A Veteran Educator's 10,000-Word Reflection on K-12 Education's Reconstruction and Resilience Amid the Pandemic | FreeS Fund Business School

A child's time is irreversible. The essence of education is to produce good outcomes.

Not long ago, in our article "After the Pandemic: Education's Survival Race", we explored how COVID-19 was impacting the education sector. That piece took more of a bird's-eye, macro view. But those who smell the gunpowder and hear the artillery first are always the ones on the front lines. Today, we're sharing the perspective of Changke Liu, a 20-year veteran of China's education industry and founder of Qingqing Education — his insights on what the pandemic has revealed.

Liu previously served as general manager and chairman of Shanghai Only Education. Back in 2014, when Feng Li was still at IDG, he would frequently meet with Liu to discuss and encourage him to start his own venture. That same year, Qingqing Education (originally Qingqing Tutoring) was founded. It began as an offline platform for door-to-door one-on-one tutoring, later pivoting to online one-on-one education and developing its own quality control systems. FreeS Fund participated in Qingqing Education's $55 million Series D round in 2017 and has continued to invest in subsequent rounds.

This article comes from Liu's recent talk on Lieyunwang. He analyzes the "changes" and "constants" in the education market during this industry-reshaping moment.

- Change: Post-pandemic, the offline education training industry will take on a pronounced dumbbell shape. On one end: large institutions that will consolidate the market. On the other end: small, resilient neighborhood shops or studios close to their users. The ones hit hardest will be mid-sized institutions — those with annual revenue between roughly 1 million to 10 million RMB, or 10 million to 200 million RMB.

- Change: The entire online education sector has hit fast-forward, making its business models crystal clear: online dual-teacher live large classes, online same-city small classes, and online one-on-one.

- Constant: The pandemic hasn't changed the fundamental nature of K12 education. Whether online or offline, the core is still delivering results for students. For online education companies, the core isn't "online" — it's still education as a service. They need technology, yes, but also time to develop teaching research, and time to build out their tutor organizational systems. Every link requires time to mature.

We hope this offers a fresh perspective. We welcome your thoughts on education in the comments.

Qingqing Education's Changke Liu: Post-Pandemic Online Education Will Settle Into Three Models — Large Classes, Same-City Small Classes, and 1-on-1

Source: Duozhi Network

Author: Tunny

/ 01 / The Pandemic Will Reshape the Offline Education Training Landscape

The impact has been truly enormous. I've been in China's K12 space for over two decades — the only person who's been at it longer than me might be our Teacher Yu Minhong. But we saw Old Yu say recently that this pandemic has posed an extremely severe test for New Oriental, that all their offline classes were suspended, and that New Oriental could face enormous challenges.

I think Teacher Yu's words deserve our full attention. New Oriental was the first Chinese education company to list in the U.S., with a market cap around $20 billion. After all these years, if he's saying something like this, I believe he's sensing that this pandemic is fundamentally different — completely incomparable to SARS in 2003.

Squirrel AI founder Haoyang Li said that in six months, 60% of purely offline small and medium-sized institutions nationwide will go under. ONE founder Xi Zhang said that 60% of online education companies will fall in the future.

Hearing all of this, it's an important signal for both online and offline — this pandemic's impact on education is no ordinary event. It will reshape industry dynamics.

I largely agree with Haoyang. While I don't think it'll necessarily mean bankruptcy, my overall assessment is that many offline education training companies will be crippled during this period, and recovery will be relatively difficult.

At the same time, I also agree with Zhang's view that 60% of online education companies will fall.

Because online education is a battle among giants, with extremely high barriers to entry. Ordinary small and medium enterprises can hardly break in. It's not like offline, where geographic location is an advantage — a small institution can survive if it's closer to consumers and delivers good teaching quality.

But the technical threshold for online education is very high, so 60% of ordinary online institutions could very well fall in the future, because online education demands so much from underlying technology, supply chains, and service chains.

Overall, whether online or offline, this pandemic has been devastating for small and medium-sized institutions.

