Farewell to a Year of Inflection Points: Will 2022 Be Better? | Li Feng's New Year Outlook

Where the heart leads, steady steps take you far.

The year 2021, now behind us, remained one of uncertainty. The ebb and flow of COVID-19, layered atop uneven economic recovery at home and abroad, caught many industries off guard. For venture capital, 2021 also deserves to be called a "year of inflection." Standing at this watershed, how we interpret the subtle signals planted over the past year, how we discern the changes brought by policy and environment and the deeper currents beneath them — these will shape our perspective and imagination for the new year, and determine whether we can maintain our foresight.

In the first week of work for 2022, we'd like to share and explore with you:

- How do we view 2021 and the capital market's evolution during this period?

- As the paradigm of early-stage tech investment shifts, what posture does FreeS Fund adopt as we enter this new torrent?

- And, will 2022 be better?

Before diving in, here are some preliminary conclusions:

- 2021 marked an inflection point for primary-market investment. The turning points: fewer uncertain model-driven startup opportunities, fewer chances to bet on entire sectors, and a narrower window for monetizing model innovation.

- China's venture capital domain underwent a gravitational shift from model innovation to technology innovation. Doubling down on tech investment aligns with China's current national conditions and policy priorities. Challenges followed. Tech innovation carries higher investment barriers, slower returns, and longer cycles — demanding that investment institutions develop more forward-looking and specialized judgment on technology and industry trends. Enhancing the ability to discover value in deeply cross-disciplinary projects, and deepening understanding and predictive capacity regarding the macroeconomy, are key to rebuilding "cognitive edge" and continuing to generate excess returns.

- From a macroeconomic perspective, three angles merit attention: carbon neutrality, manufacturing transformation, and semiconductor capacity spillover.

- Q4 2021 appeared to be a weaker quarter compared to recent years, but from a quantitative analysis perspective, China's overall economic performance in 2021 was better than most people imagined — building on the base of being the world's only major economy with positive growth in 2020, we achieved 8.1% year-on-year GDP growth in 2021; in that same year, we became the only major economy globally that did not "flood the system" with liquidity, while also ranking first globally in economic growth rate.

- In 2022, foreign trade and infrastructure-related industries look relatively optimistic. China possesses the world's largest, most complete, and longest supply chain, which helps maintain strong vitality in foreign trade and enhances resilience against inflation. Additionally, infrastructure investment that began gaining momentum in the second half of last year could become a new locomotive of growth this year.

- In the coming year we will still encounter various phased challenges and setbacks, but as long as the right people do the right things, they will ultimately be recognized by the market, making the world a better place while earning excess returns.

We hope this offers one angle for thinking. We welcome your thoughts and expectations for 2022 in the comments below — the 6 most thoughtful commenters will receive custom FreeS Fund hoodies. In the new year, let's work hard together, follow where our hearts lead, and advance steadily toward our goals.

/ 01 / 2021: A Year of Inflection for Venture Capital

Why call it a year of inflection, and where exactly did the turning occur?

Fewer Model-Driven Startup Opportunities, Narrower Capitalization Windows

The inflection first manifests in this: fewer opportunities for uncertain model-driven startups, fewer chances to bet on entire sectors, and a shrinking window for monetizing model innovation.

Why do we say this?

In the past, TMT was the absolute dominant sector for private equity and venture capital investment. PwC's MoneyTreeTM report showed that in the second half of 2017, TMT investment accounted for over 50% of total industry investment. In China, from 2000 to 2020, the most typical venture capital direction was internet and mobile internet — characterized by light assets, rapid scalability, and strong network effects.

Investing in TMT had one prominent feature: the uncertainty of model innovation. This was also the benefit of the light-asset model — rapid growth, rapid pivoting, without much idle physical assets. One could almost enter, exit, modify, or transform at will.

A classic example is Toutiao. Yiming Zhang initially built "Neihan Duanzi," then pivoted to algorithm-driven information distribution, and subsequently to short video represented by Douyin.

In my early years of investing, I witnessed numerous similar cases — founders would describe one business model when raising funding, and years later their massively successful company would operate on an entirely different model.

So during the TMT era, a phrase investors often used was: what matters most is betting on the person. Because projects frequently underwent model transformations — nobody knew what the project would eventually become, so nobody knew whether today's investment was cheap or expensive. Thus, the person became the primary judgment factor. Investment decisions were made around assessments of people.

However, in recent years, we can clearly sense policy shifting — for instance, "striving to advance the real economy from high-speed growth to high-quality development," "enhancing technological innovation's contribution to high-quality manufacturing development"; and the strengthening of antitrust regulation and enforcement in the platform economy. The result of these policy changes: fewer opportunities for uncertain model innovation.

Speaking of antitrust. Compared internationally, China's antitrust policies were not particularly early, but the timing was special. Looking at historical patterns, antitrust waves have typically emerged as liquidity-easing cycles approach their end — the last instance being after the 2008 financial crisis.

The logic is straightforward. So-called liquidity easing means the government prints more money to stimulate the economy. Thus, money as a factor of production makes earning money easier, faster, and more efficient. Those with more money become better positioned to earn with money. Inequality intensifies. Once economic stimulus reaches a certain point, society must turn back to address social problems. Antitrust follows. And this, to some extent, affects the network effects of model innovation and the profit or capital efficiency ceiling they can achieve.

On another front, compared to before, the window for domestic model innovation to access overseas capital has also narrowed. In the past, many domestic model innovation projects burned through cash heavily, but that was fine — light-asset projects, as long as growth was strong, could list on U.S. capital markets in as fast as three years or as slow as five. Now, with the continuous refinement of regulatory frameworks for overseas listings, the previously relatively loose and crude exit pathway has been closed.

Yet, an increasingly visible positive development is that for global capital, allocating to Chinese assets is becoming ever more important.

From 2004 to 2008, during China's first wave of U.S. listings, domestic internet companies had to dress themselves up "glamorously" to "marry abroad," because Chinese internet assets had not yet gained international capital's favor.

By around 2015, during the second wave of U.S. listings, the dynamic shifted. Representative internet and mobile internet companies no longer needed to dress up so elaborately or go door-to-door; some didn't even need extensive roadshows. Because China's position in the global economy was rising markedly, investing in quality Chinese assets became an active allocation need for global capital.

Going forward, we will certainly enter a third phase: Chinese assets will become increasingly important in global capital's allocation structure, with rising weight. In the future, we may not need to be so "glamorous" — perhaps just "radiant" — or need to "marry abroad" at all, to gain international capital's favor. Of course, while the outlook for Chinese companies listing in the U.S. remains unclear, we may see further clarity this year.

In sum, these changes produced a notable directional shift in the venture capital industry in 2021 — virtually all funds began increasing their tech investment. Doubling down on tech investment aligns with China's current national conditions and policy priorities.

Higher Barriers for Tech Innovation Investment, More Stable Returns, Longer Cycles

Over the past fifteen to twenty years, many of us, myself included, operated according to the investment and exit logic of model innovation. As the investment center of gravity shifts, challenges follow.

