What Will Happen to Cross-Border E-Commerce in 2022? | FreeS Fund's Going Global Series

Why has cross-border e-commerce managed to buck the trend, and who will emerge as the next winners?

On December 31, 2021, in the third episode of the "What's Next | Tech Matters" Season 5 year-end review series, FreeS Fund founder Li Feng (Uncle Feng) and Grand View Capital North America lead Richer explored the theme "Why China's Overseas Expansion Track Managed to Grow Against the Headwinds in 2021," discussing the following questions:

- What macro-level shifts shaped the overseas expansion landscape in 2021?

- What are the biggest challenges facing overseas expansion today?

- Who is positioned to become the next generation of winners in this space?

- How should we view the consumer and Taobao-native brands of that era, and how should we view cross-border e-commerce now?

- How will Chinese and global tech giants position themselves in 2022?

- What major trends might emerge in overseas expansion in 2022?

- Which regions look promising for globalized entrepreneurship?

Interested listeners can click the audio link below to tune in. We've also compiled the highlights in the main text for reading.

Starting in April 2020, import and export trade in most countries contracted to varying degrees due to the spreading pandemic. Yet China's overseas expansion track still managed a 15% growth rate — thanks not only to effective pandemic containment, but even more crucially to the support of China's "large, comprehensive, and complete" supply chain.

At the time, many believed such growth would be difficult to sustain in 2021. The rapid decline in global demand for pandemic supplies and the high base effect from the previous year, among other factors, were expected to pose significant growth challenges for China's overseas expansion track.

But by the end of 2021, even after weathering Amazon's unprecedented wave of account suspensions targeting Chinese sellers in Q2, China's overseas expansion track had unexpectedly delivered an impressive performance — export growth exceeded 20% year-over-year, and import-export trade contributed over 40% of GDP growth, continuing to command serious attention from the venture capital community.

FreeS Fund has been closely following this space since 2015. The cross-border e-commerce track may look red-hot, but surviving and succeeding in it leaves no room for "luck" or "accident."

We've transcribed Uncle Feng and Richer's discussion from the podcast to share with those following the overseas expansion track, hoping it sparks some insight and reflection.

At 10:00 AM Beijing Time on February 26, Uncle Feng will be joined by Wang Chen, founder and CEO of Beijing Lizhi and Mango Technology (Cider), and Kyle Jiang, founder and CEO of JUNO & Co., for MITCEO's Overseas Expansion Roundtable livestream series to share their industry perspectives. Click the FreeS Fund video account reservation button below to reserve your spot.

At 10:00 AM Beijing Time on March 5, we will host an online office hour for cross-border e-commerce entrepreneurs. Seats are limited and exclusively for founders. Uncle Feng will be joined by a mystery guest to exchange ideas with entrepreneurs.

We look forward to connecting with you in depth. Scan the QR code at the end of this article or click "Read More" at the bottom left to fill out the registration form. (Event details can be found in the event preview section at the end of this article.)

Engagement Giveaway We warmly welcome your in-depth thoughts on the overseas expansion track in the comments section. The 3 most thoughtful commenters will receive a custom FreeS Fund notebook set (including two notebooks in different designs). Comment screening closes at 12:00 PM on March 3, 2022.

The host and guests for this podcast episode are:

- Xu Ruicheng (Richer), North America lead at Grand View Capital, with years of deep experience in the overseas expansion space.

- Li Feng (Uncle Feng), founder of FreeS Fund, with a long-standing focus on overseas expansion.

/ 01 / 2021 Overseas Expansion Track: Macro Context Review

Richer: Hello everyone, I'm Richer. Welcome to a new episode of "What's Next | Tech Matters" focused on overseas expansion.

In 2021, I'm sure everyone in the overseas expansion space had all kinds of experiences — the circle was constantly evolving. This season of Tech Matters has covered various verticals including gaming, apps, e-commerce, and deep tech. Today we've also invited a heavyweight investor in the cross-border and overseas expansion track to help us take stock of 2021. This guest is Li Feng from FreeS Fund, an outstanding senior figure in our industry whom everyone in the VC world affectionately calls "Uncle Feng." Hello, Mr. Li.

Li Feng: Hello, hello — thank you to Tech Matters for the invitation. I'm very glad to have this opportunity on the last day of 2021 to discuss overseas expansion with Tech Matters listeners — an industry that made a special contribution to China's 2021 GDP and economy.

Richer: Great. Uncle Feng, you've already opened the door for our conversation by mentioning GDP and the economy. I'd like to start by asking you to share your overall observations on overseas expansion in 2021 and your sense of the broader environment.

Li Feng: Let me talk about this macro context from the supply chain perspective. After the 18-month US-China trade dispute that began in 2018, a very hot topic emerged during the 2020 pandemic: would supply chains move out of China?

This question sparked extensive debate at the time, with many conclusions leaning toward supply chains relocating out of China. I also discussed this issue on various platforms, and my conclusion was that supply chains would not be moved out of China.

In fact, attention to this issue only lasted until around June 2020, because starting in May that year, China's foreign trade industry began to outperform expectations, ultimately growing 1.9% compared to 2019. Faced with these results, people stopped worrying about "whether supply chains would transfer." And this outperformance in the second half of 2020 was precisely thanks to the structure and characteristics of China's supply chain.

Building on this outperformance, let's recall the predictions that economists from various countries made about China's economy from late 2020 to early 2021. At that time, most were in unanimous agreement that year-over-year foreign trade growth in Q2, Q3, and Q4 of 2021 would face significant challenges.

