A Visual Guide to China's Industrial Chain Shifts and Opportunities | Li Feng Column

The 40-Year Metamorphosis of China's Industrial Chain

In an earlier article on globalized industrial chains, we noted that China's industrial chain and the industrial structure it represents have given the country an irreplaceable position in the global industrial chain.

In this piece, we want to break down that chain with you: reviewing the evolution of China's industrial structure from 1978 to 2020, and using that to explore the opportunities and challenges China's industrial chain faces amid change.

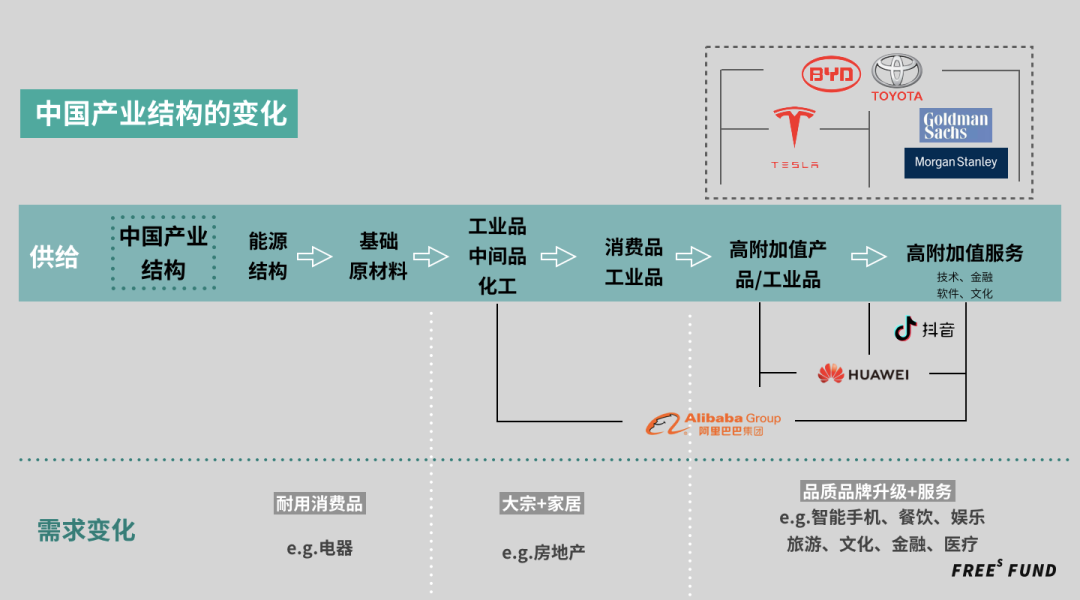

What does this chain look like? Look at the row labeled "China's Industrial Structure" in the chart below. We've drawn it as a horizontal axis: stretching from energy structure and basic raw materials, extending to industrial goods/intermediate goods/chemicals, then developing into consumer goods/industrial goods, and climbing all the way to high value-added products/industrial goods and high value-added services.

▲ One chart to understand the changes and opportunities in China's industrial chain. This chart will appear repeatedly throughout the article; each time we'll focus on different parts in detail.

Over the past 40-plus years, under different cycles and policies, China's industrial structure expanded and adjusted — sometimes proactively, sometimes reactively. The result: China has built an industrial chain that other countries can hardly match, one with three defining characteristics — it's big, long, and relatively complete.

Before diving in, here are a few conclusions to share:

- From 1978 to 2020, from the transformation of rural labor to developing foreign trade, joining the WTO, to the "Four Trillion" stimulus and new infrastructure, the expansion and adjustment of China's industrial structure has been a process of continuously climbing the value-added ladder.

- In this value-climbing process, the US model has been more like: climb, then offload the lower-value links to others — to the point where America's domestic industrial base is now concentrated almost entirely in the last two links of that industrial structure axis: high value-added products/industrial goods and high value-added services. China, by contrast, has managed to preserve the entire axis relatively intact while continuously climbing upward.