First, compared to model-driven startups, high-tech projects such as new drug R&D and chip development are not light-asset models — everyone needs to do some production, so to speak, "moving from virtual to real." Because they're not entirely light-asset, the result is that it's difficult to achieve exponential growth and monopolistic returns in a short time. Simply put, it's unlikely to go from 0 to 1 or 10 next month, then to 100 a few months later.

Second, tech entrepreneurship has higher technological barriers, requiring more forward-looking and specialized investment judgment on technology and industry trends. As mentioned earlier, model innovation frequently changes business models, but we almost never encounter a tech startup doing new drug R&D today and transforming into a chip company by the time it goes public seven years later. Tech projects have relatively strong determinacy in their development path and endgame, meaning tech entrepreneurship's general direction can largely be predicted in advance, with the value-maximizing endpoint selected ahead of time. The result: for investors or institutions, fewer opportunities to profit from the ability to perceive and control uncertainty.

Third, when massive capital floods into tech sectors, growth-stage investment competition intensifies, and exits present challenges.

For example, in April 2018, the Hong Kong Stock Exchange introduced Chapter 18A of its Listing Rules, permitting biotech companies without revenue or profits to go public. 18A provided a favorable capital market environment for innovative drug companies to list and raise financing, opening a secondary market liquidation channel and shortening the time to monetization.

However, the enormous initial policy dividend soon encountered real-world challenges. According to statistics from "Amino Finance," as of December 31, 2021, the Hong Kong-listed Biotech Index fell 27.79%; among 49 Chapter 18A companies, only 13 posted positive stock price gains, with the remaining companies averaging declines exceeding 37%. According to Choice data, among 20 biotech B-share new listings in 2021, 15 broke issue on their first trading day, a 75% first-day failure rate.

Clearly, even if some companies successfully listed via Chapter 18A, they would still be abandoned by investors if their near-term commercial prospects weren't promising. The frequent post-IPO price collapses and failed offerings cast a shadow over the smooth exits that VC/PE investors in the primary market had anticipated, potentially depressing returns for growth-stage investments and making it harder to establish sensible valuation frameworks for technology innovation projects.

Therefore, for investors betting on technology sectors, a critical task is to pre-assess what valuation and what growth rate would actually help you make money as a project develops, and what constitutes a reasonable return expectation.

There's also the question of whether to invest in multiple similar projects. In the past, we said the internet had a Matthew Effect—if you could bet on the "lead horse," investing in one company could yield greater returns than investing in twenty. To some extent, the outsized returns from a few successes could cover the losses from other failed bets. But in technology investing, whether this approach still applies may need reevaluation.

/ 02 / Standing at the Watershed: How Can Early-Stage Investing Continue to Generate Excess Returns?

Despite the challenges that this shift in investment focus brings to the venture capital industry, as a new year begins, we must confront the question: standing at this watershed, how do we continue to generate excess returns?

As mentioned earlier, against a backdrop of relatively predictable technology entrepreneurship pathways, opportunities to profit from recognizing and managing business model uncertainty have diminished. But original technology startups carry higher technical barriers, requiring more forward-looking and specialized investment judgment on technology and industry trends.

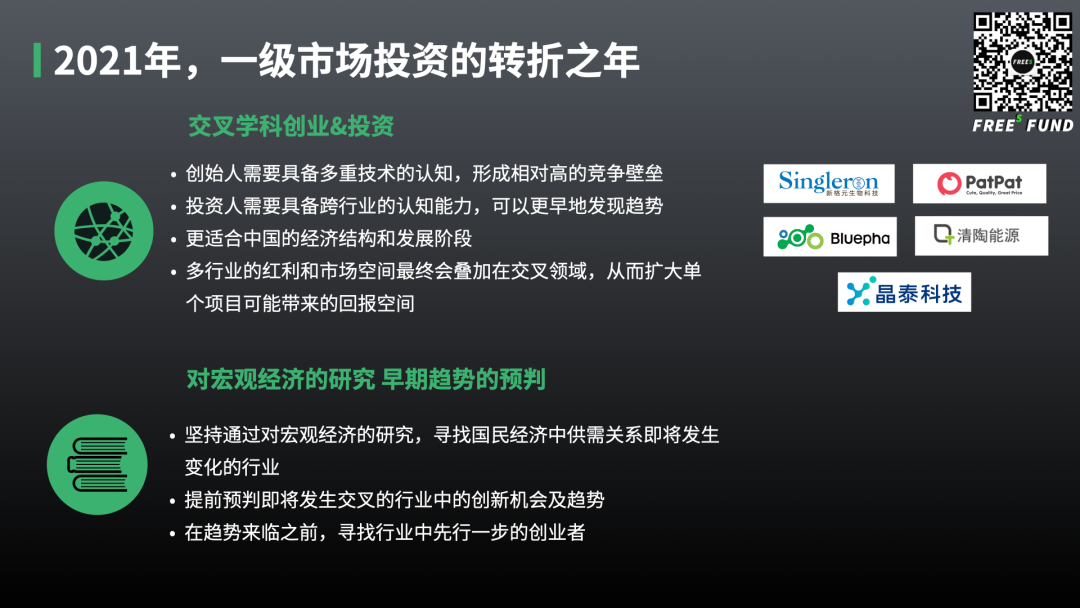

In this section, I'd like to share two approaches FreeS Fund has been exploring: betting on interdisciplinary entrepreneurship, and using macroeconomic awareness to anticipate early trends.

Building Early-Stage Investment Moats Through Understanding of Interdisciplinary Fields

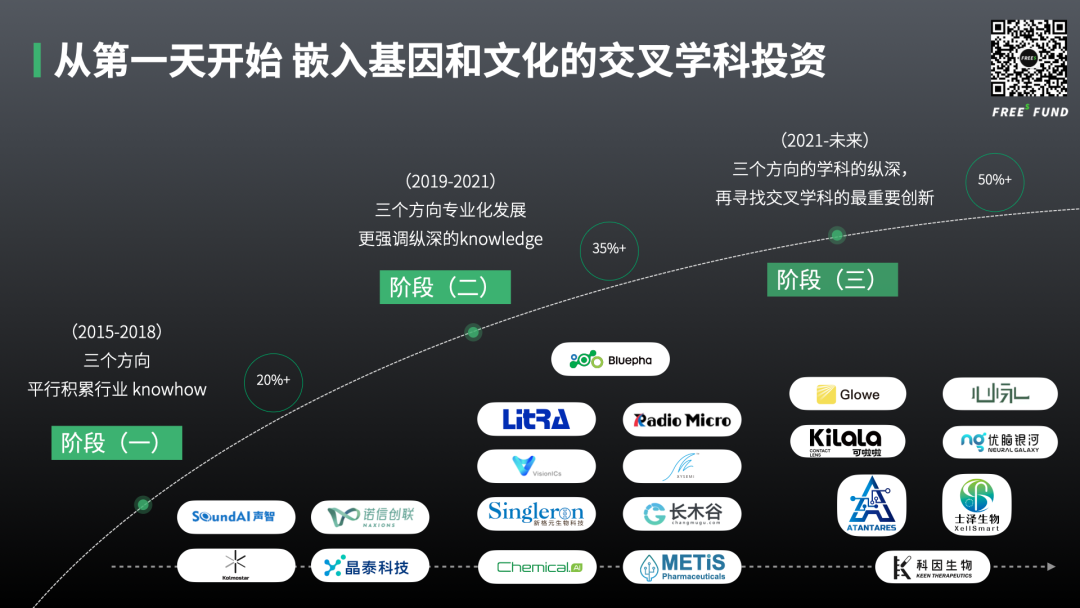

Since its founding, deep technology has been one of FreeS Fund's three investment pillars, alongside consumer & TMT and healthcare. Now, the three directions are approaching equal weight in our portfolio. Because we cover all three areas, we have the opportunity to see projects that sit at the intersection of fields—what people commonly call "crossover" projects. After more than six years of investment practice, we've come to believe that our ability to identify value in interdisciplinary projects has become key to rebuilding our information advantage and generating solid returns.