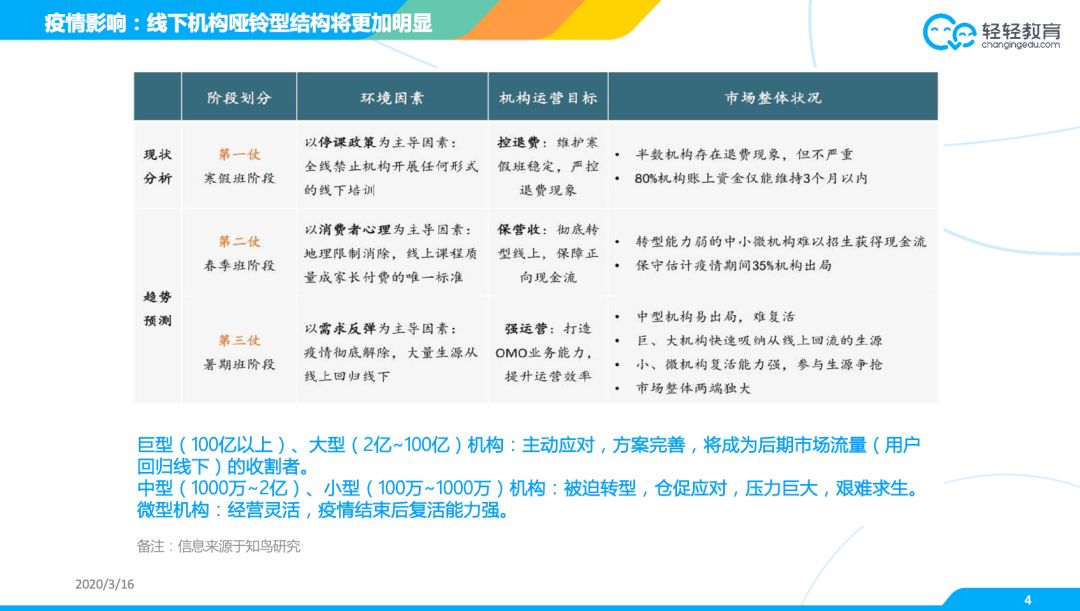

A few days ago, I saw a report from Zhiniao Research. I'm putting the chart here — this is their conclusion.

For offline institutions, this pandemic means fighting three battles.

The first battle is winter term classes — this one might be okay. Many offline institutions collected fees before the pandemic hit. Some winter courses had already finished; those that hadn't simply moved online, which wasn't too difficult — they had to go online anyway. Moving online meant relatively fewer refund requests for winter term. But we also know that most Chinese companies, not just education training companies, but small and medium institutions across sectors, have limited cash flow. Perhaps 80% of institutions only have enough cash to last three months.

The second battle is spring term. Right now, most institutions' spring courses are essentially generating zero revenue. Traditional offline institutions simply cannot open classes. And when you move students online, parents have various concerns — schools themselves are offering online classes, plus there's plenty of free content available. So many institutions have given up on charging for spring courses and are offering them for free, hoping to retain their students and prevent them from drifting elsewhere. Revenue is minimal. This second battle, lasting through May or June, will see offline institutions struggling to collect fees.

The third battle is summer term. This year, most primary and secondary students' vacation time will likely be significantly shortened. For those of us who ran offline education businesses, there were two revenue peaks each year: spring term and summer term. Missing the spring revenue, then facing a shortened summer vacation — the money you can collect will be relatively limited.

These three battles, three hurdles, will create this situation: some small and medium institutions without ample cash flow will essentially be crippled, their cash flow cut off.

Post-pandemic, the entire offline education training industry will display a very pronounced dumbbell structure. On one end of the dumbbell are large institutions that will instead harvest the market. Institutions like New Oriental, TAL (XRS), and Puxin Education will still see many students return to offline classroom settings after the pandemic ends. Who will capture these students? New Oriental, TAL, and similar institutions, plus some regional leaders — Shenzhen's Think Academy, Guangzhou's Excellence Education, Shanghai's Only Education. They can consolidate the market. As small and medium institutions are eliminated, many students will flow to these larger players.

