How Should We Think About the Consumer Market in 2023 and 2024? | Li Feng Column

Is the 82.5% contribution rate of consumption to China's economic growth a coincidence or an inevitability?

Over the past three years, a shared feature of China and the world at the macro level has been that the outcomes of specific events often run counter to individual expectations or perceptions.

The consumer market in 2023 was a quintessential example. Throughout the year, the assessments we frequently heard were: weak recovery, lack of confidence, insufficient demand. For those working in the consumer sector, they may not have yet felt any warming in the funding markets, and were further rattled by rumors of "red light, green light" restrictions on main-board IPOs. Yet, contrary to these micro-level concerns, macro data painted a very different picture: China's total retail sales of consumer goods grew 7.2% year-over-year in 2023, with consumption contributing 82.5% to economic growth.

In this piece, we'll discuss:

- What caused the divergence between micro-level sentiment and macro-level data?

- When we extend the timeline, has China's economic growth entered a stage driven by domestic consumer demand?

- How should we view the 2023 consumer market?

- What do current and future consumer innovation opportunities in China look like?

- What are the slow-moving variables that we may not have paid much attention to but will actually shape China's future consumption?

We hope to offer fresh perspectives. We welcome you to continue observing and exploring with us. You're also invited to check out our podcast series "High Energy" on Xiaoyuzhou, Apple Podcasts, or Ximalaya.

Engagement Giveaway

What are your thoughts on the 2023 consumer market? What innovation opportunities have you observed in the consumer space? By 17:00 on January 30, the five readers with the most thoughtful comments will receive a FreeS Fund New Year gift (including two books).

/ 01 / The Power of Consumption at the Macro Level

From China's 2023 economic report card, we can see that GDP growth relied almost entirely on growth in consumer goods and services. Specifically, total retail sales of consumer goods reached 47.1495 trillion yuan in 2023, up 7.2% year-over-year, contributing a remarkable 82.5% to economic growth. Meanwhile, services — or contact-based consumption industries — saw rapid growth in 2023, with full-year service retail sales up 20%.

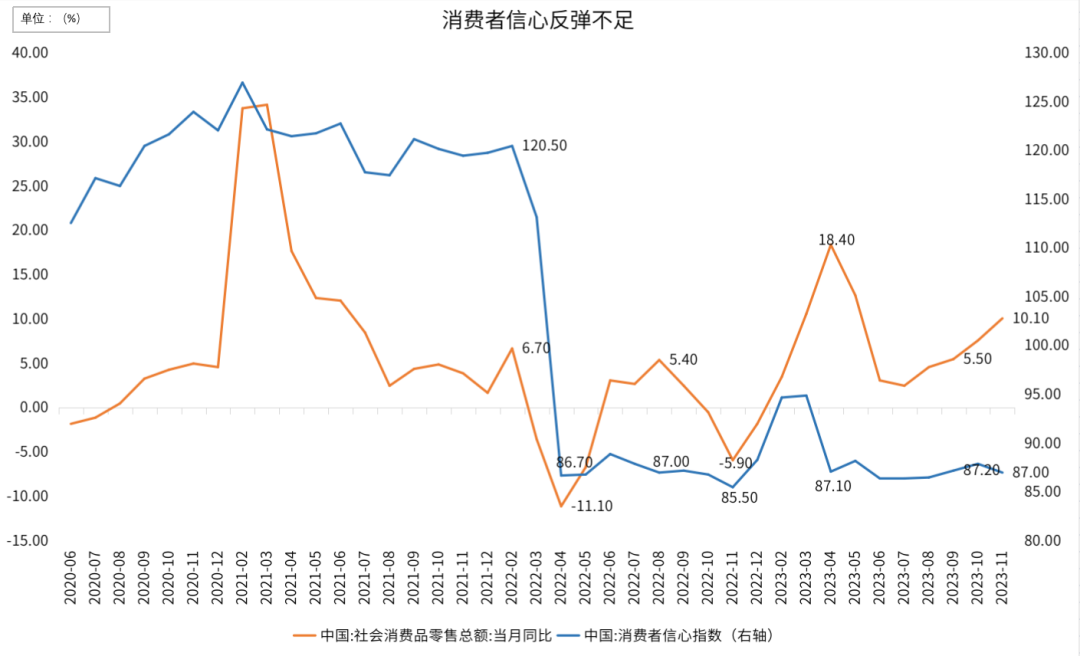

Notably, as mentioned at the outset, the growth picture reflected in macro data diverged significantly from individual lived experience. The chart below illustrates the disconnect between consumer behavior and consumer confidence.

