Four Decades of China's Healthcare System: A Journey from Past to Future | FreeS Fund Report

Finding Innovation Opportunities Behind Transformation

From newborn infants to the elderly, we interact with the healthcare system throughout our entire lives. This system comprises three components: pharmaceuticals, medical services, and health insurance. With supply and demand perpetually difficult to align, healthcare has become a challenge for nearly every nation.

On August 30, 2024, China's National Health Commission announced at a press conference that it would comprehensively promote the Sanming healthcare reform experience over the next five years. Shortly after, on September 8, three national ministries jointly issued the Notice on Expanding Open Pilot Programs in the Medical Sector, allowing foreign-invested enterprises in pilot cities to engage in human stem cell, genetic diagnosis, and gene therapy technology development and application, while also permitting wholly foreign-owned hospitals in these pilot cities.

For the medical services industry, the former policy seems to signal the broad implementation of "control," while the latter hints at a new experiment in "opening up." What do these concurrent tightening and loosening measures mean in the current context? What do they imply for the industry as a whole, and might they create new long-term opportunities?

In this article, we first examine healthcare systems across different countries to understand the factors shaping their institutional designs. We also review China's 40-plus years of healthcare reform, from which we can see the complexity of the healthcare system and reform efforts. Looking ahead, we explore potential directions for innovation in China's medical market. Our key observations:

- The healthcare system is a complex system of pharmaceuticals, medical services, and health insurance. It's difficult to say which country's system is superior; the establishment of health insurance systems appears to be an ongoing balancing act between equity and mutual aid, demand and supply.

- After more than 40 years of exploration, including an unsuccessful experiment with "market dominance," China's healthcare system has returned to macro-regulation as its primary approach. China's social medical insurance system and the social healthcare system it supports have been gradually established and are now maturing.

- The "Sanming model" has been largely established, though there remains room for long-term upgrades. Beyond basic health insurance, people have more diverse medical needs awaiting fulfillment.

- From a supply-demand perspective, building a multi-tiered medical service system is both necessary and promising. A relatively diversified market supported by commercial insurance may be beginning to take shape.

- In the long run, as national income levels rise, product and service providers in the medical industry may face questions of pricing and positioning — but the core issue remains whether their offerings are compelling enough for their target audiences.

We hope this provides fresh perspectives. If you're an entrepreneur, researcher, or practitioner in the healthcare industry, you're welcome to reach out to the author, Jieling Yang, at jieling.yang@freesvc.com.

Reader Giveaway

What potential upgrade needs do you see in the pharmaceutical and medical markets? Leave a comment below — we'll randomly select 5 readers to each receive a copy of Witnessing Major Reform Decisions: Oral Histories from Reform Insiders.

A Global Perspective: Healthcare Systems Across Countries

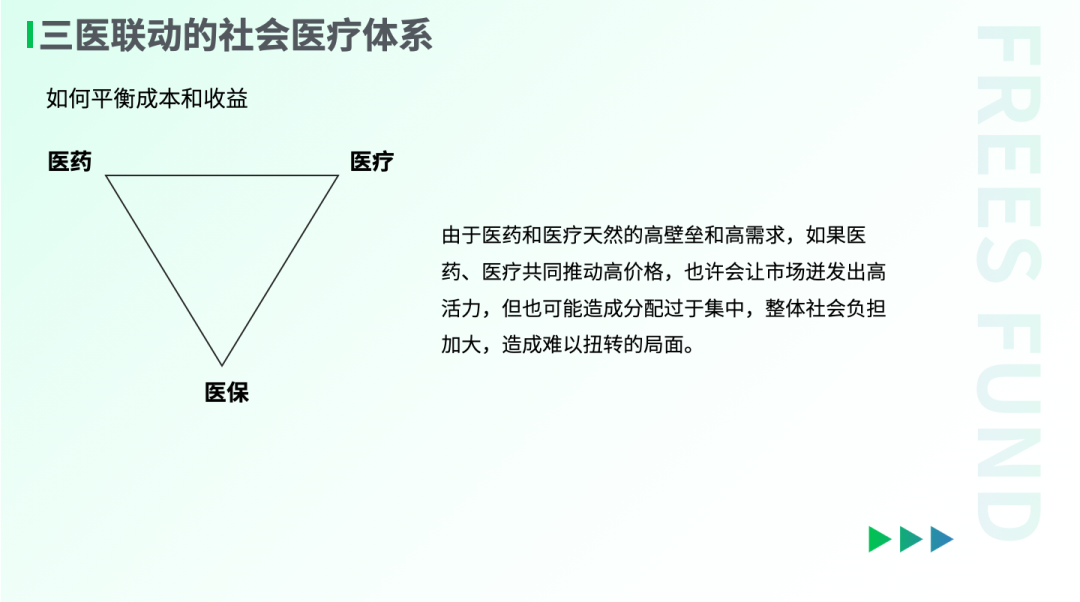

The healthcare system is a complex system of pharmaceuticals, medical services, and health insurance. In this "three-medical linkage" system of pharma-medical-insurance, pharmaceuticals and medical services represent the expenditure side, while health insurance serves as the payment side.

Healthcare systems are deeply intricate. From the supply side, they carry extremely high professional barriers; from the demand side, people naturally have strong needs for health. Under this inherent supply-demand mismatch, healthcare has become a challenge for nearly every country.

