2018 was a tough year, but absolutely one with inflection-point significance.

You don't need to get clever or cut corners. Just do what aligns with the cycle and the structure, and you'll make money in this cycle.

On the last day of 2018, I'm sharing a recent talk I gave at Hundun University. I hope it gives you a little more confidence on your entrepreneurial journey ahead.

For many, 2018 was a year of uncertainty. On the last Friday of 2018, we sat down with the CEOs of seven of our portfolio companies in tech to discuss how technology enterprises grow, and we were fortunate to hear them speak candidly about their year in review. To sum it up in one sentence: turning technology into a product, and a product into a commodity — every step, like the year 2018 itself, brings opportunity and challenge, setback and growth, alternating or arriving all at once.

The right thing is often not the easy thing. What's remarkable is that these people, among the most self-reflective you'll find, faced all their setbacks and regrets without losing confidence or courage, still certain of their direction. There's no doubt that every entrepreneurial journey has its darkest hours. Only by wading through the flood of anxiety, approaching the ups and downs of entrepreneurship with equanimity, and focusing on a company's intrinsic value can you get closer to your goal.

In the year ahead, may you on the entrepreneurial path have wisdom and resolve, with a bit of luck on your side too. Happy New Year!

— Li Feng, Founding Partner, FreeS Fund

2018 Was Hard, But It Was Also a Year of Inflection Points

By Li Feng

First published on Hundun Business School

▍Viewing China's 2018 Through History

2018 was genuinely difficult. China faced economic challenges, and public sentiment was broadly negative. But was 2018 the most difficult period?

To answer that, we need to look back at three moments in time.

First, 1978. At that time, China's GDP was just over 300 billion yuan, and 80% of the labor force came from rural areas. Per capita grain, cotton, and oil production in 1978 was roughly equivalent to 1955 levels. Meanwhile, in the cities, 8 million households lacked housing — they were living in classrooms, factories, cafeterias, and the like.

It's fair to say that for China at that time, both livelihood and economy were in dire straits.

The second time point is 1990.

1990 is somewhat special. We know there were two inflationary cycles in Chinese history. The first was in 1987, 1988, and 1989. In official statistics, annual inflation reached 20% or higher for three consecutive years. In other words, for three straight years, you could do absolutely nothing and watch your real wages fall by 20%.

Because of this inflation, China saw a wave of panic buying that has never been repeated since. Urban residents across the country rushed to supermarkets to buy everything they could think of, because prices were rising so fast.

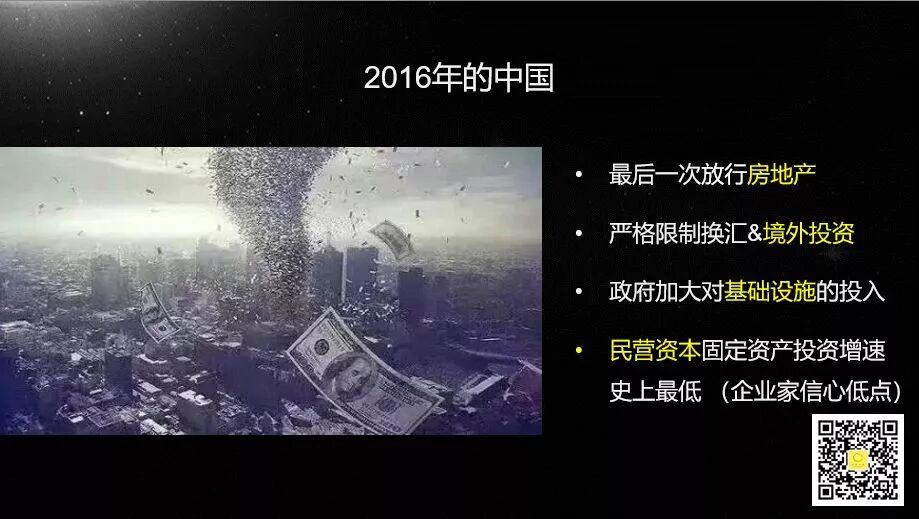

Another time point: 2016.

Some might ask, was 2016 difficult for China? Actually, all the difficulties China experienced in 2018 should have happened in 2016. If you have a good memory, you might recall a few things.

First, after the 2016 Spring Festival, China's real estate regulation policies were somewhat relaxed; strict purchase limits weren't reimposed until October 1, 2016. Second, from late Q2 to early Q3 2016, there were strict controls on outbound RMB investment, whether for enterprises or individuals, with tight foreign exchange restrictions. Additionally, the government increased infrastructure investment, and from Q3 onward funded maintenance and repairs for high-speed rail, railways, highways, and subways. In May 2016, we also saw the lowest monthly growth rate for private fixed-asset investment — business confidence hit a nadir.