On the other end of the dumbbell are very small institutions — perhaps a single small storefront, or a studio put together by a few teachers. These still possess very strong vitality. If their teaching quality is good and they're geographically close to users, they'll do well.

The mid-sized institutions — say, annual revenue of 10 million to 200 million RMB, or even 1 million to 10 million — the pandemic will essentially cripple these. This is what we're seeing across offline training institutions. Recently, I've been in touch with old friends who run offline institutions, and their situations are basically consistent with this picture.

/ 02 / When the Pandemic Ends, Online Education Hits Fast-Forward

Now let's look at online. This is another chart from Zhiniao Research that I think illustrates the point very well.

This pandemic essentially forced nearly all of China's primary and secondary students online all at once, and for a fairly extended period — perhaps a month or even two months. China has 190 million K12 students. Previously, online education penetration was roughly 10%, so about 18 or 19 million. Now that figure has essentially become 100% — except perhaps for some remote mountain villages, nearly everyone is online.

It's like hitting fast-forward for online education. All the users suddenly flooded online at once.

The biggest winner from this pandemic has been the online dual-teacher live large class model. Looking at the curves above, the top one is TAL's XRS Online, the yellow one is Zuoyebang, below that is Yuanfudao, and below that is Gaotu Techedu.

The others — including some one-on-one institutions and small-class live institutions — barely register on this chart. Why? Because during this period, only the large online class models could absorb massive numbers of online students.

We've all seen reports about online education systems crashing. The organizational, technical, and product demands on companies are extremely high. We saw even DingTalk and WeCom crash, let alone education companies. This sudden flood of users caused online large class brands' student numbers to surge dramatically.

So our basic view is that the biggest beneficiaries of this wave are the large-class brands that fought through last summer's marketing war. Back then, they were burning 10 million RMB a day on ads. But no amount of advertising spend could match what this pandemic has done for them. This time around, we're estimating each of them has added roughly 20 million new users.

Then there's small-class live instruction — represented mainly by New Oriental Online and Dongfang Youbo. Its performance has been mediocre, with no real growth. Why? Because its capacity to absorb students is simply limited. As for online one-on-one, demand has ticked up slightly, but unlike class-based models, each student needs their own teacher, so supply-chain requirements are extremely demanding. They can't scale even if they want to. So we haven't seen major growth there either.

When the pandemic ends, my own thinking is that the overall K12 online education landscape will become much clearer.

Looking back at offline K12 education, we found it went through three phases, three business models. The earliest was offline large classes — New Oriental built its brand on star teachers, and this was primarily their model. Then came offline small classes, which was the core product TAL used to build itself. Later still came offline one-on-one, pioneered by Xueda.

Today, offline large classes have basically disappeared. Only two models remain: offline small classes, and these classes keep getting smaller. What we used to call small classes might have had 30 students; now it's 20, sometimes even 10.

The other model is offline one-on-one, which actually still has considerable scale. I remember Yu Minhong once saying New Oriental's one-on-one business does roughly 4 to 5 billion RMB annually — the largest one-on-one operation domestically. Elite probably does around 2 to 3 billion. One-on-one remains very strong, very much a hard need.

The rough split is probably 20% one-on-one, 80% small classes.

Now looking at how things evolved online, it's interesting — online actually started with one-on-one. VIPKID, for instance, was the representative one-on-one model.

Why did online begin with one-on-one? Because the degradation in teaching effectiveness from moving one-on-one offline to online is the smallest. But online class-based instruction and offline class-based instruction are completely different scenarios — lacking interaction, the degradation is much higher.

Then came the online dual-teacher live large class model, which evolved from recorded online courses. TAL Online originally did recorded courses, but they never performed well. Internally, they incubated a project called "Dahai" (Ocean), which introduced the tutor role — tutors working with the lead teacher, creating a live-plus-tutor model. That eventually evolved into today's online dual-teacher live large class format.

