Deep Dive: China's "DeepSeek Moment" in Biotech | FreeS Fund Report

A Watershed Year for China's Innovative Drug Industry

On February 7, The Wall Street Journal declared on its podcast that "China's biotech industry is having its DeepSeek moment," highlighting how Chinese biotech companies are rising with distinctive competitive advantages — collaborating with top chemists while spending a fraction of what their American counterparts do.

This claim has found powerful validation in reality. Akeso Biopharma's bispecific antibody ivonescimab (AK112) became the first drug globally to defeat Keytruda (pembrolizumab) in a head-to-head Phase 3 clinical trial. Its overseas licensing deal — $500 million upfront, $5 billion total — reset industry expectations. Ivonescimab has since been approved for non-small cell lung cancer and added to China's updated national reimbursement drug list.

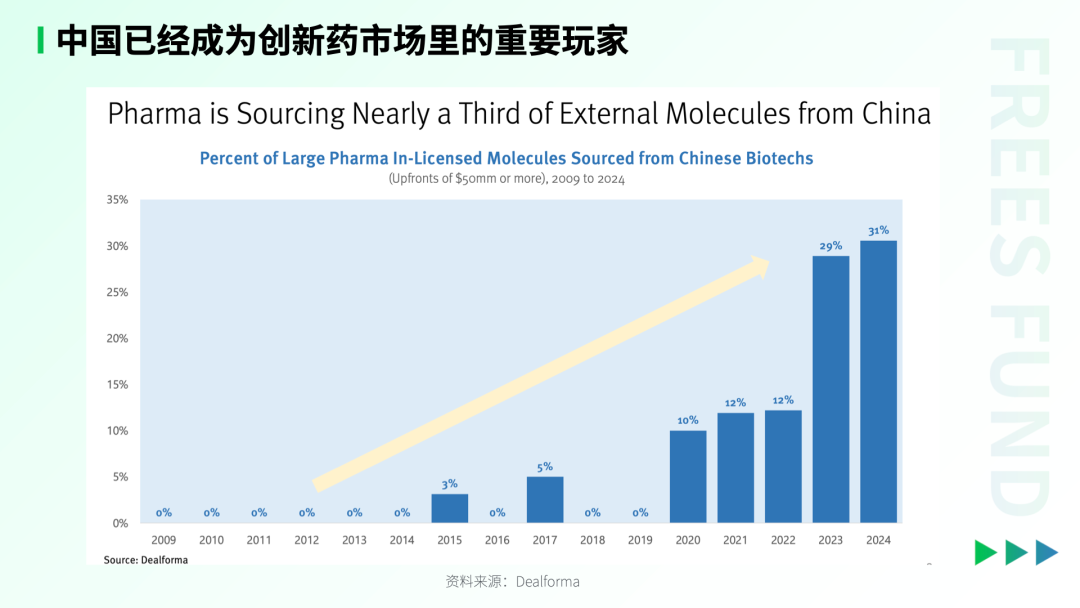

Such breakthroughs mark a historic inflection point for China's biopharma sector. According to research firm Dealforma, major pharma companies' large-scale deals with Chinese biotechs (upfront payments exceeding $50 million) surged from less than 5% before 2019 to 31% in 2024.

We believe these shifts stem from a convergence of structural changes across three dimensions: payment systems, supply capabilities, and investment dynamics. We look forward to a new virtuous cycle emerging — one built on robust supply and supported by innovative payment structures, creating fresh opportunities for Chinese innovative drugs.

In this industry research report, FreeS Fund's healthcare team uses "China's biopharma DeepSeek moment" as a framing device, taking ivonescimab as a case study to analyze the structural opportunities facing China's biopharma industry and its evolving position in the global innovative drug ecosystem from an investment perspective. We've also summarized some related investment opportunities at the end.

We hope this offers a fresh perspective. Check out the Xiaoyuzhou app or Apple Podcasts, search for and subscribe to "Gao Neng Liang" (High Energy) to listen to this episode.

Engagement Giveaway What new opportunities do you see in the innovative drug industry? Or what other industries do you think are experiencing their own DeepSeek moments? Share your thoughts in the comments. By 5:00 PM on March 18, we'll randomly select three readers to receive the updated industry research handbook compiled by the FreeS Fund team.

/ 01 / China's Biopharma DeepSeek Moment

Recently, as the "DeepSeek" concept exploded in popularity, many have begun discussing whether China is experiencing its own "DeepSeek moment" in new drug discovery.

A telling example is Akeso Biopharma's bispecific antibody ivonescimab (development code AK112), which became the first drug in the world to defeat Keytruda (brand name Keytruda, generic name pembrolizumab) in a head-to-head Phase 3 clinical trial.

Ivonescimab is the world's first bispecific antibody targeting the "PD-1+VEGF" combination, applicable for tumor treatment. At the end of 2022, Akeso licensed ivonescimab's overseas rights to Summit Therapeutics in the US. The deal carried a $500 million upfront payment with a total potential value of $5 billion — substantial figures in the innovative drug space.

Notably, at the end of 2022, Summit Therapeutics' market cap was under $800 million. After Akeso announced ivonescimab's clinical trial results in September 2024, Summit's stock price skyrocketed. As of March 11, 2025, Summit Therapeutics' market cap had surpassed $13.2 billion, or nearly 100 billion RMB.

What does ivonescimab mean for the drug discovery industry, and why has it generated such enormous buzz?

Simply put, we can understand ivonescimab as an upgraded version of PD-1 drugs, with significant implications for solid tumor treatment.

PD-1 (programmed cell death protein 1) is a protein found on the surface of T cells. Inhibitors targeting PD-1 can block this protein's function, thereby enhancing the immune system's ability to attack cancer cells.

In solid tumor treatment, PD-1 inhibitors have become far more than just another pharmaceutical product. They function more like a vessel, capable of combining with other drug molecules to achieve synergistic "1+1>2" effects.

In 2014, Bristol Myers Squibb (BMS) launched the world's first PD-1 inhibitor. By 2023, the global market for PD-1 inhibitors had reached $42.4 billion. In the US, four pharmaceutical companies offer such drugs, with Merck's Keytruda dominating — generating approximately $25 billion in revenue for Merck in 2023.

In the domestic market, PD-1 inhibitors represent roughly 12 billion RMB. The competitive landscape can be described as "four majors and three minors": the four majors being BeiGene, Innovent Biologics, Hengrui Medicine, and Junshi Biosciences; the "three minors" encompassing additional participants.

Overall, PD-1 inhibitors have become strategically critical products for major pharmaceutical companies due to their special significance in tumor treatment.

