FreeS Fund's Li Feng 2025 Year-End Share: The Logic and Outlook of AI Investment

Why Is This AI Boom Unprecedented? What Happens Next for AI Investment?

By the time you read this, 2025 is already in its final countdown, another year drawing to a close. Three years have passed since ChatGPT burst onto the scene in November 2022. In 2025, AI remains the most closely watched keyword in venture capital and startup circles. Time has given us many answers, but left us with even more open questions. Notably, China's position in this wave of AI has undergone a critical shift.

Against this backdrop, on December 17, 2025, at the FreeS Fund Annual Investor Summit in Shanghai, Li Feng (known as "Uncle Feng") delivered a keynote titled "The Logic and Outlook of AI Investment," sharing his observations and reflections on AI investing over the past two years. His topics included:

- Will AI trigger a genuine productivity revolution?

- Will artificial general intelligence (AGI) be achieved in the near term?

- What makes this AI boom unprecedented?

- What are the typical three stages of technology investing? What is the investment logic for the AI era?

- If AI enthusiasm cools in the US, will market sentiment transmit to China? If so, how can China chart an independent course?

- What are China's structural advantages in this wave of AI?

- Beyond AI, what shifts occurred in biotech and pharma in 2025, and what opportunities belong to China?

We've compiled selected insights and reflections for discussion. There are no standard answers when it comes to AI — we hope to offer one angle of thinking. A momentous 2026 awaits, and we look forward to walking alongside more innovators. Reach us at bp@freesvc.com.

AI Research Series

- Looking Ahead to 2026: What Innovation Opportunities Await in AI?

- The Hotter the Robotics Track Gets, the More We Need to Respect Its Rules

- How Can AI Hardware Startups Survive the Data Desert?

Reader Giveaway

What did AI mean to you in 2025? What are your most common use cases, and what unexpected gains or insights have you discovered? Share your thoughts in the comments. By 5:00 PM on January 5, 2026, the six most interesting responses will each receive a copy of the latest FreeS Fund Industry Research Handbook plus a book recommended by Uncle Feng.

/ 01 /

Two Open Questions About AI

When it comes to AI, two open questions come up repeatedly. First, will AI drive a productivity revolution? Second, can AGI be achieved soon? Everyone can have their own answers. Here, we'll venture ours as well.

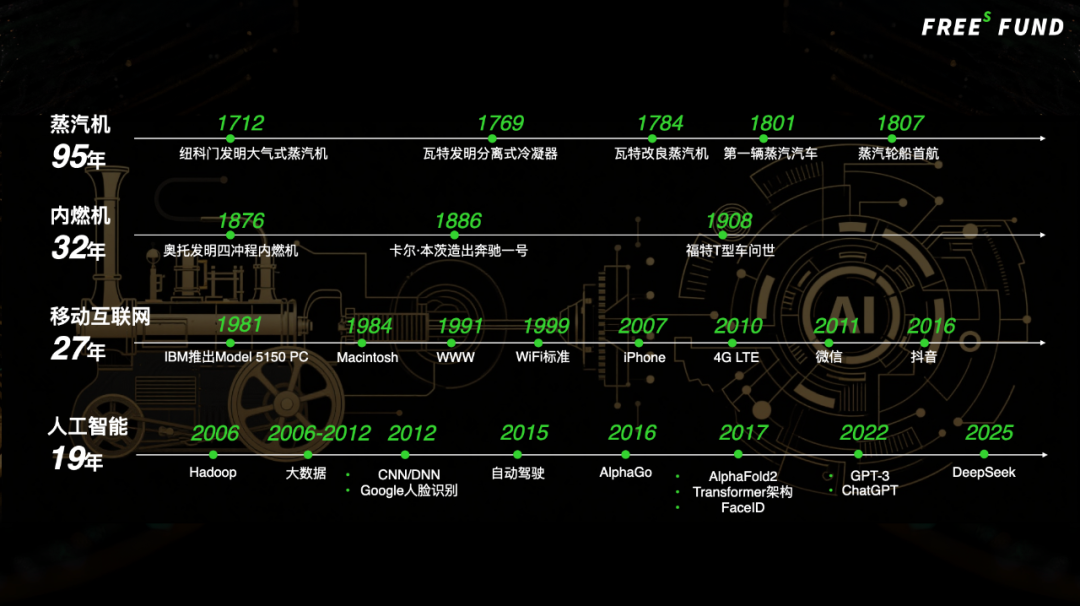

Why is competition between China and the US in AI so fierce? Underlying it is a "global consensus" — that AI may unleash a productivity revolution. Whether this consensus actually holds remains too early to call definitively. But assuming it does, a look back at previous productivity revolutions reveals something: from gestation and germination to full-blown explosion, a productivity revolution usually takes longer than most people expect.

Take the steam engine era. From the invention of the atmospheric steam engine in 1712 to the first steam-powered automobile, then to the maiden voyage of the first steamship — nearly a century elapsed.

Or consider the internet and mobile internet eras. From IBM's launch of the first personal computer, the Model 5150, in 1981 to the iPhone, and then to WeChat becoming a national-level app — roughly 30 years.

Now look at the AI era. Its beginning wasn't marked by some algorithmic breakthrough, but by the formation of data infrastructure. The emergence of Hadoop in 2006 made it possible to preserve massive datasets long-term, process them at low cost, and convert them into computable resources — laying groundwork for subsequent AI development. From Hadoop's debut to now, less than 20 years have passed. The first six years (2006–2012) focused mainly on building that data infrastructure: how to store massive data cheaply, how to conduct reliable distributed computing. Strictly speaking, this wasn't AI; it should be defined as "big data." So, rigorously speaking, the AI era dates from 2012 — only 13 years to date. Compared to the maturation cycles of historical productivity tools, this is relatively short. We can reasonably say that the systematic transformation of AI into productive force remains in its early stages.

/ 02 /

What Makes This AI Boom Unprecedented? A Macro Perspective

We just noted that the systematic transformation of AI into a productivity revolution is still in a very early stage. So some might wonder: if that's the case, why does this AI boom seem so unprecedented? I think we need to look at this from a macro perspective.