Post-pandemic, we believe three online models will remain. First, online dual-teacher live large classes — still a major hard-need market going forward. Unlike offline, these face the entire country, so they benefit from scale effects. They can also afford to hire the best teachers nationwide, and with tutors added in, they can deliver reasonably good teaching outcomes.

The second model consists of offline institutions that have developed online capabilities — call it OMO or whatever you like. The offline education companies that survived this crisis will emerge stronger. They'll have both the ability to run local small classes offline and local small classes online. We believe this model will emerge and end up resembling the original offline pattern.

Why do I say small classes must be local? It's very hard to make them national. Because all K12 academic tutoring has to account for one factor: local exam conditions and learning conditions. Localization is a real advantage.

You might join a dual-teacher live large class, but your classmates are scattered across the country. But if your product targets Shanghai local third-grade English, it can fully account for local difficulty levels and pacing. Your classmates are local, maybe your teacher is local too, and because you're connected to local offline centers, it's easy to build closer relationships with parents.

We believe post-pandemic, many will launch online local small class offerings. And this model's greatest value, we think, returns to the essence of education: it can deliver actual learning results.

Why did offline end up with only small classes and one-on-one? Because both models can deliver good learning outcomes. Why did offline large classes disappear? Because their teaching effectiveness was hard to guarantee. Offline small classes and one-on-one both can guarantee results, so they've survived — and the same will hold true online.

The third model is online one-on-one, clearly also a hard need. One-on-one's biggest advantage is its targeted approach — content can be personalized, and interaction with the student is very strong.

We believe that after the pandemic, the entire online education industry will have hit fast-forward. That fast-forward makes the online landscape very clear: online dual-teacher live large classes, online local small classes, and online one-on-one — basically these three models.

I sketched a diagram here — may not be perfect, but let me walk you through it. Of course, many people are saying students are going crazy with all this online class, lots of people aren't used to it. But personally, I still believe that if before the pandemic maybe 5-10% of users chose online, after this, while most will flow back offline, I believe 20% or even 30% will ultimately stay online — or at least choose some courses online and some offline. That's my judgment.

This applies to both offline class-based and one-on-one instruction. I remember a CICC research report from 2018 — it said if China's K12 market was 500 billion RMB that year, class-based was 400 billion and one-on-one was 100 billion. Of that 400 billion in class-based, roughly 5% was online and 95% offline. One-on-one was about the same ratio, 5% online and 95% offline.

So what changed with this pandemic? Offline may drop from 95% to 80%, while online class-based rises from 5% to 20%. What does 20% mean? If market size stays comparable to 2018, that means the online class-based segment grows from roughly 20 billion to 80 billion.

One-on-one might grow from 10 billion to 30 billion. Within the next year or two, I think by 2021 or 2022 we'll be around these market sizes.

But here's something to note: China's offline institutions — because of the major regulatory crackdown on tutoring in 2019 — you have to understand, China's tutoring industry originally had 400,000 offline institutions, including many quality-education ones, but K12 alone was at least half, 200,000 to 300,000. Yet online dual-teacher live large classes? Basically just these few players. Whether others can still enter? I think it's very difficult. Getting into online dual-teacher live large classes is relatively hard — basically around 10 companies or so.

Yu Minhong also said the other day that he thinks future online dual-teacher live large classes will have maybe around 10 players. If 10 split 80 billion evenly, that's 8 billion each. What does 8 billion mean? Among China's offline tutoring companies today, only two genuinely have annual revenue over 8 billion: New Oriental and TAL. No one else. Think about the runway, the growth trajectory for China's online dual-teacher live large class companies.

So why was Gaotu Techedu able to go public so quickly and become a company now valued at over 10 billion USD? That's remarkable. At core, everyone sees that the online barrier is extremely high, there aren't many players, and they're all benefiting from massive future market space.

Looking at one-on-one, I'm actually still quite bullish on K12 online one-on-one's future development. As I mentioned, the degradation in teaching effectiveness from moving one-on-one offline to online is the lowest. And in China, there are only a few doing online one-on-one: Zhangmen, Qingqing Education, Xuebajun, Sanhao — basically just these few.