First, in the second half of 2020, especially in Q3 and Q4, China's foreign trade had experienced extraordinary growth, with pandemic supplies alone growing 41.5% — including masks, ventilators, and so on. But by 2021, demand for pandemic supplies in various countries began to decline rapidly.

So based on this demand-side shift and the extremely high base for foreign trade growth in Q3 and Q4 of 2020, economists judged that China would face considerable growth challenges in 2021, with potential declines. But according to government-released data, by the end of 2021, China's total goods trade exports reached 21.73 trillion yuan, up 21.2% from the previous year — a ten-year high. Total import-export trade reached 39.1 trillion yuan, up 21.4% from 2020. Foreign trade had once again "seriously" exceeded expectations.

However, while both 2020 and 2021 saw "outperformance" in foreign trade, the underlying causes were quite different.

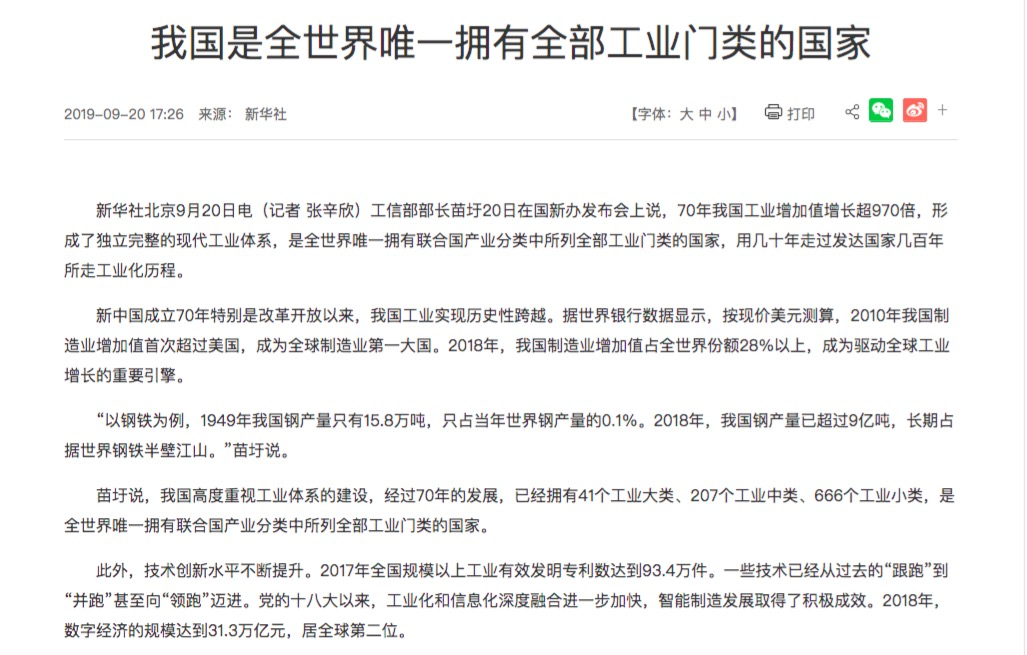

Let's start with 2020. As we mentioned earlier, China's supply chain structure is very distinctive — you could say it's both extensive and comprehensive. The UN defines 41 major industrial categories and 300+ subcategories, and China is the only country in the world with all 41 major industrial categories. Among the 300+ subcategories, China also ranks first globally in 200+ subcategories — this is officially recognized.

Xinhua News Agency

China is the only country in the world with a complete range of industrial categories

This "large and comprehensive" supply chain enabled China to play a crucial role in supporting global pandemic response when COVID-19 spread worldwide, and contributed to the outperformance in trade exports in 2020.

So why did trade exports exceed expectations again in 2021?

If in 2020 countries were scrambling to deal with the sudden onslaught of the pandemic, by 2021 the situation had relatively eased. Countries gradually restored some productivity. Although COVID-19 continued to produce variant after variant, overall export demand for pandemic supplies was shrinking, and China's "large and comprehensive" supply chain advantage was somewhat diminished.

Photo: Xinhua News Agency / Yao Jianfeng

April 2020: A mask production line at a medical equipment company in Anshan, Liaoning Province

At this point, another advantage of China's supply chain became apparent: its "length," or "completeness." At that time, almost every country besides China was highly dependent on either upstream or downstream segments of the supply chain — some on upstream raw materials and intermediate goods, others on downstream demand markets. In other words, none could fully control the entire chain from supply to demand on their own.

This created a situation where, when a country sits in the middle of an import-export supply chain, the smooth operation of that chain requires coordination with upstream or downstream regions. So even if that country's own productivity recovered, as long as its upstream or downstream regions hadn't recovered to the same level at the same time, that country's supply chain couldn't recover in a balanced way. Globalized supply chains tend to have a "pull one hair and move the whole body" quality.

From this perspective, China was then the only country with a complete supply chain that had relatively recovered in a balanced manner. In a situation where global dependence on Chinese supply actually increased rather than decreased, China's enhanced autonomous control over its industrial and supply chains, and the strong resilience of those chains, made it the "mainstay" for stabilizing and securing supply chains. Ultimately, export trade contributed over 20% of full-year 2021 GDP.

That wraps up a brief summary of the macro backdrop for 2020 and 2021. China's industrial and supply chains — "massive, comprehensive, and deeply integrated" — supported the sector through two distinct kinds of outperformance during those two years.

From a change perspective, the cross-border e-commerce landscape saw roughly two shifts, domestically and internationally.

