A Conversation About 2022 and 2023

How do we move beyond uncertainty toward a higher-quality future?

At the start of 2023, we want to share an in-depth conversation that took place in late 2022. Last week, Feng Shu (Li Feng) joined Tangning's Living Room to sit down with Tang Ning, founder and CEO of CreditEase, to look back at the year just past and discuss how to think about 2023 ahead. Here are the key takeaways:

- 2022 was an extraordinarily difficult year to predict and navigate. Though the industry was cold, it left a window for investment and growth to those who were diligent and prepared.

- The main challenge facing the economy today is not a balance-sheet-recession-driven downward spiral, but rather an expectations and confidence problem triggered by COVID shocks, weakening demand, supply-side disruptions, and other factors.

- The 2023 Spring Festival is an important moment to watch. In a relatively optimistic scenario: after three years of ups and downs, people's negative emotions are repaired during long-awaited family reunions; after returning to work, they enter a productive state with renewed confidence relatively early; shortly after comes the Two Sessions, which should introduce new economic policies, allowing people to ride that momentum into Q2. Building on the low base of Q2 2022, Q2 2023 could very well see high growth. This would in turn reinforce confidence in economic recovery, which could carry through the second half of the year. Of course, other scenarios are possible.

- In 2023, three things are critical for economic development: boosting domestic demand, improving employment efficiency, and increasing industrial value-added.

- In China's balance sheet, real estate accounts for a very high share of assets. To prevent a balance sheet recession, the property market needs to stabilize and recover. "Stabilize" means avoiding obvious decline, not returning real estate to a "hot" state. "Stabilize" first shows up in prices — they can't fall too fast or too far — and second in volume, with transaction scale coming back.

- In recent years, the "three major reservoirs" of corporate capacity expansion, infrastructure construction, and real estate have all been experiencing varying degrees of drainage. The capital market will become a new reservoir. However, in 2023, domestic capital markets still face many uncertainties, such as COVID disruptions, the trajectory of China-US relations, or external events similar to the Russia-Ukraine conflict.

- New energy vehicles hit three points: consumption, energy, and large-scale project investment. In 2022, the government introduced a dense series of stimulus policies for NEVs. Looking at the results, this round of stimulus not only boosted auto sales and to some extent alleviated the pressure of stimulating domestic demand, but also attracted substantial foreign investment, encouraged industry competition, "competed" its way to higher value-added, improved the competitiveness of domestic industry, and stimulated exports — achieving multiple goals at once, which is quite rare.

- Investment hotspots often "rotate," but when they come back around, much has changed.

- The Chinese market has a massive innovation opportunity: new supply and new structures forged by new demand. By raising technological content and value-added, we forge new supply; new demand further drives the upgrading and competition of new supply, creating new structural opportunities. Once new demand, new supply, and new structure connect, the results can be extraordinary.

- Three propositions facing entrepreneurs today: First, do you believe the economy will return to a growth trajectory? Second, if the economy can return to growth, what role should your industry play in the new cycle to support overall economic growth? Third, a set of questions: In your industry, what is the new demand? What kind of supply aligns with the direction of industrial and technological upgrading, raises value-added for both the industry and individuals, and improves employment efficiency for your own company and upstream/downstream industries? And how do you transform your company into that and embed it in the new structure, catching the beta of major economic and industrial development?

Below is the detailed conversation and discussion, which we hope offers some angles for thinking. Happy New Year!

Interactive Giveaway

We welcome you to leave a comment at the end of this article sharing your thoughts and hopes for 2023. The 6 most thoughtful commenters will receive a copy of The Power Law: Venture Capital and the Making of the New Future, a book that tells the story of how venture capital has reshaped business innovation.

/ 01 /

2022 Was an Extraordinarily Difficult Year to Predict and Navigate

Tang Ning: Looking back at 2022, what were your takeaways as an investor?

Li Feng: In 2022, I read a great many books. One of them was The Power Law: Venture Capital and the Making of the New Future, translated by Professor Tian Xuan, Associate Dean of Tsinghua University's PBC School of Finance. I wrote the foreword for the Chinese edition. The book does an excellent job showing the cycles that American venture capital has been through, and several points left a strong impression on me. First, VC industry cycles are usually relatively short; even long cycles typically don't exceed two years, usually lasting around a year or slightly more. Second, when markets are cold, because there's less noise and competition, it's actually a window for early-stage startups and new things to sprout.