- Alibaba, Huawei, and Douyin represent both the typical changes in China's industrial structure and the direction of its future adjustment.

- In both the willingness and form of exports and imports, China is working to raise industrial value-added. However, there's still a long road ahead for China's industrial value-added rate to reach the levels of countries like the US and Japan.

We hope this offers a fresh perspective. Feel free to share your thoughts with us at the end.

/ 01 /

1978–2020: The Expansion and Adjustment of China's Industrial Structure

1. How did our manufacturing sector develop?

**▲ Source: "China's Industrial Landscape: Li Feng's Hypothesis" course, first released on Dedao app. Click "Read Original" for the full course. From 00:00 to 09:50, Li Feng discusses how China's industrial chain experienced labor migration and industrial upgrading over 40-plus years.

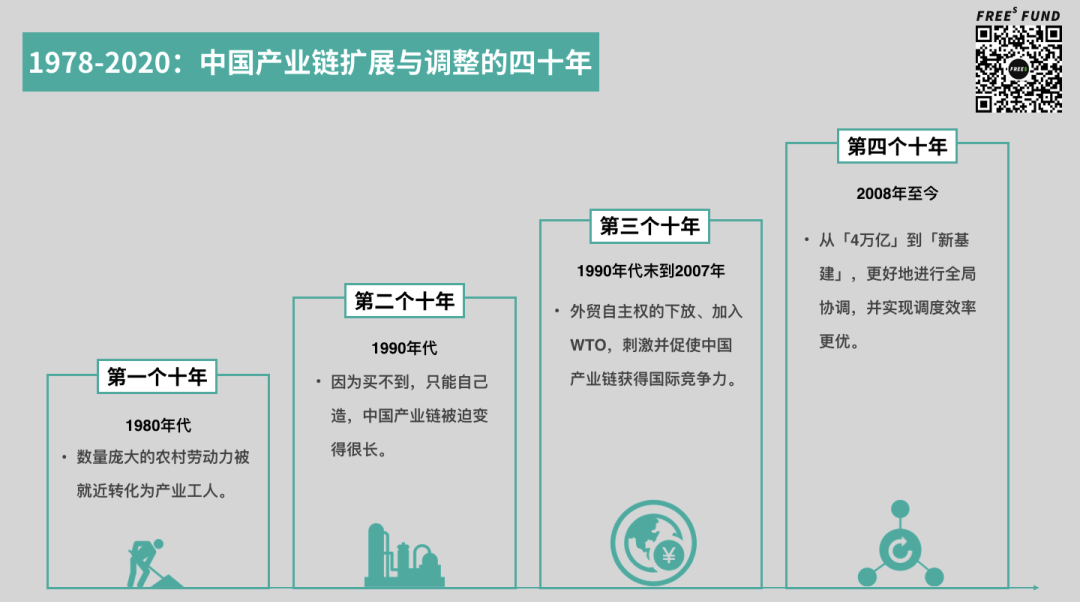

▍The first decade, the 1980s: Massive rural labor was converted to industrial workers locally

The new land policies launched in 1978, including the "household responsibility system," solved the age-old problem of putting food on the table — but created a new one. How to absorb the vast numbers of idle rural laborers now set free? Township and village enterprises (TVEs), operating in a gray area and following the proximity principle, were the first to absorb this productive capacity.

It's fair to say that the decade from the early 1980s to the early 1990s, with the massive development of TVEs, saw large numbers of rural workers flow out and become manufacturing workers. This provided manufacturing with the vast, trained, and cheap labor supply it needed to take off.

According to the China Township and Village Enterprise Yearbook, TVEs' value-added economic output accounted for less than 2% of national GDP in 1978. By 1995, this figure had climbed to 25.3%, with TVE industrial value-added accounting for 30.8% of national industrial value-added.

▍The 1990s: Because we couldn't buy it, we had to build it ourselves — China's industrial chain was forced to become very long

In the late 1980s and early 1990s, China faced severe international sanctions. Western governments in North America and Europe announced sanctions one after another, and an anti-China wave swept the world. China's international situation was far more difficult than it is today.