▲ Data source: Wind, compiled by FreeS Fund

▲ Data source: Wind, compiled by FreeS Fund

The blue line represents the consumer confidence index, while the orange line shows the year-over-year growth rate of monthly total retail sales of consumer goods. The data shows that since hitting bottom in 2022, the consumer confidence index has recovered far less than total retail sales. In other words, although consumer confidence didn't fully recover in 2023, consumer behavior was dramatically better than in 2022 — people spent the money they needed to spend.

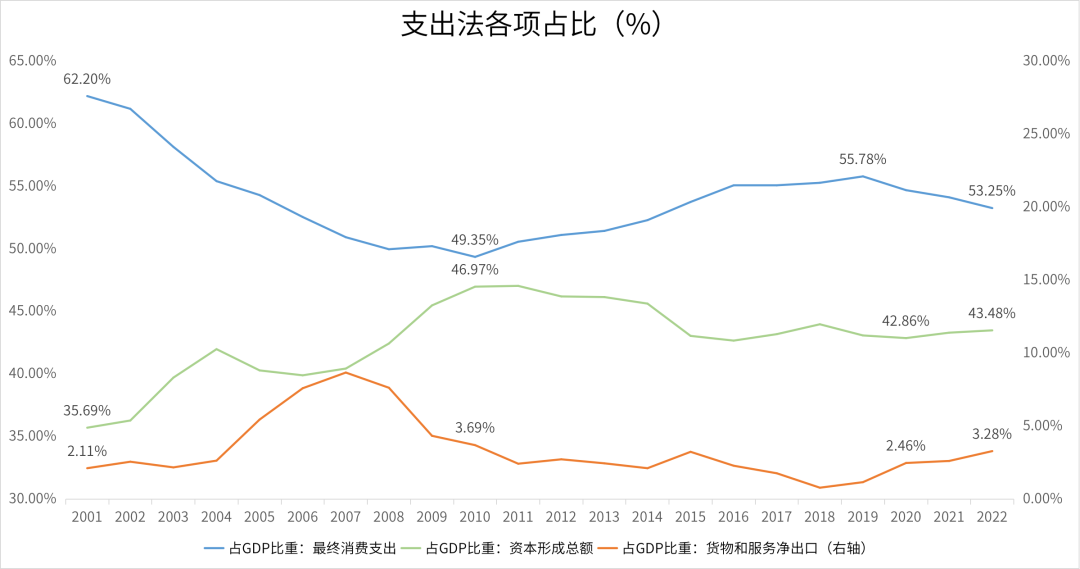

That consumption became nearly the sole hope for GDP growth was no accident. When we disaggregate historical GDP data, we find that China's economic structure is undergoing a massive transformation, or gear shift.

The three drivers of economic growth — exports, investment, and consumption, commonly known as the "three engines" — even if still the same three, saw their hierarchy begin to shift around 2010 in terms of which horse leads and which merely helps pull the cart.

Let's look at the roles these three engines have played in economic growth in recent years.

▲ Data source: Wind, compiled by FreeS Fund

▲ Data source: Wind, compiled by FreeS Fund

▲ Data source: Wind, compiled by FreeS Fund

▲ Data source: Wind, compiled by FreeS Fund

For a considerable period, investment was a critical engine of China's high-speed economic growth. Capital formation — the fixed asset investment driven by investment — consisted mainly of three components: capacity expansion across industries especially manufacturing, infrastructure construction, and real estate. However, starting in 2010, investment's pull on GDP began to weaken, with the contribution rate of gross capital formation falling from 15% in 2007 to roughly 3.5% in 2019.

Specifically for 2023, the real estate market continued the slump of the past two years, dragging on overall investment and infrastructure investment growth. Fortunately, thanks to growth in energy investment within infrastructure, and the 10.3% annual compound growth from high-tech manufacturing and services investment, China's fixed asset investment growth in 2023, while slowing, still made a positive contribution to the economy.

