2025: Has Embodied Intelligence Reached Its "ChatGPT Moment"? | FreeS Research

The "Triangular Game" of Embodied Intelligence: Success Rate, Generality, and Cost

In 2025, the humanoid robot sector remains white-hot, with "science fiction becoming reality" unfolding before our eyes. In April, the world's first humanoid robot half-marathon kicked off, with distinctly designed robot competitors taking strides on a real-world track. In May, at the first global combat sports tournament featuring humanoid robots as the sole participants, robots executed hooks, side kicks, dodges, and a full repertoire of fighting moves. Come August, the World Humanoid Robot Games will open, featuring a rich variety of events spanning track and field, gymnastics, and soccer. A year ago, in our report The Road to Embodied Intelligence, we noted that the sustained improvement in supply chain cost-efficiency and rapid growth in demand across secondary and tertiary industries could become enduring opportunities in the embodied intelligence赛道. One year on, what has changed in the embodied intelligence space? What new opportunities have emerged? On the podcast What's Next | Tech Matters, FreeS Fund executive director Pengqi Liu, Sheng Dong Huo Po co-founder and Tech Matters host Diane Ding, and Tech Matters producer Yaxian explored the new phase and core challenges facing the embodied intelligence赛道, discussing questions including but not limited to:

-

Where does the current wave of embodied intelligence enthusiasm begin? Why the pursuit of "humanoid" and "general-purpose"?

-

What factors shape the software and hardware development of humanoid robots? What core challenges do they currently face?

-

How is commercialization progressing for humanoid robots? What trends and opportunities are emerging?

We've edited and excerpted portions of the podcast, hoping to offer fresh perspectives. We welcome you to continue observing and exploring with us. You can also head to the Xiaoyuzhou app or Apple Podcasts, search for and subscribe to What's Next | Tech Matters to hear the full episode. We look forward to ongoing exchanges with you. If you're an entrepreneur in the embodied intelligence field, feel free to reach out to Pengqi Liu, executive director at FreeS Fund (pengqi@freesvc.com).

Engagement Giveaway What innovative opportunities do you see in the embodied intelligence field? Share your thoughts in the comments. By 17:00 on June 5, 2025, the three most thoughtful commenters will receive a copy of Source Code: My Beginnings, Bill Gates's autobiography. In this era of AI fervor, we might do well to look back at the history of computing and the innovators behind it.

/ 01 / Building Robots: Why Pursue "Humanoid" and "General-Purpose"?

Yaxian: The robot marathon a while back drew considerable attention, and the World Humanoid Robot Games will kick off in August. Why is this wave of embodied intelligence so explosive?

Pengqi Liu: The humanoid robot half-marathon held in Yizhuang really broke through to mainstream audiences. Beyond investment circles, I noticed running groups discussing it too — people were watching to see whether the robots could actually finish the race.

This was the first time humanoid robots stepped out of the lab environment to complete such a prolonged real-world challenge. The completion rate was roughly 30%, and the first-place finisher was faster than many human runners — actually quite remarkable.

Tesla's announcement of its entry into humanoid robots marked a symbolic starting point for this wave of enthusiasm. In 2021, Tesla officially announced its humanoid robot plans, introducing the "Tesla Bot" concept. In 2022, Tesla formally unveiled the Optimus humanoid robot prototype. That same year, Figure AI was founded, focused on developing general-purpose humanoid robots.

Unlike humanoid robot companies established earlier, Optimus and Figure AI had very clear objectives: they weren't limited to building robots capable of complex, flashy maneuvers, but aimed to send robots into factories and integrate them into production.

Around 2022–2023, numerous domestic teams were also established, betting on the embodied intelligence direction — companies like AgiBot, Galaxy Universal, and LimX Dynamics.

Why did people choose this particular moment to enter? We can understand this from both software and hardware perspectives.

On the hardware side, over the past decade, the industrialization and scaling of sectors like new energy, industrial automation, and consumer electronics have advanced, driving maturity across the hardware and component supply chain including motors, sensors, and batteries — lowering the barrier to building robots.

On the software side, starting from late 2022, the emergence of large language models was seen as potentially useful for enhancing robot algorithmic capabilities, particularly in perception and decision-making. This gave the industry substantial room for imagination in envisioning future general-purpose robots.

