Li Xiang × Li Feng: Strip Away the Emotion, What Did China Look Like in 2019?

The Year Expectations Shift

(Swipe left or right to view more slides)

For the best experience, follow along with the slides while listening to the audio 👇

In 2019, every so often, Feng Shu (Li Feng) would sit down for deep conversations with Li Xiang, editor-in-chief of Dedao, and share their exchanges with the public. Follow the Dedao app [Li Xiang's Knowledge Briefing] and lock in on FreeS Fund's WeChat account [ID: freesvc].

Today's piece is from their first discussion. The conversation took place in mid-February, when our social media feeds were essentially overrun with words like "layoffs," "cost-cutting," and "downgrading." It felt like we'd reached a consensus — 2019 was going to be rough, and hard times were ahead. But as they dug deeper, exploring how our emotions were being shaped; looking past the emotions to examine what China actually looked like today; and identifying what positive developments in 2019 might shift expectations — they found the situation wasn't what we'd imagined.

With the Two Sessions now underway, some of the things they discussed half a month ago (which we may have been skeptical about at the time) are becoming reality. Take tax and fee cuts, for instance — they've just received policy backing. We're taking this opportunity to share this article, hoping the thinking behind it might offer you some insight.

Li Xiang Interviews Li Feng: How Does a Famed Investor View 2019?

By Li Xiang, Editor-in-Chief at Dedao

First published on Dedao app's Li Xiang's Knowledge Briefing

Li Feng is a founding partner at FreeS Fund. He was previously a partner at IDG, the established investment firm. In 2015, Li Feng founded FreeS Fund. Before that, he spent seven years at New Oriental, China's largest education company.

The job of an investor is essentially to use money to validate one's judgment. For venture capitalists, if they're bullish on an entrepreneur and what they're building, they'll vote with their dollars — purchasing a stake in the company at a reasonable price. If their judgment proves correct, the company's value keeps growing, and so does the value of their stake. Venture capital profits from this growth.

Since 2011, entrepreneurship and investing have been two hot domains. Then in 2018, suddenly, both fields — like China's economy — were said to be undergoing "structural adjustment." The resonance between venture capital and the economy is pronounced. VC puts money into companies most likely to make money in the future. These growth companies are the fundamental building blocks of tomorrow's economy. And the money VCs deploy comes from beneficiaries of the last economic cycle — people looking to generate more returns, so they hand their capital to VC firms.

Given the nature of the job, venture capitalists are naturally most attuned to whether the macroeconomy is healthy, what future economic prospects look like, and which sectors and industries hold opportunity in this broader environment.

Of course, these are questions many people care about. Most just don't have as much skin in the game, or receive feedback as directly, as VCs do. So they don't spend as much time thinking about them.

Even among investors, Li Feng is known for his depth of thinking. For instance, over the past three years, from 2016 to 2018, the Time's Friend New Year's Eve talk cited Li Feng's views every single year.

Li Feng will continue sharing his observations and thinking on the economy and business with us. This time, we'll start with a question that's probably on everyone's mind: How should we view 2019? Will 2019 be better?