I. 2020–2021: Unprecedented Monetary Easing by Global Central Banks

Let's rewind six years.

In 2019, global stock market capitalization stood at roughly $89 trillion, roughly on par with global GDP of about $86 trillion. US market cap was $34 trillion, accounting for over one-third of the global total.

Historically, this structure remained within a relatively reasonable range. The reason for calling it "reasonable" references an indicator Warren Buffett proposed for measuring a country or region's overall capital market valuation — a country's total stock market capitalization divided by its GDP, known as the "Buffett Indicator."

In Buffett's view, when this ratio falls between 80% and 120%, overall market valuation roughly matches the real economy; significantly below suggests undervaluation; significantly above may signal bubble risk.

By this standard, 2019's roughly 1:1 ratio of global market cap to global GDP sat squarely in the reasonable zone.

Then what happened?

We all remember. In 2020–2021, hit by the pandemic, central banks in several developed economies adopted extraordinarily loose monetary policy, triggering an unprecedented global "liquidity flood."

How much "water" are we talking about? In 2020 alone, the combined balance sheet expansion of the Federal Reserve, European Central Bank, and Bank of Japan reached roughly $8 trillion. TradingView data further shows that around this period, major global central banks expanded their balance sheets by roughly $12 trillion total.

A brief explanation of "balance sheet expansion" — it's not simply "printing money." Central bank balance sheet expansion is essentially base money injection. By purchasing government bonds, corporate bonds, or providing liquidity to the banking system, central banks expand their balance sheets. These funds first enter the banking system or fiscal departments, representing the most foundational, primitive layer of liquidity in the monetary system. When this base money begins circulating into the real economy through bank credit and other channels, it generates a money multiplier effect.

A simple example: a bank lends to households, who don't spend everything and deposit the remainder back in the bank, which may then lend it out again. As money circulates through the system in multiple rounds, the broad money supply ultimately becomes far larger than the initial injection.

Given China's financial system's heavy reliance on banks, its money multiplier tends to be relatively high, generally around 4 or 5. In the US, where capital markets play a larger role, the multiplier still reaches 3 or 4.

Taking the average of 4, the roughly $12 trillion "liquidity injection" multiplied by 4 yields nearly $50 trillion. An annual increase of nearly $50 trillion in global liquidity, compared to 2019's global GDP of $86 trillion — the former approaching 60% of the latter — is extremely rare in global economic history. This also explains why, despite the pandemic shock to the global economy in 2020–2021, stock markets in virtually every country performed strongly, China included.

II. 2022–2023: Incremental Capital Pushed to the Limit in Dollar Assets

The following year, 2022, was equally eventful.

First, in February 2022, the Russia-Ukraine conflict broke out.

This crisis hit Europe on multiple levels: at the base, energy security, as Europe could no longer rely on Russian energy supplies; in the middle, supply chain security, as energy shortages disrupted industrial production and supply chains; at the top, national security, with uncertainty over whether the conflict would spread to NATO and other regions.

At the time, there were even reports that some Germans were forced to stockpile firewood for winter due to natural gas shortages. So you can understand why, from February 2022 — especially the second quarter onward — the willingness of global liquidity worth tens of trillions of dollars to allocate to European assets dropped significantly.

In 2022, China was still implementing pandemic prevention and control measures, and in May 2023, the G7 summit in Japan hyped up China-related issues. This multifaceted uncertainty caused foreign capital to adopt a wait-and-see attitude toward Chinese assets in the short term.

In the global capital allocation landscape, the US, Europe, and China are the three most important markets. The result of Europe and China being temporarily underweight was that incremental capital was pushed to the limit in dollar-denominated assets.

What was happening in the US market at that time?

In March 2022, the Federal Reserve raised interest rates by 25 basis points for the first time, followed by three consecutive rounds of hikes in May–July of 50, 75, and 75 basis points — roughly 200 basis points (2%) in cumulative increases over three months. Normally, dollar rate hikes would already strengthen expectations of dollar and dollar-denominated asset appreciation, attracting global capital inflows; considering the situations in Europe and China, massive liquidity had almost nowhere to go but to concentrate in dollar-denominated assets, directly driving the sustained rise of the US stock market from the third quarter of 2022 onward.

So we see a remarkable phenomenon: despite three to four years of pandemic shock and overall very slow global economic growth, global nominal GDP reached $114 trillion (including inflation). Meanwhile, global capital market capitalization hit approximately $130 trillion, about 1.14 times global GDP, approaching the upper limit of the Buffett Indicator. Among this, US capital market capitalization ($68 trillion) accounted for more than half, significantly higher than other countries.

Those interested in macroeconomics might recall that in 2023 and 2024, many economists discussed the so-called "American exceptionalism" — the idea that the US economy showed unusual resilience against a backdrop of generally weak global economic performance.

One explanation is that this resilience stems from America's economic structure: financial and related services industries (including legal consulting, investment banking, M&A, fund management, etc.) account for roughly 20% of GDP, high-tech industries about 30%, with the two combined making up roughly half of GDP. Thus, against the backdrop of massive global liquidity inflows, asset prices in the financial and technology sectors benefited most.

Capital markets don't come out and say, "Asset prices are rising because there's too much global money concentrated in too few places." To rationalize such high valuations, some kind of "grand narrative" is needed — and AI, "born at the right time," became the most suitable choice.

We can see that since October 2022, the market capitalization of the US tech "Magnificent Seven" (Alphabet, Amazon, Apple, Meta, Microsoft, NVIDIA, and Tesla) has grown rapidly; the combined market cap of these seven sisters even exceeded the GDP of any single country outside of China and the US. Finance and technology pushed each other higher, and the wealth generated by finance and technology further boosted growth in consumer and services sectors, including spending on housing, food, clothing, transportation, and entertainment.

