2004–2020: Four Reforms in China's Capital Markets — Who Benefited in the End? (Part 2) | Li Feng Column

Standing at the threshold of ChiNext's registration-based IPO system.

In yesterday's piece Will China's Capital Market Improve in the Second Half of 2020? (Part One), we explored how global capital markets have shifted since the pandemic began and where China's opportunities lie in this new landscape. Our preliminary conclusion: large-scale global asset reallocation is virtually inevitable, and the post-reallocation order will likely look different from the past. Regions that have effectively controlled the pandemic and seen stronger economic recovery will be the first to attract this capital. And compared to the US, China currently looks more attractive.

In today's follow-up, we turn our focus inward to examine the opportunities embedded in this round of capital market reform — the ChiNext registration-based IPO system — and what it means for entrepreneurs. Who actually stands to benefit?

Before diving in, a few headline conclusions:

- Looking back at China's three capital market reforms between 2004 and 2019, private enterprises were the beneficiaries each time. Specifically, the birth of the SME Board primarily benefited leading companies in various sub-sectors, especially manufacturing; the launch of ChiNext gave a major boost to private enterprises hit by the financial crisis, particularly smaller "hidden champion" companies in emerging industries; and the STAR Market, born amid trade war tensions, has especially benefited companies with core technologies aligned with the national "quality and efficiency improvement" direction of industrial transformation and structural adjustment.

- The ChiNext registration-based IPO system, introduced amid the pandemic, lowers listing barriers for startups, allows dual-class share structures and red-chip companies to list, and creates room for unprofitable companies to go public. This expands exit channels for early-stage investors, but will also reshape the competitive dynamics among VC and PE firms.

- Companies that align with national long-term policy priorities ("both red and expert") will see their valuations rise.

We hope this offers a fresh perspective. We welcome your thoughts in the comments.

Yesterday (May 27), the People's Bank of China website published an article titled "Financial Commission Office Announces 11 Financial Reform Measures." The article stated that member agencies of the Financial Commission — including the NDRC, Ministry of Finance, PBOC, CBIRC, CSRC, and SAFE — would soon roll out 11 financial reform measures. The fourth of these is "advancing ChiNext reform and piloting the registration-based IPO system," with the goal of "establishing and improving the registration arrangements, ongoing supervision, and sponsorship system for ChiNext-listed companies."

Before introducing this series of reforms, the article quoted Premier Li Keqiang's remarks from this year's Government Work Report: "The greater the difficulties and challenges, the more we must deepen reform, remove institutional barriers, and unleash endogenous drivers of growth."

If you look back at decades of China's capital market reforms, you'll find this thread running throughout: hardship begets reform, and reform unlocks momentum for development.

So to understand how this round of deepening reform, represented by the ChiNext registration-based IPO system, will affect the venture investment market and which private enterprises can ride this wave, we need to review the three capital market reforms China experienced from 2004 to 2019 — and look for answers in the rings of history.