So why didn't 2016 feel more difficult than 2018? The reasons are quite specific.

One reason: at the start of that year, the entire financial world expected the US to raise interest rates three or four times, or at least twice. But in 2016, the Federal Reserve hiked only once. 2016 also happened to bring Brexit, civil conflict in Turkey, and the election of Donald Trump as US president — a series of political black swan events that created a window of opportunity for China.

Looking back at these political black swans through an economic lens, we can see that they heightened economic uncertainty, which in turn made economic expectations more conservative. And to stimulate the economy, the pace of rate hikes was slowed — which ultimately delayed the economic crisis.

So how has China responded to these challenges and continued moving forward during each difficult period?

▍Every Low Point Is an Opportunity to Switch Lanes and Restructure

Whenever facing challenges, society tends to be filled with negativity and anxiety. But from another angle, this is precisely when structural, long-term opportunities emerge — chances to switch lanes and restructure. And each time there has been internal and external trouble, three kinds of signals have appeared: reform (such as opening up monopolized industries), opening up (such as welcoming foreign investment), and encouraging the development of private enterprises. These signals herald a historical inflection point.

Let's look at the difficult periods in history again.

In 1978, after experiencing material scarcity and backward per capita grain and cotton production, the government — for the first time in a society where everything was publicly owned — opened up agriculture, introducing the household responsibility system and contracting production to individual households.

We can imagine how this was viewed in a society where every system was publicly owned. This shift indeed sparked enormous controversy. Agriculture was the most fundamental issue affecting the entire nation's welfare. But because of the special internal and external difficulties of 1978, it catalyzed this major reform.

This reform fully mobilized farmers' enthusiasm, dramatically improved labor productivity, and even created surplus labor — laying groundwork for subsequent reforms.

Then in 1980, China faced the return of sent-down youth to the cities and a sudden spike in unemployment. In response, the government opened up urban services — supply and marketing cooperatives, state-run restaurants, and so on — allowing the first individual businesses to exist.

The third time was 1984. Because the household responsibility system had increased rural surplus labor, this gave rise to mixed-ownership reform and the first township and village enterprises (TVEs). China's TVEs were the foundation of manufacturing. Though their development was extremely painful, by 1995 TVEs contributed 25% of China's GDP.

Next, 1990. With severe inflation and economic recession, the government decided to open up what has become today's largest and most capital-intensive industry: real estate, allowing property transactions.

We all know that Deng Xiaoping's 1992 Southern Tour speech reignited the spark of reform and opening up. But that tour wasn't as smooth as it appeared on the surface. Deng went south in late January, yet the Shenzhen Special Zone Daily didn't first report on it until March 26 — two months in between, during which, much like China today, society was filled with doubt.

In 1998, to respond to the Asian Financial Crisis, China opened up several industries. One with enormous impact was granting independent foreign trade rights to private manufacturing enterprises. Before this, private operators had to apply through state-owned foreign trade companies to export. After opening up export rights, manufacturing enterprises could export on their own.

Then in 2008, affected by the global financial crisis, China finally resolved — after five or six years of continuous discussion — to launch ChiNext, which was approved in 2008 and officially began trading on the Shenzhen Stock Exchange in July 2009.

Looking back at this historical process, we can see that political and economic foundations must guarantee economic development and people's livelihoods. When these two foundations cannot be guaranteed, structural adjustments and reforms are made that affect the subsequent decades, and long-term structural industry opportunities are born at these time points.

Of course, every time these industry-level structural opportunities appear, there may be some back-and-forth in policy. Just as there were concerns about the household responsibility system in 1978, and difficulties before the Southern Tour. Every restructuring tends to happen at the most difficult moments, undertaken under pressure from all sides. Deng Xiaoping actually visited many places during his Southern Tour, but whether in Wuhan or Shanghai, neither generated much response nor immediately created a signal.

But regardless of the twists and turns along the way, once the signal is set, these opened monopolies don't truly close again. And in these industries, the ultimate winners are often private enterprises.