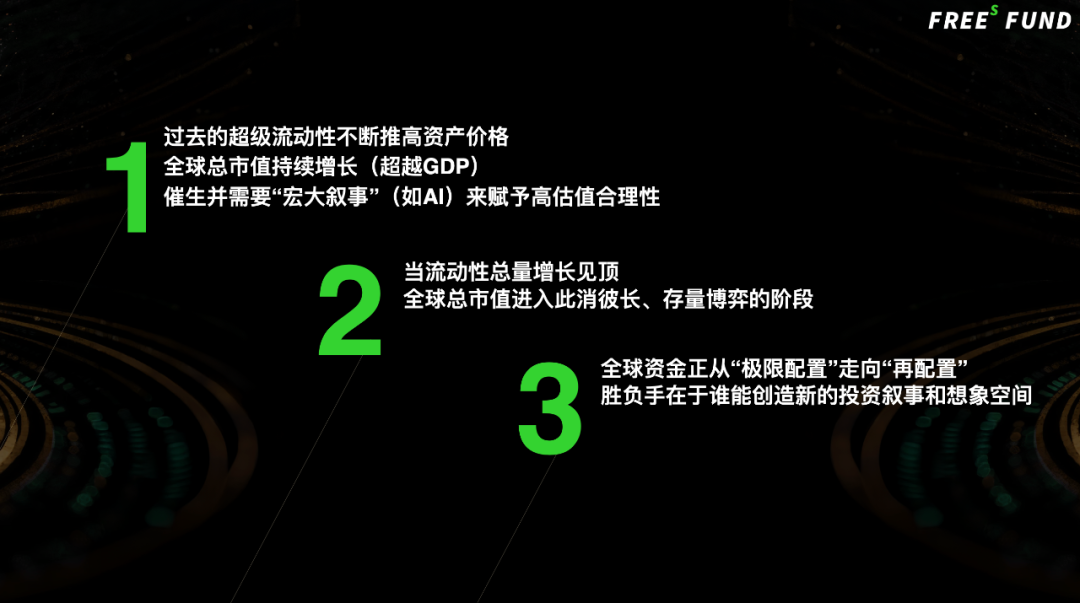

III. 2025 to Present: Global Capital Moving from "Limit Configuration" to "Reconfiguration"

Of course, the story doesn't end there.

Those who control large amounts of capital understand that big money doesn't stay concentrated in a single asset class indefinitely. Even early-stage investment institutions like ours wouldn't dare put all our capital into one hot sector. At certain stages, capital may concentrate, but eventually it will move from "limit configuration" to "reconfiguration."

Let's look at how this "reconfiguration" is happening.

From the end of Q3 2024, as the US election trajectory gradually became clear and expectations of Trump's possible return to office strengthened, markets began reassessing America's own policy continuity. Meanwhile, some major economies that had previously been under pressure showed signs of risk digestion. They all wanted to demonstrate their attractiveness to global capital to win higher allocation.

First, Europe. As market judgment on the Russia-Ukraine conflict gradually shifted from fear of escalation and spillover toward normalization of the conflict, and then toward assessing the possibility of phased de-escalation or even ceasefire — this shift in expectations and reduction in uncertainty, to some extent, formed the basis for European assets to be reconfigured. So even though Europe's economy in 2025 still showed virtually no growth, European stock market performance was superior to US stocks for a considerable period.

Then, China. Hong Kong stocks in 2025 ranked among the top globally across multiple indicators: fundraising scale, refinancing scale, number of listed companies, and market gains. Meanwhile, the continued advancement of financial opening and capital market institutional reform, AI breakthroughs represented by DeepSeek, the embodied intelligence frenzy ignited by humanoid robots appearing at the Spring Festival Gala, the private entrepreneur symposium, and a series of other events have continuously sent positive signals to the outside world, strengthening market confidence in Chinese assets.

Of course, the US doesn't want "big money" to run away either, so we've also seen the delicate tug-of-war in US tariff policy and the management of interest rate cut expectations.

So, we are currently in the midst of a financial vortex, whose essence is the reconfiguration of global assets. Almost all major countries or regions are using their own methods to "give reasons" to global capital: either telling capital "don't leave me," or telling capital "you can come here," or even "you should come here more."

This is the real picture of today's global financial markets.

I believe this logic will hold equally true in 2026. For a period going forward, if the world doesn't see another round of large-scale "liquidity injection" — that is, if total global capital market capitalization remains around $130-plus trillion — we will basically enter a kind of zero-sum "one rises, another falls" state: if A gets more, B and C get less; if A gets less, B and C get more. The decisive factor will be who can better create new investment narratives and room for imagination.

In this context, whether the stocks in your portfolio or your company's planned Hong Kong IPO next year can proceed smoothly may depend half on this round of global capital reconfiguration, and half on key variables such as China's domestic capital and policy environment, and the company's own development.

Investment Logic in the AI Era

Having covered the macro situation, let's return to investment itself. Currently, three topics about AI investment are generating heated discussion:

First, will America's AI bubble burst?

Second, if AI enthusiasm in the US cools and the bubble bursts, will Chinese AI assets be affected?

Third, if the impact is unavoidable, how can China's AI industry resist this impact and develop an independent trajectory?

To answer these three questions, perhaps we first need to examine: what kind of evolution cycle is this round of AI fever and investment going through?

