FreeS Fund 2021 Outlook ① | 8 Trends in Consumer Entrepreneurship

Where were the innovation opportunities in consumer-facing sectors in 2021? What kind of companies could break through?

FreeS Fund's 2021 Outlook

2021 will be the year when things start shifting from "uncertainty" toward "certainty."

The systemic uncertainties that kept us on edge for the past year — the pandemic, US-China relations, and the international landscape — have begun to stabilize in recent months. Having weathered the storms of 2020, we are now poised for our moment to strike in 2021.

In the coming weeks, we will publish a series of articles reviewing 2020's venture capital and investment hotspots (covering consumer, macroeconomics, biotech, and hard tech), mapping out the directions and sectors we are bullish on, and the future trends we see emerging. The point of looking ahead isn't to predict the final outcome — it's to maintain a state of constant thinking and forward momentum.

2021 won't be easy, but it shouldn't be harder than 2020. Together, with our ticket to China's era of opportunity in hand, let's discover value, drive innovation, and move steadily toward long-term success.

In consumer, there has never been a shortage of new stories — and 2020 was no exception.

Even as the consumer market entered a phase of zero-sum competition, we witnessed an "explosion of new species" among consumer brands. 2020 was also an inflection point for the digitization of services, with the migration of services online becoming increasingly pronounced. In contrast to the heat in consumer and services, entertainment investment dropped to a freezing point in 2020. Yet we see users' spiritual consumption demands entering a period of explosive growth, and new technologies are making entertainment more diverse than ever.

Overall, the structural shifts in consumer in 2020 were driven by two core variables: technology and traffic. These same factors will be critical in shaping market development in 2021 and beyond.

In this article, we focus on breaking down the opportunities across three directions — consumer products, entertainment, and services. Here are our preliminary conclusions:

- Four new opportunities in consumer product reinvention:

Supply chain technology upgrades are giving new brands more room for innovation. Shifting traffic patterns and increasingly precise distribution algorithms on traffic platforms are making it easier for brands to go "from 0 to 1." The dividend period for video and live-streaming platforms hasn't ended. Offline brand renovation and new consumption scenarios also create favorable conditions for new brands to rise.

- Three opportunity points in entertainment:

New traffic and new demographics are embracing new social tools and new content. The emergence of new technologies is driving computing platform upgrades, thereby spawning new forms of entertainment. Interaction modes are expanding from entertainment into commerce.

- Services upgrading hits an inflection point:

Digital tools are elevating the degree of standardized service in industries, while online entry points are helping brands and consumers build longer-term connections.

We hope this offers fresh perspectives. You're welcome to reach out to the author, Xiao Yang, for further discussion (yangxiao@freesvc.com).

Contact Us & Join Us

FreeS Fund continues to pay close attention to investment opportunities in consumer. We welcome business plans sent to bp@freesvc.com, and you can also reach out to Feng Xiaorui (WeChat ID: freesfund).

FreeS Fund is currently seeking investors in biotech, deep tech, and consumer/TMT across Beijing, Shanghai, and Shenzhen. We welcome candidates with industry backgrounds and an interest in investing — both full-time and internships — and we also welcome referrals of outstanding candidates to hr@freesvc.com (resumes encouraged).

Four Opportunities to Reshape Consumer Categories

Throughout 2020, the consumer sector was exceptionally hot. Many people said every industry has a chance to be rebuilt. So where are the opportunities to reshape consumer categories in 2021? I see four main areas: supply chain and technology innovation, new traffic, offline brand renovation, and brand opportunities from new consumption scenarios.

First, seize the opportunity for new domestic brands born from supply chain technology.

Chinese manufacturing's supply chain capabilities have earned the recognition of a new generation of consumers on quality. This generation, born into the internet, also has strong identification with domestic brands — an unprecedented cultural confidence. These two factors together solve the two most important elements for a brand's launch: confidence in quality and confidence in culture.

With quality confidence and cultural confidence as our foundation, where do we look for new domestic brands? We still need to look at the普及 of new supply chain technologies and their联动 optimization with industrial chains.

Saturnbird (三顿半) and Xinliangji (信良记) are examples we've cited many times. Whether it's Saturnbird's freeze-drying technology or Xinliangji's liquid nitrogen quick-freezing technology, both were originally applied in other industries before being普及 to new sectors and fields. In the process of普及, they were optimized and adjusted, bringing product and experience upgrades to these new industries — better flavor还原, more convenient usage.

Taking existing technologies, carefully adapting and upgrading them for new products and categories, and achieving industrialized production — this represents a major wave of opportunity for consumer category reinvention.

