Li Feng's 2021 Outlook: How We See China's Present and Future

Steady progress toward enduring success.

Farewell to the Year of the Rat, when we "kept witnessing history," and welcome to the Year of the Ox, filled with hope. So what will be different about 2021? What opportunities and challenges will it bring? And what posture will we adopt as we step into this new current?

On the first workday of 2021, we share with you the third installment of the "FreeS Fund 2021 Outlook" series. Key points:

- A major opportunity in 2021: systemic uncertainty is shifting toward relative certainty. Greater inner certainty breeds optimism and tilts people toward longer-term decisions — in consumption and investment alike — driving economic recovery and creating more opportunities.

- In 2020, domestic internet giants faced internal and external challenges, from international expansion to antitrust pressure. These challenges will push them to adjust their behavior and shoulder more social responsibility. This may open up more room for startups to grow and accelerate the普及 and deep application of technology.

- Risks lie mainly in the financial realm. To combat the pandemic, central banks worldwide adopted zero or negative interest rates and created massive liquidity. Unlike 2008, many countries printed too much money too quickly this time, without a huge overhang of damaged underlying financial assets needing repair. The result: a stock market party before the economy has recovered. These anomalies will eventually be corrected. When and what triggers it remains hard to judge. But if and when adjustment comes, developed markets like the U.S. will likely feel the impact earlier and more severely than China.

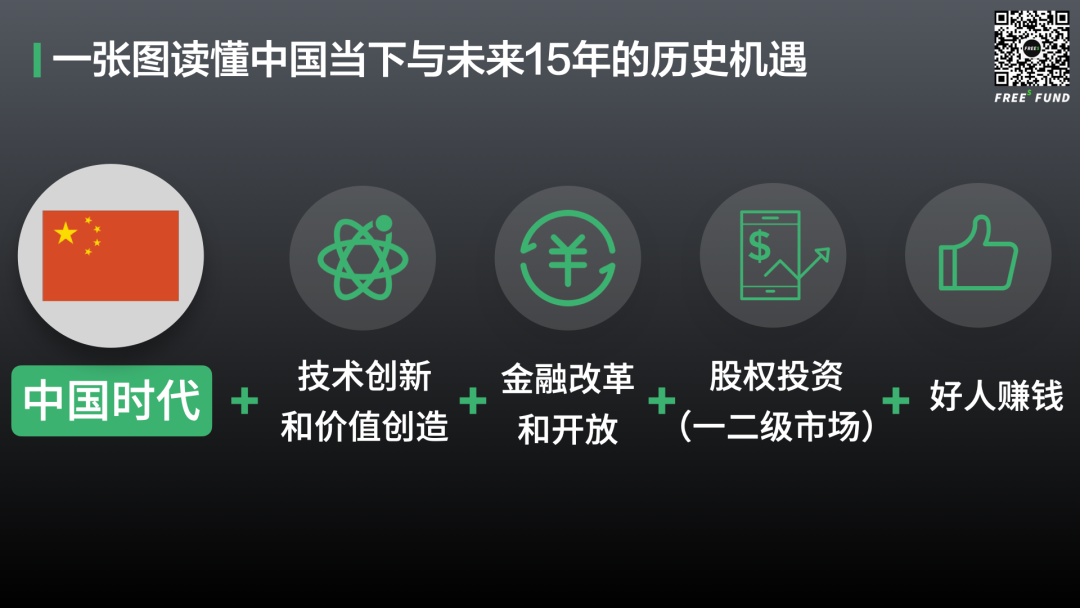

- Specifically for China, the next 15 years belong to the country. Post-2020, we can see: technological innovation and value creation have become the defining themes of the era; financial market reform proceeds steadily, with deepening openness that will become irreversible over time, benefiting domestic enterprises; and the comprehensive optimization of multi-tier capital markets has raised the share of direct financing, improved financing structures, and significantly enhanced capital markets' ability to serve technological innovation and the real economy. The convergence of these factors opens an entirely new historical window of opportunity. Without question, this is an era where good people make money.