The more visible domestic shift: constrained by pandemic-related travel restrictions, China's traditional foreign trade enterprises increasingly pivoted toward cross-border e-commerce, accelerating the digitization of Chinese foreign trade and the broader shift of global commerce online. B2B e-commerce became a particularly strong growth engine.

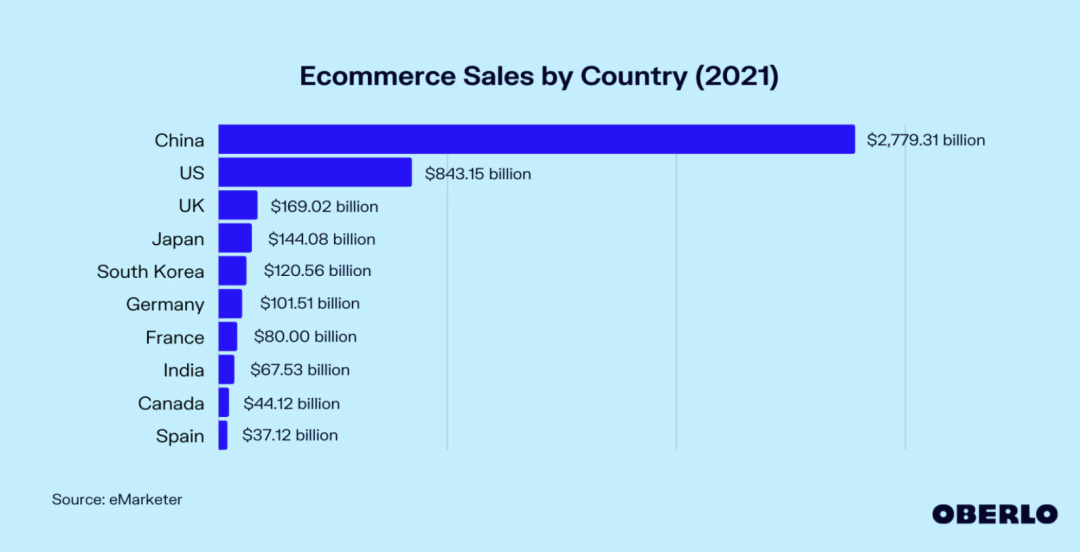

From the perspective of foreign markets, especially developed Western economies, pandemic-induced restrictions and isolation on trade methods directly or indirectly drove rapid growth in local e-commerce penetration. An eMarketer report showed sustained growth in global retail sales, with e-commerce accounting for 21.8% of total retail in 2021. The UK, Japan, South Korea, and others saw notably increased e-commerce penetration.

Developed countries typically represent demand markets, so this phenomenon can be seen as demand-side rapid digitalization — or e-commerce-ization.

eMarketer

Global E-commerce Retail Sales by Country, 2021

/ 02 / What Challenges Might Going Global Face Today?

Richer: What Teacher Li Feng just described was the growth wave of the going-global track in 2021. Looking at the present, the situation seems overwhelmingly positive. In these past two years, have you seen any challenges that this situation has brought to Chinese entrepreneurs or large enterprises going global? Do people have any experiences or reflections?

Li Feng: Let's look at some of China's more successful global business models — for instance, Alibaba's AliExpress, SHEIN, and companies FreeS Fund has invested in like PatPat, Cider, and Wholee. These currently successful cross-border e-commerce businesses are still essentially exports of Chinese supply chain capacity, and broadly speaking, still feature cost-performance as their main characteristic.

[Watch the video to hear Uncle Feng talk about the little-known accumulation and story behind PatPat]

The industry's outperformance in 2020 brought sustained investment enthusiasm to these companies. By 2021, however, the sector's high profile also brought intense competition and survival pressure. In May 2021, for example, Amazon's "account suspension wave" — where Amazon officially banned over 3,000 Chinese stores for suspected violations including "brushing" fake orders and "manipulating reviews."

This caused panic among many merchants, but some survived the stricter environment. The survivors include those mentioned above, and their survival can largely be attributed to two factors:

- They conscientiously followed platform rules and made corresponding business adjustments.

- They upgraded their brands and increased their brand influence.

On the first point: Chinese foreign trade e-commerce achieved unexpectedly strong results in both investment and development during 2020 and 2021, with apparel, small home goods, home appliances, and 3C digital products as typical representatives.

These merchants were mainly distributed across two types of e-commerce platforms. First, Type I platforms focused on online payments and store promotion, such as Taobao and JD.com. Second, Type II platforms focused on cash-on-delivery and single-item promotion, such as Kuaishou and Tencent's Guangdiantong.

Because platforms differ, the rules and risks merchants face vary. But as long as merchants need to rely on platforms for traffic, they must constantly face challenges from changing platform rules to survive.

On the second point: How does brand influence manifest? We typically call cross-border e-commerce enterprises with certain brand influence "independent sites." What is an independent site? It's when users come to the platform for your brand, not just happening to find you while searching for products on the platform.

This concept closely resembles retail itself. Generally, merchants need to strictly follow the rules and playbooks of platforms or channels to acquire traffic — no changing or breaking them. But when your influence grows large enough, you can become your own channel, with users coming to you rather than you chasing users.

But building e-commerce brand influence is no small challenge for many merchants, especially traditional foreign trade players who later joined cross-border e-commerce as newcomers. Whether they can find the right path to brand upgrading is also key to their survival.

Who Might Become the New Winners in the Going-Global Track?

Richer: You just mentioned many problems enterprises faced in the past and their corresponding adjustments. Now they're becoming increasingly mature. Among founders or projects you've invested in, communicated with, or observed, which left relatively deep impressions on you?