Why so few? Mainly because everyone has believed one-on-one isn't scalable, that capital isn't interested. But I believe this view will change quickly, because K12 online one-on-one is actually very different from offline one-on-one. At scale, it absolutely becomes economical — this may differ from online one-on-one in kids' English, because LTV (lifetime value) is much larger, and it's more of a hard need. Online one-on-one has very large future development space; it's also a hard need.

Similarly, the barrier to entry in online one-on-one is also extremely high. Why? Education isn't a typical C-end internet product — education actually demands extremely high organizational and operational capability, extremely high barriers. Why were TAL Online, Yuanfudao, and Zuoyebang able to absorb 20 million free students this time? Everyone knows these companies each have over 10,000 employees. Among our offline institutions, genuinely having over 10,000 is also rare — New Oriental and TAL probably do, but many others don't. Yet TAL Online, Yuanfudao, Zuoyebang basically all have over 10,000 employees, with thousands of class mentors. A company of over 10,000 people, and an internet company tightly integrated with technology — the organizational and operational demands are extremely high.

Take Qingqing Education: on our supply side, we have tens of thousands of teachers, tens of thousands of one-on-one teachers. Imagine building that supply chain — without years of accumulation, it's incredibly difficult to build quickly.

The core of an online education company isn't "online" — its core is still an education service company. It has technology needs, but also teaching and curriculum R&D that needs time to accumulate. Its entire class mentor organizational system needs time to build. Every link needs to be forged over time. Everyone looks at Gaotu Techedu and wonders why it shot up so fast, but think about it — Larry Chen was formerly New Oriental's executive president, he worked in offline companies for many years, and Gaotu Techedu itself has been operating for five or six years. All of this takes time to refine.

The pandemic hasn't changed the essence of education — you still have to deliver good results

After the pandemic, my personal realization is that the fundamental nature of K-12 education hasn't changed — whether online or offline. At its core, you still have to deliver good results for parents and students. And "good results" in education is very clearly defined: it's about improving test scores. The core reason parents send their children to tutoring is for score improvement. Why? Because a child's time is irreversible. So price isn't the top priority — results are.

From the perspective of delivering good results, many people have been saying that after the pandemic, a lot of students will return to offline learning. Yes, absolutely many will. The classroom experience offline, especially for group classes, is still quite different from online group classes.

So we say the fundamental nature of K-12 education hasn't changed.

First, you need good teachers. The instructor has to be strong, particularly for online dual-teacher large classes — your lead teacher must be excellent, able to interact well with students. And of course you need curriculum R&D, developed over a long time.

Second, you need good classrooms. If we're talking about online education, how do you guarantee instructional effectiveness? At the most basic technical level, at least don't have lag or stuttering, right? Beyond that, you certainly need AI-based tools that can analyze the class session.

Third, you need good service. Most children in China choose extracurricular tutoring because many lack self-discipline — they still need someone keeping an eye on them. That's why dual-teacher live large classes all include a role called the "class teacher" or homeroom teacher, who provides services including Q&A, corrections, and encouragement to motivate the student. So service is indispensable too.

You can go small and niche — if you have good educational results, you can survive well. Of course if you want to scale, scaling also requires delivering good results. If you can't provide good results, you'll basically struggle to survive competition.

So after the pandemic, I believe the essence of education hasn't changed. Whether online or offline, your core mission is still to deliver good results for students. Everything needs to revolve around this — including addressing the environmental limitations of online learning through whatever means can achieve good results.

Live Q&A Session

Q: The pandemic caused online education traffic to surge. How should companies handle this influx?

Liu Changke: My own view is that it comes down to whether you have the capacity to handle it. Most companies can't. Because education services aren't purely a traffic business — if they were, then today's Toutiao, Tencent, and Baidu should all be doing great at it, but that's not the reality.

Q: Please share some experience and advice for entrepreneurs in this industry.

Liu Changke: As I mentioned earlier, online education has relatively high barriers to entry. That's why I say there are basically only so many players left in online dual-teacher live large classes now. Online one-on-one also has high competitive barriers — organizing tens of thousands of teachers nationwide isn't easy either. The technical requirements, product requirements, and organizational demands are all quite substantial.