Yaxian: Back in 2017, Unitree's quadruped robots could already accomplish many tasks. And in factories, robotic arms assembling cars and performing precision operations are highly proficient. So why insist on making robots "humanoid"? Why must we pursue "general-purpose"?

Pengqi Liu: To some extent, "humanoid" reflects a universal human imagination of the ultimate form of future general-purpose robots. Countless sci-fi films and TV series present robot figures resembling humans — like Baymax, the intelligent robot in the animated film Big Hero 6.

Technically, the capabilities embodied in humanoid form may appear more advanced and general, which is why many companies treat "humanoid" as a goal.

But in the narrow sense, comparing humanoid and non-humanoid forms, "whether it has legs" mainly represents a difference in mobility. In terms of mobility, I'd say 80–90% of scenarios don't require humanoid form — wheeled bases are sufficient. So now we're seeing more companies directing resources toward the upper body of robots, particularly the development of manipulation capabilities, which may be where greater commercial value lies.

▲ Scan the QR code to listen to the podcast conversation.

Yaxian: What capabilities must a robot possess to be considered "general-purpose"?

Pengqi Liu: The logic behind our current discussions of general-purpose robots and humanoid forms parallels how we discuss AGI in the large model space. Generality is the ultimate goal we pursue, but the challenge is that world resources are finite. While pursuing generality, we also need to balance efficiency, success rates, and cost.

For instance, in industrial and manufacturing domains, factors like efficiency, success rate, and cost clearly matter more than whether something is general-purpose. But in home service scenarios, generality becomes more important. We might allow robots to sacrifice some success rate and efficiency in exchange for being able to do more things.

The industry hasn't yet reached consensus on what capabilities general-purpose robots require. I think we can reference autonomous driving, grading general-purpose robot capabilities from L1 to L5, with metrics looking at how many scenarios are covered and how many tasks are covered within different scenarios.

Diane: In the robotics field, whether in research or specific application scenarios, isn't what's needed more convergence rather than generalization?

Pengqi Liu: Founders with more academic backgrounds may favor the route of directly pursuing full-scenario generalization. Founders with more industrial backgrounds may subtract from the general-purpose direction, choosing to solve problems well in one vertical scenario before expanding to others. But this can't be generalized either.

/ 02 / How Are the Software and Hardware That Intelligent Robots Need Developing?

Yaxian: What types of hardware do robots currently need, and what stages are different hardware components at?

Pengqi Liu: Robot hardware can be simply divided into several major categories: mechanical components (analogous to human bones, muscles, tendons), sensing (analogous to human facial features and touch), control (analogous to human brain, cerebellum, nervous system), and supporting systems for power supply, communication, and so on.

From an investment perspective, different types of hardware modules are at completely different development stages, which relates to the maturity of their associated industries.

Currently mature hardware units are largely spillover results from the scaled development of established industries like new energy vehicles, industrial automation, and consumer electronics.

Take joint reducers, for example — they're important components of the integrated joints commonly used in robots. Joint reducers are already quite mature in the new energy vehicle and industrial automation industries, with costs continuously declining, requiring only slight customization for use in the robotics industry.

Another example is sensors: thanks to the development of autonomous driving and robot vacuum industries, visual perception modules like LiDAR and millimeter-wave radar have become low-cost enough for robots to use out of the box.

Conversely, some less mature hardware units have core components that previously lacked industrialization and scaling in other industry directions, requiring custom R&D for embodied intelligence. This also presents entrepreneurship and investment opportunities.

Dexterous hands (a novel type of robotic end-effector, the final link and execution component for robot-environment interaction) and associated tactile and force sensors are one example. Before 2024, dexterous hands were primarily used in prosthetics and research. It was only with the rising enthusiasm in the embodied intelligence industry in recent years that dexterous hands were "brought into the spotlight," attracting more capital and talent to advance their development.

Inspiritech Robotics is a particularly interesting case. When FreeS Fund invested in their Series A in 2021, the company already had a dexterous hand product demo, but what we focused more on was their core component, the micro servo cylinder (a linear joint for humanoid robots, also called a linear actuator — an integrated motion unit combining servo motors, reducers, ball screws, and other components).