Below is the detailed analysis. We hope it offers some food for thought, and we welcome ongoing dialogue.

Contact Us & Join Us

FreeS Fund continues to track investment opportunities in consumer, hard tech, and biopharma. Pitch decks welcome at bp@freesvc.com, or reach out to Feng Xiaorui on WeChat (ID: freesfund).

We're hiring investors in biopharma, deep tech, and consumer/TMT across Beijing, Shanghai, and Shenzhen. Candidates with industry backgrounds and an interest in investing — full-time or internship — are welcome. Referrals appreciated too: hr@freesvc.com (resumes encouraged).

/ 01 / Three Major Shifts in 2020, and What Will Be Different in 2021?

From "Uncertainty" to "Relative Certainty"

From 2019 to 2020, everyone was constantly "witnessing history." We were forced to accept and gradually adapt to massive uncertainties: domestic economic restructuring, shifts in U.S.-China relations, the sudden pandemic, and more.

Entering 2021, one change is underway — these systemic uncertainties are moving toward relative certainty.

On the pandemic: while the world is currently experiencing resurgences, the accumulated experience in containment, expanding vaccine coverage, and ingrained public health habits collectively suggest that pandemic-induced uncertainty will likely diminish in 2021.

On China's economic structure and growth: we can roughly delineate a cycle. From Q4 2015 through the pre-pandemic period, China was in a sustained "deleveraging cycle." The 2020 outbreak prompted policy adjustments. But by the final three months of 2020, most major macro indicators had turned positive.

On U.S.-China relations: the Biden administration has taken office. Compared to its predecessor, "establishment" governance will likely reduce uncertainty in U.S. global political and economic policy, potentially stabilizing U.S.-China relations. On January 29, 2021, Reuters reported that the Biden administration would reassess the Phase One trade deal, suspending additional tariffs on $370 billion in Chinese goods during the review period.

On the international situation: you may recall that in the spring of 2020, a heated debate erupted over whether supply chains would move out of China. Our position was clear: China's supply chains would not be damaged but would actually benefit. (Click to read "One Chart to Understand Globalization vs. Deglobalization | Li Feng Column")

By August-September 2020, this was no longer controversial. We all saw that supply chains did not relocate en masse. Instead, China's long and complete supply chains helped solve problems for the world during the pandemic.

Two key data points illustrate this:

On November 30, 2020, the National Bureau of Statistics released China's November 2020 Purchasing Managers' Index (PMI). The manufacturing PMI came in at 52.1%, up 0.7 percentage points from the previous month, marking nine consecutive months above the threshold and the fastest recovery growth — the highest reading in 38 months since October 2017.

On January 14, 2021, China Customs data showed that December 2020 exports grew 18.1% year-over-year, with full-year growth at 3.6%. Export strength pulled export-related manufacturing sectors into faster recovery.

In sum, we believe the single biggest shift as 2020 ended was this: the massive uncertainties we had been forced to accept over the past two years were mostly beginning to move toward relative certainty.

Relative Certainty Changes Expectations and Psychology

Our psychology doesn't flip overnight with a few macro data points, but it does shift gradually.

In early 2020, at the pandemic's height, National Bureau of Statistics data showed China's total retail sales of consumer goods plunged 20.5% year-over-year in January-February. This likely reflected how extreme uncertainty leads people to avoid or postpone long-term decisions — in consumption and investment alike, from home and car purchases to business expansion.

Per preliminary full-year 2020 GDP data, quarterly year-over-year growth was -6.8%, 3.2%, 4.9%, and 6.5% respectively. Growth recovered steadily, with full-year GDP up 2.3%. As quarterly GDP growth climbed through 2020, expectations for Q1 2021 likely improved.

Meanwhile, seeing previously uncertain factors — the pandemic, international situation, China's economic restructuring, U.S.-China relations — gradually stabilize, you gain inner certainty and tilt toward longer-horizon decisions. This is a shift likely to occur in the first two quarters of 2021, potentially affecting investment and financing as well as personal wealth allocation in equities and real estate.

