Will China's Capital Market Improve in the Second Half of 2020? (Part 1) | Li Feng Column

Asset reallocation is, at its core, a process of money making direct judgments between safety and growth potential.

Since the pandemic triggered a global financial tsunami, we've witnessed too many historic moments. When real money and silver dissolve into ethereal digits and flickering trend lines, when we repeatedly exclaim "just when you thought you'd seen it all" at the "spectacles" of capital markets, we also have no choice but to choose reason between "fear" and "greed," and re-examine this world in flux where everything awaits rewriting.

This is one reason we've been sharing our internal thinking since the pandemic began. Next, we'd like to explore a topic with you — will China's capital markets perform well in the second half of 2020?

We'll unfold this argument across two articles. The first covers changes in global capital markets since the pandemic and China's opportunities under the new landscape; the second focuses on China's capital markets themselves, reviewing three reforms from 2004–2019 and exploring who will benefit from ChiNext's registration-based IPO system.

Before diving in, here's our conclusion:

- Since March, we've witnessed global assets falling in unison while the dollar alone rose, and the arrival of the zero-interest-rate era. This series of unusual economic phenomena will produce one inevitable result: asset reallocation. This round of reallocation will likely change the previous allocation pattern — whether in asset type, regional sector, or country.

- Referencing the classic principles of asset allocation (safety and growth), the reallocation process is also money making direct judgments based on safety and growth. Places that have effectively controlled the pandemic and recovered economically will be the first to attract this capital. Based on current results, China is among the most favored contenders.

- If China's capital markets begin generating wealth effects this year due to asset reallocation, this will heat up the primary market by year-end.

We hope this offers fresh perspective. We welcome your thoughts at the end.

/ 01 / What do simultaneous asset declines, dollar strength, and the zero-interest-rate era bring?

▍Two unusual economic phenomena: "stocks, bonds, oil, gold" falling together while the dollar rises; the zero-interest-rate era

In the months since the pandemic erupted, we've witnessed two unusual economic phenomena.

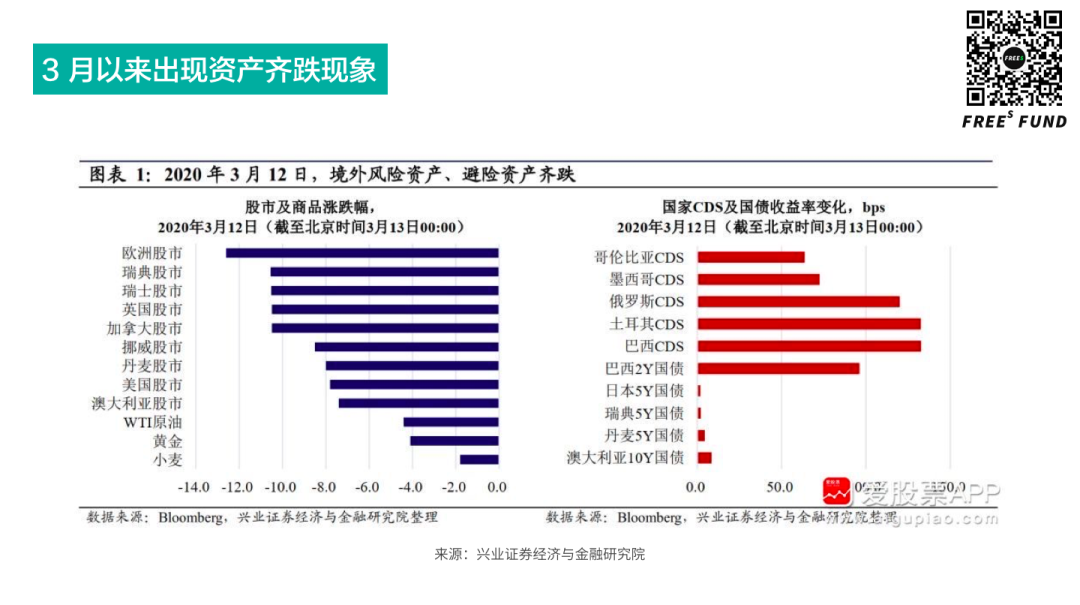

The first is the simultaneous decline of assets and solo rise of the dollar since March.