At the time, Inspiritech's micro servo cylinders already had relatively mature applications in the new energy and medical aesthetics industries. While dexterous hands accounted for a small revenue share, they served as proof of technical capability. In retrospect, the scaling of other industries likely drove the gradual maturation of core component technologies and cost reduction for micro servo cylinders, ultimately accumulating key capabilities for dexterous hand productization. Today, Inspiritech enjoys significant first-mover advantages in the dexterous hand赛道, leading the industry in shipment volume.

So the maturity of humanoid robot components and hardware modules was, in early stages, heavily dependent on support from other established industries. Relying solely on the embodied intelligence industry itself would have been slower and more difficult.

Diane: This reminds me of Robosen Robotics — they started with servo motors, then pivoted to the toy industry, and actually achieved considerable commercial success.

Pengqi Liu: Capabilities that companies have built up and refined in other industries, when applied to emerging markets, may actually align better with market logic.

Yaxian: Having covered hardware, let's look at the software layer. There are two relatively mainstream development routes for robot control systems.

One is the end-to-end architecture (where large models directly understand problems and output decisions or answers) — the VLA model (visual language action, mapping from language and vision to action), with Tesla's FSD (Full Self-Driving) being a typical end-to-end representative.

The other is traditional control systems, dividing robot motion components into modules like perception, decision-making, and control, combining AI large models module by module to achieve various functions.

Pengqi Liu: I don't think these two routes are in a "zero-sum" state — there are numerous compromise solutions that draw from each other.

For example, one or two modules in a hierarchical model can use large models to achieve partial end-to-end functionality; and within VLA, a hierarchical structure can also be designed, such as dividing into fast and slow system structures.

Companies need to choose suitable routes based on their positioning, scenarios, and business models.

The past decade of autonomous driving development can serve as a reference for the embodied intelligence industry.

In the early days of autonomous driving, some companies immediately pursued ultimate L4 (highly autonomous driving) solutions, while others started with L2 (partial autonomous driving) solutions. Companies doing L2 typically first pushed enough products to market, collected data, and then trained models.

Tesla's FSD didn't start with an end-to-end model either. It likely began with a hierarchical model, accumulated sufficient user data, and then trained the end-to-end model in reverse.

Of course, end-to-end models may not be the "endgame" either. Some in the industry believe end-to-end models can at best serve imitation learning. Whether more methods and data need to be incorporated into training end-to-end models mainly depends on a company's positioning and vision.

Yaxian: What are the advantages of end-to-end models?

Pengqi Liu: The simplest understanding is that end-to-end model structures appear cleaner and more straightforward. With sufficient data and compute, they might leverage the Scaling law (OpenAI's proposed scaling law, which posits that large model performance depends primarily on compute, model parameter count, and training data volume) to directly train the model.

The question is, in specific application scenarios, how high is the model's ultimate success rate — for instance, can accuracy meet industry targets? Taking autonomous driving as an example, is the upper limit of end-to-end models achieving one intervention per hundred kilometers or so? Is once per hundred kilometers actually good enough?

Yaxian: What challenges exist in applying large models to general-purpose robots?

Pengqi Liu: On the "robot brain" side, the challenge is that robots need to interact with the physical world, perceiving 3D environmental information and physical properties, yet large models currently provide limited information about the "real world" that robots need. Autonomous driving can use large models because vehicles require relatively little interaction with their environment — the goal is to avoid contact and collision with the outside world.

On the "robot cerebellum" side of planning, control, and manipulation, existing large models may fall far short of the accuracy and response speed robots require. For example, a robot's end-effector control system may need signal update frequencies of hundreds or even thousands of hertz, which the current Transformer architecture (a novel deep neural network structure underlying mainstream large models) struggles to achieve.

From another angle, embodied intelligence is essentially an AI Agent oriented toward the physical world. A good AI Agent needs environmental perception and memory, reasoning and decision-making capabilities, and more importantly, tool use (the ability of an AI Agent to effectively leverage external tools to enhance task execution). Embodied intelligence as an AI Agent similarly requires these characteristics. While environmental perception and reasoning capabilities can improve with large model evolution, tool use for physical world interaction clearly faces greater challenges.