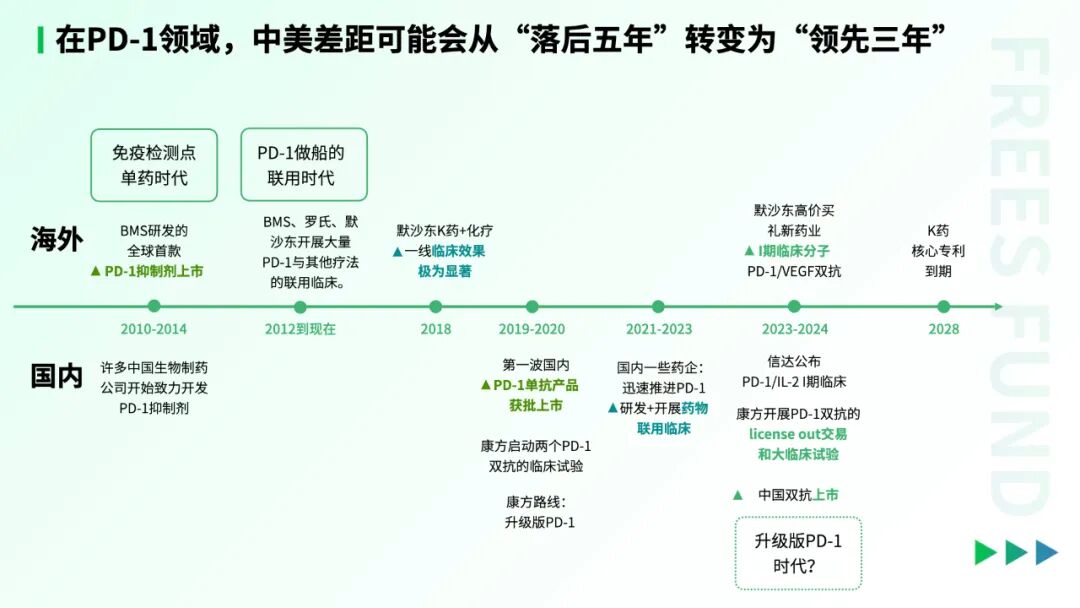

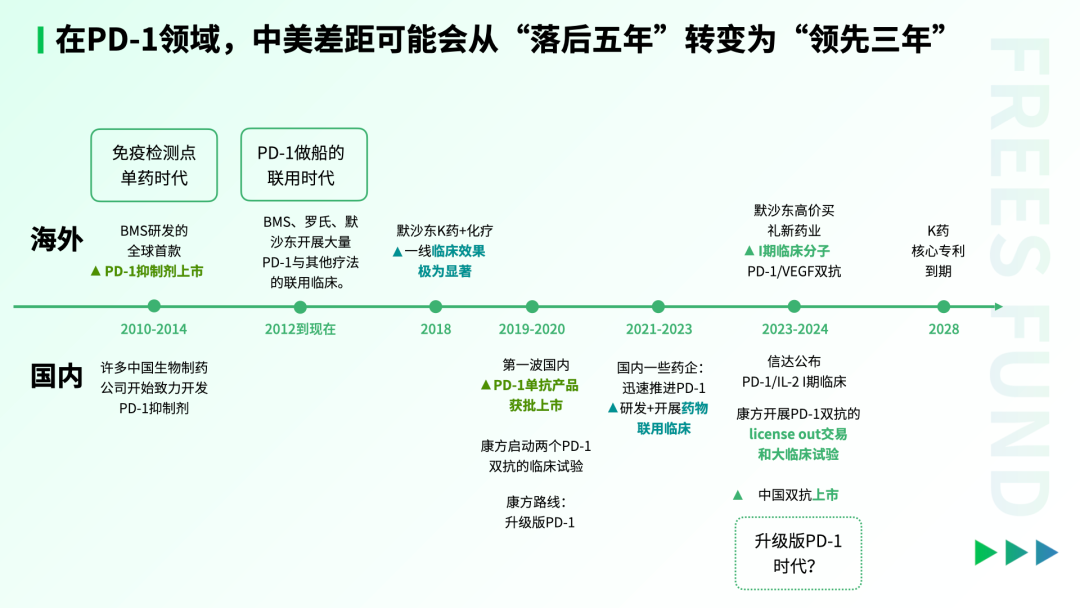

/ 02 / In PD-1, the China-US Gap Could Flip from "Five Years Behind" to "Three Years Ahead"

We view Akeso's development of ivonescimab as a differentiated exploration conducted within controllable costs. When a company manages its downside risk, failure is less costly while the upside can be substantial.

If ivonescimab's efficacy continues to be validated at subsequent milestones — for instance, if US clinical trial results prove equally significant as domestic ones, and if combination therapies also demonstrate marked effects — then in the PD-1 space, China's position relative to the US could shift from five years behind to three years ahead.

I. The Evolution of Cancer Therapy

We can review major advances in cancer treatment over the past two decades to understand the shifts occurring in the PD-1 space.

Broadly speaking, cancer therapy has passed through three main stages. First came chemotherapy, where drugs indiscriminately killed both tumor cells and normal body cells, carrying severe toxicity.

Next was the targeted therapy era. Targeted drugs attack specific biomarkers or signaling pathways unique to cancer cells, blocking tumor growth, proliferation, and metastasis with high specificity. Roche's Herceptin, for example, precisely targets proteins overexpressed in tumors.

Then, between 2010 and 2014, following the clinical success of PD-1 drugs, cancer treatment entered the immune checkpoint monotherapy era.

The underlying concept: theoretically, the immune system should recognize and attack tumors. But tumors evade immune surveillance through certain mechanisms, sometimes rendering the immune system ineffective. Immune checkpoint therapy blocks this tumor escape, allowing the immune system to re-recognize and attack tumors. PD-1 inhibitors were developed based on this immunotherapy concept.

In 2014, BMS launched the world's first PD-1 inhibitor.

II. The Overseas PD-1 Inhibitor Market: The Era of Drug Combinations Begins, with Merck Dominating

Around 2015, companies including BMS, Roche, and Merck began experimenting with combining PD-1 drugs with various other agents — chemotherapy drugs, targeted small molecules, and other immune checkpoint agents — achieving some initial successes.

In 2018, Merck's Keytruda, combined with chemotherapy, demonstrated significant efficacy in a large-scale Phase 3 clinical trial for first-line lung cancer treatment. Because the first-line lung cancer patient population is enormous, this result allowed Keytruda to pull far ahead of competing drugs in global sales, creating a dominant, winner-take-all competitive landscape.

III. China's PD-1 Monoclonal Antibody Track: Racing to Catch Up in a Crowded Field

China's new drug R&D industry began around 2000, more than 30 years behind Europe and the US.

Around 2000, China saw the emergence of CXO companies represented by WuXi AppTec, providing R&D services for pharmaceutical firms. At that time, the expansion of higher education in China had cultivated a large talent pool for the new drug industry. Leveraging this demographic dividend, pharmaceutical companies were able to reduce R&D costs through the CXO model, and China gradually entered the new drug R&D sector.

With the establishment of upstream industry chains, after 2010 China gained the capability to develop biosimilars (also known as biological generic drugs — biologics similar to already approved originator biologics). After PD-1 inhibitors debuted overseas, many Chinese biopharmaceutical companies began working to develop their own.

In 2019, PD-1 monoclonal antibody products developed by Innovent, Hengrui Medicine, and Junshi were approved for market launch. After that, the PD-1 mAb track became extremely crowded. In 2022, there were as many as 60 registered clinical trial records related to PD-1 in China.

From 2021 to 2023, some domestic pharmaceutical companies rapidly advanced PD-1 R&D while simultaneously building other pipelines, and following the example of multinational pharmaceutical companies like Merck, began conducting clinical research on combination therapies.

If we look at the timeline of PD-1 drug approvals and combination therapy approvals, the gap between China and overseas markets was roughly five years in both the monotherapy era and the combination therapy era.

IV. PD-1 Bispecific Antibodies: Akeso's Differentiated Competitive Strategy

When the PD-1 monoclonal antibody track became crowded, Akeso seemed to adopt a different strategy, beginning to develop PD-1-based bispecific antibodies and launching clinical trials for two PD-1 bispecific antibodies. One is the aforementioned ivonescimab, which can simultaneously target PD-1 and VEGF; the other is cadonilimab, which targets PD-1 and CTLA-4.