Next, I'll use three industries — cosmetics, health supplements, and small home appliances — as examples to show how supply chain upgrade opportunities unfold.

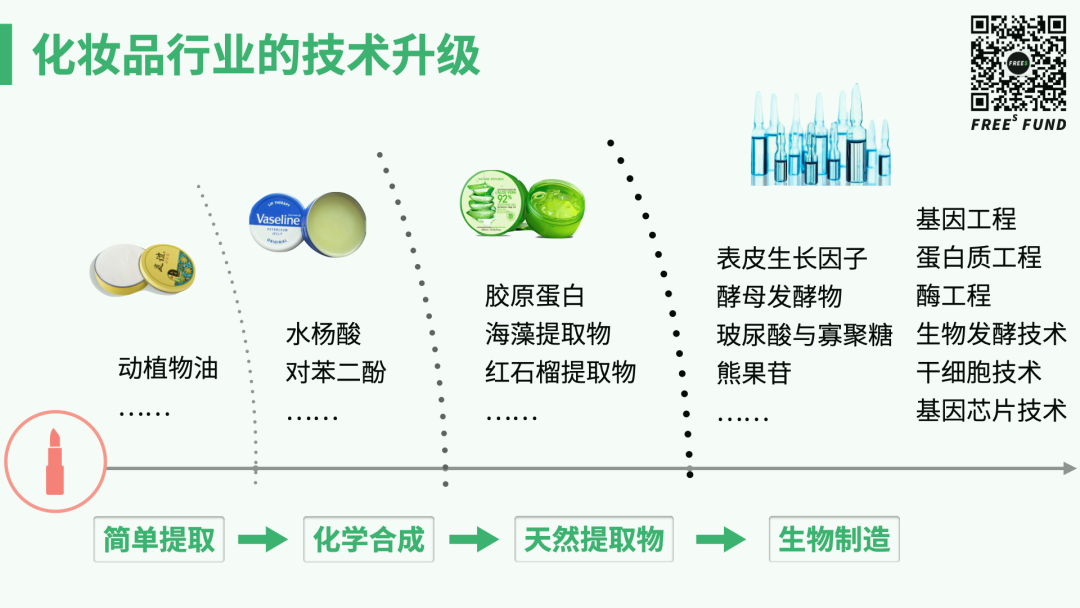

The technology used in cosmetics has advanced from simple extraction to chemical synthesis to natural extracts. The current upgrade underway is a shift toward biotechnology applications. This upgrade in the technology itself may give birth to new brands.

This type of bio-plus-consumer interdisciplinary project is something FreeS Fund hopes to focus on going forward. Because we believe that innovation today is almost entirely cross-disciplinary, and breakthrough innovation mostly happens at the intersection of disciplines.

The logic for health supplements and small home appliances is somewhat similar.

Many health supplements now have better efficacy or use new ingredients, and in the process of technology upgrades, they also satisfy consumers' emotional needs.

If the supply chain upgrade in cosmetics is a natural evolution, the upgrades in health supplements and small home appliances are more like dimensional reduction strikes — technologies previously restricted to strict usage scenarios are being brought down to more everyday contexts. For example, pharmaceutical-grade ingredients being applied to health supplements, or equipment previously used in beauty salons becoming available for home use. This allows more people to enjoy these previously "more advanced" technologies at lower prices and for longer periods, creating opportunities for new brands.

For example, contact lenses, as Class III medical devices with relatively high risk, are showing a trend across demand, supply, and distribution channels from medical product to consumer product, and from consumer product to fast-moving consumer good. In this赛道, FreeS Fund invested in Tongxue (瞳学), a contact lens company whose brands include Kilala (可啦啦) and Mitata (米塔塔). Since May 2020, Tongxue surpassed Hydron and Bausch & Lomb to become the #1 brand in colored contact lenses online, and it currently also ranks #1 in both long-cycle and short-cycle disposable lenses online. (Click the link "Galaxy in Your Eyes: Understanding the Rise of Colored Contact Lenses in One Chart | FreeS Research Institute" to read our thinking on the colored contact lens market.)

To summarize, the new brand opportunities from supply chain upgrades fall into three main categories: cross-industry普及 of existing technologies creating new opportunities; supply chain upgrades within an industry itself; and dimensional reduction application of technology.

Second, seize traffic shifts to build new brands.