Under Investment Fever, What Trends and Opportunities Exist in the Embodied Intelligence赛道?

Yaxian: What stage is humanoid robot commercialization at? How is implementation progressing?

Pengqi Liu: Let's start from a technical perspective. Many technologies, including end-to-end models, are at very early research stages.

Therefore, commercialization isn't the core concern for many companies. Currently, strategic priorities center on how to acquire more resources and advance frontier technology R&D.

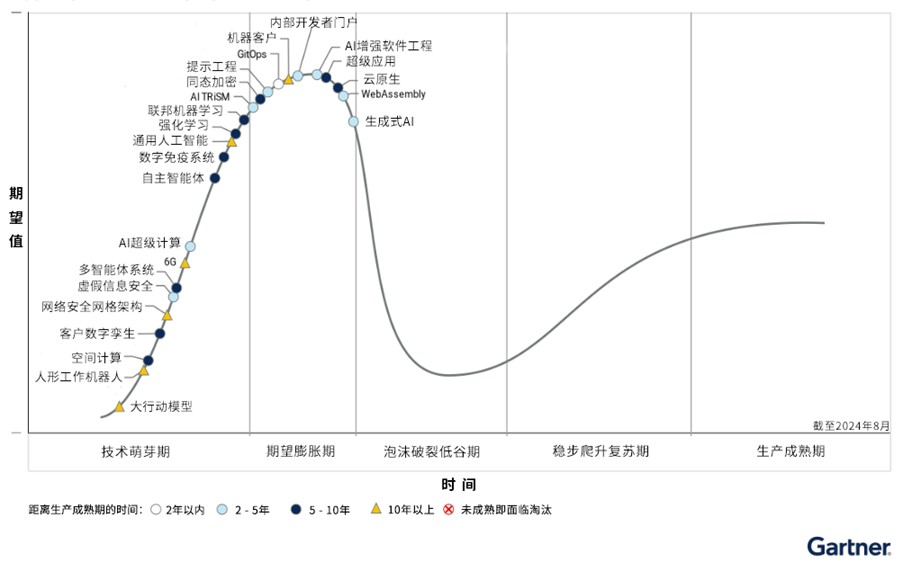

From an investment perspective, embodied intelligence is in a clearly overheated state, likely positioned at the first peak of the Gartner Hype Cycle.

▲ 2024 Emerging Technologies Hype Cycle. Image source: Gartner

The upside of "hotness" is that it can accelerate the maturation of related technologies and industries. Take dexterous hands: with capital support, the industry has produced many decent solutions.

Even if the embodied intelligence industry subsequently enters a capital downturn and cooling period, many "eggs laid along the way" opportunities will emerge. Models, algorithms, and core components developed by the embodied intelligence industry may spill over into other industries — for instance, enhancing existing service robot capabilities or enabling robotic arm forms previously difficult to achieve. Some industrial robots currently operate only at very fixed stations; in the future, they may execute multiple tasks in more generalized scenarios.

From a mass production perspective, there are still few domestic embodied intelligence companies capable of scaled production. One major challenge is not yet having found PMF (Product-Market Fit); the current focus remains more on serving research scenarios and demonstration needs. Additionally, both software-level upper limb manipulation capabilities and the balance between hardware-level mechanical performance, stability, and cost still have room for optimization.

If we discuss how humanoid robots might land in the future, we need to balance the "impossible triangle" (where three elements of a matter cannot simultaneously exist) — in embodied intelligence, this mainly refers to success rate, generality, and cost.

▲ Scan the QR code to listen to the podcast conversation.

In the Chinese market, humanoid robots need to achieve higher success rates than manual operation, realize generalization within vertical scenarios, and are particularly suited to entering industries with relatively higher added value.

For example, manual experimental procedures in biomedicine might be completed by robots. First, laboratory operations are relatively limited, placing lower generality demands on robots. Second, in specific experimental procedures, robots may be more precise than humans in controlling experimental conditions and standardizing operations. Additionally, experimental operators typically need bachelor's degrees or higher with backgrounds in chemistry or biology — they're high-skill labor. If humanoid robots can perform such substitutive work, the economic value created would be relatively higher.