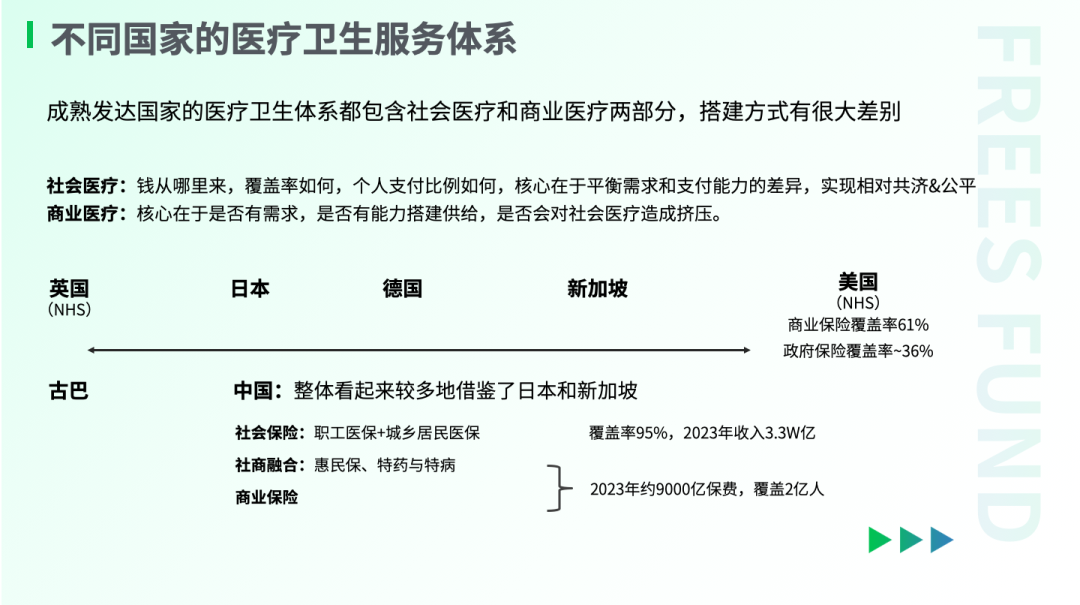

The key to solving healthcare problems lies in health insurance. Insurance typically comprises commercial medical insurance and social medical insurance. Social medical insurance must consider funding sources, coverage rates, and how to balance disparities between different groups. Commercial medical insurance generally offers greater flexibility. Different countries' insurance policies are often tied to their social realities. A nation's insurance revenue and expenditure methods, scale, composition, and policy guidance significantly influence the operational logic of pharmaceutical and medical markets. The establishment of insurance systems appears to be an ongoing balancing act between equity and mutual aid, demand and supply.

For instance, looking at funding sources for healthcare systems, the UK and Cuba have essentially adopted free healthcare systems relying on national fiscal revenue, while the US depends heavily on commercial insurance. Most other countries have found a relatively coherent point between the two approaches of "state as backstop" and "commercial insurance as primary."

Cuba: Universal Free Healthcare

Let's start with Cuba. Cuba has established a universal free healthcare system. Free healthcare essentially means the state equalizes medical resources through taxation or fiscal revenue. How has Cuba achieved free healthcare with a per capita GDP of only $2,000 (varying slightly by statistical methodology)?

In The Healthcare Systems of Cuba, Brazil, and Argentina: Mechanisms and Implications, scholars including Jingchun Zha note that Cuba trains large numbers of medical students. With a total population of about 11 million, Cuba has more than 8 doctors per 1,000 people according to Index Mundi data — the highest globally. Additionally, Cuba's domestic pharmaceutical industry (including both chemical drugs and herbal medicines) has been gradually developing.

With low population base and low per capita income, medical demand is limited, while the state continues increasing supply. This may be the primary reason Cuba's healthcare can achieve supply-demand balance at relatively limited cost.

Japan: Social Healthcare in a High-Per-Capita-GDP Country

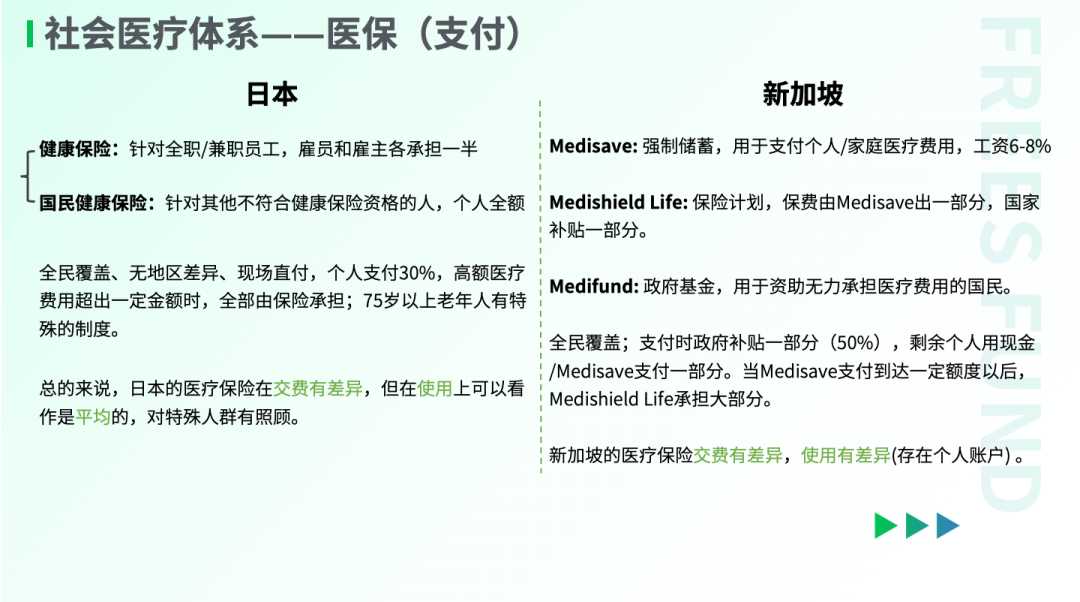

Japan found a position between Cuba and the US. Japan's health insurance demonstrates significant mutual aid characteristics, with social medical insurance meeting most people's needs and commercial insurance accounting for only 5% of payments.

Japan's social insurance accounts are divided into Employees' Health Insurance and National Health Insurance, covering corporate employees and those without income respectively. On the usage side, there's no difference between the two — both use direct on-site payment, with social insurance covering 70% and individuals paying 30%. When medical expenses exceed certain amounts, insurance covers everything. Additionally, there are certain benefits for special groups.