1. What Are Bispecific Antibodies?

Simply put, we can imagine an antibody molecule as a Y-shaped structure. In a monoclonal antibody, both arms of the Y recognize the same target. In a bispecific antibody, each arm of the Y recognizes a different target. It's worth noting that different bispecific antibodies may have somewhat different structures — some are engineered into an X-shape, for instance.

Compared to monoclonal antibodies, bispecific antibodies introduce an additional target, achieving additive effects. Take ivonescimab as an example: it can both relieve immune suppression and inhibit tumor angiogenesis.

2. The Era of Upgraded PD-1

As mentioned above, we can understand Akeso's ivonescimab as a kind of upgraded PD-1 drug, one that holds significant importance for solid tumor treatment.

When multinational pharmaceutical companies (hereinafter referred to as MNCs), represented by Merck, pushed solid tumor treatment into the combination therapy era, Akeso adopted a different strategy — upgrading PD-1 through bispecific antibody technology.

In 2021, Akeso's PD-1 monoclonal antibody was approved in China, and its sales rights were transferred to Chia Tai Tianqing. Meanwhile, Akeso devoted more resources to bispecific antibody R&D, conducting more clinical trials.

Between 2023 and 2024, clinical trials for Akeso's two bispecific antibody projects were approved one after another. In September 2024, Akeso announced head-to-head clinical results comparing ivonescimab with Keytruda. Then, in November 2024, both Merck and BioNTech (the mRNA vaccine company) purchased early-stage clinical molecules for PD-1/VEGF bispecific antibodies in China.

We have a bold speculation: in the future, will the field of tumor immunotherapy collectively switch from PD-1 to upgraded versions of PD-1?

If the answer is yes, then we can see that domestic companies have already established certain advantages in the upgraded PD-1 space — Akeso's ivonescimab was already on the market in 2024, while the comparable molecules purchased by Merck and BioNTech are still in Phase 1 clinical trials.

03 / China Has Become a Major Player in Global Innovative Drugs

I. China Has Gained More International Collaboration Opportunities Through Antibody-Based Drugs

In recent years, China has become an important player in the innovative drug market, with overseas pharmaceutical companies putting substantial "real money" into Chinese biotech firms.

Research firm Dealforma tracked global drug licensing deals with upfront payments exceeding $50 million. The data shows that from 2009 to 2014, the proportion of large pharmaceutical companies conducting major deals with Chinese biotech companies was nearly zero. However, starting from 2020, this proportion grew rapidly, surging to 29% in 2023 and 31% in 2024.

Overseas markets' recognition of and investment willingness toward China's early-stage R&D projects are also increasing.

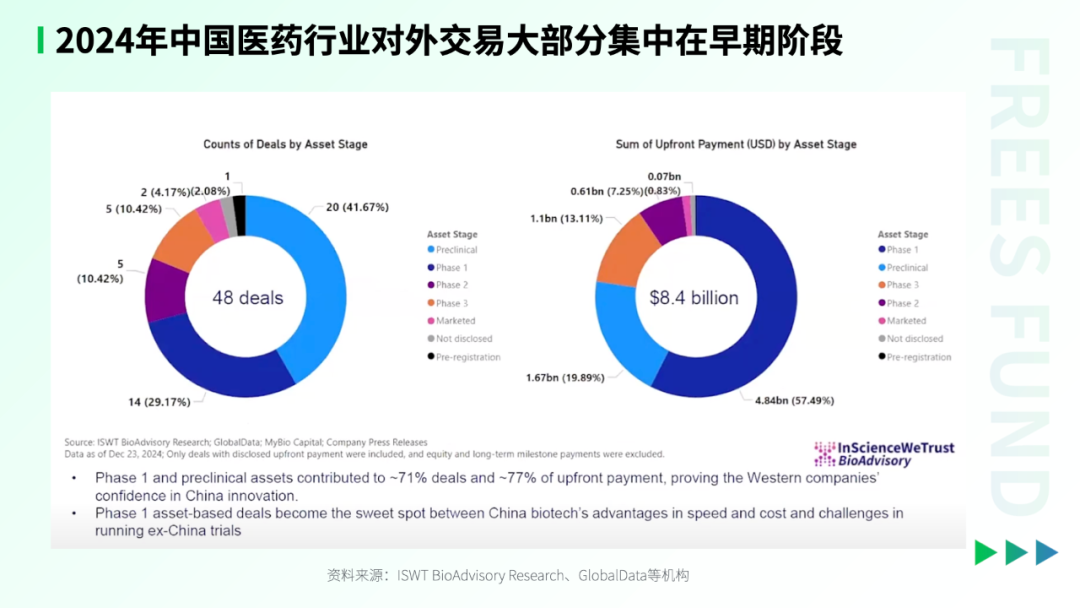

According to statistics from ISWT BioAdvisory Research, GlobalData, and other institutions, in 2024, most of China's pharmaceutical outbound deals were concentrated in the preclinical and Phase 1 clinical stages, accounting for 71% of total deal volume. Moreover, early-stage projects attracted the majority of overseas capital investment — particularly Phase 1 clinical projects, which accounted for 57.49% of total upfront payments.

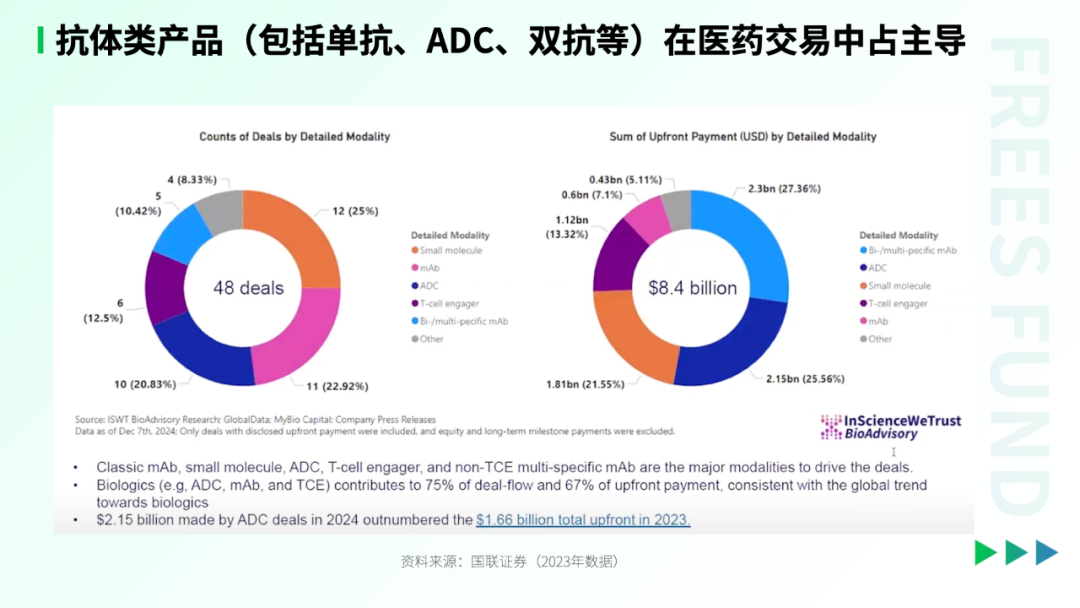

By drug type, in 2024 China's outbound deals were dominated by antibody-related products (including monoclonal antibodies, ADCs, bispecific antibodies, etc.), contributing 75% of deal volume and 67% of total upfront payments.