Turning to exports and foreign trade. When we speak of foreign trade, we typically mean net contribution — exports minus imports, or net exports. Since peaking in 2007, net exports' contribution to China's economic growth has gradually declined. Although the overall scale of exports and trade hasn't decreased, its net contribution to economic growth has shrunk.

An important reason for the declining share of net exports' contribution is that imports have increased significantly, reflecting the continuous expansion of China's consumer market. If you recall, after 2008 — roughly following the implementation of the four-trillion-yuan stimulus — people bought many foreign-brand products for daily use. However, starting around 2015 and 2016, domestic brands gradually came to dominate end-consumer manufactured goods, including apparel, footwear, and even the controversial domain of infant formula. Since then, some primary product consumption has shifted back to imports, mainly regional specialty items like cherries, deep-sea fish, and king crab.

In 2022, despite our struggles with COVID, exports achieved 10.5% growth. Precisely because of this high base in 2022, foreign trade's contribution to economic growth was negative in the first three quarters of 2023, even though total volume and scale didn't drop sharply. Of course, this is a challenge faced by major export-dependent countries globally, including China, India, and Vietnam. For production-oriented countries, 2023 saw rising export volumes but falling prices, with exceptionally fierce competition in midstream industries. Looking at full-year 2023 data, total foreign trade imports and exports slowed compared to 2022.

In any case, we still need external demand, because with roughly 17% of global population we generate one-third of global manufacturing value-added — we need to "sell things." But looking further ahead, against the backdrop of challenged globalization, as China seeks to build new, extensive trade systems, it also needs to let trading partners make money — that is, we need to "buy things."

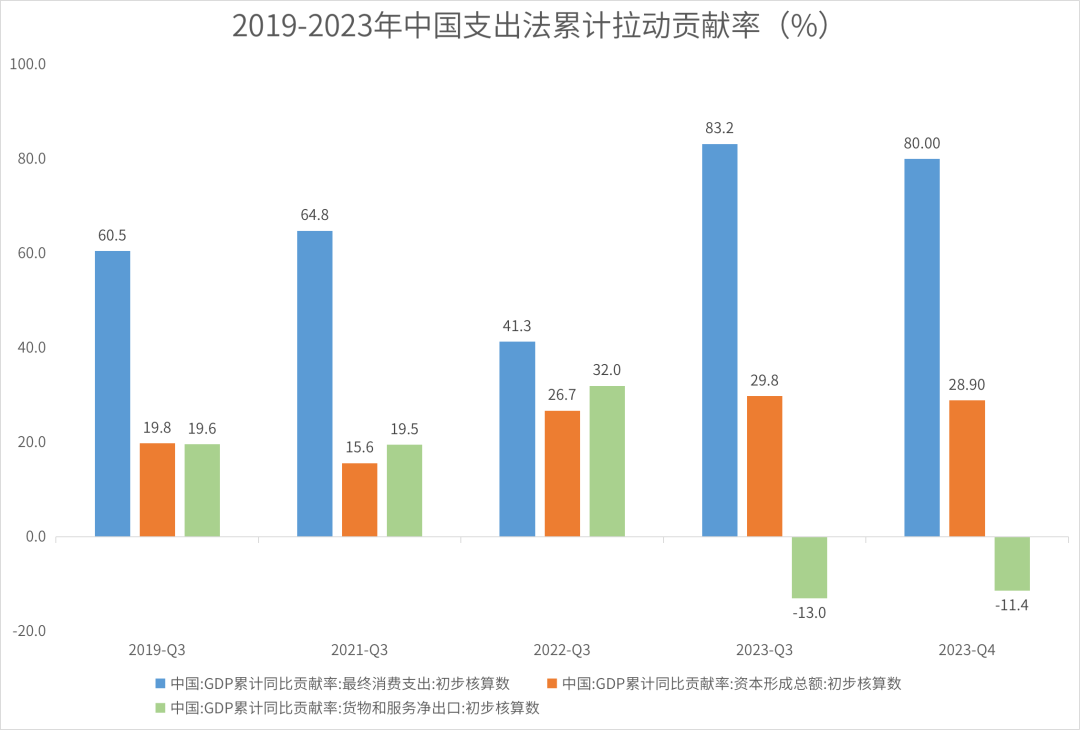

Turning specifically to consumption. Over time, consumption's contribution to China's economy and its share of growth contribution have continued to rise. From a growth rate perspective, from 2011 to 2019, the actual growth rate of final consumption expenditure centered around roughly 7%, consistently outpacing capital formation growth. During the pandemic, the consumption component fluctuated significantly, averaging about 3.5% growth from 2020 to 2022. In 2023, consumption became the primary contributor to China's economic growth.