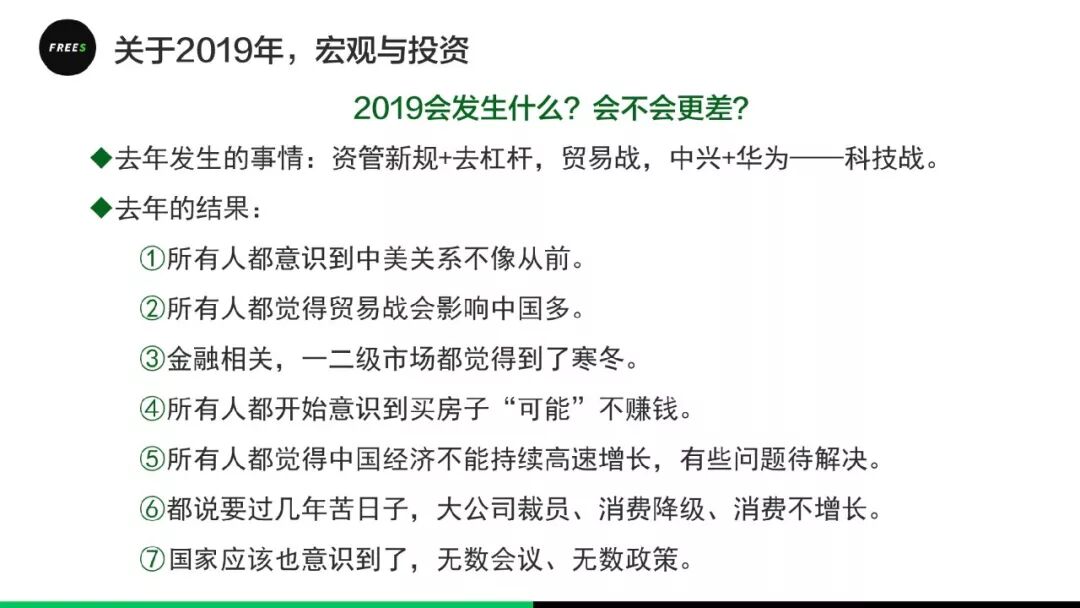

Why Is Everyone So Pessimistic About 2019?

Let's start with one question: What's different about 2019 versus 2018?

Li Feng's answer: expectations. By 2019, expectations for the economy had already hit rock bottom. If there were a dial indicating pessimism versus optimism, the needle had swung fully to the pessimistic side.

There was a popular quip at the end of 2018: "2019 might be the worst year of the past decade, but it will be the best year of the next decade." Xing Wang, founder of Meituan, reposted it, and it exploded across social media.

This quip perfectly captures the pessimistic mood.

The inflection in expectations began in 2018. In fact, before the FIFA World Cup in Russia wrapped up in mid-July, no one was this gloomy. The most visible evidence was TV advertising during live World Cup broadcasts. Some companies that later announced layoffs or restructuring were still running pricey TV ads at the time. Buying ads signals confidence in future growth.

Why did expectations shift so dramatically?

Li Feng's analysis: two developments in 2018 caught people off guard, forcing them to recalibrate.

The "deleveraging" that the government had been talking about. Simply put, deleveraging means reducing debt burdens across individuals and companies. Debt is fuel for economic growth — more money enables more investment and consumption. But excessive debt, and the potential for defaults, can drag down the entire economy. So China needed to deleverage.

Li Feng says that in 2018, no one foresaw how significantly deleveraging would impact investment, financial markets, and the broader economy. He spoke with many secondary market investors — those who invest in stocks. Everyone said they expected deleveraging to start affecting the market from April 2018. But by August, they all admitted they hadn't anticipated the magnitude of the impact. "It exceeded everyone's expectations."

When you're wrong, you adjust. As a response, people immediately revised their expectations downward and adjusted their behavior accordingly. Expecting it would be harder to borrow, they cut back on investment and consumption. Meanwhile, policy was actually slowly walking back — shifting from tight credit and tight monetary policy toward gradually easing monetary conditions. But people's expectations didn't adjust in tandem.

The US-China trade friction. Similarly, in the first half of 2018, few people viewed US-China trade friction as a long-term issue. Most assumed it could be quickly resolved through negotiation. But as the trade conflict kept escalating, everyone's psychological expectations underwent another adjustment: people began to believe that US-China trade friction, and the broader bilateral relationship, would become a long-term issue that would inject massive uncertainty into China's economy. The expectations needle swung sharply toward pessimism once again.

In Li Feng's words: "Everyone saw these two things coming and prepared for them. But when they actually happened, each one's impact was far greater than expected, and lasted much longer. This outperformance of expectations caused people to adjust their own expectations downward, pricing in much more pessimism about China's economy. Simply put, once I realized I was wrong, I overcorrected."

These two expectation-beating developments, combined with the fact that China's economy happened to be in a structural adjustment phase, produced a triple whammy: people have now adjusted their expectations for China's economy to a "worst-case" setting.

Everyone has mentally prepared themselves for the challenges ahead. And so we get all the reactions we can read about in the media: layoffs, pay cuts, bracing for hard times.