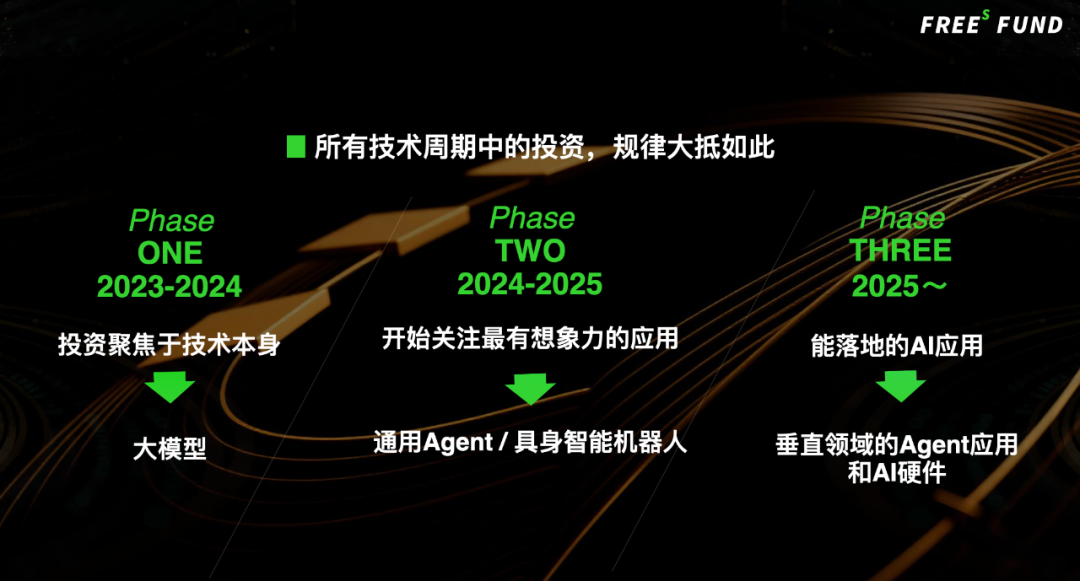

The preliminary conclusion is that virtually all technology-driven investments in the past, whether big data, facial recognition, or autonomous driving, have basically gone through three stages:

- First, investment focuses on the technology itself;

- Second, attention shifts to the most imaginative applications;

- Finally, applications that can actually be deployed.

Current large model and AI investment, as well as AI for Science investment, should be no exception.

I. Three Stages of AI Technology Investment

1. First Stage (2023–2024): Investing in technology itself. Especially in 2023, market discussion and investment were almost entirely concentrated on large models themselves. The characteristic of this stage was technology making leapfrog progress, with expectations constantly being refreshed. However, no technological progress can continuously exceed expectations indefinitely. When technology completes a key leap and reaches a new plateau, it tends to enter a period of linear development. Thus, investment moves to the second stage.

2. Second Stage (2024–2025): Investing in the most imaginative applications. For AI, the most imaginative things fall into two categories: First, general-purpose intelligent agents (AI Agent), attempting to help humans complete operations in the virtual world; second, humanoid robots in the physical world, i.e., embodied intelligent robots, attempting to replace and assist humans in completing various tasks in the real world. These two directions became focal points because their room for imagination covers virtually "everything humans can do." But "most imaginative" has another side: they are not so easy to scale and deploy. This is easy to understand — if they could be immediately deployed and quickly monetized, they wouldn't be called the "most imaginative" directions.

3. Third Stage (2025 to present): Investing in applications that truly deploy and can make money. When the market enters this stage, technology applications become more grounded, and the valuation logic for a project shifts from "storytelling" to "doing the math." Current AI investment has already begun moving toward this stage. In evaluating a project, the questions we need to answer are:

- Who can use this technology today?

- Who can push it to thousands or tens of thousands of users?

- Who can make users willing to pay for it?

Specific to FreeS Fund's investments, those who have communicated with us frequently know that FreeS has concentrated its layout in embodied intelligence, AI applications (AI hardware, vertical-domain AI Agents), AI infrastructure, and AI + new drug R&D and AI for Science. Taking embodied intelligence as an example, before investment in this area became hot, we had already begun concentrating our efforts and explicitly proposed internally to "invest wherever possible." A bit regrettably, we were still somewhat conservative, causing us to hit the brakes too early. In July 2024, we were already discussing internally that robot investment was overheating and that further investment in robot bodies should be cautious. As it turned out, the heat in this direction continued for more than another year. Then from the end of 2024, we began investing in AI hardware. When we first started investing in this direction, we could say we invested quite comfortably: because no one was competing, we could think slowly and look carefully. Valuations were still relatively easy to negotiate then, but in the most recent quarter, the market has become very hot, rapidly evolving into a state of "fighting for allocation."

II. AI Investment — What Happens Next?

So, a new question arises: if this cycle has already reached the third stage, what happens next?

First, we need to be clear: any major technological transformation in the history of technology does not go through just one round of the three stages mentioned above before ending, but rather multiple rounds of three-step cycles. The more rounds it goes through, the deeper the penetration and greater the influence of that technological transformation on society and the economy.

The internet is a classic example — it went through multiple cycles and is now deeply embedded in virtually every aspect of our daily lives.

Returning to AI, we can think together about how these next three stages might develop.

First Stage: Will Large Models' Next Step Be a Hundred Flowers Blooming, or Winner Takes All?

If you've been paying attention to news in the past month, you'll notice a very obvious change: discussion around large models has almost entirely concentrated on major companies. Whether Google's Gemini, Alibaba's Qwen, or ByteDance's Doubao, the center of the stage basically belongs to the headliners.

Why is this happening?

The reality is, if a technological transformation remains confined to "the technology itself" without fundamentally reshaping front-end product forms and end-user habits, large companies can usually close the gap through sustained spending, eventually catching up and even surpassing early movers.

The big data era illustrates this well. You'll notice that while some companies successfully went public during the big data wave, no new hundred-billion-dollar companies have emerged from it. One key reason is precisely what I just mentioned: big data didn't bring fundamental changes to front-end UI (user interface) or trigger shifts in user behavior.

Douyin is the exception. As a company built on big data recommendation, Douyin's path to hundred-billion-dollar valuation can be examined from a different angle:

First, the technology changed — information distribution shifted from search engines to big data recommendation.

Second, the UI changed — from typing keywords on a keyboard to swiping with a finger.

Third, user habits changed — from sitting at a PC to using the internet on mobile devices, in fragmented moments throughout the day.

Looking at other great hundred-billion-dollar companies in history — Microsoft, Google, Tesla — they all benefited from simultaneous changes across the front end (UI), middle layer (technology), and back end (devices and user habits).