Japan's ability to establish this system is closely tied to its high per capita GDP, spindle-shaped income distribution, and relatively early government intervention.

Briefly, in building its healthcare system, Japan primarily pursued separation of prescribing and dispensing on the medical services side, and cost control on the pharmaceutical side.

According to records preserved in Japan's National Diet, as early as 1955 Japan proposed the separation of prescribing and dispensing (dividing prescription writing from drug preparation), but short-term results were limited. In 1974, Japan increased doctor prescription fees fivefold, and over the following 20 years continuously raised doctor consultation income, established drug preparation fees and prescription outflow fees, and prohibited medical institutions from operating off-site pharmacies. Under these measures, prescription outflow rates only began significantly increasing in the 1990s. By 2003, the national off-site prescription rate exceeded 50%, with major public hospitals required to reach 70%. Thanks to prescription outflow, Japan's offline pharmacies developed robustly.

For drug and device cost control, Japan set reimbursement standards for hospital insurance claims without limiting procurement prices — the difference was borne/earned by hospitals. Meanwhile, every two years (changed to annually after 2021), existing products' insurance reimbursement prices were revised and recalculated based on hospital procurement prices. In this system, hospitals themselves have strong incentives to reduce prices, though Japan's drug prices are still determined by market mechanisms.

US: Commercial Health Insurance Dominates

Contrasting with Cuba's approach is the US healthcare system. Overall, the US system relies on a relatively free market. According to US Census Bureau data, on the insurance side, over 60% of Americans depend on commercial insurance, while social insurance (Medicare and Medicaid) that truly provides mutual aid across income groups covers only about 30% of the population.

A fully marketized pricing system may provide ample incentives for medical institutions and promote innovative drug and device R&D. But in horizontal comparison, the US system also has corresponding problems, such as heavy social medical burdens and insufficient bottom-layer protection. Looking at common evaluation criteria like life expectancy, the US doesn't seem to receive returns commensurate with its high investment.

China: Social Health Insurance Is Currently the Primary Payer

In terms of reform measures and health insurance funding sources, China's healthcare system shares some similarities with Japan's. China is also pursuing separation of prescribing and dispensing on the medical services side and cost control on the pharmaceutical side, though there are considerable differences in specific rules.

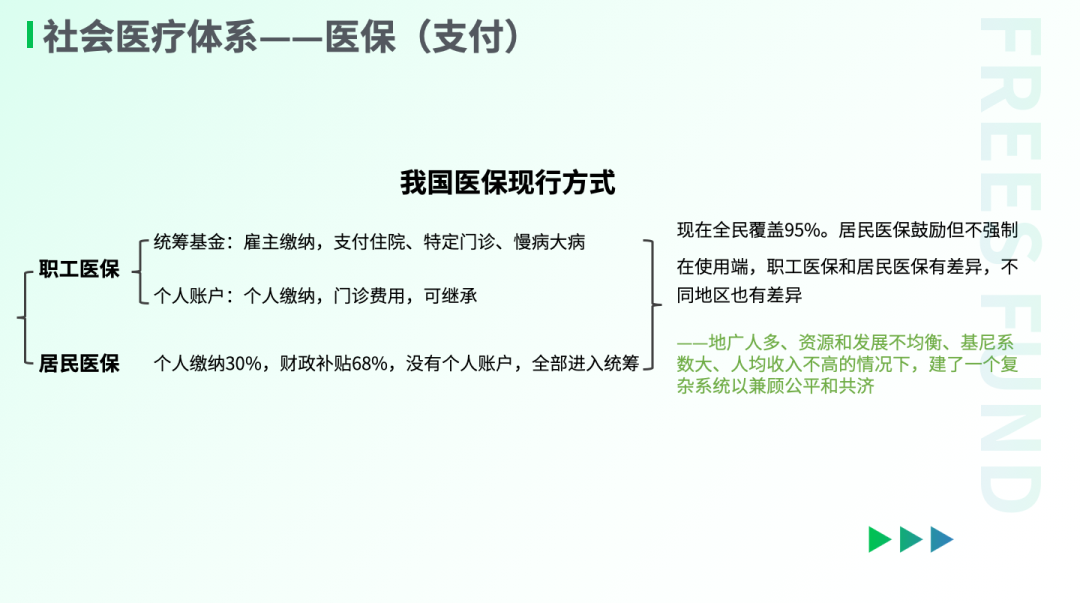

After multiple rounds of reform, China's current health insurance system mainly has two types of accounts: employee health insurance and urban-rural resident health insurance. These two accounts operate independently — the more individuals contribute, the more they can access when seeking care. While account funds cannot be directly withdrawn, medical insurance personal account balances can be inherited or shared within families.