▍Structural Opportunities for the Next 5-10 Years

Policy Signals in 2018

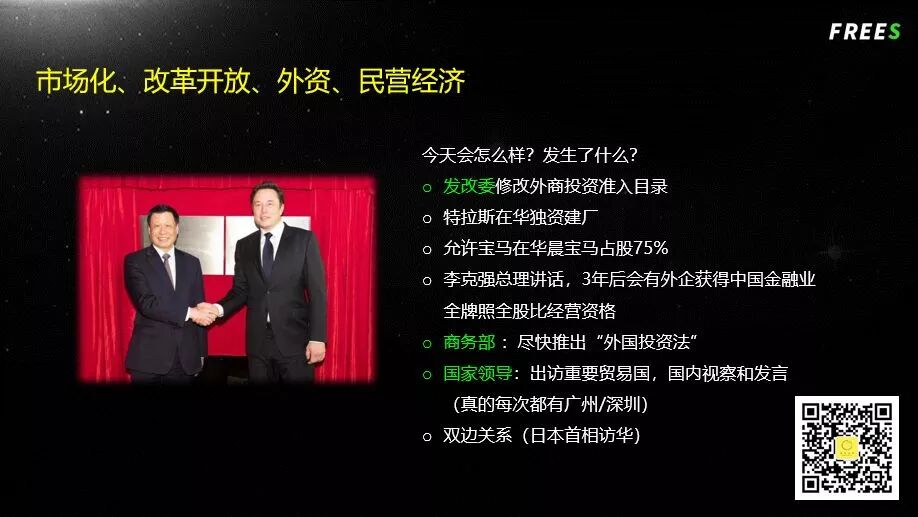

On July 20, 2018, the National Development and Reform Commission disclosed some contents in its revision to the Foreign Investment Access Catalog. Though this was an official document published on the highest-level NDRC website, the news was relatively low-key and not widely disseminated.

But if you happened to notice this news, you would have found that it covered nearly all of China's infrastructure industries and service sectors, including energy, grain circulation and production — almost all of these industries were opened up.

On July 1 this year, Tesla established its first wholly-owned factory in China, with the government providing land and loans. Tesla setting up a main plant in China counts as a signal that the auto industry welcomes foreign investment and encourages market-based competition.

Therefore, if you re-examine what happened in China in 2018, it's no different from how certain industries in 1978 created enormous structural opportunities for private enterprises. And in the early stages of these structural opportunities, both foreign and private enterprises enter simultaneously; but after 5-10 years of development, the biggest winners are mostly private enterprises.

Learning from Developed Countries' History, Finding the "Nails" in China's Industrial Chain

So in the coming 5-10 years, in what industries will long-term structural opportunities actually emerge?

Today, China has roughly 780 million employed people. The workforce breaks down to roughly 38% in agriculture, 27.8% in industry, and 34.1% in services — with agriculture and industry combined accounting for nearly 520 million people. And some of those registered as agricultural workers are likely actually working in manufacturing. So China's manufacturing share, whether measured by employment or GDP, is extraordinarily high.

One challenge China currently faces is keeping these manufacturing jobs — which represent such a large share of total employment — anchored in the country long-term. As labor costs gradually rise, some portion of this manufacturing will obviously shift elsewhere. So what approaches can keep manufacturing in China over the long run?

Japan's approach was to increase the total value contribution across the entire industrial chain — that is, to raise the overall value-added of the supply chain and thereby stabilize it.

There are only two ways to increase value-added across a supply chain. One is building brands. The other is raising technological content. A representative example of the latter is Huawei.

Huawei is both a brand and a technology benchmark. Before 2016, China essentially had no chip industry to speak of. Then Huawei's HiSilicon division broke into the global top 20 in 2016. Give it another three to four years, and HiSilicon will likely rank in the top five globally.

If Huawei has brand, technology, mid-to-high-end positioning, and low-end coverage all together, that means the entire mobile phone manufacturing supply chain can remain in China for a considerable period and at significant scale. Huawei's presence can also drive and support the related supply chain ecosystem.

Companies like Huawei are what we call "nails" in the industrial chain. They provide enough stability value and critical value across the entire supply chain to keep it anchored in China. This is why China now hopes to use these nails to solve problems of structural stability, political stability, and economic stability.

So the critical question becomes: who and what model can deliver long-term value appreciation for China's supply chain? If these questions aren't resolved, enormous other problems will emerge. This also means that if you're working in this dimension, you're basically moving with the economic structure and with the economic cycle.

