Li Feng Column | A $2 Trillion Market and $10 Trillion Output: Why We're Bullish on Chinese Chips?

When Will Homegrown Chips Break Through?

In this seventh column installment, we're talking about the ZTE sanctions and investing in China's semiconductor industry.

The ZTE embargo by the US Commerce Department has been unfolding for over a week now. We're watching ZTE's fate closely, but we're also watching the situation and future of China's chip industry as a whole.

Since its founding, FreeS Fund has bet on deep tech investing, and we've treated chip investments as a priority. For me personally, this has been challenging — I hadn't invested in semis before, so I had to start from scratch. Fortunately, we found two colleagues who really know their way around this space.

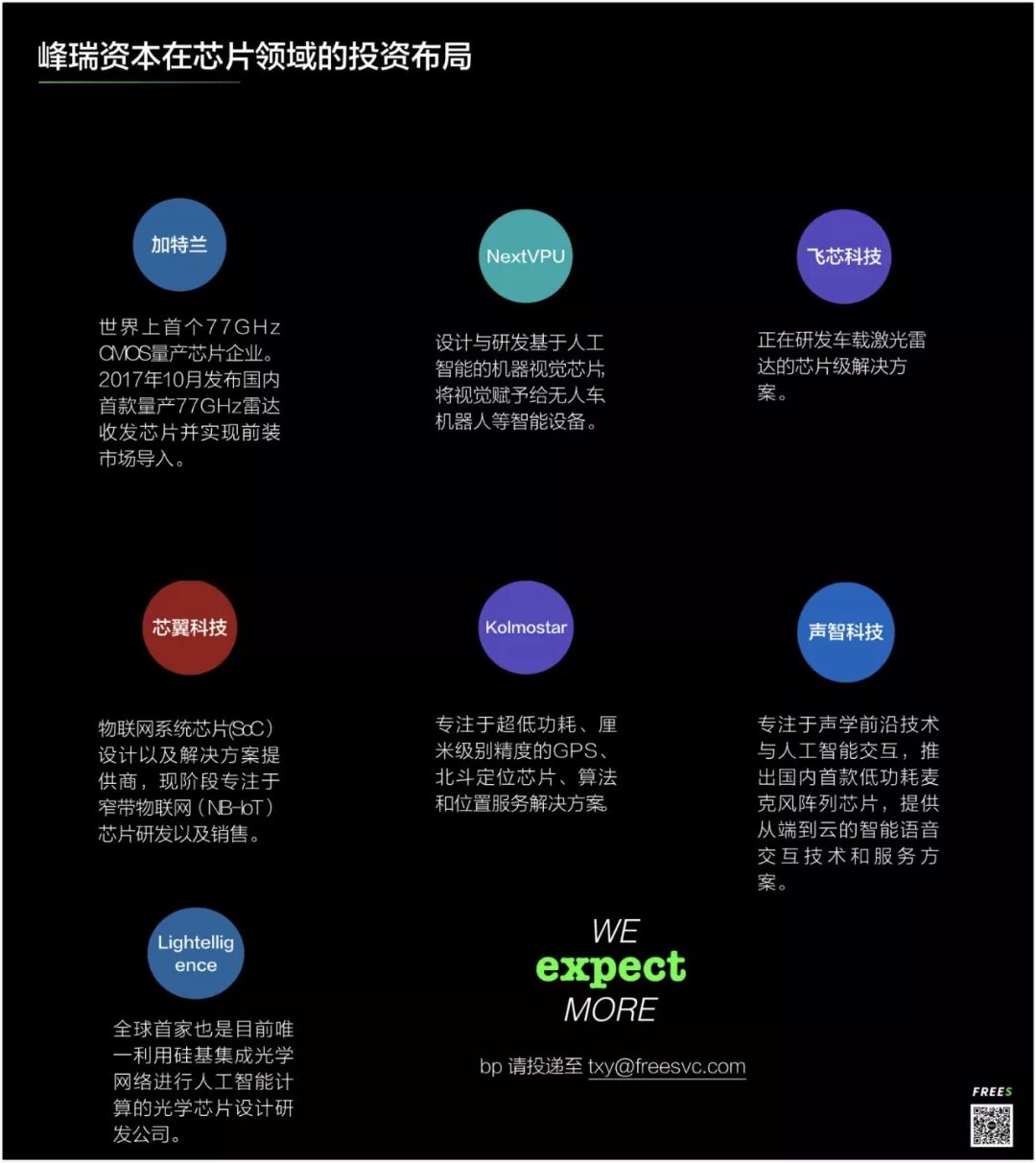

Over the past two years, we've invested in nearly 10 chip-related companies (see the list and bonus content at the end). They've developed well — most have reached the sampling or mass production stage. Going forward, we'll be devoting more time, energy, and capital to the chip sector, and we're especially eager to exchange ideas, discuss, and collaborate with all of you.

