A 10,000-Word Deep Dive: Deconstructing the Changes and Opportunities in New Energy Vehicle Sales and Aftermarket Services | FreeS Report 35

What innovation opportunities exist in sales and after-sales service amid the fierce competition in new energy vehicles?

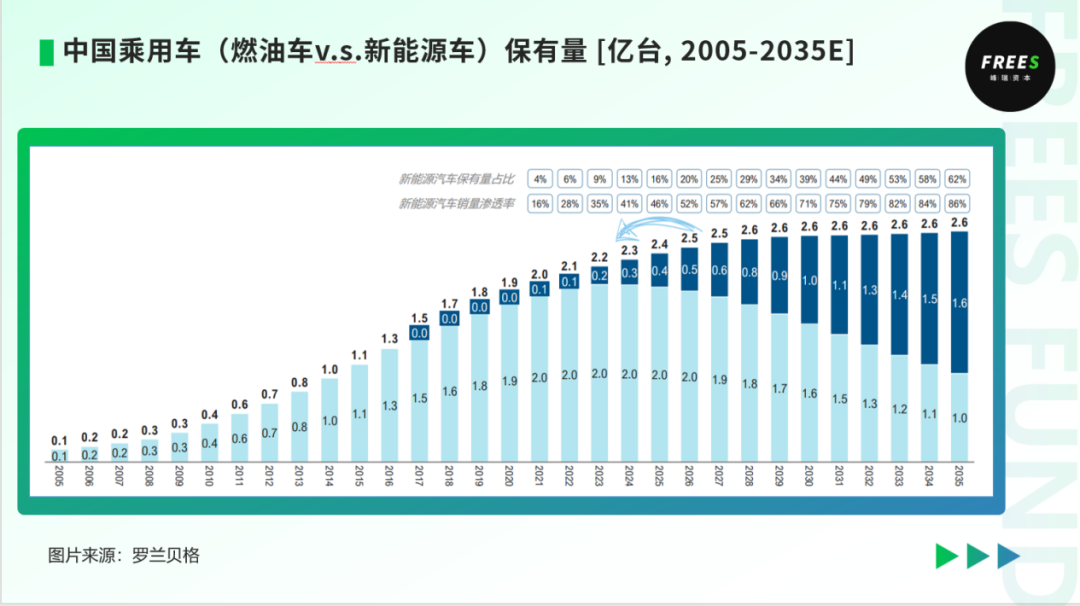

Whether or not we own an NEV ourselves, the odds of hailing one keep climbing. Data released in September by Gao Bo, deputy director of the Transport Service Department at the Ministry of Transport, tells the story. By end of 2022, the total number of new-energy taxis on the road approached 300,000, accounting for 22% of all taxis. Going forward, the new-energy transition rate for buses, taxis, and logistics vehicles will reach no less than 80%. That 80% means four out of every five taxis will be electric. That's no small share. Another figure set to keep surging: NEVs' share of passenger vehicle sales. According to data from the China Passenger Car Association, this figure was 27.6% in 2022; it's projected to jump to 36% in 2023. Consulting firm Roland Berger estimates that by 2035, NEVs will account for over 80% of new vehicle sales in China and over 60% of total vehicle stock.

The spread of NEVs has already unleashed a storm of change on the brand and manufacturing sides. We're curious what happens to sales and after-sales service as the industry shifts lanes from internal combustion to electric. Some changes are directly tied to the fundamentally different architecture of NEVs.

- NEVs replace the internal combustion engine with a three-electric system: battery, motor, and electronic control. That nearly eliminates maintenance needs around engine oil and oil filters — demands that previously made up nearly half of the traditional vehicle maintenance market. How to properly maintain the three-electric system has become the auto service industry's new imperative.

- Because NEVs deliver higher horsepower and feature different braking systems, among other factors, accident rates and per-repair costs currently run significantly higher than for ICE vehicles.

- NEVs are also enabling new lifestyles. When camping outdoors, drivers can tap into their vehicle's battery to power lighting, heating, and more.

Favorable policy has arrived too. In October 2023, the Ministry of Commerce, together with nine other departments, issued Guiding Opinions on Promoting High-Quality Development of the Automotive Aftermarket, calling for optimized circulation of auto parts, upgraded repair services, accelerated development of technical standards for NEV maintenance, support for RV campground construction, and richer automotive cultural experiences.

This article examines the evolution across four domains: vehicle sales and logistics, maintenance and parts, car wash and film application, and automotive lifestyle. It seeks to answer:

- As NEVs rise, what changes are unfolding in sales and after-sales services? What's driving them?

- The automotive sales and service ecosystem is sprawling, involving OEMs, dealerships, used-car platforms, repair shops, and detailing shops. At which points in this chain do OEMs versus service providers hold more leverage?

- How will the NEV sales and after-sales landscape shift over the next 5–10 years?

- What new entrepreneurial and investment opportunities emerge from these changes? Which links in the previously tightly coupled service chain might break free and develop independently?

- What can the evolution of home appliance and mobile phone repair markets teach us about the NEV aftermarket?

We hope this offers fresh perspective. If you're an entrepreneur or practitioner in the automotive ecosystem, you're welcome to reach out to Meng Changjie, early-stage project lead at FreeS Fund and co-author of this piece (mengchangjie@freesvc.com).

Engagement giveaway: What innovation opportunities do you see in automotive sales and after-sales services?

Share your thoughts in the comments. By 5:00 PM on November 13, the five most thoughtful commenters will receive Robert M. Pirsig's Zen and the Art of Motorcycle Maintenance.

01 From Traditional 4S Stores to Direct-Sales Experience Centers: What's Changing in NEV Sales and Logistics?

Sales: The traditional 4S model is partially giving way to direct-sales experience centers + multi-brand authorized dealerships

The most visible change in the NEV industry compared to traditional ICE vehicles is the evolution of the sales system. In prime mall locations across tier-1 and tier-2 cities, you now regularly spot direct-sales experience centers for brands like NIO and Li Auto.

▲ NIO Xi'an Zhengda International store. Image source: NIO official website

Traditional 4S stores selling ICE vehicles are typically located in suburban areas, with large footprints combining sales and service. These dealerships are primarily opened by distributor groups, not brand-owned.

▲ Chongqing Baoxianghang BMW 4S store, located at Chongqing Southwest International Auto Trade City. Image source: Maiche.com

NEV OEMs, particularly the new-wave players, have begun experimenting with direct-sales experience centers. These centers tend to share several characteristics:

First, they're mostly located in shopping malls, closer to consumers with higher foot traffic. Second, they're well-designed, with sales separated from service and from delivery centers, aiming to project a high-tech, forward-looking brand image. Third, they're currently concentrated in tier-1 and tier-2 cities where charging and maintenance infrastructure is mature, brand recognition is strong, and order density is high.

Most traditional OEMs' NEV brands still leverage existing dealer networks. However, some traditional OEMs seeking to refresh their brand image and escape distributor system constraints have in recent years experimented with building new dealer networks or direct-sales layouts.