The data bears this out. Two November 2020 figures were particularly telling. Private investment growth turned positive for the first time that year, up 0.2% in the first eleven months. High-tech industry investment grew 11.8%, with high-tech manufacturing and services up 12.8% and 10% respectively.

The return to positive private investment growth and double-digit high-tech manufacturing investment reflect restored business confidence in industrial and long-term investment. This will also provide meaningful momentum for domestic economic development in 2021.

Liquidity (Money), Investment, and Valuations

Two unusual phenomena marked 2020: First, amid turbulent U.S.-China relations, Chinese companies listed in the U.S. raised the most capital there; Second, the U.S. printed more money in the past year than at any point in history.

How much more? Let's use the 2008 financial crisis as reference. Before 2008, the Federal Reserve's balance sheet was relatively stable at around $800 billion. By around 2015, post-crisis, it had reached roughly $4.5 trillion.

From 2015, the U.S. exited its rate-cutting cycle and entered a hiking cycle, working to "shrink" its balance sheet. Per a prior New York Fed report, a $4.5 trillion balance sheet might need five years to reach "normal" levels. The Fed's balance sheet peaked at $4.5 trillion and was once shrunk to $3.8 trillion by 2019.

But the pandemic hit during this shrinking process. Through asset purchases and credit easing, the Fed created enormous liquidity. By end-October 2020, its balance sheet had surged past $7 trillion — expanding faster than during the 2008 global financial crisis.

The same thing happened last time: massive money printing alongside ultra-low rates.

But this time is different from the financial crisis in two key ways:

First, the money was printed too fast, in too short a time. Second, during the financial crisis the financial system itself was deeply broken — much of that money went to buying bad debt and toxic assets. This time around, there is no massive pile of underlying financial assets that need fixing. So the nearly $4 trillion in newly printed money went searching for returns wherever it could find them.

Let's briefly trace how this money flowed.

The first wave came in late March 2020. Gold, US stocks, US bonds, Bitcoin — nearly every asset class on earth fell in unison. Only one thing held up: the dollar. As the world's reserve currency, most investors treated it as a safe haven. While US stocks triggered circuit breakers four times in ten days, the dollar index rose for ten straight days, breaking above 100 on March 18 for the first time since April 2017. The whole point of printing money was to stimulate the economy, but mass panic led investors to dump everything and hoard cash.

By April 2020, the dynamic shifted. With nearly $4 trillion in newly minted dollars earning nothing for too long, investors gradually adapted and emerged from panic. The money began flowing back into risk assets. Over the following months, despite weak US economic data, capital markets surged — especially the stocks of a handful of leading companies.

The same thing happened after the financial crisis. In late 2010, the Federal Reserve launched its second round of quantitative easing, and US stocks climbed steadily. Once the Fed had printed enough money to repair the financial system's fundamentals, people gradually shed their fear and moved into risk assets for higher returns.

Why did leading stocks perform so well last year? One major reason: people tend to seek relative certainty amid broad uncertainty. These leading companies were that relative certainty. Even if hit by the pandemic, they would suffer less than others — and might even benefit.

In China's domestic market, one symbol of "relative certainty" was Moutai. During the 2020 outbreak, Moutai's stock fell from around 1,100 yuan per share to 993 yuan on March 19, 2020 — then climbed steadily to become the most valuable stock on the A-share market.

Will this trend continue forever?

Obviously not. Whether it's massive money printing in a short period or a stock market frenzy while the real economy hasn't recovered, these are unsustainable phenomena. Unsustainable phenomena eventually correct. When and what triggers it remains hard to predict, but it will happen.

Although foreign financial institutions have gained ground in China as the country gradually opens its financial sector, we have not yet liberalized the renminbi's free convertibility in capital markets. So when the correction comes, developed markets like the US will feel the impact earlier and more severely than China.