Currently, global demand for antibody-based drugs is strong. According to statistics from media outlets including Drug Hunter Club and Pharma Notes, among the top ten drugs by global sales in 2023 and 2024, the vast majority were antibody-based drugs.

It is evident that antibody-based drugs occupy a dominant position in the global pharmaceutical market, whether measured by deal activity or sales volume. This is why major global MNCs are actively pursuing self-developed or acquired assets in this category.

In short, antibody-based drugs have become the focus of the global pharmaceutical industry due to their significant market advantages and potential value, and China, through technological advancement in this field, has gained more opportunities for international collaboration.

II. Value Distribution in the Innovative Drug Industry Chain Still Heavily Tilts Toward MNCs

The Akeso case demonstrates China's breakthroughs in new drug R&D on one hand, while on the other hand reflecting challenges faced by China's biotech industry in recent years: domestic drug prices have long remained low, and there is a lack of globally competitive MNCs. Therefore, some domestic innovative drug companies have chosen to integrate into the global value chain to seek survival space.

Multinational pharmaceutical companies, with their financial advantages (such as trillion-dollar M&A budgets) and needs to replenish R&D pipelines, have become important participants in the industry chain, providing strategic exit windows for Chinese biotech enterprises with technological advantages.

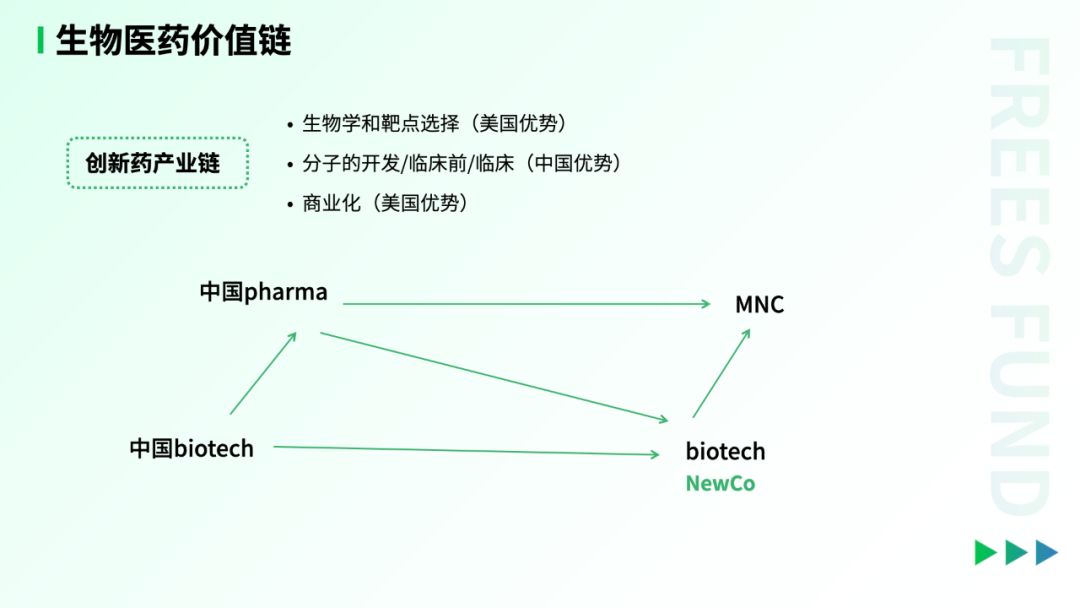

From the perspective of global biomedical value chain distribution, the core industry links can be divided into three parts: first, target discovery and biological validation — that is, deciding which targets to pursue, where the US overall still holds the advantage; second, molecule development, preclinical and clinical trials, which is China's area of strength; third, commercialization, where the US still maintains the upper hand.

In the molecule development and clinical trial segment, Chinese companies' competitiveness is concentrated in execution capability, trial-and-error efficiency, and the ability to rapidly initiate clinical trials. For example, Hengrui Medicine simultaneously advanced 147 R&D pipelines (ranking in the global top ten by scale), completing molecule development quickly and at low cost, then realizing value transformation through overseas partnerships or asset sales.

However, the ultimate value distribution in the innovative drug industry chain still heavily tilts toward MNCs. US innovative drug prices average 15-20 times those in China, and the overall biomedical market size reaches 3-4 times that of China. MNCs not only control commercialization channels but also continuously optimize their ability to judge target value through internal R&D investment.

In this landscape, a "DeepSeek moment" in biotech might benefit MNCs more than biotech companies and their investors. Although Chinese companies occupy key nodes in the molecule development segment, the maximum value is still extracted by MNCs through acquisitions or partnerships.

04 / The Breakthrough Year for China's Innovative Drug Industry

What historical moment is China's innovative drug industry currently at?

We believe China's innovative drug industry is currently at a breakthrough year following a "downward spiral" involving three intertwined stakeholders: the payer, the supplier, and the investor. This "year" may not literally be one or two years, but rather a period that requires gradual observation and discovery.

I. A Downward Spiral of Overall Confidence Triggered by Active Contraction from a Dominant Payer, Accompanied by Insufficient Domestic Supply

Over the past five years, China's innovative drug industry has experienced an overall "downward spiral." This decline manifested in continuously shrinking primary market financing and sustained drops in the Hang Seng Innovative Drug Index in the secondary market.

How to understand this? We can examine it through three components: the payer, the supplier, and the investor. The payer historically referred primarily to domestic health insurance; the supplier refers to the industry's capacity to provide innovative drugs or develop truly novel medicines.

1. Payer Contraction

Around 2018, the National Healthcare Security Administration introduced the drug pricing negotiation mechanism, whereby drug prices are jointly determined by innovative drug companies and the NHSA. The NHSA decides the final sales price of drugs in China based on the payment capacity of health insurance and the innovativeness of the drug. Meanwhile, the entire drug sales channel underwent restructuring and compression.

2. Insufficient Supply, Difficulty Gaining Overseas Recognition

The high value of new drugs lies in their extended patent exclusivity periods, or even their ability to open entirely new markets. However, the core reason for the innovative drug industry's downward spiral over the past five years has been insufficient supply — the so-called "new drugs" weren't actually new, and pipeline homogenization was severe.

At the same time, we saw domestic innovative drug companies encountering setbacks in their overseas expansion at that time. For example, some of BeiGene's rights were returned, Innovent's head-to-head overseas clinical trial of PD-1 versus Keytruda failed, and companies like Junshi experienced similar issues.

3. Declining Investment Appetite

With domestic payment sources tightening and supply quality too weak to earn overseas recognition, investment appetite for innovative drugs declined — completing a vicious cycle that stalled innovation and sent the industry into a downward spiral.

II. The Breakthrough: Stronger Supply Chains Maturing and Going Global, Alongside a Bottoming-Out in Payment Sources

Over the past two to three years, despite continued contraction on the payment and investment fronts, we've still seen some supply-side breakthroughs. At the same time, payment sources appear to have hit bottom.

1. Stronger Supply Chains Breaking Out

From 2022 to 2024, Chinese innovative drugs' overseas expansion changed dramatically.

Take the "twin champions of going global" — BeiGene and Legend Biotech. BeiGene's BTK inhibitor succeeded in a head-to-head trial against its competitor, and the company went global through building its own sales team. Legend Biotech's cell therapy showed remarkable clinical results and entered overseas markets through its partnership with Johnson & Johnson. Both drugs achieved significant sales volume abroad.

