Tea Drinks 1990–2017: 27 Years of Ups and Downs, and a New Street Story Worth 50 Billion RMB | Frees Fund

The Quest for the Next Starbucks

Two Questions About the Tea Drink Industry

In July, Starbucks — the world's largest coffee chain — acknowledged that selling tea and selling coffee are two different things, shutting down all 379 of its Teavana tea stores. After four years and at least $620 million, Starbucks' foray into the tea business ended in failure.

They shifted their hopes to China instead: Teavana beverages rolled out in Chinese stores last autumn, and in May this year, two ready-to-drink bottled milk teas hit the market. Meanwhile, homegrown Chinese tea drink brands were staging a new street-level movement of their own, with queueing scenes flooding social media feeds.

From the perspective of Huang Hai, VP at FreeS Fund, here are the key issues worth watching in this bustling industry:

▍On one hand, Starbucks is closing its tea stores; on the other, people are asking whether China's tea drink industry will produce the next Starbucks. How did we get here?

Tea drinking has a long history in China, with deep cultural roots. Starbucks' tea products have always faced formidable competition here: from CoCo and Happy Lemon a decade ago, to Gong Cha and A Little Tea five years ago, to HEYTEA and Nayuki today.

The current rise of the tea drink industry is essentially the natural result of consumption upgrading. The first wave of milk tea shops relied heavily on flavoring agents, then shifted to fresh milk, and eventually to fresh-brewed and whole-leaf teas as selling points — tea became healthier, younger, and higher-quality. At around 25 yuan per cup, tea drinks are priced below Starbucks, making them reasonable and more accessible to consumers.

▍What does the rapid expansion of tea drink stores reveal about the category?

Tea is a thirst-quenching beverage, and beverages share one defining trait: high-frequency, rigid demand. Everyone needs to drink something, and they can drink it every day, at any time. We don't buy clothes daily, or eat Western food daily, but every time we visit a shopping mall, we might buy a drink. Beverages are a crucial traffic driver for malls. Compared to other drinks like cola, tea drinks are healthier, with more distinctive characteristics and advantages. For malls and other retail venues, tea drinks are excellent business — which is why new-style tea shops have maintained impressive expansion speed.

This article traces the romantic growth history of the tea drink industry, then calculates incremental demand and replacement demand to arrive at an estimated potential market size of 40–50 billion yuan for new Chinese-style tea drinks. From this, we can glimpse the secrets of the tea drink business.

New Chinese-Style Tea Drinks: A TEA-Flavored New Consumption Trend, Nurturing a "Chinese Starbucks"

Authors / Zhou Yu, Xu Xiaofang

Source / CITIC Securities Research

New Chinese-Style Tea Drinks:

From Powder and Street Corners to the TEA Era

▍A World History of Milk Tea

Milk tea originated in Tibet, China. Tibetans were the first to combine milk and tea. After the Silk Road opened, milk tea spread to India, where locals added spices to suit their palate. During the colonial era, milk tea traveled to the West and evolved into Dutch-style and British-style milk tea.

- Dutch-style milk tea: The Dutch disliked the pungency of Indian milk tea, so they blended different tea varieties to replace the spices and added maple syrup as a sweetener. Dutch milk tea was rich and creamy, winning favor across continental Europe and becoming the prototype and basic formula for modern milk tea.

Taiwanese milk tea is an offshoot of Dutch-style milk tea. During Dutch colonial rule in Taiwan, milk tea was introduced; later, Taiwanese people added "pearls" — tapioca balls made from sweet potato starch and cassava flour that turn dark and translucent when cooked, hence the name. Taiwanese milk tea became known as "bubble tea" or "pearl milk tea."

- British-style milk tea: In 1680, the Duchess of York added fresh milk and sugar to Dutch-style milk tea, creating British-style milk tea. It became a symbol of status, consumed mainly by royalty and the upper class, with elaborate names like Earl Grey, Royal Milk Tea, and Yuanyang Milk Tea.