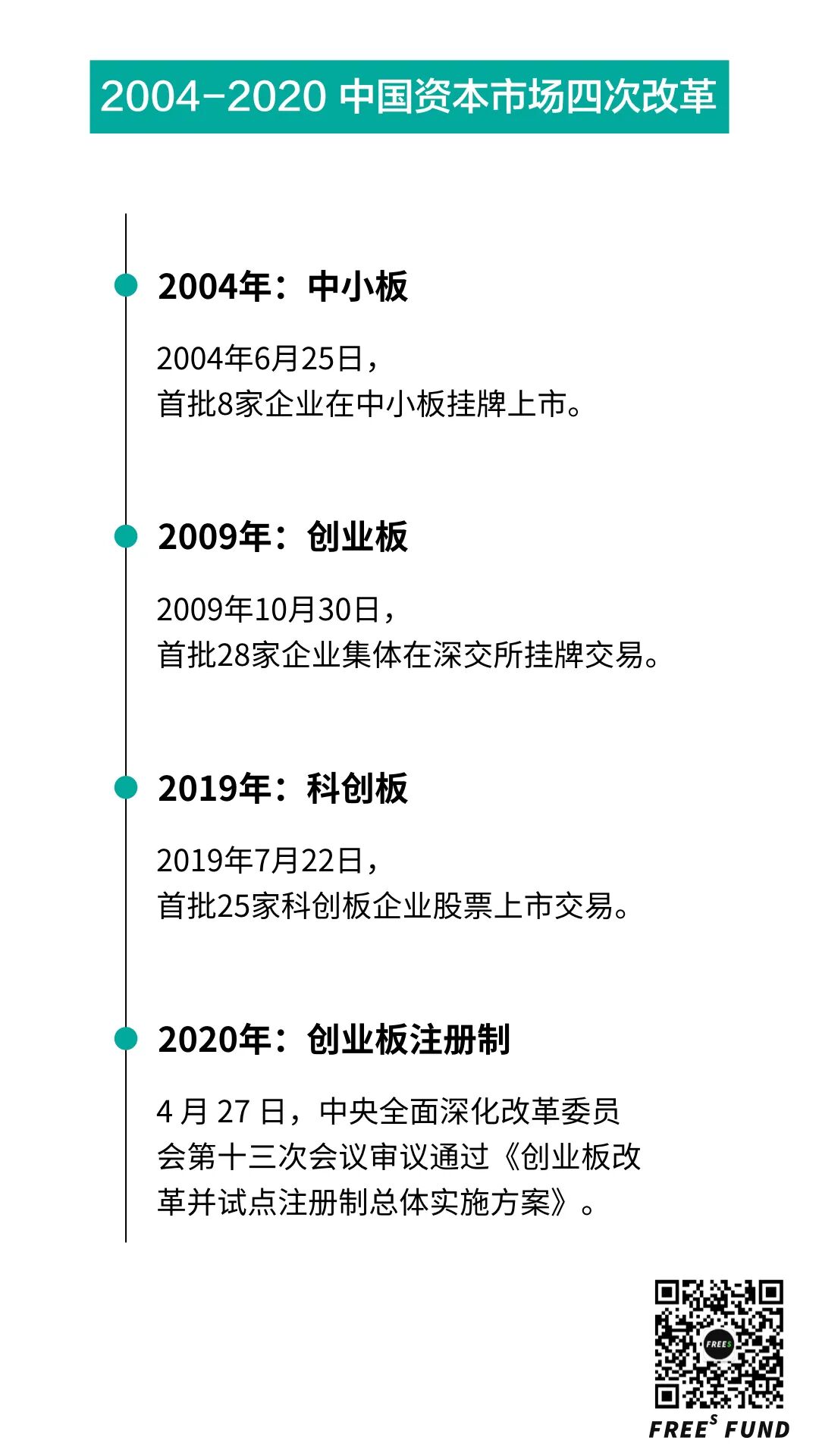

01 Three Capital Market Reforms, 2004–2019: SME Board, ChiNext, STAR Market

Serving China's small and medium-sized enterprises has long been recognized as one of the enduring missions of the country's capital markets. Let's look at the major economic conditions, both domestic and external, that gave birth to these reforms over the past decade-plus.

First, the SME Board. Born from crisis, it addressed the urgent financing needs of smaller companies.

In the late 1990s and early 2000s, the internet was taking off, China was deepening its foreign trade system reform, and WTO accession was on the horizon. SMEs were flourishing. But in the early 2000s, the Nasdaq dot-com bubble burst, and the ChiNext board then in preparation was put on hold. The vigorous funding needs of countless SMEs went unmet.

Citing a People's Daily report, regulators responded with a phased approach: first launch the SME Board, then build on that experience to open ChiNext. On May 27, 2004, the SME Board debuted; one month later, its first eight companies began trading.

So in a sense, the SME Board was born from ChiNext's "difficult delivery" and the suspension of main board IPOs. It opened a dedicated channel for qualified quality SMEs to access capital markets, improved financing convenience for sub-sectors and lowered financing costs, and helped construct a multi-layered capital market architecture.