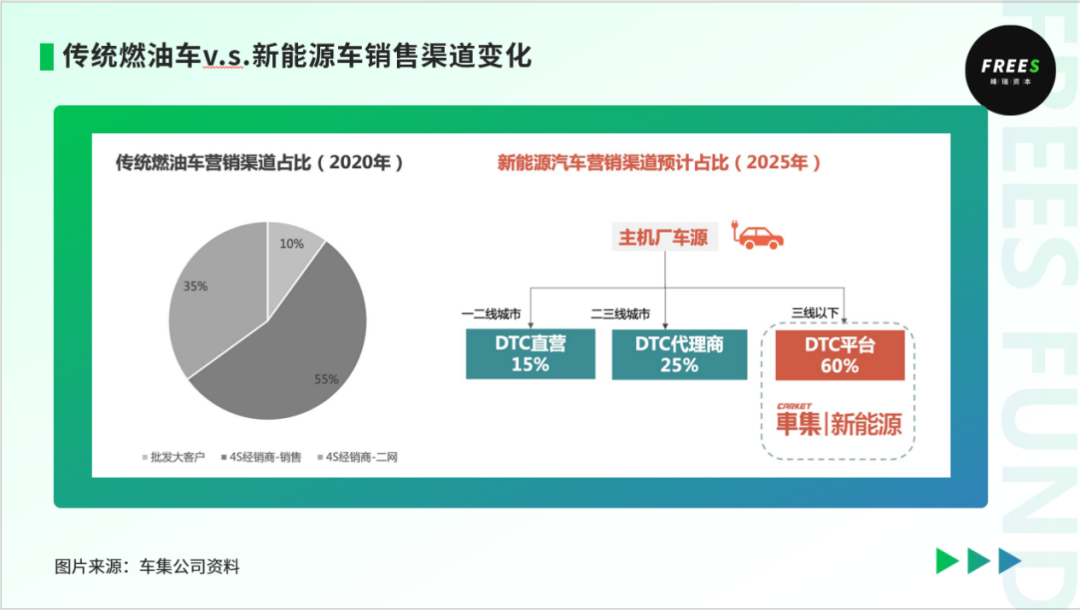

The prerequisite for direct-sales stores is sufficiently concentrated sales volume. In recent years, NEVs have shown a clear下沉 (market penetration into lower-tier cities) trend. In 2022, NEV penetration rates in tier-2 through tier-5 cities more than doubled.

For the vast non-tier-1/new-tier-1 cities, NEV OEMs mainly employ three approaches to complete sales and delivery:

First, online lead generation directing customers to provincial-capital direct-sales stores for ordering and cross-city delivery — though this approach is less efficient and delivers inferior customer experience.

Second, in some provincial capitals where NEV penetration remains relatively low, we've seen the emergence of large multi-brand collection stores. For example, JD.com has opened JD Auto Super Experience Centers in Shenyang and Xi'an, occupying large ground-floor spaces in core commercial complexes and aggregating brands including Tesla, BYD, and Voyah. These centers also incorporate JD's home appliances, furniture, and 3C products.

▲ Image source: JD Auto

Third, for more下沉 tier-3 and tier-4 cities and county-level markets, NEVs and ICE vehicles alike use multi-brand authorized collection stores, but with smaller footprints, mainly street-facing showrooms, and focusing on more affordable brands.

Taking Cheji — a one-stop NEV service platform backed by FreeS — as an example, it currently operates multi-brand collection stores primarily in tier-3 and tier-4 cities in central and western China, carrying brands such as Neta and Leapmotor.

▲ Cheji NEV Experience Center. Image source: Cheji New Energy

The cash flow problems of traditional 4S stores are already industry consensus. As NEV competition intensifies, brands seeking to relieve sales pressure are offering multi-brand collection stores more relaxed payment terms, partially resolving the cash flow issues that have long plagued traditional 4S stores and creating new opportunities for innovative players.

Used-Car Market: Higher Standardization in NEVs Creates New Opportunities for Platform-Based Trading

If you've ever bought a used gas-powered car, you probably remember staring at the engine, transmission, body frame, chassis, and countless other components — completely lost on how to assess the vehicle's condition. Maybe you only found out after bringing it home when friends or family broke the news: "This was in a major accident," or "The engine was completely rebuilt." Too late.

In the traditional used-car market for gas vehicles, the sheer variety of brands and models, the complexity of parts, and the highly non-standardized condition of vehicles have made it difficult for online trading platforms to consolidate market share. Offline independent dealers have long dominated, leaving internet platforms under persistent profit pressure.

NEVs are different. Their supply chains are relatively standardized — closer to consumer electronics — with significantly fewer parts SKUs. A gas vehicle requires roughly 30,000 components; a pure electric vehicle needs only about half to two-thirds of that. This makes NEV condition easier to inspect, raises standardization levels, and enables more transparent pricing systems.

This creates fresh opportunities for internet-based used-car platforms and third-party service providers. For instance, the automotive service platform Chaboshi (查博士) received a strategic investment from CATL. According to ChinaVenture, the company originally specialized in inspection services for traditional gas vehicles but may extend its business into used NEV services.

▲ Chaboshi web platform service page. Image source: Chaboshi official website

Logistics: The Rise of Socialized Third-Party Logistics and Increasing Market Concentration — Who Will Be the "SF Express" of NEVs?

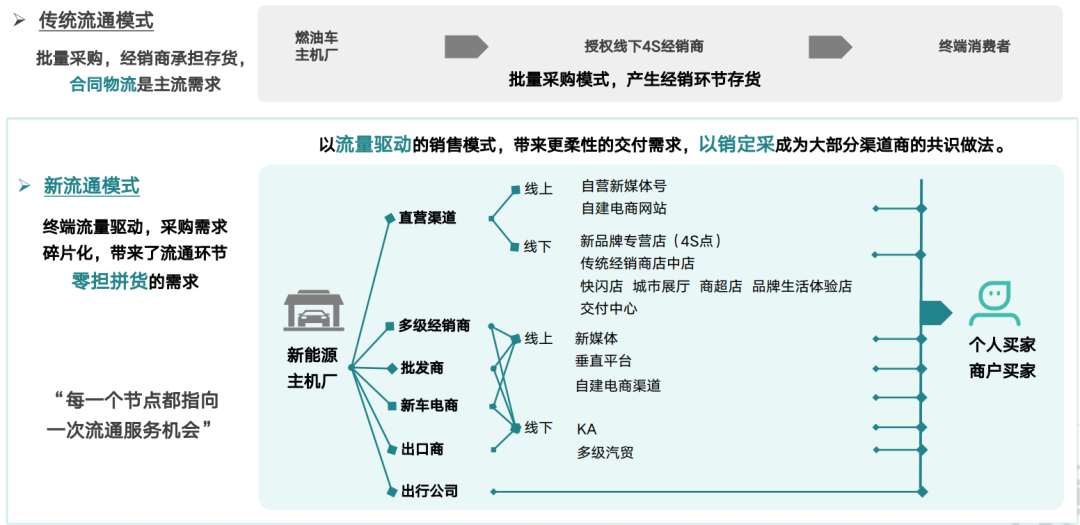

Changes in sales systems tend to drive changes in logistics. How do cars get from the OEM to the customer? In the traditional gas vehicle distribution model, dealers typically purchase in bulk, with transportation handled by contract logistics systems tightly bound to OEMs, supplemented by fragmented dedicated line transport.