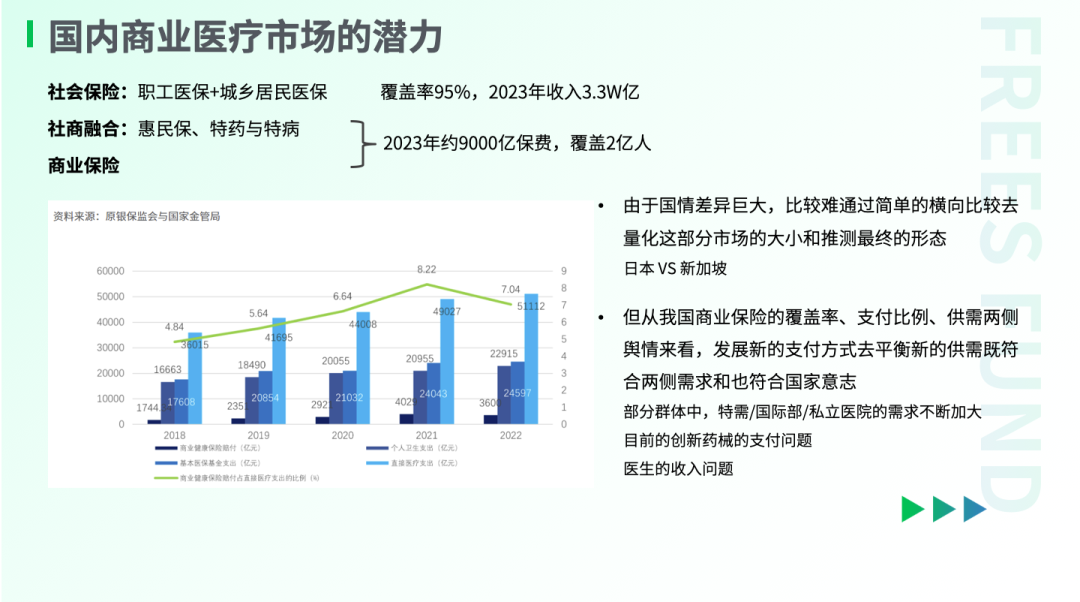

After years of development, social insurance has become the primary payer. According to National Healthcare Security Administration data, in 2022, China's social medical fund had total revenue of about 3 trillion RMB, covering 95% of the population, with expenditures of about 2.4 trillion. In comparison, commercial health insurance premium income that same year was 865.3 billion RMB, with claim payments of 360 billion — only 7% of direct healthcare expenditures.

How Does the WHO Measure National Healthcare System Quality?

The WHO primarily measures healthcare system quality across five dimensions: population health level, medical service quality, disease prevention and control indicators, accessibility, and medical costs and payment mechanisms — including specific metrics like average life expectancy, medical staff and hospital beds per 1,000 people, and neonatal mortality.

For instance, on the life expectancy indicator, World Bank statistics for 2022 show the UK at 82 years, the US at 77, Japan at 84, and China at 79. China's population life expectancy is already very close to that of high-income countries (80 years).

40 Years of Chinese Healthcare Reform

▎Payment Side: Increasing Mutual Aid and Coverage

Xiaowu Song, Chairman of the Academic Committee of the China Society of Economic Reform, participated in theoretical research and policy design related to labor system reform, pension insurance, unemployment insurance, and minimum living security reform. In Witnessing Major Reform Decisions: Oral Histories from Reform Insiders, he states directly: "Health insurance is truly a global challenge."

Looking back at the evolution of China's social health insurance system over the past 40-plus years, we can see that China's health insurance reform has been crossing the river by feeling the stones. Throughout this process, there have been numerous disputes, pilots, and corrections.

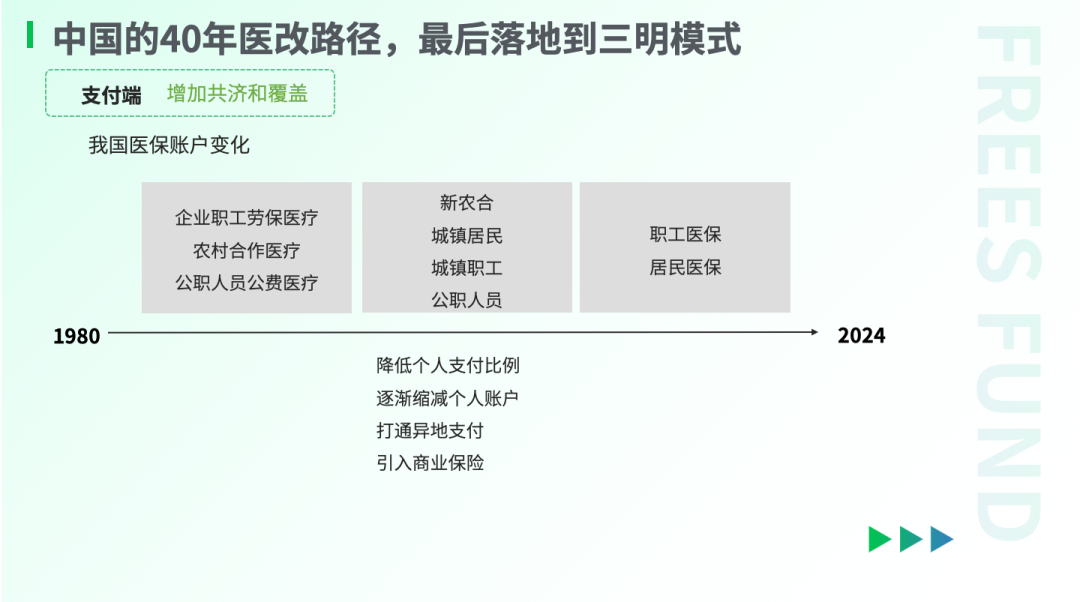

In terms of outcomes, China's healthcare reform ultimately developed from employer-burdened to socially mutual, with overall coverage continuously expanding and individual payment ratios steadily decreasing.

Before 1978, China's medical costs were mainly paid by employers, with relatively low individual burden but heavy collective burden. Health insurance then consisted of three types of accounts: enterprise employee labor-protection medical care, rural cooperative medical care, and public servant public-expense medical care. Rural healthcare mainly relied on the cooperative medical system, with most rural populations lacking coverage.

With the launch of reform and opening up in 1978, health insurance reform exploration also began. According to the China Commercial Medical Insurance Development Research Blue Book, health insurance reform can be broadly divided into two phases.

The first phase was the establishment of basic social security systems. Between 1980 and 2000, the rural cooperative medical system for agricultural populations and the social medical insurance system for urban employees were gradually established and took shape.

The second phase involved gradual evolution and improvement, forming a more comprehensive, inclusive, and high-coverage system.

Today, China's social health insurance has essentially achieved full coverage institutionally, with coverage exceeding 95% — a significant increase.

From the insurance account perspective, there were once three accounts: enterprise employee labor-protection medical care, rural cooperative medical care, and public servant public-expense medical care, with considerable disparities in benefits. Today, public servants' public-expense medical care ratio has been substantially reduced, and the accounts have become employee health insurance and resident health insurance, covering approximately 370 million and 963 million people respectively.