Hong Kong-style milk tea is an offshoot of British-style milk tea, but more accessible in price, represented by "silk stocking milk tea" and "yuanyang milk tea," gaining popularity alongside the rise of Hong Kong-style cafés. "Silk stocking milk tea" gets its name from the filter, which turns dark with prolonged use and resembles a flesh-colored stocking. "Yuanyang milk tea" blends silk stocking milk tea with coffee, combining the richness of milk tea with the aromatic bitterness of coffee.

▍The Evolution of China's Tea Drink Chains

China's tea drink chain industry has gone through three stages.

Stage One: The Powder Era (1990–1995)

Taiwanese entrepreneurs first introduced powdered milk tea to mainland China, sparking a "milk tea craze." At this stage, shops measured about 3–5 square meters, some existing as small window counters. Products were mixed from various powders — flavors typically included original, strawberry, taro, watermelon, and mango. This milk tea contained neither milk nor tea, representing the elementary phase of mainland China's tea drink chains, known in the industry as the "powder era."

Stage Two: The Street Era (1995–2016)

▲ CoCo is a representative brand that rose during the "tea base" phase.

Ingredients evolved and upgraded, and shops spread across streets and alleys. This stage saw the emergence of the "tea base" — a tea concentrate made from tea dust and tea residue, stored in tea buckets and replaced every few hours. Real tea leaves replaced powder in milk tea, though milk remained mostly powdered. Numerous brands emerged in this phase, such as CoCo and Happy Lemon.

In the later part of this stage, milk underwent some reform: fresh milk appeared. To boost attention, merchants also innovated on form, such as the creation of "cheese foam tea" — whipped cream floated atop pure tea, creating an entirely new form and texture.

Stage Three: The New Chinese-Style Tea Era (2015–present)

With consumption upgrading, milk tea has placed greater emphasis on quality, moving toward "premium tea drinks."

In ingredient selection, it has become healthier. Premium tea leaves, processed through different extraction methods, replace broken leaves and tea residue; fresh milk, imported cream, and natural animal cream replace non-dairy creamer, elevating taste across the board. The category has expanded with various fresh fruits, becoming fruit tea.

In production techniques, it has become more professional. Innovation in extraction equipment and the development of new Chinese-style tea drinks have reinforced each other. Extraction equipment enables standardization of the tea brewing process; traditional handcrafting, by contrast, is constrained by staff training and skill level, making it inefficient and difficult to maintain consistency. Brewing methods have also been refined: beyond traditional hot brewing, cold brewing and vacuum high-pressure extraction have been introduced. Cold brewing, in particular, reduces astringency and decreases tannin release, making it gentler on the stomach.

In store design, it has become more comfortable. Tea shops have generally increased their footprint, expanding from 15–20 square meters to 50–100 square meters. Some chains have moved away from uniform decor, designing unique themes for each location — combining quality products with pleasant environments to provide a comfortable experience.

▍New Attributes: Leisure, Socialization, and Labeling

The thirst-quenching function of milk tea has faded. In its early days, milk tea was popular because it was cheap and refreshing. In summer, a 5–10 yuan iced freshly-made milk tea satisfied consumers' desire for on-the-spot freshness while beating the heat. In winter, a steaming hot milk tea warmed the body.

Against the backdrop of consumption upgrading, new Chinese-style tea drinks have acquired leisure and social attributes. These products satisfy people's pursuit of quality of life; consuming them is itself a process of socializing and relaxing. As tea shop footprints have grown and environments become more pleasant, and as the products themselves have become healthier, tea shops have become a stop in the itinerary of gatherings, shopping trips, and movie outings. Consumers are buying not just a beverage, but also the social and leisure value of a balanced, measured lifestyle.

From tea drink to lifestyle and identity, new Chinese-style tea drinks carry a fashion label; their integration with new media constantly reinforces this labeling. The post-85s and post-90s generations are the core target demographic for new Chinese-style tea drinks. This consumer group has high marginal propensity to consume, values quality of life and lifestyle, and emphasizes individuality. New Chinese-style tea drinks fully satisfy this group's need for bodily identity, giving them label attributes that new media marketing further amplifies.

Robust demand, amplified by new media marketing, has led to buying frenzies and queueing at some new Chinese-style tea shops. When consumers wait over an hour for a cup of milk tea, a sense of pride and accomplishment wells up — a classic case of "small but certain happiness" (xiao que xing). Posting new Chinese-style tea drinks on Moments, Weibo, and other public platforms expresses the joy and excitement of queueing, while also affixing a fashion label to oneself.

