75 percentage point increase), 50% on semiconductors and solar cells (a 25 point increase), and 50% on select medical devices (a 50 point increase).

/ 05 / Supply Chain Diversification: From "All-in China" to "China plus N"

Driven by geopolitical factors among others, numerous American companies have in recent years sought to diversify their supply chains — establishing production bases across different countries and regions, particularly India, Southeast Asia, and Central and Eastern Europe, to disperse risk and enhance stability.

Take Apple. The company has long maintained extensive supply chain and sales networks in China, and CEO Tim Cook stated in a 2023 interview that "about 95% of Apple's products are still manufactured, assembled in China."

Yet change is underway. According to The Paper, India assembled roughly 14% of iPhones in 2023. JP Morgan analysts, as well as Indian Minister of Commerce and Industry Piyush Goyal, have noted that Apple aims to produce 25% of iPhones in India by 2025.

As Apple expands its presence in India and elsewhere, Southeast Asia has emerged as a major beneficiary of partial supply chain relocation from China. Vietnam currently stands as the preferred destination under companies' "China plus N" strategies; Malaysia is becoming a rising semiconductor hub within ASEAN; and significant smartphone and pharmaceutical supply chains are shifting to India.

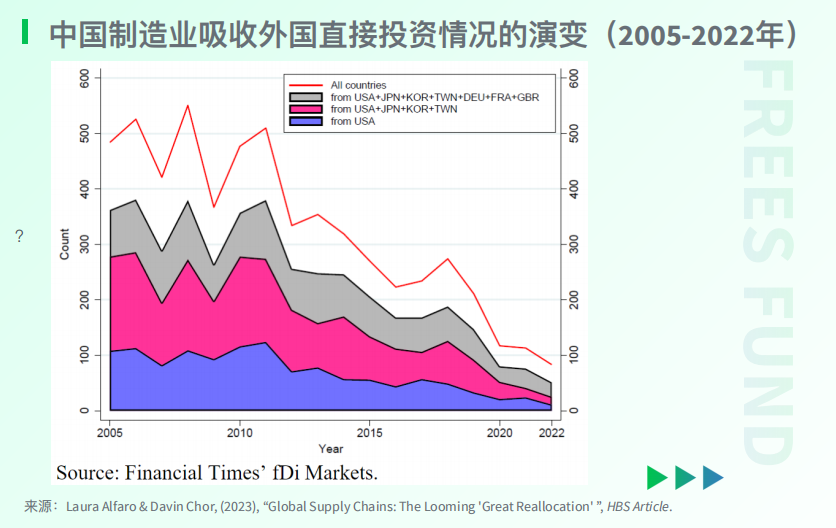

/ 06 / Asia-Pacific FDI Diversification Confirms the "China plus N" Trend

Financial Times data shows that since the end of the global financial crisis, China's greenfield FDI in manufacturing has actually been declining. Meanwhile, in the Asia-Pacific, foreign direct investment is diversifying, with new hotspots continually emerging.

According to UNCTAD data, during 2010–2014, 27.7% of greenfield FDI flowing to the Asia-Pacific went to China, making it the absolute center of regional supply chains at the time. By 2022, this share had dropped to 4.9%. Conversely, Vietnam, Indonesia, India, and others saw their combined greenfield investment absorption jump from 33.7% to 56.7%, with India showing the largest increase, from 10% to 21%. These investments may translate into manufacturing and trade capabilities.

/ 07 / Nearshoring Drives Trade Growth in Eastern Europe and Mexico

Citing a September 21, 2024 article from The Economist titled "Nearshoring Is Turning Eastern Europe Into the New China," as the US and EU restrict imports from China, companies on both sides of the Atlantic are shifting strategies to move production chains to "nearshore" and "friendshore" locations. Nearshoring can shorten supply chains, improve logistics efficiency, reduce transportation costs, and mitigate geopolitical risk.

For instance, the US has made Mexico a key nearshoring base. US Commerce Department data shows that in 2023, Mexico began displacing China as America's largest trading partner. Meanwhile, Central and Eastern Europe is becoming an important nearshoring base for European countries, expected to attract more investment and industrial transfer going forward.