During the last mobile internet boom, traffic was concentrated in the hands of a few internet giants. The rise of short-video platforms, lifestyle-sharing platforms, and live-streaming platforms has redistributed traffic from a few dominant players to several smaller oligopolies. We call this trend "the decentralization and recentralization of traffic." (Click the link for our thoughts on traffic shifts and the birth of new platforms: Is the Internet Destined to Have a Next New Platform? | FreeS Research Institute)

If traffic is too fragmented, building brands becomes difficult; if it's entirely concentrated, brand-building is also tough. The current situation — where different traffic platforms compete against each other — forces them to open up. And it's in this open environment that brands have more opportunities.

The distribution logic of traffic platforms gives brands a precise starting point. Today, AI + big data recommendation algorithms have lowered customer acquisition costs for brands searching for their target customers at the earliest stage. Whether through new media or private-domain traffic, brands can reach their target users more easily than ever before. This is undoubtedly favorable for brands going "from 0 to 1" — you can find your users at lower cost and iterate your product quickly. (Click the link for our thoughts on how traffic trends affect timing for entrepreneurs: FreeS Fund's Li Feng: From 0 to 1 Is Easy for Consumer Brands, From 1 to 10 Is Hard | 10/31 Closed-Door Registration)

Additionally, the rise of content platforms has created new development opportunities for consumer brands. Even without a large budget, you have a chance to blow up from a single viral piece of content — a crucial change in the overall ecosystem.

This is platform dividend. Content platforms always start with entertainment-heavy content, then gradually transition to knowledge-based content — which greatly benefits brand-building. In other words, explanatory content suits brand-building. First, you can tell brand stories; second, you can explain the relatively complex, need-to-understand aspects of your product. For example, why is a particular supplement effective? What are the nuances of selecting red wine?

FreeS Fund's 2020 investment, Paperclip, excelled at explaining complex principles through video. How did COVID-19 emerge and spread? What's freeze-drying technology, the kind used in Saturnbird's coffee? What are the underlying logics of artificial intelligence?

▲ Paperclip's first interactive video course, The Birth of an Artificial Intelligence.

If consumer brands can output content like Paperclip — using appropriate presentation and explanation to clarify products that were previously hard to describe, or where consumers struggled to distinguish quality. Why is it good? Where exactly is it good? How does it differ from similar products? This represents a massive opportunity.

Beyond using video for 360-degree product showcases, some categories can incorporate interactive sales formats like live-streaming. Nearly every brand is live-streaming now — both for sales and customer service. Collectibles (wenwan) is a category particularly well-suited to live-streaming: they're non-standardized products, and hosts can display items, explain them, and answer consumer questions in real time. These products need live-streaming more than other categories.

To summarize, thanks to the rise and development of short-video platforms, lifestyle-sharing platforms, and live-streaming platforms, efficiency has been dramatically improved across distribution, decision-making, and shopping guidance. Within this wave of efficiency upgrades, there's a window for new brand growth — particularly in certain vertical categories.

Third, offline brand renovation.

Expanding from online to offline has become an inevitable choice for online-native brands. From the consumer's perspective, offline presence gives consumers "instant gratification" — especially for ready-to-drink and ready-to-eat products. Sparkling water, ice cream, and similar items fall into this category.

Take Chicecream's ice cream as an example. You can certainly stock up through online orders, but now that you can also buy it at nearby convenience stores and supermarkets, the consumer decision process becomes shorter and conversion easier. This has also spawned other opportunities, such as brand front warehouses.

The "see online, buy instantly offline" dynamic is valuable not just for new brands, but also attractive to offline merchants.

On one hand, online viral products raise the price ceiling for entire categories, improving offline channel margins. Take ice cream again: previously, the most expensive item offline might have been Magnum, selling for just a few RMB. Now Chicecream has pushed unit prices to around 15 RMB — and for offline merchants, higher price bands mean better margins.

On the other hand, fresh brands bring shelf dividend. Introducing online brands that users already love can drive foot traffic for merchants. This offline renovation opportunity also serves as a new growth engine for online-native brands that have already built some recognition.

Fourth, new consumption scenarios.

The new consumption scenarios we refer to here aren't about products, but new retail formats. What we're seeing now is that many experience-and-display-oriented products are thriving in these new consumption scenarios.

For example, FreeS Fund's invested jewelry brand ACC Super Accessories puts considerable thought into its offline store layout. The combination of mirrors and lighting, the magic of color and light — it gives consumers an overall "bling-bling" feeling when selecting jewelry in-store, making it easy to get carried away. So jewelry sells better in offline stores; we call this a new consumption scenario.

▲ ACC Super Accessories stores in Wuhan and Guangzhou, with customers selecting jewelry.

Different categories create different new consumption scenarios. "Three pits" (hanfu, JK uniforms, Lolita fashion) experience stores are one new format — you can try them on, take photos. Low-ABV alcohol is another: online it's just selling products, but offline it's completely different. Recently, we visited a tavern whose entire scene was perfectly designed for low-ABV tea and alcohol consumption. VR experience stores, escape rooms — these are all new consumption scenarios.