We could barely buy from abroad, and we could barely sell abroad — so we had no choice but self-sufficiency. To stimulate the national economy, a series of policies were rapidly introduced: persist in reform and opening up, affirm the development of special economic zones, encourage a spirit of "daring to try and risk," and continue attracting foreign investment. Under the pressure of survival, China was forced to develop a remarkably long industrial chain during that decade.

▍The third decade: Two landmark events stimulated and pushed China's industrial chain to gain international competitiveness

These two events were the decentralization of foreign trade autonomy in the late 1990s, and China's accession to the WTO in the early 2000s.

In early 1999, to fend off the sustained impact of the Asian financial crisis on Chinese industry and amid accelerating WTO accession negotiations, China deepened reforms to its foreign trade and economic system. These included: "relaxing approval standards for all types of enterprises and simplifying approval procedures"; and "breaking the 'lifetime' system for export quota allocation, implementing dynamic management, and tilting toward enterprises with good export performance, high product value-added, and strong economic capacity." This meant all of China's manufacturing enterprises could engage in foreign trade autonomously.

In 2001, China formally joined the WTO. This needs no further elaboration.

We can understand the significance of these two events this way. Over the past two decades or so, we experienced a transfer of labor and development of basic education, and extended our industrial chain. Then, spurred by the above policies, this long chain would further expand and be tempered under the pressure of international competition. In other words, to sell what you made — and especially to earn foreign exchange — you needed to satisfy the world's more demanding consumers, which forced you to make better products.

▍The fourth decade: From the 4 trillion stimulus starting in 2008, to new infrastructure in the spring of 2020

We've barely entered the second decade of the 21st century, and already witnessed the rise of "new infrastructure" as a buzzword.

In the first quarter of this year, multiple high-level meetings — including State Council executive meetings and the 12th meeting of the Central Committee for Comprehensively Deepening Reform — began frequently mentioning the need to "accelerate the progress of new infrastructure construction such as 5G networks and data centers." New infrastructure mainly covers seven areas: 5G base stations, ultra-high voltage power transmission, intercity high-speed rail and urban rail transit, new energy vehicle charging stations, big data centers, artificial intelligence, and industrial internet — involving numerous industrial chains.

This led many to recall the ten measures introduced by the Chinese government to expand domestic demand and promote stable economic growth, in response to the global financial crisis that swept from the US in September 2008 — commonly known as the "Four Trillion Stimulus Plan." This plan was controversial, but left us valuable infrastructure assets like high-speed rail and subways, greatly improving the circulation efficiency of China's industrial chain.

In our view, "new infrastructure" will act upon the long industrial chain China has built over the past 40 years, fully utilizing the circulation efficiency we've built over the past decade, to better achieve overall coordination and optimal dispatch efficiency. (We'll discuss new infrastructure in detail in the next article — consider this a preview.)

2. After 40 years of development, what does our manufacturing sector look like now?

The result of over four decades of effort is that China has formed the largest, longest, and most complete industrial chain — and in many segments and links along this chain, China has become number one in the world.

Overall, in 2018 global manufacturing value-added was $14 trillion, of which China's manufacturing output was $4 trillion, accounting for roughly 30% of global manufacturing value — far exceeding the US, Japan, Germany, and South Korea, which ranked second through fifth.

Take energy. Starting in 2017, China surpassed the US to become the world's largest crude oil importer. According to data released by the General Administration of Customs in January 2020, China's total crude oil imports in 2019 increased 9.5% year-on-year to 506 million tons. Aside from civilian use, this crude oil is mainly for chemical and industrial purposes. Take liquefied petroleum gas: its industrial applications involve glass, ceramics, metals, textiles, plastics, and other industries.