Projecting China's Systemic Opportunities Over the Next 5-10 Years

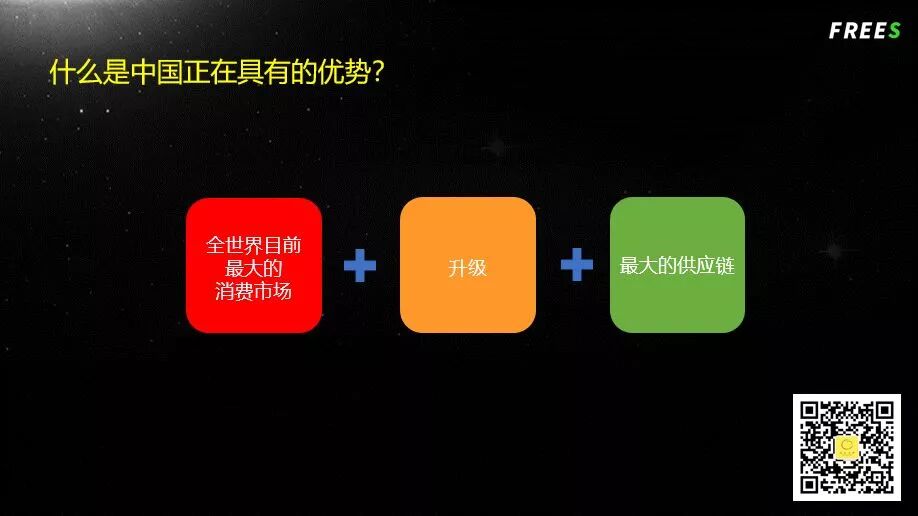

For many industries, China either is or is becoming the world's largest consumer market. China's total consumer market is already the biggest globally, at nearly $7 trillion. This creates the possibility for world-class consumer brands to emerge across many Chinese industries.

Take electronics as an example. In 2015, if someone had said China would produce a world-class consumer electronics brand, not many people would have believed it. Today, most people accept this as fact — without realizing it became reality in just three years. One reason behind this is that after 2000, China became the world's largest supply chain for mobile phone production.

And after China became the world's largest mobile phone manufacturing supply chain, the emergence of smartphones represented a technological transition and upgrade. At the same time, China also became the largest consumer market for smartphones. Collect all three of these stamps, and China could produce the biggest companies and, years later, the biggest brands in that space.

The same logic applies to the auto industry. China became the world's largest auto parts producer over a decade ago, and since 2009 has been the largest new car consumer market globally. The technological transition in autos is the shift toward new energy and batteries. So if these three elements converge in the auto industry, China could eventually produce world-class automotive brands.

While these things may seem implausible right now, whether you're starting a company or choosing a career, it's worth believing that this will generate enormous technology companies plus world-class brands over the long cycle of 5-10 years.

Of course, China also has some unique national conditions. First, the one-child policy implemented after 1980. Second, the massive expansion of university enrollment that began in 1999.

By 2018, China had roughly 8-9 million higher education graduates, accounting for one-quarter of the global total. How to leverage the world's largest pool of relatively inexpensive, college-educated knowledge workers is a core question for business development. Additionally, China has the largest consumer market and the largest industrial chain. So whoever can best take advantage of these strengths will see the greatest growth potential.

Take WuXi AppTec as an example. WuXi's industry is CRO (Contract Research Organization) — in other words, outsourced research services that help pharmaceutical companies with drug discovery. Specifically, this means hiring chemistry and biology graduates at the bachelor's, master's, or PhD level to run experiments in labs for drug companies.

Before 2003, China's share of this industry worldwide was zero. Today, China accounts for 70% of global preclinical CRO. WuXi AppTec started from that point and, over more than a decade, became the world's largest CRO — later splitting into three listed companies each valued above 100 billion yuan.

To sum up, what is truly rare in China today is that everything — from the state, from government, from policy to economic structure, to supply chain needs, to people's daily lives, to capital markets, to liquidity — all these factors are converging on just two or three directions.

My advice to entrepreneurs is very simple: stop looking for shortcuts. Just do what moves with the cycle and with the structure, and you can make money in this period.

Finally, a question for reflection — welcome to discuss:

Q: What trends might emerge in your industry over the next 5-10 years? Where might the potential breakthrough points lie?

(This article was first published on Hundun Business School. Click "Read Original" to view. For reprint requests, please reply "reprint" to learn the rules and contact FreeS Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

▲ Li Feng Column | China Is at Its Most Rare Historical Moment

▲ Li Feng Column | The Middle Road of New Retail

▲ Li Feng Column | Speculations on the Endgame of China's New Retail

▲ Li Feng Column | The Middle Road of New Retail

▲ Li Feng Column | US Dollar and HK Dollar Rate Hikes, and the Unicorn Winter

▲ Li Feng Column | The US-China Tech Rivalry: China's Secret Weapon

▲ Li Feng Column | What Was the One and Only Successful Great Power Transition in History?

▲ Li Feng Column | A 2 Trillion Market and 10 Trillion in Output: Why We're Bullish on Chinese Chips?

▲ Li Feng Column | The Essence of New Retail in Ten Words

▲ Li Feng Column | Lipton 120 Years Ago, Walmart 50 Years Ago, Muji 30 Years Ago — How I Think About Consumption Upgrades and New Retail

▲ Li Feng Column | The Origin and Future of ICO

▲ Li Feng Column | Mimeng's 8 Million Followers and Martin Luther 500 Years Ago — How I Think About Content Entrepreneurship

▲ Li Feng Column | From iPhone X and Smart Speakers to New Drug R&D and Environmental Monitoring — How I Think About Technological Innovation

▲ Li Feng Column | Bike-Sharing Enters the IoT Track — Where Does the Data War Go Next?