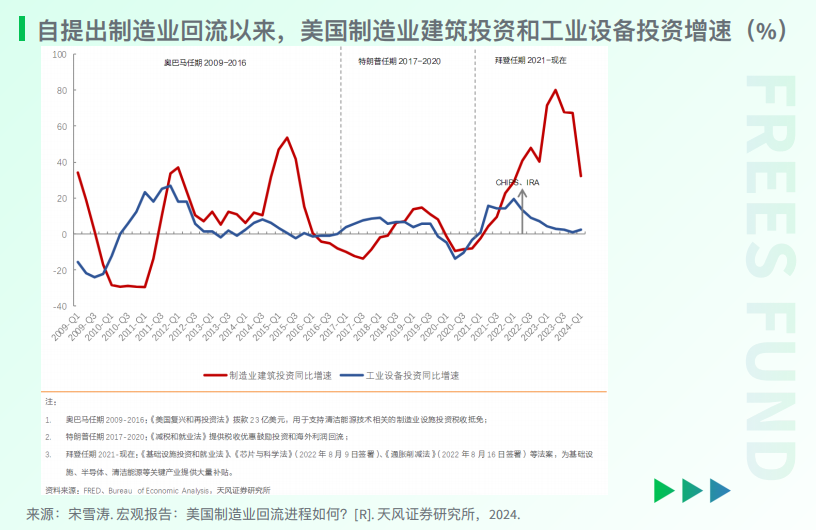

/ 08 / How Effective Is the US-Promoted "Manufacturing Reshoring"?

Since the Obama administration, every US government has made manufacturing return a cornerstone of economic policy. From Obama's reindustrialization and manufacturing revival, to Trump's manufacturing repatriation, to Biden's series of manufacturing renewal policies — all have served the goal of bringing manufacturing back to America.

Yet multiple indicators suggest this push has fallen short of expectations.

First, employment. US Bureau of Labor Statistics data shows that manufacturing employment has trended downward since 2002. After 2008, as the US began emphasizing manufacturing return, employment saw modest recovery. The 2022 legislative packages also produced some rebound. But compared to 2002, America has lost two to three million manufacturing jobs over the past two decades.