Certain beliefs have taken hold: the US-China relationship will be a long-term problem; US-China trade will create massive uncertainty for China's economy; China's economy won't grow at the breakneck pace of the past 40 years. Returning to Li Feng's own industry, investors have all accepted the narrative of a capital winter — that there's no longer as much money in the market. For ordinary people, there's a growing realization that buying property may no longer be a can't-lose investment. Constant news of layoffs and consumption downgrading makes everyone feel they need to start preparing for lean times.

Why Does Li Feng Say 2019 Will Be Better?

Li Feng is clearly not a "worst-case" expectation holder.

He offers three arguments for why 2019 will only get better.

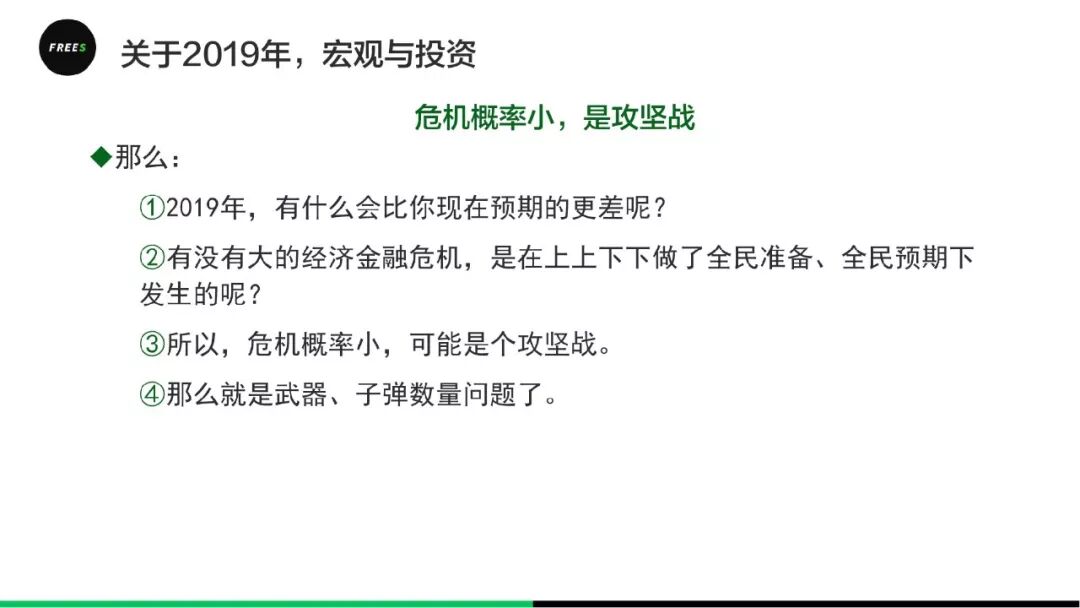

Once you've already priced in the worst case, then in theory things can only turn out better than expected, not worse. If you've already imagined the worst-case scenario, what else is there to fear?

Crises happen when you don't see them coming. But at the start of 2019, virtually everyone in China — top to bottom — was putting on a show of readiness: we've prepared for the worst, we're ready to confront potential economic downturn. For individuals, that meant tightening purse strings and cutting consumption. For companies, it meant trimming headcount and boosting efficiency. For government, it meant rolling out policies and convening meetings, offering both policy support and confidence.

And there's broad consensus on what China's economy needs to do next, including upgrading manufacturing and reducing excessive reliance on real estate investment. Almost everyone knows what needs to be done, how to do it, and has braced for hard times. "Everyone has overcorrected by preparing for all the pessimistic scenarios."

By normal logic, sudden crises are unlikely in this environment. It feels more like a starting point where everyone knows what's missing, what needs to be done, a target has been set, and now it's about reaching that target.