But I've observed that as consumers have developed online habits through this wave, there are two dimensions where entrepreneurs can enter. The first is same-city online small classes — the giants find it hard to participate because it's street fighting, not tank warfare or aerial combat. Street fighting actually lets you avoid direct competition with those online giants. The other possibility is leveraging Kuaishou, Douyin, or even WeChat livestreams. Livestreaming is extremely hot right now — how to combine it with education to create entrepreneurial opportunities, I think there's room there too.

Q: What is the core underlying capability for online education companies to survive?

Liu Changke: First, as I said, the core of online education is education, not online. So it can't escape the essence of education, which is delivering teaching outcomes. This requires focusing on good teachers, good content, good classrooms, and good service — all of which test organizational and operational capabilities.

I believe the underlying core capability for online education is probably organizational and operational capability. Basically all the online dual-teacher live large classes and online one-on-one companies we discussed are at ten-thousand-employee scale, and this ten-thousand-person organization is in services, in fulfillment. You have to deliver service fulfillment properly, so at its foundation this is still about organizational operations — whether your organizational and operational capabilities are sufficient to provide good teachers, good content, good classrooms, and good service, so that students achieve good results.

Q: Do small and medium offline institutions have opportunities to partner with large online institutions? Do large institutions have this need?

Liu Changke: I believe they definitely do. Because online education has made industry division of labor much clearer. Think about it — originally, if you ran an offline institution in any small place, however small, it had to be fully equipped. You had to do marketing, student recruitment, teaching and curriculum R&D, teacher recruitment, teacher retention, teacher performance evaluation, teacher assessment, student services — you had to do everything across the entire chain.

But today, you can partner with online education companies and focus on what you're good at. For example, locally, what do you do? You mainly do recruitment and service locally. Teaching and curriculum R&D, you can leave to the online institutions. Locally, you focus more on localization — recruitment, building close relationships with users, and follow-up services. I think this is viable.

The core of online education is supply chain restructuring. Originally, to open a school somewhere, students were local and teachers had to be local, so the supply chain was basically local. But today, online education can build supply chains nationwide. Why can institutions like TAL's online school and Yuanfudao simultaneously serve tens of millions of students? Because they can distribute their supply chain across the country — their tutoring teachers might be in Xi'an, Zhenjiang, or Jinan.

So the core of online education is supply chain restructuring, which also makes the cost structure more rational. A teacher living in Shanghai might cost you 10,000 RMB. But if the teacher is in Xi'an, maybe 6,000 RMB suffices. Online education has restructured the entire supply chain system of the education and training industry, and thereby restructured its cost structure.

Q: In online and offline education, what aspects can AI replace human labor?

Liu Changke: I think people are thinking about this a lot now. Honestly I haven't researched it deeply, but I believe for many K-12 students, the main problem with supplementary tutoring is addressing insufficient self-discipline in learning. That's why even with such amazing teachers in dual-teacher live large classes, they still pair them with tutoring teachers — because students still need human service.

I think service is something AI will have difficulty replacing. Education involves human nature. For students, you need to encourage them, motivate them — I don't think AI can replace humans in this. Humans still need to be there. Of course, I believe AI may in the future assist teachers in teaching better. It can assist students — it's not a replacement relationship. It will only make student learning more efficient and teacher instruction more efficient. I don't really accept the word "replacement" here; the two should still be combined.

Q: How can offline education combine with online to become stronger?

Liu Changke: As I said, for offline education, going forward you still need to be local, but you must embrace online — find a way to create a new business model called same-city online small classes. Your recruitment is local, your service is local, you can interact with local parents and students, and your teaching content closely follows local curriculum progress, exam conditions, and student situations. So I think this combination is essential. Because consumers have already been educated to accept many things.

Probably going forward, online-offline integration will be necessary. For example, much of students' future homework, testing, and follow-up Q&A can be completed online. But offline classrooms may still be needed.