I strongly agree with both points. 2022 was a cold year for the investment industry. The overall chilly environment affected the entrepreneurial atmosphere, and founders — especially those returning from abroad to start businesses — also decreased. However, I've always maintained that the colder the market, the more it's a rare opportunity to make decisions and invest decisively. Over the past year, I've consistently encouraged my colleagues at FreeS Fund to learn more and see more, and to seize the window to make investments while ensuring project quality. Whether this relatively "counter-trend" decision is correct remains to be tested by time.

Looking at the final results, compared to 2021 and 2020, our investment amount in 2022 did not decrease. Considering that this flat performance was achieved while encouraging everyone to find ways to invest more, it shows that doing early-stage investment this year was still quite challenging.

Tang Ning: If we broaden our view from the investment field to the macro economy as a whole, how would you summarize the past year?

Li Feng: Over the past year, almost every month brought various challenges from internal worries or external threats. Some were caused by external factors, others by the uncertainty in balancing COVID prevention with economic development. In macroeconomics, I might count as a relatively diligent observer and learner, but even for me, 2022 was extraordinarily difficult to predict and navigate. Because there were too many unexpected events on both internal and external fronts, and each event had phased ripple effects.

In 2022, Richard Koo's The Holy Grail of Macroeconomics was very popular, and the book's popularity perhaps reflected a certain broadly shared social mood. The book devoted considerable space to analyzing the financial crises of 1930s America and 1990s Japan, and introduced the concept of "balance sheet recession."

In 1995, Japan's GDP reached $5.55 trillion, then fell continuously to $4.1 trillion by 1998. Assets on the corporate and household sides shrank dramatically.

When people's assets shrink, their debt becomes relatively larger, and debt ratios rise. Although Japan implemented low or even negative interest rates after 2000, it didn't generate effective borrowing — neither individuals nor businesses wanted to borrow, because everyone was first trying to address the deleveraging problem caused by excessively high debt ratios.

/ 02 /

The Main Challenge We Face Today Is Expectations and Confidence

Tang Ning: Is this comparable to China's current situation?

Li Feng: Let's look at whether China has also experienced asset shrinkage. In 2022, the real estate industry returned to the scale of several years ago. According to CRIC data, total commercial residential transaction area across 100 cities in 2022 fell 40% compared to 2021. On the equity market side, at the end of 2021, the total market capitalization of both the Shanghai and Shenzhen exchanges exceeded 100 trillion yuan; by December 30, 2022, A-share total market capitalization was 78.44 trillion yuan, a cumulative evaporation of 13.08 trillion yuan for the full year compared to the prior year-end figure.