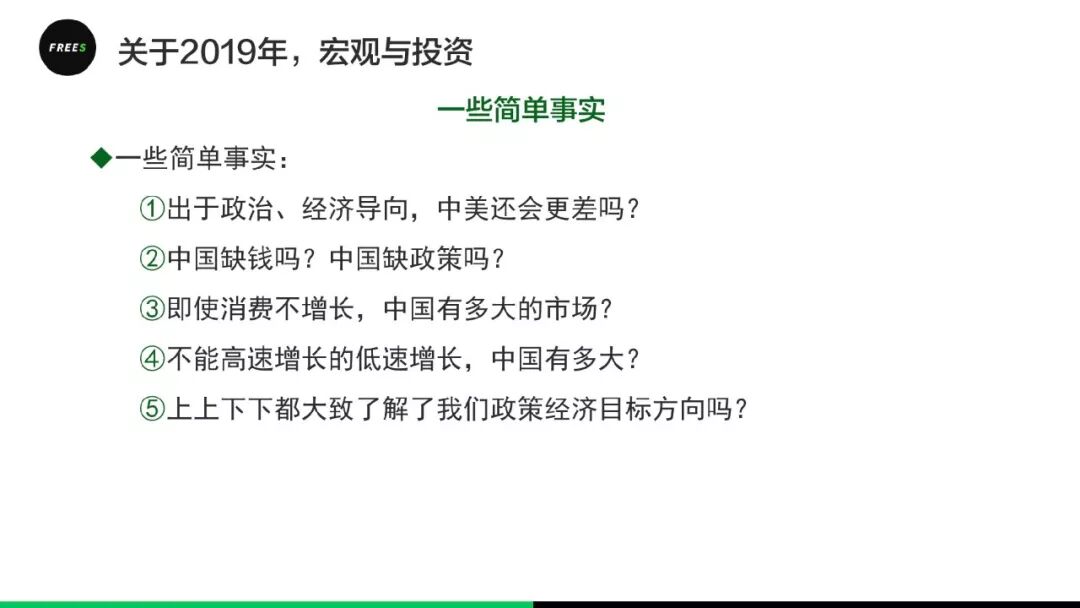

China's economy has grown massive in scale. Even preparing for the worst-case scenario, you'll find opportunities throughout. For example, China's 2018 GDP was 90 trillion RMB. Even using a very pessimistic growth rate, if China's 2019 economic growth slowed to 4%, that would still mean 3.6 trillion in new output. If that were a country's entire GDP, it would rank in the global top 30 — higher than the total GDP of Norway or Israel. At this scale, even tiny increments are staggering.

Looking at total retail sales of consumer goods, China's 2018 figure exceeded 38 trillion, making it the world's second-largest consumer market after the US. Even zero growth would still represent a vast domestic market.

These three arguments are based on the most conservative assumptions. Since worse outcomes won't materialize, and since government, companies, and ordinary people all understand how the economy should adjust and develop going forward, the deduction is: China's current economic problems are primarily problems of expectation. The surprises of the second half of 2018 caused everyone to overcorrect, dialing expectations down to their lowest setting.

So the question becomes: what positive changes could shift this worst-case expectation?

What 3 Variables Could Change the Worst-Case Expectation?

Now let's look at another question: What could happen in 2019 to change this "worst-case" expectation?

Li Feng's view: to assess 2019's macroeconomy, look at what could change people's expectations for the economy as a whole. With the economy still functioning reasonably normally, growing above 6%, changing expectations changes the entire economic picture.