Stocks: Starting March 12, from Asia-Pacific countries like Australia, Japan, and South Korea to European countries like Germany and France, equity markets fell almost across the board. Since March 12, 11 countries' stock markets have circuit-broken due to plunges. The US alone saw four circuit breakers in March.

Bonds: Since mid-February, driven by safe-haven flows, US 10-year Treasury prices rose continuously while yields fell, hitting a historic low of 0.318% on March 9. Similarly, 10-year government bond yields in the UK, France, Germany, and others also fell to阶段性 lows. However, on March 17 US Eastern time, the benchmark 10-year Treasury yield rose to 1.062%, and from March 18 to March 26 maintained above 0.7%. This yield rise since March 17 indicates selling pressure.

Gold: Gold staged a roller-coaster of "sharp rises and sharp falls." Wind data shows that although international gold prices briefly broke through $1,700/oz on March 9, hitting a high not seen since December 2012, they subsequently plunged, falling to $1,561.8/oz on the evening of March 12.

Oil: Oil prices made history. On April 20 US Eastern time, during the final trading session of the US WTI May crude oil futures contract, prices plummeted to as low as -$40.32 per barrel, down 320%. The final settlement price for WTI May was -$37.63. This marked the first time in the 37 years since the New York WTI oil futures market opened in 1983 that crude oil futures settled at a negative price.

One could say that since March, we've witnessed the collective "nosedive" of risk assets and safe-haven assets including "stocks, bonds, oil, and gold." But the sole exception was the dollar.

According to China Securities Journal, during Asia-Pacific trading on March 19, the Australian dollar fell to 0.5511 against the US dollar at one point, a low not seen since October 2002; the British pound broke below 1.15, a low not seen since March 1985. Among emerging market currencies, the Russian ruble, Indian rupee, South African rand, and Mexican peso all hit record lows. Even the Swiss franc and Japanese yen fell to multi-week lows. On March 19, the yuan's central parity rate against the dollar was 7.0522, a more than 4-month low. Non-US currencies suffered systematic blows.

Why did this happen?

One important reason: out of pandemic-induced panic and concerns about economic "recession," people rushed to safety by selling assets for cash. And as the world's currency, the dollar saw surging demand — its appreciation was entirely logical.

The second noteworthy phenomenon is the return of the zero-interest-rate era.

The Federal Reserve suddenly cut rates sharply on March 15, lowering the federal funds rate to the 0–0.25% range. The statement said the benchmark rate would be maintained at current levels until the Fed is confident the US economy has weathered recent events and is on track toward maximum employment and price stability. To address the financial crisis, the Fed had cut the benchmark rate to the 0–0.25% range in December 2008, not raising rates until December 2015.

After the pandemic hit, the Bank of England also cut rates consecutively, lowering its benchmark from 0.75% to 0.1%. By contrast, Europe had already entered "negative rate" territory in September 2019, with the eurozone deposit rate cut to -0.5%. Like Japan, which also maintains negative benchmark rates, it had nowhere lower to go.

Zero and negative rates also mean that many central banks' interest rate stimulus tools (including rate cuts and yield curve guidance) face (or have already faced) ineffectiveness.

▍Against this backdrop, why does asset reallocation become inevitable?

What results do these two phenomena produce?

First, people converted their holdings to cash out of panic, but this cash won't be stuffed under mattresses — it will most likely sit in banks.

According to Federal Deposit Insurance Corp. data, US businesses and individuals deposited a record nearly $1 trillion into American banks in Q1, roughly double the previous quarterly record for new deposits. Data shows that a large portion of this $1 trillion flowed into banks during just two weeks in March.

China's situation was similar. In Q1 2020, GDP contracted 6.8%, while RMB deposits increased by 8.07 trillion yuan, of which household deposits rose 6.47 trillion yuan and non-financial corporate deposits rose 1.86 trillion yuan.

Commercial banks became safe harbors for panicked individuals and companies. Historically speaking, this is a rare opportunity — such massive liquidity, retreating from assets to cash.

But here's the problem. Except for China, most major countries or developed nations have bank deposit rates either near zero or negative. This means that even setting aside CPI (consumer price index), money sitting in banks basically has only one path: depreciation.