We were likely among the earliest investment institutions in the industry to explore interdisciplinary investing.

In mid-August 2015, at the Phoenix LINK+ Conference, I spoke about the "deep technology" model: "Exploration at the frontier intersections of multiple disciplines can unleash the imaginative potential of internet thinking to a tremendous degree. When the fluidity of data is redefined: the efficiency of all trial-and-error, exploratory products will increase dramatically."

At that time, my understanding of deep technology investing was still somewhat colored by internet thinking. This "imprint" existed for two reasons: besides my prior experience investing in internet companies, our fund had just been founded and was relatively "poor"—we didn't have the resources to recruit senior partners steeped in technology and pharmaceutical investing. I had to do it myself, leading three teams to cover three directions.

In a short time, I couldn't make up for the lack of specialized depth. Fortunately, we did manage to hire some colleagues from professional fields. So it became a structure where, at the abstract level, I contributed the underlying logic and patterns of seeing things and people from my internet investing background, while at the concrete level, my colleagues contributed specialized depth.

The fusion of these two perspectives allowed us to approach technology project evaluation with a more open mindset—to identify, and even debate, value in projects, salvaging "pearls lost in the ocean" in non-consensus territory.

For instance, back then we invested in projects like Kolmostar and Ingdan Electronics, which combined algorithms with chips. They weren't favored by mainstream institutions at the time. On one hand, there were few specialized early-stage chip investors then; on the other, many institutions felt that although they were doing chips, they were more algorithm-biased.

Returning to 2016, the Kolmostar story is particularly illustrative. Even though we were already inclined to look at crossover projects, Kolmostar sparked heated, contentious debate among our internal PhD investors. What the team wanted to do sounded too good to be true: dramatically improving existing GPS positioning performance, either by 100x better accuracy or 100x lower power consumption. The core technology was algorithms and a cross-disciplinary approach to improving signal-to-noise ratio (drawn from the founder's prior experience working on gravitational wave detectors at Stanford).

One of our EIRs (Entrepreneurs in Residence) conducted deep research into Kolmostar's direction and concluded: based on first principles, this was achievable. After completing his research, he chose to join the project team, and FreeS Fund became Kolmostar's exclusive angel-round investor. In the years since, Kolmostar has focused on developing GNSS (GPS, BeiDou, etc.) satellite positioning solutions, completed tape-out, delivered on its original promises, and over the past three years raised multiple rounds from mainstream VCs and strategic investors.

So in Phase One (2015–2018), the technology projects we touched all carried some internet attributes to varying degrees. By around 2019, we had completed the build-out of partner teams and investment teams for all three directions. By 2021, we had further established interdisciplinary investment groups within each of the three teams.

According to internal statistics, from 2015 to 2018, interdisciplinary projects accounted for only one-fifth of our investments. By 2021, interdisciplinary projects had grown to over half our portfolio—meaning more than 50% of our investments were the result of two or more industries converging on a single application.

For example, in 2019, FreeS Fund invested at the angel stage in Neuracle, a frontier brain science technology company. Neuracle is led by three brain scientists from Harvard Medical School and MIT, plus a serial successful entrepreneur from the technology sector, dedicated to conquering brain diseases through interdisciplinary science. Their R&D team brings together talent from brain science, clinical diagnosis and treatment, software technology, data science, brain-computer hardware, and high-end manufacturing, integrating signal processing, high-performance computing, and hardware-software integration to provide a series of products spanning from understanding brain disease mechanisms to detection, diagnosis, and treatment.

Although the project has since completed multiple funding rounds with total capital raised reaching 650 million yuan, fundraising was challenging in its first two years. The main reason: many institutions couldn't figure out what they were actually doing—they didn't seem to belong to neurobiology, nor to AI, but were stuck in the middle ground between several fields.

Therefore, building up and iterating one's understanding of interdisciplinary fields can help institutions become more discerning about new directions and seize the initiative when relevant projects emerge. However, forming this understanding and judgment is no easy task.

Take a more recent example. Over the past two years, AI drug discovery has been white-hot. In this direction, we've made consecutive investments in companies including XtalPi, ChemAIRS, and METiS Pharmaceuticals. In 2020, at the angel stage, we invested in a related company called Coing Biotechnology.

Coing Biotechnology founder Dr. Yikai Wang graduated successively from Peking University and Harvard. Before founding the company, he worked as an investor at FreeS Fund; before that, he worked at WuXi AppTec's domestic drug discovery services unit, participating in the R&D and clinical filing preparation for multiple drug candidates.

Before deciding to start his company, Yikai explained his entrepreneurial logic to me. He said that for China to become the world's largest CRO market, beyond the R&D cost advantages brought by its engineer demographic dividend, it must also maximize efficiency. Global top-tier CROs (Contract Research Organizations) were already partnering with early-stage AI drug discovery companies we had invested in to improve drug discovery and screening efficiency. What Coing Biotechnology does is introduce multiple new efficiency tools across the entire new drug development process, comprehensively improving R&D efficiency. Based on its discovery platform's iterative optimization capabilities, within less than a year, Coing made significant progress on multiple early-stage targets in tumor metabolism.

However, despite AI drug discovery having been hot for two years, and despite Yikai's background and capabilities, Coing still encountered incomprehension when fundraising. In contrast, we are very bullish on interdisciplinary entrepreneurial projects like Neuracle and Coing that have "one foot on two or even three boats." Because they have the potential to achieve "innovation squared"; meanwhile, in interdisciplinary domains, there is much less invalid competition, because perceiving the innovation opportunities created by the intersection of different directions is itself difficult, and teams capable of "standing on two or even three boats simultaneously" are inherently scarce.

Using Macroeconomic Research to Identify Early Trends Sooner

Beyond building understanding of interdisciplinary fields, another key lies in attention to and research on macroeconomics.

Macroeconomics is arguably the largest, most certain set of ongoing events. While these may not immediately and completely affect people's daily lives, as the largest and relatively longest-term variables, they will eventually feed back into our everyday existence. We primarily do early-stage investing, typically accompanying a company for five or even ten years before it becomes successful. Over such long cycles, their development will inevitably be shaped by macro policy.