Li Feng: Quite a few going-global startups left very deep personal impressions on me in 2021. I'll roughly categorize them.

The first category: traditional foreign trade players forced by the pandemic to shift their business from offline to online. They already had considerable understanding of foreign trade and supply chain rules. For example, merchants doing traditional apparel foreign trade — they possessed rich offline retail experience. And as they gradually mastered various cross-border e-commerce skills, their solid supply chain foundations could become considerable advantages for their future development.

The second category: players who, despite lacking deep supply chain backgrounds, climbed up through years of learning and accumulation.

When we invest in consumer, we often say we want to back "old hands doing new things" — meaning an entrepreneur or company that has immersed themselves in an industry for many years, who begins exploring new directions when major industry changes emerge. But actually, among the going-global startups we backed early that are now relatively successful, PatPat, for example, wasn't strictly "old hands doing new things" back then. The core team's background was basically from internet and technology fields.

But PatPat began building momentum during 2016–2018, when the cross-border e-commerce industry was still nearly ignored. They thoroughly learned the important nodes and operational methods on the supply chain side that "veterans of cross-border e-commerce should know." They also experienced considerable hardships — insufficient supply chain handling efficiency, inadequate supply chain capabilities, and so on — before finally enduring until dawn broke. Of course, the competitive environment was relatively simple back then. But this category of companies' ability to ride the wave today cannot be separated from that lengthy period of industry accumulation and learning back then.

PatPat official website interface

Then there's another category: new players who entered the industry after 2020, not deeply familiar with industry supply chains, who nonetheless raised decent money amid the cross-border e-commerce investment fever. But whether they ultimately develop well still depends on whether they can clear the hard threshold of supply chain in cross-border trade.

Let's extend this further. China's sizable investment in e-commerce brands began roughly around 2011. In 2011, China's online shopping scale first surpassed Japan's to become world number two.

At that time, within the "Tmall + Taobao" ecosystem, what mattered most was a batch of internet-native brand merchants, also called Taobao brands. In apparel, footwear, bags, and luggage — the category with the largest share of online sales — over half were Taobao brands. This situation lasted until roughly around 2015. In subsequent years' Double Eleven events, among the top ten merchants in apparel categories, only a few Taobao brands remained; the rest were all traditional apparel brands.

These traditional apparel brands initially also experienced the shock and baptism of industry e-commerce-ization, and gradually began entering to learn e-commerce rules starting from 2010, 2011, 2012. When they had learned the rules sufficiently, their accumulated supply chain capabilities and advantages as traditional offline retail brands became apparent. In subsequent years, they gradually transformed into e-commerce leading brands. Looking back at Taobao brands, many may not have timely accumulated equally deep supply chain capabilities, and so gradually fell behind or were even eliminated from platforms.

If we analogize this to today's cross-border e-commerce industry, you'll discover that the different types of players today are remarkably similar to back then. There are those who climbed out of numerous pits, finally combining their original industry DNA with supply chain DNA after years of accumulation. There are those who entered with internet DNA and traffic DNA, facing considerable challenges due to lacking systematic supply chain understanding. There are offline veteran players naturally endowed with supply chain DNA, forced by circumstances to begin transitioning online and learning new traffic and new rules.

Looking perhaps three to five years ahead, many of the new winners may well come from this group of people who flipped up from traditional industries and were forced by circumstances to go online and do cross-border e-commerce.

How to View Consumer and Taobao Brands Back Then, and Cross-Border E-Commerce Today?

Richer: I'm actually particularly curious about two things. First, why did you originally pay attention to consumer and Taobao brands — that is, why did you focus on these tracks ten years ago? Second, why did you later begin paying attention to the cross-border e-commerce track, or rather the cross-border brand track? These are two fairly interesting shifts, and I'd love to hear you talk about the stories or journey at that time.

Li Feng: In 2010, China's e-commerce saw its first massive investment bubble. According to data from the China E-Commerce Research Center, in 2010 there were over 40 disclosed investment and financing deals in domestic e-commerce, including B2B and B2C, with financing amounts expanding to the billion-dollar level. It also ushered in the first wave of B2C IPOs (Dangdang, Mecox Lane).

Under such tremendous momentum, both entrepreneurs and investors inevitably fell into frenzy. By 2011, investment across the entire e-commerce industry had extended to every link in the industrial chain, with venture capital alone exceeding $1.8 billion.

When I was doing investment back then, I only started paying attention to the e-commerce sector around late 2010, early 2011. By then the industry had already experienced a year of investment bubble immersion. Company prices were all particularly expensive — hard to pull the trigger. I also observed that the biggest investment bubble during those two-plus years was actually in independent D2C. Whether you were selling socks, underwear, or snacks, you could raise money. Many merchants thus conceived ideas of building independent sites, doing B2C brand e-commerce. The most representative were the likes of VANCL, JD.com, and VIP.com back then.

Based on the e-commerce investment backdrop at that time, I summarized two views. First, when everyone chooses to invest in channels, channel competition becomes especially fierce — for instance, numerous B2Cs emerged. When channel competition is fierce, brands actually benefit, consumers benefit, and cognition of e-commerce gets elevated.

My second view: When channels undergo major transformation, new brands emerge within channels. Because channels undergoing new changes need more brand merchants who can cater to new channel characteristics to cooperate, thereby mutually benefiting and enhancing value for consumers. From that perspective at that time, e-commerce was also a new channel transformation that would catalyze new brands.

So in both of these views, the channel transformations involved all contained hidden opportunities for new brands to emerge. That's why I chose to focus on investments related to new brands at that time — specifically, consumer brands and Taobao-native brands.