Microsoft's success wasn't just about PCs; it was about bringing graphical software operating systems to the mass market through the mouse, an entirely new device and experience. Google combined keyword input as a new interaction paradigm with web search and early AI technology, reshaping how people access information. Tesla similarly didn't merely add autonomous driving to cars; through "software-defined vehicle UI," it completely transformed human-vehicle interaction.

Returning to large models: is "the big companies' opportunity" a temporary outcome or a lasting trend?

Currently, large models are moving toward "cloudification." That is, they're no longer a point-product competition but gradually evolving into foundational infrastructure, much like hardware clouds. If this logic holds, we can almost certainly conclude that the competitive landscape will consolidate among first-tier giants.

Only they simultaneously possess:

- The ability to sustain massive capital expenditure on compute and data centers over the long term;

- Mature cloud infrastructure and vast user bases already in place;

- Capacity for continuous large model R&D investment;

- The ability to sell large models as software capabilities directly "bundled" with foundational cloud services.

Whether this truly comes to pass — we may not have to wait long, perhaps we'll know by next year.

To summarize, a technology innovation cycle doesn't automatically spawn a wave of hundred-billion-dollar companies. It depends on whether front-end, middle-layer, and back-end changes occur simultaneously, and whether consumer habits genuinely shift. If the answer is no, the technology dividend tends to be rapidly absorbed by incumbents through resources, capital, and scale advantages, ultimately devolving into competition among existing players.

Stage Two: Can Robots Break Through in Manipulation Capability?

The robot demos we see today mostly focus on boxing, running, jumping, dancing, playing soccer — these are all demonstrations of locomotion capability. Behind the advancement of robotic locomotion lie two key drivers: first, hardware progress in motors, sensors, and other components driven by industries including new energy vehicles; second, algorithmic improvements from autonomous driving and reinforcement learning.

What needs emphasis is that today's robots can compete on locomotion, but they struggle with manipulation.

"Manipulation" refers to grasping objects, using tools, changing object states — truly "doing work." Why is manipulation the current weak point? The main reason is that manipulation involves complex interaction between robots and the physical world, and we have virtually no directly transferable accumulated experience here.

You might say we've seen plenty of impressive demo videos of robots folding clothes, chopping vegetables, or pouring coffee. But these tasks mostly involve manipulation of fixed objects with clear limitations.

For example, a robot folding clothes on a table — suddenly change the table height, and it may no longer be able to fold.

Or having a robot pour water: how much water is in the cup? Is the cup soft or hard? Is the water cold or hot? At what tilt angle does water spill? The material, weight, state, and force feedback involved — none of this data has been systematically collected for robots.

The problem is, if we can only solve locomotion, robots are limited to scenarios like transport and inspection, unable to take on the general task of "helping people with all kinds of things." So further iteration in robotics inevitably requires breakthroughs in manipulation capability.

One approach resembles the "autonomous data collection" used in autonomous driving.

However, this method has clear advantages and disadvantages: the upside is data reusability; the downside is low collection efficiency. Beyond Tesla, which has deployed millions of vehicles globally enabling large-scale, real, and diverse data collection, most automakers still rely on smaller test fleets with obvious limitations in data volume and scenario diversity.

One challenge is that robot hardware hasn't standardized yet — any design change, such as five fingers to three, three to two, two to gripper, or altered joint movement patterns, can invalidate previous data and training results, requiring fresh collection and training.

Another category of methods involves synthetic data and VLA (Vision-Language-Action), which certainly help, but with clear limitations.

Take VLA — I'll use an analogy. I love playing badminton. I've watched and studied every match available, yet my skill level never advances to national-athlete caliber. That's because the conversion chain from Visual information to Language understanding to Action execution doesn't automatically complete through data accumulation alone; it involves complex perception, cognition, and execution processes. Robots face similar challenges.

Additionally, physical models as a route for training robotic manipulation have garnered significant attention. I believe physical models are certainly necessary, since robots must change objects' physical states. But improving robotic manipulation capability cannot rely solely on algorithms plus "brain."

If the problem could truly be solved by algorithms plus brain, large language models would have emerged long ago. In fact, the breakthrough in large models didn't stem merely from algorithmic innovation, but from learning across 40-plus years of gradually accumulated massive internet text data.

Referencing the evolution of past technology waves, the birth of many internet super-apps was inseparable from the proliferation of smart devices equipped with high-precision, low-cost, low-power chips and sensors.

For instance, WeChat's emergence depended on microphone arrays in smartphones enabling clear voice parsing; ride-hailing apps became possible when GPS chips were installed in every phone, making real-time location data accessible; the rise of Douyin, Kuaishou, and Meitu relied on high-definition, variable-focus optical cameras becoming widespread in smartphones. As these applications proliferated, vast new-dimension data was generated.

Therefore, regardless of technical approach, breakthroughs in robotic manipulation capability depend on access to rich new-dimension data — and the acquisition of this data is closely tied to the AI applications we'll discuss next.

Stage Three: AI Applications That Can Land

The AI applications we currently invest in fall roughly into three categories: AI infrastructure, vertical-domain AI Agents, and AI-driven smart hardware.

Direction One: AI Infrastructure, i.e., AI Chips

Looking back, new applications always spawn new infrastructure — chip giants.

In the era when PCs were the sole hardware, "affordable personal computing" became the core need, making Intel. Subsequently, the proliferation of internet gaming and video content demanded far greater high-performance graphics and image processing capabilities than ever before, giving rise to NVIDIA. Later, as smartphones became the new core terminal, with highly diverse form factors and power consumption and integration becoming key constraints, the chip and infrastructure system iterated accordingly — Qualcomm, Broadcom, and others stepped into the spotlight during this phase.

Returning to the present, once AI truly moves toward application, data storage, communication, compute, power consumption, cost, and form factor will be redefined. This combination of needs, entirely different from NVIDIA's server-side focus, will almost certainly give birth to new, highly verticalized AI infrastructure chip opportunities, spanning inference, server-side, and edge-side applications.

Direction Two: Vertical-Domain AI Agents

Building vertical-domain AI Agents typically requires satisfying two conditions simultaneously:

First, the industry and its supply chain must already possess relatively high digitalization levels — preferably with business processes, data flows, and customer interactions already online and structured.