The same goes for basic raw materials like steel. Since China's steel output broke through 100 million tons at the end of 1996, it has maintained the top global position for 23 consecutive years. According to preliminary statistics from the World Steel Association, China's crude steel output in 2019 was 996.3 million tons, accounting for 53.3% of global crude steel output. Ranking second through fourth were India, Japan, and the US, with crude steel outputs of 111.2 million tons, 99.3 million tons, and 87.9 million tons respectively. Steel products cover a wide range, from household refrigerators and washing machines, to automobiles, railways, bridges, and ships in transportation, to transmission towers, residences, and factories...

In chemicals, citing a Xinhua report from September 2019, China's chemical industry capacity accounts for 40% of global capacity; by 2030 this ratio will approach 50%.

In industrial goods and intermediate goods, China currently has 41 industrial categories, 207 industrial subcategories, and 666 industrial sub-subcategories, forming an independent and complete modern industrial system — the only country in the world to possess all industrial categories in the UN's industrial classification. Among over 500 major industrial products worldwide, China ranks first in global output for more than 220.

In consumer goods, even taking high value-added products/industrial goods like smartphones as an example, China already has brands like Huawei that represent the highest global technical level in consumer electronics. And China's global competitiveness in smartphone manufacturing is also gradually rising. Industrial Securities data shows that from a CKD (complete knock-down) perspective, roughly 75% of global smartphone production capacity is in China.

The highest end of the value chain is high-value-added services — technology, finance, software, culture, and the like. These are areas where the gap between China and developed countries like the US remains significant. But China is making progress. Huawei is again a good example: it not only provides high-tech industrial goods (consumer products), but also encompasses high-value-added services — technology, software, design capabilities, and more. Of course, Huawei is not the only representative company.

▲ The result of more than four decades of effort: China has built the largest, longest, and relatively most complete industrial chain.

To summarize what we've seen:

- From the emergence of township and village enterprises in 1978 to the present, China's industrial structural expansion and adjustment has been a process of deep accumulation and steadily rising value-added: starting from energy and basic raw materials, moving to industrial intermediates and chemicals, then up to consumer and industrial goods, then high-value-added products and industrial goods, and more recently to the vigorous development of services with the highest value-added — entertainment, finance, and software.

- While "getting bigger," our industrial structure has also been "gaining value": beyond taking on increasingly sophisticated precision manufacturing, Chinese manufacturing has layered on more and more technology, software, and other services on top of high-value-added processing.

It should be noted that China's industrial evolution differs from America's.

The US model is more like climbing the value chain and then "offloading" the lower-value links to others. Today, America's domestic industrial base is concentrated almost entirely in the final two links of the structural axis described above: high-value-added products/industrial goods and high-value-added services.

China, by contrast, has relatively completely preserved the entire axis throughout its climb. The reasons likely include three factors: first, China climbed too fast; second, China's massive population; and third, overall planning has played a role.

This long and relatively large axis points to our supply capacity. And another major Chinese advantage is that this supply axis aligns precisely with another axis: the axis of consumption stage changes.

3. The Alignment Between China's Industrial Chain Upgrading and Consumption Upgrading Stages

▲ The three stages of consumer demand change and the development stages of China's industrial chain — that is, the development of supply and demand — are broadly in sync.

In 2003, an article by Yan Xianpu of the National Bureau of Statistics' Trade and Economic Department, published on China Statistical Information Network, argued that with rapid income growth, Chinese residents' consumption capacity was also upgrading. Yan believed that from pre-1978 reform to the early 21st century, Chinese residents' consumption upgrading had gradually shifted from traditional basic living consumption toward development-oriented and enjoyment-oriented consumption, passing through three main periods:

— The primary stage focused on basic living consumption. The main pursuit was the "three rotations and one sound" — the "old four items": bicycles, sewing machines, watches, and radios. (Pre-1978)

— The appliance popularization stage of greatly improved living standards. Beginning in the 1980s, the durable consumer goods boom represented by household appliances lasted roughly a decade. Its main markers were the wave-like popularization of home appliances in cities, and household appliances beginning to enter rural families.