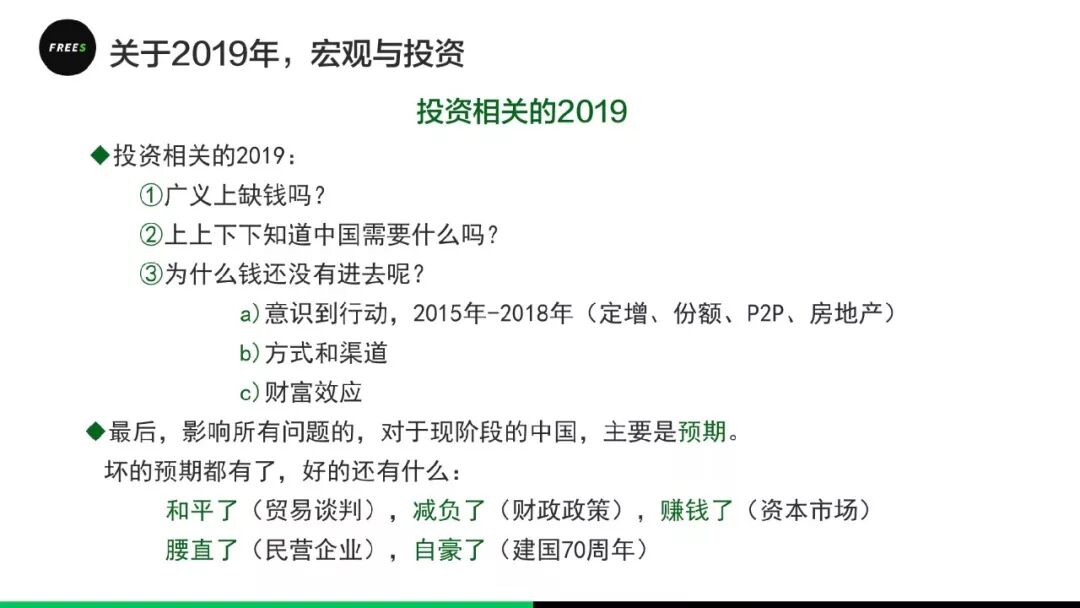

First, he doesn't believe there's any so-called "capital winter." His exact words: "Definitely not." If capital winter means insufficient money supply, then China doesn't have this problem. The central bank released data in January showing that by end-2018, China's broad money supply grew 8.1% year-over-year, with broad money balances exceeding 182 trillion.

The government recognized the counterproductive effects of 2018's tight credit and deleveraging on the economy, and is consciously adjusting. Measures include encouraging state-owned commercial banks to lend to SMEs; moderately easing monetary policy to encourage capital to flow into markets.

There's no shortage of money in the market — what's lacking is confidence about where money can be made. In China's economy, real estate played this role for a long stretch; entrepreneurship also played it for a time. Capital flows to where it can generate returns — where it can make money. Hence the real estate boom and the entrepreneurship boom.

Which sectors can make money and produce so-called "wealth effects" will become the variables that could shift the macroeconomic picture and change expectations in 2019.

Li Feng lists several variables he expects to materialize.

First, the STAR Market. Li Feng considers this the most likely to succeed and the most likely to generate wealth effects.

The STAR Market is a new listing board, independent from the main board. The types of companies it aims to attract, according to public materials, include next-generation information technology, high-end equipment, new materials, new energy, energy conservation and environmental protection, biomedicine, and other technology companies and strategic emerging industries.

Why does Li Feng believe the STAR Market is most likely to succeed? Because China's capital markets have a successful precedent. During the 2008 global financial crisis, beyond adopting proactive fiscal policy and rolling out the 4 trillion RMB stimulus, China also decided to launch ChiNext. The approach then was to select quality companies that fit ChiNext's logic and were already mature enough for the main board, and list them on ChiNext instead. This ensured the quality of ChiNext-listed companies, attracting capital to flood into ChiNext and buy their stocks. The STAR Market's launch could follow this precedent, selecting quality companies that fit the tech entrepreneurship concept to list on the new board.

Li Feng did some math: assume 20 companies are selected, each with an average market cap of 15 billion RMB, for total market cap of 300 billion. If tradable shares represent 25% of total equity, then only 75 billion in capital needs to enter this market to sustain that valuation. Seventy-five billion isn't much. If the STAR Market rallies, with listed quality companies reaching 80-90x P/E ratios like ChiNext back then, it would also drive capital into related companies across the supply chain. The simplest path: main-board companies trading at 10x+ P/E would want to acquire tech-sector companies to boost their stock prices.

The STAR Market's demonstration effect "would rapidly direct money toward investments in these industry directions. Beyond money becoming enthusiastic again, it would flow in specific directions — and those are directions the government wants." Whether advanced manufacturing, biomedicine, or new materials and new energy.

This wealth effect would ripple outward, spreading across the secondary market, then to the primary market, then reaching entrepreneurs. Everyone would think this is great — better than gaming even. You work in chips, you're both politically correct and you can make serious money.

However, the entrepreneurship scale would tilt toward founders with industry experience. After all, whether chips or advanced manufacturing, no matter how hot it gets, it's not something any random entrepreneur can jump into.

The second variable that could shift expectations is the government's fee-cutting and tax-reduction policies. These too would have spillover effects.