Second, its service value must be deliverable through natural language interaction.

Industries like education, psychological counseling, and financial services fit these two conditions well.

But in practice, vertical Agents are better suited for transformation by existing companies. The reason is simple: these companies already possess real business flows, stable data streams, and existing customers, plus the technical capability to transform business and products — including re-abstracting cheap, usable models adapted to their operations.

Of course, over the past two to three years, some promising new directions have emerged: fully digitized e-commerce live-streaming Agents, fully digitized programming Agents, and fully digitized gaming Agents.

Overall, vertical Agents are more likely to become "second growth curves" for mid-sized companies, enabling both "revenue expansion" and "cost reduction." Opportunities in entirely new tracks currently appear difficult to find, with the core challenge being the lack of long-accumulated data and stable customer foundations.

Direction Three: AI-Driven Smart Hardware

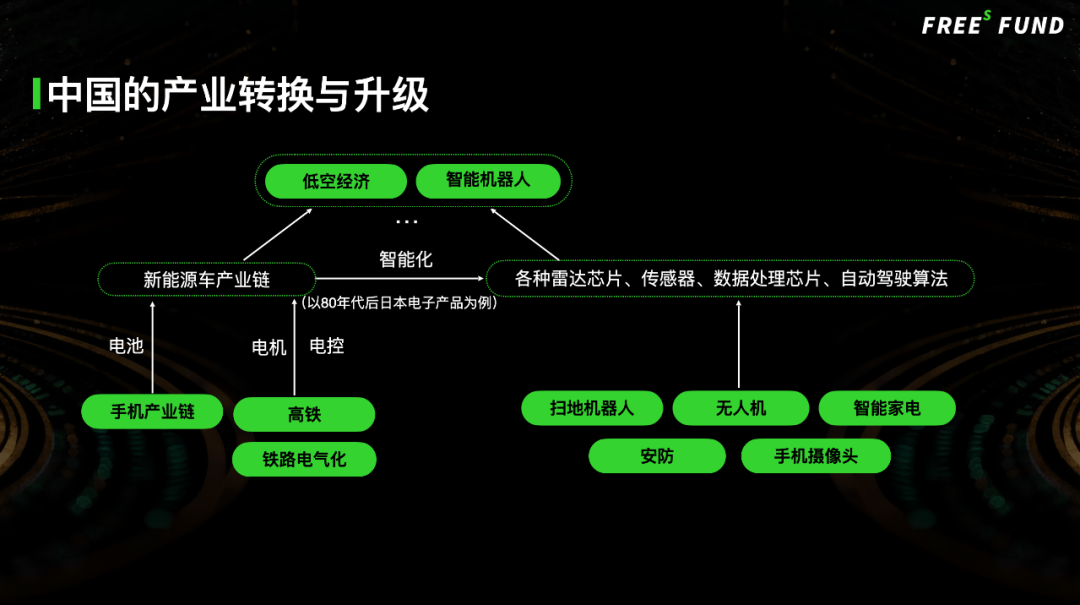

The image below illustrates the opportunities China currently faces in the smart hardware direction.

In the 1980s, Japan pulled off something remarkably successful — electrification. They systematically converted mechanical products into electronic ones: pianos became synthesizers (Yamaha), watches became digital watches (Casio), cameras became point-and-shoots (Canon). But Japan's industrial upgrade stalled at that electrification layer. There simply weren't enough rich, high-quality, affordable sensors and chips to support the next leap into true intelligence.

A simple example: moving from a broom to a vacuum cleaner is electrification; moving from a vacuum cleaner to a robot vacuum that can autonomously navigate your home is genuine intelligence.

The automotive industry is now heading down the same path. New energy vehicles have already gained significant penetration in China. On top of that foundation, with the official release of L3 conditional autonomous driving standards (on December 15, 2025, the Ministry of Industry and Information Technology announced China's first batch of L3-approved vehicle models), cars are becoming deeply integrated sensor and computing platforms — making the leap from "electrified products" to "intelligent terminals."

So China today is positioned not only to do what Japan did decades ago — systematically "rework" traditional products that haven't yet been electrified — but more importantly, to take already-electrified products and upgrade them further into intelligent systems.

The data continuously generated through this intelligence process happens to be precisely the kind of new-dimensional data that is extremely valuable yet currently scarce for training next-generation embodied robots and intelligent systems. Unlike the internet text and image data accumulated over the past 40 years, this data originates from the real physical world, involving state changes and continuous actions. It has only just begun to be generated at scale, and its production depends heavily on the proliferation of consumer-grade smart hardware. This is a key reason why we have been steadily investing in AI hardware this year, and why investment activity in this space has noticeably heated up.

Overall, China excels at leveraging soft technology plus industrial chain capabilities to develop new products, stimulate new demand, and cultivate "new species" that emerge first in China. Any such new species that can survive China's fierce domestic competition has a shot at selling globally — and can continuously generate fresh data assets through real-world usage, creating a virtuous cycle.

This is China's structural advantage in the current wave of intelligence, and where the opportunity lies for China's AI hardware industry.

First, this round of intelligentization will continuously create vast new data dimensions. I've covered this above, so I won't belabor it.

Second, new demand driving new supply is evolving into a new form of Chinese export capability. These products target global markets with few comparable overseas competitors; the main rivalry is among Chinese companies themselves. Among such companies in our portfolio, most that have been operating for two to three years or more are already profitable.

Third, it helps maintain a reasonable manufacturing share. To achieve this requires two industrial chains operating in parallel: a high-efficiency manufacturing chain, and a high-efficiency chip and sensor chain. Only when these two chains achieve high-frequency, synchronized iteration within the same product system can truly globally competitive products be built, while supporting manufacturing's long-term maintenance of a healthy share. This capability is particularly crucial for China today.