— The high-level enjoyment-oriented stage. After appliance popularization, a new consumption boom centered on housing and automobiles surged forth with unexpected momentum.

Following Yan Xianpu's three-stage framework, China entered an overall consumer goods branding process around 2012–2013, manifested as better quality and broader scope.

A survey report on China's consumer goods market released in early 2013 by the China Industry and Enterprise Information Publishing Center showed that in 2012, China's famous and quality brand enterprises, leveraging superior product quality and relatively complete after-sales service, further increased their market share. The top ten brands by sales volume held an average market share of 68.66%, up 1.39 percentage points from the previous year. By category, home appliances maintained the highest market concentration, followed by daily chemical and daily use products, food products, culture and office supplies, and clothing and footwear.

And as residents' consumption levels rose (in 2010, China's per capita household consumption first exceeded 10,000 yuan), consumers not only began pursuing quality and brand upgrades more intensely, service consumption demand also rose rapidly. In 2012, the tertiary industry's share of China's economy reached 45.5%, surpassing the secondary industry for the first time to become the largest sector of the national economy. Catering, entertainment, tourism and culture, finance, healthcare, and other services also entered a period of rapid development.

Overall, from the 1980s to the present, China's consumption stage changes have roughly followed this pattern:

- The first stage was the popularization of durable consumer goods represented by appliances.

- The second stage focused on bulk commodities plus home consumption, with real estate as the typical representative.

- The third stage is quality and brand upgrading plus services, manifested in smartphone popularization and the rapid development of catering, entertainment, finance, and other service industries.

The three stages of consumption development and the development stages of China's industrial chain — that is, supply and demand development — are broadly in sync.

Another data point reflecting residents' consumption level is total retail sales of consumer goods. National Bureau of Statistics data shows that in 2019, China's total retail sales of consumer goods first exceeded 40 trillion yuan, growing 8.0% nominally year-on-year (6.0% in real terms after adjusting for price factors). According to US Census Bureau data, US total retail sales of consumer goods in 2019 were $6,237.557 billion, up 3.6% year-on-year.

Using the 2019 RMB-USD average exchange rate published by the State Administration of Foreign Exchange (6.8985:1), China's total retail sales of consumer goods last year were $270.332 billion less than the US. Compared with the previous two years, the gap in consumption scale between China and the US further narrowed. If the pandemic's impact on US retail persisted longer and more intensely, China could very likely become the world's largest single consumer market in 2020.

In summary, we can see that the process of forming China's "largest, longest, and relatively most complete" industrial chain development also accompanied China's gradual growth into the world's largest and most layered single consumer market.

The mutual strengthening of market consumption capacity and supply capacity has been an important reason why China's industrial development speed has surpassed other countries over the past forty-plus years.

02

Viewing China's Industrial Chain Structural Changes

From the Perspectives of Imports and Exports

1. Export Cases: Alibaba, Huawei, Douyin

▲ Source: "China's Industrial Landscape: Li Feng's Conjecture" course, first released on Dedao APP. Click "Read Original" for the full course. From 00:00 to 10:42, Li Feng discusses how China's industrial chain advances toward high-value-added products and services.

As discussed above, China's industrial chain structure has undergone significant changes over the past four decades: no longer limited to low-end processing, but gradually moving toward high-end industries. Typical characteristics include long industrial chains, high chain completeness, and steadily rising industrial value-added.

This has also meant China's role in international trade is advancing from general goods trade to service trade. General goods trade is the inevitable result of production and manufacturing; service trade involves exporting finance, technology and patents, consulting, software, and other products. Simply put, internationally, companies like Apple and Tesla lean toward goods trade, while Facebook, Google, and Qualcomm belong to the latter category — selling technology and services globally.