So compared to the first two macro factors trending positive — the move toward "relative certainty" and the shift in expectations and psychology it brings — the massive liquidity unleashed during the pandemic is more like a sword of Damocles.

From an investor's perspective, a major challenge right now lies in valuation logic.

When vast sums flow into ever more risk assets, they inflate those assets' values, and bubbles inevitably form. So we've constantly reminded ourselves internally: we cannot use Chinese concept stocks' current market performance as the basis for our investment valuation logic. We can't say that because Company A is worth $50 billion post-IPO, and Company B is 1/100th its size, it should be worth $500 million.

From entrepreneurs' perspective, though, when money is flowing into China and capital markets are white-hot, founders may be able to raise more money — a temporary tailwind.

02 How Do We See the Present and Future? The Next 15 Years Belong to China!

Returning to China, where we live, a question we all care about: where is China headed, now and in the future?

My preliminary conclusion: the next 15 years belong to China, and 2021 marks the beginning of a critical historical window.

Why 15 years?

Assume China maintains moderate growth (in recent years, China's GDP growth has stayed above 6%, while US GDP growth has ranged between 1-3%). Using a 5% growth estimate, in 15 years China's economy would roughly double in size.

Right now, our per capita GDP has crossed $10,000. Doubling that means per capita GDP exceeding $20,000 — placing China in the developed-nation camp.

That sounds distant. Indeed, in recent years there has been much debate about whether China will fall into the middle-income trap. The logic: with $20,000 per capita GDP as the threshold, crossing it or reaching just above it makes you developed; failing to cross leaves you middle-income.

But with a reasonable 5% growth assumption, China could reach developed-country status in as little as ten years, or at most 15.

Of course, there are shorter timeframes. In 2020, our GDP reached 100 trillion yuan, about 70% of US GDP. Even without our 5% moderate-growth assumption — using the US's 1-3% GDP growth instead — it won't take 15 years for our GDP to surpass America's.

Setting predictions aside, looking just at the past year and the start of 2021, we've already seen remarkably encouraging data: China is the only major economy to maintain positive growth, GDP crossed 100 trillion yuan, and our industrial structure continues climbing and adjusting.

In the coming 15 years, being rooted in China represents one of the best historical opportunities we can identify anywhere in the world. We happen to stand at the center of this opportunity.

In the China era, we see multiple favorable factors converging.

Technological Innovation and Value Creation: The Defining Themes of the Era

From the emergence of township and village enterprises around 1984, we spent nearly 40 years to become the world's largest manufacturing value-added country by 2010, a position we've held ever since. (For more on how China's industrial structure and scale have evolved over the past 40 years, see "One Chart to Understand Changes and Opportunities in China's Industrial Chain."). Put simply, China's industrial chain climbed from low-value-added raw materials, to low-value-added processing, step by step to the final two links: high-value-added products and industrial goods, and high-value-added services.

The smartphone and home appliance smart manufacturing industries that rose in recent years, and the new energy vehicle industry that has been hottest over the past six months, are representatives of high-value-added products and industrial goods. Social and cultural content products that sell no physical goods, and the financial industry, are typical representatives of high-value-added services.

As we optimize our industrial chain structure and concentrate our efforts on conquering these final two links, we must raise value-added. Our current industrial value-added ratio has just crossed 20%, while in countries like the US, Germany, and Japan it ranges between 30-40%. Raising value-added necessarily requires technological innovation and value creation.