According to statistics from Shenzhen Stock Exchange researcher She Jian, as of October 2008, 96 of 273 SME Board companies were sub-sector leaders, accounting for 35.2%; and of these leaders, over 95% were in manufacturing. In short, the SME Board's creation primarily benefited leading companies in various sub-sectors, especially manufacturing.

Now ChiNext.

From preparation to official launch, ChiNext took over ten years — what was called "a decade to sharpen one sword." According to Cheng Siwei, then Vice Chairman of the Standing Committee of the Tenth National People's Congress, in a 2009 interview with Yicai, ChiNext was originally slated to launch after the 2008 Two Sessions, but was delayed to 2009 due to the financial crisis.

At the 2009 China Securities Market Annual Conference that April, Long Wuhua, then Director of Shenzhen Stock Exchange's Planning and International Department, stated that ChiNext was an effective response to the financial crisis, suited to promoting economic growth and structural adjustment, strengthening the SME support system, and boosting employment through entrepreneurship.

This represented the mainstream view at the time. That October, at the China-ASEAN Financial Cooperation and Development Leaders Forum, then CSRC Assistant Chairman Zhu Congjiu likewise described ChiNext's launch as a new highlight of China's proactive response to the international financial crisis.

In short, ChiNext's debut gave substantial support to private enterprises battered by the financial crisis, becoming a gathering place for smaller "hidden champions" in emerging industries.

The 2019 launch of the STAR Market followed the same pattern.

According to National Bureau of Statistics data, 2018 GDP growth showed a "high before, low after" trajectory. While China remained the largest contributor to global growth, the economy faced downward pressure (6.8% year-on-year in Q1, 6.7% in Q2, 6.5% in Q3, 6.4% in Q4 — the lowest quarterly reading in ten years). China's economy urgently needed to transition from high-speed growth to high-quality development.

There was external pressure too. Since the first half of 2018, US-China trade friction had escalated repeatedly, with high-end manufacturing and other high-tech sectors taking the hardest hits.

On January 30, 2019, the CSRC issued guidance clarifying the STAR Market's positioning: facing the global frontier of science and technology, facing the main battlefield of the economy, facing major national needs. In just over a year, the STAR Market supported a batch of companies fitting this innovation-focused profile — with core technologies, aligned with national quality-and-efficiency industrial restructuring — covering next-generation information technology, high-end equipment, new energy and materials, energy conservation and environmental protection, and biomedicine, among other high-tech and strategic emerging industries.

Overall, the STAR Market was created partly to fill the capital market's gap in serving technological innovation, deepen financial supply-side structural reform, and increase direct financing's share; and partly to address independent industrial chain security and technological innovation, serving the national innovation-driven development strategy.

To summarize: whether SME Board, ChiNext, or STAR Market, their launches were all inevitable steps in building a multi-layered capital market system and improving the corporate financing environment over the medium to long term. Each emerged at a specific historical juncture. Internal and external difficulties were the soil that nurtured reform — and the window where opportunity sprouted.