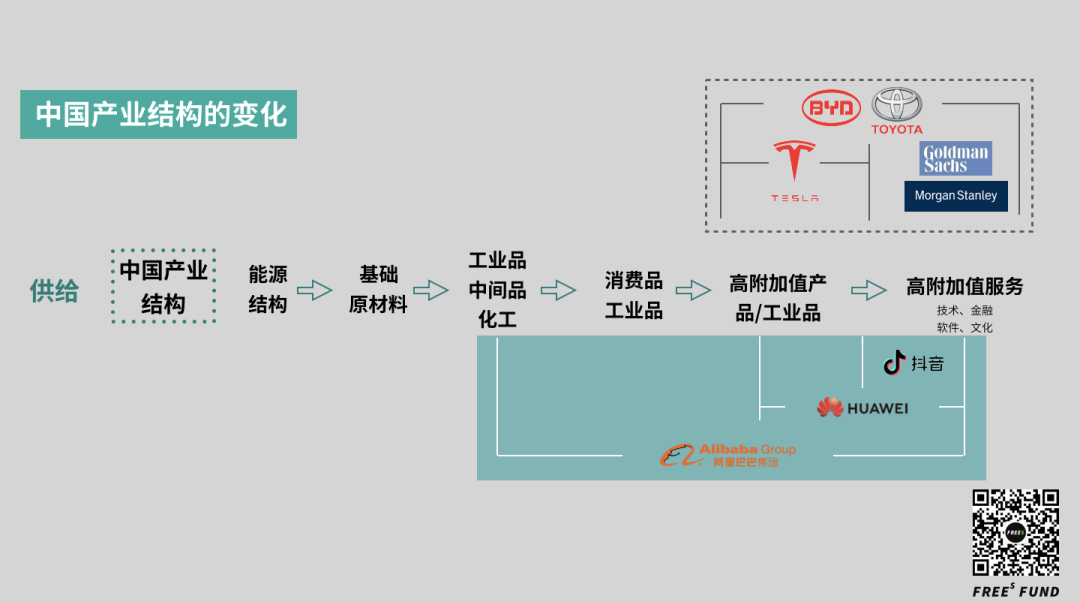

In China, Alibaba, Huawei, and Douyin represent both the typical changes in China's industrial structure and the direction of its industrial structural adjustment.

▲ From the development of Alibaba, Huawei, and Douyin, we can see our industrial chain increasingly moving toward high-value-added directions.

Alibaba has played nearly the full field, spanning the entire cycle. Early Alibaba (1688.com) provided raw materials, production, and processing services, representing China's chemicals, industrial goods, and intermediates; later, Taobao and Tmall represented general goods trade; in recent years, Ant Group, Alibaba Cloud, and Pingtouge (T-Head) chip company have represented financial services, cloud services, and chip technology services respectively. On this horizontal axis, Huawei's current position is half high-value-added manufacturing and half service trade. The former is Huawei's electronic products sales; the latter is Huawei's self-developed chips, 5G and other technologies and software, patents and services, and so on.

With Douyin, it's entirely service trade. Like the internationalization of Facebook, Google, Disney, and Netflix, Douyin sells 100% non-physical goods globally. Douyin has become like Facebook, exporting cultural entertainment and running advertising-related businesses. This belongs to knowledge-intensive, high-value-added products.

From the development of Alibaba, Huawei, and Douyin, we can see our industrial chain increasingly moving toward high-value-added directions. Among these, services are the typical representatives of high value-added. Like the GDP share of China's primary, secondary, and tertiary industries, we are also increasing the share of the tertiary industry (goods and services).

However, the sanctions Huawei has faced from the US, and the internationalization challenges Douyin has begun to experience, both reflect a problem: in China's trade structure, we are also increasing the external output of high-value-added portions; but for China's continuously optimizing industrial chain structure to gain global recognition, this will not happen overnight.

In other words, the world readily accepts a Chinese company like Alibaba representing Chinese manufacturing and trade, because this is an established Chinese advantage. Yet it still struggles to accept a consumer brand representing top-tier technology coming from China, like Apple, or a globally popular company like Facebook also coming from China.