▲ Image source: Cheliuzi logistics company materials

We speculate that NEV vehicle logistics systems will likely achieve higher concentration, creating an opportunity for an "SF Express" of the NEV sector.

First, NEV sales systems are more diverse, with richer multi-brand collection store formats. Correspondingly, logistics has evolved from one-to-one systems between OEMs and 4S stores to many-to-many networks. These changes intensify brands' demand for less-than-truckload (LTL) consolidated shipping. Analogous to consumer goods logistics, OEMs independently managing the full fulfillment chain is clearly less efficient than independent logistics systems with greater economies of scale. Meanwhile, more dispersed and diverse sales systems demand higher digitalization, bringing innovation opportunities.

Second, NEV production bases are mainly located in second- and third-tier cities — Hefei, Chongqing, Lishui, Xi'an, Changzhou, Changsha, Fuzhou, Zhengzhou, Xiangyang, and others — while demand concentrates in first-tier cities. In recent years, some local governments have abolished restrictions on cross-regional used-car migration (policies that previously limited vehicles from other provinces or cities through emissions standards or model year requirements to prevent market flooding). This has channeled large volumes of used cars from first-tier cities into more下沉 markets. Combined, these two factors create a compelling dynamic: logistics moves new vehicles from second- and third-tier cities to first-tier cities, then carries used vehicles back on return trips — substantially addressing the "empty backhaul" problem that has long plagued vehicle logistics.

Third, as the Belt and Road Initiative advances, NEV sales in Central Asia, the Middle East, and Southeast Asia have grown markedly, creating new opportunities for vehicle export logistics.

02 The Maintenance, Repair, and Parts Market Won't Shrink Immediately, But Will Undergo Structural Adjustment

Market Demand Will Decline Significantly, Mainly in Maintenance and Powertrain Repair; Accident Repair Average Order Value and Frequency Both Increase

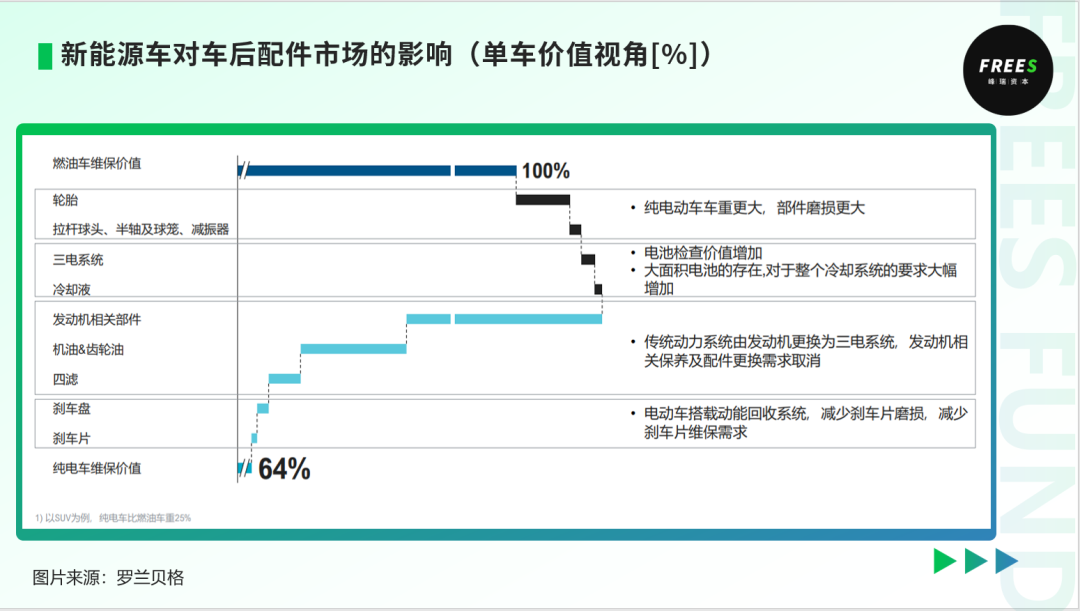

Compared to gas vehicles, overall NEV maintenance and repair demand is expected to drop substantially. According to Roland Berger estimates, in the long term, NEV maintenance value will be roughly 60% that of gas vehicles. The biggest driver: the engine-transmission system in gas vehicles is replaced by the battery-motor-electronics ("three electric") system in NEVs, causing structural demand for maintenance to fall.

Specifically, we typically break passenger vehicle maintenance into four categories: maintenance, wearables, repair, and accident. For traditional gas vehicles, maintenance mainly means oil and coolant changes; wearables means inspecting and replacing tires, brakes, and other consumable parts; repair covers engines, transmissions, and chassis; accidents include body panels, paintwork, and structural repairs.

Because NEV components differ from gas vehicles, all four demand categories shift significantly.

First, due to different powertrains, NEV demand for oil and oil filter changes will virtually disappear — previously nearly half of the gas vehicle maintenance market.

Second, for wearables: NEVs don't need spark plugs, and brake pad wear is lighter than gas vehicles. However, battery inspection and replacement demand grows. Meanwhile, NEVs' heavier weight causes more severe tire wear. Overall, the wearables sub-market size remains flat.

Third, for repair: traditional engine and transmission repair demand disappears, representing roughly 40-50% of the overall repair market. Three-electric system repairs are relatively rare. Additionally, under the intelligence trend, NEV chassis complexity is increasing — many mid-to-high-end models now use smart chassis with intelligent, real-time adaptive suspension — raising chassis repair average order values.

Finally, current NEV accident probability and repair costs are both noticeably higher than gas vehicles. Several factors: one, NEVs are new to most drivers, and NEV users skew younger with less driving experience; two, NEV horsepower is extreme — often four to five hundred — increasing handling difficulty; three, drivers sometimes struggle to adapt to NEV brake pedals, causing operational issues; plus NEVs' higher intelligence means abundant cameras and radar, with costly repairs when accidents occur.

Thus, accident repair may become a growth market in the near term. However, as consumers gradually adapt to NEV power and handling, accident repair demand will normalize over the long run.

In the medium to short term, though, the maintenance and repair market won't shrink immediately. Gas vehicle ownership and fleet age are still growing; the aftermarket parts market will likely peak around 2030, expanding from roughly 600 billion RMB to nearly 800 billion. Afterward, as NEV ownership share rises, the corresponding aftermarket will experience growth followed by gradual decline.