This same logic applies today. In 2020 and 2021, cross-border e-commerce saw extraordinary growth, and the industry raised enormous amounts of capital. This phenomenon likely produced two direct consequences.

First, this boom educated developed countries and their consumers on "what is cross-border e-commerce?" — from online selection to logistics speed to the overall purchasing experience. It served as consumer education, much like how in 2010 and 2011 major e-commerce companies spent heavily on blanket advertising to educate consumers.

Second, cross-border e-commerce merchants built their own influence, including different types of channels, channel brands, or platform rule ecosystems — new channels and new brands took shape.

From these two points, we saw new changes on both the consumer side and the channel/platform side. Add to that the pandemic period, when logistics, transit, and warehousing infrastructure and operational processes in the supply chain got trained and strengthened. Combining these three new changes, it wasn't hard to predict that new industry brands would certainly emerge.

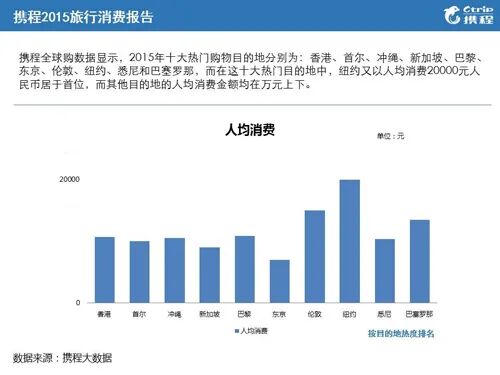

Returning to my personal investment experience: why did I start investing in cross-border e-commerce in 2015–2016? Anyone who followed China's economic situation should remember that at the 11th meeting of the Central Financial and Economic Affairs Leadership Group in 2015, senior leadership first explicitly emphasized supply-side structural reform. At the time, domestic supply-demand mismatch had emerged — Chinese consumers had strong purchasing power, but domestic enterprises' products and services couldn't meet demand, leading to purchasing power flowing overseas. Chinese "overseas shopping power" repeatedly made headlines.

Trip.com Group 2015 Global Shopping Consumption Report

Looking back, every time we've adjusted our economic structure, we've placed relatively more emphasis on foreign trade — and foreign trade has indeed absorbed economic development pressures and challenges. So from a macroeconomic perspective at that time, I tended to believe that new opportunities and windows should emerge in the foreign trade industry.

Another reason: every time a new traffic structure changes, new e-commerce models appear — not limited to cross-border e-commerce. An earlier wave of Chinese cross-border e-commerce, like LightInTheBox, built its business primarily on search traffic. At that time, PC traffic had clearly grown and held high share. This new traffic structure supported China's first wave of cross-border e-commerce.

By the time we started investing in cross-border e-commerce, Facebook had completed its product transition from PC to mobile. Traffic structure shifted from search traffic to social traffic, from PC traffic to mobile traffic — and叠加了 (叠加了) a type of visual traffic around images that had barely existed on PC, such as images on Facebook and Instagram. This change in traffic structure meant new traffic opportunities. The cross-border e-commerce companies doing well now, whether SHEIN or PatPat, which we invested in early, all seized the new traffic created by this structural shift and thus gained红利 (红利).

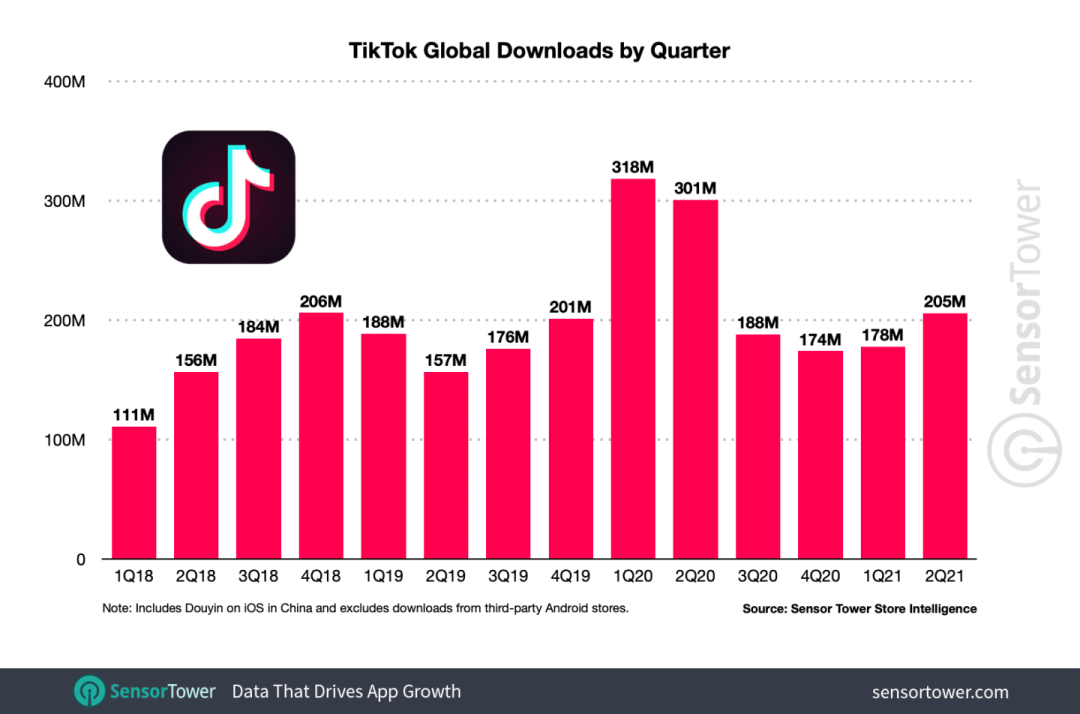

Speaking of which, let's do another extrapolation. I've seen data from SensorTower, the well-known app analytics company, showing that from 2020 to 2021, TikTok's global app downloads and user time spent successively surpassed Facebook's, becoming number one globally. This represents another major shift in traffic structure — the first time globally that traditional social traffic based on text + images transformed into video traffic represented by Douyin (domestically) and TikTok (internationally).