China's successes in new energy vehicles, smartphones, smart home appliances, drones, and smart consumer hardware have already preliminarily validated this path. Meanwhile, the development of industries like smartphones and new energy vehicles has scaled up and upgraded upstream core component supply chains, laying a mature industrial foundation for AI hardware innovation.

So which companies are best positioned to capture this wave?

One category: companies with accumulated core technology. These firms have deep expertise in chips, sensors, and systems, with mature technical capabilities on the industrial side. When these capabilities are released toward consumer applications, they naturally possess the foundation to transition from B2B to B2C. We've already seen numerous portfolio companies successfully make this B2B-to-B2C shift.

Another category: companies that deeply understand consumer needs and technology trends. These new hardware companies typically start from consumer insight rather than technology-first, scene-second. By observing shifts in user habits and new opportunities for product integration, they can reverse-integrate hardware, sensor, and algorithm capabilities — making it easier to launch next-generation consumer smart hardware that actually lands in the market.

Around this logic, FreeS has already deployed capital in a batch of smart hardware-related companies. Conversely, we've invested relatively little in the currently hyped "AI-native hardware." My personal view is that no hardware can be AI-native from day one; the smart hardware that has been genuinely validated as successful was never built overnight.

Take Apple as an example. Before the iPhone came the iPod; before the iPod, MP3 players laid groundwork; and before that, in Japan's electrification wave I mentioned earlier, boomboxes were transformed into portable Walkmans. This is a process of continuous evolution. Apple's innovation didn't "descend from the heavens" — it was built on long-term accumulation of technology and user habits.

The smartphone's development path was similar: from feature phones, to shanzhai phones, to the smartphone era, user habits were gradually "educated." At first, phones were just for calls and texts; then people started browsing Weibo, playing games like Angry Birds; and today, the phone has become the core terminal carrying WeChat, Douyin, and countless other applications.

/ 04 / If U.S. AI Hype Cools, What Becomes of China's AI Opportunity?

If you agree that AI will drive a productivity revolution — an innovation opportunity we must seize — then a natural concern follows: when U.S. AI enthusiasm cools, or when the two distinctly American waves of large models and agents begin to retreat, will their risk appetite and market sentiment transmit to China? Can China's AI industry forge an independent development path?

I'm on the optimistic side. It's true that at the starting phase of this large model and AI wave, the U.S. was unquestionably the technology leader, and China held no advantage in underlying model capabilities or compute resources. However, as the wave advances into the engineering deployment and application-driven stage of technological innovation, I believe China has the potential to rapidly catch up, and even surpass in certain directions.

Take facial recognition as an example. When it first emerged, conventional wisdom held that China couldn't catch up to the U.S. But by 2018, China had achieved comprehensive leadership at top conferences and journals. The reason: China pushed facial recognition applications to their limits — from hotel check-in, to transfer payments, to business registration changes, virtually every scenario was using facial recognition. This widespread real-world deployment ultimately enabled technological iteration and overtaking.

Look at autonomous driving. Before 2021, mainstream market judgment held that this opportunity belonged exclusively to Tesla, with little chance for others. Yet by 2025, as domestic new energy vehicle shipments continue scaling up, intelligent driving functions rapidly penetrate mainstream models, and multimodal sensors achieve scaled vehicle deployment, I expect that in another two years, there will be a different answer to who can deliver on autonomous driving technology and applications.

So, barring surprises, the next phase of large models and AI will likely follow a similar pattern: once applications fully deploy and achieve scale, China will have its opportunity to surpass.

/ 05 / In Biopharma, What Opportunities Belong to China?

One: Over the Past 5 Years, Chinese Innovative Drug License-Out Deals Have Exploded

Beyond AI's main track, biopharma has long been an important domain that FreeS closely watches and consistently invests in. In 2025, China's biopharma industry reached an inflection point — its "DeepSeek moment."

This qualitative shift shows up in the amounts global pharmaceutical companies pay for pipeline rights: in 2024, China accounted for slightly over 30%; in the first three quarters of 2025, of the $191 billion in global pharmaceutical transaction value, China-related deals contributed $93.7 billion, or 49%. Including the October transaction between Innovent Biologics and Takeda, total outbound licensing value for Chinese innovative drugs has surpassed $100 billion — a genuinely meaningful milestone.

Looking ahead, will China's share in global innovative drug pipeline rights transactions continue rising, or fall back? My judgment is that from a long-cycle perspective, this proportion likely continues climbing. The current structure of China's innovative drug industry is analogous to where China's new energy vehicles or auto exports stood in the global market in 2022–2023.

Two: What's Next for Chinese Biopharma?

What happens next? Mainly three things.

The first is "faster and better." Once Chinese biopharma companies have found their path to monetization — how to make money — the next challenge is how to move pipelines faster and build more of them. The key to achieving this is new R&D efficiency tools, such as AI for Science.

The second is "more expensive" — meaning biopharma companies need to master new scientific discovery capabilities to enhance their potential for developing First-in-Class drugs. Tools like high-throughput single-cell sequencing, mass spectrometry, and high-throughput DNA synthesis platforms can accelerate experimental processes, generate more data, and significantly boost R&D efficiency and scientific discovery capability. This not only helps develop first-in-class drugs but also creates higher value in global markets.

The third is "more and better quality." This is the harder path: exploring scientific mechanisms that even the U.S. hasn't yet discovered, achieving truly leading scientific breakthroughs.