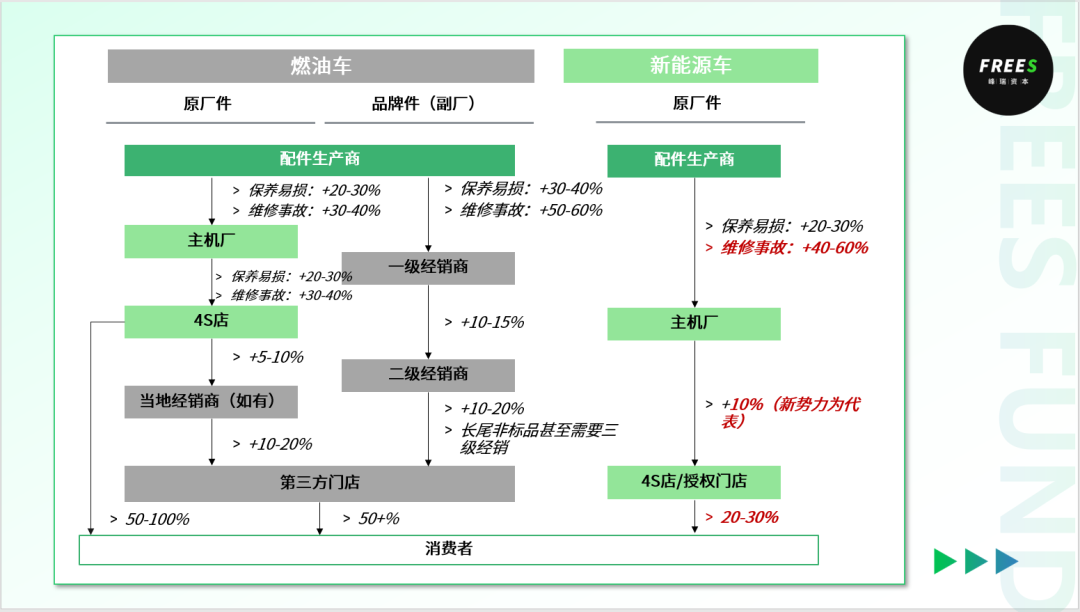

Changes in Parts Distribution: Third-Party Socialized Networks Gradually Replaced by Authorized Systems, Supply Chain Efficiency Improves, Terminal Markups Decline

First, as the market shifts from gas to NEVs, third-party socialized aftermarket parts distribution networks will gradually be replaced by authorized systems.

▲ Comparison of gas vehicle and NEV distribution systems. Data sources: Autohome, expert interviews

Traditional gas vehicle parts are complex with numerous SKUs; OEMs cannot encompass the entire supply chain in their authorized systems and must rely on socialized distribution to properly serve consumers. So from Tier 1 suppliers selling branded parts directly, to midstream vertical distribution systems like the automotive wearables platform Santouliubi (三头六臂车服), the parts procurement platform Kuaizhun (快准车服), the full-vehicle-parts-focused Kaisi (开思车服), and various regional distributors — even 4S stores, pressured by ordering requirements, would sell branded OEM parts externally to aggregate orders and secure larger OEM discounts.

NEV parts are more streamlined with fewer SKUs. In this environment, OEMs can bring the parts supply chain under their authorized system control, reducing dependence on third-party socialized networks.

The second change: as distribution systems streamline, markup rates at each环节 decline. For gas vehicle maintenance, 4S stores typically mark up parts by 100% or even several times, far exceeding street-level independent shops. Currently, some new-force OEMs keep parts markups for their stores quite low, and some NEV 4S/authorized stores can compress parts markups to 20-30% — significantly below gas vehicle 4S stores. Why such lower markups for NEVs?

On one hand, this reflects efficiency gains from streamlined distribution. When SKU counts drop dramatically and distribution links decrease, 4S and authorized stores don't need large markups to offset the efficiency losses and cost increases from managing complex SKUs.

On the other hand, NEV companies' business philosophy differs from traditional automakers. The gas vehicle market has become a bloody red ocean, with vehicle sales margins extremely thin or loss-making. So these stores tend to acquire customers through car sales first, then pivot to long-term maintenance services for high profits. NEV automakers, for now, mostly don't need to plug profit gaps through after-sales maintenance.

Changes in Maintenance Terminal Formats: Authorized Replaces Third-Party, Suburban Large Stores Replace Street Shops, OEM Dispatch Replaces ToC Customer Acquisition, Multi-Brand Collection Replaces Single-Brand 4S, Sales-Service Separation Replaces Sales-Service Integration

Above we analyzed how NEVs will impact maintenance demand and parts distribution. These two changes will jointly reshape maintenance terminal formats.

Gas vehicle maintenance comprises two systems: warranty-period service dominated by 4S stores, and out-of-warranty service dominated by third-party independent networks. The typical third-party format is street-level quick maintenance shops like Tuhu Car — small footprint, roughly 4-6 bays, close to residential areas, focused on maintenance and simple repairs. But as NEV ownership penetration rises, direct-operated and authorized service centers are becoming mainstream relative to third-party independent networks.

Additionally, looking at the current state of new car-making forces, sales terminals are separating from after-sales service terminals. Cities with high NEV ownership typically have direct-operated service centers. In cities with lower ownership, large authorized repair shops have emerged. These authorized repair shops are usually located on urban outskirts, with floor space exceeding 1,500 square meters, aggregating maintenance services for multiple authorized brands. Currently, the rapid development of direct-operated and authorized service centers is squeezing the growth space of street-level quick maintenance shops.

V-Sheng New Energy represents the typical NEV authorized service system. V-Sheng started with luxury vehicle repairs for Mercedes-Benz, BMW and others. In 2017, it entered the NEV maintenance market and has since established strategic partnerships with multiple leading NEV manufacturers and battery suppliers.

▲ Image source: Qixiu Tianxia

In short, the terminal formats of NEV maintenance are undergoing the following changes: authorized service replacing third-party, suburban large shops replacing street-level small shops, OEM dispatch replacing B2C customer acquisition, multi-brand authorized shops replacing single-brand 4S stores, and sales-service separation replacing sales-service integration.

So why are these changes happening in NEV maintenance terminal formats? Why can NEV manufacturers achieve the strong control that traditional ICE OEMs could never realize?

From the perspective of subjective intent, OEMs want to improve consumer vehicle experience and more comprehensively capture vehicle performance data and long-term consumer usage data. Through direct-operated and authorized service systems, OEMs can understand consumer vehicle usage throughout the entire process.

Furthermore, the first reason lies in "controlling the venue through inventory." We analyzed above the changes in parts distribution systems — traditional ICE vehicle parts supply chains relied on third-party distribution networks. NEVs can incorporate parts distribution into their authorized systems, thereby controlling the service terminals through inventory control and bringing maintenance terminals into the authorized system.

The second reason relates to NEV intelligence. Core NEV components require authorization codes to access for repairs. Therefore, such repair needs can currently only be met through authorized systems.

Third, compared to ICE vehicles, NEVs have significantly reduced maintenance needs, transforming the after-sales business from high-frequency to medium-low-frequency. For repair needs, in the long term, the customer acquisition logic for shops may shift from B2C to OEM dispatch.