SensorTower

TikTok Global Downloads (Quarterly)

To extrapolate a bit further: this traffic structure change creates opportunities for a large batch of companies abroad that want to capture traffic红利 (红利) in new e-commerce models. Of course, these companies will prove quite useful for China's cross-border e-commerce. Because over the past few years, nearly all Chinese e-commerce practitioners have operated in an intensely competitive, terrifyingly cutthroat environment. They've accumulated rich experience in playing Douyin traffic, livestream traffic — but abroad, these become advanced "struggle" experiences. Overseas, there aren't many local e-commerce players who understand or have fully engaged in streaming media competition, or learned how to sell through video. This contains new opportunities.

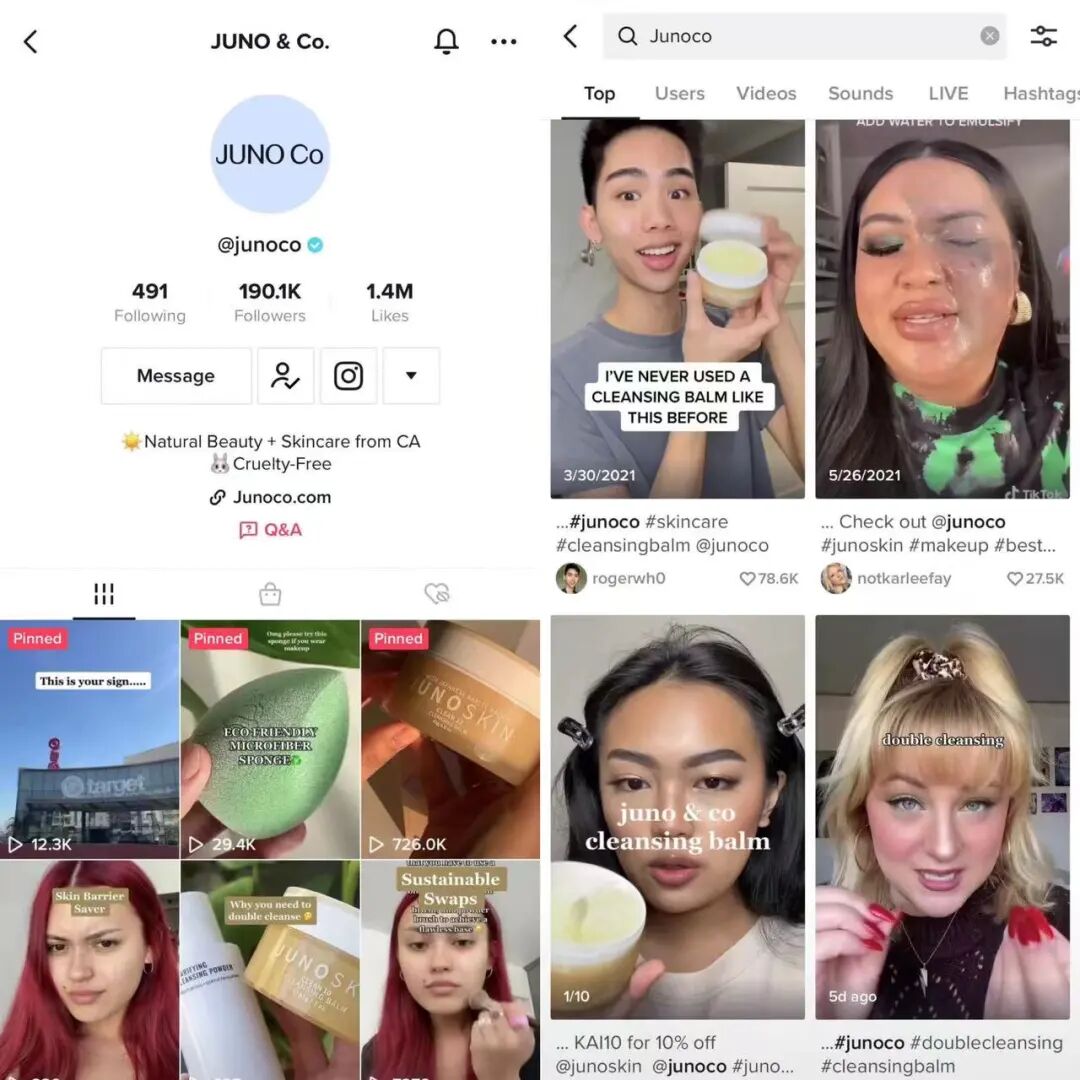

On this point I have a ready example: among our portfolio companies, one happens to be a skincare brand in the US, JUNO. They're among the best in their category on TikTok in the US region, and have achieved solid growth over the past six months. (Click here for related JUNO sharing → How to Win Gen Z Consumers in China and the US? Thoughts and Moves of a D2C Streamlined Skincare Brand)

JUNO's TikTok homepage and overseas beauty influencer shares

As Douyin itself or TikTok gains popularity in North America, and as overseas markets need templates to learn monetization on traffic platforms like Douyin, new channels need the support and cooperation of new brands — more new brands that deeply understand new traffic structures and new media structures will benefit. Of course, the "struggle" experience cultivated in China will also bring them significant gains. This is the new business opportunity created by new traffic structures.