▲ Data source: Wind, compiled by FreeS Fund

▲ Data source: Wind, compiled by FreeS Fund

The sustained increase in domestic demand and slowing exports align with the direction of China's economic structural adjustment.

If we compare China's economy to a building, the foundation at the bottom represents the basis for economic growth, the pillars in the middle are the drivers of growth, and the ceiling at the top represents the ultimate form of economic growth, with its structure reflecting the proportional scale of different economic models.

Before and including 2015, domestic demand and foreign trade each contributed roughly one-third to the economy. However, currently and going forward, domestic demand's contribution to China's economy may reach two-thirds, while external demand and internationalization may account for only one-third.

/ 02 / When We Discuss 2023 Consumption, What Are We Really Discussing?

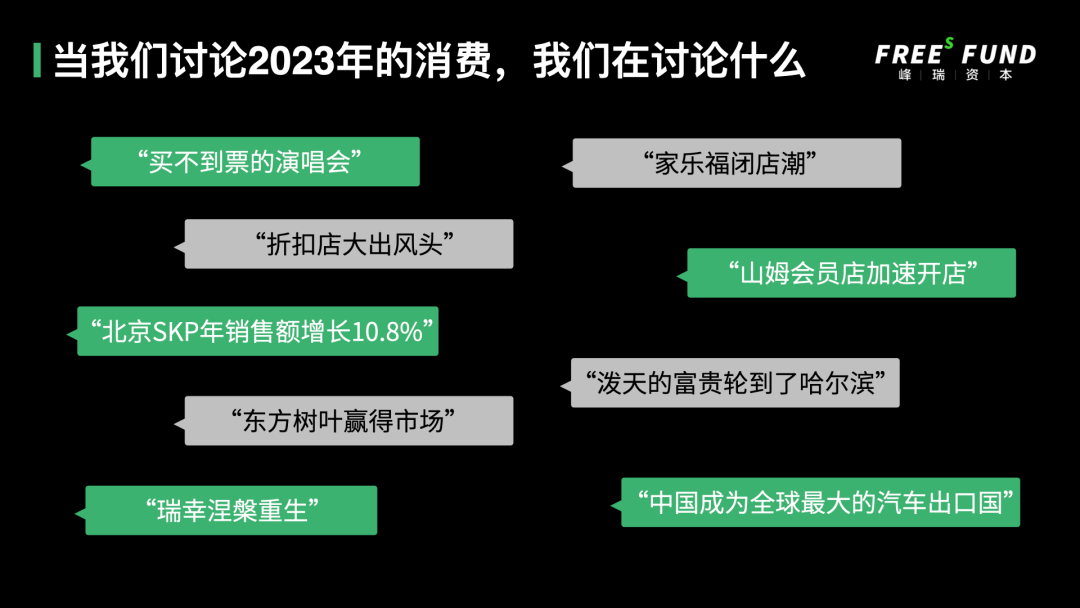

Looking back at the past year, China's consumer market produced many emblematic phenomena. For example:

- "Concerts where tickets were impossible to get"

- "Discount stores stealing the spotlight"

- "Beijing SKP's annual sales up 10.8%"

- "Luckin Coffee's phoenix rise from the ashes"

- "East Leaf Tea winning the market"

- "Carrefour's wave of store closures"

- "Sam's Club accelerating expansion"

- "The 'heaven-sent fortune' finally reaching Harbin"

- "China surpassing Japan as the world's largest auto exporter"

...

Some of these phenomena appear quite contradictory, but they actually reflect post-pandemic consumer psychology — rationality and self-indulgence coexisting. People spent the money they needed to spend; they just changed how they spent it, becoming more focused on personal feeling and experience. Put bluntly: "I don't necessarily need others to think I'm doing well; I need to feel good about myself." For example: although everyone talks about consumption downgrading, when we travel during the May Day and National Day holidays, we still inevitably book very expensive hotels, and we still walk into SKP to pay premium prices for luxury department store goods; although everyone wants to save money, we're still willing to shell out big bucks for sold-out concerts.