In 2023, more and more innovative drug companies began expanding overseas. ADC (antibody-drug conjugate) deal volume, for instance, increased notably. The industry even joked that "multinational pharma companies started coming to China to bulk-buy ADC drugs."

In 2024, Chinese pharmaceutical companies not only saw growth in both deal volume and value, but also expanded into new therapeutic categories, significantly raising their international profile.

For example:

- Ascentage Pharma and Hutchmed: Though their drugs target smaller indications, they were first-in-China and subsequently licensed to the U.S. market.

- Akeso: Large-market drugs like PD-1 inhibitors began leading deal trends.

- Harbour BioMed and WuXi Biologics: These companies' platform technologies started being licensed through designated R&D arrangements, further boosting international recognition.

We see at least three drivers behind this stronger supply going global:

First, the global pharmaceutical industry seems to be in a "transition gap" for novel drugs, with many facing patent expiration. Overseas companies have strong incentives to acquire new drugs or pipelines to secure future cash flows. China, building on the previous biotech investment wave, developed numerous R&D pipelines that met this overseas demand.

Second, while the pharmaceutical financing environment cooled over the past five years, this environment allowed technically superior companies to stand out. They continued securing funding, growing, and creating a "the strong get stronger" dynamic.

Third, China's pharmaceutical sector has abundant talent. On the back of China's large population, various overseas study programs since the 1980s cultivated today's industry leaders; the university expansion starting in 2000 then stocked the pipeline with mid-career talent for China's innovative drug industry.

2. Chinese Innovative Drug Assets Reach a New Equilibrium in Quality and Bargaining Power

Overall, from a pipeline strategy perspective, domestic innovative drug companies are increasing differentiation and innovation in their pipelines. From the volume and stage of BD deals, international recognition of Chinese pharma companies continues to rise. From deal structures and content, we believe Chinese innovative drug assets have reached a new equilibrium in quality and bargaining power.

By "equilibrium," we mean whether both sides share comparable understanding on three critical points: assessment of a pipeline asset's potential value, capability for continued development investment, and judgment of potential risks.

We believe the current situation is this: domestic supply capabilities are gradually emerging and gaining recognition, and the market environment on both domestic and international sides is becoming clearer over the medium to long term — thus reaching a new equilibrium. This equilibrium manifests in deal volume and pricing, whether upfront payments are increasing, and whether pharmaceutical companies retain rights to later-stage allocations.

3. Domestic Payment Sources Bottom Out

The National Healthcare Security Administration (NHSA) has been very clear on reform direction. In December 2024, at the national healthcare security work conference, the NHSA set the tone for social medical insurance: cover the basics, squeeze out excess, and build a unified national market. We're optimistic about healthcare insurance reform being fully implemented under this new direction.

At the same time, the NHSA clarified its 2025 work priorities at the conference. According to Yicai's tally, the term "commercial insurance" appeared seven times in the conference — including statements that the NHSA will explore deeper cooperation with insurers on data sharing and individual account usage. The previous year: zero.

We see this as signaling that commercial insurance, as a payment source, is beginning to face new development opportunities. In the past, for China's entire healthcare system, the payment side was dominated by public health insurance. Going forward, three new payment sources may gradually emerge:

- Domestic commercial health insurance: With the NHSA's clear support for commercial insurance, domestic commercial insurance could become an important supplementary payment source for innovative drugs.

- European and American multinational pharma companies: These companies hold substantial cash reserves but face patent cliffs, urgently needing to acquire new drug pipelines to maintain future cash flows.

- Belt and Road countries: As these countries and regions see rising per-capita GDP, demand for high-quality healthcare is increasing, potentially becoming a new payment source for Chinese drugs.

We look forward to the innovative drug industry forming a new positive cycle — built on stronger supply and supported by new payment sources, bringing new opportunities for Chinese innovative drugs. (Welcome to read China's Healthcare System Over 40 Years: From Past to Future | FreeS Fund Report)

III. Development Space and Payment Logic of New Payment Sources

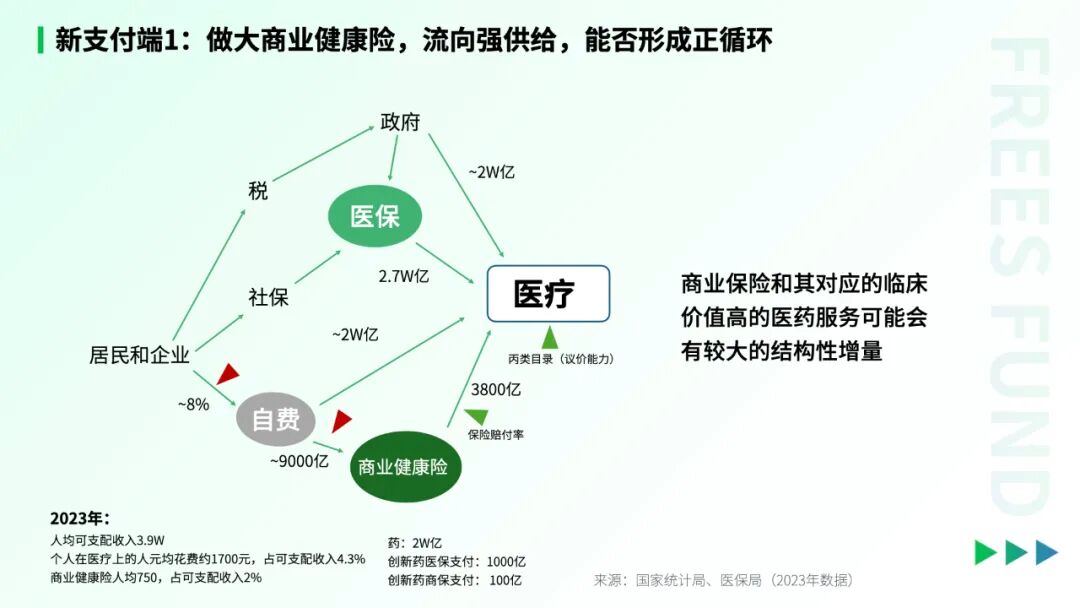

1. Commercial Insurance and Its Corresponding High-Clinical-Value Medical Services Will See Significant Structural Growth

Let's start with domestic commercial health insurance.

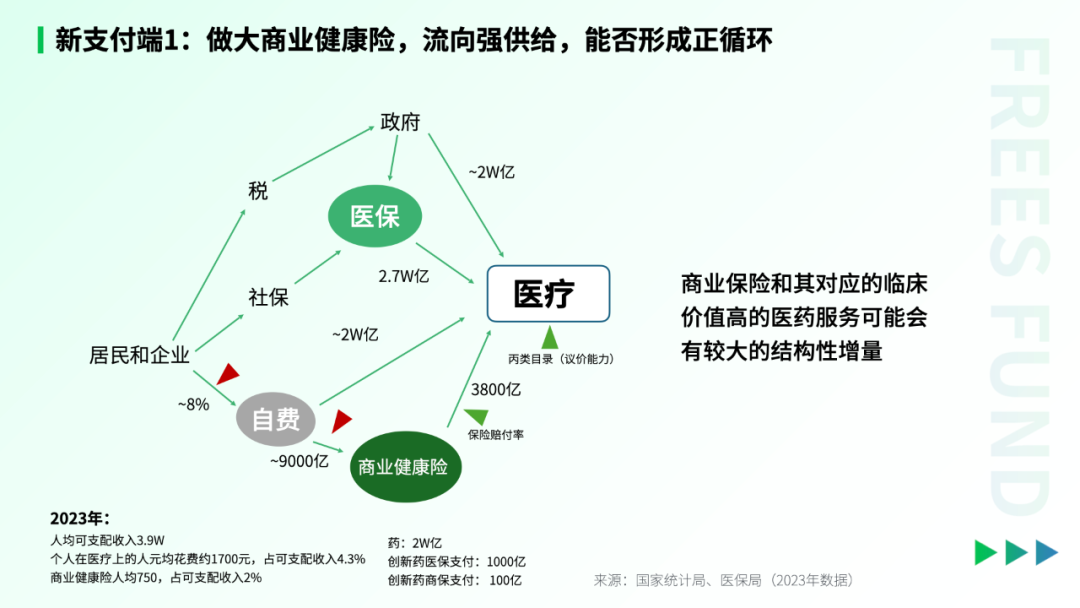

- What determines the total capital pool available to healthcare?