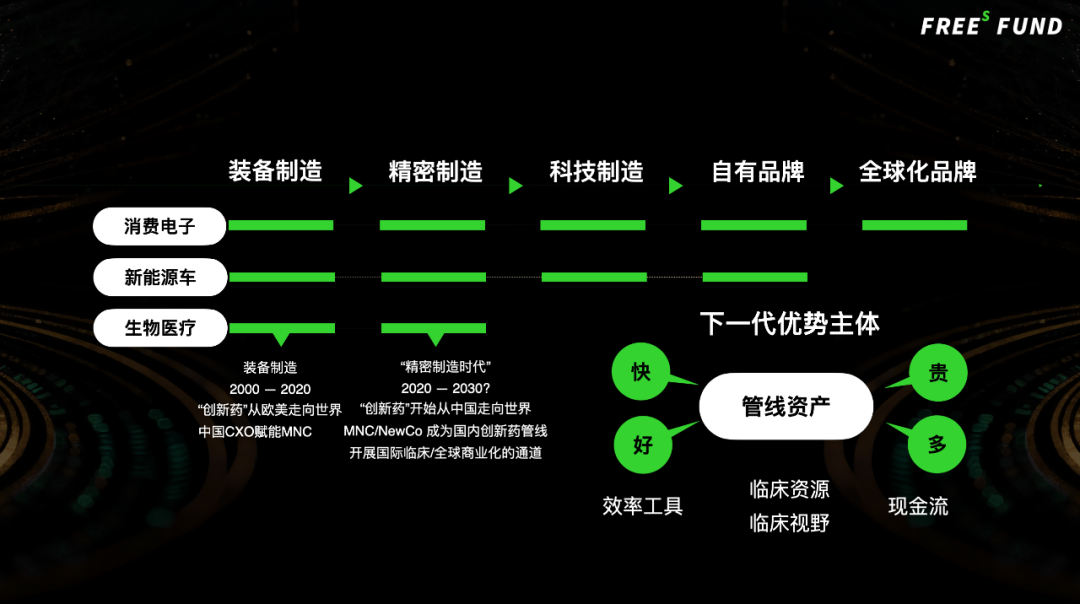

Three: From Precision Manufacturing to "Global Brands" — Will China Have MNCs in Biopharma?

If we place biopharma alongside the consumer electronics and new energy vehicle industries we often discuss, and view them through a more macro lens, we find that the evolution of China's major industries repeatedly validates a clear upgrade logic: starting from equipment manufacturing, progressing through precision manufacturing and technology manufacturing, and ultimately building proprietary brands and global brands.

Take consumer electronics as an example. Starting around 2000, China went through 25 years of development: from a global manufacturer of knockoff phones to producing globalized brands like Huawei, Xiaomi, vivo, and OPPO. Each leap took five to ten years. The reason China surpassed the US to become the world's largest single smartphone market isn't complicated: initially we lacked purchasing power, and even later we were hardly wealthy — but we had the ability to make products good enough and cheap enough, and market scale naturally followed.

New energy vehicles followed a similar pattern. If we take 2003, when BYD founded BYD Auto, as the starting point, the industry has spent roughly two decades upgrading its industrial chain. Most automakers have now reached the proprietary brand stage and are working hard toward becoming global brands.

Biotech will likely follow the same trajectory. China's biotech sector currently sits at a stage comparable to consumer electronics in 2010–2012 — transitioning from equipment manufacturing to precision manufacturing. Back then, companies like Luxshare Precision Industry Co., Ltd., Lens Technology, Sunny Optical, and Goertek demonstrated manufacturing efficiency across the entire industrial chain. The next step would be entering the technology manufacturing stage, requiring the tool-level and science-level innovations we discussed earlier. Further down the road, China will also give rise to its biotech equivalents of Huawei, Xiaomi, vivo, and OPPO.

Of course, how smoothly this process unfolds depends on the answers to three questions.

First, can we build new efficiency tools: algorithms + data + novel equipment?

Second, can we efficiently utilize clinical resources, understand clinical needs, and accumulate clinical knowledge?

Third, can cash flow continue to improve, and will new payers emerge?

On the third point, some might say China's biotech market is still small. True — but change is underway. In 2025 alone, we've seen dense and critical changes to commercial insurance-related systems and policies. Most importantly, the Category C drug list was introduced this year. (Note: The Category C list serves as an effective supplement to the basic medical insurance drug directory, focusing on innovative drugs with significant clinical value and clear patient benefits that exceed the "basic coverage" mandate and thus cannot yet be incorporated into the standard medical insurance directory.)

While there are currently no explicit regulations mandating that the Category C list be covered by commercial insurance, the list was essentially designed to create space for commercial insurance. Commercial insurance is positioned to address consumption upgrades in eldercare and healthcare beyond basic medical coverage. In December 2025, the National Healthcare Security Administration and the Ministry of Human Resources and Social Security issued the Commercial Health Insurance Innovative Drug Directory (2025), which proposed actively promoting the inclusion of the commercial insurance innovative drug directory within commercial health insurance coverage. This is a change happening right now.

Over the long term, we'll move toward a system where social insurance provides a safety net and commercial insurance addresses healthcare consumption upgrades, with both jointly meeting multi-layered medical needs. Meanwhile, commercial insurance capital will also serve as long-term money in primary and secondary markets. As these changes take effect, China's biotech market will be substantially larger than it is today. More importantly, the industry will advance along the path we just described, completing the full chain and giving rise to China's own MNCs (multinational pharmaceutical companies).

That concludes today's sharing. It may sound somewhat motivational or even rah-rah, but we've certainly "drunk it all in." If you've followed our analytical thread and "drunk half of it in," I believe you'll agree that we are indeed in a special historical window of opportunity. Here's to getting in the game together in the new year and winning this new cycle.

AI Industry Research Series

Looking Ahead to 2026: What Innovation Opportunities Await in AI?

The Hotter the Robotics Track Gets, the More We Need to Respect Its Rules

How Can AI Hardware Startups Cross the Data Desert?

Reader Engagement

What did AI mean to you in 2025? What are your most common AI use cases, and what unexpected gains or insights have you had? Share your thoughts in the comments. By 17:00 on January 5, 2026, the 6 most interesting comments will each receive a copy of the latest edition of the FreeS Fund Industry Research Handbook and a book recommended by Feng Shu.

Looking Ahead to 2026: What Innovation Opportunities Await in AI?

From Foundation Models to AI Companions: What Cyclical Patterns Lie Behind AI's Shifting Hot Topics?

Is AI Healthcare Having Its DeepSeek Moment?

Virtual Cells: Can Life Be Digitally Simulated?

Star the FreeS Fund WeChat Official Account for timely business insights delivered to your feed.