For individuals and businesses, the dilemma is: assuming I previously held many assets, and due to pandemic-induced uncertainty I sold most of them to hold cash, but holding cash not only fails to make money — it actually loses money — so I'll most likely reinvest, putting cash back on the asset allocation track to seek at least capital preservation.

Therefore, asset reallocation is almost inevitably a large-scale phenomenon. And when massive amounts of cash re-enter the asset allocation track at nearly the same time, the resulting large-scale wealth transfer will certainly have enormous impact on the economy and markets. This round of reallocation will likely change the previous allocation pattern — whether in asset type, regional sector, or country.

Everyone may have their own views on the new landscape after reallocation. The real answer may become clear in three or four months, half a year, or a year. However, we can already see some relatively explicit trends.

/ 02 / Where money flows, China is one important option

▍A recent financial market phenomenon: consensus optimism on China

In early April, Huang Qifan, former Vice Chairman of the Financial and Economic Affairs Committee of the 12th National People's Congress, published an essay titled "Global Capital Flowing to China Is a High-Probability Event; Once in a Century," sparking widespread discussion.

One of his key points: to save their economies, governments worldwide are releasing various resources and continuously injecting liquidity into markets. When massive funds enter global markets, there aren't many markets that can absorb this capital and meet return requirements. China's market currently has the best pandemic control and is the place with the smallest investment risk, so global liquidity flowing to China is a high-probability event for the coming period.

It's not just Huang Qifan. Recently you may have noticed two international finance heavyweights: one who has repeatedly cheered for China, and another who has frequently appeared in China. Yes, we're talking about Bridgewater founder Ray Dalio and Blackstone Group co-founder Stephen Schwarzman (Chinese name Su Shimin). One heads the world's largest hedge fund; the other leads a global PE giant. Their choice to increase attention on China recently isn't simply about selling books.

Recently, I also spoke with the head of a top US quantitative hedge fund, focused mainly on macro and fundamental quant strategies.

Currently they're relatively bearish on Europe, believing its economy faces major challenges, with growth and national debt issues behind it.

Compared to before, they lean toward overweighting China, mainly from two angles: sectors that wouldn't be affected even if US-China decoupling occurred; and sectors where China already has strong competitiveness.

Meanwhile, they choose to slightly underweight the US, mainly considering that US pandemic control remains inadequate, plus political uncertainty in an election year.

In my view, this person's perspective represents the genuine views of global top-tier funds, at least with considerable short-term reference value. It also indirectly explains why two financial elites whose time is extraordinarily valuable (Dalio and Schwarzman) are willing to spend so much time (livestreaming, publishing books, writing articles) making frequent appearances in China to increase their influence.

▍Classic principles of asset allocation (safety & growth) and the current "exam" (how to recover economically after the pandemic)

Why has China's position in capital markets risen currently?

Returning to the asset allocation topic, to put it plainly, asset allocation has two principles: first, high growth; second, safety. Safety is probably the first thing you'd consider, because you were just frightened by the pandemic. Once you're less afraid, you'd probably seek growth.

High growth is easy to understand — money flows to places that can bring it appreciation, that is, can make money. Stock trading, home buying, venture capital — all aim for asset appreciation, just through different paths.

If high growth means "seeking profit," then safety is "avoiding harm" — allowing assets to evade risk, circulate normally according to their original holding purpose, and not suffer any value impairment.

Among common asset types, US Treasuries and gold are for capital preservation, with lower risk coefficients; stock investment is high-risk, high-return. As people's risk-averse sentiment subsides, they gradually move from holding cash to capital preservation, then toward appreciation. In other words, investors start buying from low-risk asset categories, then buy those with growth expectations, even if risky.