Industry Scale:

A New Street Story Worth 40–50 Billion Yuan

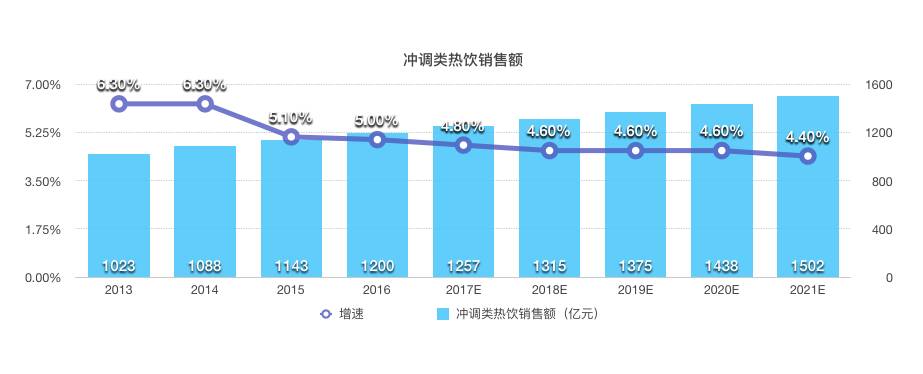

In 2016, China's instant hot drink category (instant coffee, tea, fruit powder, etc.) generated sales of 120 billion yuan, up 5.0% year-on-year; 2021 sales are projected at 150.2 billion yuan, representing a 4.6% CAGR from 2016–2021. Growth has continued to slow from 2013–2021.

▲ Instant Hot Drink Sales (Source: Euromonitor, CITIC Securities Research)

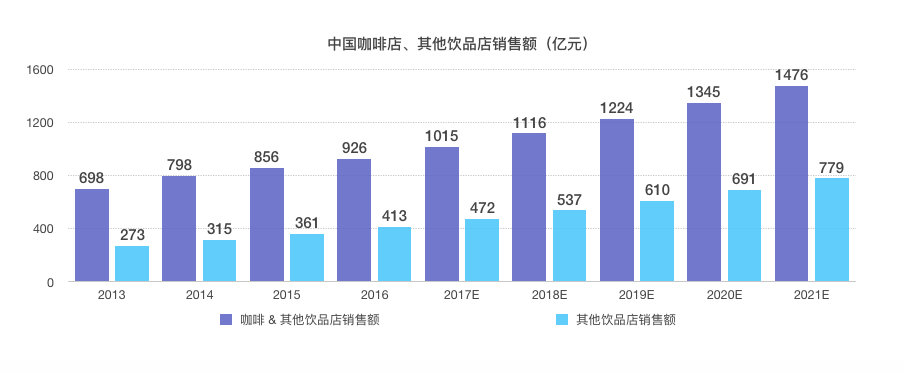

In 2016, coffee and other beverage shops generated combined sales of 92.6 billion yuan, up 8.2% year-on-year; among these, other beverage shops (dessert shops, various bars, traditional milk tea shops, traditional tea houses, new Chinese-style tea shops, etc.) generated sales of 41.3 billion yuan, up 14.5%. By 2021, coffee and other beverage shop sales are projected to reach 147.6 billion yuan, a 9.8% CAGR from 2016–2021; other beverage shop sales are expected to reach 77.9 billion yuan, a 13.5% CAGR.

▲ China Coffee Shop and Other Beverage Shop Sales. Other beverage shop sales are included in "Coffee & Other Beverage Shop Sales" (Source: Euromonitor, CITIC Securities Research)

We believe new Chinese-style tea drink market demand comes partly from replacement demand: replacing traditional milk tea shops, tea houses, and coffee shops; replacing instant hot drinks (instant coffee, brewed tea, fruit powder, etc.); replacing bottled juices and carbonated beverages (Coca-Cola, Sprite, etc.). Another part comes from incremental demand. Comparing instant hot drink sales, "coffee & other beverage shop" sales, and "other beverage shop" sales, we estimate the potential market size for new Chinese-style tea drinks at 40–50 billion yuan.