At its core, the important reason early-stage investing needs to pay attention to the macro is that finance is the economy's regulator—finance should fundamentally follow and promote changes in economic structure and development. As one component of finance, early-stage investing needs to understand the direction of macro policy and invest in alignment with China's economic structural adjustment direction, methods, and pace. This is also the premise for our obtaining relatively long-term, stable, certain, and attractive returns.

Here's an interesting example. In 2021, the title of China's richest person kept rotating between two individuals. One was Zhong Shanshan, chairman of Nongfu Spring; the other was Robin Zeng, founder of CATL. If you spend time studying China's rich lists over the past fifteen years, you'll find that the ranking changes somewhat mirror adjustments in economic and industrial structure. Behind last year's richest-person competition, what was reflected was that technology and consumption are becoming the dominant forces driving economic development.

Zhong Shanshan alone represented both directions. He not only held substantial shares in Nongfu Spring but also in listed company Wantai Bio, a biopharmaceutical company producing vaccines and diagnostic reagents. In 2021, benefiting from the volume ramp of its bivalent HPV vaccine and COVID testing products, Wantai Bio's earnings exploded.

CATL, meanwhile, is among the first domestic power battery manufacturers with international competitiveness, focusing on R&D, production, and sales of new energy vehicle power battery systems and energy storage systems. An important backdrop to founder Robin Zeng's ascension to China's richest person is the rise of the new energy vehicle industry in China in recent years. And as the most core component of new energy vehicles, the battery system typically accounts for 35% to 40% of total cost.

Data from the China Association of Automobile Manufacturers shows that in 2021, China's new energy vehicle production reached 3.545 million units, with a market share of 13.4% — eight percentage points higher than the previous year. A quick back-of-the-envelope calculation: assuming an average price of 130,000 RMB per NEV, the sector generated roughly 460 billion RMB in output value for the year. Typically, the automotive industry's multiplier effect on the broader supply chain is 1:4.2. Since NEVs have fewer components and lower operating costs, let's assume a more conservative multiplier of 1:3. That means the NEV industry drove over one trillion RMB in GDP last year, with four to five hundred billion RMB tied directly to battery systems. This is part of why Robin Zeng was able to claim the top spot on the wealth rankings.

We began researching the new energy sector relatively early, and in 2016, we made a sole angel-round investment in QingTao Energy, following up with six additional rounds as the company grew. Back in 2016, there was no NEV boom like today, and new energy batteries weren't a hot topic. We believed new energy would become a distinctive opportunity in China because of an easily overlooked macro factor: petroleum import dependence.

China relies heavily on imported oil, which accounts for roughly 70% of total consumption. One major driver of this dependence is the rapid expansion of vehicle ownership. According to the Ministry of Public Security's Traffic Management Bureau, national vehicle ownership reached 372 million in 2020, including 281 million automobiles. By the end of 2020, national NEV ownership stood at just 4.92 million — a mere 1.75% of total automobile volume.

We can project that as China's consumption continues to upgrade, moving from the current level of "over 200 vehicles per 1,000 people" to the developed-country benchmark of "roughly 400 vehicles per 1,000 people," the nation's vehicle stock would roughly double. That, in turn, would require doubling oil imports.

Therefore, China's push to develop new energy vehicles isn't just about "leapfrogging" in an industrial sense — it's a necessary move to ensure energy security. (For more, see "Why Is the NEV Sector So Hot? What's the Long-Term Outlook? | FreeS Research")

That said, the changes the new energy industry has undergone in recent years, and the industrial scale these changes have supported, have far exceeded my early expectations. People often ask me about QingTao. My inclination is to think that following the structural evolution of the new energy battery industry, we'll eventually need solid-state lithium batteries, since they offer higher energy density and better safety than current lithium batteries. From what I've observed, QingTao essentially rebuilt the entire battery materials system from the ground up to make solid-state batteries work — drawing on the team's cross-disciplinary capabilities in materials, computing, and industrial engineering. In 2021, passenger vehicles equipped with QingTao's solid-state power batteries achieved single-cell energy density exceeding 360Wh/kg, with tested pure-electric range surpassing 1,000 km.

To sum up: while the trajectory of technology projects has become more predictable, narrowing the cognitive gap; on the other hand, developments at interdisciplinary junctures, or industry shifts driven by broader macro trends and changes, still create massive divergence in understanding. Whether one can get ahead cognitively, seize the initiative, and capture early trends sooner and more accurately — this is what allows early-stage investing, standing at the watershed moment, to continue generating excess returns.

From a Macro Perspective, What Opportunities Will 2022 Bring?

Opportunities from Carbon Neutrality

How to Avoid a Climate Disaster notes that globally, roughly 51 billion tons of greenhouse gases are emitted into the atmosphere each year. Production and manufacturing (including steel, cement, and plastics) account for the largest share at 31%. Electricity generation and storage come second at 27%. Agriculture and livestock, and transportation, rank third and fourth at 19% and 16% respectively.

Looking at China, the country currently produces half the world's steel, roughly 60% of global cement output, and holds 40% of the petrochemical market. Given China's outsized share of global capacity in steel, cement, and plastics, while we can make near-term carbon reduction gains through clean energy and new energy vehicles, achieving carbon neutrality in the long run will ultimately require tackling these three sectors.

This presents numerous entrepreneurial opportunities, which we can consider from several angles: process innovation, materials innovation, and supply-demand matching. For at least the next decade, these directions offer enormous room for improvement, and the industrial scale and volume of these sectors can support innovative companies in commercializing effectively.

Take a simple example: using synthetic biology to replace chemical manufacturing products. Synthetic biology, put simply, uses bacteria, enzymes, or microorganisms to carry out carbon chain decomposition and transfer processes.

FreeS Fund invested in Bluepha at the angel round. The company applies synthetic biology to drive molecular and materials innovation across consumer goods, food, healthcare, agriculture, and industrial applications. The 2020 plastic restriction order and 2021 carbon neutrality commitments gave Bluepha successive tailwinds from policy. On January 1, 2022, Bluepha broke ground on its first product line — a "super-factory" in Binhai County, Yancheng, Jiangsu Province, with annual capacity of 25,000 tons of PHA, a biodegradable material. Going forward, everything from plastic bags and disposable utensils to paper-plastic composite packaging could use PHA, a bio-based plastic with performance comparable to conventional petrochemical plastics but a green, low-carbon full lifecycle. If produced using "clean energy + bio-manufacturing," PHA's full-lifecycle carbon emissions can be reduced by 90% compared to traditional petroleum-based plastics.

Driven by carbon peaking and carbon neutrality targets, the relatively steep path of energy conservation and emissions reduction will inevitably create development opportunities for more related ventures.