Fourth, longer warranty periods for NEVs, currently higher repair complexity, and consumer lack of trust in third-party repair capabilities lead consumers to prefer staying within the authorized system.

Taking NIO as an example, owners first submit repair requests through the app, then dedicated personnel pick up the vehicle and deliver it to the service center. Owners never need to directly interact with the repair party. From the terminal perspective, obtaining more brand authorizations is a key factor in customer acquisition. Therefore, although street-level quick maintenance shops are closer to customer traffic, their lack of authorization makes customer acquisition difficult. Compared to maintenance, repairs take longer, meaning vehicles sit for longer periods, requiring shops to have larger parking areas and stronger order aggregation capabilities — leading to the large-shop format becoming mainstream, what the offline chain industry often calls "high-frequency small shops, low-frequency large shops."

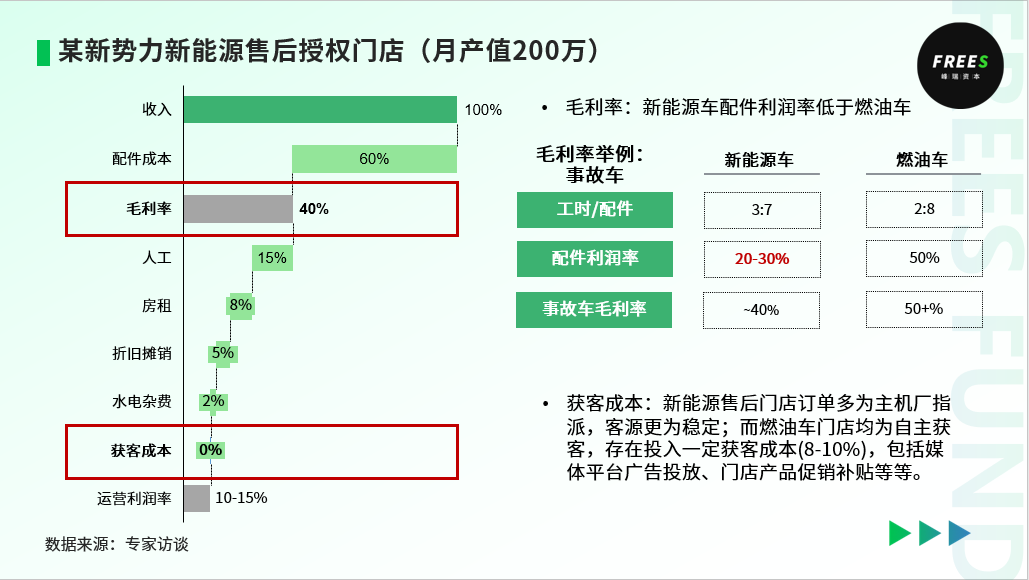

On the foundation of the authorized system, the chain rate and profitability of NEV after-sales maintenance could both outperform the current third-party ICE vehicle maintenance system. Regarding chain development, for OEMs, managing several chain systems within a certain region is more efficient than one-on-one management of dispersed shops. In terms of profitability, since OEM dispatch saves customer acquisition costs, although authorized shops cannot earn excess profits, they can still substantially improve the persistent profitability challenges faced by current automotive maintenance chains.

The following figure shows an example of a new energy after-sales authorized store. This store's gross margin is approximately 40%, down from the roughly 50% gross margin of traditional ICE vehicle after-sales shops. However, because new energy after-sales stores save on customer acquisition costs, they can still maintain relatively decent store profits.

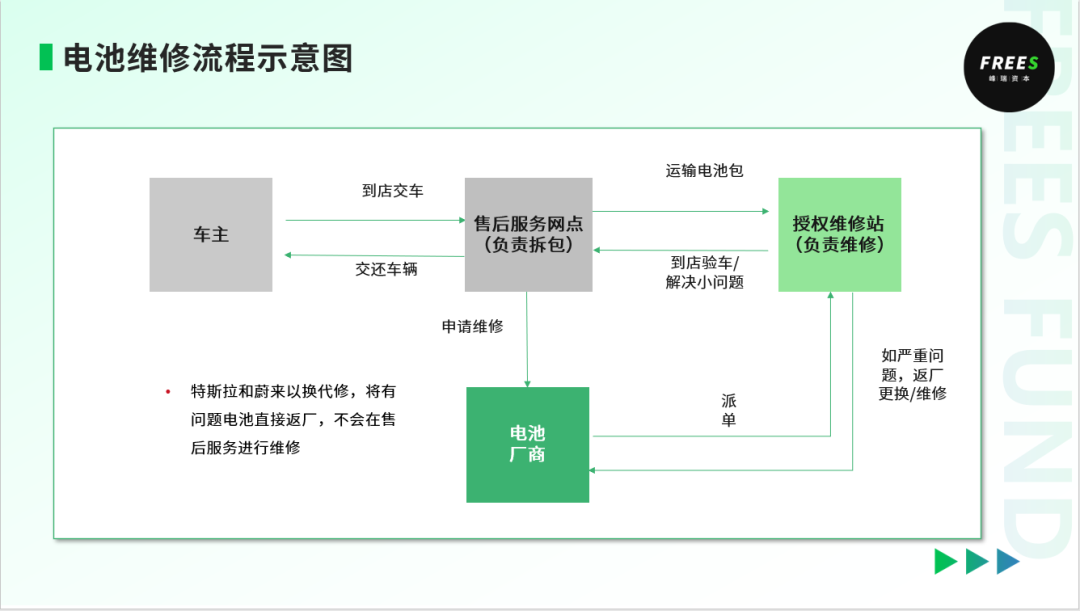

▎Battery Repair System Development Trends: Vehicle Repair and Battery Repair Moving Toward Integration, Battery Repair Potentially Replaced by Direct Battery Swap, New Opportunities in Front-End Recycling Systems

Currently, due to the high technical difficulty of battery repair, battery repair and vehicle repair remain separate. Most vehicle repair outlets only handle pack removal, then dispatch to battery manufacturer-authorized battery repair stations (represented by CATL) or direct factory return for repair (represented by BYD, where battery technology confidentiality is high and vehicle-battery integration is advanced).

Currently, battery manufacturers hold strong bargaining power throughout the battery repair service chain. But in the long term, it's not efficient for battery manufacturers to分散精力自营售后, and battery repair technology will likely gradually become widespread. Therefore, the authorization systems for vehicle repair and battery repair will likely move toward integration. As NEV battery range and lifespan continue to increase, batteries may follow phones in shifting from repair to direct replacement. In the future, retired NEV batteries could be reused in numerous industrial and commercial scenarios, potentially creating new opportunities for front-end recycling systems.

/ 03 / What Insights Does the Evolution History of Home Appliance and Phone Repair Markets Offer for Thinking About the NEV Aftermarket?

The current NEV aftermarket remains in early development stages. Looking ahead, say ten years from now, how the NEV aftermarket will evolve remains to be seen. But we can attempt to project the development trajectory of the NEV aftermarket by examining the evolution history of home appliance and phone repair markets.