The Path to Victory:

Quality, Supply Chain, and Marketing

Tea Drink Quality as Foundation: Innovation Sustains Differentiation and Fashion Appeal

High-quality tea drinks are the bedrock.

- Healthiness. Health is the core direction of consumption upgrading. Replacing processed toppings like tapioca pearls and coconut jelly with milk and fresh tea leaves, while adding fresh seasonal fruits, creates healthier new-style tea drinks.

- "Deliciousness." Tea drink chains must control tea leaf and ingredient quality, innovate on technique, and maintain hygiene to ensure taste.

- Stability and consistency. Stable quality for the same product and consistency across chain locations help build a strong reputation. A blockbuster tea drink that captures attention won't arbitrarily change its flavor due to external factors.

▲ Tea leaf quality affects tea drink taste.

Continuous product innovation maintains differentiation and fashion appeal. Tea drink products are easily imitated; hit drinks often become industry standards within short order. Sustained innovation is essential for leading tea drink chains.

- Ingredient and recipe innovation. To maintain momentum, merchants should actively develop new beverages: adding seasonal fruits for seasonal offerings, and updating existing recipes based on customer feedback to attract new patrons.

- Actively developing derivatives. Beyond beverage innovation, merchants can expand into tea drink-adjacent businesses: making mango pastries from seasonal mangoes, packaging fresh upstream tea leaves as retail products, or developing tea-related snacks.

Supply Chain: Quality and Stability Assurance, Scale Purchasing Reduces Costs

Barriers to entry in new Chinese-style tea drinks are relatively low, with single-store investment ranging from 300,000 to 1.5 million yuan. Robust demand has attracted numerous entrants; chains are generally small-scale, the industry is highly fragmented, and competition is fierce.

Tea drink quality depends primarily on the tea base, and tea leaves for making the base represent the largest cost item for new Chinese-style tea drinks. Controlling upstream tea leaf supply chains is one of the necessary conditions for large new Chinese-style tea drink chains to build core competitiveness. Establishing strategic partnerships with origin tea gardens and achieving bulk purchasing can ensure product quality, flavor consistency, and stability across stores; exclusive supply can create unique tea bases, strengthening product differentiation.

Currently, fruit-based tea drinks represent a limited share of new Chinese-style tea drinks, with relatively low overall fruit consumption; meanwhile, fruit is perishable with short procurement radiuses, so tea drink chains mostly source from local wholesale markets — supply chain barriers are not high here.

Marketing: New Media Connects with Target Demographics, Reverse Promotion Amplifies Buzz

In the new media era, marketing has played an indispensable role for each wildly popular new-style tea shop. These shops actively pursue online marketing to boost visibility: regularly updating their official websites, WeChat public accounts, and Weibo pages, interacting with fans across social platforms, and responding to customer feedback with adjustments. Additionally, customers posting photos creates reverse promotion that dramatically amplifies heat.

Searching for the Next "Starbucks"

Short Term: Low Barriers, Capital Inflows, Intensifying Competition

New brands are emerging. New tea drink brands have rewritten the history of low-end tea consumption through product quality, experiential store design, pricing, and payment methods — revitalizing traditional Chinese tea and elevating it to fashionable, branded consumption. With capital backing, more companies and entrepreneurs will enter the tea drink market, digging deeper into latent consumer demand, seizing opportunities in product innovation extensions and business model extensions, increasing product value, and capturing market share.

Successful brands are launching sub-brands. As new-style tea heat continues to rise and more new brands flood the market in pursuit, certain established names have already begun plotting new territory — the sub-brand movement in new tea drinks.