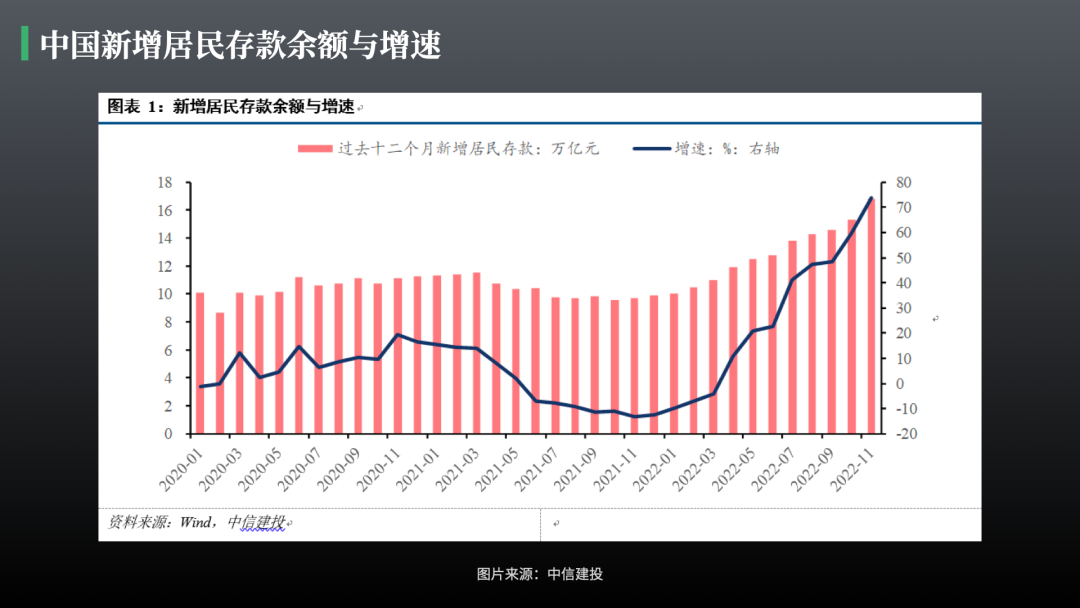

On the other side, due to heightened uncertainty and insecurity in 2022, societal deposits increased substantially. According to a CITIC Securities strategy report, as of November, cumulative new household deposits in 2022 reached 14.95 trillion yuan, an increase of roughly 5 trillion yuan year-on-year — a level never before seen in the same period historically. Additionally, in the first 11 months of 2022, corporate deposits increased by roughly 5 trillion yuan. These two items — household and corporate deposits — together represent a cumulative net increase of roughly 20 trillion yuan.

During the Great Depression of the 1930s, the US lost asset value over four years equivalent to roughly 1.5 years of GDP, and social deposits also fell by nearly 30% — this was a two-way balance sheet recession.

Looking at China, although in 2022 the items lost on the asset side and the gained deposit items may offset each other to some degree, from a balance sheet perspective it may have declined by around 10%. From this angle, at least China has not yet entered a balance sheet recession, or rather, the level of such recession certainly cannot be mentioned in the same breath as 1990s Japan or 1930s America.

So the main problem facing China's economy today is not a spiral decline caused by balance sheet recession, but rather an expectations and confidence problem triggered by COVID shocks, weakening demand, supply-side disruptions, and other factors. Similar confidence deficits or phase-specific confusion have occurred in history, but under policy guidance, we emerged from them.

Tang Ning: So the next three to five years are very important.

Li Feng: Yes. At the end of December 2022, the Central Economic Work Conference proposed that we must focus on expanding domestic demand, accelerate the building of a modern industrial system, and earnestly implement the "two unwaverings" — that is, "unwaveringly consolidate and develop the public sector economy, and unwaveringly encourage, support, and guide the non-public sector economy." In a sense, this was also "clarifying our stance" and "adjusting expectations" at a time of widespread confusion.

/ 03 /

The Upcoming Spring Festival Is an Important Moment to Watch

Ning Tang: What will 2023 look like?

Feng Li: As we were just discussing, 2022 brought a different challenge every month — internal pressures and external headwinds alike. In December, we saw the pivot in COVID policy, followed by infection peaks rolling across provinces, hitting various industries. This pattern was similar to what other countries experienced after reopening.

As for what 2023 will look like, it's still hard to predict. One important inflection point to watch is the upcoming Spring Festival. This year's holiday will be very different from the past two years, when the government encouraged people to stay put. This time, many cities will have already passed their infection peaks before the holiday, so for the first time in two or three years, many people may be able to return home with peace of mind. At the same time, with infection peaks hitting different regions, many factories and companies may let out early for the holiday, and many workers may head home ahead of schedule — the Spring Festival travel rush could begin earlier than usual. Early 2023 could see the largest wave of migration in several years. So this year's Spring Festival will be especially significant. After such a turbulent 2022, there's an urgent need to restore confidence in the future.

Looking on the bright side: during China's most important traditional holiday, families reuniting after so long should help release and heal negative emotions. With the holiday coming early this year, there will be all of February and March after returning to work to get back into rhythm. Then in March comes the Two Sessions. If we take our cue from the tone set at the December 2022 Central Economic Work Conference, 2023 should see more economic policies rolled out. This could create a positive cycle: emotions first heal during long-overdue family reunions, wounds begin to mend, people return to work early with renewed confidence, and then new economic policies emerge from the Two Sessions, setting the stage for the second quarter.

In Q2 2022, GDP grew just 0.4% year-over-year due to COVID containment measures in Shanghai and elsewhere. If the positive cycle I described gets going smoothly, Q2 2023 could see relatively strong growth on top of that low base from 2022. We'd welcome that outcome because it would further reinforce confidence in the economic recovery, likely carrying that momentum into the second half of the year.