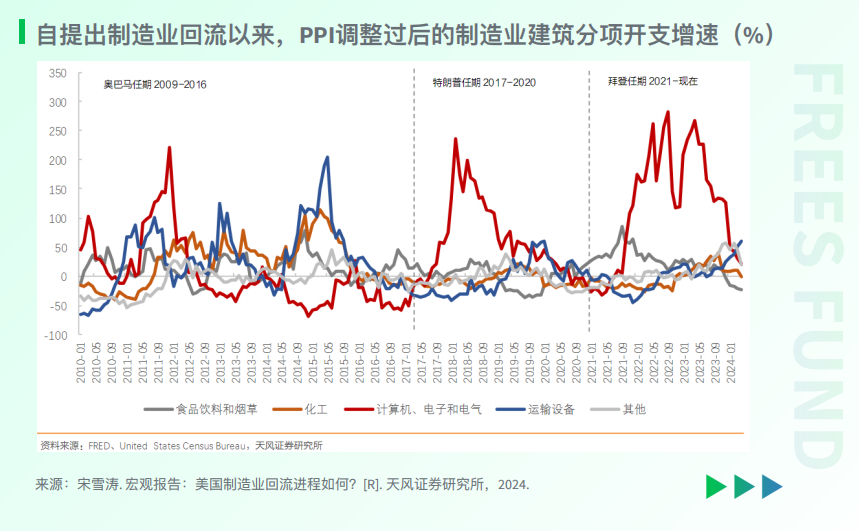

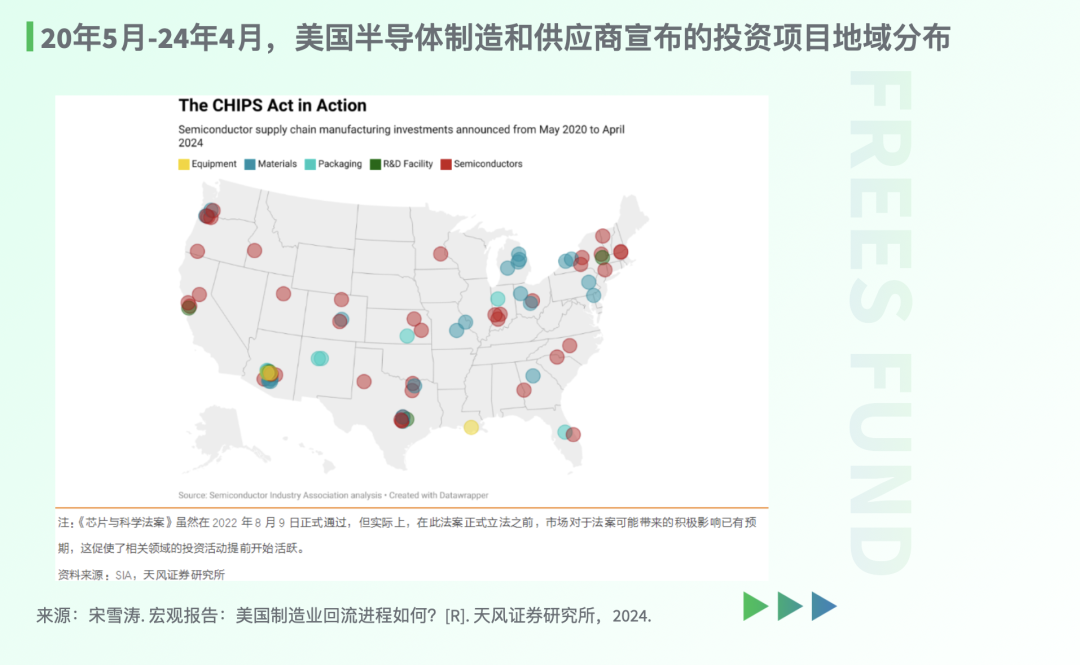

Second, investment. Similar to employment, each new legislative package triggers an investment surge. But as these effects wane, investment falls back. Take the CHIPS and Science Act passed on August 9, 2022. The act spurred rapid growth in construction investment for computers, electronics, and electrical equipment, with growth rates exceeding 200% at peak. However, since 2024, related investment has begun slowing.

According to data from the Semiconductor Industry Association (SIA), as of April 2024, over 80 new semiconductor-related projects had been announced across the US, attracting $447 billion in total investment. These plans focus on building new chip fabrication plants and packaging facilities, as well as expanding existing ones.

Yet the progress and outcomes of these investments remain to be seen, as some past projects have faced delays or indefinite suspension. Take TSMC. Public reports show that since first announcing its US fab plans in May 2020, TSMC has cumulatively announced $65 billion in investment — roughly three years of TSMC's net profit — making it the largest foreign direct investment in American history. Four years on, it wasn't until early September 2024 that TSMC's Arizona facility began small-batch trial production.

09 Supply Chain Links Between China and the US Are Weakening, But Can China Be Circumvented?

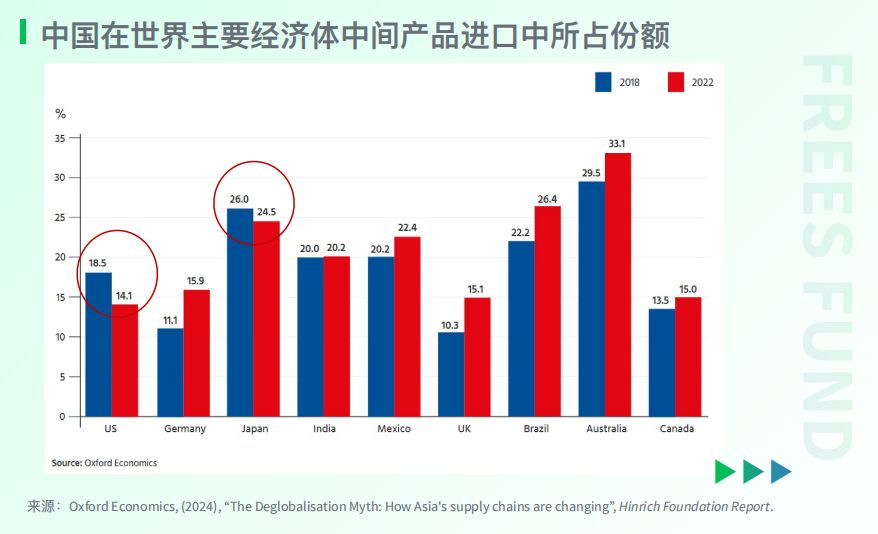

A January 2024 report from Oxford Economics tracked China's share of intermediate goods imports among major world economies. We can see that the proportion of US intermediate imports coming from China fell from 18.5% in 2018 to 14.1% in 2022, and further to 11.4% in the first half of 2023. Japan also showed a slight decline.