In earlier years, the home appliance installation and repair market was dominated by socialized networks, with street repair shops and independent repair technicians as the main service providers. The current home appliance installation and repair market has gradually evolved to be primarily authorized-system based, with socialized networks as supplementary. The authorized system includes service provider networks established by appliance companies and retail channels. Appliance companies often establish a service company to specifically organize these authorized service outlets, such as Midea Group's Meimei Jiayuan, TCL's Shifen Daojia, etc. Additionally, retail channels build their own service networks, such as Gree delegating all after-sales repair to dealers, Suning's Suning Bangke, and JD.com's JD Service+.

▲ Image source: Eastday

Leading brands' authorized service outlets can achieve coverage at the county level and above. Second-tier brands' authorized service outlets can achieve coverage in tier-1 and tier-2 cities. More下沉 markets are handed to socialized networks (such as Wan Shifu, Zhuomuniao, etc.) to complete services.

Long-tail brands with limited capabilities mainly rely on socialized service provider networks, as well as other brands' service provider networks and channel service provider networks, to achieve product installation and repair. For example, TCL's installation and repair service company Shifen Daojia also undertakes installation and repair needs for major brands in下沉 markets and small-to-medium brands.

The key factors in the home appliance aftermarket's evolution toward authorized systems as primary and socialized networks as supplementary are:

First, home appliance delivery, installation, and repair are integrated, and delivery and installation services are under strong brand control. Additionally, brands have more direct communication channels with consumers, making it easier for consumers to develop the habit of going to official channels when problems arise. Calling brand customer service and seeking solutions through sales channels have become consumers' preferred options.

Second, authorized system repair prices are not significantly more expensive than socialized networks — the after-sales system is not a profit center.

Third, home appliance quality has improved and become more durable, making it difficult for most street shops and independent repair technicians to obtain sufficient orders to sustain operations.

For the phone repair market, before smartphones were introduced, due to high communication costs between brands and consumers, low phone technical complexity, and other reasons, socialized repair networks similarly dominated the market.

In 2007, Apple released the first-generation iPhone, ushering in the smartphone era. Because smartphones were more expensive and technically complex, and socialized repair networks had uneven repair capabilities that made it difficult to gain consumer trust, authorized systems gradually came to dominate the repair market.

After most manufacturers including Huawei and Xiaomi launched smartphones, smartphone supply chain systems became increasingly mature, and socialized repair networks once again became market mainstream through lower prices. The main reasons were that core phone components (screens, batteries) had mature supply chains with overcapacity, enabling socialized repair networks to obtain high-quality components from leading suppliers at sufficiently low prices. Additionally, socialized repair networks' repair capabilities were gradually improving.

But notably, due to short phone replacement cycles and high integration, trade-in programs within authorized systems became consumers' more primary way of handling phone damage, leading to an overall small repair market.

In summary, whether the NEV aftermarket will form broader direct operation, remain primarily authorized-system based, or gradually move toward socialization in long-term development mainly depends on the following:

-

The degree of battery supply chain standardization and overcapacity, whether sufficient to enable socialized repair systems to obtain sufficiently high-quality aftermarket replacement batteries at low prices, breaking free from OEM control on core components.

-

The degree of NEV intelligence and vehicle integration, whether high enough to enable OEMs to continuously maintain after-sales orders in their own hands.

-

Whether NEV brand concentration will be higher or lower than ICE vehicles, and the degree of concentration at different city levels, which will determine whether OEMs ultimately form one-to-one direct operation or multi-brand authorization models. Compared to ICE vehicles, NEV brand concentration and concentration levels at different city tiers will to some extent determine whether OEMs ultimately form one-to-one direct operation or multi-brand authorization models.

/ 04 / How Will the Car Wash, Detailing, and Film Application Market Upgrade and Innovate?

▎Car Wash Market: Car Wash Format Gradually Separating from Maintenance System, Solving Efficiency and Customer Acquisition Through Deep Automation and Digital Marketing

Traditionally, car wash services have functioned as an appendage to the maintenance and repair ecosystem. As noted above, NEVs dramatically reduce routine maintenance needs, and repairs are needed far less frequently. So what impact does this have on the car wash business?

The classic car wash model is a quick-service maintenance shop with one or two wash bays. The store doesn't profit from washing cars; instead, it uses the higher-frequency service to funnel customers toward more lucrative maintenance and repair work. Under this operating logic, the car wash format faces two major problems: first, brutal price competition makes profitability difficult; second, operating hours are constrained by the maintenance business. Many car owners who work late, for example, know the frustration of not being able to find an open car wash.

Going forward, as NEV maintenance and repair frequency declines, car wash operations may gradually separate from the quick-service maintenance system. Operating as a standalone business, the first challenge to solve is profitability — which means solving for efficiency and customer acquisition.

One solution for improving efficiency is automation and assembly-line specialization.

America's largest car wash chain, Mister Car Wash, went public in 2021 and currently trades at a market cap of nearly $2 billion. Mister Car Wash operates primarily large-format locations where the entire wash process unfolds along an elongated tunnel with a conveyor belt moving vehicles through. This approach enables finer division of labor: each step handles just one task — pre-soak, foam application, rinse, exterior wipe, blow-dry — creating a highly streamlined operation that "trades space for time."

▲ Image source: COLEMAN HANNA, Foursquare

In Car Wash Automation 1.0, represented by automatic car wash machines, some progress was made on reducing wash duration and exterior-wash labor, but efficiency gains were marginal and the customer acquisition problem remained unsolved.

In Automation 2.0, we've observed players building on 1.0 with deeper innovations. Through more comprehensive automation, they're automating additional processes including sales, store assembly, and wiping.

Take Beijing-based startup chain "Midnight Car Wash" as an example: the company uses a "prefabricated store" approach, where floor drainage, exterior frames, and equipment are all integrated at a factory, then shipped as standardized finished products to locations nationwide, enabling store assembly within a single day. The stores are also experimenting with sales robots and robotic arms to replace human labor, achieving cost reduction and efficiency gains.

▲ Image source: Midnight Car Wash

Additionally, Midnight Car Wash has strong content production and traffic operations capabilities that help solve customer acquisition. For instance, stores are designed with a cyberpunk aesthetic, complete with photo setups that encourage car owners to shoot and share on social media; the chain also collaborates with influencer store visits and marketing campaigns to drive foot traffic.