Why do I say this? Look at 2021. At the end of December 2022, the National Bureau of Statistics released final verified data showing 2021 GDP grew 8.4% year-over-year. One reason for such a strong performance was the low base in 2020. Q1 2020 saw GDP contract 6.8% year-over-year; by Q1 2021, growth had surged to 18.3%. The strong performance continued into Q2 2021 with 7.9% growth. That confidence in economic development carried into the second half, producing full-year growth of 8.4%.

If we go back to late 2020, economists' forecasts for 2021 Chinese economic growth varied widely. Some were conservative, arguing that China's supply chain would no longer benefit from pandemic disruptions to other countries' supply chains, and that external demand would drop significantly. There were optimists too, but even among them, few successfully predicted that 2021 would achieve growth exceeding 8%.

Standing here now, the situation feels somewhat similar. Economists' forecasts for 2023 growth range from conservative estimates around 4.5% to optimistic ones exceeding 8%. But what no one knows is: when does the "positive cycle" begin?

Of course, other possibilities exist. Could holiday travel trigger a new wave of infections? Will the starting point of the "positive cycle" really be Q1? ...There's still much uncertainty. We'll have to wait and see how things develop. I'm currently leaning optimistic, but we'll have answers in roughly a month or a month and a half.

04 Preventing Balance Sheet Recession

Ning Tang: How do you view potential policy moves next year, or the possible impacts of various factors?

Feng Li: Let me share my understanding briefly — it may be somewhat one-sided. First, looking at policies already rolled out, with external demand weak, economic growth requires boosting domestic demand. Equally important is solving the employment problem, especially raising youth employment rates. On top of that, we need to increase industrial value-added and competitiveness. Only then can we maintain sufficient attractiveness and competitiveness globally.

We can look at the first two together. The contact-intensive consumer sectors were hardest hit during the pandemic — mainly services, including tourism, financial services, catering, and so on. In 2019, services value-added accounted for 54.3% of China's GDP; by 2021 this had fallen to 53.3%. Services were most affected by the pandemic, so they also have the most room to bounce back and grow. I expect services' share of GDP to recover and rise further over the next two years. Moreover, services is a high-employment sector with strong short-to-medium-term job creation. So from an employment perspective, focusing on boosting services makes sense. Another benefit of developing services: it helps raise household disposable income as a share of GDP, which also falls under the "common prosperity" umbrella.

As for the third point — raising industrial value-added and competitiveness.

If you look closely at many policies, they encourage raising China's degree and level of industrial digitalization. China's internet model has produced much innovation. The reason we've seen increasing regulation and anti-monopoly policies in recent years is partly that these companies have moved beyond being digital platforms for industries — they have become the industries themselves. This is a major difference between China's internet model and America's.

So, looking at it from a policy perspective, Chinese concept stocks can indeed improve industrial efficiency, drive industrial scale, provide employment platforms, and enhance comprehensive industrial competitiveness. But when you grow large enough that the development of upstream and downstream industries becomes constrained by you, you hit the monopoly ceiling.

We can't look at just one side of the coin. In fact, China has been deepening SOE property rights reforms and diversifying investment entities across many sectors — finance, telecommunications, power, steel, coal, and others.

So anti-monopoly isn't something that only emerged in recent years, nor is it targeted only at certain industries or internet platforms.

Ning Tang: How do you view the impact of COVID policy changes on Q1 economic performance — for example, will we see revenge spending?

Feng Li: Looking at post-pandemic consumption recovery in major countries globally, typically within one quarter of "reopening," elastic consumer sectors including services gradually see varying degrees of recovery. The restaurant industry usually recovers earliest and most strongly. However, from what we've seen abroad, while other sectors recover at different times, the degree of recovery varies — not every sector achieves full recovery within half a year or three quarters.

Ning Tang: How will the real estate market evolve?