However, for other major economies, the share of intermediate imports sourced from China has risen. Among developed economies, Germany, the UK, and Australia show the most pronounced increases. Among emerging economies, China's share of Brazil's intermediate imports rose from 22.2% to 26.4%. To some extent, this indicates that China's position in global supply chains has been maintained.

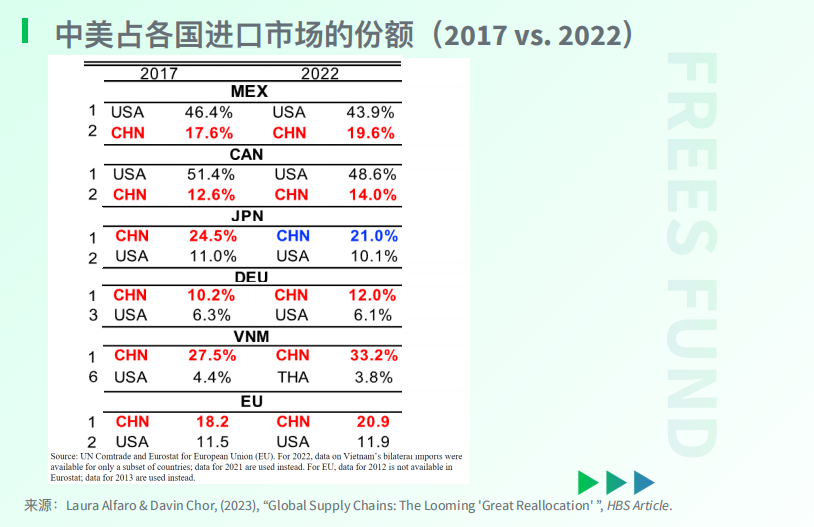

10 China's Supply Chain Is Connecting to the US Through Third Countries

Excluding China, America's main import sources are Mexico, Canada, Japan, Germany, and Vietnam. Among these five, except for Japan, China's share in their import markets has increased, and China is their first or second largest import partner.

This shows that the US has merely reduced its direct dependence on China. A new form of connection is emerging between the two countries — many Chinese companies are using transshipment trade through other regions, or reassembling products in these locations, to access the US market.

More notably, Chinese companies are increasing direct investment in Vietnam, Mexico, and other countries, transferring some production capacity there. This helps China maintain its ultimate market share in the US and globally.

Consider India, often touted as a potential successor to the "world's factory." India's economic development remains heavily dependent on China. According to data from the think tank Global Trade Research Initiative (GTRI), in fiscal year 2024, India's imports from China exceeded $100 billion, and after two years, China once again surpassed the US to become India's largest trading partner.

India imports a diverse range of products from China. Perhaps surprisingly, despite being a globally renowned generic drug producer, India imports substantial quantities of chemicals and pharmaceuticals from China. GTRI data shows that in 2022 alone, India's chemical and pharmaceutical imports totaled $76.94 billion, with China accounting for 26.8%. This is a considerable share, and may explain why some say the true upstream of the global pharmaceutical supply chain isn't India, but China.

From this perspective, global supply chains have merely become more complex, with additional intermediate nodes, rather than experiencing large-scale decoupling.