By contrast, humanoid robots may not easily land in labor-intensive scenarios like warehousing, logistics, or industrial settings, partly because these scenarios have lower added value. Moreover, domestic labor costs are low while overseas labor costs are high — thus, overseas markets have greater need for humanoid robots to replace human labor.

Of course, we've also observed attempts at industrial applications, such as in car manufacturing, but currently robots may mostly do quality inspection, random搬运, and similar tasks — truly entering core production processes still has a long road ahead.

The profiles of humanoid robot companies domestically and abroad differ considerably.

Well-known American humanoid robot companies include Tesla, Figure AI, and Physik Instrumente (PI), among others. There aren't many emerging companies, but individual company valuations and funding amounts are very high. Overall, American companies tend to pursue technical leadership, with R&D focus concentrated on software and algorithms — the robot brain. Beyond a few companies like Optimus and Figure AI, not many develop robot bodies in-house.

China has many entrants in humanoid robots. Beyond the far-leading first tier, there are countless second and third tiers. In the first half of 2025, many entrepreneurs continue to enter — according to estimates from the New Strategy Humanoid Robot Industry Research Institute, numbering in the hundreds. Additionally, Chinese embodied intelligence companies appear to want to achieve "all-around" capability — doing both software and body hardware, showcasing flashy technical demos while also having thoughts and plans for implementation.

From a market environment perspective, China possesses unique advantages for nurturing the humanoid robot industry: complete industrial chain foundations, scaled market demand, proactive policy guidance, and broad overseas expansion opportunities.

Yaxian: Regarding future humanoid robots, the public may have some "robots entering homes" imagination. From the current stage of technological development, will robots entering home scenarios require a longer timeline?

Pengqi Liu: Indeed. Beyond the success rate, generality, and cost issues in the "impossible triangle," robots entering homes also presents many ethical and philosophical questions that need resolution.

Diane: Hopefully, with capital's boost, the embodied intelligence industry can reach a technological breakthrough node, pushing forward bit by bit — I think this goal should ultimately be achievable.

Pengqi Liu: If one wave alone could push it to its ultimate height, then it wouldn't be a truly significant matter. Something significant requires several waves to push it to its final state.

Yaxian: So have robots reached their "ChatGPT moment"?

Pengqi Liu: I think we're far from it.

In May 2024, we published a report, The Road to Embodied Intelligence.

Compared to a year ago, I believe embodied intelligence has become hotter — more teams have emerged, more institutions have entered. What hasn't changed is that the industry as a whole remains in early stages; although many phenomena like the robot marathon have "broken through," commercial implementation remains scarce.

In hardware, numerous new startups and teams have positioned themselves in force sensors, tactile sensors, dexterous hands, and so on. In the niche direction of robot cerebellum data, companies or platforms providing teleoperation, motion capture, and synthetic simulation data have emerged. This aligns with previous judgments in our report.

Going forward, new trends and opportunities may appear in the control algorithms for the brain and cerebellum — this is currently one of embodied intelligence's biggest bottlenecks. The solution may lie in first selecting a落地 scenario that balances success rate, generality, and cost, using existing technical capabilities to form closed-loop solutions, accumulating scenario data, and then gradually evolving new algorithm architectures.

If we extend the timeline, the emergence of humanoid robots in their ultimate form may come later than the realization of quantum computing and nuclear fusion. Humanoid robots might be like Iron Man in Marvel — using controllable nuclear fusion as the power source and quantum computing as the compute unit, thereby truly achieving the general-purpose humanoid form.

Engagement Giveaway What innovative opportunities do you see in the embodied intelligence field? Share your thoughts in the comments. By 17:00 on June 5, 2025, the three most thoughtful commenters will receive a copy of Source Code: My Beginnings, Bill Gates's autobiography. In this era of AI fervor, we might do well to look back at the history of computing and the innovators behind it.

The Ambition, Dilemma, and Endgame of AI Coding | FreeS Research Institute

The Road to Embodied Intelligence | FreeS Report 37

Feng Li in Conversation with LimX Dynamics Founder Wei Zhang: Humanoid? Robot? | FreeS VC Dialogue

Star the FreeS Fund WeChat Official Account — timely business insights delivered to you