The year-end hottest consumption phenomenon, "the heaven-sent fortune finally reaching Harbin," also illustrates this psychology. Not long ago, I was chatting with a highly accomplished marketing professional who happens to be from Harbin. He had two fascinating observations about Harbin's tourism boom.

First, China entered a new phase around four or five years ago where people are willing to pay for experience and emotional value, not merely pursuing brand recognition or "looking good to others." This is one of the most important consumer trends of the present and future. Perhaps precisely for this reason, combined with the personality traits of Northeasterners, this heaven-sent fortune finally reached Harbin. He said, look — the South opened up earlier in reform and has better economic development, with finer service quality and commercialization, but one major characteristic of Harbin people representing Northeasterners is "I only have face if you're happy," so they created a service experience that "spoils" tourists, or rather, people provided a different kind of emotional value.

Harbin's explosion is one example of the rise of services; Sam's Club's counter-trend expansion is an example of retail's upward momentum. Over the past three years, offline supermarkets have faced considerable challenges, with many traditional retailers experiencing waves of closures. Yet Walmart China achieved rapid sales growth through Sam's Club. Compared to traditional supermarkets, Sam's Club is clearly not the cheapest, its product range isn't particularly extensive, and its selection may not follow internet viral trends. Still, it became the main source of Walmart China's performance growth, opening nearly 50 stores in China, including several in non-first-tier cities. To some degree, this means Chinese consumers have reached a stage where "I don't want more choices; I want good things, and I'm willing to pay a premium for what I consider good."

/ 03 / China's Unique Consumer Innovation Opportunities

In the consumer investment space, 2020 to 2021 was one of the hottest periods for consumer investment. At that time, popular consumer brands fell into two categories. The first were traffic-operation types: as long as you poured money into buying traffic, GMV would grow. Although ROI would decline, and repurchase rates and margins might be unsatisfactory, the results came fast — money in, growth out. The second were product-driven types, relying on competitive products to win consumers, achieving brand repurchase and longer user lifetime value. Compared to the former, this approach was more demanding, possibly slower to develop, but unquestionably more sustainable.

Returning to the present, one long-term trend in consumer innovation is that consumer entrepreneurship is increasingly beginning to integrate with technology. The underlying logic is that however hot technological innovation becomes, its ultimate outlet — or the end of the tech industry chain — has essentially only two destinations: military and consumer. Among these, the consumer market is undoubtedly the largest in scale.

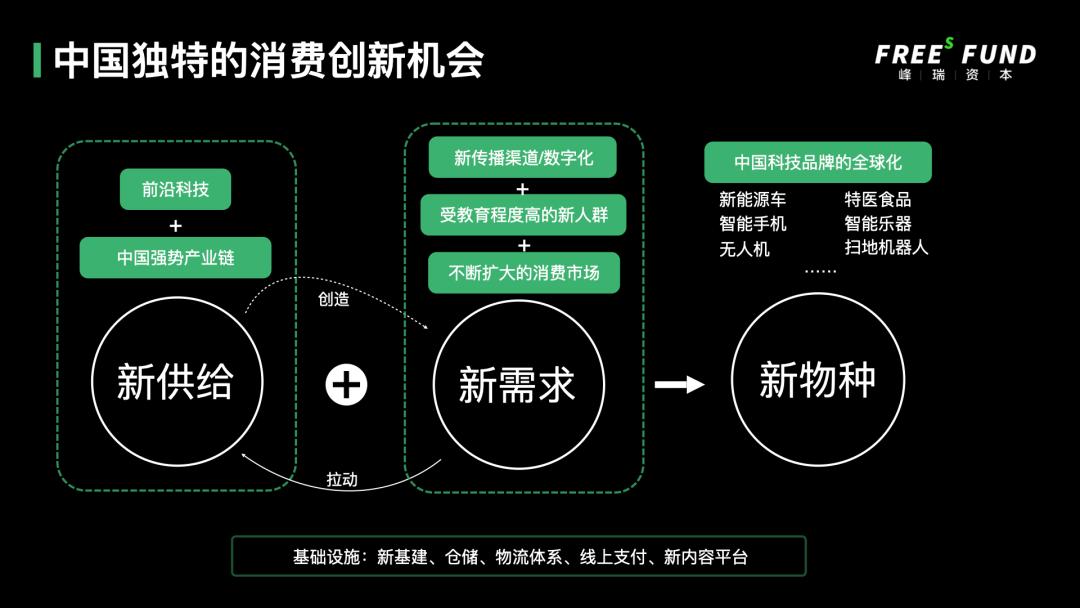

China's consumer innovation has its unique characteristics:

First, China possesses rich underlying infrastructure, including new infrastructure, warehousing, logistics systems, online payments, new content platforms, and more, providing solid support for the integration of technological innovation and commercial implementation.