11 Chinese Supply Chains Going Global

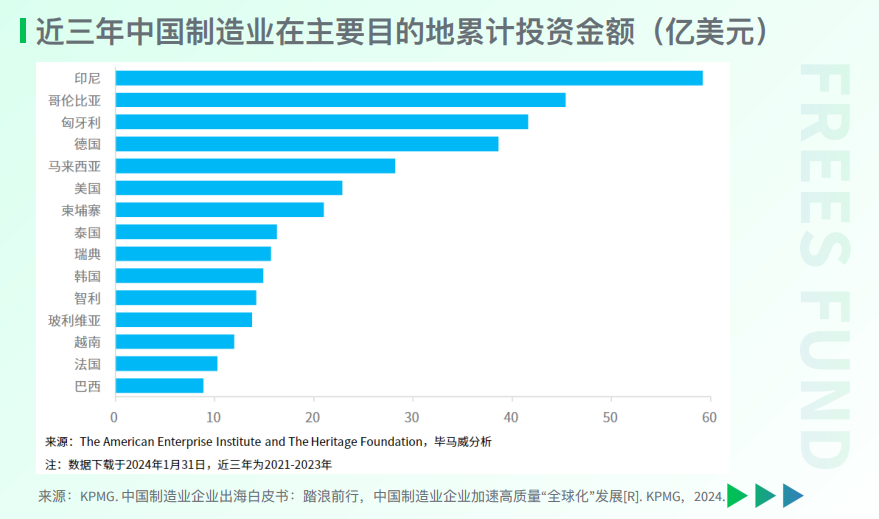

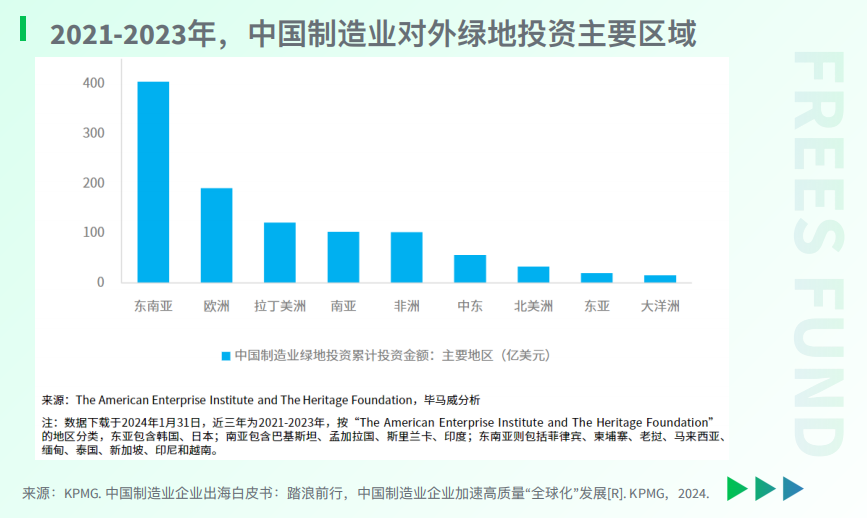

China's outward investment has ranked among the global top three for 11 consecutive years, placing second globally in 2022 and 2023. Through years of accumulation, Chinese companies' supply chain investments worldwide have proliferated, with major manufacturing investment destinations including Indonesia, Colombia, Hungary, Germany, and Malaysia.

The US was once an important destination for Chinese outward investment, but has now fallen out of China's top ten. According to a September 2023 report from Rhodium Group, Chinese FDI to the US has slowed since 2017, with annual investment plummeting from $46 billion in 2016 to under $5 billion in 2022.

12 New Trend in Chinese Outward Investment: Greenfield Investment

According to China's Ministry of Commerce, the total overseas investment announced by Chinese companies is increasing, reaching $163.1 billion in 2022.

Chinese companies are shifting their focus from the US toward markets in Southeast Asia, Europe, and Africa.