/ 05 / How Will Chinese and Global Cross-Border E-Commerce Giants Respond to the New Landscape?

Richer: Following this thread, I'd like to ask questions on two levels. First, I'd like to understand how some Chinese giants might change their positioning and competitive posture in cross-border e-commerce under these trends — for example, Douyin and TikTok, or Alibaba. I recall Alibaba also made overseas布局 (布局) through Lazada, SEA, and others.

On another level, let's talk about overseas giants. With TikTok's global rise as a representative case, how are traditional overseas internet giants like Facebook, Google, and Amazon responding to this wave of Chinese companies going global, or to the challenges brought by China's traffic changes?

Li Feng: E-commerce is also called the online retail industry — this one phrase defines its two natures: "online" and "retail."

"Retail" represents supply chain efficiency and industrial chain circulation. In plain terms: how goods are produced, where production offers the best cost-performance, how goods flow to consumers, and how to assemble the right assortment of goods for different populations.

"Online" involves traffic structure and media form, as well as differences in time consumers spend on different traffic types.

Let's start with the "retail" part — the so-called supply chain part, encompassing production and circulation. Look at global e-commerce霸主 (霸主) Amazon. We can define what Amazon does as: global sourcing & local merchandising. Global sourcing means I find goods globally; local merchandising means, on that basis, I assemble the assortment best suited to each region's consumer needs.

Finding goods globally, then doing different product mixes for different regional consumer demands — that's the summary. This global sourcing capability is Amazon's advantage, which also includes Amazon's circulation advantage in its self-built warehousing and logistics. Amazon thus established its global advantage on the retail end.

MBA@Syracuse

Amazon Supply Chain Simplified Flow Chart

But this faces challenges in China. Why? For a long time, globally only China could satisfy local merchandising (consumer demand across regions) with merely local sourcing (sourcing within its own borders). Simply put, China produced too many consumer goods and FMCG categories — comprehensive range, high cost-performance, and happening to be in the midst of consumption upgrading, able to supply and sell to itself. On this foundation, Amazon's approach of global sourcing then local merchandising proved inefficient. This is one reason why China could massively give birth to e-commerce platforms with domestic competitive advantages different from Amazon — Taobao, Tmall, JD.com.

Something similar happened to some extent in Southeast Asia. Although consumption capacity varies across Southeast Asian countries, because they're in the same broad ecosystem, they also achieved to some degree having both demand and supply, plus localization — even if this localization might mean Vietnamese-produced goods being sold to Thailand.

Broadly speaking, Southeast Asia also achieves reasonably good local merchandising through local sourcing alone. Thus this region produced its own commercial phenomena — for example, SEA or Shopee, which solved Southeast Asian demand by sourcing in Southeast Asia and nearby China.

Today, most consumer-facing supply chains are rooted in China and Southeast Asia. In four or five years, we'll likely see these supply-chain-based cross-border e-commerce players gradually extend their retail efficiency to more countries. Put another way, Chinese cross-border e-commerce stands a very good chance of becoming a formidable competitor to Amazon in many countries after some time.

This is determined by the fundamental laws of retail itself. The supply chains in these countries were born and bred there, and their scale and efficiency have been profoundly educated and guided by this unusually long pandemic, enabling better matching between supply and demand. This growth efficiency is gradually beginning to take effect.

Having covered the "retail" side, let's now turn to "online" — what we commonly call traffic platforms. Traffic platforms often serve different functions, yet their paths cross. Google and its acquired YouTube, Facebook and its acquired Instagram — TikTok, by contrast, is a relatively pure, independent short-video platform.

In the more primitive text-based internet era, say before 2008, if you wanted to buy something online in China, you'd most likely search for text descriptions first, then go offline to purchase. For instance, you'd search online for information about a particular computer or 3C product, then head to places like Hailong Electronics City in Zhongguancun to buy in person.

In the text era, purchase decisions were usually made with few product images to look at — you could only read text descriptions, such as differences in graphics cards, CPUs, and memory between computers. However, responding to the national "Broadband China" strategic initiative, broadband began rapidly spreading across China from 2000 to 2010. Soon, the combination of text-plus-image traffic distribution emerged.

So who benefited from this shift in traffic structure? Categories where text descriptions alone couldn't showcase selling points — clothing, for example. Having images to showcase products was certainly more reliable than text alone. Later, video distribution appeared. What kinds of products couldn't be adequately hawked through images alone, but needed video? Makeup, for instance.

Looking at this history, changes in "online" traffic structure often create numerous new traffic opportunities. They also represent new distributions of user time, new media formats, and the ability to encompass more diverse product and category types.

To sum up, Chinese and global internet giants' future strategic layouts for this industry will mainly revolve around "online" aspects like traffic structure and media format, as well as "retail" aspects like supply chain efficiency and industrial chain circulation.

/ 06 / Key Trends for the Going-Global Track in 2022

Richer: You've just reviewed a lot of history with us, and along the way discussed how companies should best ride these two types of tailwinds. We'd also like to hear you specifically discuss what important trends in 2022 for going global or cross-border e-commerce you think everyone must seize. Beyond the two aspects you just mentioned, what other possibilities are there? Please share your predictions with us.