Total social capital flowing into healthcare is determined by three factors: first, overall societal wealth, typically measured by GDP; second, capital allocation ratio — how capital is distributed across different directions; third, allocation efficiency — how much capital gets stuck at each stage.

Take commercial insurance as an example. In 2023, 900 billion RMB flowed into China's commercial health insurance, but only 380 billion RMB ultimately reached the healthcare industry. That means China's commercial health insurance payout ratio is roughly 43% — nearly half of premiums don't go toward claims. By comparison, the four major U.S. insurers achieve payout ratios around 80%, and Germany once reached 90%. If we can optimize payout ratios, we could significantly improve commercial health insurance's economic efficiency and direct more capital into healthcare.

- Which payment sources direct money into healthcare?

Capital flowing into China's healthcare industry comes from three payment sources: public health insurance, out-of-pocket payments, and commercial health insurance. Public health insurance and government funding are relatively stable. For out-of-pocket payments: as society ages and productivity develops, basic needs like food, clothing, housing, and transportation are approaching saturation. Over the long term, personal disposable portions will increasingly shift toward upgrade needs including healthcare.

- New Developments in Commercial Health Insurance

Currently, out-of-pocket payments flowing directly to healthcare total roughly 2 trillion RMB, while capital flowing to commercial health insurance is 900 billion RMB. If more out-of-pocket payments could flow through commercial health insurance into healthcare, the incremental growth would be substantial.

The NHSA is pursuing strategies to use health insurance data, payment systems, and individual account access to more deeply engage with and empower commercial health insurance — thereby channeling more out-of-pocket payments through commercial insurance into healthcare.

Specific measures include attempting to establish a Category C medical directory and improving insurance payout ratios to enhance commercial insurance's accessibility and economic viability, making it more cost-effective or less expensive.

Take the Category C directory that the NHSA is promoting. The Category C directory would include some higher-priced but innovative and clinically valuable drugs that typically struggle to enter basic health insurance. Expanding the Category C directory, in other words, would help increase commercial health insurance's attractiveness and facilitate more cash flow into healthcare through commercial insurance.

If these measures are ultimately implemented, one significant change would be: capital that previously flowed into healthcare through personal payments would, after passing through commercial insurance, go in different directions — this is what we mean by structural growth.

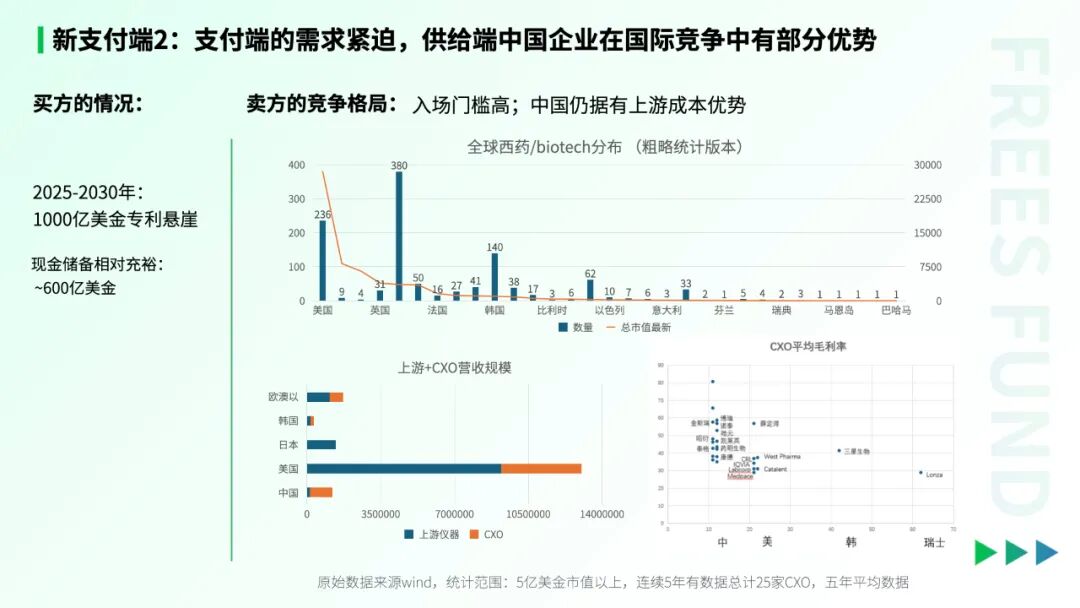

2. Multinational Pharma Companies Face Urgent Needs, and Chinese Companies Hold Partial Advantages in International Competition

Now let's discuss the second new payment source: multinational pharma companies.

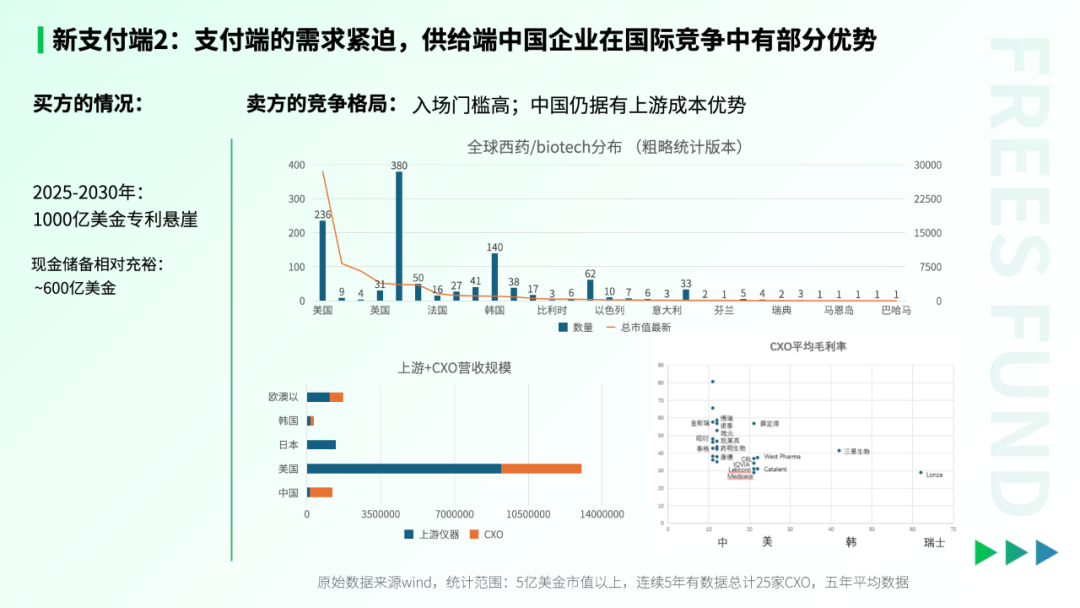

- In the near term, multinational pharma companies have ample cash reserves to address the "patent cliff"

Over the next five years or longer, overseas multinational pharma companies face a significant "patent cliff" — large numbers of patented drugs will expire, reducing these companies' cash flows by $100 billion to $300 billion.