▲ Image source: Midnight Car Wash

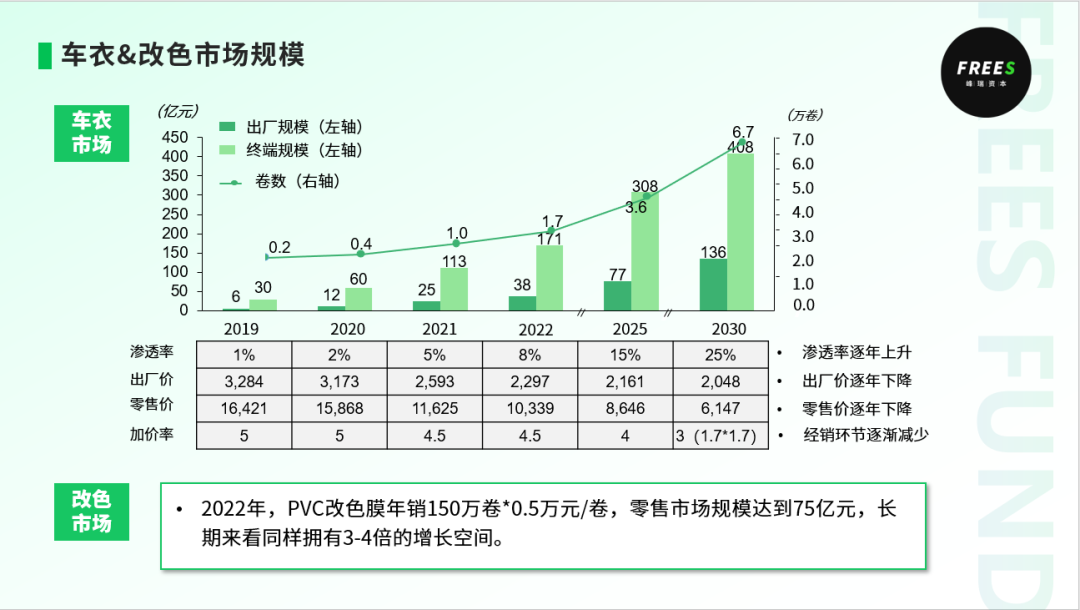

▎ Paint Protection Film and Color-Change Wrap Market: Significantly Higher Adoption Rates on NEVs; Domestic Substitution of Core Technology Creates New Opportunities for Chinese Brands

In recent years, NEV exteriors have become increasingly diverse, with significantly higher adoption rates for paint protection film (PPF) and color-change wraps. Two main factors drive this.

First, NEV owners skew younger and tend to embrace novelty. Compared with traditional ICE vehicles, NEVs offer less differentiation across brands and models, making it harder to satisfy consumer demand for personalization and customization. As a result, more consumers are choosing post-purchase color changes to express individuality.

▲ Left: Space+ NIO ET5T color-change wrap case "Tea Birch"; Right: MX2 Tesla color-change wrap case "Silver-to-Green Gradient." Image sources: Space+ Xiaohongshu, MX2 WeChat Mini Program

Second, environmental regulations restrict NEVs to water-based paints. Compared with oil-based paints, water-based paints are less wear-resistant, more prone to chipping, and deliver inferior gloss — making PPF protection more necessary.

*Note: PPF and color-change wraps are not the same product. PPF is primarily transparent, made from TPU material, and provides significant protection against paint scratches and chips, priced between RMB 8,000–20,000. Color-change wraps use PVC material to alter vehicle color but offer no paint protection, priced under RMB 10,000. Historically, combining paint protection with color change was difficult because TPU dyeing processes were technically challenging and prohibitively expensive.

Beyond significantly higher PPF adoption on NEVs, rapid price declines lowering the consumption barrier have also been a key driver of market expansion. So why have PPF prices, once routinely exceeding RMB 20,000, fallen so quickly in recent years?

Historically, China's PPF market was dominated by four international brands: 3M, LLumar, V-KOOL, and XPEL. Their products were manufactured overseas, then distributed through national, provincial, and city-level agents before reaching stores — a markup of roughly 5x or more.

In 2018, Chinese companies Nalinwei and Kaiyang New Materials achieved domestic substitution of the TPU cast film process. Currently, fewer than five factories worldwide can produce high-quality TPU base film, with Nalinwei emerging as the leader, commanding 35–40% market share. The challenge of cast film lies in maintaining uniform thickness: when TPU pellets are melted and extruded through a die, pressure inconsistency within the die makes it difficult to achieve highly uniform base film thickness.

Further upstream, Chinese chemical giant Wanhua Chemical has also achieved domestic substitution of HMDI and TPU pellets in recent years, now ranking among the world's leading producers of both materials. Breakthroughs in cast film processing and upstream raw materials have enabled full TPU PPF supply chain production within China, dramatically reducing factory costs.

Supply-side domestic substitution has in turn created possibilities for brand-level domestic substitution. For example, MoXiaoEr, a leading Chinese PPF and color-change wrap brand, has rapidly captured market share in recent years. On the channel front, MoXiaoEr has developed an integrated online-offline fulfillment system that breaks from traditional multi-tier distribution, improving fulfillment efficiency and diversifying customer acquisition channels.

05 How Are NEVs Changing Our Lifestyle?

Automotive Aftermarket Modification: Post-Sale Modification Demand for Power Upgrades Will Gradually Decline; Pre-Sale Modification Shifts from Vertical OEM Integration to Horizontal Consolidation

Automotive modification has long been a vital way for car enthusiasts to express personality and passion. What impact does the rise of NEVs have on this market? First, modification divides into post-sale and pre-sale modification. Post-sale modification refers to DIY upgrades after purchase, primarily in three directions:

- Power upgrades: ECU tuning, turbochargers, intake/exhaust systems, cooling systems, engine reinforcement, etc., to achieve stronger acceleration.

- Chassis tuning: Tire, wheel, brake, suspension, and sway bar upgrades to improve handling, maximum grip, and off-road capability.

- Aesthetics and stance: Interior/exterior styling, carbon fiber, air suspension, etc.

▲ Yiche collaborated with renowned Chinese automotive KOL "Liuliuge" to create the custom Hongqi H9 "Wencheng," showcased at the Osaka Auto Messe. Image source: Yiche.

For power upgrades, NEVs have effectively achieved "acceleration democratization" by disrupting traditional engine and transmission systems, so this demand category will gradually weaken as NEV penetration rises. For aesthetics and stance, as noted above, the relative homogeneity of NEVs combined with a younger consumer base will further stimulate development in this modification segment. For chassis tuning, as intelligent chassis systems proliferate and consumers demand higher ride quality, we'll see increasing innovation and domestic substitution — adaptive electronic dampers, for example, essentially install a "brain" in the chassis system, continuously monitoring road conditions, feeding back vehicle dynamics, and adjusting damper settings for damping and height.

Pre-sale modification refers to customized and personalized upgrades built on mass-production vehicles from OEMs, often released as limited editions. Traditional ICE modification centered on engines and transmissions as a vertically integrated system, with modification houses deeply bound to OEMs and relatively weak bargaining power. Typical pre-sale modification houses include Brabus (Mercedes-Benz), Alpina (BMW), and ABT (Audi).

New energy vehicle powertrains are largely homogeneous. Traditional ICE automakers were mostly engines of internal-combustion technology themselves; new energy OEMs behave more like product-definition companies. This creates room for horizontal integration in the new energy pre-sale modification market — modification houses could develop a unified design language and chassis tuning, then roll out customized products across different OEMs, building brands independent of any single manufacturer.