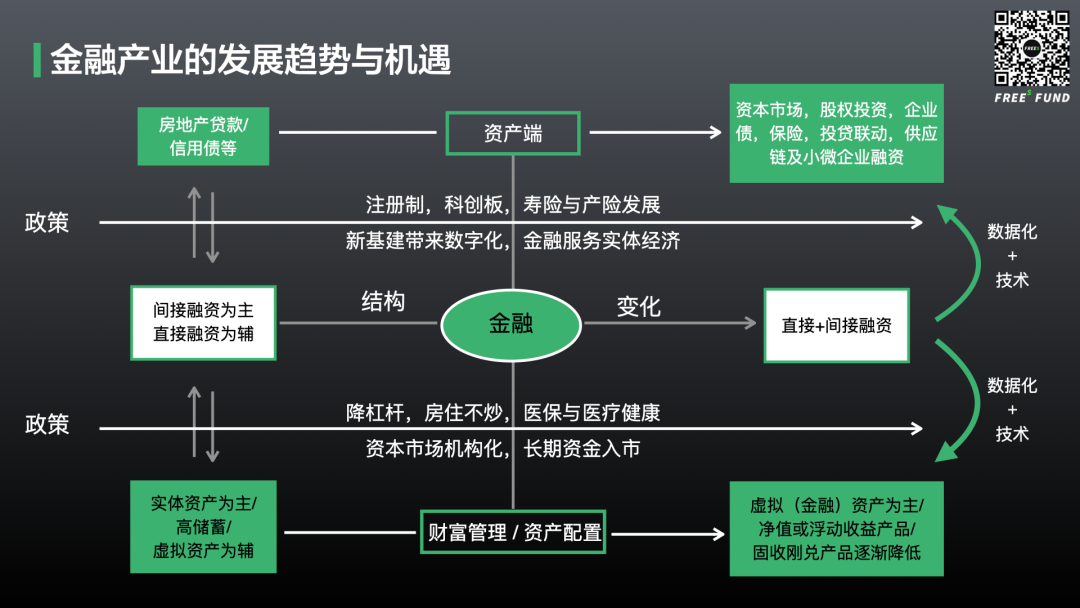

Financial Market Reform and Opening

As we climb toward the final two links of the industrial chain, finance — the faucet that supports economic transformation — is undergoing two simultaneous changes: reform and opening.

A key direction of financial reform is shifting from a system dominated by indirect financing with direct financing playing a supplementary role, to one where direct and indirect financing are both primary.

Before 2018, China's total social financing scale增量 remained below 20 trillion yuan, with bank-loan-dominated indirect financing in the leading position. 2020 was an exceptional year: China's total social financing scale增量 broke through 30 trillion yuan, with direct financing's share rising to 13.68 trillion yuan, growing at an average rate of 39% — faster than the overall total social financing增量 growth rate.

Indirect financing was a product of the horizontal expansion era. When developing the earlier links of the industrial chain, our method of growing bigger and stronger was horizontal expansion: one factory became two, then five to ten. We could easily calculate the returns from this kind of scale expansion, and banks could easily extend loans accordingly.

When we enter the stage of developing high-value-added products/industrial goods and services, the path to growing bigger and stronger becomes increasing talent density and raising value-added. No longer through simply adding factories and fixed investment, the old loan model no longer applies. For example, Huawei has only a handful of factories but nearly 200,000 employees globally — its total value-added isn't calculated as 10,000 people times twenty.

Vigorously developing direct financing supports innovation and entrepreneurship, and drives technological innovation and value creation.

Alongside reform, China is gradually opening its financial markets to the outside world. Although there was the recent disruption of Ant Group's suspended IPO, we remain optimistic about financial market opening.

Our optimism stems from summarizing historical patterns. Over the 40-plus years of reform and opening, every major industry — manufacturing, real estate, urban distribution, and so on — has experienced opening to the outside and opening to the inside. The outcomes have been remarkably encouraging:

- Once opening begins, it doesn't stop.

- Looking back twenty years after an industry opens up, the best-performing and strongest companies in those industries are almost always private enterprises. (Click to revisit "Li Feng's Column 13: China Is at Its Most Precious Historical Moment")

To get specific about the financial industry: on June 28, 2018, the National Development and Reform Commission and the Ministry of Commerce released the Special Administrative Measures for Foreign Investment Access (Negative List) (2018 Edition), removing foreign ownership caps for banks and financial asset management companies and treating domestic and foreign capital equally. For securities firms, fund management companies, futures companies, and life insurers, the foreign ownership ceiling was raised to 51%, with no limits after three years. By 2021, that three-year period is nearly up, and financial opening will only deepen. In the long run, domestic companies will certainly benefit.