However, these companies still hold substantial cash reserves. According to Huatai Securities Co., Ltd., as of end-2024, Johnson & Johnson, Roche, Merck & Co., Novartis, Amgen, Bayer, and BMS all held cash reserves exceeding $10 billion. We might understand this as: these funds can, in the near term, be used by these companies to acquire R&D pipelines and increase future cash flows.

- High barriers to entry in new drug R&D, with China holding advantages in R&D and cost control

Next, let's examine which global markets can provide R&D pipelines or innovative drugs for multinational pharma companies to acquire.

Overall, the new drug R&D industry has extremely high barriers to entry.

The chart above is exported from the Wind database, showing the distribution of global Western medicine and biotechnology companies. While the data may not be completely rigorous, it roughly reflects the industry landscape: these companies are mainly concentrated in the U.S., Europe, China, South Korea, and Japan.

Over the past decades, China's drug R&D capabilities have improved significantly. For instance, a batch of companies with new drug R&D capabilities has emerged among Hong Kong Stock Exchange's Chapter 18A listings and A-share listings.

Furthermore, upstream in China's new drug R&D industry, there are numerous CXO companies as well as instrument, reagent, and raw material producers. Based on gross margin data (using five-year averages), these upstream Chinese companies still maintain relatively high gross margin advantages — that is, price advantages. This means China's new drug R&D retains cost advantages.

05. From the Historical Coordinates of Current Drug R&D, Looking at Future Industry Opportunities

From our current historical coordinates, we explore the development logic and stages that drug R&D has passed through.

I. The Evolution of Drug R&D Approaches

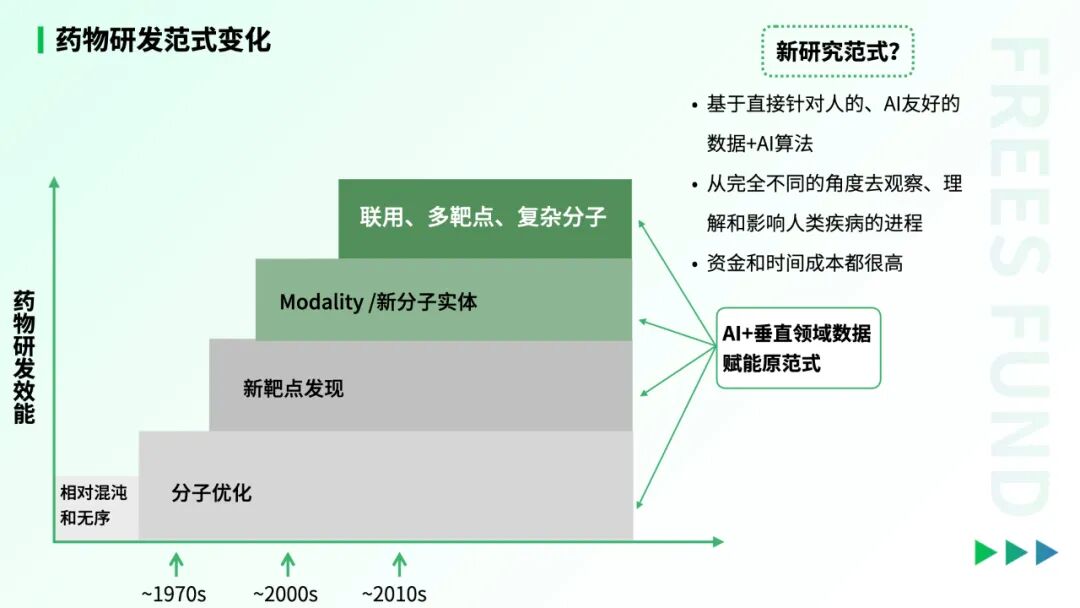

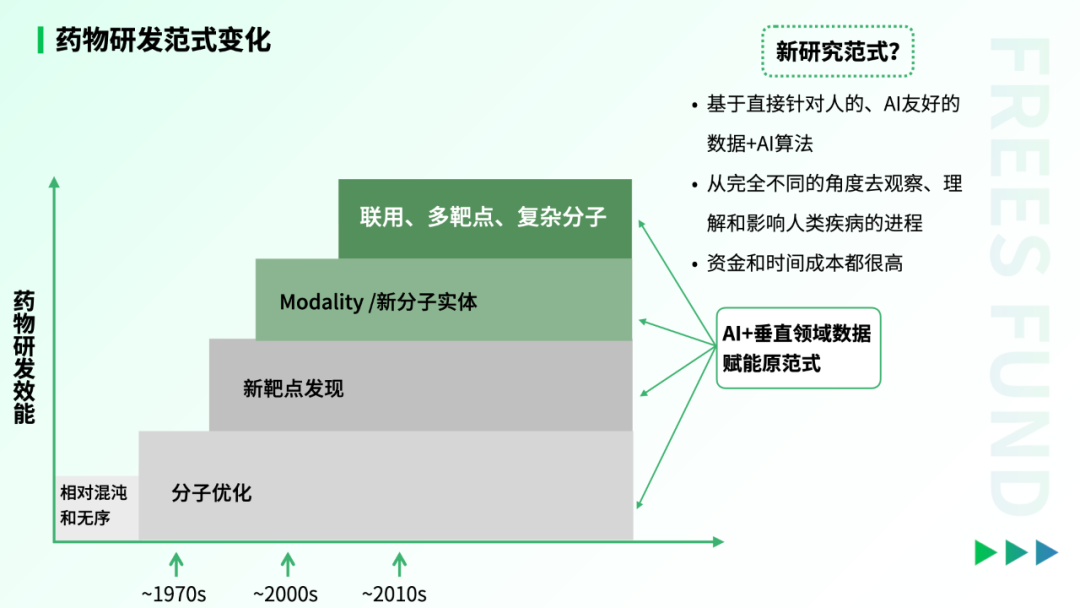

Over the past century, drug discovery paradigms have evolved dramatically alongside advances in life sciences.

Before the 1970s, pharmaceutical R&D relied primarily on trial-and-error and accumulated experience. Multinational pharma companies maintained vast libraries of small-molecule compounds. When they found a molecule that proved non-toxic in animals, they might proceed directly to human efficacy testing. This unsystematic, unscientific approach led to infamous tragedies under early lax regulatory regimes — most notably thalidomide, which was later linked to severe fetal malformations.

From the 1960s and 70s onward, continued development in chemistry enabled researchers to deliberately modify drug molecules to improve efficacy and safety. Simultaneously, developed nations led by the United States strengthened oversight, and the modern framework for drug R&D began taking shape.

Starting in the 1980s and 90s, progress in life sciences revealed the role of proteins in disease, allowing scientists to design drugs with specific targets in mind.

Researchers subsequently discovered that therapeutic potential extended beyond small chemical molecules to novel modalities — antibodies (since the 1980s) and siRNA (small interfering RNA, 2000). These new molecular types expanded the possibilities for treating disease.