I think this actually makes you stronger. Don't worry about competition from online dual-teacher live large classes — they can't do the street fighting work. Of course when you do street fighting, combined with this advantage, your core is still being able to deliver better teaching results for local students. With both localization and the combined advantages of online and offline, if you can deliver better results than online dual-teacher live large classes, you'll be stronger.

Q: Do dual-teacher, triple-teacher, or even multi-teacher models still have opportunities?

Liu Changke: If you're doing online dual-teacher live large classes, the opportunity isn't great. But if you're doing local same-city online small classes, I think the opportunity is very large. Because consumers have been fully educated through this wave — they accept online elements, but many consumers still feel their children need that offline group class environment. So I believe same-city online small classes should have very good opportunities.

Q: Why did you change Qingqing Jiajiao (轻轻家教) to Qingqing Education (轻轻教育)?

Liu Changke: That's a very good question. In 2014, when I left Only Education and founded Qingqing Jiajiao, my thinking was quite simple. Online wasn't that hot yet then. We saw a major trend across industries — the shift from "going to the store" to "delivery to home." In education, we believed consumers had a very rigid need: rather than taking their child to a tutoring institution themselves, because it takes a lot of time on the road, those with means wanted to have teachers come to their home. So we named it Qingqing Jiajiao and did door-to-door service.

But starting from the year before last, we gradually shifted to online. Last year, online business was about 50%. This year it's about 85%, with offline business only 10-15%. "Jiajiao" (home tutoring) still feels like offline door-to-door service, so based on this we renamed to Qingqing Education. Because we're mainly doing online now, currently focused on online one-on-one business.

Q: Your entrepreneurial experiences in education have all been quite successful. Please share your insights.

Liu Changke: Actually I wouldn't say very successful. I'm just quite persistent — once I'm set on something, I don't give up easily. All these years I've only built two companies. The first was Only Education, which I ran for over twenty years. Our generation caught a good time, unlike today's intense competition. We were in Shanghai, and just plugged away at it. Later because we did reasonably well, we went public in 2014.

Around the IPO, I saw some limitations in the offline tutoring model, and saw the trends toward "home delivery" and "online." After going public, I left to start Qingqing Education. Just these two experiences — nothing to say about success or not success. I just commit to something and don't turn back until I hit a wall, keep persisting, and I believe eventually you can make it work.

Didn't Jack Ma also say — improve a little bit every day compared to yesterday, be a friend of time and accumulate slowly, and eventually you can succeed. Especially in education — I often say education is like long-distance running, it's hard to go fast. Because parents definitely spread the word based on experience and reputation. So it's a long run. Founders of education companies are all in it for the long run. I'm also a marathon enthusiast, have been running for nearly 10 years, probably quite a seasoned marathoner. My personal best full marathon time is 2 hours 59 minutes. So I actually approach building companies as a long-distance run — I quite enjoy it, and just keep at it.

Summary

-

After the pandemic, the entire offline education and training institution industry will display a very pronounced dumbbell-shaped structure. One end of the dumbbell is large institutions; the other end is small institutions close to users, with tenacious vitality.

-

Online education has restructured the entire supply chain system of the education and training industry, and thereby restructured its cost structure.

-

The pandemic didn't change the fundamental nature of K-12 education. Whether online or offline, the core is still delivering real results for students.

-

Education services aren't purely a traffic business. It's more like a long-distance run — hard to rush.

(This article originally appeared on DuoZhi Network. Feel free to share it on Moments.)

2020: Tourism's Reset and Restart | Frees Fund After the Pandemic: Education's Survival Tournament | Frees Fund Post-Pandemic: New Landscapes in Fresh Produce, Dining, and Food | Frees Fund After the Pandemic: A New Era for "Good Companies" | Frees Fund Li Feng Column 16 | Fresh Retail: Learning Early-Stage Investing from the Secondary Market Li Feng's New Year Outlook | Mapping China's Opportunities in 2020 Will Logistics Produce Companies Like Uber or DiDi? | Frees Fund — Learning to Invest Through Investing