Second, on the supply side, in the process of becoming the world's factory, China has accumulated long and comprehensive industrial chains with cost-effectiveness. When these industrial chains combine with cutting-edge technology, they can create many new forms of supply unlike anything before. This integration not only improves production efficiency but also gives rise to new products and services.

Third, on the demand side, despite frequent talk of consumption downgrading, China's consumer market continues to expand. In 2023, total retail sales of consumer goods reached 47.1495 trillion yuan, up 7.2% year-over-year. In one of the world's largest single-country consumer markets, communication channels continuously iterate and broaden, with internet penetration leading globally. As higher education becomes more widespread, China's core consumer demographic has far greater understanding of technology and information than before. Based on this, various new demands continuously emerge.

Thus, new supply creates new demand, new demand pulls new supply, bringing new growth — this has become a new cycle. The representative industries of new tech consumer goods we see today, such as new energy vehicles, smartphones, robot vacuums, and so on, have all gone through this development process. These new species combining tech manufacturing with production, and with services, are things that can be done better only in China. Moreover, representative enterprises that prevail in China's intense competitive environment have the opportunity to go global and become international companies representing China.

Take new energy vehicles as an example. In 2023, which just passed, China surpassed Japan to become the global leader in auto exports, including new energy vehicle exports. Behind this, China's auto industry experienced several key developments:

On the supply side, starting in 2003, China became a major global producer of auto parts, but primarily in low-to-mid value-added segments. As the auto industry underwent structural transformation — from internal combustion engines to battery power — China's auto industry chain continuously upgraded, gradually mastering core technologies for new energy vehicle batteries and motors, and achieving leading positions in complete vehicle manufacturing.

On the demand side, in 2009, China became the world's largest new car market, and in 2023, China was the world's largest new energy vehicle market for the ninth consecutive year.

So China first became a manufacturing powerhouse in low-to-mid value-added auto segments, then became the top auto-consuming country, and only then, when the auto industry shifted from gas to electric, did we achieve the corner overtaking that makes our new energy vehicles number one globally. In many other industries, there are opportunities to be "redone" and recreated like new energy vehicles.

Let me give two examples of early-stage projects FreeS Fund has invested in recently.

One company is called SPEEDIANCE, which makes intelligent strength training equipment. When doing strength training, traditional fitness products tend to use physical weight — hence the term "pumping iron." SPEEDIANCE uses direct-drive motors to achieve digital weight. The reason it can achieve digital weight is that thanks to the development of new energy, robotics, and other industries in China, Chinese motors have achieved globally leading cost-effectiveness and reliable performance. Digital weight brings many benefits: on one hand, it fully digitizes strength, so everyone's training can become personalized; on the other hand, it doesn't require constant coaching presence and protection, saving labor costs, and from this angle it also transforms fitness services. (Welcome to read "Consumer Innovation Never Sleeps: How to Leverage Interdisciplinary Approaches to Create New Categories? | FreeS Fund VC Dialogue") In 2023, SPEEDIANCE's sales both domestically and internationally exceeded expectations.

Another company is called Dair Music, focused on smart musical instruments. Founded in 2016, when we met the team, their motion-sensing drum kit product had already been popular overseas for quite some time. The reason they're called motion-sensing drums and digital guitar is that Dair uses motion-sensing capture technology and digital audio synthesis technology to change the usage habits and sound production methods of traditional instruments. This is also using technology to redefine traditional instruments.

Although these companies are still in early stages of development, they all rely on technology and traditional industry chain upgrades to create new products and meet new demands. The demands they satisfy happen to be exactly the rationality and self-indulgence I mentioned earlier — "I want to feel good about myself."

/ 04 / Three Slow-Moving Variables Affecting China's Future Consumption

When studying consumption and domestic demand, population is an important factor that cannot be ignored. Looking further ahead, population structure and distribution are slow-moving variables affecting China's consumption over the medium to long term.