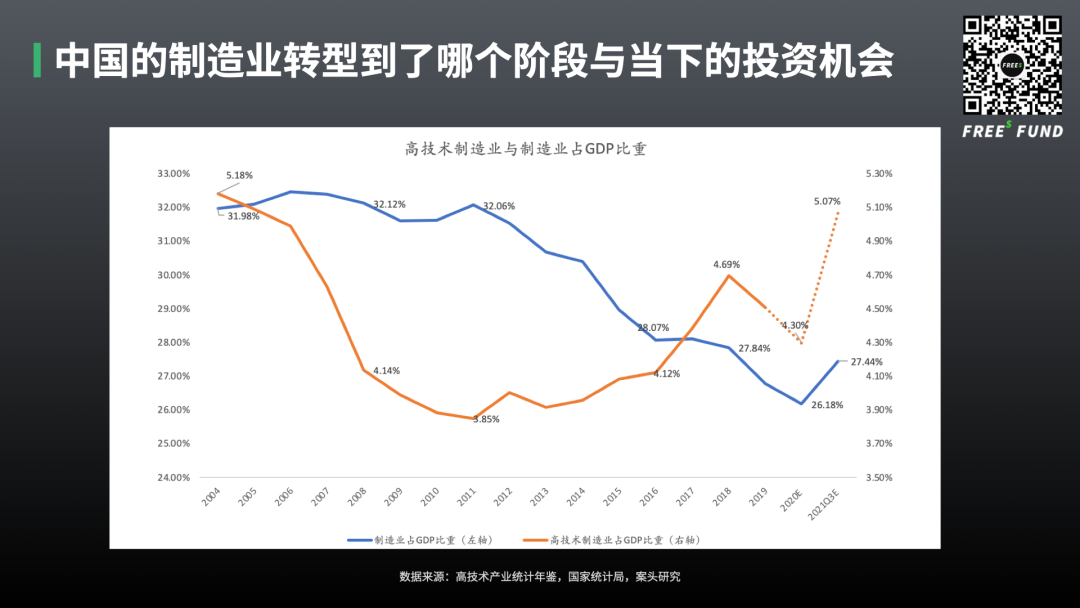

Opportunities in Manufacturing Transformation

Looking back at 2021 economic data, two bright spots stand out: foreign trade and high-tech manufacturing.

China's foreign trade achieved above-expectation growth, making an important contribution to stabilizing economic expansion. Ministry of Commerce data shows that from January to November 2021, total import-export volume reached $5.47 trillion, up 31.3% year-over-year, with 553,000 active trading entities. In the first three quarters, net exports of goods and services contributed 19.5% to GDP growth, driving roughly 2 percentage points of GDP expansion.

High-tech manufacturing also performed well, with value-added growth maintaining double-digit momentum month by month throughout the year. Take November 2021: high-tech manufacturing value-added grew 15.1% year-over-year, further strengthening its leading role in industrial growth. The electronics sector grew 13.5%, continuing double-digit expansion; high-tech industries including electronic communications equipment, computer and office equipment, aerospace equipment, medical instruments, and pharmaceutical manufacturing all maintained above-10% growth. By product, smart and low-carbon products showed strong momentum: NEV output surged 112.0% year-over-year; industrial robots, solar cells, and integrated circuits — products reflecting industrial upgrading — grew 27.9%, 15.4%, and 11.9% respectively.

Everyone talks about China's economy undergoing transformation and upgrading, but where exactly does that process stand right now?

CCTV data shows that during the 13th Five-Year Plan period, China's advanced manufacturing grew rapidly. High-tech manufacturing and equipment manufacturing accounted for 15.1% and 33.7% respectively of value-added industrial output above designated size, up 3.3 and 1.9 percentage points from 2015, becoming the main drivers of manufacturing development. In 2020, annual profits from high-tech manufacturing accounted for 17.8% of industrial enterprises above designated size, up 1.9 percentage points from 2019, making it the fastest-growing profit segment in industry.

That 15.1% figure means there are still many opportunities in the primary market for China's structural economic transformation. When that figure rises to 40-50%, primary and secondary market opportunities will be roughly balanced. Once it exceeds 60%, China's structural economic transformation will be largely complete.

So, to answer the question of where our economic transformation stands: based on the most straightforward data, roughly one-fifth of the way there.

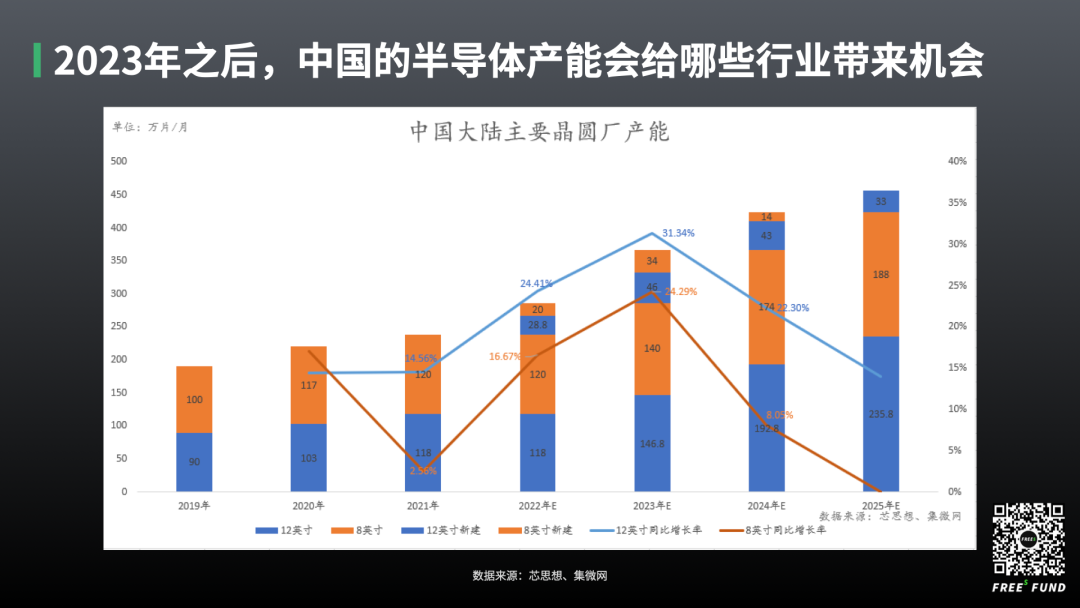

Opportunities from Semiconductor Capacity Expansion

Another closely watched sector is semiconductors.

Based on publicly available data, from 2019 to 2024, mainland China's major wafer fabs will roughly triple their capacity for 8-inch and 12-inch chips. And this doesn't even factor in new capital investments and capacity coming online in the next two to three years. Although a supply-demand gap in chips still exists, assuming that by 2023 or 2024, major mainland wafer fabs achieve supply-demand balance or even oversupply — how might that excess capacity be utilized?

One speculation: excess semiconductor capacity could be applied to a broader range of industries. We recently invested in Xinsu Technology, a startup working at the intersection of biotechnology and semiconductor-ization. What they're doing sits at the crossroads of chips and healthcare. We're very optimistic about their use of new semiconductor technologies to explore high-throughput synthesis and detection applications for DNA, RNA, and proteins in molecular biology.

So after 2023, China's semiconductor capacity may bring entirely new development opportunities to many other industries. Which industries will be transformed, and in what ways — these are questions we need to think through.

How to View 2021, How to Look Ahead to 2022?