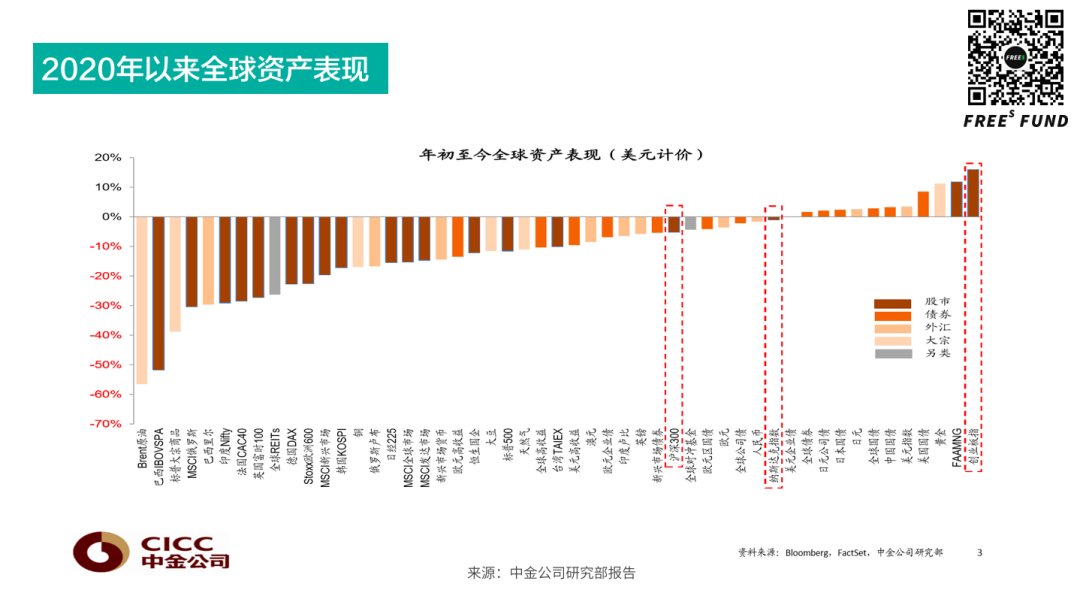

We can see that this March gold prices briefly fell below $1,500/oz, while by May 12 gold reclaimed the $1,700 threshold. Bitcoin also recovered from its March crash low of $3,800 to nearly $9,000 by May 12. This is the process of cash being reallocated to assets. Under panic, assets are sold and prices fall; as funds slowly return, asset prices rise again.

One could say that the asset reallocation process is also money making direct judgments based on safety and growth.

If we compare the pandemic to an exam, we can understand it as every country in the world receiving the same exam paper, with only two questions. The first is about safety: how does the country ensure the safety of its people and economy? The second is about growth: after the pandemic is basically controlled, how does the country stimulate and recover its economy?

In another four or five months, or within a year, we may be able to see the world's final answers to these two questions. This is an exam without standard answers; the answers won't be uniform.

What will ultimately measure the scores is money. Money will use the reallocation process to tell you who scored higher — those places that effectively controlled the pandemic and recovered economically will be the first to receive this capital's favor.

▍From the perspective of pandemic and changing international environment impacts, why China is doing better than the US

We can briefly compare the current exam results of these two heavyweight contenders, China and the US. Though the exam questions are the same, the challenges of answering them differ.

- US industrial composition: higher services sector share than China, greater pandemic impact

First, compared to the US and Europe, the pandemic's short-term impact on China is smaller. The pandemic struck during China's Spring Festival, when secondary and tertiary industries were basically shut down. However, in the US, Europe, and other countries and regions, the pandemic hit during a period of very active economic activity; sudden shutdowns cost far more.

Moreover, because pandemic control's main measure is physical isolation, the impact on services is greatest, especially gathering-related services. In economic composition, taking 2018 as an example, the US tertiary sector accounted for as much as 80%, while China's was 52.16%. Thus, the US economy is more obviously affected by the pandemic in the short term; European countries are the same.