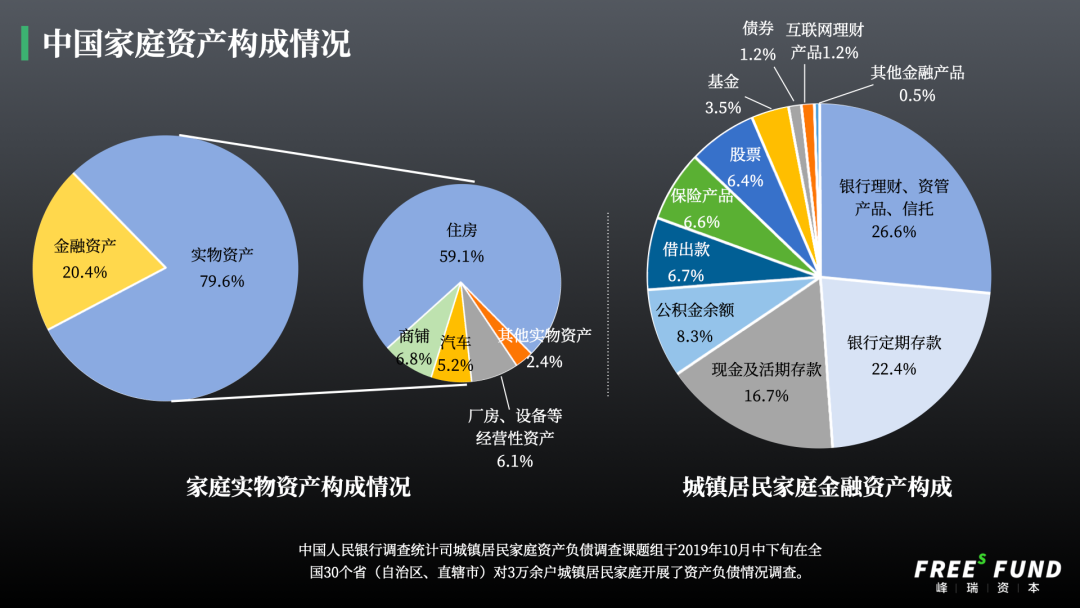

Feng Li: Real estate accounts for a very high share of assets on Chinese household balance sheets. According to the "2019 China Urban Household Balance Sheet Survey" published by the Survey and Statistics Department of the People's Bank of China, urban households held average total assets of 3.179 million yuan, with roughly 70% in real estate and only 20.4% in financial assets.

In this context, I'm inclined to believe that preventing balance sheet recession requires real estate to stabilize and recover. "Stabilize" means avoiding obvious decline, not returning real estate to a "hot" state. "Stabilize" first manifests in prices — they can't fall too fast or too far — and only secondarily in volume, with transaction scale needing to come back.

We can already see policy beginning to act. Recently, the PBOC and CBIRC issued a notice establishing a dynamic adjustment mechanism for first-home mortgage rates. Additionally, in cities where prices of newly built commercial housing have fallen month-over-month and year-over-year for three consecutive months, local first-home mortgage rate floors may be maintained, lowered, or removed on a temporary basis.

China's urbanization rate is approaching 65%. Recently, a colleague at FreeS Fund did some research: what happens if urbanization rises further to around 73%? Assuming we maintain "housing is for living in, not speculation," deterministic demand falls mainly into two categories: first homes for young people, and upgraded family housing after household structure changes. With only these two types of rigid demand, and factoring in young people's marriage attitudes, urbanization, population density, and existing per-capita housing stock, over a cycle of roughly five to ten years — by which point China's demographic structure may no longer change dramatically — there would still be annual transaction volume of 10–14 trillion yuan.

In 2022, although China's real estate market shrank considerably, rigid demand still bought homes. National new commercial housing sales are expected to remain around 14 trillion yuan (data source). Going forward, for real estate to stabilize, it will likely build from this 2022 base that has already squeezed out speculative froth, with rigid-demand transaction scale as the foundation.

Ning Tang: Where will the stock market go?

Feng Li: This is a question of where 2023's money will flow. The 1994 foreign exchange reform marked the beginning of RMB exchange rate marketization. After that, China entered a rapid development phase. Domestic currency had roughly three main destinations: corporate capacity expansion, infrastructure construction, and real estate — known as the "three reservoirs."

When Japan's economy ran into trouble in the 1990s, all three reservoirs collapsed simultaneously.

Looking at China, we've been talking about "cutting overcapacity" for years. On infrastructure, to reduce state sector debt leverage and guard against hidden debt risks, regulators have been trying to decouple local government credit from local financing vehicles. On real estate, we've witnessed the process and impact of real estate deleveraging over the past two years.