Equity Investment (Primary and Secondary Markets)

Equity investment, as one of the typical forms of direct financing, will benefit from this financial reform and opening regardless of whether we're talking about the primary or secondary market. Taken as a whole, the "China era" may mean tens of trillions of RMB in opportunity every year for the coming decade.

In 2020, China became the only major economy to achieve positive growth. As China's economy recovers, fiscal stimulus and spending in 2021 may not match last year's levels, but as China's financial markets reform and open, global capital will continue flowing in from every direction.

On another front, 2020 saw China advance structural adjustments in capital market financing, achieving "dual expansion" in the inclusiveness and coverage of direct financing: from the gradual rollout of comprehensive reforms to the NEEQ (New Third Board), to the first batch of NEEQ Select Layer companies beginning trading, to the ChiNext registration-based IPO reform taking effect, to NEEQ-to-board transfer rules being finalized... The comprehensive optimization of China's multi-tiered capital market has increased the proportion of direct financing, improved financing structures, and significantly enhanced the capital market's ability to serve technological innovation and the real economy. The wealth effect in secondary markets will also motivate more active participation in primary market investment.

Putting this all together, the convergence of these factors in 2021 will open up an entirely new historical window of opportunity.

The Era When Good People Make Money

With the spread of the internet, data and information circulate with unprecedented ease. Communication between people, and between people and information, has become ever more efficient. Making money from information asymmetry is getting harder, while "good people" who genuinely create value — those more durably recognized by their industry, by the market, and by the users they serve — are finding it easier to succeed. Hence our phrase: "good people make money."

03 New Year's Message: Steady Progress for Lasting Success

In January and February of last year, we were busy fighting the pandemic (click to revisit "Mobilizing Against the Novel Coronavirus: Our Actions and Call to Action | FreeS Fund") while adapting to the changes it brought. At that time, many of us — myself included — underestimated the severity of the outbreak. What happened next, we all saw: COVID-19 spread globally, social distancing became the defining phrase of the year, and masks seemed to become a second skin.

Over the past year, the venture capital world we inhabit has also seen many changes. The pandemic accelerated failure and catalyzed success. As an early-stage investment firm, what we observed in the founders of our portfolio companies was this: finding opportunity in crisis, growing toward the light; staying true to original intentions, ideals intact, continuing to strive.