How Did Our Economy Actually Perform in 2021?

Before the December Central Economic Work Conference, we did a brief internal analysis of this year's economic situation.

Official data wasn't yet available, but various sources estimated Q4 2021 GDP growth at roughly 3.7% (the actual figure came in at 4.0%) — a relatively weak Q4 by recent standards. The downward trajectory from Q1 through Q4, from 18.3% to 7.9% to 4.9% to 4%, naturally affected sentiment.

But if we look at this calmly, is the data really that bad?

First, we need to account for the base effect from the same period last year — after all, Q4 2020 GDP growth was 6.5%, a relatively high baseline. Second, we should look at the full-year picture. Data released by the National Bureau of Statistics in January 2022 showed that China's GDP grew 4.0% year-on-year in Q4 2021, 8.1% for the full year, and averaged 5.1% annual growth over the two-year period.

What does 8.1% mean?

At the start of 2021, the government set a full-year GDP growth target of "above 6%." When asked at the time whether this target was "a bit low," the Premier responded: "With China's economy now at 100 trillion yuan in total output, 6% growth means 6 trillion yuan. To achieve that at the beginning of the 13th Five-Year Plan period, you'd need growth above 8%." So we clearly exceeded our "KPI."

To put this in perspective, consider the US. In December 2021, the Federal Reserve held a monetary policy meeting. Compared to its September meeting, it downgraded its 2021 real GDP growth forecast (from 5.9% to 5.5%) while upgrading its 2022 forecast (from 3.8% to 4.0%).

Measured by real GDP growth, China's 8% still outpaced America's. Its growth rate remained first globally. And this was achieved against a high base in 2020. Recall that in 2020, China was the world's only major economy to record positive growth. Its GDP broke through 100 trillion yuan for the first time in history, reaching 70% of US GDP. Relative to China's 2.2% GDP growth in 2020, the US saw -3.4%.

What's more notable is the context in which we exceeded our "KPI" — every major economy worldwide was, without exception, "turning on the taps." Take the US: data from the Treasury Department in early 2022 showed that US federal government debt had surpassed $30 trillion, exceeding its entire 2021 GDP.

Our country not only refrained from "turning on the taps," but actually had room to adjust policy while ensuring full-year GDP growth, supported by "exceptional growth" in foreign trade and other sectors. We were even deleveraging, "draining liquidity." So for us, the growth rate was largely a result of deliberate calibration.

Thus, while market sentiment was hardly upbeat, from a purely quantitative analysis perspective, China's economic situation was better than most people imagined. To be sure, market sentiment was real and partially grounded in fact. In early December, "stabilizing growth" was established as the theme for 2022, potentially signaling renewed attention to efficiency on the foundation of fairness.

Will 2022 Be Better?

- Possessing the world's largest, most complete, and longest supply chain helps sustain strong vitality in foreign trade while building greater resilience against inflationary pressures

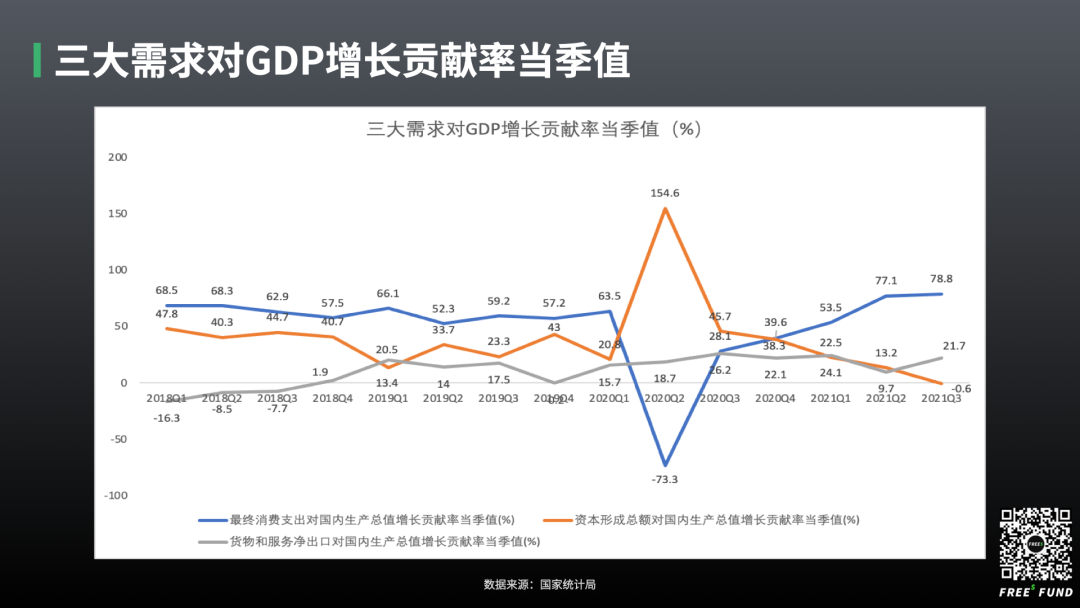

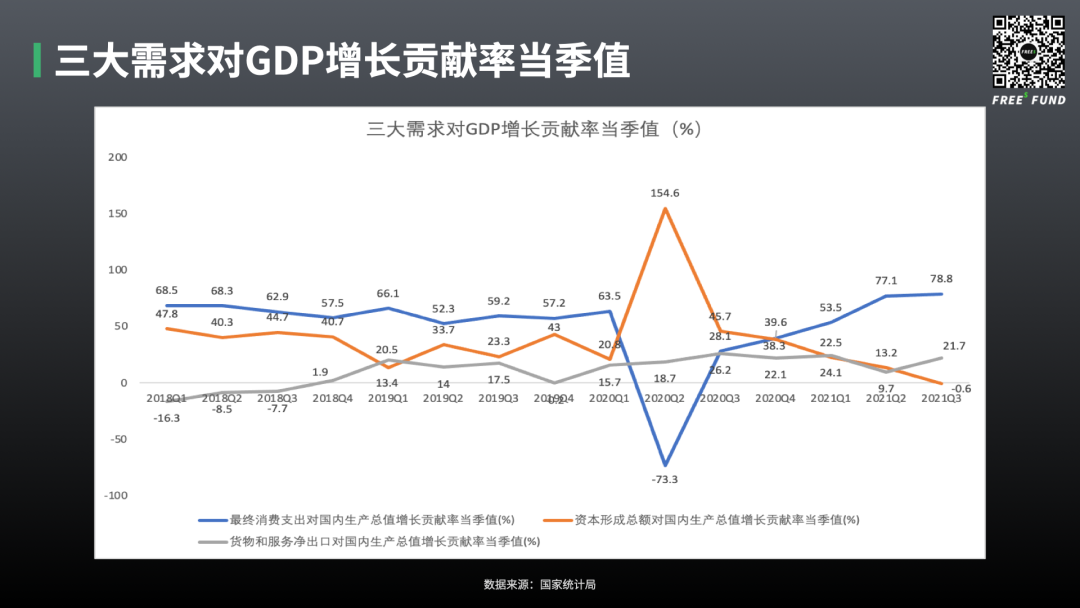

To assess how 2022 might unfold, we can start by analyzing how 2021's GDP growth was achieved. This can be judged from the contribution rates and quarterly pull of the three major demand drivers — investment, consumption, and exports — on GDP growth.