02 In All Three Past Reforms, Private Enterprises Ultimately Benefited More

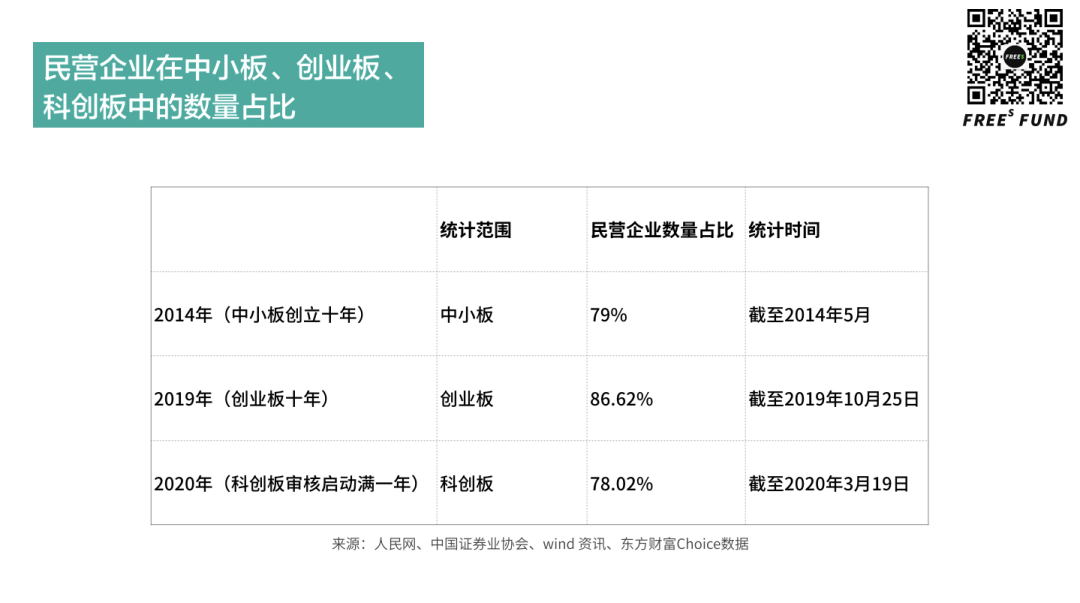

▍ Share of private enterprises among companies listed on SME Board, ChiNext, and STAR Market

Above we outlined the birth contexts of these three representative reforms (2004 SME Board, 2009 ChiNext, 2019 STAR Market listings). Let's compare some data to see whether state-owned or private enterprises captured more of the reform dividend.

Here's what we found by year:

First, by number. Whether looking at A-shares overall, SME Board, ChiNext, or STAR Market, private enterprises hold an absolute majority.

2012 — CSRC data released May 31, 2012 showed private enterprises exceeding 50% of A-share listed companies. Specifically: nearly one-third of main board companies were private; nearly 80% of SME Board companies; and over 95% of ChiNext companies.

2014 (ten years after SME Board's founding) — Shenzhen Stock Exchange data showed private ownership and high-tech orientation as the two defining characteristics of SME Board companies. As of May 2014, private companies accounted for 79% of the SME Board, and 519 companies (72.49%) were high-tech enterprises.

2018 — According to a December 2018 speech by CSRC Vice Chairman Yan Qingmin, as of end-October 2018, 2,498 of 3,573 listed companies were private, with their share rising from 55% in 2012 to 70%. From 2016 through October 2018, 621 private enterprises conducted IPOs, raising 311.6 billion yuan — representing 83% of IPOs by number and 63% by amount.

2019 (ten years of ChiNext) — Wind data as of October 25, 2019 showed 775 ChiNext listings with total market cap of 5.67 trillion yuan. Of these, 693 were private enterprises, or 86.62%.

2020 (one year after STAR Market review began) — East Money Choice data as of March 19 showed 91 STAR Market listings with combined IPO fundraising of 108.673 billion yuan. Private enterprises numbered 71, or 78.02%.

▍ Private enterprise fundraising share on SME Board, ChiNext, and STAR Market

Second, by fundraising amount. Total fundraising = IPO + private placement + bond issuance.