We've already seen players experimenting with this horizontal approach: Chaojing Auto (Cyber Tank) with its techwear and sci-fi makeovers of the Tank 300; Galaxy Roam doing retro conversions of the Wuling Hongguang MINI EV; and Songsan Motor, which uses BYD contract manufacturing to produce premium retro-styled vehicles like the Songsan Dolphin.

▲ Image sources: Chaojing Auto, Autohome

Shifts in energy infrastructure are expanding demand and capability for outdoor recreation, camping, and off-roading — while spawning waves of accessory innovation

Today, new energy batteries make outdoor camping far more convenient. Campers can opt for portable power stations, or simply tap into their vehicle's own battery. Take this year's Rox Motor launch: positioned as an "outdoor camping family vehicle," it features two external discharge ports with combined peak output of 4.4 kW, enough to simultaneously run an outdoor kitchen, entertainment systems, lighting, refrigerator, water heater, and more. Whether the "light outdoor / camping" brand positioning will succeed remains an open question, but there's no doubt that NEVs are catalyzing far more outdoor camping demand.

With the explosion of camping culture and NEV adoption in recent years, we're seeing rapid proliferation of accessories: Iceco-style in-car refrigerators, EcoFlow-style mobile power stations, in-car espresso machines, and integrated vehicle-tent systems.

▲ NIO ES7 with camping mode. Image source: NIO official website

Energy infrastructure shifts are also reshaping RV product design. Startups like Lightship and Oasis are exploring new energy RVs with distinctive characteristics:

First, new energy RVs carry substantial fuel and electric reserves — essentially a range-extension charging solution that alleviates range anxiety during outdoor recreation.

Second, they feature independent drivability. Traditional RVs place heavy burden on the towing vehicle, make reversing and parking genuinely painful, and demand considerable driving skill. New energy RVs connect to the tow vehicle's hitch and use control algorithms to match its speed, reducing the towing burden.

Finally, NEVs enable intelligent control of interior and exterior facilities. Traditional unpowered RVs rely on open windows in summer and space heaters in winter. New energy RVs let you adjust facilities via smartphone, while thermal management systems repurpose battery waste heat for hot water and underfloor heating.

▲ Concept rendering of a new energy RV. Image source: Oasis

For the off-road market, NEVs carry unique advantages that may seem counterintuitive. Isn't off-roading ICE territory? Why do we see so few electric vehicles tackling trails?

NEVs actually possess inherent off-road strengths:

First, their instantaneous torque is massive — a huge asset for getting unstuck.

Second, with batteries integrated into the chassis, torsional rigidity runs 3-4× higher than comparable ICE vehicles. This effectively prevents micro-deformations from extreme body positioning, reducing the rattles, looseness, vibrations, deformation, and safety degradation that accumulate over hard off-road use.

Third, four-motor distributed drive maximizes "four-wheel drive" capability. Unlike traditional ICE vehicles that rely on differential locks and driveshafts for power distribution and wheel locking, NEVs give each wheel its own independent drive system — cooperating yet non-interfering, maximizing traction recovery.

Fourth, adjustable wire-controlled chassis combined with road surface scanning and control algorithms enable real-time adaptive terrain response, automatically adjusting damper height and stiffness based on conditions — no more driver mode buttons.

▲ How intelligent dampers from ClearMotion work. Video source: ClearMotion

Fifth, eliminating the intake and exhaust system dramatically improves water fording capability.

In summary, as NEVs continue evolving, ever more product innovations will help people improve their lifestyles, express individuality, demonstrate their unique passion for vehicles, experience richer and more colorful lives, push limits, and explore the unknown.

06 Conclusion

Under the sweeping wave of rapid NEV development, the service ecosystem is undergoing massive transformation — incumbents face existential challenges even as innovators push boundaries.

In new vehicle sales, the trend is toward direct-operated experience centers plus multi-brand authorized dealerships replacing portions of the traditional 4S model. In used vehicles, standardized NEV condition assessment and more transparent pricing create new opportunities for internet platforms. For vehicle logistics, less-than-truckload shared transport demand is strengthening and digital capabilities matter more. Looking ahead, vehicle logistics may become more socialized and concentrated, potentially creating the conditions for an "SF Express of NEVs."

With the three-electric system replacing engines and transmissions, NEV maintenance and repair demand will drop substantially — fluid changes and engine repairs will disappear entirely. For parts distribution, as SKU counts and circulation layers精简, OEMs gain stronger control over parts flow while markup compression becomes possible across the chain.

NEV maintenance and repair terminal formats are evolving along several dimensions: brand-authorized replacing independent third-party; suburban mega-shops replacing street-corner garages; OEM-dispatched jobs replacing consumer direct acquisition; multi-brand collectives replacing single-brand 4S shops; sales-service separation replacing sales-service integration. Long-term, whether NEV maintenance remains authorization-dominated or shifts toward a socialized system depends primarily on: battery supply chain standardization and capacity surplus; NEV intelligence and vehicle integration levels; and brand concentration.

For battery recycling and repair, battery repair currently operates separate from vehicle repair. Long-term, the two may converge. Drawing analogy from mobile phones: as battery quality and performance improve, replacement may overtake repair as the dominant battery treatment method, creating new front-end recycling opportunities.

As NEV maintenance demand shrinks, car washing may gradually decouple from the maintenance ecosystem and face the challenge of profitable standalone operation — customer acquisition and operational efficiency. We're seeing innovative players pursue highly automated solutions. The NEV paint protection film and color-change wrap market holds massive growth potential: upstream supply chain technological breakthroughs enabling domestic substitution at the raw material and product levels; downstream brands innovating on product formats and improving sales-fulfillment systems to achieve domestic brand ascendancy.

Additionally, we're seeing NEVs enrich consumer demand for vehicle personalization and recreation. In the pre-sale modification market, horizontal integration is possible — breaking the traditional ICE pattern where modification houses were bound to single OEMs. The shift in vehicle energy infrastructure has dramatically expanded people's demand and capability for outdoor recreation, camping, and off-roading, catalizing waves of accessory innovation.

As an early-stage investment institution, we're actively tracking innovative players across the NEV value chain. If you're working to improve efficiency or service experience in manufacturing, distribution, or service; or developing supply chain innovations, accessories, intelligence solutions, or even whole-vehicle product innovations for NEVs — we'd love to hear from you.

Engagement Giveaway

What innovation opportunities do you see in vehicle sales and aftermarket services?

Share your thoughts in the comments. By 5:00 PM on November 13, the 5 most thoughtful commenters will receive Robert M. Pirsig's Zen and the Art of Motorcycle Maintenance.

One Chart to Understand China's Industrial Chain Shifts and Opportunities | Li Feng Column

What New Opportunities Did AI Bring to Gaming in 2023? | FreeS VC Dialogue

3D Printing at 40: How Far From Niche Tech to Mass Adoption? | FreeS Report 31

How Should We Approach Aging in the Future? | FreeS Report 29

After the ChatGPT Boom, Where Is AIGC Headed? | FreeS Report 28

Star the FreeS Fund WeChat official account for timely business insights delivered straight to you.