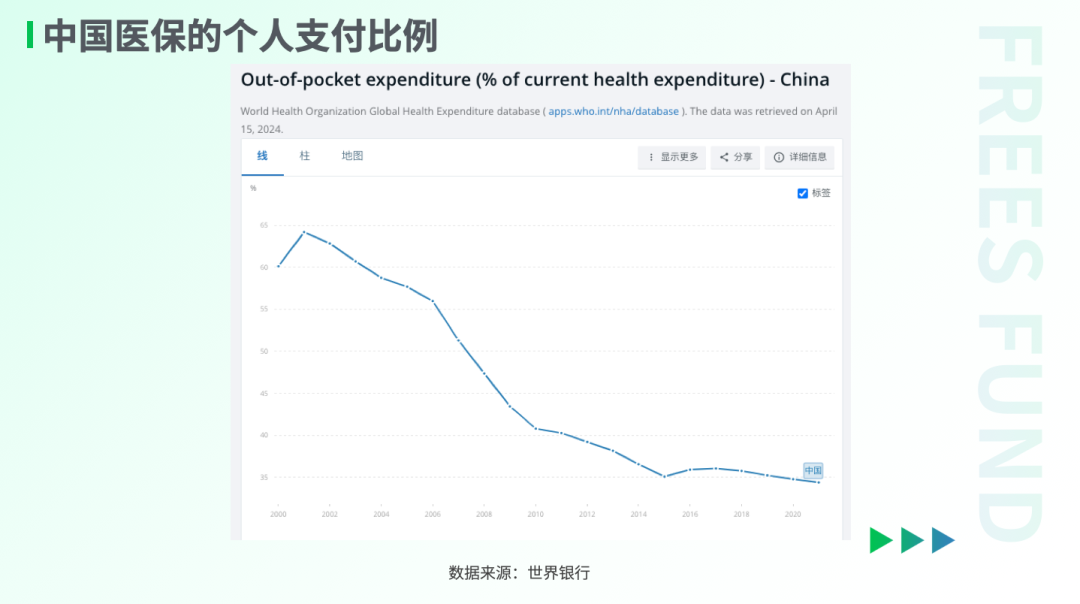

Additionally, according to World Bank data, from 2000 to 2021, China's individual payment ratio for health insurance decreased from 60.13% to 34.39%.

To summarize, on the social health insurance side, the general direction of China's healthcare reform is to expand coverage while considering equity, making it the most basic protection for most of society. The other side of the coin is that current health insurance cannot fully satisfy people's diverse medical needs.

Overall, China's 3 trillion RMB social health insurance volume is substantial, but dividing by approximately 1.33 billion insured people reveals relatively limited payment capacity. Disparities in per capita income determine differences in demand, with the inevitable result that under social health insurance payment methods, some groups feel heavy medical burdens while others have higher quality demands.

Using multi-tiered payment methods to meet various differentiated needs appears to be a clear direction. With social health insurance coverage reaching 95%, further developing commercial health insurance to meet more needs may become inevitable — we'll elaborate below.

▎Expenditure Side: From Marketization to Strengthened Regulation

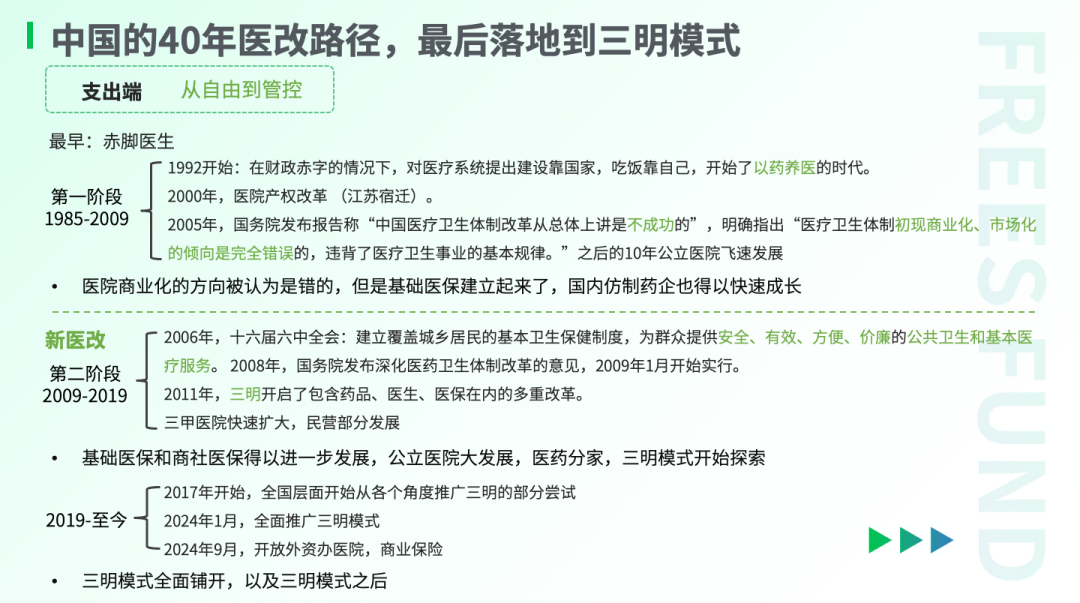

Broadly speaking, China's healthcare system reform can be divided into two phases, with 2005 as the watershed. The overall arc might be summarized as: after an unsuccessful attempt at "market dominance," China's healthcare system returned to macro-regulation as primary, with the Sanming model as its ultimate concrete manifestation.

In 1992, as China vigorously advanced reform and opening up, the government explicitly proposed that "the goal of China's economic system reform is to establish a socialist market economy." That same year, the State Council issued Several Opinions on Deepening Health and Medical System Reform, proposing "construction relies on the state, meals rely on oneself," with health department work conferences requiring hospitals to "support medical care with industry, supplement medical care with sideline businesses."