From 2010, combination therapies and complex molecular designs (such as bispecific antibodies, ADCs, and others) emerged as new trends. These approaches enhanced drug efficacy while broadening their applications.

Over the past decade, AI has gradually empowered drug discovery, leveraging domain-specific data to improve R&D efficiency.

II. The New Paradigm in Drug Discovery

We believe the central challenge facing drug discovery today is that the efficacy of traditional R&D paradigms is approaching systemic limits — and AI may offer a path to break through. By "limits," we mean that certain steps in conventional drug discovery resist efficiency gains. For instance, we cannot eliminate the gap between cellular and whole-animal biology, nor the differences between animals and humans.

As observational and measurement technologies advance, if researchers can directly detect and record human data — combined with AI algorithms — they may be able to observe, understand, and influence human disease progression from entirely new angles.

For example, measuring individual biomarkers such as transcription levels and methylation patterns, then correlating them with future health outcomes (like cancer risk), and using AI for data analysis and prediction. Such data targets humans directly, eliminating dependence on animal models or cell-based experiments. This approach echoes the holistic perspective of traditional Chinese medicine: starting from the human body itself, bypassing the limitations of animal and cellular models.

Admittedly, this new approach will likely require substantial investment in time and capital, and remains to be validated with concrete examples. If proven viable, it could become an entirely new direction for drug discovery.

After all, the biomedical field has accumulated vast quantities of data, and data, applications, and technology are tightly interconnected — with sufficient data as foundation, applications begin to emerge and drive technological progress. We look forward to seeing new paradigms emerge in drug discovery. (We welcome you to read "AI for Science: At the Turning Point of Scientific Research Paradigms | FreeS Fund Report")

06. China's Biopharma Industry Is in a Confidence Recovery Phase

I. Characteristics of the Current Phase

Over the past few years in biopharma, we have seen the payment side bottom out and new payment sources gradually emerge, while the supply side continues to strengthen. The industry is currently at a stage where the bottom has been established and confidence is returning. This "confidence" stems partly from the certainty of new payment sources and the expansion of payment space.

This phase is characterized by: 1) Certainty of new payment sources: New payment channels (such as domestic commercial insurance and foreign multinational pharma companies) are gradually taking shape, showing clear payment capacity. 2) Supply-side strengthening: Companies with robust supply capabilities are emerging, able to deliver products with both clinical and commercial value.

At present, the biopharma industry is recovering its confidence, and drugs and services that support this upgrading of demand will gain greater market opportunities.

II. The Logic of Following New Payment Sources

Whether domestic commercial insurance or foreign multinational pharma companies, both prioritize products with strong clinical and commercial value when selecting targets. Therefore, only companies capable of delivering such products can win recognition from new payment sources. Entrepreneurs and investors might do well to focus more on which products or directions are likely to attract these new payment sources.

III. Directions for the Next Phase

Looking ahead, we can expect new payment sources to become further established and refined. Of course, this process still involves uncertainties that need validation at several critical junctures:

For domestic commercial insurance: Can it be successfully established? What cooperative models will it adopt with the National Healthcare Security Administration? What varieties will be included in the Category C drug list, and how will their prices be determined?

For foreign payment sources: Will multinational pharma companies adjust the types of drugs they purchase and their purchasing methods? How will domestic pharma companies price their products?

If each of these nodes can be effectively validated, we may see a surge of new, powerful supply emerge, propelling Chinese innovative drugs into an entirely new development stage.

07. Investment Implications

I. Reconstructing the Value Ecosystem

Over the past month, we have discussed DeepSeek, Nezha 2, and progress in Chinese biomedicine. Their common thread is breakthrough through innovation-led technological advances.

DeepSeek unlocked the shackles on China's advantaged industrial chains, giving them wings to soar and achieving a breakout in the technology ecosystem. In the previous generation of advantaged industries — internet, cloud computing, new energy, smartphones — China did not fully enjoy the benefits of high valuations. This is now changing because of DeepSeek.

Nezha 2 once again reminds us that China possesses a super-large, unified consumer market. Whether Nezha 2, DeepSeek, or ivonescimab, these "blockbuster products" all demonstrate enormous market potential.

In the near to medium term, in biomedicine specifically, the United States still holds the advantage, with China supply temporarily serving US demand.

If US market pricing remains far above China's, then the greatest value will likely continue to flow to the United States. Going forward, we hope to see innovation-driven growth combined with domestic demand support, bringing about a breakout and reconstruction of the value ecosystem in biomedicine. Building on China's advantaged industries, leveraging technological innovation, and叠加 (superimposing) the mega-market, we can potentially break through the old order between China and the US.

Currently, we believe directions where China's pharmaceutical industry can achieve breakthroughs include but are not limited to:

- Continued development to cultivate domestically rooted, larger-scale MNCs, gaining more voice in commercialization and pricing;

- Upgrading medical services, increasing commercial insurance penetration, raising innovative drug prices, and expanding domestic demand;

- Developing non-US markets, diversifying market strategies to increase revenue and reduce dependence on a single market.

Additionally, although AI's penetration in pharmaceutical applications remains limited, its cost-effectiveness may eventually surpass traditional drug discovery over time. However, it is worth noting that the United States may also increase investment in artificial general intelligence (AGI) to maintain its technological leadership.

Therefore, looking globally, future competition in biomedicine may extend beyond technological breakthroughs to include market strategy and business model innovation.

II. For Now, Innovative Drug Globalization Remains a Viable Path

Innovative drug R&D requires ample funding support. During 2019 to 2022, despite the biopharma market bubble, it objectively catalyzed a cohort of globally competitive pipelines. The core assets in current Chinese pharma license-out deals have benefited, to varying degrees, from R&D investment during this period.

Globally, China's innovative drug market shares certain similarities with Japan's. Before the 1980s, Japan's innovative drug market flourished, once capturing roughly 20% of the global innovative drug market. After the 1980s, as Japan's health insurance began regulating new drug prices, Japanese pharma companies pivoted to overseas expansion. For example, Xofluza was originally developed by Shionogi, which licensed ex-Japan rights to Roche, and it became one of Roche's important products.

Currently, in global innovative drug transactions, diversified exit channels have made drug valuation systems more transparent. Looking at the development of US biotech companies, the actual potential of drug pipelines is the key determinant of value. A company's business model has relatively little impact on the underlying value of its drugs. Moreover, the US payment system (including commercial insurance, Medicare, and Medicaid) can sustain high drug prices. Therefore, for Chinese innovative drugs, overseas markets still offer substantial room for imagination.

Reader Engagement What new opportunities do you see in the innovative drug industry? Or what other industries do you see experiencing a "DeepSeek moment"? Share your thoughts in the comments — by 5:00 PM on March 18, we'll randomly select 3 readers to receive the new industry research handbook written by the FreeS Fund team.

▲ DeepSeek Fired the First Shot, But AI Democratization Is More Worth Looking Forward To | A Conversation with Ji Yu of Xingyun

▲ China's Healthcare System Over 40 Years: From Past to Future | FreeS Fund Report

▲ Seven Core Questions About DeepSeek, Explained | FreeS Fund Report

▲ AI for Science: At the Turning Point of Scientific Research Paradigms | FreeS Fund Report

▲ 2025: Three Directions for AI Reshaping Drug Discovery

▲ The Right Timing, Right Place, and Right People Behind Nezha 2's Blockbuster Success | FreeS Fund Research

Star the FreeS Fund WeChat Official Account for timely business insights delivered to your inbox