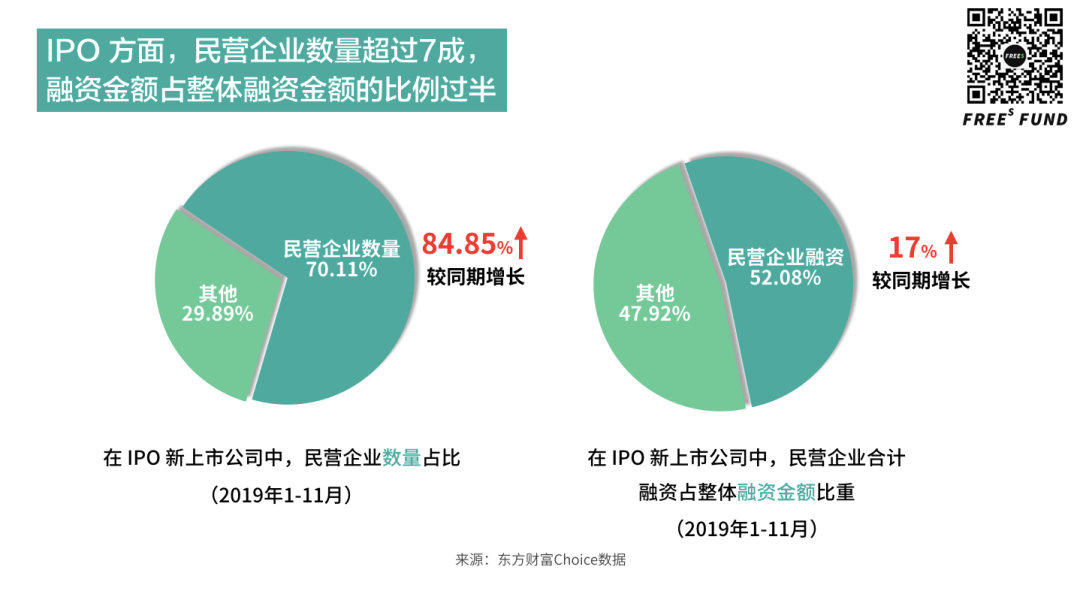

For IPOs, private enterprises' fundraising exceeded half the total.

According to Times Business School's 2019 A-Share IPO Financing Report (Jan-Nov) based on East Money Choice data: among 174 IPOs in the first eleven months of 2019, 122 were private enterprises (70.11%). Their combined fundraising of 105.412 billion yuan was up 124.53% year-on-year, representing 52.08% of total IPO proceeds — up about 17 percentage points from 34.78% in the same period of 2018.

Private enterprises' average IPO size was also rising. The Jan-Nov 2019 average of 864 million yuan was up 21.52% from 711 million yuan in the same period of 2018.

For private placements, private enterprises dominated by number but lagged central and local SOEs by amount.

According to Niuniu Financial Research citing Wind data, among 215 companies conducting private placements in 2019, private enterprises were the main force at 133 companies (62%), roughly flat from 61% the previous year.

Local and central SOEs followed at 42 and 34 companies respectively. But by amount, the numerically dominant private enterprises raised 246.4 billion yuan, about 40.81% of the total; central and local SOEs combined raised about 314.6 billion yuan, or 52.10%.

For bond issuance, private capital was at a clear disadvantage.

Per East Money Choice data, A-share private listed companies raised 335.6 billion yuan through bond issuance in Jan-Nov 2019, representing just 8.89% of total A-share corporate bond financing. This share was 15.47% in 2017 and 13.04% in 2018 — showing a declining trend over three years.

Overall, returning to CSRC Vice Chairman Yan Qingmin's December 2018 data: from 2016 through October 2018, 540 private listed companies conducted refinancing, raising 864.8 billion yuan — 66% by number and 41% by amount of all listed companies.

To summarize: private enterprises hold an absolute majority by count across all boards; by fundraising, they lead in IPO proceeds but lag in refinancing compared to central and local SOEs.

That said, there's no denying that capital market reforms have provided quality private enterprises with more layered, more flexible, and more effective financing channels.

Choice data also shows that in Jan-Nov 2019, the STAR Market led all four A-share boards in total fundraising at 72.947 billion yuan. Less than four months after its first listings, STAR Market had already surpassed the main board, SME Board, and ChiNext — becoming the board with the highest fundraising potential in the A-share market. This means outstanding technology companies will receive stronger capital market support and broader exit channels going forward.

Who Gets the Opportunity in the Latest Policy Push?

Having reviewed the past, let's look at the series of capital market policies rolled out over the past month.

On April 27, the Central Committee for Comprehensively Deepening Reform approved the Overall Implementation Plan for ChiNext Reform and Pilot Registration-Based IPO System. This includes streamlining and optimizing ChiNext refinancing conditions; optimizing review and registration procedures, compressing timelines, and making standards, procedures, content, and processes transparent and public.