In the chart above, the blue line represents consumption, the orange line investment, and the gray line exports. We can clearly see that exceptional growth in foreign trade was an important driver of China's strong economic performance last year.

Why was foreign trade able to outperform? Simply because China handled the pandemic well? Clearly that's only part of the story.

I drew the chart above in Q1 2020. A hot topic at the time was the impact of global "manufacturing reshoring" strategies on China. There was pessimism in the market, with concerns that manufacturing supply chains would move out of China.

At the time, we firmly argued such worries were unnecessary. (See "One Chart to Understand Globalization vs. Deglobalization | Li Feng Column" for details.) And indeed, by mid-2020, nobody was discussing this anymore. Starting in June, everyone was busy rushing to fill export orders — no one had time to keep worrying.

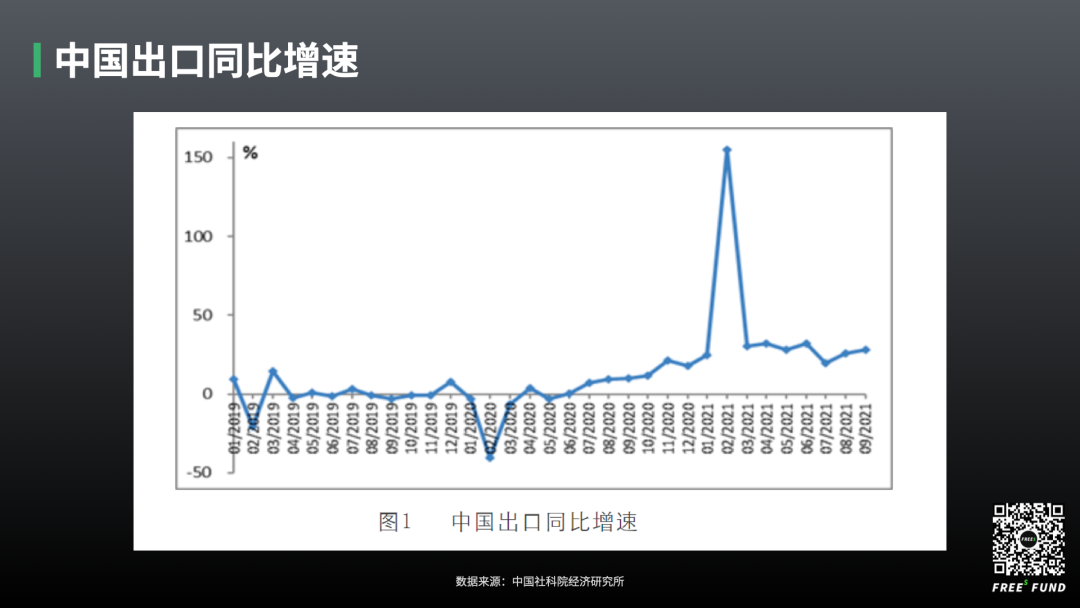

However, by late 2020 and early 2021, another wave of anxiety hit. There was widespread concern that Q3 2021 would pose challenges for trade growth because the base from 2020 was so high. 2020 was high because during the global pandemic, only Chinese factories were in a position to produce, and only China had a supply chain long enough, large enough, and complete enough. Yet the trade results for Q3 2021 proved these worries excessive once again. According to customs statistics, in the first three quarters of 2021, China's total imports and exports reached $4.37411 trillion, up 32.8% year-on-year. Exports were $2.40082 trillion, up 33.0%.

According to January 2022 data from the State Council Information Office, China's foreign trade hit new highs for the full year 2021, with total goods trade of 39.1 trillion yuan, up 21.4%. Exports grew 21.2% and imports 21.5%. Foreign trade "made important contributions to stabilizing economic growth, becoming a major bright spot in the national economy."

Why could foreign trade achieve "exceptional growth"?

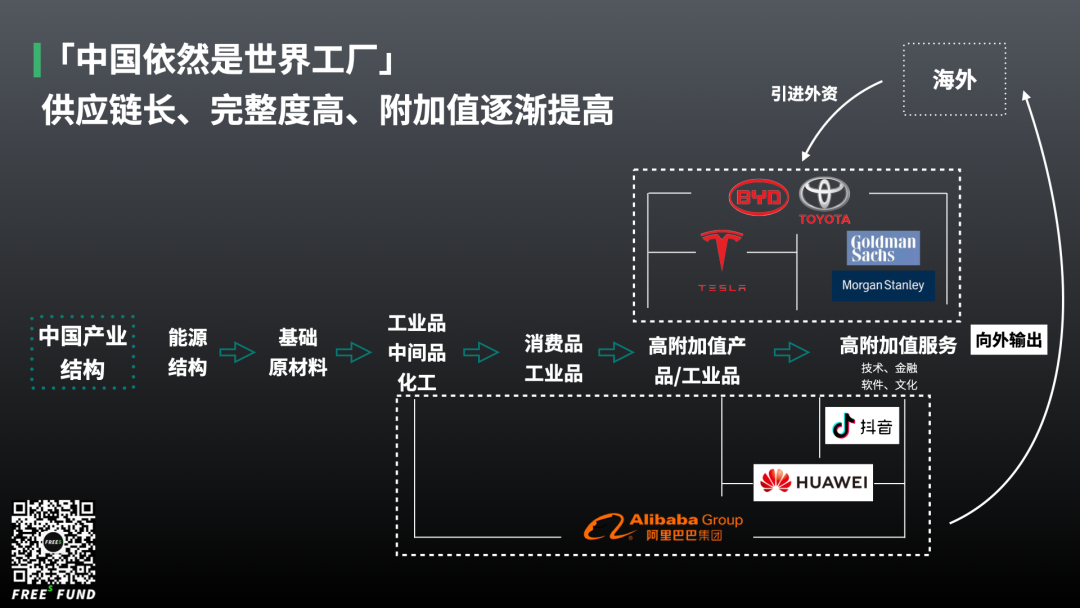

The reason, as we argued two years ago in One Chart to Understand Globalization vs. Deglobalization | Li Feng Column, is that after nearly 40 years of development, Chinese manufacturing has become the world's largest, most complete, and longest all at once. Looking globally, as long as pandemic control worldwide hasn't returned to equilibrium, global supply chains spanning multiple countries will struggle to fully recover. Apart from China, it's hard to find alternatives right now.

Similarly, precisely because our industrial chain is long enough and complex enough, we've also shown greater resilience in facing externally transmitted inflation. Compared to US CPI rising 6.8% year-on-year in November 2021 — a new high since June 1982 — China's CPI that same month rose only 2.3% year-on-year.