If a company's value-added tax or business tax drops by 2%, that's a 2% increase in net profit. Improved profitability triggers a chain reaction. First, stronger profitability means stronger debt repayment ability, which means banks are more willing to lend to you for expansion.

Second, if you're a listed company, profit growth gets reflected in your stock performance — share prices rise, market cap grows, your fundraising capacity strengthens. Both outcomes mean companies can access more capital and have more money to invest in expanding production. This too produces spillover effects.

This is also what happened after the US tax cuts in 2018. In December 2017, the US Congress passed what was billed as the largest tax reform in 30 years. Subsequently, US economic growth in 2018 exceeded many economists' expectations, hitting 4.1% and 3.5% in Q2 and Q3 respectively.

The third variable is the smoothing of bank capital's long-term investment channels. On February 17, the China Banking and Insurance Regulatory Commission announced formal approval for Industrial and Commercial Bank of China Limited to establish a wealth management subsidiary — an important signal. Regulators are also encouraging commercial bank capital to enter market circulation, providing more compliant funding for the real economy and financial markets. This would supply more money and more liquidity to the entire market.

These three variables would interact and compound. The STAR Market drives wealth effects that spread through capital markets; tax and fee cuts boost corporate profits, showing up in financial statements and reigniting market enthusiasm; meanwhile, bank capital's long-term investment channels are unblocked. In this scenario, a market sentiment inflection occurs.

To summarize, the three key variables are: the STAR Market's launch — its smooth launch would be the first spark to ignite wealth effects; the government's tax and fee reduction policies, which may take half a year to show up in companies' operating data; and regulators unblocking bank funding for long-term investment, opening channels for bank capital to enter markets.

What Does This Have to Do with Ordinary People?

Of course, you might say, what does this have to do with ordinary people?

The answer: wealth effects gradually diffuse to ordinary people too, on one hand changing their expectations for the economy; on the other, letting ordinary people benefit from wealth growth.

Real estate, for instance, successfully accomplished this. You bought an apartment for 1 million, and five years later it's worth 5 million. This makes you feel your wealth is growing, you become more optimistic, more willing to consume. Even if you didn't buy property, you were influenced by this wealth effect. If on one side property prices are falling, and on the other you're seeing news of P2P collapses, company layoffs, US-China trade friction, and slowing Chinese economic growth — this makes you worry about the future, feel your wealth isn't growing but rather facing depreciation, and you stop consuming.

If real estate no longer plays this role of making ordinary people's wealth grow, then a thriving capital market is needed. It can let people participate in some form, generating wealth effects, making them feel their wealth is growing.

Beyond these three expectation-shifting variables, Li Feng also lists other factors that would bring positive change: on international relations, US-China trade negotiations moving in a positive direction, bringing certainty to bilateral relations; politically, 2019 marks the 70th anniversary of the founding of the People's Republic, and the celebrations around it would boost national pride; on the corporate front, beyond the mentioned tax and fee reductions, the government has been continuously giving private entrepreneurs confidence.

These things that will happen in 2019, or that people aren't yet willing to think too optimistically about but are likely to turn out well — they will compound and reinforce each other, gradually shifting public sentiment, and in turn changing the pessimistic expectations pervasive at the year's start.

And then, "once expectations turn positive, everything immediately flips."

Expectation shifts are an interesting phenomenon. Li Feng says that major expectation shifts are usually caused by consecutive expectation-beating events moving in the same direction. Take 2018: if deleveraging, US-China trade friction, the ZTE and Huawei incidents, financial regulatory tightening, and P2P collapses — if only one of these had occurred, people might not have turned so pessimistic. But these events happened in dense succession, and each one's fallout exceeded expectations. The resonance they created made everyone start adjusting their expectation dial.

Similarly, in 2019, consecutive expectation-beating events moving in the same direction could also compound and shift the pessimistic expectations from early 2019, swinging the expectations needle back toward optimism.

In sum, investor Li Feng offers a logic for viewing China's economy in 2019. In his framework, 2019 is a year of changing expectations. Three key economic-level changes could potentially shift the extreme pessimism people held at the year's start.

(This article originally appeared on the Dedao app. Feel free to share to your social media; for reprints please contact Dedao app.)