Li Feng: Regarding important trends that might emerge in the 2022 going-global track, I personally speculate on the following possibilities:

-

Competition will become extremely intense and brutal. First, the pandemic is increasingly coming under control globally, and we can foresee the gradual recovery of social operations and productivity abroad. From the demand side, consumers' offline demand will recover to some extent — people can get out of their homes more. The total online demand may not be as large as during the pandemic. At the same time, the supply side will also change. Compared with pre-pandemic times, the cross-border e-commerce field is now vastly larger, with new entrepreneurs joining and large numbers of traditional cross-border trade merchants who shifted from offline to online due to the pandemic. Supply-side competition has become extremely fierce. Combining these two points: if demand lacks growth or even decreases while supply significantly increases, industry competition will undoubtedly intensify dramatically. The investment bubble in cross-border e-commerce may also begin to burst.

-

Cross-border e-commerce will see more branding phenomena. Merchants that survive the competition typically have very high brand efficiency — their consumers form deep impressions of the brand rather than just stumbling upon it through casual search. Brands or channels that stick in users' memories gain long-term value from users, and this value will continue to deliver after the shakeout.

As we mentioned earlier, during the pandemic, the powerful comprehensive capabilities of Chinese cross-border e-commerce also educated foreign users to some extent, cultivating their purchasing habits. This process was the same as Taobao's domestic trajectory back then. Fifteen years ago, when many people first started using Taobao, they tended to begin with inconsequential small items. Two or three years later, users' purchasing maturity grew — they knew how to filter and find what they wanted on Taobao. Further along, the concept of branding began to emerge. The same applies to China's cross-border e-commerce exports. Once the entire trade export supply chain is smoothed out, it enters a clear phase of channel branding and product branding. This branding isn't limited to the "high cost-performance" label that "Made in China" has been tagged with domestically and internationally — it's branding with certain premium pricing and quality representation. This is also a new opportunity for going-global e-commerce.

-

Due to intensifying industry competition, cross-border e-commerce players will begin social division of labor. Faced with fierce industry competition, sellers cannot or will not choose to handle everything themselves. Especially when a brand or channel has both capital and traffic, keeping all workflow in-house may be inefficient or impossible to complete on time. At this point, they need to distribute workload to different suppliers. Currently, with the industry's rise, more and more B2B services on the e-commerce side are also emerging.

-

We'll see high-performing players in cross-border or export e-commerce begin horizontal expansion, becoming formidable competitors that directly challenge well-known foreign cross-border e-commerce channels or brands. This corresponds to the "retail" aspect of the "strategic layout" we discussed above.

Richer: I've also observed a very interesting phenomenon. When we talk with many entrepreneurs now, people are intentionally or unintentionally starting to avoid the term "going global." Many brands, from day one of their founding, don't position themselves merely as "product exporters" — they want to build global brands. What does this trend signify?

Li Feng: It signifies that more brands' export focus has shifted to showcasing Chinese innovation and quality. China will see more global brands emerge. Initially, exports may have followed the path of offloading China's excess production capacity, with overseas consumers tagging them more as "cost-effective." But after two years of cultivating and educating global consumers, plus infrastructure and supply chain upgrades and improvements, as consumers gradually adapt to the process and experience, they'll increasingly pursue the innovation and quality of Chinese manufacturing, granting recognition from a global brand perspective. This is why many going-global entrepreneurs now intentionally or unintentionally avoid saying "going global," instead resolving from day one to build global brands.

Richer: One final question. Teacher Li Feng, from an investment perspective, which region do you favor most for going-global or global entrepreneurship in 2022?

Li Feng: Different regions correspond to different supply chain structures.

For example, Southeast Asia's supply chain structure, though similar to ours, is mostly still developing or in early stages of development — comparable to the supply chain of early Taobao-style e-commerce. Europe and the US correspond to the upper-middle portion of China's supply chain structure, or in other words, the quality supply chain, where products themselves are required to incorporate branding and premium pricing. So it's difficult to evaluate all regions worldwide using the same supply chain structure — at least not yet.

Richer: Thank you, Teacher Li Feng, for talking with us today about so many specific issues regarding going global and cross-border e-commerce. I've personally benefited greatly.

In the new year, we wish all going-global entrepreneurs success in breaking new ground. Thank you to all Tech Morning listeners for your long-term support. Thank you, Teacher Li Feng, and we wish everyone smooth sailing and a Happy New Year. See you again in 2022's "What's Next | Tech Morning" going-global series.

Li Feng: Thank you, Happy New Year! See you next time.

Event Announcement

We are currently hosting the FreeS Fund Going Global online event series.

Event 1: Eastern Time, February 25, 9 PM; Beijing Time, February 26, 10 AM. Feng Shu will be joined by Wang Chen, Founder & CEO of Beijing Lizhi & Mango Technology Co. (Cider), and Kyle Jiang, Founder & CEO of JUNO & Co., to share their industry insights on Zoom.

Welcome to click the FreeS Fund video account reservation button below to register for the event.

Event 2

Beijing Time, March 5, 10 AM. We will host an online office hour for going-global e-commerce. Limited seats, entrepreneurs only. Feng Shu will be joined by a mystery guest to exchange ideas with entrepreneurs.

We look forward to in-depth communication with you. Welcome to scan the QR code below or click "Read Original" at the bottom left of this article to fill out the form.

▲4 Companies Raise Nearly 2 Billion RMB in Total | FreeS Family Funding News · Vol 8

▲Bidding Farewell to a Year of Inflection Points: Will 2022 Be Better? | Li Feng's New Year Outlook

▲Our Year: Working Together, Persisting Upward | FreeS Fund 2021 Year in Review

↙ Click "Read More" at bottom left to enter the livestream registration process