2. Foreign Investment Attraction Cases: Tesla, Goldman Sachs, Morgan Stanley

▲ We must not only bring in high-value-added terminal product manufacturing like Tesla and Toyota, but also drive the related high-value-added industrial chains.

China's industrial structure optimization and adjustment is also reflected in imports, mainly manifested as attracting investment and capital. From bringing in Tesla to recent financial opening policies, we can see that we are actively working toward a goal: vigorously developing the final two links of the industrial chain — high-value-added products/industrial goods and high-value-added services.

Take foreign direct investment in the automotive sector, for example. In previous years, we attracted parts and component processing and supporting industries, becoming the world's largest automobile manufacturer. Now, we are working to attract higher value-added automotive processing industries — such as the Tesla Gigafactory, the largest foreign-invested manufacturing project in Shanghai's history.

This is Tesla's first overseas factory and China's first fully foreign-owned automobile plant. Song Gang, Manufacturing Director at Tesla Shanghai, stated in early 2020 that the localization rate of parts for China-made Model 3s was then 30%, and was expected to reach 70% by mid-year and 100% by year-end — meaning complete vehicle localization.

As we discussed earlier, companies like Tesla, like Huawei, carry both high value-added consumer products and high value-added services — specifically software services including intelligent driving. The significance of complete vehicle localization is that we are not only introducing the manufacturing of these high value-added end products, but also driving the related high value-added industrial chains.

This is extremely important for optimizing China's industrial structure. Although we have a very long and robust industrial axis, measured by the industrial value-added rate, we still have distance to cover in moving from an industrial giant to an industrial power. According to calculations by Li Yizhong, then Vice Chairman of the Economic Committee of the CPPCC National Committee, in 2015, China's average industrial value-added rate during the 11th Five-Year Plan period was 25.6%; around 2015 it had actually declined to below 23%, while developed countries maintained industrial value-added rates of 35% to 40%.

This indicator reflects input-output efficiency. The higher the value, the greater the enterprise's value-added and profitability, and the better the input-output results. If we want to maintain both the length of the industrial chain and maximum industrial output, while ensuring that enterprises and workers in the chain see rising incomes and profits, we need to raise the industrial value-added rate. This is why we are actively bringing in companies like Tesla.

Thinking Exercise

Q: Take the same piece of land — used for processing industrial intermediate goods versus used for producing Teslas. What difference would that make? Feel free to hit "Like" at the end of this article, and reply with the keyword "Tesla" in the WeChat official account backend to see our preliminary answer.

In terms of attracting capital, we have been continuously expanding financial opening, with the pace of opening not slowing even under the pandemic.

On April 1, 2020, China announced it would formally remove foreign ownership caps on securities firms and publicly offered fund management companies. That same day, Goldman Sachs and Morgan Stanley both stated they would increase their equity stakes in their China joint ventures to 51% to achieve controlling interest. Adding to Nomura Orient International, which opened in November 2019, and JPMorgan Securities (China), which opened most recently on March 20, as well as UBS Securities, which achieved control back in 2018, there are now five foreign-controlled joint venture securities firms in China.

On May 11, 2020, news emerged that Shanghai International Trust Co. would transfer its 49% stake in China International Fund Management (J.P. Morgan). If the transaction completes, China's first wholly foreign-owned public fund management company will be born.

Another recent policy was also designed to encourage and further facilitate foreign capital participation in China's financial markets. On May 7, 2020, the People's Bank of China and the State Administration of Foreign Exchange issued the Administrative Measures for Funds of Overseas Institutional Investors for Domestic Securities and Futures Investment, removing quota restrictions for overseas institutional investors and simplifying fund management requirements.

To summarize: China's manufacturing already holds a leading global position; along with changes in industrial structure, the value-added, length, and completeness of China's industrial chains are all increasing, and in both the willingness and form of exports and imports, China is working to upgrade industrial value-added.

03

Next, can we successfully move from industrial giant to industrial power?