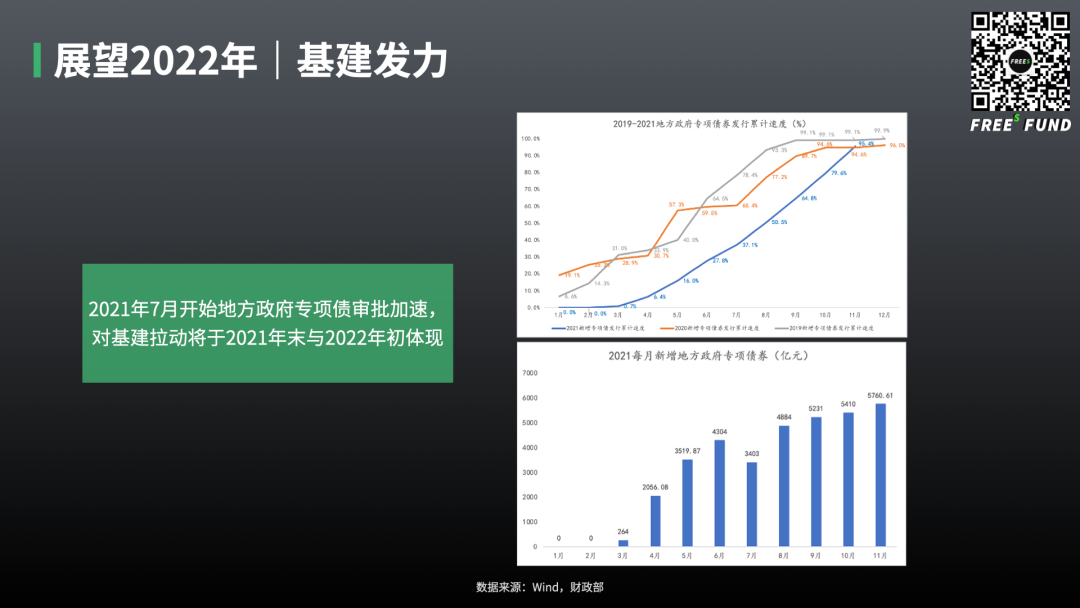

- Local government special-purpose bond approvals accelerated starting July 2021, with infrastructure investment effects likely materializing in early 2022

Based on the chart of contribution rates from the three major demand drivers, fixed asset investment appeared to make a negative contribution to GDP starting in Q3 2021.

So where might the locomotive for 2022 GDP growth come from?

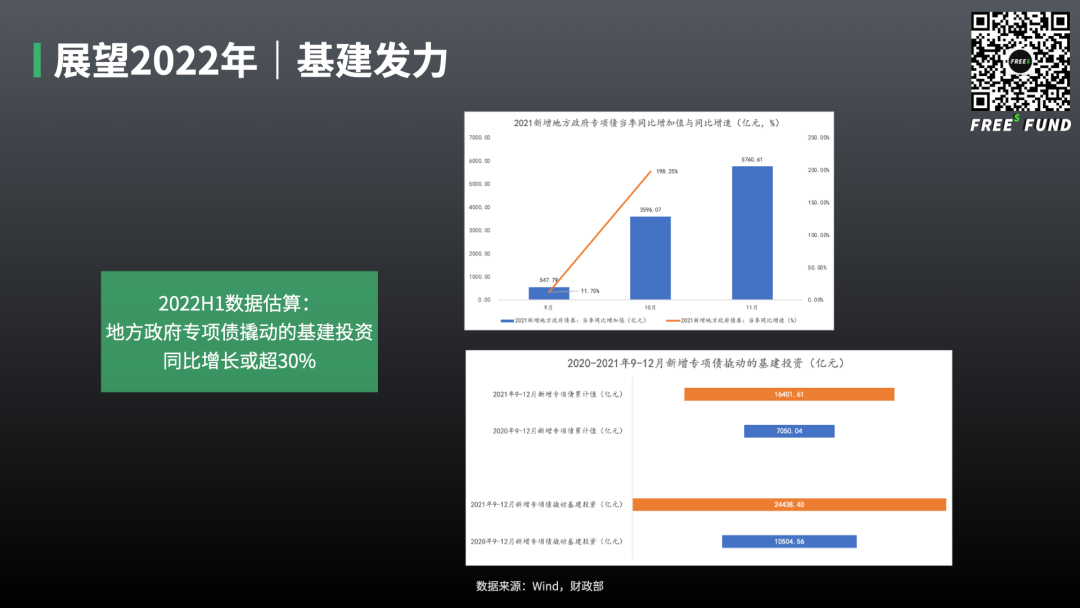

One key indicator we noticed last year was the change in special-purpose bonds. Since the pandemic, these have become a new handle for analyzing infrastructure investment. Over 60% of special-purpose bond proceeds flow to infrastructure, making them a major source of leverage for infrastructure investment. Compared to the past two years, the issuance pace of new local government special-purpose bonds in 2021 was somewhat backloaded. But starting in July 2021, new special-purpose bonds gradually picked up steam, with particularly strong momentum in the second half — November reached 95.4% of the issuance target. Assuming a leverage multiplier of 1.49, the period from September to December 2021 would leverage infrastructure investment of 2.44384 trillion yuan, compared to 1.050456 trillion yuan in September-December 2020 — an increase of 1.393384 trillion yuan, or 32.65% year-on-year growth.

Given that it takes about one to two quarters from special-purpose bond issuance to the formation of physical work, the new local government special-purpose bonds issued from September to December 2021 will translate into infrastructure investment in Q1 to Q2 2022, creating a pull on the economy. This is what's meant by cross-cycle adjustment. Meanwhile, according to the latest information disclosed by the Ministry of Finance, although the 2022 front-loaded quota is only 1.46 trillion, representing 40% of this year's total, we must consider that some of the special-purpose bonds from Q4 last year will be put to use in Q1 this year, and the Ministry has required that front-loaded quotas be "issued early, used early" in Q1. The two will have a compounding effect. Even if some volume was reduced last year, it will be made up by late last year and early this year.

/ 05 / Closing Thoughts

Setbacks are inevitable, and uncertainty can be maddening. But amid the chaos, there are eternal, universal principles and forces that guide us forward — anchors that give us steadiness.

As the state has put it, the economic agenda for 2022 centers on stability: "prioritize stability while pursuing progress." Standing at the industry's inflection point, our watchword is "steady steps, far-reaching goals."

In the next cycle, FreeS Fund will continue to focus on early-stage, small-scale, technology, and cross-disciplinary investments. We will keep strengthening our cognitive moats and growing alongside exceptional CEOs who stay true to their original vision. Though we may face various short-term challenges and bumps ahead, it doesn't matter — as long as the right people do the right things, the market will ultimately recognize their value. And in making the world a better place, they will earn outsized returns.

Join the Conversation

We hope this offers one useful perspective. We welcome your thoughts and hopes for 2022 in the comments below. The 6 most thoughtful responses will receive a FreeS Fund custom hoodie. Let's keep pushing forward together in the new year. Where the heart leads, steady steps yield far-reaching goals.

Our Year: Working Together, Keeping Upward | FreeS Fund 2021 Year in Review

What Kind of Spiritual Consumption Does Gen Z Need? | 2021 FreeS Fund Annual Investor Summit