For the following decade-plus, the market entered the "drug-supported medical care" era, with medical costs increasing substantially, enterprises and public institutions overburdened, and fiscal burdens also heavy. Fiscal investment in public hospitals decreased, hospitals operated independently, and "drug markups" became the mainstream choice after marketization. Notably, many of China's first-generation leading pharmaceutical companies' transition from active pharmaceutical ingredients to generic drugs, with substantially expanded revenues, also occurred during this period.

Subsequently, problems from this direction gradually emerged. Drug and consumable companies and medical institutions jointly pursued maximizing health insurance fund expenditures, with public welfare greatly diminished. Major tertiary hospitals had unavailable appointments and long queues, and people fell into the predicament of "difficulty seeing doctors, expensive medical care."

Around 2000, Suqian in Jiangsu Province conducted property rights system reform on 134 public hospitals, including 124 township health centers and 10 county-level and above hospitals, forming partnership, mixed-ownership, shareholding, and sole proprietorship healthcare entities. This radical reform generated considerable controversy.

The 2003 SARS outbreak revealed difficulties in efficiently coordinating medical resources, and combined with the 2005 Harbin "sky-high drug price" scandal and other continuously exposed problems, doctor-patient conflicts intensified.

By 2005, the State Council Development Research Center and WHO jointly published the research report China's Health Care System Reform, explicitly stating that "China's health care system reform has generally been unsuccessful," and that "the commercialization and marketization tendencies in the health care system are completely wrong, violating the basic laws of health care."

Debates about the general direction of healthcare reform gradually deepened. Thus, returning to "providing safe, effective, convenient, and affordable public health and basic medical services for the masses" became the new direction for healthcare reform.

In September 2008, the State Council released the Opinions on Deepening Health Care System Reform (Draft for Comment). In January 2009, the new healthcare reform officially launched, with "public welfare of public medical and health services" and "government leadership" as the new overarching direction.

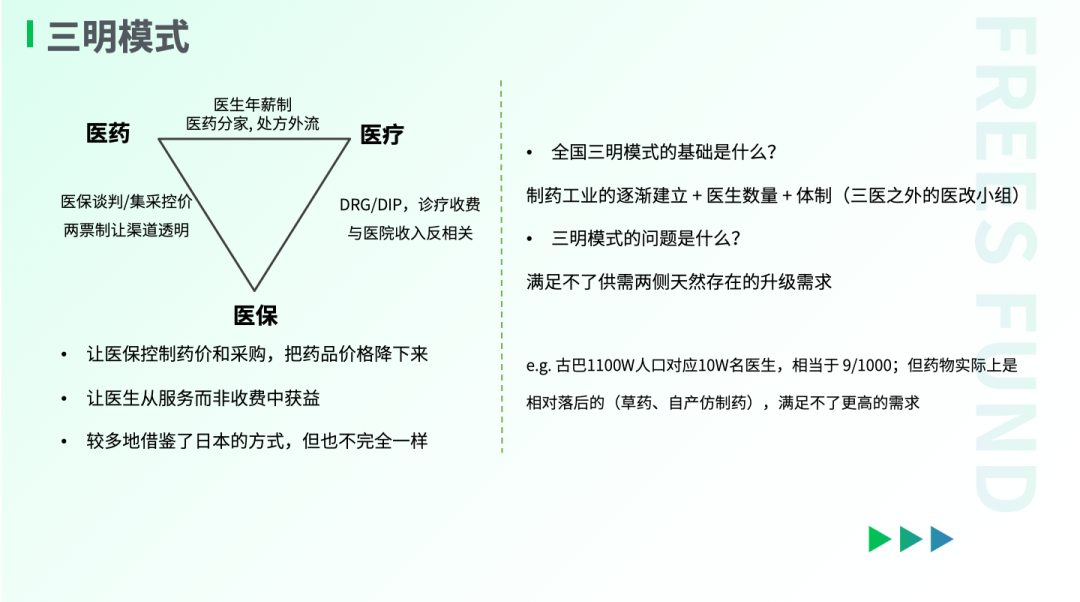

The Sanming healthcare reform, launched in 2011, was a bold attempt under this new direction.

Before the reform, Sanming's local health insurance had no surplus, and hospitals couldn't pay doctors' salaries. Zhan Jifu, then Vice Mayor of Sanming and head of the healthcare reform leading group, had previously served as Director of Sanming's Food and Drug Administration. According to Zhan's account: "In 2010, Sanming's employee health insurance pooling fund had a deficit of 143.97 million RMB, representing 11.66% of that year's municipal-level public fiscal revenue. The government couldn't cover the shortfall and owed 17.4864 million RMB in medical expenses to 22 public hospitals citywide."

From start to formation, Sanming's healthcare reform took nearly 10 years. It is a comprehensive package of measures. Sanming's approach: First, "separation of medicine and medical care," implementing zero drug markup and severing the connection between hospitals and drug costs. Second, "centralized procurement and price control," using health insurance to control drug prices and procurement, bringing drug prices down, while also adopting Diagnosis-Related Group (DRG) / Diagnosis-Intervention Packet (DIP) payment methods to improve health insurance fund efficiency. Third, "inverse correlation between consultation fees and hospital revenue," adjusting doctors' income models to annual salary systems, allowing doctors to benefit more from services. During leadership inspections, Sanming's reform received affirmation: "Sanming's healthcare reform embodies people-first principles and pioneering spirit; its experience is worth adapting by various regions according to local conditions."

Comparing China's exploration process with different countries' models, our understanding is that although it's difficult to evaluate which model is superior, two conclusions are relatively clear:

- If the needs of the vast majority are to be considered, pharmaceuticals and medical services are unlikely to become a completely free market — this is determined by their essential supply-demand mismatch.

- China's current situation may be that the basic medical service system has essentially taken shape; how to further evolve on this foundation to meet the development needs of both supply and demand sides may be the important proposition for the next stage.

The Future of China's Healthcare System

In August 2024, the National Health Commission announced at a press conference that it would guide other provinces to select 2-3 regions annually as priorities for promoting Sanming's experience, achieving full coverage within 5 years.