But just two years ago, whether chips were even investable was controversial within the industry. Investor friends who heard about our plans warned me against it. Their reasoning: in the last cycle, pretty much nobody who invested in chips made money. "This isn't something VCs should be touching."

Even internally, we had differing voices on whether to invest in chips, and how. Of course, we eventually reached consensus. In this article, I'll share:

- Why we're bullish on China's chip industry, and why we're determined to invest despite the difficulty

- China's chips have been almost entirely import-dependent for a long time. Do domestic chips actually stand a chance?

- Why now is the right time to invest in chips?

We welcome your thoughts in the comments.

▍A 2-trillion-RMB market, 10 trillion in output value, and the unavoidable imperatives of core technology localization and supply chain pricing power

Let's start with necessity. At the broadest level, finance is ultimately in service of the economy — it's the faucet that directs economic restructuring and cyclical transformation. Equity investing is fundamentally a financial business model, so it should follow economic logic, channeling capital toward the directions and structures that economic adjustment requires.

China is a manufacturing powerhouse. The US of the 1950s shares many parallels with China today. America was then the "world's factory." Manufacturing's importance to the US economy then exceeded what it means to China today.

Over the past 30 years, the US transferred out a net total of over 10 million manufacturing workers. Meanwhile, its information industry workforce grew 2.2x over the same period.

A key driver of this dual transformation was that from the 1960s to today, America led nearly every technology wave — from semiconductors to PCs to the internet — using technology to convert labor skills at massive scale. The result: a substantial increase in information industry employment and output raised overall US productivity per capita and reshaped national competitiveness. America thus became the only major power in history to successfully transform.

Looking at China, our manufacturing workforce share remains high (agriculture, industry, and services account for 38%, 27.8%, and 34.1% of labor respectively). As the world's manufacturing center, it would be difficult and unrealistic to move all these workers into services.

So in this economic cycle, we must work to keep manufacturing in China, continuing to absorb hundreds of millions of workers. Yet manufacturing that relies purely on cheap labor can easily shift to regions with even lower labor costs.

Therefore, to keep Chinese manufacturing in China, we must — like America back then — seize the "window" of technological upgrading, pursue industrial upgrading, and solve two problems: core technology localization and the supply chain pricing power that comes with it, turning "Made in China" into "Intelligently Made in China."

What does this have to do with the chip industry?

Here's one fact: China produces 70% of consumer electronics globally, and 90% of chip-containing consumer electronics are made in China. Yet roughly 90% of those chips are imported.

According to Rui Xiaowu, chairman of China Electronics Corporation, chips — not crude oil — are currently China's largest import by value. Chip imports alone cost $240 billion annually. Take Qualcomm as an example: over 60% of its $5.7 billion net profit in fiscal 2016 came from China alone.

Beyond direct imports of $240 billion, China's domestic chip production capacity is roughly $50 billion, for a total approaching $300 billion — about 2 trillion RMB. Of that domestic $50 billion, most is produced by foreign-majority-owned enterprises. They're simply manufacturing here; the technology remains foreign.

In short, China's chip market is roughly 2 trillion RMB, but domestic share is minuscule and import dependence is near-total. We lack core technology and pricing power over the high-margin components at the heart of the value chain. This must change.

Moreover, chips have strong upstream and downstream multiplier effects — between 1:4 and 1:5. (Real estate has the highest multiplier effect, roughly 1:8.3 to 1:9, as is well known.) This means a 2-trillion-RMB chip market can drive roughly 10 trillion in output value. In China, that's comparable to the value created by 200 million manufacturing workers.

In other words, the chip industry is a matter of 200 million people and 10 trillion RMB. Without autonomy over core, high-margin pricing components, the chip supply chain can easily flow to lower-labor-cost regions. When that happens, one direct consequence is structural unemployment.