Medium to Long Term: Rebuilding Starbucks

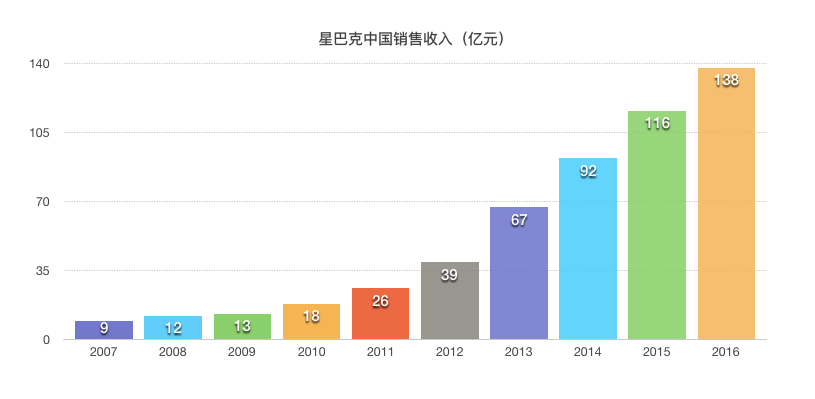

▲ Starbucks China Revenue. Unit: 100 million yuan. (Source: Euromonitor, CITIC Securities Research)

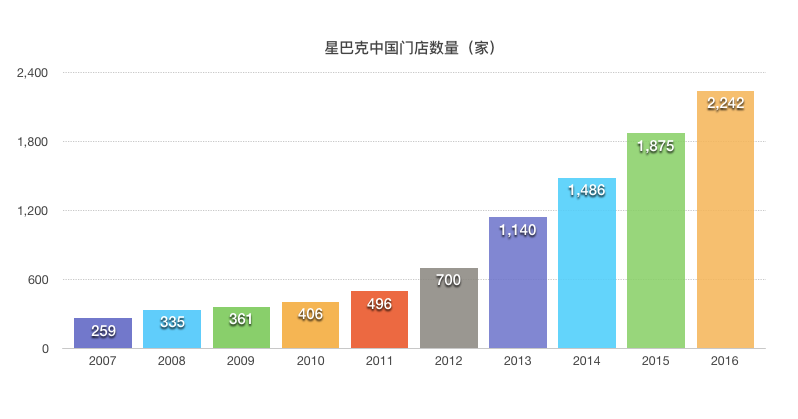

▲ Starbucks China Store Count. Unit: stores. (Source: Euromonitor, CITIC Securities Research)

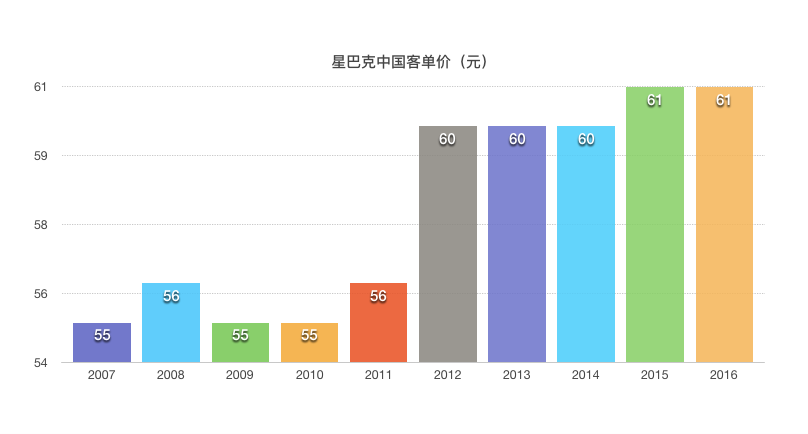

▲ Starbucks China Average Ticket. Unit: yuan. (Source: Euromonitor, CITIC Securities Research)

According to Euromonitor data, Starbucks China had 2,242 locations in 2016, with revenue of 13.8 billion yuan, average single-store revenue of 6.17 million yuan, and average ticket of 61 yuan. Based on current new Chinese-style tea shop operations, we project that future industry leaders could reach roughly 1,000 stores (about half of Starbucks), with average annual single-store sales potentially reaching 12 million yuan (about double Starbucks'), and annual revenue potentially exceeding 12 billion yuan — comparable to Starbucks' sales volume.

(This article is sourced from CITIC Securities Research. Feel free to share to Moments.)

▲ FreeS Report (8): Will the Matcha Industry Produce the Next Starbucks? (Includes Perks)

▲ Starbucks 1987–1997: The Cold Start and "Clunky" Expansion of a Coffee Empire | FreeS Original

▲ Shopping Is a Form of Self-Expression: Can New Retail Win Over the Rebellious New Generation? | FreeS Business School