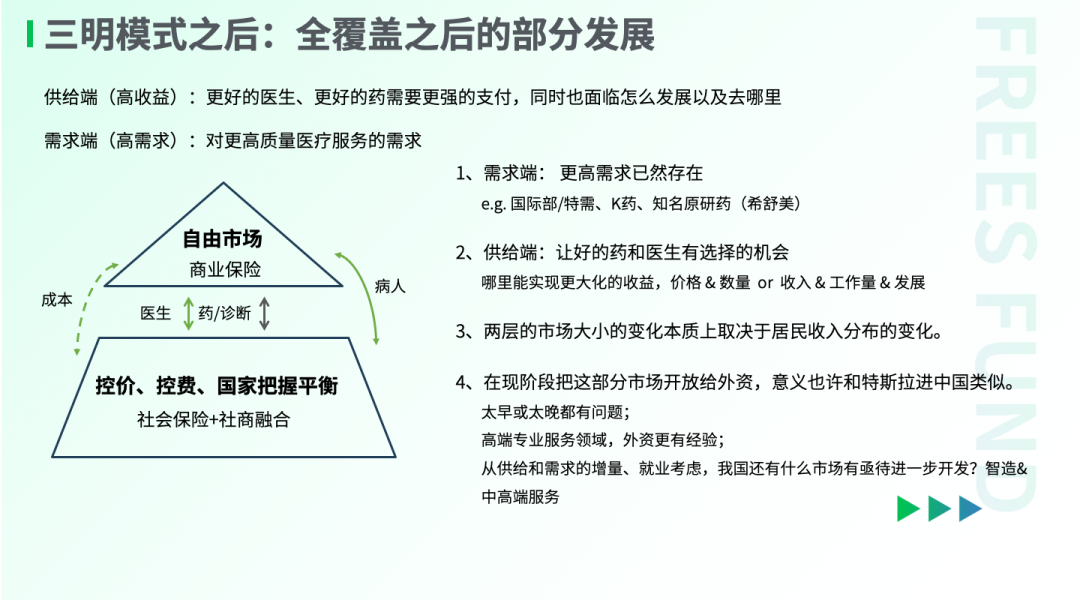

The Sanming model has been largely established. Looking ahead, can the Sanming model long-term satisfy different groups' medical needs? Which direction will China's medical market develop and evolve?

We attempt some exploration from the demand and supply sides.

▎The Increasingly Divergent Demand Side

In September 2024, at a State Council Information Office press conference on "Promoting High-Quality Development," the National Healthcare Security Administration Director mentioned that the contradiction between current health insurance protection and demand is prominent, requiring a "1+3+N" multi-tiered health insurance system to meet diverse differentiated needs. The "3" refers to China's basic health insurance system currently covering basic insurance, individuals in difficulty, and critical illness insurance. The "N" represents the multi-tiered health insurance system, including inclusive insurance (public-private integration), commercial health insurance, and charitable mutual aid. The "3" and "N" are connected, protected, and clarified through a unified digital information platform.

On the market side, multi-tiered needs are easily observed. For example, while some groups aren't clear what mycoplasma infection is, others are already complaining: "I only want Zithromax (produced by Pfizer, mainly for respiratory and reproductive tract infections), but it's actually 'unavailable' at hospitals."

Whether upgraded medical service needs exist essentially depends on changes in Chinese residents' income. According to research by Renmin University scholar Qiong Li, China's current income distribution structure is "pyramid-shaped," with relatively small proportions of middle-income and high-income groups. But with social development, this portion of the population should theoretically continue increasing.

A 2022 survey report on health investments by China's high-net-worth individuals (with financial assets exceeding 35 million RMB) shows that when seeking medical care, this group primarily chooses public tertiary hospital special-needs departments or private hospitals, and when facing major illnesses, some choose overseas medical care mainly in the US, Germany, and Hong Kong.

Just looking at domestic medical care, rough estimates suggest service fee differences between special-needs and regular outpatient departments are about 10-fold. From the drug perspective, taking PD-1 monoclonal antibodies (immune checkpoint inhibitors for cancer treatment) as an example, Keytruda (Chinese trade name Keruida, English name Keytruda, an anti-cancer drug, scientific name pembrolizumab) is not covered by domestic health insurance, with pricing approximately double that of domestic PD-1 monoclonal antibodies. But according to sample data from医药魔方, in 2023 Keytruda still ranked in the first tier by sales revenue, only slightly below comparable PD-1 monoclonal antibody drugs produced by BeiGene, Innovent, and Hengrui Medicine.

All this demonstrates that despite basic health insurance non-coverage, demand for upgraded medical services already exists and can tolerate certain premiums. The key question is whether suppliers have the capability to meet corresponding requirements.

▎The Continuously Developing Supply Side

From the supply side, China is fundamentally capable of building a market that meets upgraded needs. On one hand, China's doctor numbers continue increasing. On the other hand, in horizontal comparison, China has already begun occupying relatively advanced positions in areas like innovative drugs and medical services.

From the pharmaceutical perspective, we can glimpse industry development through the evolution of 50-year-old company Hengrui Medicine. According to Guohai Securities analysis: 1970-2011, Hengrui Medicine mainly produced active pharmaceutical ingredients; starting 2011, Hengrui Medicine entered an innovation transformation period, investing in early R&D and expanding its innovation pipeline; in 2018, centralized procurement began, with generic drugs facing revenue pressure, while some innovative drug/patent drug pipelines began commercialization. In the past year or two, some more forward-looking early new drug pipelines have begun licensing out.

Although we still don't hold advantages in groundbreaking original drug R&D, it's undeniable that China has established a modern pharmaceutical industry R&D and production system and talent pool, still continuously evolving. Some pioneers stand at the forefront, successfully going global with BIC (Best in Class) patented drugs, such as BeiGene's zanubrutinib and Legend Biotech's ciltacabtagene autoleucel.

From the medical services perspective, China currently still relies primarily on public hospitals, meeting higher demands through special-needs departments, international departments, and a small number of private hospitals.