1. Take the autonomous driving industry as an example — China has the best soil for industry development

▲ Source: China's Industrial Landscape: Li Feng's Conjecture course, first released on Dedao APP. Click "Read Original" for the full course. From 00:00 to 03:34, Li Feng discusses industrial internet and the landing of autonomous driving technology.

In recent years, "industrial internet" has been mentioned with increasing frequency. If we say that since the internet began developing in the 1970s and 1980s, internet companies have primarily solved problems of information transmission efficiency and methods (Google, Facebook and other giants being no exception), then starting around 2010, more and more entrepreneurs began doing something else — combining technology with manufacturing, truly embedding technology into the physical world. This is what we call industrial internet.

Take autonomous driving, widely acknowledged as the most challenging field in artificial intelligence.

You probably still remember that about five years ago, autonomous driving was one of the hottest areas for VC investment. What's the biggest change five years later? Everyone realized that technology matters, but what matters more is that technology must land on large numbers of vehicles in daily operation.

In other words, good lab results alone are useless. You must jointly develop with OEMs, have users willing to buy, willing to drive after buying, and continuously provide feedback during driving. Based on user needs and data, you can constantly iterate autonomous driving technology, gaining continuous real-world experience.

So simply put, for autonomous driving to work, three conditions must be met: enough people making cars; enough people riding in cars; and based on the first two, continuous technological iteration and updating.

This leads us to a question — where is the ideal soil for developing autonomous driving?

China is certainly highly competitive.

Looking globally, China has the most complete automobile manufacturing capability and the world's largest car-buying population. Take new energy vehicles as an example: since 2015, China has ranked first globally in NEV production and sales for four consecutive years, with annual NEV production, sales, and stock each accounting for over 50% of the global market.

Beyond talent reserves and technological development, having the most complete supply chain and largest market in the same geographic region also shortens the cycle of market feedback and technological iteration. This was a major reason why new energy vehicles could rise abruptly in China from 2015 to 2019.

If industrial chain + market + continuous technological iteration = the ideal environment for autonomous driving development, then other countries will find it relatively difficult to assemble all three simultaneously.

Therefore, we are inclined to believe that China has fertile soil for developing high technology, and this is an important opportunity for China to move from industrial giant to industrial power. However, as we mentioned earlier, measured by industrial value-added rate, we still have clear gaps compared with developed countries like the US and Japan. We must be clear-eyed about this.

Summary

1 From 1978 to 2020, the expansion and adjustment of China's industrial structure has been a process of continuously increasing value-added. While "getting bigger," our industrial structure has also been "adding value": beyond taking on increasingly difficult precision processing, Chinese manufacturing has been adding more and more technology, software, and other services on top of high value-added processing. Meanwhile, in both the willingness and form of exports and imports, China is working to upgrade industrial value-added.

2 The mutual growth of market consumption capacity and supply capacity has been an important reason why China's industrial development speed has surpassed other countries over the past forty-plus years.

3 In the process of climbing the industrial chain value ladder, the US model more resembles climbing up and then "passing off" the lower-value portions to others, such that US domestic industry is now almost concentrated in the final two links of the industrial structure axis described above — high value-added products/industrial goods and high value-added services. China, in the process of continuous ascent, has relatively completely preserved the entire axis.

Thinking Exercise

Q: Take the same piece of land — used for processing industrial intermediate goods versus used for producing Teslas. What difference would that make? Feel free to hit "Like" at the end of this article, and reply with the keyword "Tesla" in the WeChat official account backend to see our preliminary answer.

(Welcome to read, share, and hit "Like." For reprint requests, please reply with "reprint" to learn reprint rules, and contact Frees Xiaorui [ID: freesfund] for authorization. Copyright belongs to FreeS Fund.)

Where Is the Endgame of E-commerce Livestreaming? | Frees Fund

What Exactly Did Minister Miao Wei Say About Chinese Manufacturing? | Frees Fund

One Chart to Understand Globalization or Deglobalization | Li Feng Column

Post-Pandemic, A New Era for "Good Companies" | Frees Fund