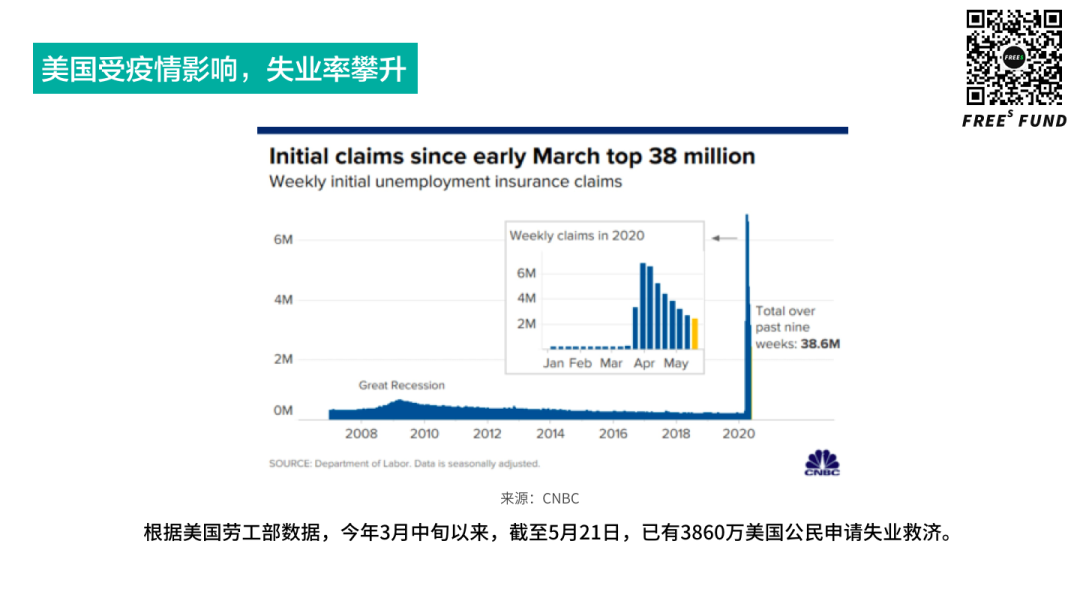

According to US Department of Labor data, since mid-March this year through May 21, 38.6 million US citizens have applied for unemployment benefits. Federal Reserve Chair Jerome Powell predicted unemployment could peak at 20%–25%.

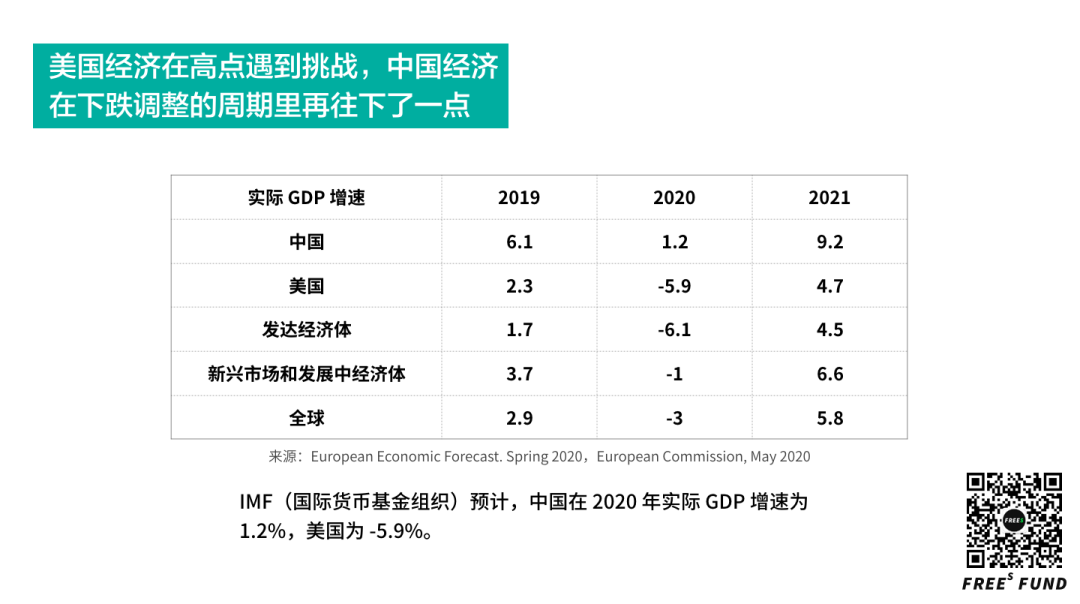

- US economy hit challenges at a high point; Chinese economy fell a bit further during a down-adjustment cycle

US stock volatility — the pandemic was merely the trigger; US economic fragility was the main cause.

First, high-yield debt and high government debt are both risk factors. Second, US stock market leverage far exceeds other markets; high leverage means when it falls, it falls fast. Also, US ETF totals are massive — in 2018, ETF assets reached $5.595 trillion, 16 times 2004's level. Once massive ETFs face redemptions, they need to continuously sell in markets and increase margin requirements, causing massive capital outflows and liquidity tightness.