We believe these new consumption scenarios hold opportunities, but the prerequisite is handling the online-offline integration logic well, and addressing the standardization challenges of chain store expansion.

02 Three Opportunity Points in Entertainment and Media

Whenever a dominant social or communication tool reaches its ceiling, new challengers emerge. Instagram and Snapchat to Facebook, WeChat to QQ — all followed this pattern.

One reason for the rise of new social platforms is generational differences. Each generation has different preferences and choices among social and communication tools. Differences in lifestyle across generations also lead them to prefer different brands.

The core of new social platforms lies in differences in content production methods. For example, Weibo rewards the ability to write witty one-liners, Douyin rewards video production skills, Zhihu rewards the ability to answer questions well... Different platforms stimulate different content creation methods.

From one-liners to video, from bullet comments to dialogue-style fiction — these completely different content creation methods and platforms are what we should focus on. When the traffic of current-generation platforms nears its ceiling, new formats will inevitably emerge to serve the next generation of consumers. What specific new formats? Which ones will succeed? We don't have definitive answers, but this is a direction worth watching.

This is one type of opportunity we see: opportunities from traffic shifts and new demographics.

Next, let's look at what's driving it?

I believe the main driver is new technology upgrading computing platforms, which brings new entertainment formats. This is the second type of opportunity.

One example is virtual figures represented by virtual streamers and virtual idols. In 2020, various real-life celebrity scandals and "building collapses" gave virtual figures an excellent window of opportunity. The two core technologies behind virtual figures are motion capture and modeling. Currently, we're at an inflection point in motion capture technology — the mobile-ization of mocap.

Previously, both optical and inertial motion capture were extremely expensive, potentially running from hundreds of thousands to millions of RMB for a setup. Optical mocap also required very large spaces for filming. These costs were prohibitively high for most startups, even unbearable.

But as major players like Apple enter the market and AI algorithms continue to evolve, motion capture through ordinary smartphone cameras has become viable. So we believe that reasonably priced technical solutions will emerge to lower the cost and barrier to entry for mocap, which will in turn increase the supply of virtual idol content. (See Why We're Bullish on Virtual Idols | FreeS Research)

FreeS portfolio company Virtual Pictures is exploring this direction. The company uses traditional 3D CG and motion capture technology, combined with new media platforms where younger demographics gather — like Douyin and Bilibili — to produce new forms of content.

Here's another example: new sensors generate new dimensions of data, which enable new entertainment experiences. Looking back at the evolution of mobile gaming helps us understand this logic.

In the era of keypad phones, gaming experiences were relatively crude. When the first-generation iPhone debuted, hits like Angry Birds emerged. The touch-sensitive screen dramatically enhanced the gaming experience — we could play simply by swiping our fingers. From that point on, people suddenly realized that phones could be used for entertainment, not just communication.

The defining characteristic of this entertainment tool is portability: you carry it with you at all times, use it constantly, and the time spent on it can be fragmented. With the proliferation of smartphones, the mobile gaming industry grew rapidly, and today its market size exceeds $100 billion.

Now, Apple has added another new sensor to the iPhone — the ToF camera. Will this create new entertainment or other opportunities? If you have good ideas, we'd love to hear from you (yangxiao@freesvc.com).

Other examples of new technology enabling new entertainment include the proliferation of wireless Bluetooth headphones and other wearable devices. Our FreeS Fund video channel has previously shared the relationship between AirPods adoption and podcast content consumption growth — follow us for more.

Tap to watch our original short video 👆

Follow FreeS Fund's video channel

Our third observation: looking back, many interaction patterns start with entertainment, applied to people's most fundamental needs, before gradually extending to mass commerce.

For example, live streaming in China originated from real-person interactive video chat rooms in the PC era, then evolved to showrooms like Inke and YY, and more recently to e-commerce live streaming. Over more than a decade, live streaming transformed from an entertainment tool into a way of doing business.

Following this logic, we can also consider which entertainment formats have not yet been applied to commerce — this may reveal new entrepreneurial opportunities.

Discussion

Which entertainment formats have not yet been commercialized and could create new consumption opportunities? Share your thoughts in the comments.

03 Why Is the Service Industry Upgrade Starting to Become Attractive?

As mentioned at the outset, 2020 may mark a new starting point for the digitalization of services.

In our view, the prerequisite for service industry upgrades is an upgrade in the quality of practitioners. Currently, the main workforce in offline services consists of those born in the 1970s. Compared with previous generations of workers, they are more proficient with smartphones and the internet, and possess stronger reading and communication skills. This makes them a critical component in the digitalization of services.