Then on April 30, the CSRC issued the Announcement on Arrangements for Innovative Pilot Red-Chip Enterprises' Domestic Listing, adjusting listing thresholds for red-chip companies already listed overseas and not yet listed overseas. For already-overseas-listed red chips, the market cap requirements were adjusted to meet either: (1) market cap of at least 200 billion yuan; or (2) market cap above 20 billion yuan, with independent R&D, internationally leading technology, strong technological innovation capability, and relatively advantageous competitive position in the industry.

The ChiNext Registration-Based IPO System Is a Rare Opportunity

Again, consider the launch context. The crises differ, but the problem-solving logic is similar.

Whether it's the pandemic's massive blow to the global economy, or the trust crisis facing US-listed Chinese companies triggered by fraud scandals. At this particular moment, the state is not only continuing to push deleveraging and increase direct financing, further lowering capital market barriers — it's also paving the way for some US-listed Chinese companies to "return home." We're already seeing this: on the evening of May 5, Hong Kong-listed SMIC announced it planned to apply for STAR Market listing.

For private enterprises, the registration-based system is a rare opportunity. The most direct reason is that the new plan lowers listing barriers for startups, allows dual-class share structures and red-chip companies to list, and creates room for unprofitable companies to go public — expanding exit channels for early-stage investors.

At the same time, the rollout of the registration-based system will reshape VC and PE competitive dynamics. In the near term, PE will feel some impact. As noted, lower listing barriers may shorten company growth cycles — companies could list before achieving scaled profitability, reducing the number of funding rounds needed and potentially eliminating the need for PE pre-IPO rounds. If PE firms move their investment focus earlier, VC competition will intensify, and some bubbles may even emerge.

Specifically for Startups, Whose Opportunity Is This?

In my view, quality companies that align with national long-term policy priorities will see their valuations rise. In short: companies that are "both red and expert."

Specifically, in consumer sectors, "red and expert" means companies that serve domestic Chinese demand and fit the consumption upgrade trend — especially important as foreign trade faces short-term headwinds and domestic consumption needs boosting.

"Red and expert" tech companies are those in directions the country needs: new infrastructure, localization of critical technologies, and related areas.

Summary

-

Looking back at China's three capital market reforms from 2004 to 2019, private enterprises were the beneficiaries each time. Specifically, the SME Board's birth primarily benefited leading companies in various sub-sectors, especially manufacturing; ChiNext's launch gave major support to private enterprises hit by the financial crisis, particularly smaller "hidden champions" in emerging industries; and the STAR Market, amid trade war tensions, especially benefited companies with core technologies aligned with national "quality and efficiency improvement" industrial transformation and structural adjustment.

-

The ChiNext registration-based IPO system, introduced amid the pandemic, lowers listing barriers for startups, allows dual-class share structures and red-chip companies to list, and creates room for unprofitable companies to go public. This expands exit channels for early-stage investors, but will also reshape VC and PE competitive dynamics.

-

Quality companies that align with national long-term policy priorities ("both red and expert") will see their valuations rise.

Discussion Question

Q: Are you optimistic or pessimistic about China's capital market right now?

Share your views in the comments. Through 21:00 on June 3, we'll give away copies of Why the West Rules — For Now to the 6 most thoughtful commenters. This book offers a broader, more diverse, more scientific perspective on how we got here and where we're headed — and might offer some psychological grounding amid the pandemic.

(Welcome to read, share, and hit "like." For reprint permission, reply "reprint" for our rules and contact FreeS Little Rui [ID: freesfund] for authorization. Copyright FreeS Fund.)

Will China's Capital Market Improve in the Second Half of 2020? (Part One) | Li Feng Column

Hammer and Dance: Healthcare Investment Opportunities After the Pandemic | Frees Fund Why Is New Infrastructure the Stimulus Policy That Will Most Shape China's Next 10 Years? | Li Feng Column One Chart to Understand Changes and Opportunities in China's Industrial Chain | Li Feng Column What Did Minister Miao Wei Actually Say About Chinese Manufacturing? | Frees Fund One Chart to See Globalization or Deglobalization | Li Feng Column After the Pandemic, A New Era for "Good Companies" | Frees Fund