Since all three reservoirs have been undergoing partial, sustained deleveraging to avoid sudden collapse, where will newly printed money mainly flow? Capital markets will become the new reservoir.

But on the other hand, we should also recognize uncertainties facing capital markets in 2023 — such as persistent COVID disruptions, the trajectory of US-China relations, or external black swan events like the Russia-Ukraine conflict.

05 A Case Study in Policy Stimulus: NEV Consumption

Ning Tang: Given various possibilities, what are FreeS Fund's views on opportunities in primary and secondary markets?

Feng Li: Finance is always the faucet that supports economic transformation. The recent Central Economic Work Conference mainly pointed toward domestic demand and consumption. Why these two directions?

Consider this data from the Ministry of Finance: China's 2021 national fiscal deficit was 3.57 trillion yuan, with a deficit ratio of 3.83%. From January to November 2022, the overall domestic fiscal deficit reached 7.75 trillion yuan, a historical high. This figure isn't particularly high by global standards — the US fiscal 2021 deficit was $2.77 trillion, or 15% of GDP, and $1.375 trillion in 2022.

The reason 2022 relied mainly on fiscal stimulus is that with COVID's wide scope and frequent, repeated outbreaks, contact-intensive consumption was impossible. Consumption was hard to stimulate, so fiscal stimulus on infrastructure and major projects was almost the only option.

The bright spot in consumer spending for 2022 was new energy vehicles. The Russia-Ukraine conflict exposed many economies worldwide to an energy crisis — a wake-up call for us too. Energy security is tied to national security and foreign strategy.

In 2022, the government rolled out a dense series of NEV stimulus policies. Spending on new energy vehicles was money well spent. NEVs hit three birds with one stone: consumption, energy security, and large-scale industrial investment.

On November 13, 2022, at a China Association of Automobile Manufacturers press conference, CAAM deputy secretary-general Chen Shihua projected that "annual vehicle production and sales breaking through 27 million units shouldn't be a problem." Twenty-seven million units at an average price of over 100,000 yuan comes to roughly 3 trillion yuan. Against the backdrop of 44 trillion yuan (China's 2021 total retail sales of consumer goods), that's one of the largest consumption items. And that 3 trillion-plus is just sales — it doesn't include after-sales service, fuel/charging, or upstream and downstream industries.

So through this series of NEV stimulus policies, China not only pushed its new energy vehicle sales to over 60% of the global total (according to data from the China Passenger Car Association, China's NEV passenger vehicle sales accounted for 63% of global sales from January to October 2022), but also triggered several knock-on effects.

First, while boosting domestic sales, it also drove exports. CAAM data shows that from January to October 2022, automakers exported 2.456 million vehicles, up 54.1% year-over-year; new energy vehicle exports reached 499,000, up 96.7%. In the first three quarters of 2022, China's auto exports surpassed Germany's, ranking second globally behind only Japan. At the same time, Chinese auto exports began showing signs of moving upmarket — the average export price per vehicle was $12,900 in 2018, and has now reached $18,900.

Another notable development: in November 2022, BMW announced an additional 10 billion yuan investment to expand its Shenyang power battery production base, following the major investment in its Lydia plant in June. Shenyang has now become BMW Group's largest production base globally. In October 2022, Volkswagen Group also invested 2.4 billion euros to establish a joint venture in China.

To summarize, this round of stimulus policies not only lifted auto sales and to some extent alleviated the pressure of boosting domestic demand, but also attracted substantial foreign investment, encouraged industry competition, "competed" its way to higher added value, improved local industrial competitiveness, and stimulated exports — multiple wins at once, which is quite rare.

Another point worth noting: looking only at sales within China, BYD surpassed FAW-Volkswagen to take first place in 2022. In the past, domestic passenger vehicle brands had never cracked the top two. At the same time, BYD completed full coverage across high, mid, and low-end segments. The May 2022 national NEV penetration rate top 10 list showed that except for Shanghai, the rest were basically third-tier or lower-tier cities. A November 2022 China Times report showed that BYD's dealerships in third-tier and lower-tier cities now account for 50% of its total network, and NEV startup brands are also expanding their presence in these cities.

06 Investment Hotspots Rotate, But When They Come Back Around, Much Has Changed

Tang Ning: What promising primary market investment opportunities do you see for 2023?