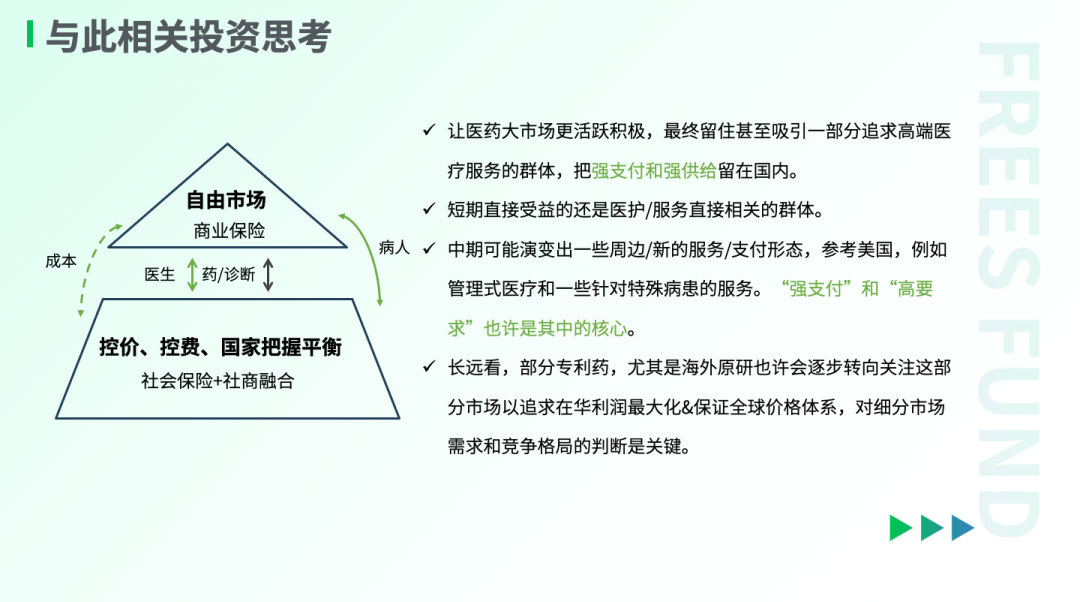

Based on these observations, our understanding and inference is that due to the existence of differentiated demands and the gradual evolution of domestic pharmaceutical/medical supply capabilities, a more clearly defined new market may gradually integrate atop the current basic social healthcare system, primarily supported by commercial insurance, with relatively high payment capacity and accompanying high demands as its main characteristics. And this renewed mention of opening to foreign investment for hospital construction also seems to signal this new beginning: against the backdrop of the basic healthcare system gradually taking shape, meeting differentiated demands may become the focus of the next stage.

For product and service providers in the medical industry, questions of pricing and positioning may arise in the future, but whether their products/services are compelling enough for their target groups remains the core consideration.

| References

[1] Yuteng Liu, Jing Ye. DRG Domestic and International Payment Updates and Innovative Technology Payment — Medical Investment Opportunities Under DRG/DIP Payment Reform: 100-Roadshow Update[R]. Beijing: Northeast Securities Research Institute, 2024.

[2] Wei Yuan. Overseas Review: Japan's Healthcare Reform Cost Control Roadmap and Pharmaceutical Industry Fate Reflection[R]. Beijing: Guojin Securities Research Institute, 2023.

[3] Wei Zheng. Foreseeing the Future — Lessons from Sanming Small City's Healthcare Reform Journey[R]. Beijing: Guolian Securities Research Institute, 2023.

[4] Jingwei Zhang, Kang Xu, Jinping Hong. Exploring Typical Country Characteristics, Dispelling Channels Development Fog for Life Insurance[R]. Beijing: Huachuang Securities Research Institute, 2021.

[5] Nankai University Health Economics and Healthcare Security Research Center, PICC Health Insurance Co., Ltd., Ant Insurance Agency Co., Ltd. China Commercial Medical Insurance Development Research Blue Book[R]. 2024.

[6] Weiyi Wang, Bingting Li. Health Industry Special (II): Overseas Mainstream Health Insurance Model Research[R]. Beijing: Ping An Securities Research Institute, 2022.

[7] Tsinghua University PBC School of Finance China Insurance and Pension Research Center, China Association of Enterprises with Foreign Investment R&D-based Pharmaceutical Association Committee, PhRMA. Commercial Health Insurance and Pharmaceutical Collaborative Innovation Model Research Report[R]. 2024.

[8] Cigna & CMB Life Insurance, Hurun Report, Peking University Institute for Global Health and Development. 2022 High-Net-Worth Individuals Health Investment White Paper[R]. 2022.

[9] Xiaogang Zhou. Hengrui Medicine Company Deep Report: Innovative Drugs Continuously Delivering, Operations Entering New Cycle[R]. Beijing: Guohai Securities Research Institute, 2024.

[10] Jingchun Zha, Zhennan Duan. Healthcare Systems and Mechanisms of Cuba, Brazil, and Argentina and Their Implications[J]. Special Zone Practice and Theory, 2019, (02): 116-120.

[11] China Society of Economic Reform, ed. Witnessing Major Reform Decisions: Oral Histories from Reform Insiders[M]. Social Sciences Academic Press, 2018.

Reader Giveaway

What potential upgrade needs do you see in the pharmaceutical and medical markets? Leave a comment below — we'll randomly select 5 readers to each receive a copy of Witnessing Major Reform Decisions: Oral Histories from Reform Insiders.

18 Charts to Understand Global Supply Chain Changes | FreeS Research

Deciphering Aging, Resisting Aging | FreeS Report

The Truth About Weight Loss, and Innovation Opportunities | FreeS Report 36

Dialogue with Shize Bio's Xiang Li: Past, Present, and Future of Stem Cells

Everything Has Two Sides: How to Use "Nuclear Radiation" as Anti-Cancer Medicine? | FreeS Report 28

Star FreeS Fund's WeChat Official Account for timely business insights