Unquestionably, this is a problem we must solve in the current economic cycle. Therefore, increasing investment to solve core technologies including chips is the necessary path to solving employment and keeping manufacturing domestic.

Investing is betting on what will inevitably happen. Since we believe the chip industry's development holds long-term value for the industry itself and for economic structure, we will persist in looking at and investing in quality opportunities.

▍Is the timing right to invest in chips?

My answer: yes.

First, after more than a decade of development, chips have grown substantially across all three infrastructure links in China: design, manufacturing, and packaging/testing.

In the last economic cycle, a major challenge for the chip industry was general-purpose chips — products like CPUs and GPUs that require longer R&D cycles, greater R&D investment, and more advanced production processes to complete together.

The reason: the technology barrier in chips is simply too high. And in the last economic cycle, no new major computing devices emerged. While Moore's Law still held, this meant leading enterprises became increasingly dominant. This is also why US sanctions could hit ZTE hard — ZTE is heavily dependent on general-purpose chips in its main business areas, and general-purpose chips are increasingly controlled by leading players like Intel, NVIDIA, and Qualcomm.

People often cite general-purpose chips as unsuitable for VC investment.

But in the current cycle, whether from industrial applications or the consumer side, vertical application chips have opportunities to emerge and rise. There are two main reasons:

First, proximity to supply chain and demand.

In solutions that embed new controllers and sensors into new devices, the goal isn't purely optimal computing power — it's combining power consumption, size, cost, and algorithms with specific application scenarios. The chips required for these verticalized scenarios are essentially combinations of software, algorithms, and hardware, ultimately integrated into what's called a chip. They may present as modules or as chips themselves.

This type of demand is growing. Smart speakers, autonomous driving, IoT communications — these are all new vertical application scenarios. Their demand for chip-based solutions isn't as high as for general-purpose chips. What's more needed is chip design and manufacturing capability combined with understanding of the entire scenario.

It requires teams with certain algorithm capabilities, able to design in combination with scenarios and specific hardware applications — with the chip being just one productized outcome.

In this context, China's opportunity lies in the fact that for most of these new vertical scenarios, the entire hardware supply chain is in China. When you're creating a chip-based solution for a specific scenario, theoretically, the closer you are to its supply chain and demand, the easier it is to succeed.

Second, talent.

Over the past couple of years, as Moore's Law itself has approached its limits in general-purpose chip iteration, many large chipmakers have stopped accelerating iteration by hiring large numbers of technical staff. Meanwhile, the demand scale from new vertical application scenarios hasn't yet reached the point where major firms are willing to invest heavily in technology and manpower.

This has led large numbers of people with chip design, development, and manufacturing capabilities to return to China, developing products for these new vertical application scenarios by leveraging China's relatively mature supply chain. We can define these products more broadly as sensors and chips.

These broadly defined, vertical-scenario-based chip solutions — in the past two years, we've invested in 7 such companies, with another two or three in the deal pipeline. They're developing well, with most having reached the sampling or mass production stage. (Bonus: reply "芯片" in the FreeS Fund WeChat account [ID: freesvc] to get a glimpse of these Chinese chips' business scope, progress, founding team backgrounds, and more.)

Again, going forward, we'll be devoting more time, energy, and capital to the chip sector, and we're especially eager to exchange ideas, discuss, and collaborate with all of you.

Summary

1 Equity investing should follow economic logic. We believe the chip industry's development holds long-term value for the industry itself and for economic structural adjustment.

2 Necessity. A 2-trillion-RMB chip market can drive roughly 10 trillion in output value, comparable to what China's 200 million manufacturing workers create. Yet China's chip industry is almost entirely import-dependent. We lack core technology and pricing power over core high-margin components.

3 Possibility. Whether from industrial applications or the consumer side, vertical application chips have opportunities to emerge and rise.

(Feel free to share to Moments. For reprint permission, reply "转载" to learn the rules and contact Feng Xiaorui [ID: freesfund] for authorization. Copyright FreeS Fund.)

▲ Li Feng's Column | What Was the Secret of the Only Major Power in History to Successfully Transform?

▲ Li Feng's Column | From iPhone X and Smart Speakers to New Drug R&D and Environmental Monitoring: How I View Tech Innovation

▲ Li Feng's Column | The Origins and Future of the ICO Bubble