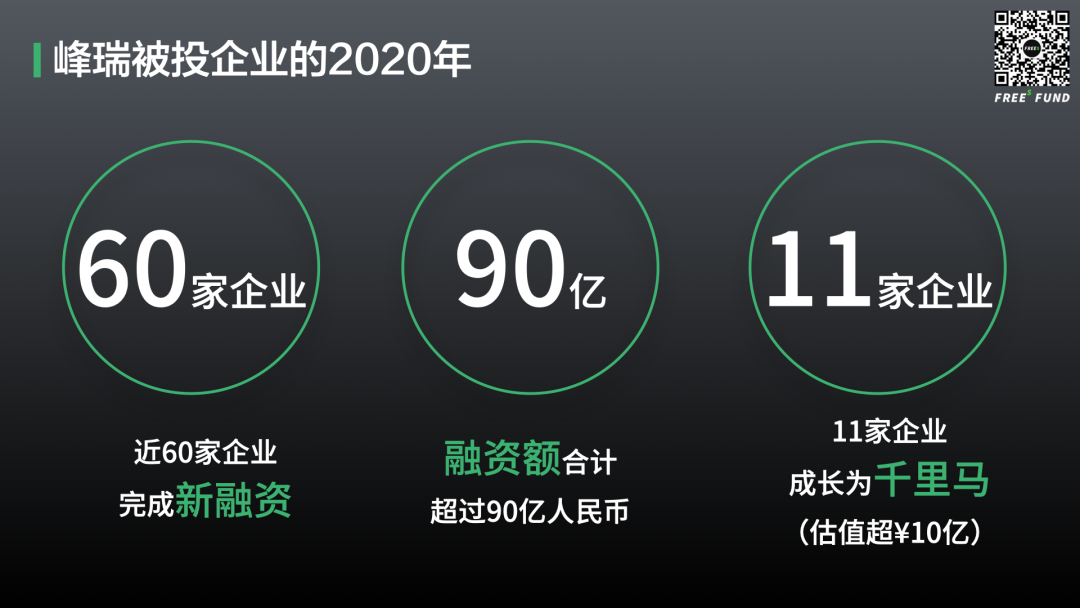

Despite the difficulties of the past year, preliminary statistics show that nearly 60 FreeS portfolio companies completed new funding rounds in 2020, with total raised exceeding 9 billion RMB. During this year, 11 portfolio companies grew into "thousand-li horses" (valued above 1 billion RMB), many of them in biotech and pharmaceuticals. Seeing companies in this widely acknowledged longest-growth-cycle sector begin to emerge in 2020 was especially gratifying for us.

For FreeS itself, 2020 saw us complete the oversubscribed final closing of our RMB Fund II. Beyond our early-stage fund, we now also have a growth fund for continued follow-on investment in portfolio companies. Additionally, we established tech-focused angel investment funds in Shenzhen and Shanghai. In 2021, we will begin planning and establishing RMB Fund III.

Despite significant capital market volatility over the past year, we maintained cautious optimism, investing in 43 projects — 18 follow-on investments in existing portfolio companies and 25 new investments. Our investment areas span consumer, hard tech, and biotech/pharmaceuticals; we also actively deployed in cultural entertainment and financial services, sectors that had frozen over in the primary market, and hope to walk alongside more outstanding entrepreneurs in 2021.

We have reason to believe that 2021, however difficult, should not be harder than 2020. Based on this judgment and outlook, we are expanding our investment team. Recently, we have been seeking investors focused on biotech, deep tech, and consumer/TMT in Beijing, Shanghai, and Shenzhen. We welcome those with industry backgrounds and an interest in investing to join us (hr@freesvc.com), whether full-time or as interns, and welcome referrals of outstanding candidates.

The Book of Rites · Biao Ji has a saying: "Be careful at the beginning and respectful to the end; proceed steadily to go far." This has resonated with me lately.

As mentioned earlier, looking ahead fifteen years will be a crucial period of opportunity for China. As an early-stage investment firm founded in 2015, we too are experiencing cycles in the financial industry. In this industry, we don't seek overnight riches — we seek to be good people, to proceed steadily and go far.

FreeS has always been committed to discovering and creating value; finding value is our capability and our joy. The most important thing is not to rush, but to take each step well. China is entering fifteen years of tremendous prospects, and the opportunities in our industry are substantial. As long as we improve each year over the last, as long as we keep growing, in fifteen years we will certainly realize the value we should. It is this process of continual growth (长, zhang) that will achieve lasting (长, chang) vitality.

So, a final word — to ourselves, and to all of you: be good people, discover value, drive innovation, stand firm in finance, win in China, and proceed steadily to go far!

▲ FreeS 2021 Outlook ② | Three Trends in Biomedical Innovation

▲ FreeS 2021 Outlook ① | Eight Trends in Consumer Entrepreneurship

▲ How New Platforms Are Born, in One Chart | Li Feng Column

▲ Four Reforms of China's Capital Market, 2004–2020: Who Benefited in the End? (Part 2) | Li Feng Column

▲ Will China's Capital Market Improve in the Second Half of 2020? (Part 1) | Li Feng Column

▲ Why "New Infrastructure" Is the Most Consequential Stimulus Policy for China's Next Decade | Li Feng Column

China's Industrial Chain: Changes and Opportunities, in One Chart | Li Feng Column

Globalization or Deglobalization, in One Chart | Li Feng Column