Plus, the US economy had been prospering for 10-plus years, with the stock market experiencing an unprecedented bull run; the recent sudden downturn gives people a sense of frustration and anger like instantly downgrading from milk and bread to cornmeal buns. When people's emotions are continuously affected by unexpectedly bad news, they naturally choose to hold more pessimistic expectations.

By contrast, since 2015 China has been conducting economic structural adjustment — supply-side reform aimed at improving quality and efficiency — with relatively stable economic fundamentals. Hit by the pandemic, China's economy fell slightly further during its adjustment cycle, but worldwide, China experienced the pandemic first, first achieved阶段性 victory in fighting it, economic activity recovered first, and the economy will recover first, with higher certainty and safety in economic growth.

Also because the previous five years were in an adjustment cycle, China's capital markets are at a low point, with considerable room for stock and other asset valuations to rise. Moreover, having experienced the 2015–2016 stock market crash (2015 A-share "thousand-stock limit down," two circuit breakers in early January 2016), China's stock market entered negative correction logic, with less A-share margin financing; additionally, although financial derivatives have gained attention and development in China, the derivatives market and ETF (exchange-traded fund) total scale remain relatively small.

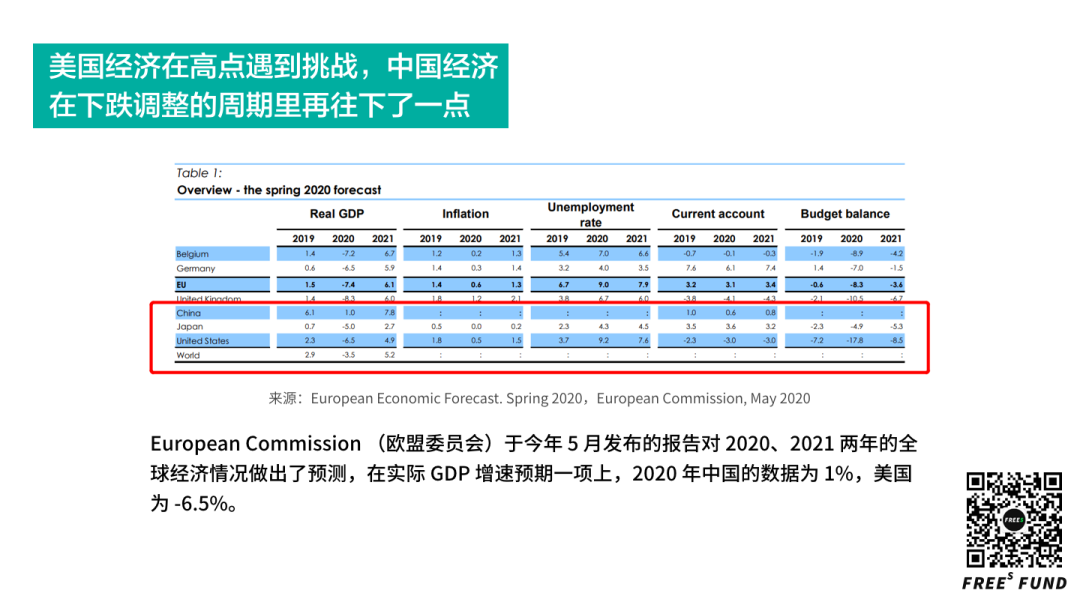

From major institutions' published 2020 economic expectations for China and the US, even though both are in "downward revision" status under the pandemic, China's situation is better than the US.

The European Commission's report released this May made predictions for global economic conditions in 2020 and 2021. For real GDP growth expectations in 2020, China's figure was %, the US -6.5%.

IMF (International Monetary Fund) economic expectations align with the EC's. For 2020 real GDP growth expectations, China is at 1.2%, the US at -5.9%.

Therefore, when people no longer want to clutch cash and return to the asset allocation track, investing in China is one rational choice — including primary and secondary markets. The former is buying stocks of Chinese listed companies; the latter is buying equity in Chinese companies.

In fact, money's voting has already begun. According to a May 13 CNBC report, Todd Willits, head of fund flow monitor EPFR, said in a late-April interview that they've found many fund managers globally have already begun reorganizing assets, with a common choice being to increase allocation to China.

EPFR data shows that as US stocks fell to three-year lows in March, over 800 funds chose to allocate nearly 25% of the nearly $2 trillion they manage to Chinese stocks. A year ago, this figure was around 20%; six years ago it was 17%.