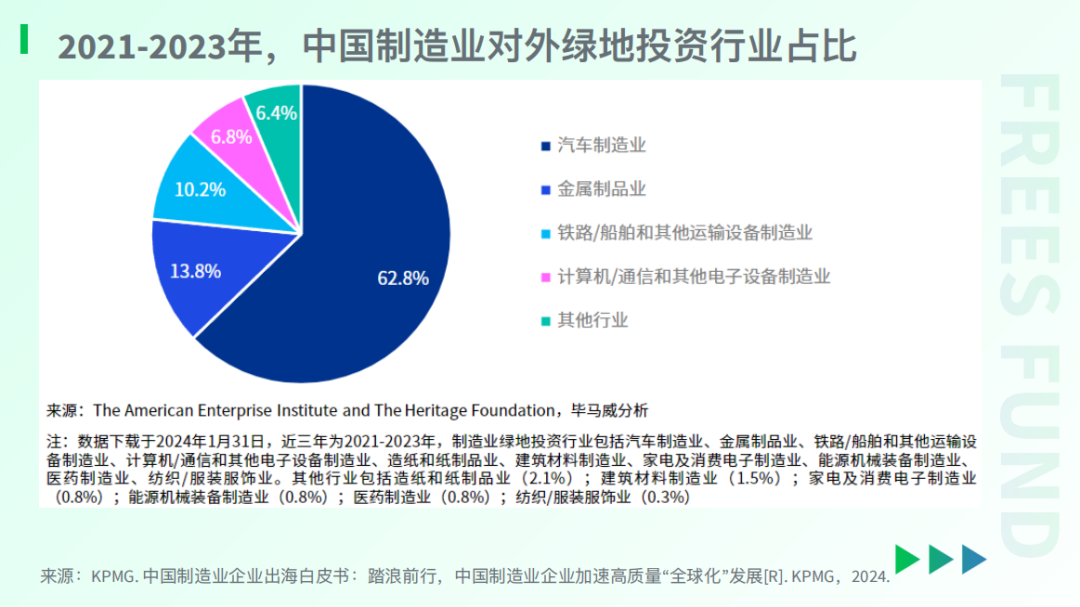

This trend is especially pronounced in China's advantaged industries, such as electric vehicle manufacturing. By establishing factories abroad and operating under their own brands or subsidiaries, Chinese companies can better control production chains and ensure that technology and quality standards remain consistent with their domestic operations.

Summary and Reflections

- Currently, the underlying logic of global supply chain reshaping is driven less by economics than by great-power competition in the context of US-China rivalry.

- Due to geopolitical factors among others, global supply chains are being restructured — not fully decoupled, but growing more complex and diversified, requiring coordination across more countries.

- Globalization remains the overarching trend. Future globalization will involve not just market globalization, but increasingly supply chain globalization.

- China's position in global supply chains remains difficult to shake. Even as direct supply chain links between China and the US diminish, connections with America's major trading partners are increasing. China-US supply chains are becoming more interconnected through third countries. Decoupling in the supply chain realm is unlikely.

- For Chinese-born companies going global, supply chain reshaping means:

- Where companies previously might have managed supply chains within the Yangtze River Delta and Pearl River Delta regions, the rising complexity now demands higher operational management capabilities.

- Supply chain restructuring is increasing global trade costs, which may ultimately translate into consumer inflation or corporate losses.

- Supply chain capability alone is insufficient; it must be converted into brand value and global competitiveness.

- Proactively explore overseas supply chains, but make decisions cautiously, with particular sensitivity to policy environments.

- Embracing going global does not mean abandoning the Chinese market, because strong supply chain foundations + new technology + large market typically yield the highest product iteration efficiency.

As mentioned at the beginning, the main arguments here echo discussions from our podcast High Energy. You can find it on Xiaoyuzhou, Apple Podcasts, or Ximalaya — search and subscribe to "高能量."

Giveaway

What do you think about the changes in global supply chains? Leave a comment below. We'll randomly select 5 readers to receive a copy of Marc Levinson's The Box: How the Shipping Container Made the World Smaller and the World Economy Bigger.

▲ Even as Globalization Slows, Why Is Going Global Still a Must? | Li Feng Column

▲ "Not Going Out, But New Globalization": Thoughts and Practices from Nearly 20 Companies ▲ New Playbooks for Global Entrepreneurs: From "Air Force" to "Marine Corps" | FreeS Research ▲ The Truth About Weight Loss, and Innovation Opportunities | FreeS Report

▲ Embodied Intelligence vs. Sports Tech: One Makes Machines Like Humans, the Other Turns Humans Into Machines? | FreeS Report

▲ Dialogue with Tsinghua Professor Chen Wenguang: What If Large Models Stop Competing on "Large"?

▲ Even Siri Took 14 Years — What's Hard About Voice Intelligence, and Why Is AI Hardware Suddenly Hot? | Dialogue with Chen Xiaoliang of SoundAI

Star the FreeS Fund WeChat Official Account for timely business insights