Li Feng: Looking at China's economic structure, domestic economic development shouldn't, in principle, be lopsided. By "lopsided," I mean a very important industry not developing for five to eight years.

So what happened in the primary market in recent years? First, 2019 to 2020 saw a super cycle in semiconductors, against the backdrop of US-China tech tensions and the launch of the STAR Market. 2020 to 2021 was pharma's turn, which had some connection to the pandemic. From the second half of 2020 through the end of 2021, consumer investment was super hot. This was mainly due to changes on the traffic side, which created opportunities for many new brands — "new consumption." These three sectors experienced VC peaks at different times, then over the past year and a half, fell into varying degrees of downturn. Recently, however, with new US export controls on chips, semiconductor investment has warmed back up somewhat, returning to the "mildly hot" state of 2018 to 2019.

I'm bringing these up to say: hotspots rotate. Even though few people are looking at consumer investments today, perhaps after reopening, consumer interest will return next year — but when it comes back, it won't be the same as the last round. Because the previous bubble burst, many consumer companies were proven wrong, and the high valuations many fetched will be hard to chase again.

New drug R&D is similar. In the last cycle, people invested heavily in me-too innovative drugs across primary and secondary markets. However, as the bubble burst for biotech companies listed under Hong Kong's Chapter 18A rules, this sector has cooled down too. If it heats up again, companies will need to be on the cutting edge of new drug R&D technology.

07 China's Huge Opportunity: New Demand Forging New Supply and New Structure

Tang Ning: These industries need to focus on model innovation, technological innovation. In fintech, for instance, you have to look at whether it's creating new value.

Li Feng: I very much agree. One enormous opportunity in the Chinese market is new supply and new structure forged by new demand. Take NEVs again: driven by policy stimulus, market education, and other factors, consumers accepting new energy vehicles as a viable option is new demand. New demand drove new supply, which brought new structure. Whether it's skateboard chassis, batteries, motors, power control chips, or integrated three-electric-system design — all of these represent new supply and new structure.

Building on China's deep accumulated automotive manufacturing capacity, we've forged new supply by upgrading technological content and added value. The new demand side further pulls supply upgrades and competition, creating new structural opportunities.

New demand, new supply, and new structure — once these three connect, they become incredibly powerful.

08 Three Major Propositions Facing Entrepreneurs Today

Tang Ning: As we enter 2023, what advice do you have for people to move out of uncertainty toward a higher-quality future?

Li Feng: This question is both abstract and concrete, so it's actually rather difficult to answer. But I think for entrepreneurs and founders, everyone is facing three main propositions.

First, after experiencing varying degrees of wavering and doubt over the past year, do you believe the economy will return to a growth track?

Second, if the economy can return to a growth track, what role should your industry play in coordinating with overall economic growth in the new cycle?

Finally, a set of questions: In your industry, what is the new demand? What kind of supply aligns with both industrial and technological upgrade directions while also increasing industrial and personal added value, and improving employment efficiency for your own company and upstream and downstream industries? How do you transform your company into this and embed it into the new structure, catching the beta of the broader economic and industrial development?

Additionally, it's worth noting that even if you have the opportunity to enjoy that beta, you'll still experience the ups and downs of seasons.

Reader Giveaway

We welcome you to share your thoughts and hopes for 2023 in the comments. The 6 most thoughtful commenters will receive a copy of The Power Law: Venture Capital and the Making of the New Future by Sebastian Mallaby, on how venture capital reshaped business innovation.

▲ What Will Humans Eat in the Future | FreeS Report 27

▲ Li Xiang x Li Feng: The "Monopolistic Success" and "Gradual Dilemma" of the Dollar | Li Feng Column

▲ One Chart to Understand Changes and Opportunities in China's Industrial Chain | Li Feng Column

▲ One Chart to Understand Globalization vs. Deglobalization | Li Feng Column

▲ How Will Humans Work in the Future? | FreeS Report 26

▲ Bidding Farewell to a Year of Inflection, Will 2022 Be Better? | Li Feng's New Year Outlook

▲ If You Don't Lose the Domestic Rat Race, You'll Win Globally | Li Feng's New Year Consumer Outlook

▲ 2022: Where Are the Next-Gen New Consumption Opportunities? | Li Feng Column

▲ Why Are Chinese and American VC Drifting Apart? | Li Feng Column