Domestic data also confirms this. On May 14, Ministry of Commerce spokesperson Gao Feng announced at a press conference that in April, China's actual utilized foreign capital was 70.36 billion yuan, up 11.8% year-on-year. This marks the first positive growth in foreign capital utilization this year. Structurally, in January–April, high-tech industries' actual utilized foreign capital grew 2.7% year-on-year. Among these, information services, e-commerce services, and professional technical services grew 46.9%, 73.8%, and 99.6% respectively.

Of course, markets will continue changing. Assuming financial turbulence doesn't spread into a systemic new financial crisis, China's investment market improving in the latter half of 2020 is certain.

Going further, if China's capital markets begin generating wealth effects this year due to asset reallocation, this will heat up the primary market by year-end.

/ 03 /

Is China's capital market itself up to the task?

Returning to China's capital markets themselves, whether they perform well relates to three important variables: first, whether there's enough money; second, whether there are asset classes easier to profit from than capital markets or equity investment; third, policy direction.

First, the market isn't short of money. In 2019, everyone talked about "capital winter"; a major reason was that the April 2018 asset management new rules restricted banks, the largest fund-of-funds contributors. The good news is this tightened money is beginning to flow to market. Since February 2019, regulators have encouraged commercial banks to establish wealth management subsidiaries; if policy further promotes these capital flows into primary and secondary markets, it can provide more compliant funding for the real economy and financial markets.

Second, over the previous 20 years, massive money went to China's real estate industry; now real estate's wealth effect is weakening, making capital markets more attractive and beginning to play the role of growing people's wealth.

Additionally, China's policy direction is also a driver of capital market prosperity. For example, the ongoing ChiNext registration-based IPO system. Simply put, registration means that as long as there's market demand, it can be sold. Compared to the approval system with its persistent profitability standards, registration relaxes requirements for corporate profitability, focusing more on growth potential and development space — meaning the bar for companies to go public is lowered considerably.

To add: even with lower listing barriers, full competition will ultimately prevail. In the long run, great companies are all good companies.

With registration's launch, the RMB investment market situation is: STAR Market on the left, registration on the right. Taking a longer view, both will bring wealth effects, thereby attracting money into capital markets. The likely sequence: first concentrating in secondary markets, then gradually entering primary markets.

▍Preview

In tomorrow's second installment, we'll focus more closely on China's capital markets themselves, reviewing three reforms from 2004–2019 and exploring which companies will benefit from this round of deepened capital market reform. Advance notice — stay tuned.

Summary of this article

1. When group panic subsides and global funds urgently need reallocation, considering factors like high growth and safety, Chinese assets will become one of the more welcomed targets.

2. If China's capital markets begin generating wealth effects this year due to asset reallocation, this will heat up the primary market by year-end.

3. No one can escape the currents of the era. Whether you're optimistic or pessimistic, those skilled at running will certainly find their own ladder amid uncertainty, seeing opportunities and benefiting from them.

Discussion Question

Q: The pandemic unexpectedly pushed China to center stage internationally, while the US, preoccupied with its own troubles, didn't play the global leader's role. How do you understand the post-pandemic world? Will China and America's international influence change? Will the world move toward multipolarity?

Welcome to hit "Like" at the end, and reply "influence" in the official account backend to get our preliminary answer.

Also welcome to share your views in the comments section. By 21:00 on June 1, the 6 readers with the most thoughtful comments will each receive a copy of Why the West Rules—For Now. This book will take you from a broader, more diverse, more scientific perspective to examine why we've arrived where we are today and where we're headed; with the current pandemic, this book may help steady your nerves.

(Welcome to read, share, and hit Like. For reprint permission, please reply "reprint" to understand reprint rules, and contact FreeS Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

The Hammer and the Dance: Investment Opportunities in Healthcare's Next Wave Amid the Pandemic | Frees Fund Why Is New Infrastructure the Most Impactful Stimulus Policy for China's Next 10 Years? | Li Feng Column One Chart to Understand Changes and Opportunities in China's Industrial Chain | Li Feng Column On Chinese Manufacturing, What Did Minister Miao Wei Actually Say? | Frees Fund One Chart to See Globalization or Deglobalization | Li Feng Column After the Pandemic, the New Era of "Good Companies" | Frees Fund