Second, the abundance of sophisticated digital tools today helps improve standardization in the service industry. These tools allow workers who already have some digital foundation to collect data at the front end, while standardized warehousing happens in the back office — making it easier to establish SOPs for the entire service process.

Furthermore, online entry points like mini-programs and official accounts help brands build longer-term connections with consumers. Previously, to get consumers to use your services, you either posted flyers or handed out business cards — which consumers would likely slip under the glass on their desk or stick on their refrigerator, finding them when needed and forgetting about them otherwise. Later, many service brands developed their own standalone apps, but getting people to download an app for a single service is costly. Providing services through lightweight applications like mini-programs and official accounts allows emerging brands to retain users more effectively in their early stages.

Looking at the market today, service-oriented brands remain scarce; what we see more of are channel-type brands like 58.com. One important reason we believe service-oriented brand models, though operationally heavy, represent significant opportunities is that traffic giants cannot directly monopolize them.

For instance, a major competitive advantage for food delivery platforms is the management of offline riders; for ride-hailing platforms, it's the management of offline drivers; similarly, for courier platforms, it's the management of offline delivery personnel.

Whether it's ride-hailing, food delivery, or courier services — virtually any "online matching, offline fulfillment" business model — because the service delivery happens offline, these are not models that purely online, closed-loop traffic giants can easily replicate.

We are optimistic about opportunities in service industry upgrades. In the home renovation services sector, FreeS invested in Yiniu Technology in 2020. Yiniu focuses on the post-renovation market, providing services like wall repainting, waterproofing and leak repair, and partial remodeling. Yiniu's workforce skews younger — even its oldest workers were born in the 1970s. The company has also established standardization systems and talent development frameworks, enabling it to deliver stable, standardized services to users.

We tend to believe that entrepreneurs in the service industry who can do two things well — manage people well and deliver good service — have opportunities. Service industry upgrades are indeed demanding, but like education, finance, healthcare, and other service sectors, doing it well yields tremendous results; the better it gets, the larger it grows.

Summary

1. New opportunities in consumer goods reshaping: Supply chain technology upgrades give new brands more room for innovation. Changes in traffic distribution, with increasingly precise algorithms on traffic platforms, make it easier for brands to go "from 0 to 1"; the红利期 of video/live streaming platforms is not yet over. Offline brand renovation and new consumption scenarios both create favorable conditions for new brands to rise.

2. New opportunities in entertainment: New traffic and new demographics are embracing new social tools and new content; the emergence of new technologies drives computing platform upgrades, catalyzing new entertainment formats; interaction patterns expand from entertainment into commerce.

3. Service industry upgrades reaching an inflection point: Digital tools have improved the degree of standardized service in the industry, while online entry points help brands build longer-term connections with consumers.

Discussion

Which entertainment formats have not yet been commercialized and could create new consumption opportunities? Share your insights in the comments.

Contact Us & Join Us

FreeS Fund continues to pay attention to investment opportunities in the consumer sector. Business plans are welcome at bp@freesvc.com, and you can also reach out to Feng Xiaorui (WeChat ID: freesfund).

FreeS Fund is currently seeking investors in biotech, deep tech, and consumer/TMT in Beijing, Shanghai, and Shenzhen. We welcome those with industry backgrounds and an interest in investing (full-time or internship) to join us, and also welcome referrals of excellent candidates to hr@freesvc.com (resumes welcome).

Is the Internet Destined to Have a Next New Platform? | FreeS Research

Where Is the Endgame of E-Commerce Live Streaming? | FreeS Research

Li Feng Column 15 | How Long Will Live E-Commerce Stay Hot?

FreeS Report 19 | The Age of Tipsiness: Where Are the Opportunities for Low-Alcohol Startups?

▲ Understanding the Instant Food Boom in 4 Minutes | FreeS Daily Business Thoughts

▲ FreeS Fund's Li Feng: From 0 to 1 Is Easy for Consumer Brands, From 1 to 10 Is Hard | 10/31 Closed-Door Session Registration

▲ Galaxies in Your Eyes: Understanding the Colored Contact Lens Trend in One Chart | FreeS Research

▲ Three Squirrels' Zhang Liaoyuan: A Once-in-20-Years Brand Opportunity — How to Win in Three Steps? | FreeS Fund 2020 CEO Annual Meeting

▲ Surpassing Nestlé and Starbucks During 618 to Become #1 in Instant Beverages: What Did Saturnbird Do Right? | FreeS Research — Learning from Investment