▎Rising urbanization rate of registered household population

In June 2022, the National Development and Reform Commission specifically noted in the "14th Five-Year" New Urbanization Implementation Plan that "urbanization is where China's greatest demand potential lies." By end-2021, China's urbanization rate of permanent residents reached 64.72%, while the urbanization rate of registered household population rose to 46.7%. The nearly 20 percentage point gap between these figures means roughly one-third of urban permanent residents lack local household registration. The increase in registered household urbanization rate will bring enormous economic opportunities. Changes in how these new registered residents consume and access urban public resources will accumulate into a deep-seated variable.

▎Labor migration from primary industry

Depending on statistical methodology, rural labor accounts for roughly 25% of China's total labor force. Among these, the proportion actually engaged in agricultural production is relatively low and gradually declining. Where this agricultural-related labor ultimately goes, where they live, which industries they transition to, their income levels, and how they consume — all of these will affect China's future consumption. This variable connects to the first slow-moving variable, because this original agricultural labor may migrate to cities and become new registered residents, facing a series of consumption issues including renting, home buying, education, and elder care.

▎Revitalizing the下沉市场 [lower-tier/sinking market]

According to the "14th Five-Year" New Urbanization Implementation Plan, even when China basically achieves urbanization, around 400 million people will still live in rural areas. Compared to urban populations, most rural populations have less asset-based income. In recent years, many policies have been introduced to promote the circulation of rural homestead land and farmland, enabling farmers to obtain income security beyond wage income. When farmers' income sources increase and the sustainability of asset-based income improves, their consumption patterns will change. They may more easily settle in towns and cities, and with deepening household registration system reform, they can also begin working and consuming as urban residents.

These three variables concern the survival and development of several hundred million people. Whether or not we can personally relate, where these hundreds of millions ultimately live, work, and consume relates to how China's consumer market will change, and how China's urbanization will advance.

/ 05 / How Will 2024 Spring Festival Consumption Fare?

With the 2024 Spring Festival approaching, we can hazard a guess at how this year's festival will be and how it might differ from last year.

Since 2023 was the first Spring Festival after COVID restrictions were lifted, the wave of homecoming reunions created 4.733 billion person-trips in total social mobility, with self-driving travelers also hitting record highs surpassing 2019. For the 2024 Spring Festival, both tourist trips and total consumption should maintain relatively high levels, possibly even exceeding pre-pandemic 2019.

First, looking at the three short holidays of 2023 — May Day, National Day, and 2024 New Year's Day — people are eager to travel and quite action-oriented. Additionally, the 2024 Spring Festival holiday structure is somewhat unusual. Although still seven official days, the last working day is New Year's Eve, and companies will basically let out early, so we can understand it as an eight-day holiday. This holiday structure may somewhat affect people's travel plans. Perhaps everyone will have the chance to get around — whether going home, traveling, or even splitting the Spring Festival holiday in half to both reunite with family and travel. We'll wait and see what new changes and opportunities this Spring Festival brings.

Engagement Giveaway

What are your thoughts on the 2023 consumer market? What innovation opportunities have you observed in the consumer space? By 17:00 on January 30, the five readers with the most thoughtful comments will receive a FreeS Fund New Year gift (including two books).

▲ A Tumultuous 2023: Courage and Aspiration | FreeS Fund Year-End Special

▲ Toward 2024: How We Think About AI Entrepreneurship and Investment | FreeS Fund Year-End Special

▲ Li Xiang × Li Feng: Stripping Away Emotion, Discussing Economic Variables in the Second Half of 2023 | Li Feng Column

▲ Li Xiang × Li Feng: From Purified Water to Pure Tea Beverages, A Research Sample of China's Consumption Upgrade | Li Feng Column

▲ Li Xiang × Li Feng: Institutional Reform, Silicon Valley Bank, GDP Targets, Money Flows... Discussing Recent China-US Macro Hot Topics | Li Feng Column

▲ Li Xiang × Li Feng: The Dollar's "Monopolistic Success" and "Gradual Dilemma" | Li Feng Column

▲ Expansion or Store Closures, Re-examining Offline Opportunities | Li Feng Column

Star the FreeS Fund WeChat Official Account for timely business insights